Home Designs Ltd: Financial Statements, Inventory, and Ratio Analysis

VerifiedAdded on 2022/09/15

|19

|3857

|20

Homework Assignment

AI Summary

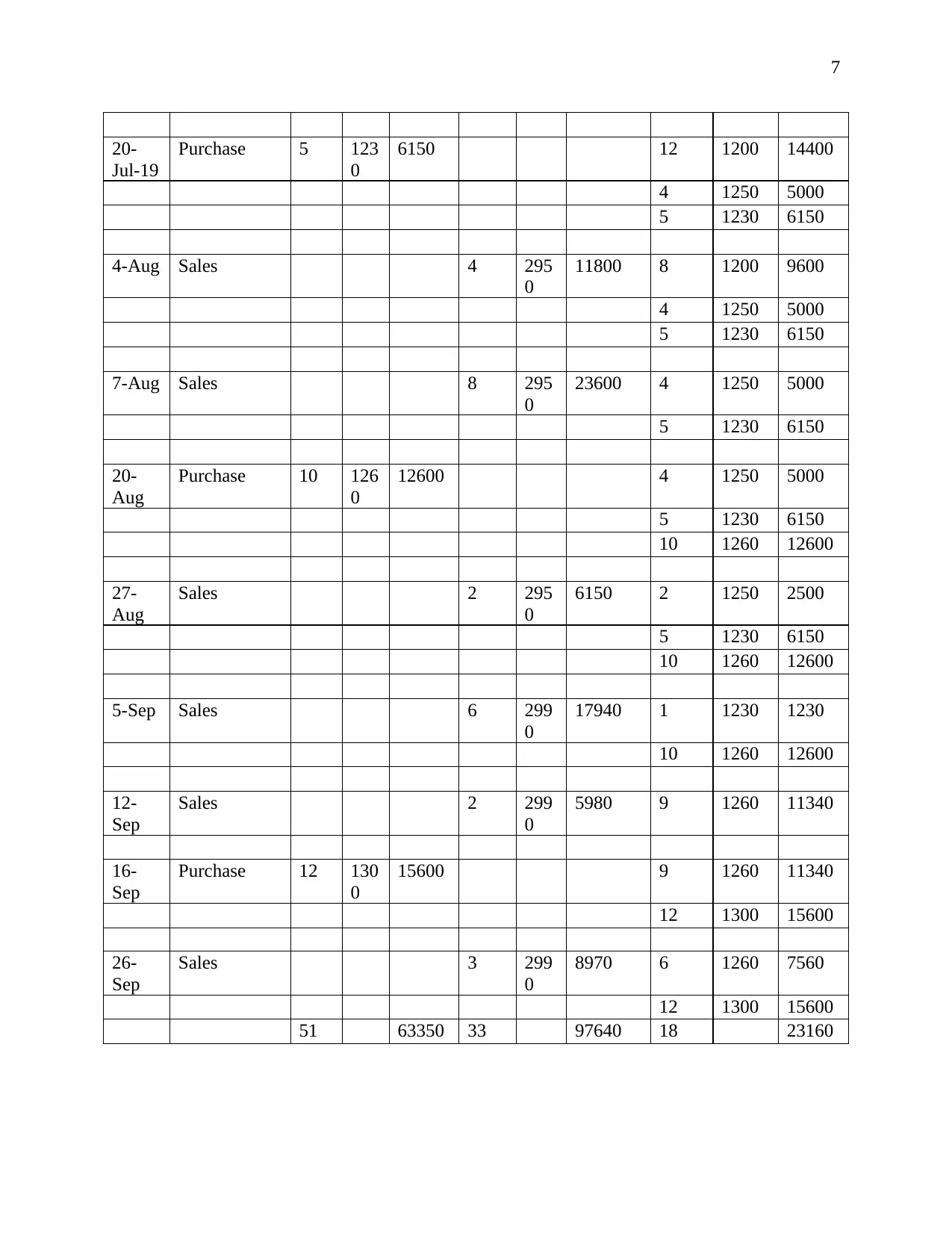

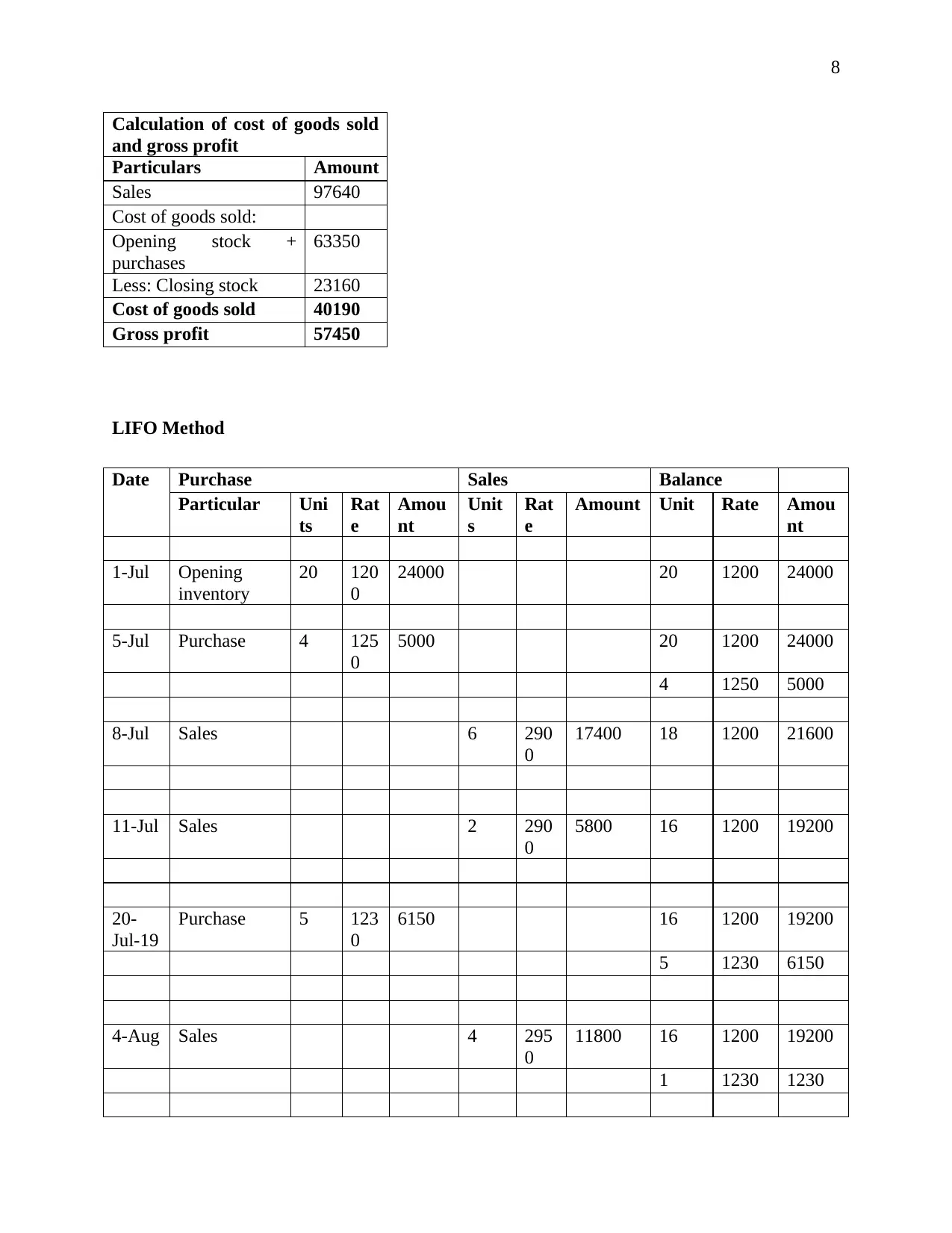

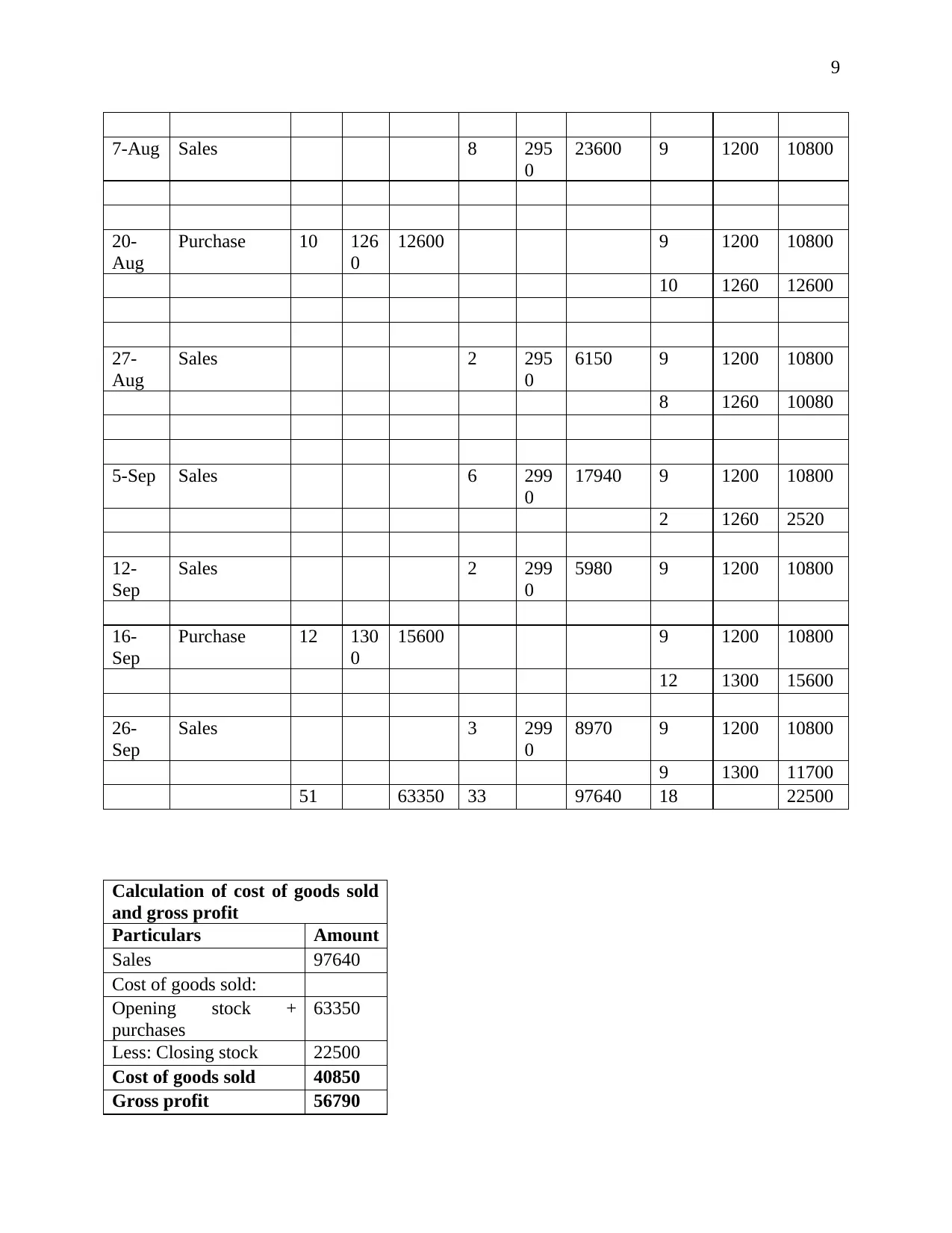

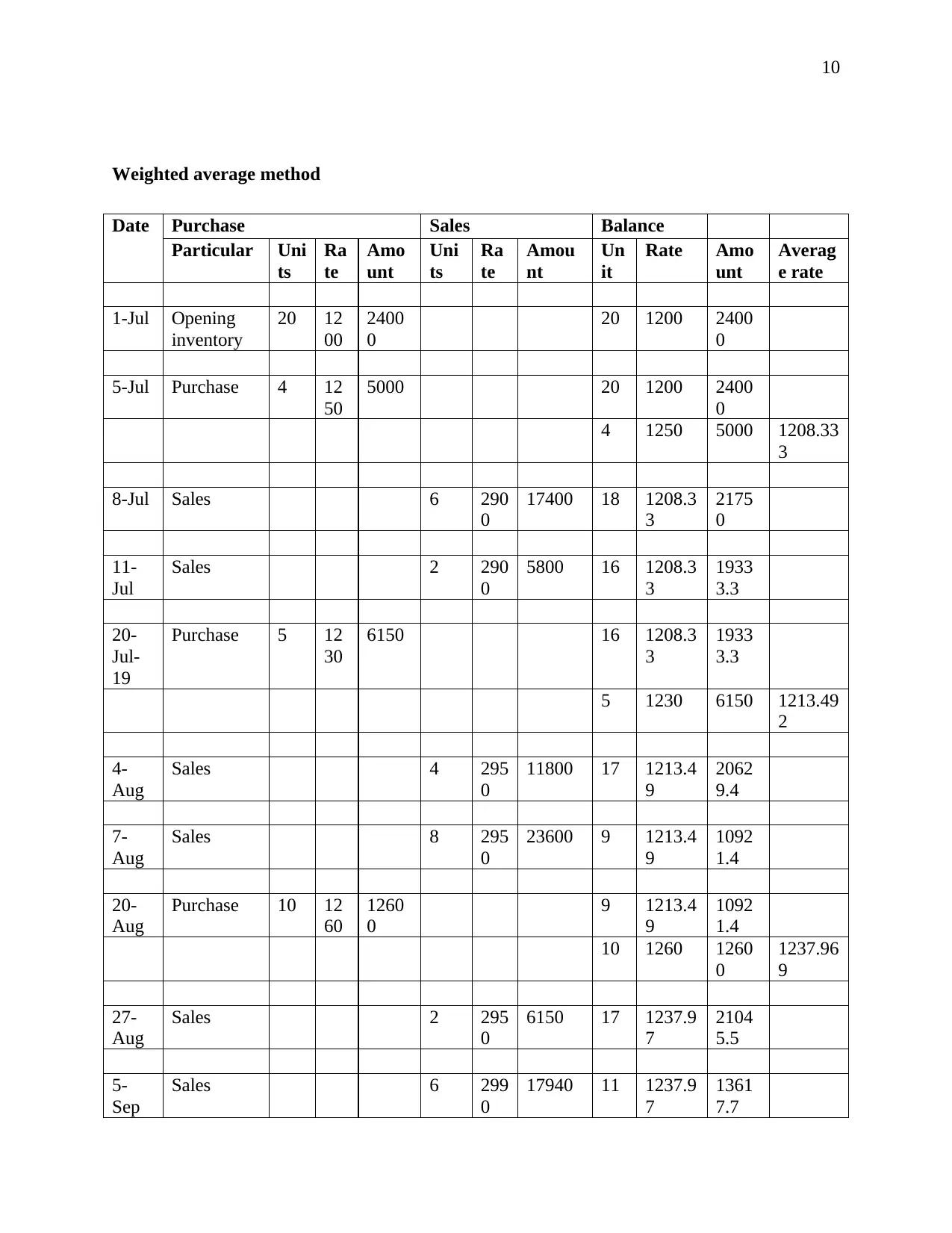

This assignment solution addresses key aspects of business accounting and finance, including the preparation of financial statements (income statement and balance sheet) for Home Designs Ltd., and the analysis of its financial performance. It demonstrates the application of inventory costing methods (FIFO, LIFO, and weighted average) to determine the cost of goods sold and gross profit. Ratio analysis is performed for three companies to evaluate profitability and liquidity, and the use of ratios for investment decisions is explored. The importance of working capital management is identified, and the concept of economic order quantity (EOQ) is explained and calculated. The assignment also examines the afterpay service, considering its benefits and disadvantages. The solution includes calculations, memo, and recommendations, providing a comprehensive overview of the financial concepts covered.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.