University Corporate Finance Report: CML, SML, CAPM Analysis

VerifiedAdded on 2023/06/08

|13

|2867

|187

Report

AI Summary

This report provides an in-depth analysis of key concepts in corporate finance. It begins by differentiating between the Capital Market Line (CML) and the Security Market Line (SML), explaining their risk and return attributes and how they are used in investment strategies. The report then delves into the significance of minimum variance portfolios, illustrating how they help investors manage risk and optimize portfolio returns. The report also explores the Capital Asset Pricing Model (CAPM), explaining why it remains a widely used method for calculating the required rate of return, despite the existence of alternative models. Through graphical representations and detailed explanations, the report provides a comprehensive overview of these essential financial tools, offering valuable insights for investors and students alike.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

1

Table of Contents

Introduction:...............................................................................................................................2

Understanding the differences between Capital Market Line and Security Market Line:.........2

Understanding the significance of minimum variance portfolio:..............................................5

Understanding why CAPM calculation has been extensively used by investors over the years:

....................................................................................................................................................8

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

1

Table of Contents

Introduction:...............................................................................................................................2

Understanding the differences between Capital Market Line and Security Market Line:.........2

Understanding the significance of minimum variance portfolio:..............................................5

Understanding why CAPM calculation has been extensively used by investors over the years:

....................................................................................................................................................8

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

CORPORATE FINANCE

2

Standard Deviation

Expected return

Capital Market Line

Efficient Frontier

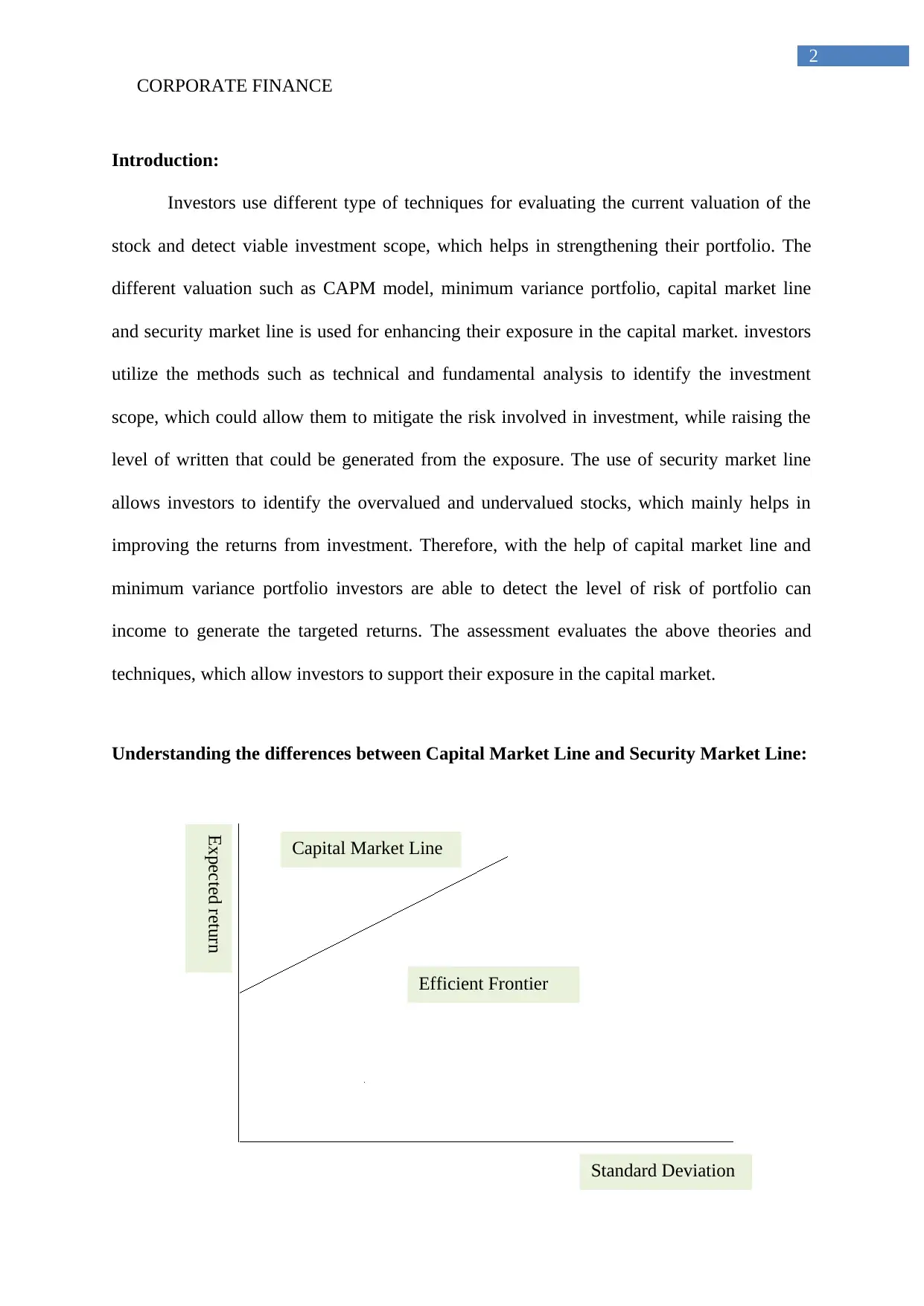

Introduction:

Investors use different type of techniques for evaluating the current valuation of the

stock and detect viable investment scope, which helps in strengthening their portfolio. The

different valuation such as CAPM model, minimum variance portfolio, capital market line

and security market line is used for enhancing their exposure in the capital market. investors

utilize the methods such as technical and fundamental analysis to identify the investment

scope, which could allow them to mitigate the risk involved in investment, while raising the

level of written that could be generated from the exposure. The use of security market line

allows investors to identify the overvalued and undervalued stocks, which mainly helps in

improving the returns from investment. Therefore, with the help of capital market line and

minimum variance portfolio investors are able to detect the level of risk of portfolio can

income to generate the targeted returns. The assessment evaluates the above theories and

techniques, which allow investors to support their exposure in the capital market.

Understanding the differences between Capital Market Line and Security Market Line:

2

Standard Deviation

Expected return

Capital Market Line

Efficient Frontier

Introduction:

Investors use different type of techniques for evaluating the current valuation of the

stock and detect viable investment scope, which helps in strengthening their portfolio. The

different valuation such as CAPM model, minimum variance portfolio, capital market line

and security market line is used for enhancing their exposure in the capital market. investors

utilize the methods such as technical and fundamental analysis to identify the investment

scope, which could allow them to mitigate the risk involved in investment, while raising the

level of written that could be generated from the exposure. The use of security market line

allows investors to identify the overvalued and undervalued stocks, which mainly helps in

improving the returns from investment. Therefore, with the help of capital market line and

minimum variance portfolio investors are able to detect the level of risk of portfolio can

income to generate the targeted returns. The assessment evaluates the above theories and

techniques, which allow investors to support their exposure in the capital market.

Understanding the differences between Capital Market Line and Security Market Line:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

3

Standard Deviation

Expected return

Under Valued Stocks

Over Valued Stocks

Figure 1: Capital Market Line Graph

(Source: Zhou, Simnett and Green 2017)

Figure 2: Security Market Line Graph

(Source: Dash 2017)

The graph depicted in the above figure relatively represents the risk and return

attributes of two different measures, which are used by investors to formulate their

investment strategy. The measure that is used by capital market line directly allows the

investor to formulate an adequate portfolio, which can generate the expected returns from a

certain level of risk exposure. Furthermore, the Security Market Line graph directly allows

the investor to detect that the stock is undervalued or overvalued, which help them to improve

their exposure in the capital market (Jerkins 2017). However, from the evaluation of above

graph certain differences between the capital market line and security market line can be

identified, which are depicted as follows.

3

Standard Deviation

Expected return

Under Valued Stocks

Over Valued Stocks

Figure 1: Capital Market Line Graph

(Source: Zhou, Simnett and Green 2017)

Figure 2: Security Market Line Graph

(Source: Dash 2017)

The graph depicted in the above figure relatively represents the risk and return

attributes of two different measures, which are used by investors to formulate their

investment strategy. The measure that is used by capital market line directly allows the

investor to formulate an adequate portfolio, which can generate the expected returns from a

certain level of risk exposure. Furthermore, the Security Market Line graph directly allows

the investor to detect that the stock is undervalued or overvalued, which help them to improve

their exposure in the capital market (Jerkins 2017). However, from the evaluation of above

graph certain differences between the capital market line and security market line can be

identified, which are depicted as follows.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

4

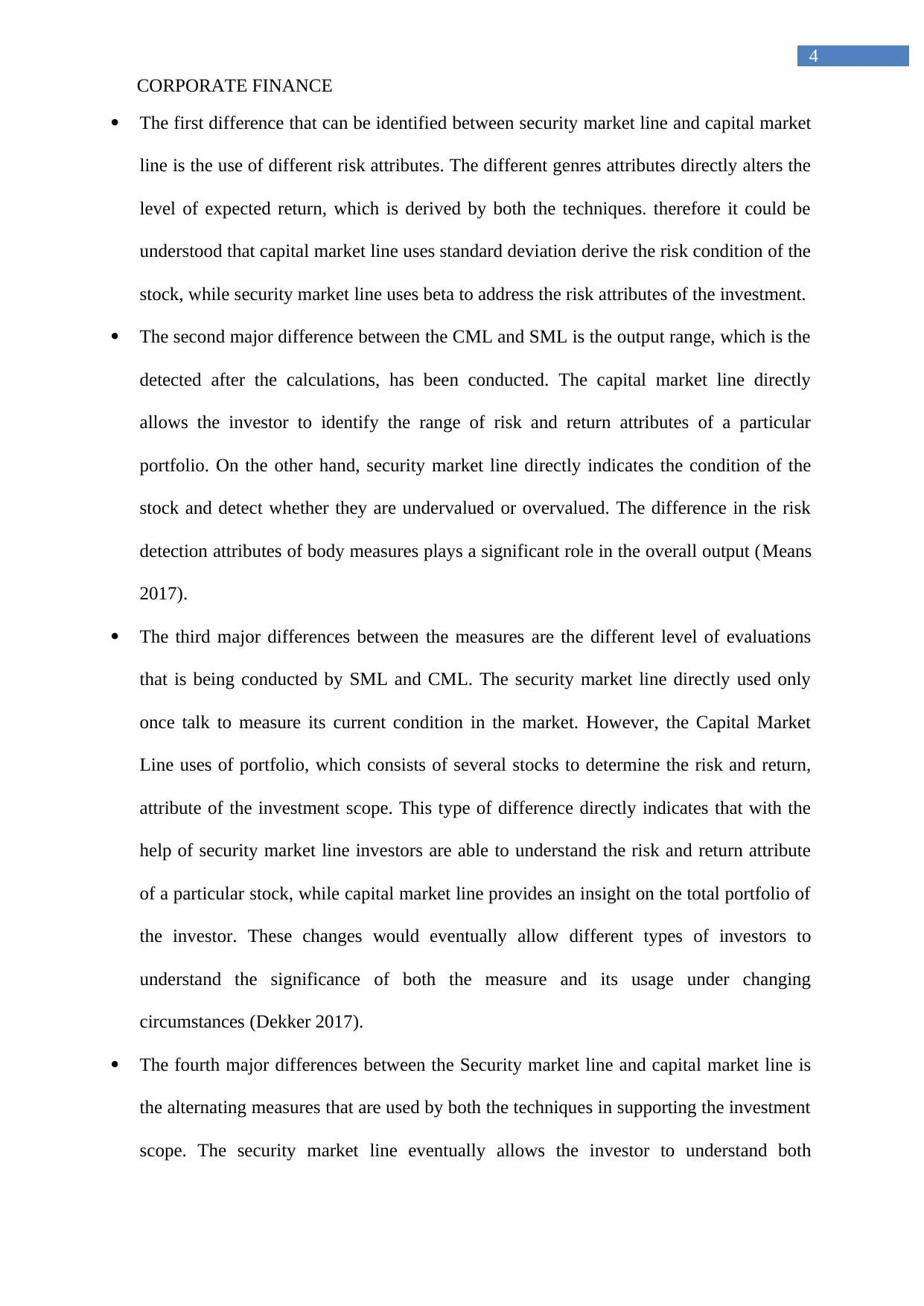

The first difference that can be identified between security market line and capital market

line is the use of different risk attributes. The different genres attributes directly alters the

level of expected return, which is derived by both the techniques. therefore it could be

understood that capital market line uses standard deviation derive the risk condition of the

stock, while security market line uses beta to address the risk attributes of the investment.

The second major difference between the CML and SML is the output range, which is the

detected after the calculations, has been conducted. The capital market line directly

allows the investor to identify the range of risk and return attributes of a particular

portfolio. On the other hand, security market line directly indicates the condition of the

stock and detect whether they are undervalued or overvalued. The difference in the risk

detection attributes of body measures plays a significant role in the overall output (Means

2017).

The third major differences between the measures are the different level of evaluations

that is being conducted by SML and CML. The security market line directly used only

once talk to measure its current condition in the market. However, the Capital Market

Line uses of portfolio, which consists of several stocks to determine the risk and return,

attribute of the investment scope. This type of difference directly indicates that with the

help of security market line investors are able to understand the risk and return attribute

of a particular stock, while capital market line provides an insight on the total portfolio of

the investor. These changes would eventually allow different types of investors to

understand the significance of both the measure and its usage under changing

circumstances (Dekker 2017).

The fourth major differences between the Security market line and capital market line is

the alternating measures that are used by both the techniques in supporting the investment

scope. The security market line eventually allows the investor to understand both

4

The first difference that can be identified between security market line and capital market

line is the use of different risk attributes. The different genres attributes directly alters the

level of expected return, which is derived by both the techniques. therefore it could be

understood that capital market line uses standard deviation derive the risk condition of the

stock, while security market line uses beta to address the risk attributes of the investment.

The second major difference between the CML and SML is the output range, which is the

detected after the calculations, has been conducted. The capital market line directly

allows the investor to identify the range of risk and return attributes of a particular

portfolio. On the other hand, security market line directly indicates the condition of the

stock and detect whether they are undervalued or overvalued. The difference in the risk

detection attributes of body measures plays a significant role in the overall output (Means

2017).

The third major differences between the measures are the different level of evaluations

that is being conducted by SML and CML. The security market line directly used only

once talk to measure its current condition in the market. However, the Capital Market

Line uses of portfolio, which consists of several stocks to determine the risk and return,

attribute of the investment scope. This type of difference directly indicates that with the

help of security market line investors are able to understand the risk and return attribute

of a particular stock, while capital market line provides an insight on the total portfolio of

the investor. These changes would eventually allow different types of investors to

understand the significance of both the measure and its usage under changing

circumstances (Dekker 2017).

The fourth major differences between the Security market line and capital market line is

the alternating measures that are used by both the techniques in supporting the investment

scope. The security market line eventually allows the investor to understand both

CORPORATE FINANCE

5

Standard Deviation

Expected return

Efficient Frontier

Minimum Variance Portfolio

Systematic and unsystematic risk associated with an investment. On the other hand, the

capital market line directly depicts the level of systematic risk, which is involved in the

particular portfolio (Arrow 2017).

Investors by using the capital market line are able to create an adequate portfolio eating

their investment and risk requirement. On the other hand, the security market line only

portrays the current position of a particular stock and depicts whether it is overvalued or

undervalued. therefore, the investment scopes is also a difference between the capital

market line and security market line, as investors altering investment scope uses different

measures for controlling their exposure in the capital market (O'connor 2017).

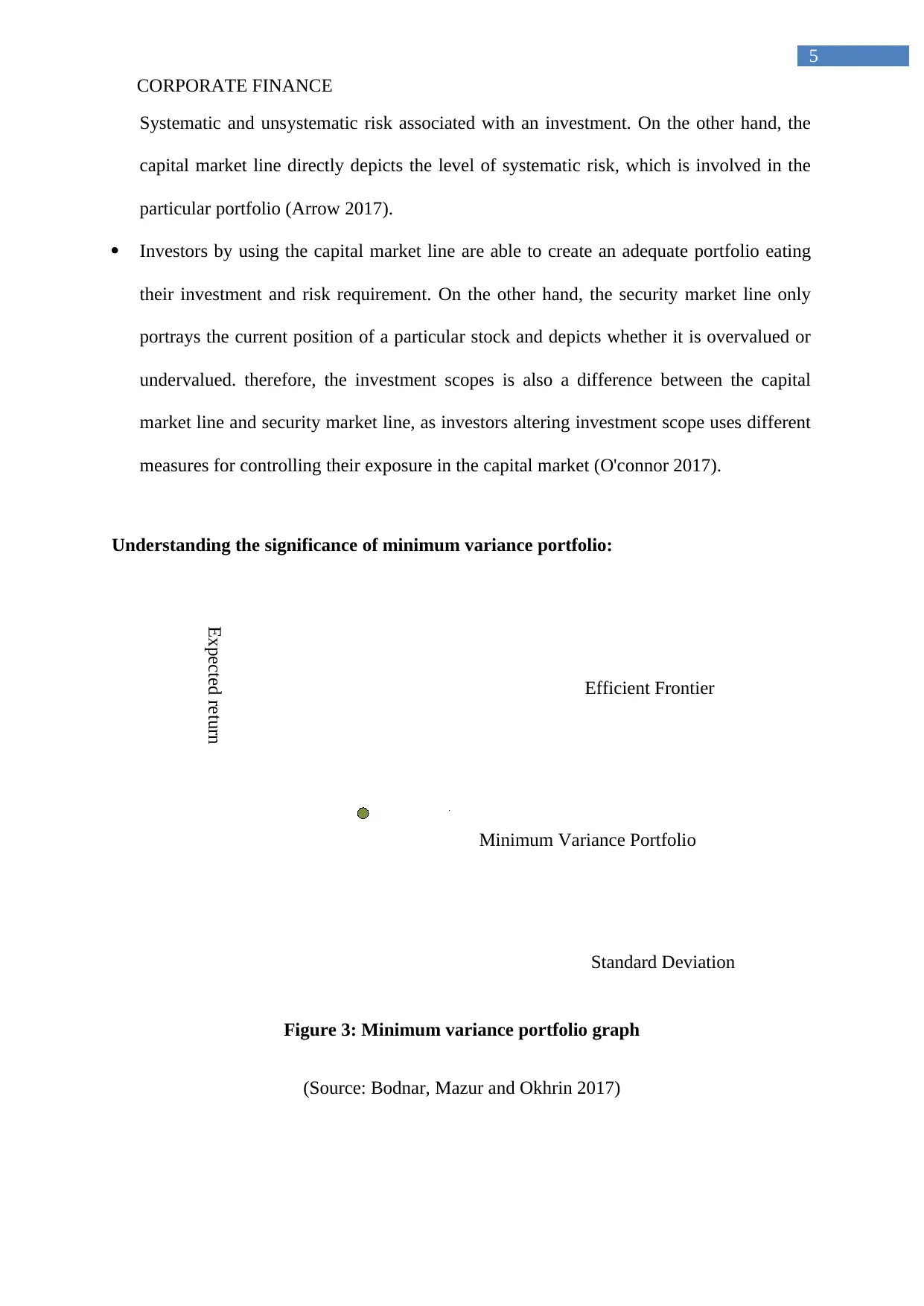

Understanding the significance of minimum variance portfolio:

Figure 3: Minimum variance portfolio graph

(Source: Bodnar, Mazur and Okhrin 2017)

5

Standard Deviation

Expected return

Efficient Frontier

Minimum Variance Portfolio

Systematic and unsystematic risk associated with an investment. On the other hand, the

capital market line directly depicts the level of systematic risk, which is involved in the

particular portfolio (Arrow 2017).

Investors by using the capital market line are able to create an adequate portfolio eating

their investment and risk requirement. On the other hand, the security market line only

portrays the current position of a particular stock and depicts whether it is overvalued or

undervalued. therefore, the investment scopes is also a difference between the capital

market line and security market line, as investors altering investment scope uses different

measures for controlling their exposure in the capital market (O'connor 2017).

Understanding the significance of minimum variance portfolio:

Figure 3: Minimum variance portfolio graph

(Source: Bodnar, Mazur and Okhrin 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

6

The minimum variance portfolio graph is adequately depicted in the above figure,

which relatively allows investors to identify an adequate, which structure to support their

investment criteria. Minimum variance portfolio is considered to derive an adequate

weightage of different stock, which would reduce the level of risk involved in investment,

while maximizing the return capability of the portfolio. The graph depicted in the above

figure directly represents a certain risk, which indicates the different combination of portfolio

weights that could be used by investors to reduce or increase their risk exposure as and when

they need to raise the level of returns (Cui, Li and Li 2017).

Minimum variance portfolio contributes to a positive attributes of investors where it

has significant value, which are depicted as follows.

The major significance of minimum variance portfolio is its contribution to formulate an

adequate portfolio, which has the lowest risk involved in investment. This type of

measure directly allows the investor to minimize the level of risk exposure of their

investment in the capital market. Furthermore, the reduction in risk attributes of an

investment directly allows the investor to ensure the security of their investment capital,

which would eventually generate secure returns from investment (Bessler, Opfer and

Wolff 2017).

The minimum variance portfolio also allows the investor to detect the level of investment

that need to be conducted on each stocks consisting in the particular portfolio. This

detection of investment weights would eventually allow the investor to reduce the

negative impact of volatile capital market. Furthermore, the investors with the combined

portfolio of diverse stock could eventually generate higher Returns from investment

(Pedersen and Peskir 2017).

Furthermore, investors using the minimum variance portfolio are able to tap into the

diversification method, which substantially reduces the level of risk involved in

6

The minimum variance portfolio graph is adequately depicted in the above figure,

which relatively allows investors to identify an adequate, which structure to support their

investment criteria. Minimum variance portfolio is considered to derive an adequate

weightage of different stock, which would reduce the level of risk involved in investment,

while maximizing the return capability of the portfolio. The graph depicted in the above

figure directly represents a certain risk, which indicates the different combination of portfolio

weights that could be used by investors to reduce or increase their risk exposure as and when

they need to raise the level of returns (Cui, Li and Li 2017).

Minimum variance portfolio contributes to a positive attributes of investors where it

has significant value, which are depicted as follows.

The major significance of minimum variance portfolio is its contribution to formulate an

adequate portfolio, which has the lowest risk involved in investment. This type of

measure directly allows the investor to minimize the level of risk exposure of their

investment in the capital market. Furthermore, the reduction in risk attributes of an

investment directly allows the investor to ensure the security of their investment capital,

which would eventually generate secure returns from investment (Bessler, Opfer and

Wolff 2017).

The minimum variance portfolio also allows the investor to detect the level of investment

that need to be conducted on each stocks consisting in the particular portfolio. This

detection of investment weights would eventually allow the investor to reduce the

negative impact of volatile capital market. Furthermore, the investors with the combined

portfolio of diverse stock could eventually generate higher Returns from investment

(Pedersen and Peskir 2017).

Furthermore, investors using the minimum variance portfolio are able to tap into the

diversification method, which substantially reduces the level of risk involved in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

7

investment. Therefore, minimum variance portfolio allows the investor to increase the

diversification process to accommodate mode stocks which good yield high returns on

yearly basis. However, the depicted in the above figure relatively represents the level of

different risk and return attributes that can be generated from the efficient Frontier.

Investors can use different combination of weeds represented by the efficient Frontier to

increase the level of risk and return from their investment.

Another significance of minimum variance portfolio is its compatibility to utilize

different stocks to derive the adequate portfolio that could have the least risk involved in

investment. This is a major significance for the investment technique, as it could combine

different investment categories such as equity, bonds, and risk-free interest to derive the

level of returns that could be generated from investment. Minimum variance portfolio

allows investor to formulate an accurate investment scheme, which could help in securing

the returns for long duration (Kuehin, Simutin and Wang 2017).

Lastly, the minimum variance portfolio directly supports the conservative investors and

secures their invested capital, which directly helps in reducing the level of risk involved

in investment. The investors using the minimum variance portfolio are able to maximize

the level of income, which can be generated from investment. Hence, it can be understood

that with the use of minimum variance portfolio investors can conduct adequate

investments to secure their invested capital.

7

investment. Therefore, minimum variance portfolio allows the investor to increase the

diversification process to accommodate mode stocks which good yield high returns on

yearly basis. However, the depicted in the above figure relatively represents the level of

different risk and return attributes that can be generated from the efficient Frontier.

Investors can use different combination of weeds represented by the efficient Frontier to

increase the level of risk and return from their investment.

Another significance of minimum variance portfolio is its compatibility to utilize

different stocks to derive the adequate portfolio that could have the least risk involved in

investment. This is a major significance for the investment technique, as it could combine

different investment categories such as equity, bonds, and risk-free interest to derive the

level of returns that could be generated from investment. Minimum variance portfolio

allows investor to formulate an accurate investment scheme, which could help in securing

the returns for long duration (Kuehin, Simutin and Wang 2017).

Lastly, the minimum variance portfolio directly supports the conservative investors and

secures their invested capital, which directly helps in reducing the level of risk involved

in investment. The investors using the minimum variance portfolio are able to maximize

the level of income, which can be generated from investment. Hence, it can be understood

that with the use of minimum variance portfolio investors can conduct adequate

investments to secure their invested capital.

CORPORATE FINANCE

8

Understanding why CAPM calculation has been extensively used by investors over the

years:

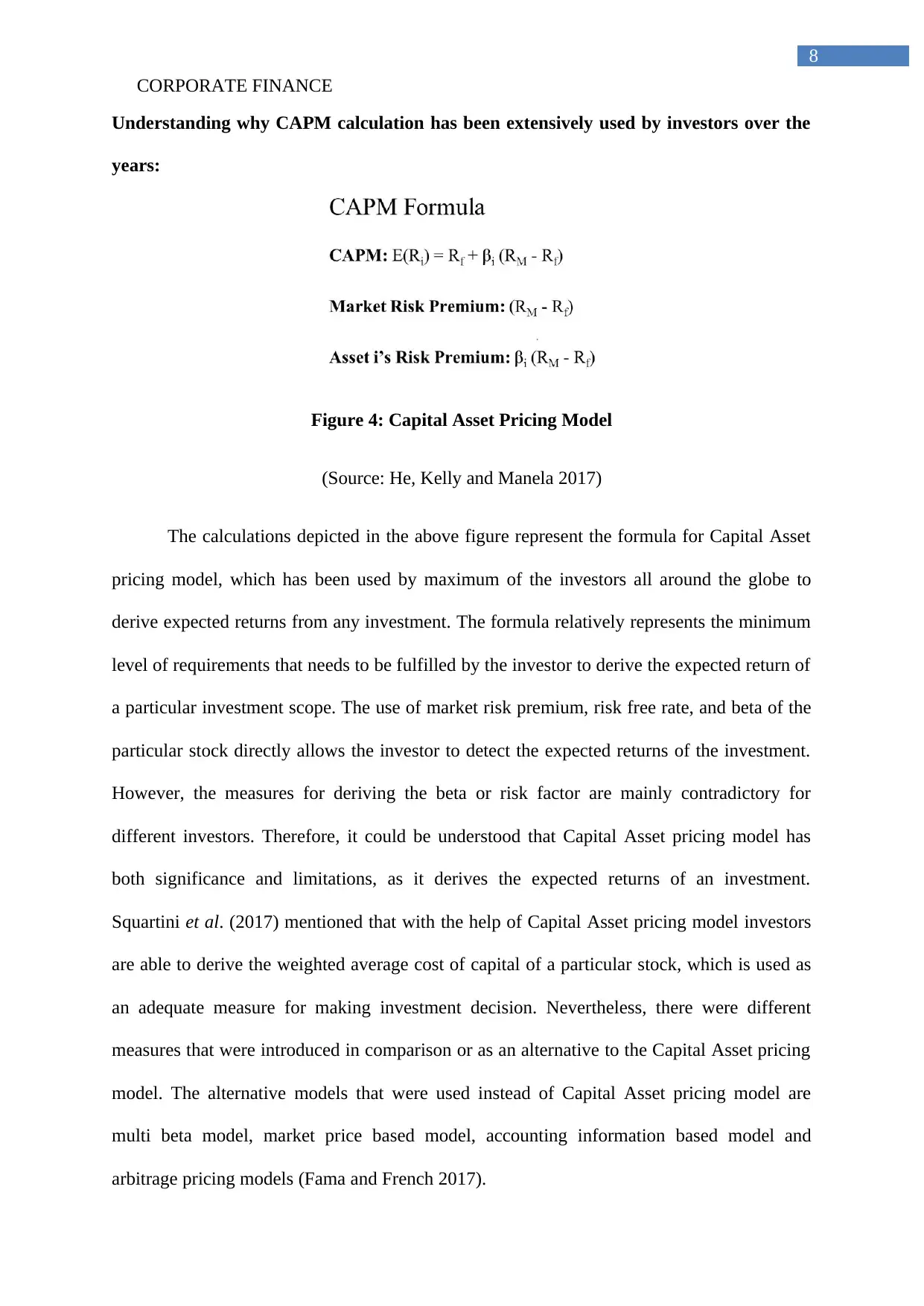

Figure 4: Capital Asset Pricing Model

(Source: He, Kelly and Manela 2017)

The calculations depicted in the above figure represent the formula for Capital Asset

pricing model, which has been used by maximum of the investors all around the globe to

derive expected returns from any investment. The formula relatively represents the minimum

level of requirements that needs to be fulfilled by the investor to derive the expected return of

a particular investment scope. The use of market risk premium, risk free rate, and beta of the

particular stock directly allows the investor to detect the expected returns of the investment.

However, the measures for deriving the beta or risk factor are mainly contradictory for

different investors. Therefore, it could be understood that Capital Asset pricing model has

both significance and limitations, as it derives the expected returns of an investment.

Squartini et al. (2017) mentioned that with the help of Capital Asset pricing model investors

are able to derive the weighted average cost of capital of a particular stock, which is used as

an adequate measure for making investment decision. Nevertheless, there were different

measures that were introduced in comparison or as an alternative to the Capital Asset pricing

model. The alternative models that were used instead of Capital Asset pricing model are

multi beta model, market price based model, accounting information based model and

arbitrage pricing models (Fama and French 2017).

8

Understanding why CAPM calculation has been extensively used by investors over the

years:

Figure 4: Capital Asset Pricing Model

(Source: He, Kelly and Manela 2017)

The calculations depicted in the above figure represent the formula for Capital Asset

pricing model, which has been used by maximum of the investors all around the globe to

derive expected returns from any investment. The formula relatively represents the minimum

level of requirements that needs to be fulfilled by the investor to derive the expected return of

a particular investment scope. The use of market risk premium, risk free rate, and beta of the

particular stock directly allows the investor to detect the expected returns of the investment.

However, the measures for deriving the beta or risk factor are mainly contradictory for

different investors. Therefore, it could be understood that Capital Asset pricing model has

both significance and limitations, as it derives the expected returns of an investment.

Squartini et al. (2017) mentioned that with the help of Capital Asset pricing model investors

are able to derive the weighted average cost of capital of a particular stock, which is used as

an adequate measure for making investment decision. Nevertheless, there were different

measures that were introduced in comparison or as an alternative to the Capital Asset pricing

model. The alternative models that were used instead of Capital Asset pricing model are

multi beta model, market price based model, accounting information based model and

arbitrage pricing models (Fama and French 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

9

The different measures that was used instead of Capital Asset pricing model relatively

needs excessive calculations and research, which is not possible for small investors.

Therefore, it could be understood that Capital Asset pricing model directly allows the

investor to see the level of returns that it would generate from the investment in a particular

stock. Capital Asset pricing model has a relevant significance and limitations, which are

depicted as follows.

The major disadvantage of the Capital Asset pricing model is it a combination of different

assumption that need to be conducted by investors for deriving the expected returns of a

particular stock. The investors need to evaluate the stocks beta, which is derived from

different sources, while the detection of market returns and risk free rate is also essential.

Therefore, it could be understood that the assumptions that is made by the Capital Asset

pricing model directly reduces the level of efficiency of expected Returns derived from

the calculation. Furthermore, Capital Asset pricing model only consists of a single factor

method, which relatively does not allow the investor to comprehend the risk and return

attribute of a particular stock (Finkel et al. 2017).

There is also a significant advantage for the use of Capital Asset pricing model, as it

allows the investor to understand the significant expected Returns of an investment. the

calculations that is conducted in Capital Asset pricing model is a relatively simple and

does not need statistical method to derive the overall output. This eventually helps the

investor to minimize the exposure of calculation that can be conducted for a particular

stock. Furthermore, small investors use Capital Asset pricing model, which does not have

the capability to support statistical calculation in arriving at investment decision.

Therefore, the CAPM method would eventually support the investor to detect the current

valuation of a particular stock before conducting any kind of investment decision.

9

The different measures that was used instead of Capital Asset pricing model relatively

needs excessive calculations and research, which is not possible for small investors.

Therefore, it could be understood that Capital Asset pricing model directly allows the

investor to see the level of returns that it would generate from the investment in a particular

stock. Capital Asset pricing model has a relevant significance and limitations, which are

depicted as follows.

The major disadvantage of the Capital Asset pricing model is it a combination of different

assumption that need to be conducted by investors for deriving the expected returns of a

particular stock. The investors need to evaluate the stocks beta, which is derived from

different sources, while the detection of market returns and risk free rate is also essential.

Therefore, it could be understood that the assumptions that is made by the Capital Asset

pricing model directly reduces the level of efficiency of expected Returns derived from

the calculation. Furthermore, Capital Asset pricing model only consists of a single factor

method, which relatively does not allow the investor to comprehend the risk and return

attribute of a particular stock (Finkel et al. 2017).

There is also a significant advantage for the use of Capital Asset pricing model, as it

allows the investor to understand the significant expected Returns of an investment. the

calculations that is conducted in Capital Asset pricing model is a relatively simple and

does not need statistical method to derive the overall output. This eventually helps the

investor to minimize the exposure of calculation that can be conducted for a particular

stock. Furthermore, small investors use Capital Asset pricing model, which does not have

the capability to support statistical calculation in arriving at investment decision.

Therefore, the CAPM method would eventually support the investor to detect the current

valuation of a particular stock before conducting any kind of investment decision.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

10

Conclusion:

After evaluating the theories and techniques described in the above assessment, it

could be identified that investors meet and accurate and reliable measure for detecting the

level of risk and return attributes of an investment. These measures can be identified with the

help of several techniques and theories such as Capital Asset pricing model, minimum

variance portfolio, security market line, and capital mark. The use of the above theories and

techniques is relatively based on the choice and consideration of the investors, as it allows

small and large investors to make adequate investment decisions. Hence, the assessment

highlights the significance of risk and return evaluation, which allows the investors to secure

their exposure in the capital market.

10

Conclusion:

After evaluating the theories and techniques described in the above assessment, it

could be identified that investors meet and accurate and reliable measure for detecting the

level of risk and return attributes of an investment. These measures can be identified with the

help of several techniques and theories such as Capital Asset pricing model, minimum

variance portfolio, security market line, and capital mark. The use of the above theories and

techniques is relatively based on the choice and consideration of the investors, as it allows

small and large investors to make adequate investment decisions. Hence, the assessment

highlights the significance of risk and return evaluation, which allows the investors to secure

their exposure in the capital market.

CORPORATE FINANCE

11

References:

Arrow, K.J., 2017. Optimal capital policy with irreversible investment. In Value, capital and

growth (pp. 1-20). Routledge.

Bessler, W., Opfer, H. and Wolff, D., 2017. Multi-asset portfolio optimization and out-of-

sample performance: an evaluation of Black–Litterman, mean-variance, and naïve

diversification approaches. The European Journal of Finance, 23(1), pp.1-30.

Bodnar, T., Mazur, S. and Okhrin, Y., 2017. Bayesian estimation of the global minimum

variance portfolio. European Journal of Operational Research, 256(1), pp.292-307.

Cui, X., Li, D. and Li, X., 2017. Mean‐variance policy for discrete‐time cone‐constrained

markets: Time consistency in efficiency and the minimum‐variance signed supermartingale

measure. Mathematical Finance, 27(2), pp.471-504.

Dash, M., 2017. “Reverse-Engineering” the Market Portfolio. Journal of Applied

Management and Investments, 6(3), pp.151-156.

Dekker, H.A., 2017. The invisible line: land reform, land tenure security and land

registration. Routledge.

Fama, E.F. and French, K.R., 2017. International tests of a five-factor asset pricing

model. Journal of financial Economics, 123(3), pp.441-463.

Finkel, A., Moses, K., Munro, C., Effeney, T. and OKane, M., 2017. Independent review into

the future security of the National Electricity Market. Australia. Department of the

Environment and Energy.

He, Z., Kelly, B. and Manela, A., 2017. Intermediary asset pricing: New evidence from many

asset classes. Journal of Financial Economics, 126(1), pp.1-35.

11

References:

Arrow, K.J., 2017. Optimal capital policy with irreversible investment. In Value, capital and

growth (pp. 1-20). Routledge.

Bessler, W., Opfer, H. and Wolff, D., 2017. Multi-asset portfolio optimization and out-of-

sample performance: an evaluation of Black–Litterman, mean-variance, and naïve

diversification approaches. The European Journal of Finance, 23(1), pp.1-30.

Bodnar, T., Mazur, S. and Okhrin, Y., 2017. Bayesian estimation of the global minimum

variance portfolio. European Journal of Operational Research, 256(1), pp.292-307.

Cui, X., Li, D. and Li, X., 2017. Mean‐variance policy for discrete‐time cone‐constrained

markets: Time consistency in efficiency and the minimum‐variance signed supermartingale

measure. Mathematical Finance, 27(2), pp.471-504.

Dash, M., 2017. “Reverse-Engineering” the Market Portfolio. Journal of Applied

Management and Investments, 6(3), pp.151-156.

Dekker, H.A., 2017. The invisible line: land reform, land tenure security and land

registration. Routledge.

Fama, E.F. and French, K.R., 2017. International tests of a five-factor asset pricing

model. Journal of financial Economics, 123(3), pp.441-463.

Finkel, A., Moses, K., Munro, C., Effeney, T. and OKane, M., 2017. Independent review into

the future security of the National Electricity Market. Australia. Department of the

Environment and Energy.

He, Z., Kelly, B. and Manela, A., 2017. Intermediary asset pricing: New evidence from many

asset classes. Journal of Financial Economics, 126(1), pp.1-35.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.