FIN20002 Finance Assignment: Equity, WACC, and Risk Analysis

VerifiedAdded on 2022/08/13

|13

|1744

|21

Homework Assignment

AI Summary

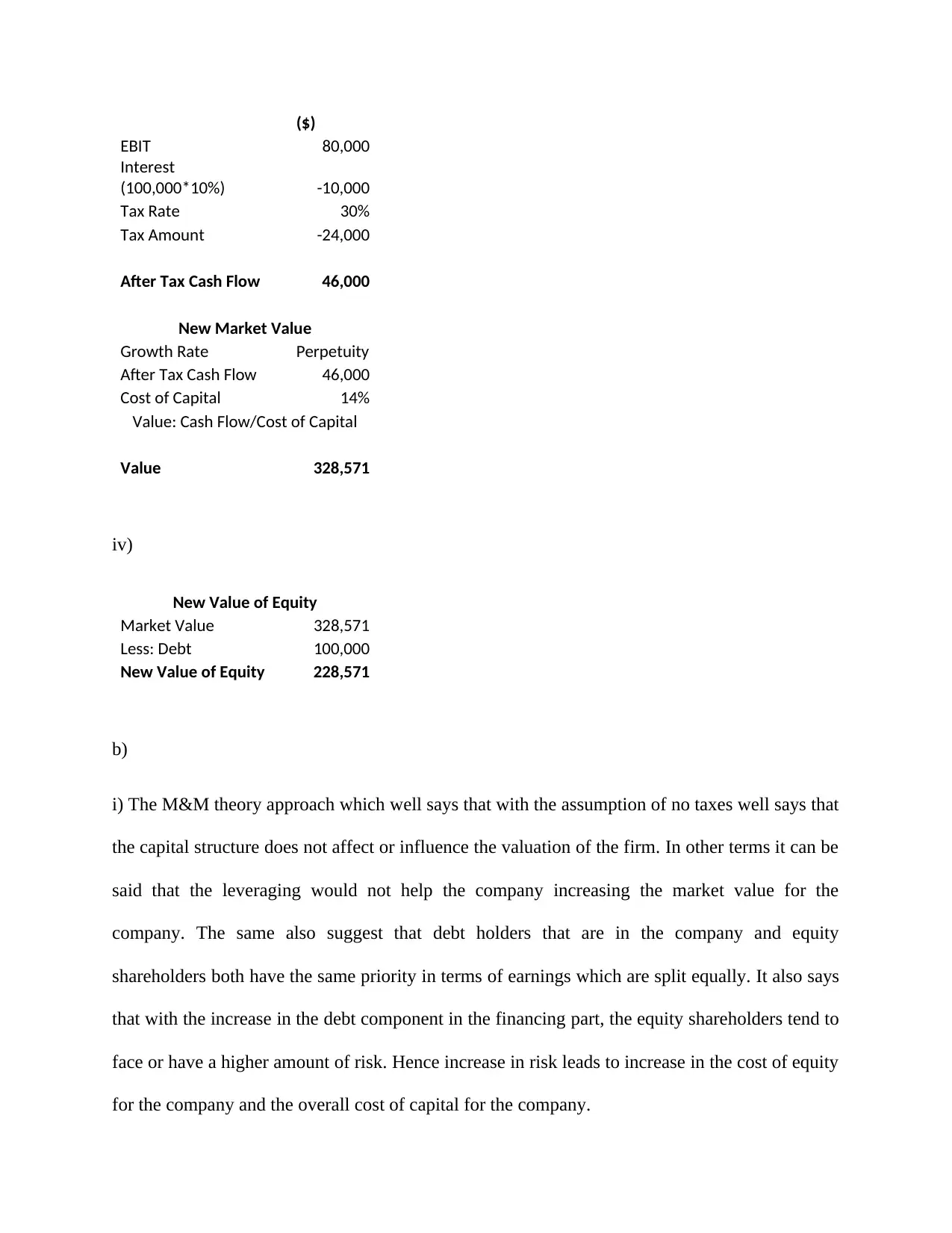

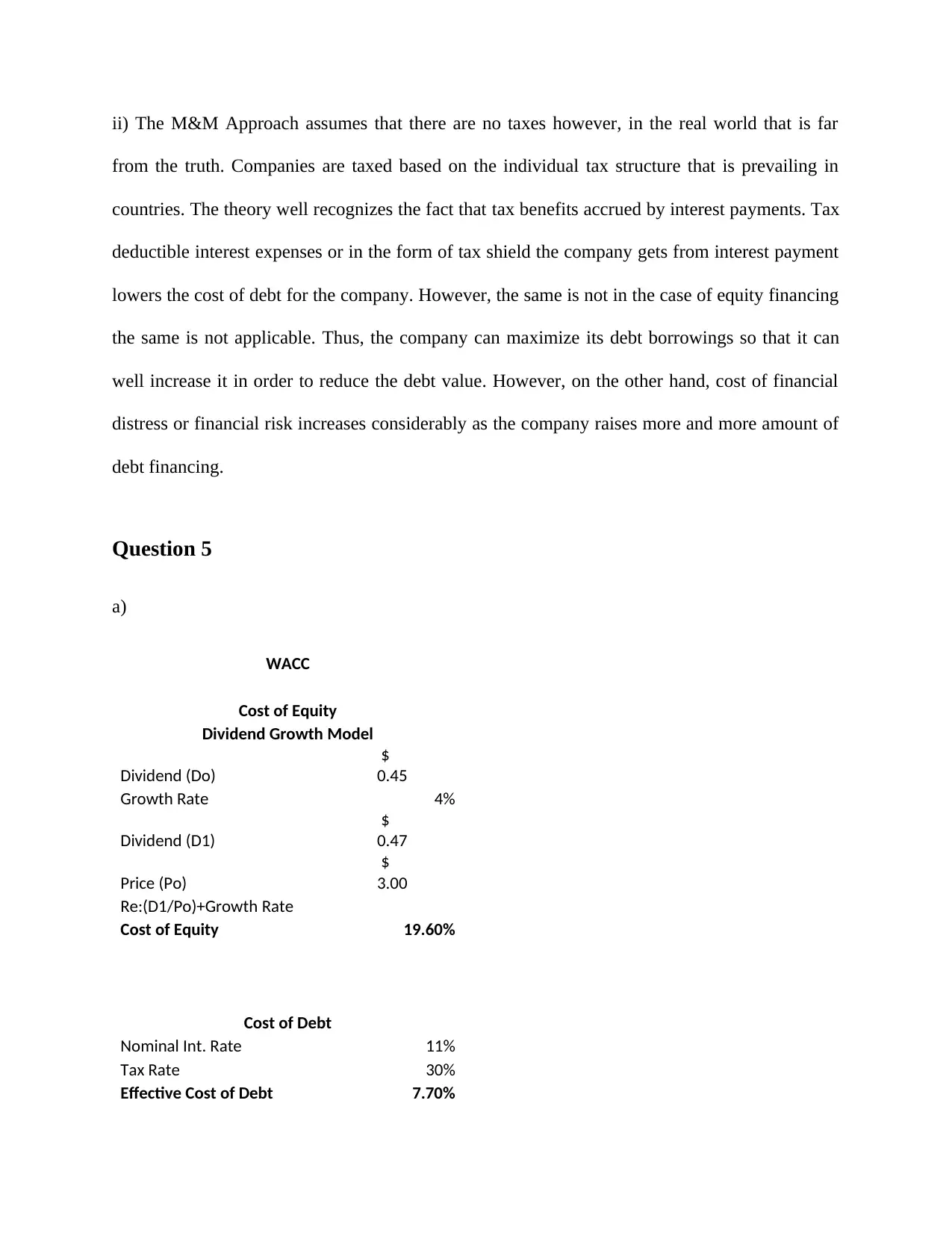

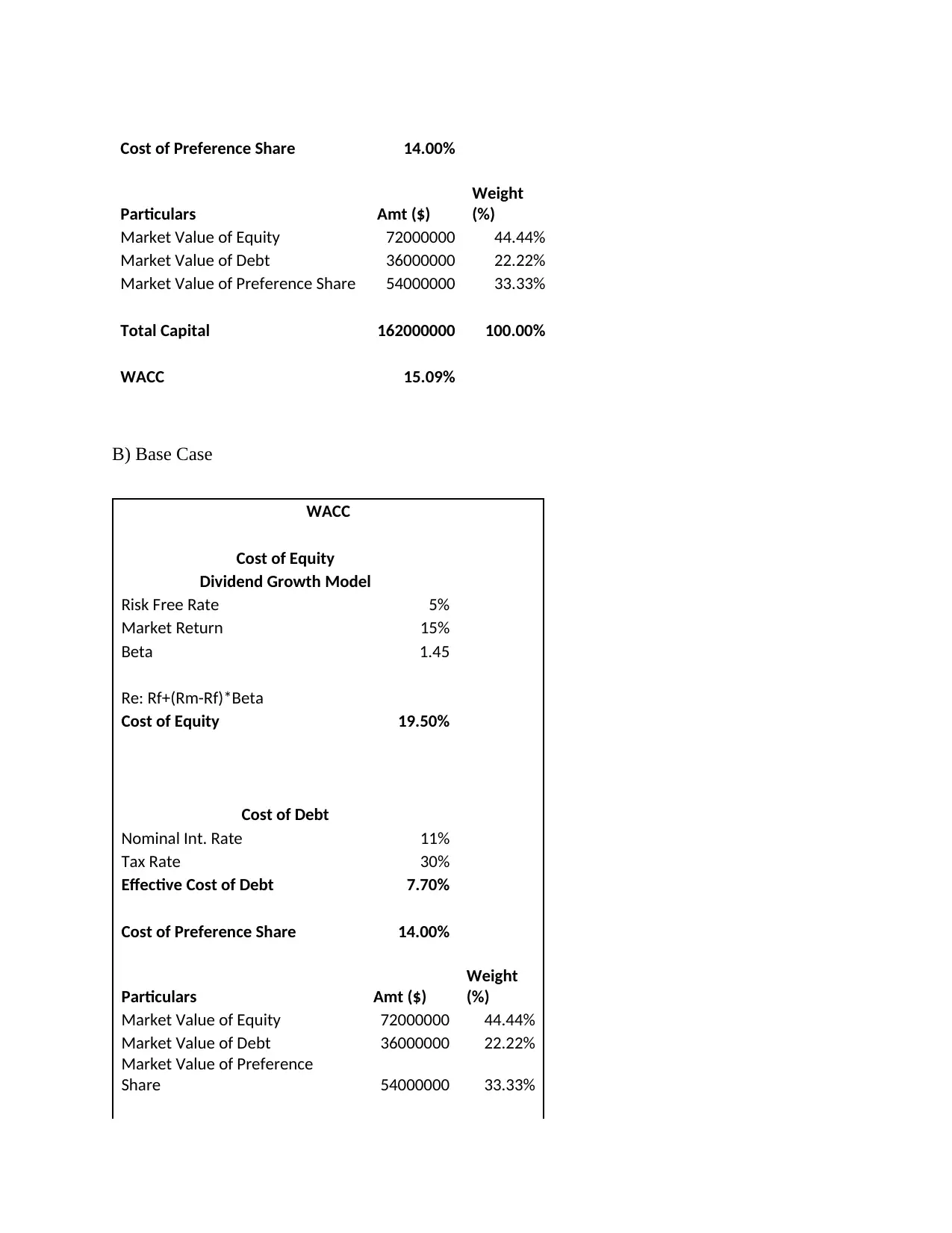

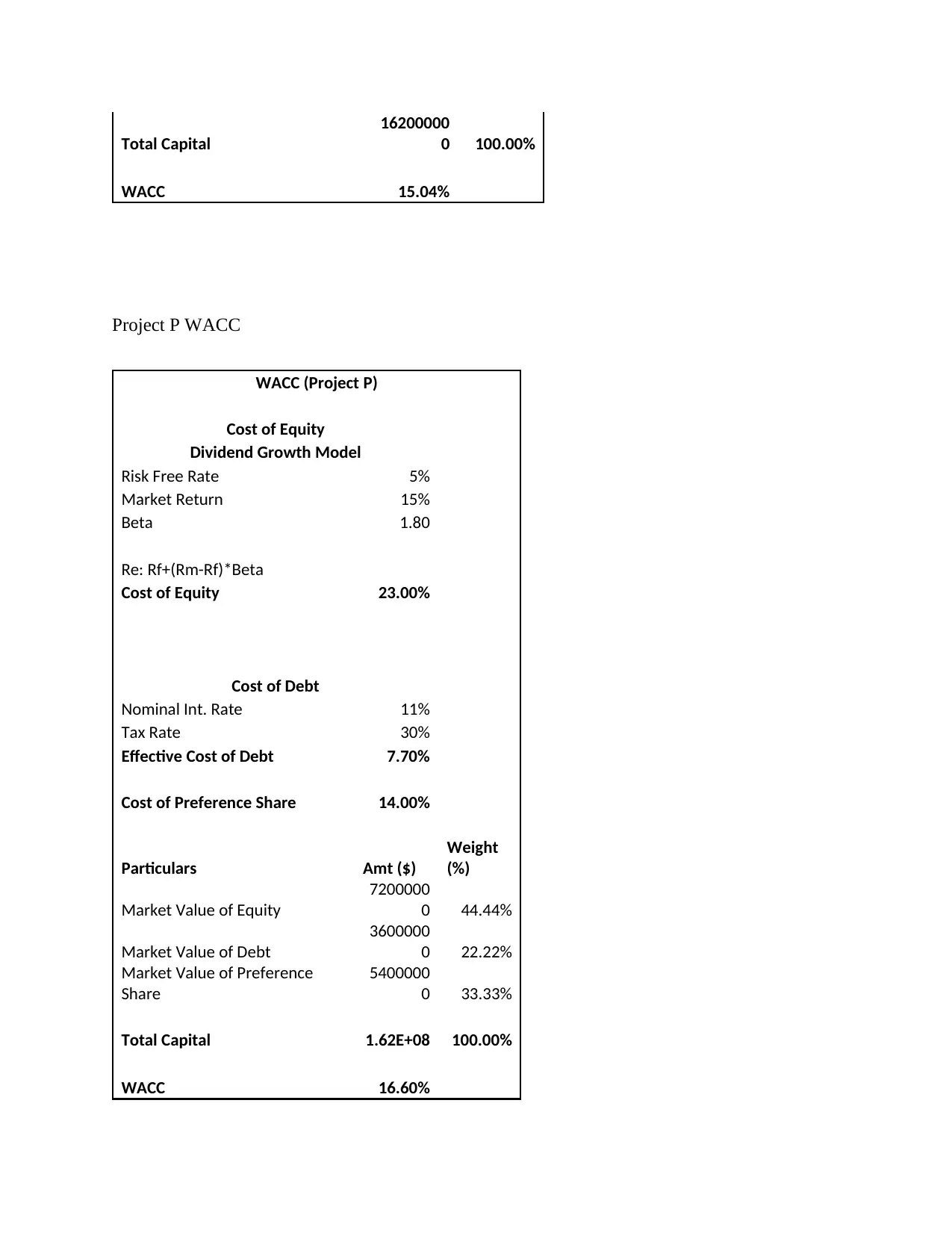

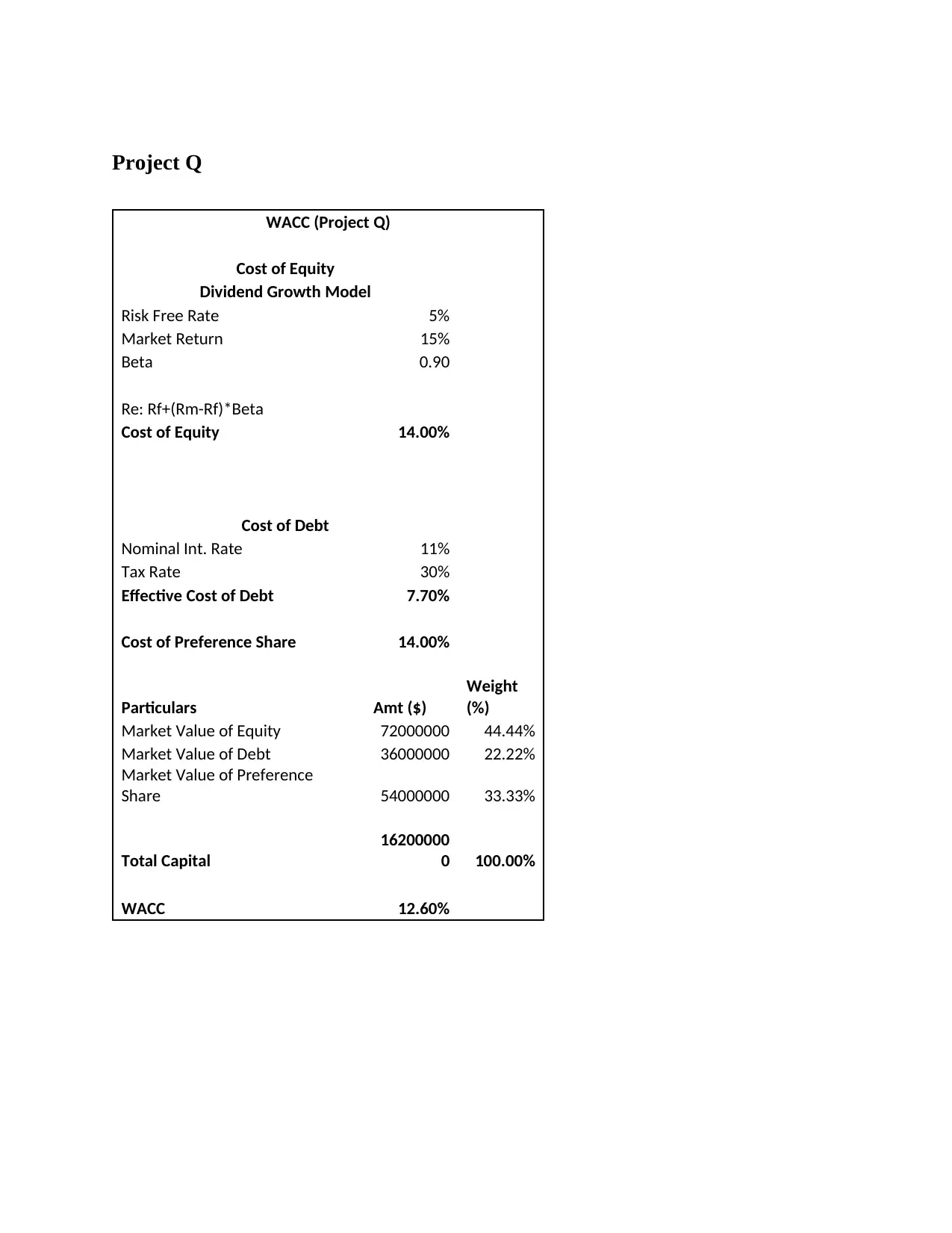

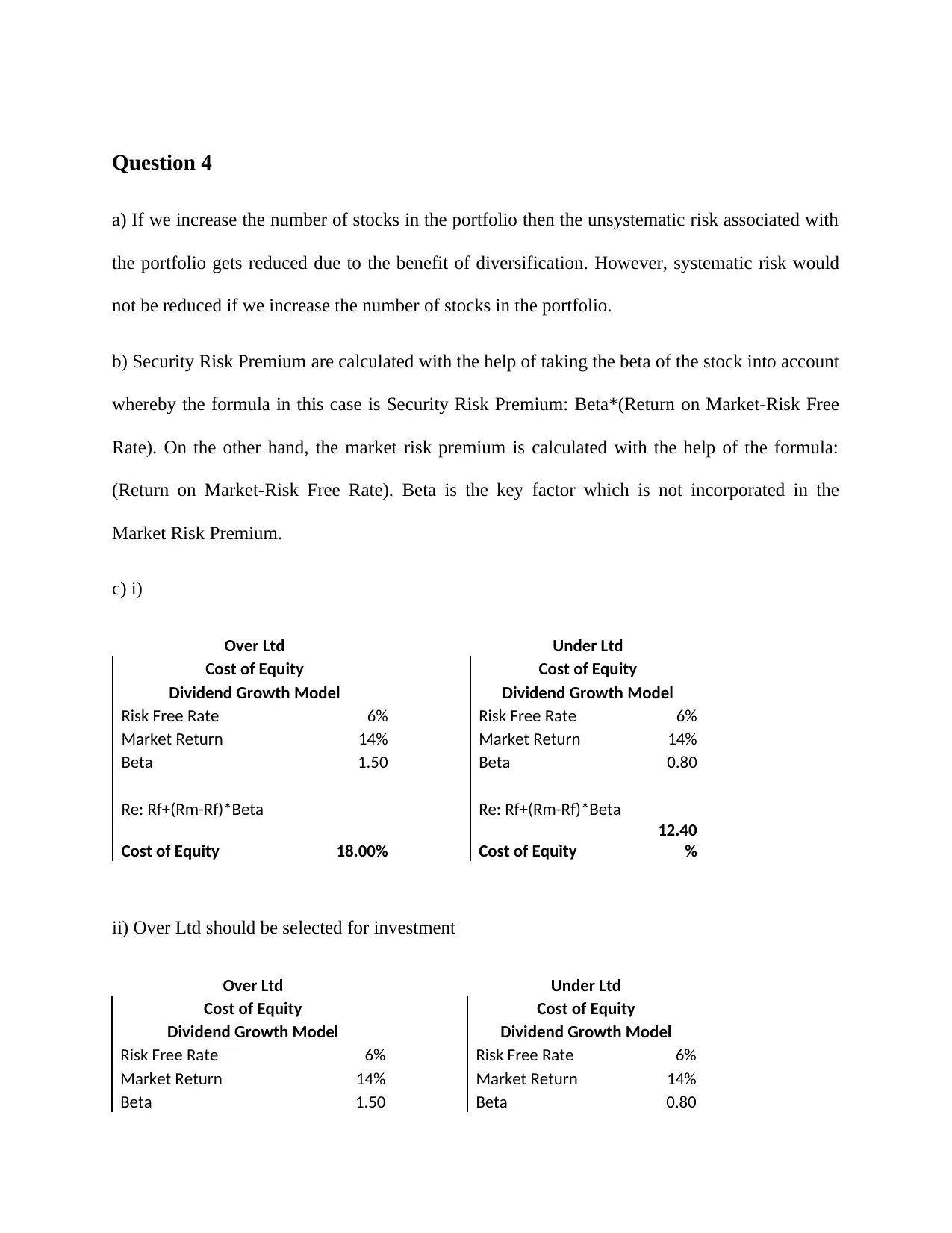

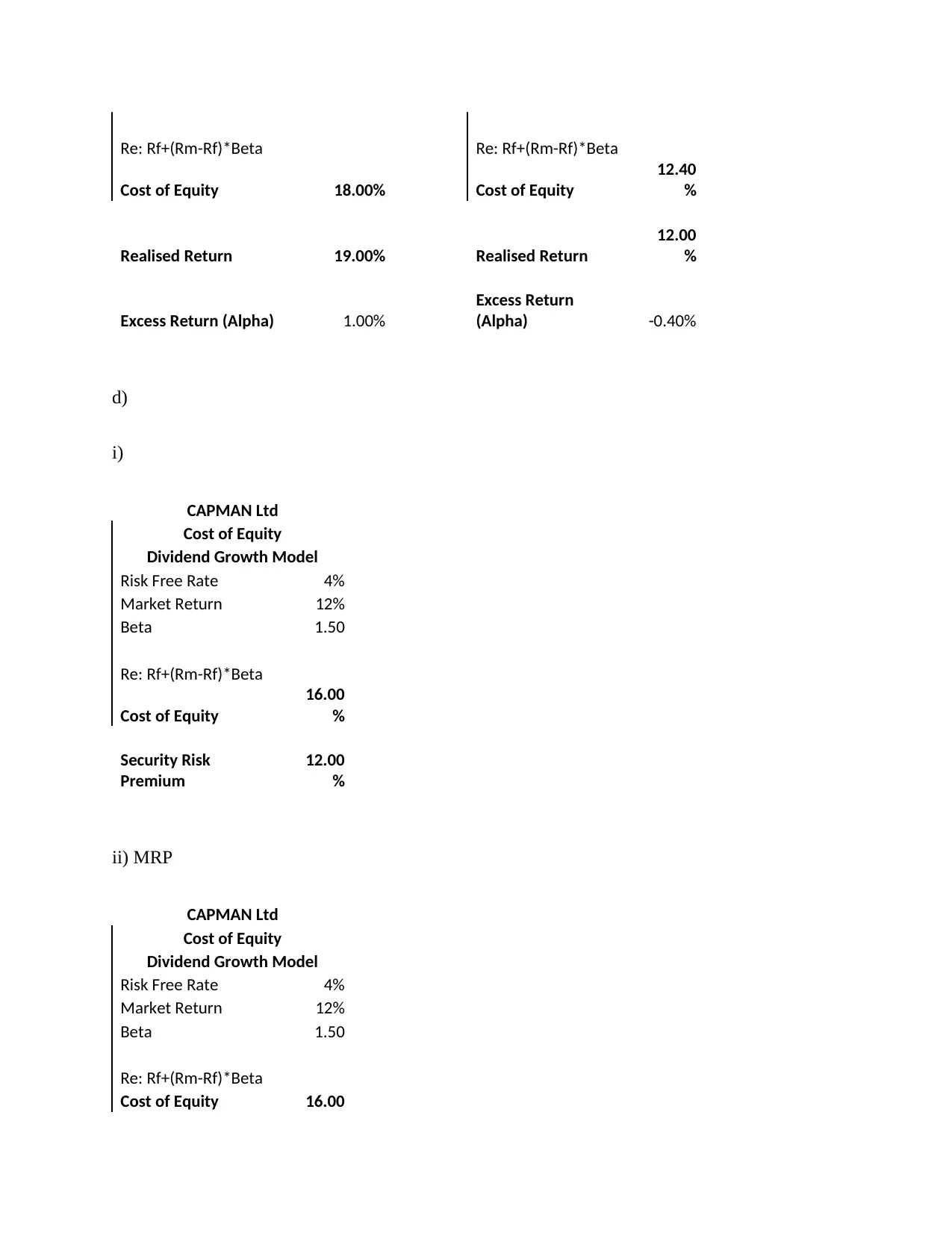

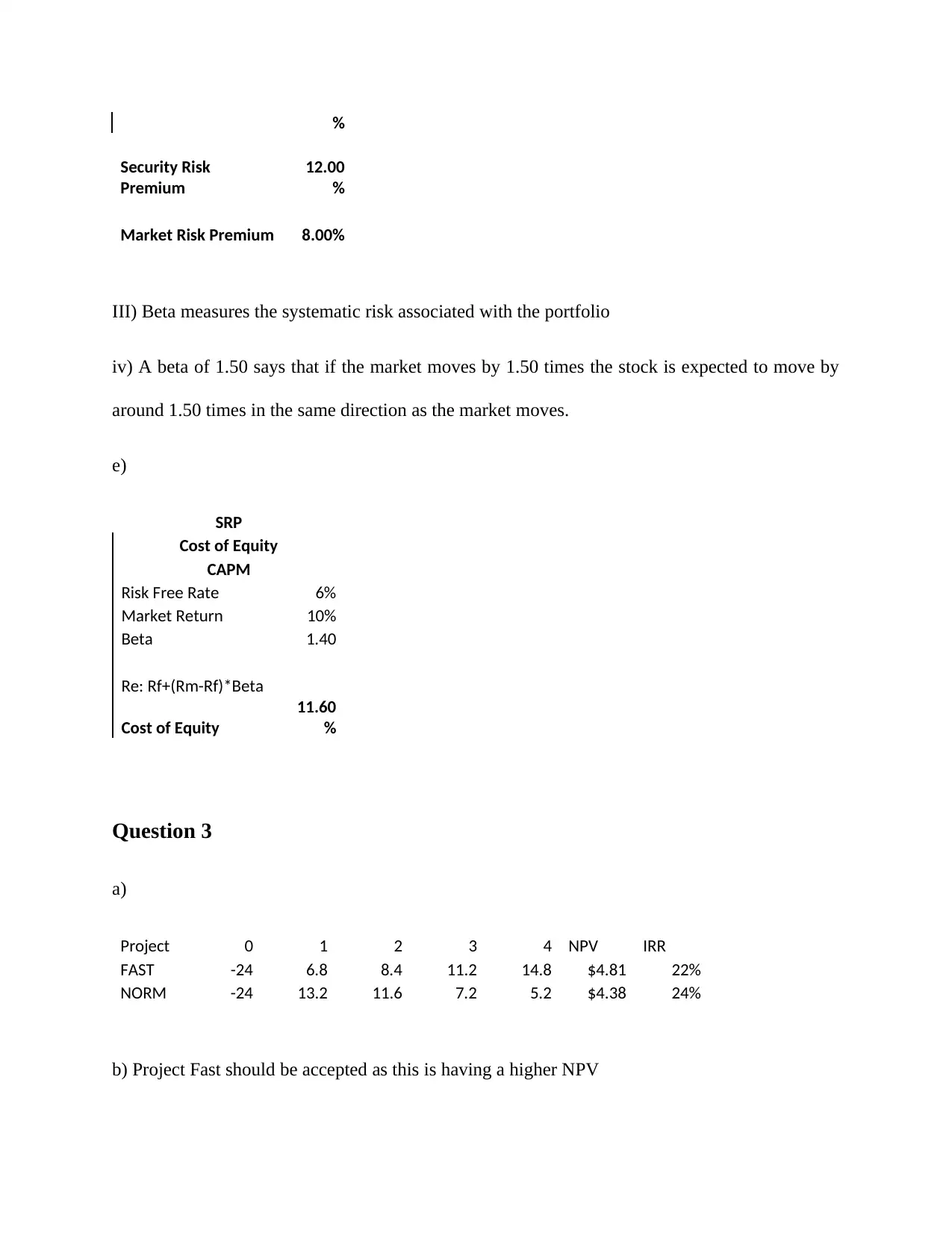

This document presents a comprehensive solution to a finance assignment, addressing key concepts in financial management. The solution begins with an analysis of equity finance, exploring sources like private placements, venture capital, and business angels, while also calculating right share values. It further delves into valuation techniques, including after-tax cash flow analysis, market value calculations, and the application of the M&M theory in capital structure decisions. The assignment also covers the calculation of the Weighted Average Cost of Capital (WACC) using both the dividend growth model and CAPM, along with the analysis of project-specific WACCs. Furthermore, it tackles risk and return concepts, including portfolio diversification, security risk premiums, and the Capital Asset Pricing Model (CAPM). The solutions include detailed calculations of NPV, IRR, and beta, offering a complete overview of financial analysis for investment and capital structure decisions.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.