UGB 163 Accounting and Finance Assignment: Financial Analysis Report

VerifiedAdded on 2023/01/18

|19

|2489

|76

Homework Assignment

AI Summary

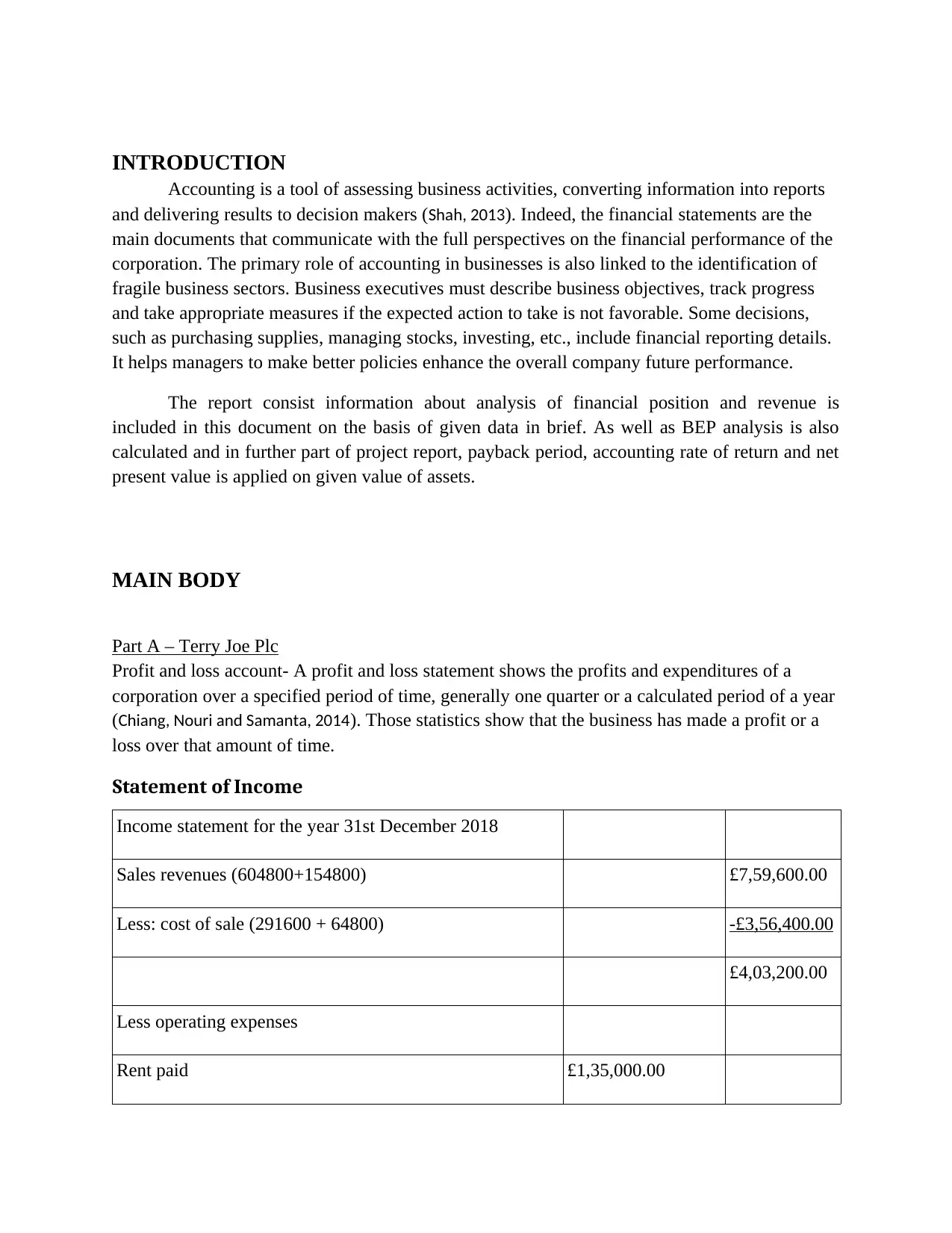

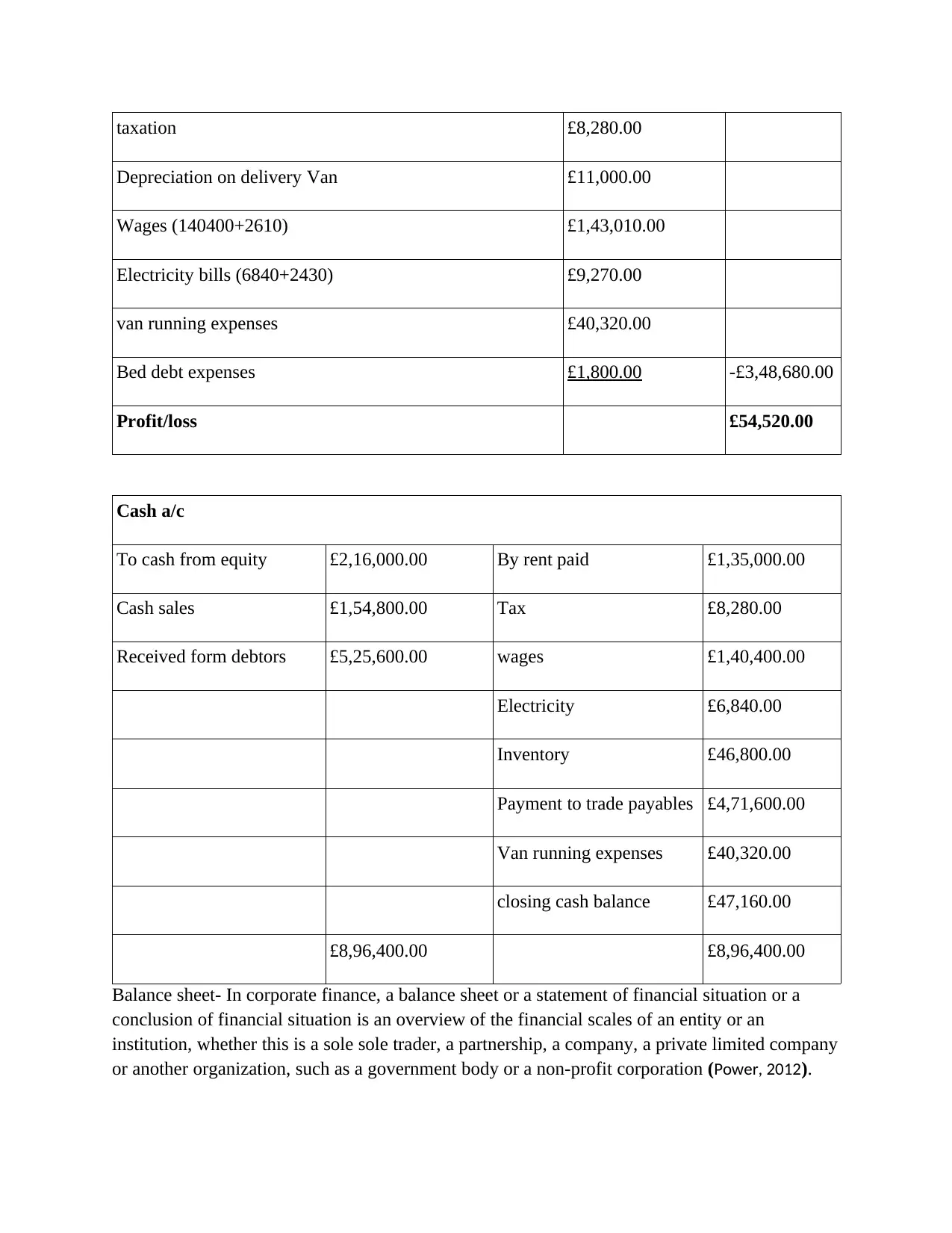

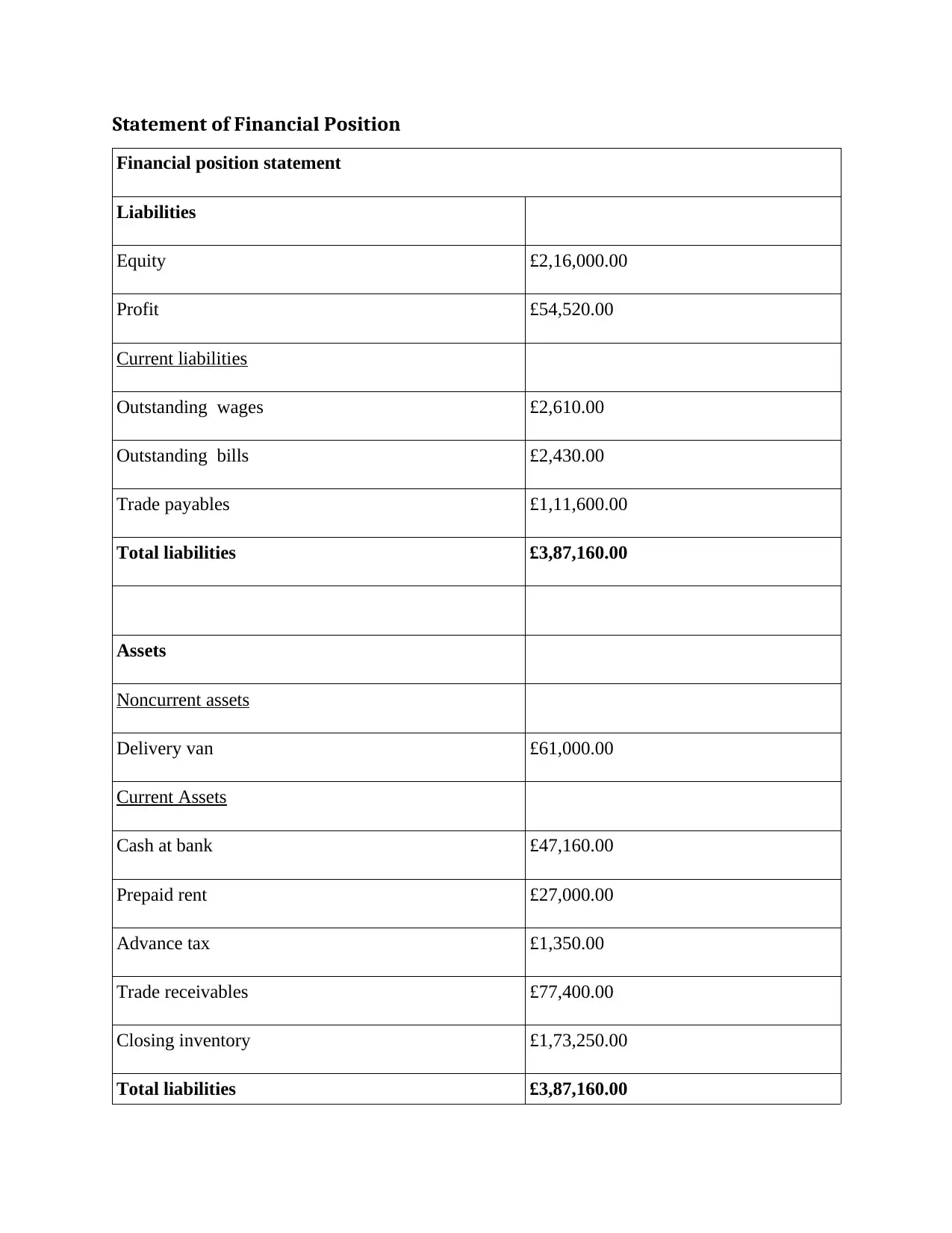

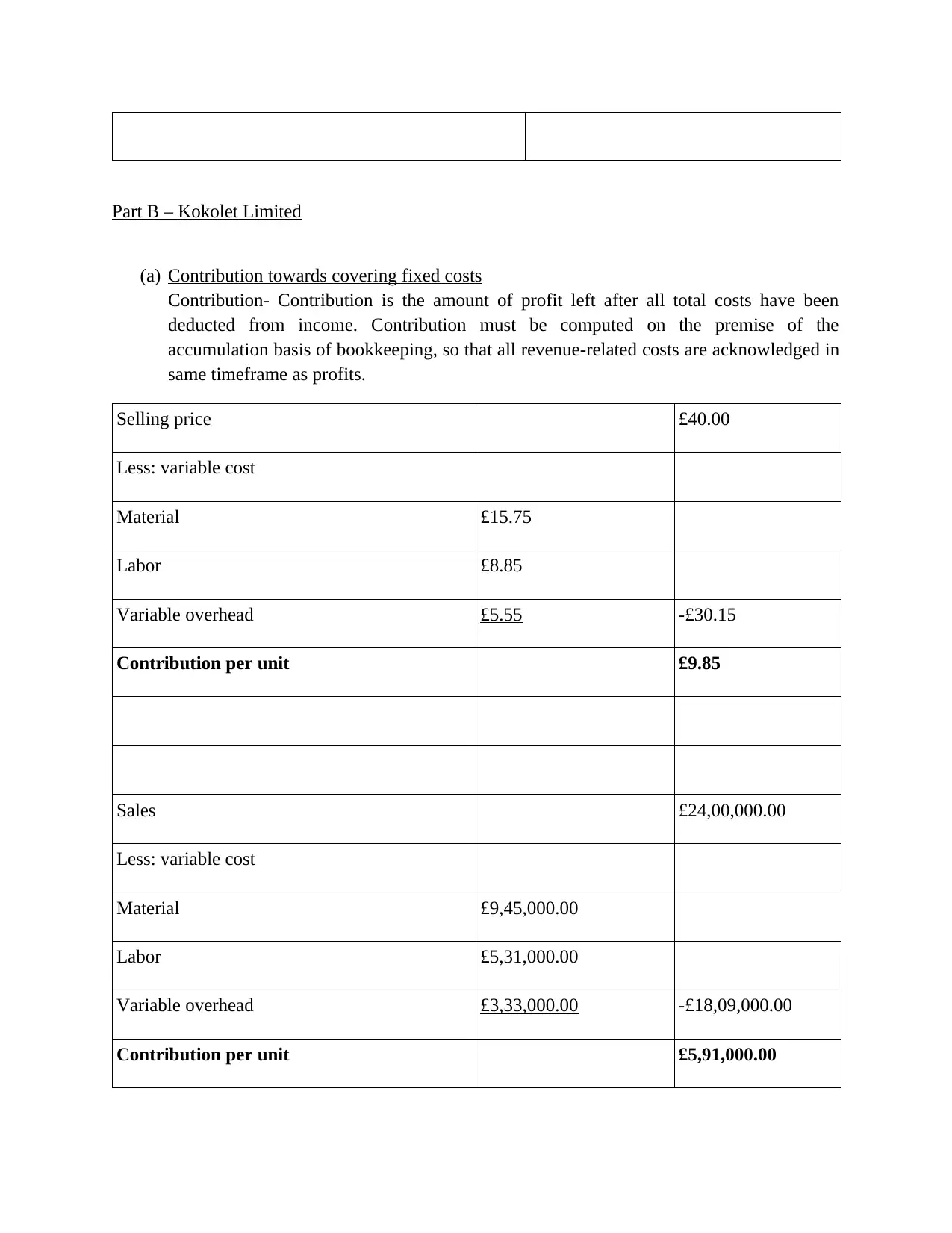

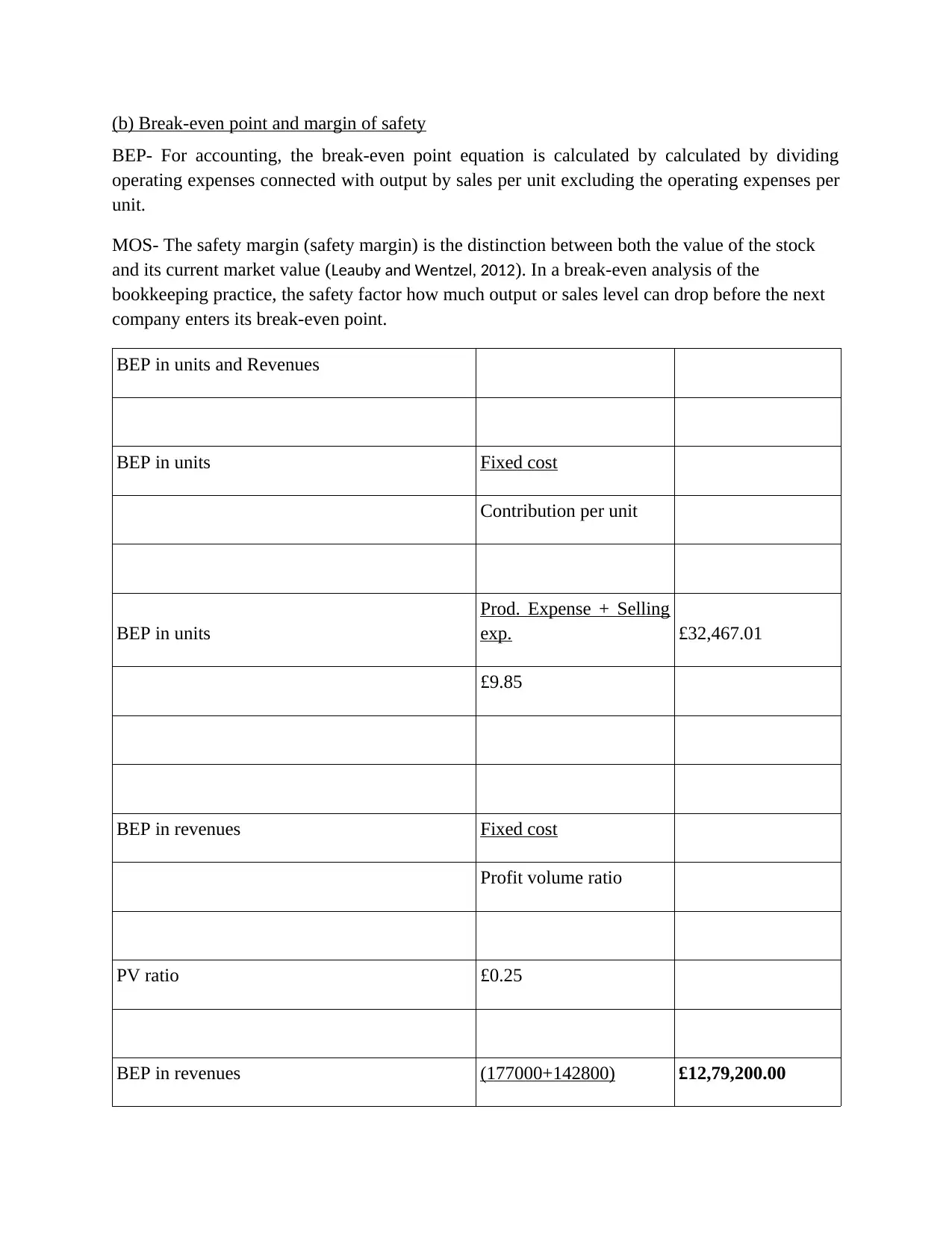

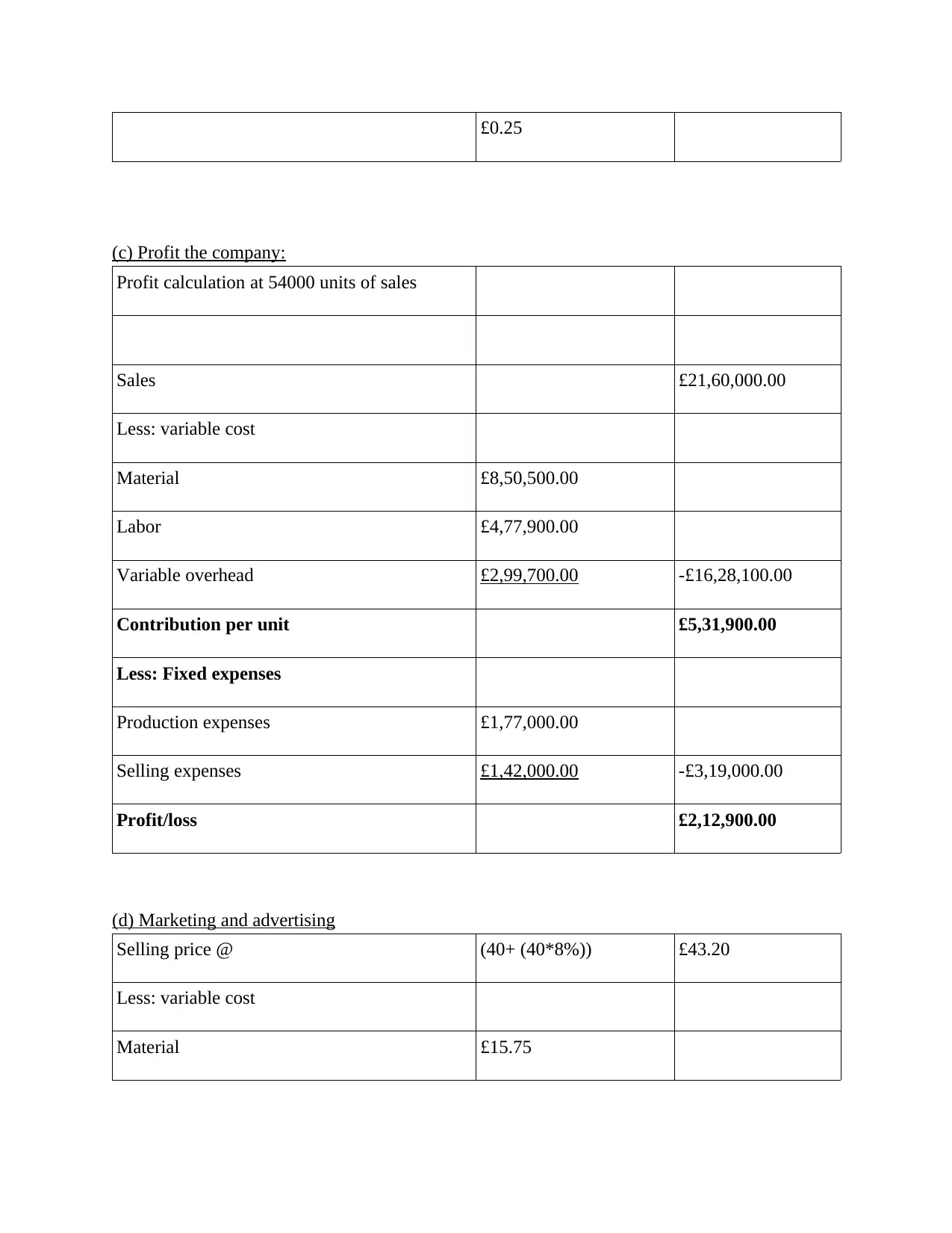

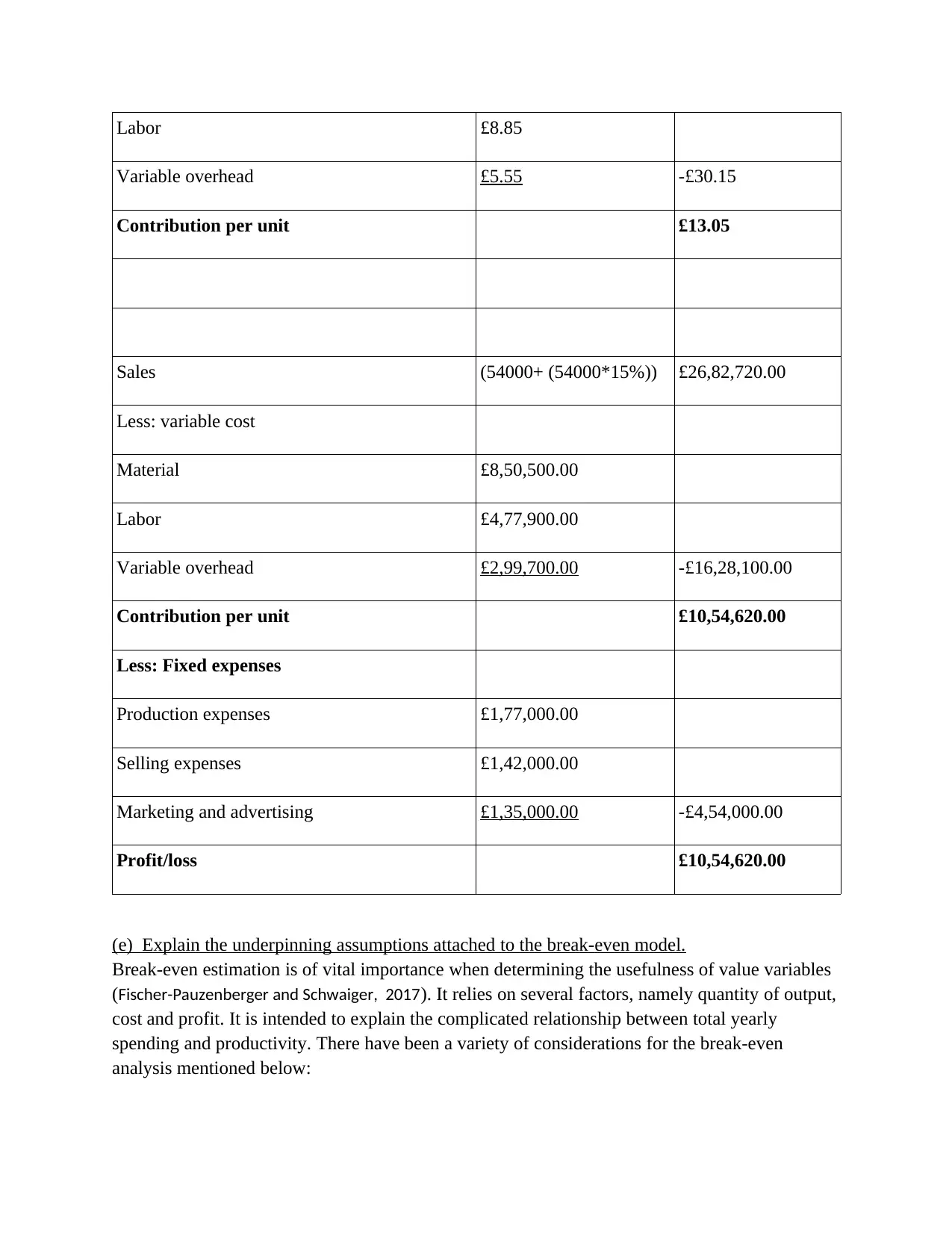

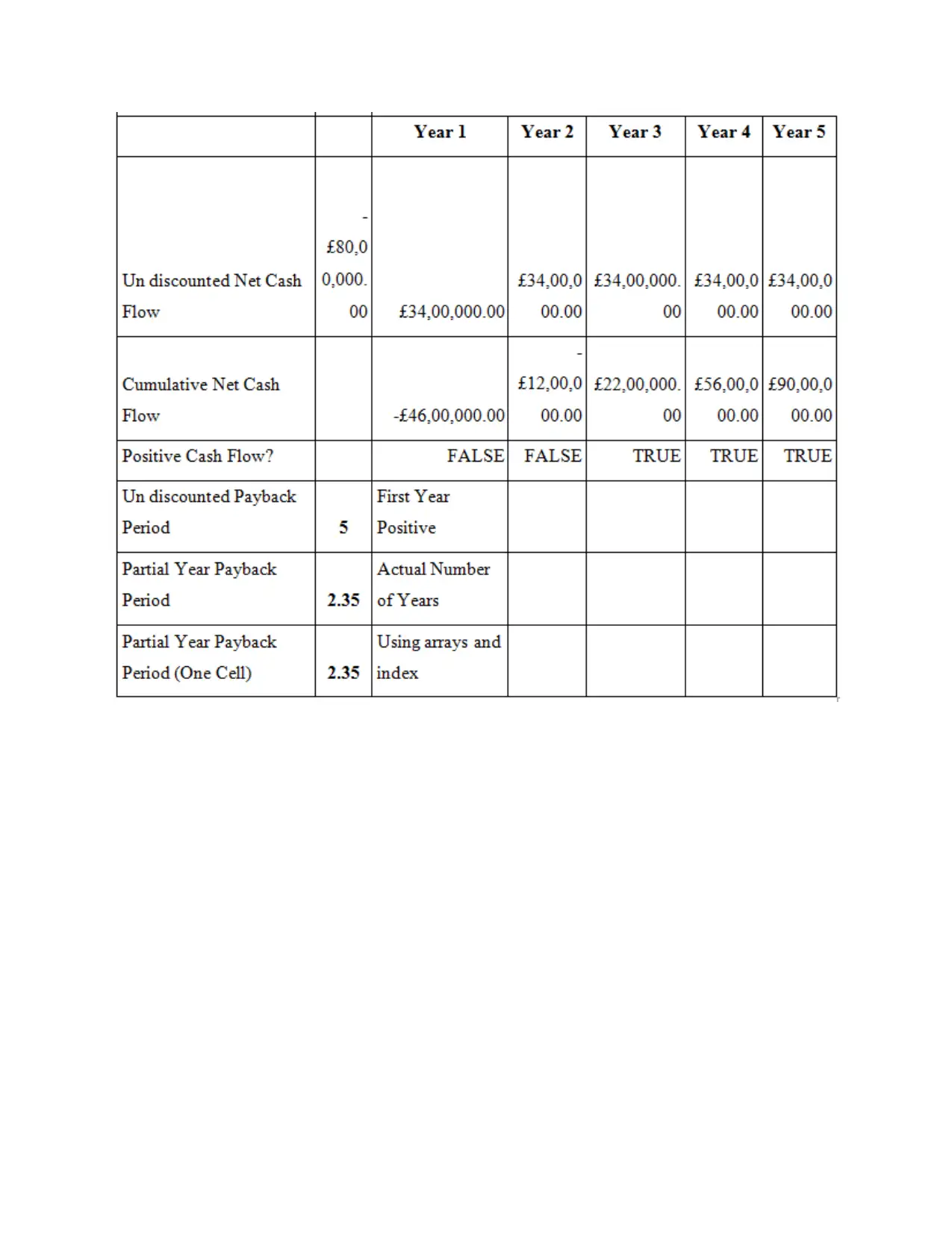

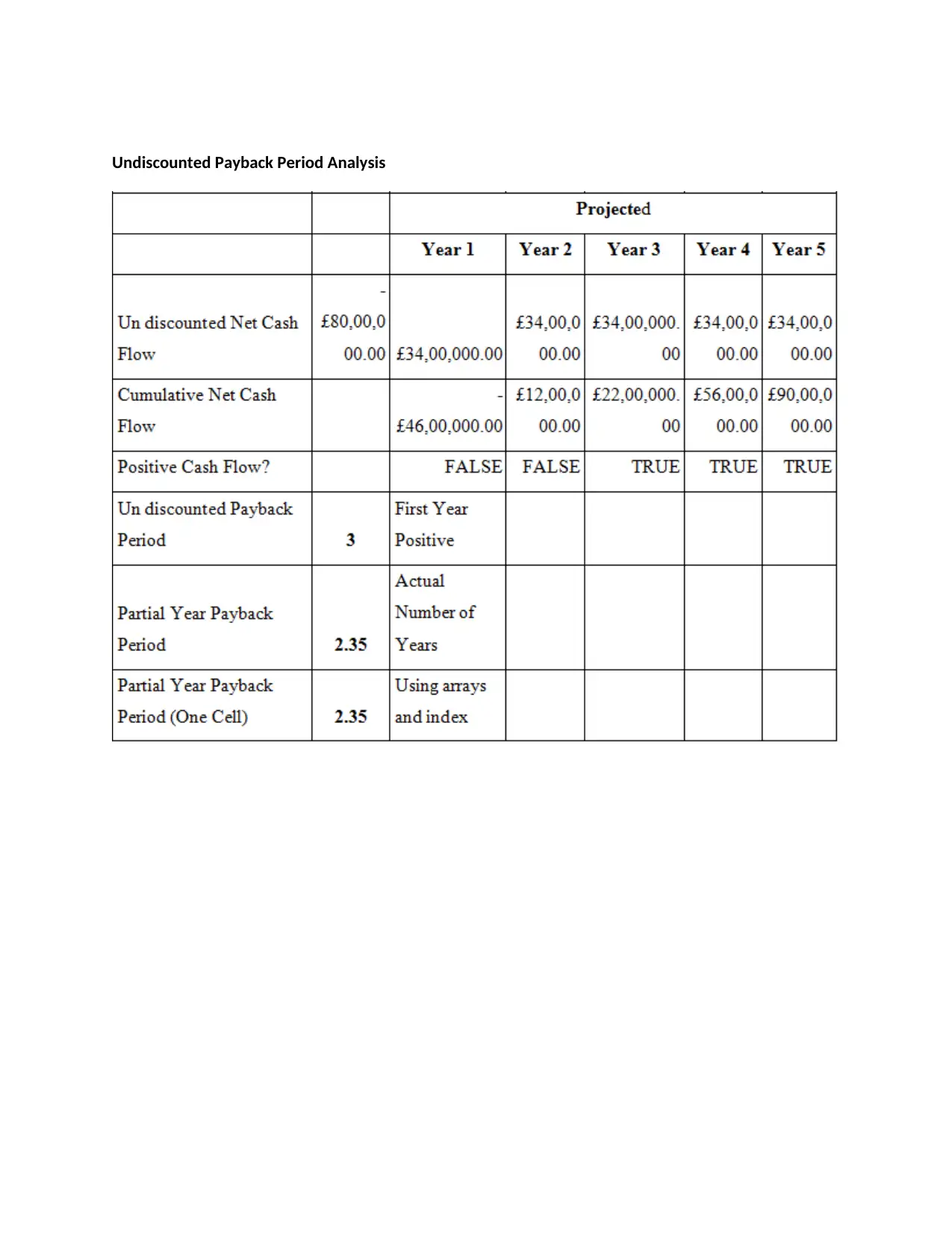

This assignment solution addresses a comprehensive accounting and finance problem, encompassing three distinct parts. Part A analyzes the financial performance of Terry Joe Plc, including the preparation of an income statement and a statement of financial position. Part B delves into cost accounting concepts, such as break-even analysis, contribution margin, and profit calculations for Kokolet Limited, also exploring marketing and advertising implications and the underlying assumptions of the break-even model. Part C evaluates investment appraisal techniques for Smith Howe Limited, including payback period, accounting rate of return, and net present value, alongside a comparative analysis of the merits and limitations of these techniques and the benefits and drawbacks of various budgeting methods for strategic planning. The solution provides detailed calculations, explanations, and analyses, offering a robust understanding of key accounting and finance principles.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.