Business Finance Assignment: Cash Conversion, NPV, and WACC Analysis

VerifiedAdded on 2023/01/05

|15

|2880

|44

Homework Assignment

AI Summary

This business finance assignment addresses key concepts including the cash conversion cycle, net present value (NPV), and internal rate of return (IRR) to evaluate investment decisions. It analyzes a company's financial statements, calculates the cash conversion cycle, and assesses the impact of factoring on working capital. The assignment also involves the calculation and comparison of NPV and IRR for two projects, considering changes in the cost of capital. Furthermore, it delves into the theoretical ex-rights price, net cash raised, and the value of rights in a rights issue, along with the advantages and disadvantages of such issues. Finally, the assignment calculates the weighted average cost of capital (WACC) and discusses strategies to minimize it through capital structure adjustments, providing a comprehensive overview of financial analysis and valuation techniques.

Business

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A. The length of cash conversion cycle and its significance to the company:............................1

B. should it accept the offer:........................................................................................................2

QUESTION 2...................................................................................................................................2

A. Net present value:....................................................................................................................2

B. Internal rate of return:.............................................................................................................3

C. Increase in cost of capital in year 5:........................................................................................4

QUESTION 3 ..................................................................................................................................5

A. The theoretical ex- rights price per share:...............................................................................5

B. The net cash raised:.................................................................................................................6

C. The value of the rights:............................................................................................................6

D. Advantage and disadvantage of right issue:............................................................................7

QUESTION 4...................................................................................................................................7

A. The company's weighted average cost of capital using market weightings:..........................7

B. Discussion of integration a sensible level of gearing into their capital structure, can

minimise their weighted average cost of capital:.........................................................................8

CONCLUSION................................................................................................................................8

REFRENCES.................................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A. The length of cash conversion cycle and its significance to the company:............................1

B. should it accept the offer:........................................................................................................2

QUESTION 2...................................................................................................................................2

A. Net present value:....................................................................................................................2

B. Internal rate of return:.............................................................................................................3

C. Increase in cost of capital in year 5:........................................................................................4

QUESTION 3 ..................................................................................................................................5

A. The theoretical ex- rights price per share:...............................................................................5

B. The net cash raised:.................................................................................................................6

C. The value of the rights:............................................................................................................6

D. Advantage and disadvantage of right issue:............................................................................7

QUESTION 4...................................................................................................................................7

A. The company's weighted average cost of capital using market weightings:..........................7

B. Discussion of integration a sensible level of gearing into their capital structure, can

minimise their weighted average cost of capital:.........................................................................8

CONCLUSION................................................................................................................................8

REFRENCES.................................................................................................................................10

INTRODUCTION

Business finance is concern with external financial resource that a firm realise for fulfil

its financial or monetary needs. It tells firm about the fund and money credit requirement to run

business operations. It helps firm in managing and raising fund by planning, organising, analysis

and controlling. This report covers such task that are length of cash conversion cycle and

evaluation of it, some methods of investment techniques that are net present value, internal rate

of return. Apart from this it also covers task such as valuation of different share, weighted

average cost of capital and its discussion and dividend or dividend return calculation (Steffen,

2018).

QUESTION 1

A. The length of cash conversion cycle and its significance to the company:

Cash conversion cycle refers the time in which firm convert its investment into inventory

and resources into cash by sales. It helps firm to know about the actual cash flow from growth. It

is method between cash outflow and cash inflow. It is important for the company to determine

the efficiency of the firm that it can convert its investment into cash and sales into cash. The cash

conversion period for the firm is approx 140 days. It is important in company to assessing firm's

operations and understand of risk (Motta, V., 2020).

1. Cash conversion cycle

CCC= DIO + DSO – DPO

Days inventory outstanding

DIO= ( Average inventory / cost of goods sold) * 365

average inventory= 1634 + 2018 = 3652

cost of goods sold = 8860

=( 3652 / 8860 ) * 365

= 138.50

Days sales 0oustanding

DSO = (account receivables / net credit sales ) * 365

Business finance is concern with external financial resource that a firm realise for fulfil

its financial or monetary needs. It tells firm about the fund and money credit requirement to run

business operations. It helps firm in managing and raising fund by planning, organising, analysis

and controlling. This report covers such task that are length of cash conversion cycle and

evaluation of it, some methods of investment techniques that are net present value, internal rate

of return. Apart from this it also covers task such as valuation of different share, weighted

average cost of capital and its discussion and dividend or dividend return calculation (Steffen,

2018).

QUESTION 1

A. The length of cash conversion cycle and its significance to the company:

Cash conversion cycle refers the time in which firm convert its investment into inventory

and resources into cash by sales. It helps firm to know about the actual cash flow from growth. It

is method between cash outflow and cash inflow. It is important for the company to determine

the efficiency of the firm that it can convert its investment into cash and sales into cash. The cash

conversion period for the firm is approx 140 days. It is important in company to assessing firm's

operations and understand of risk (Motta, V., 2020).

1. Cash conversion cycle

CCC= DIO + DSO – DPO

Days inventory outstanding

DIO= ( Average inventory / cost of goods sold) * 365

average inventory= 1634 + 2018 = 3652

cost of goods sold = 8860

=( 3652 / 8860 ) * 365

= 138.50

Days sales 0oustanding

DSO = (account receivables / net credit sales ) * 365

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

account receivables = 1538

net credit sales = 12000

DSO = 1538 / 12000 * 365

= 46.78

Days payable outstanding

DPO = ending accounts payables / ( cost of goods sold / 365 )

net credit sales = 12000

DSO = 1538 / 12000 * 365

= 46.78

Days payable outstanding

DPO = ending accounts payables / ( cost of goods sold / 365 )

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ending account payables= 1092

cost of goods sold = 8860

DPO = 1092 / ( 8860 / 365 )

= 44.986

CCC= DIO + DSO – DPO

= 138.50 + 46.78 – 44.986

= 140.294 DAYS OR 140 APPROX

B. should it accept the offer:

It should accept the offer because its all allocations are higher as it shows days in

inventory outstanding is 138.50, days in sales outstanding is 46.78 and its payable outstanding is

44.986 that is less then cash inflow. It is a negative sign for the firm that firm can convert its

inventory in 138.50 days and its cash inflow is 46.78 days and cash outflow is 44.986 because

the lower the cash conversion days indicates firm's more liquidity (Lee and Shin, 2018).

QUESTION 2

A. Net present value:

Net present value is tool used in capital budgeting to identify investment planning and

profitability of project or investment. It is to determine all current value of future cash flows

generated by project. The importance of NPV is to determine which project or investment will

result in profit and loss for company. It helps to know whether the value of all cash flows exceed

the cost of project or not. Also it helps firm to know which option give more return rather than

other one. From the above analysis, The cost if investment of project A is 150 and 152 in project

B. It is to be suggested that project B is more profitable as it is higher than project A, because

NPV is higher in project B and less in project A which indicates that future cash flow is more

than in project B. In project A it gives return about 51.81 over 150 outflow and in project B it

give return about 61.25 over 152 invested amount that shows Project B gives higher return on

investments than A.

(A) NET PRESENT VALUE

3

cost of goods sold = 8860

DPO = 1092 / ( 8860 / 365 )

= 44.986

CCC= DIO + DSO – DPO

= 138.50 + 46.78 – 44.986

= 140.294 DAYS OR 140 APPROX

B. should it accept the offer:

It should accept the offer because its all allocations are higher as it shows days in

inventory outstanding is 138.50, days in sales outstanding is 46.78 and its payable outstanding is

44.986 that is less then cash inflow. It is a negative sign for the firm that firm can convert its

inventory in 138.50 days and its cash inflow is 46.78 days and cash outflow is 44.986 because

the lower the cash conversion days indicates firm's more liquidity (Lee and Shin, 2018).

QUESTION 2

A. Net present value:

Net present value is tool used in capital budgeting to identify investment planning and

profitability of project or investment. It is to determine all current value of future cash flows

generated by project. The importance of NPV is to determine which project or investment will

result in profit and loss for company. It helps to know whether the value of all cash flows exceed

the cost of project or not. Also it helps firm to know which option give more return rather than

other one. From the above analysis, The cost if investment of project A is 150 and 152 in project

B. It is to be suggested that project B is more profitable as it is higher than project A, because

NPV is higher in project B and less in project A which indicates that future cash flow is more

than in project B. In project A it gives return about 51.81 over 150 outflow and in project B it

give return about 61.25 over 152 invested amount that shows Project B gives higher return on

investments than A.

(A) NET PRESENT VALUE

3

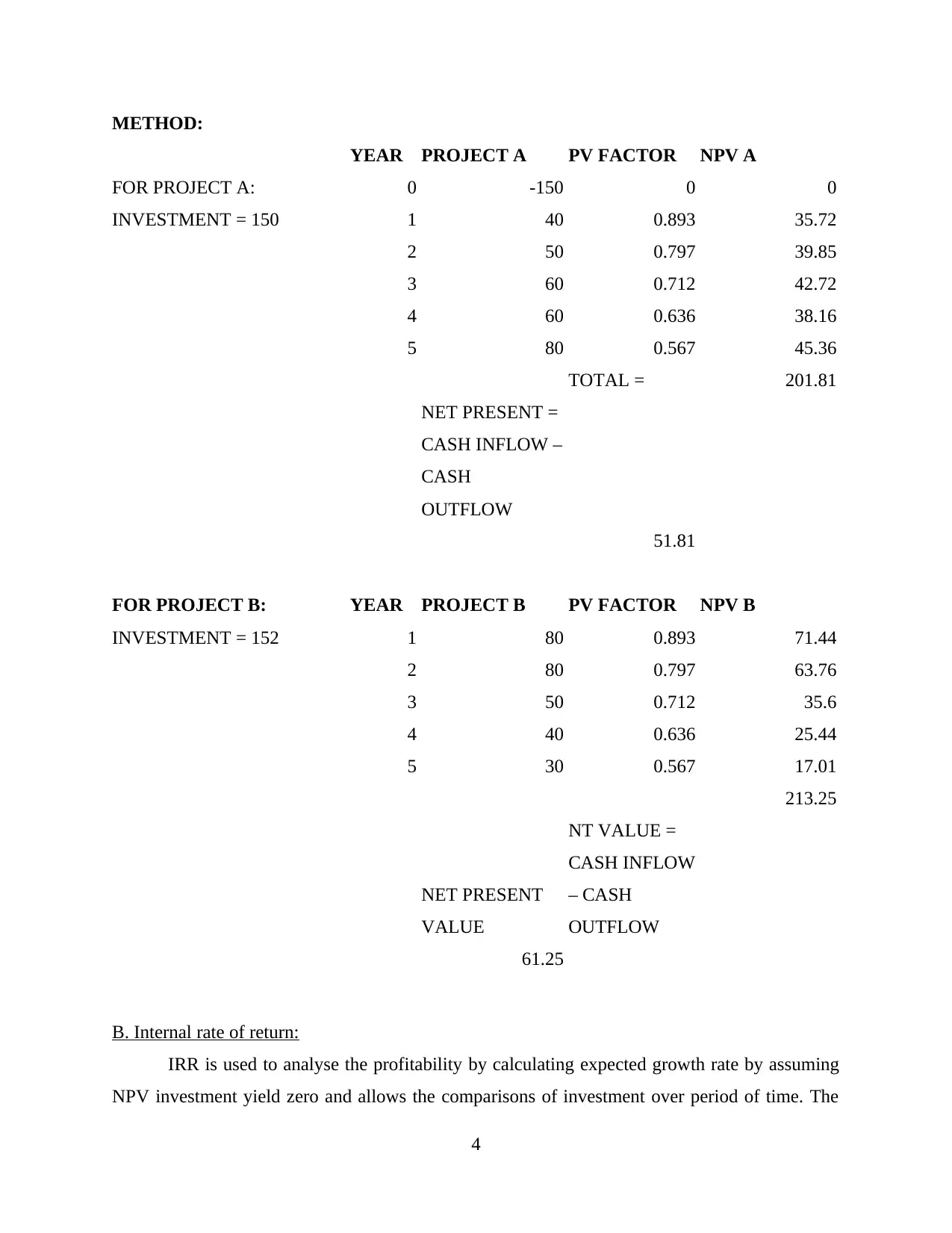

METHOD:

YEAR PROJECT A PV FACTOR NPV A

FOR PROJECT A: 0 -150 0 0

INVESTMENT = 150 1 40 0.893 35.72

2 50 0.797 39.85

3 60 0.712 42.72

4 60 0.636 38.16

5 80 0.567 45.36

TOTAL = 201.81

NET PRESENT =

CASH INFLOW –

CASH

OUTFLOW

51.81

FOR PROJECT B: YEAR PROJECT B PV FACTOR NPV B

INVESTMENT = 152 1 80 0.893 71.44

2 80 0.797 63.76

3 50 0.712 35.6

4 40 0.636 25.44

5 30 0.567 17.01

213.25

NET PRESENT

VALUE

NT VALUE =

CASH INFLOW

– CASH

OUTFLOW

61.25

B. Internal rate of return:

IRR is used to analyse the profitability by calculating expected growth rate by assuming

NPV investment yield zero and allows the comparisons of investment over period of time. The

4

YEAR PROJECT A PV FACTOR NPV A

FOR PROJECT A: 0 -150 0 0

INVESTMENT = 150 1 40 0.893 35.72

2 50 0.797 39.85

3 60 0.712 42.72

4 60 0.636 38.16

5 80 0.567 45.36

TOTAL = 201.81

NET PRESENT =

CASH INFLOW –

CASH

OUTFLOW

51.81

FOR PROJECT B: YEAR PROJECT B PV FACTOR NPV B

INVESTMENT = 152 1 80 0.893 71.44

2 80 0.797 63.76

3 50 0.712 35.6

4 40 0.636 25.44

5 30 0.567 17.01

213.25

NET PRESENT

VALUE

NT VALUE =

CASH INFLOW

– CASH

OUTFLOW

61.25

B. Internal rate of return:

IRR is used to analyse the profitability by calculating expected growth rate by assuming

NPV investment yield zero and allows the comparisons of investment over period of time. The

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

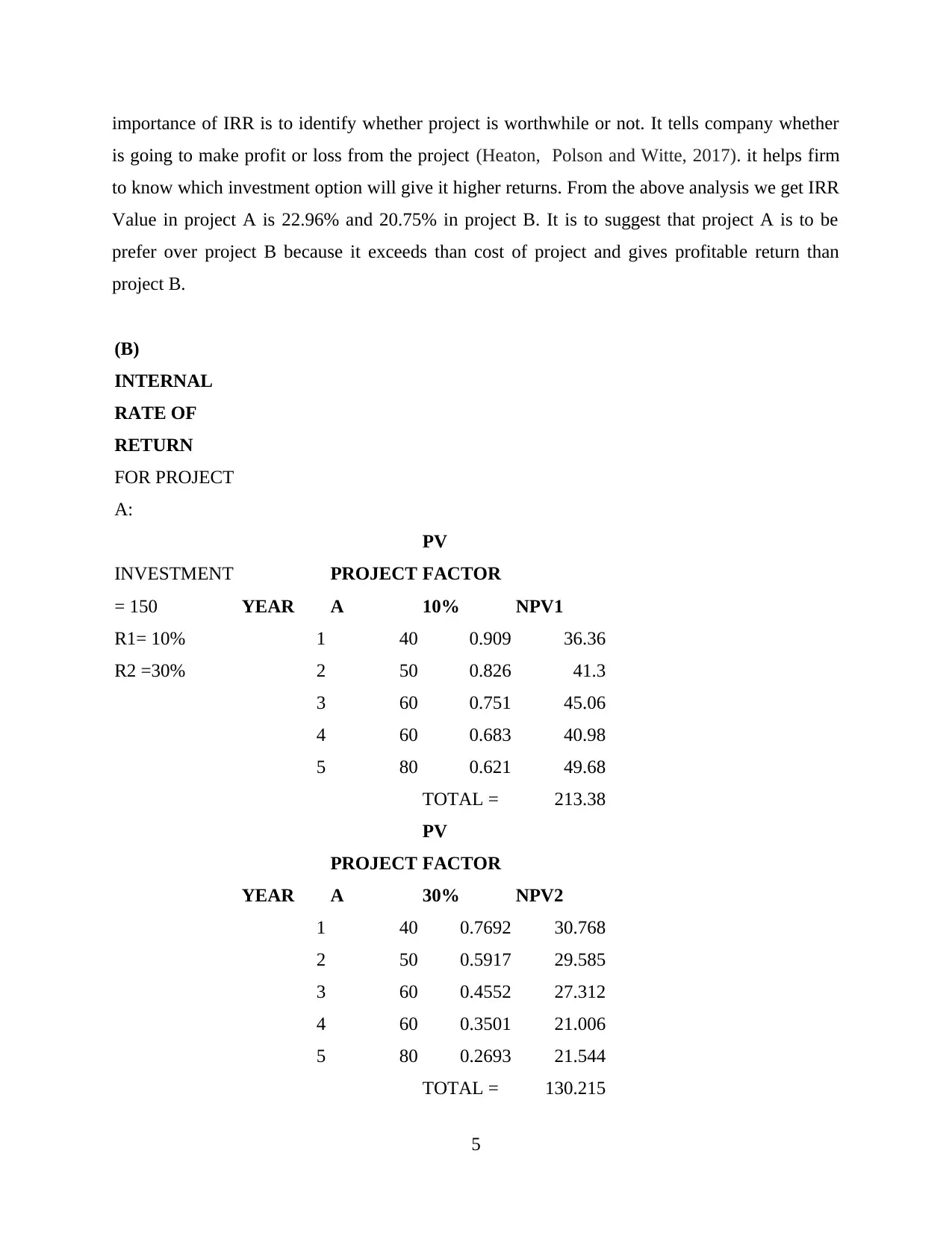

importance of IRR is to identify whether project is worthwhile or not. It tells company whether

is going to make profit or loss from the project (Heaton, Polson and Witte, 2017). it helps firm

to know which investment option will give it higher returns. From the above analysis we get IRR

Value in project A is 22.96% and 20.75% in project B. It is to suggest that project A is to be

prefer over project B because it exceeds than cost of project and gives profitable return than

project B.

(B)

INTERNAL

RATE OF

RETURN

FOR PROJECT

A:

INVESTMENT

= 150 YEAR

PROJECT

A

PV

FACTOR

10% NPV1

R1= 10% 1 40 0.909 36.36

R2 =30% 2 50 0.826 41.3

3 60 0.751 45.06

4 60 0.683 40.98

5 80 0.621 49.68

TOTAL = 213.38

YEAR

PROJECT

A

PV

FACTOR

30% NPV2

1 40 0.7692 30.768

2 50 0.5917 29.585

3 60 0.4552 27.312

4 60 0.3501 21.006

5 80 0.2693 21.544

TOTAL = 130.215

5

is going to make profit or loss from the project (Heaton, Polson and Witte, 2017). it helps firm

to know which investment option will give it higher returns. From the above analysis we get IRR

Value in project A is 22.96% and 20.75% in project B. It is to suggest that project A is to be

prefer over project B because it exceeds than cost of project and gives profitable return than

project B.

(B)

INTERNAL

RATE OF

RETURN

FOR PROJECT

A:

INVESTMENT

= 150 YEAR

PROJECT

A

PV

FACTOR

10% NPV1

R1= 10% 1 40 0.909 36.36

R2 =30% 2 50 0.826 41.3

3 60 0.751 45.06

4 60 0.683 40.98

5 80 0.621 49.68

TOTAL = 213.38

YEAR

PROJECT

A

PV

FACTOR

30% NPV2

1 40 0.7692 30.768

2 50 0.5917 29.585

3 60 0.4552 27.312

4 60 0.3501 21.006

5 80 0.2693 21.544

TOTAL = 130.215

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

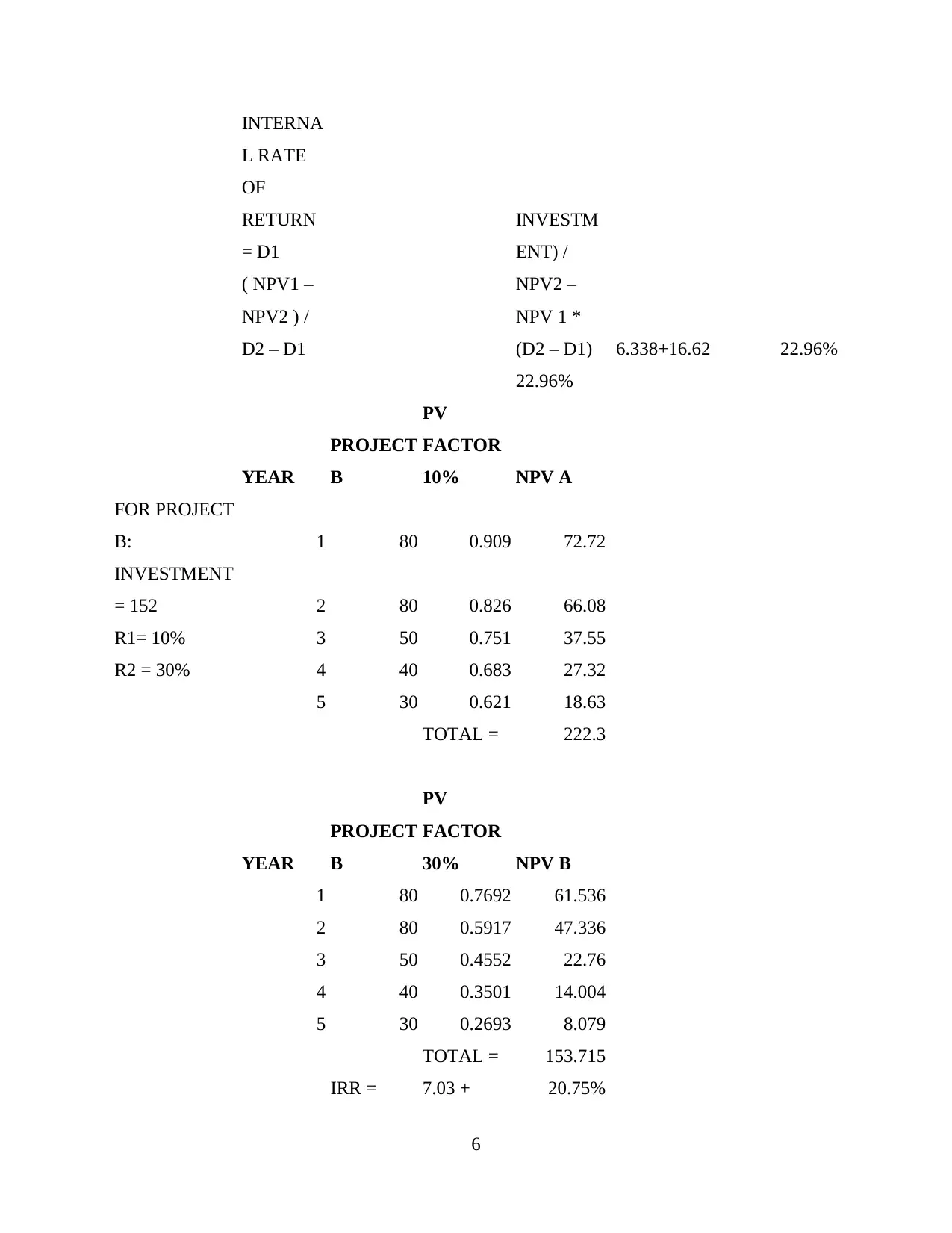

INTERNA

L RATE

OF

RETURN

= D1

( NPV1 –

NPV2 ) /

D2 – D1

INVESTM

ENT) /

NPV2 –

NPV 1 *

(D2 – D1) 6.338+16.62 22.96%

22.96%

YEAR

PROJECT

B

PV

FACTOR

10% NPV A

FOR PROJECT

B: 1 80 0.909 72.72

INVESTMENT

= 152 2 80 0.826 66.08

R1= 10% 3 50 0.751 37.55

R2 = 30% 4 40 0.683 27.32

5 30 0.621 18.63

TOTAL = 222.3

YEAR

PROJECT

B

PV

FACTOR

30% NPV B

1 80 0.7692 61.536

2 80 0.5917 47.336

3 50 0.4552 22.76

4 40 0.3501 14.004

5 30 0.2693 8.079

TOTAL = 153.715

IRR = 7.03 + 20.75%

6

L RATE

OF

RETURN

= D1

( NPV1 –

NPV2 ) /

D2 – D1

INVESTM

ENT) /

NPV2 –

NPV 1 *

(D2 – D1) 6.338+16.62 22.96%

22.96%

YEAR

PROJECT

B

PV

FACTOR

10% NPV A

FOR PROJECT

B: 1 80 0.909 72.72

INVESTMENT

= 152 2 80 0.826 66.08

R1= 10% 3 50 0.751 37.55

R2 = 30% 4 40 0.683 27.32

5 30 0.621 18.63

TOTAL = 222.3

YEAR

PROJECT

B

PV

FACTOR

30% NPV B

1 80 0.7692 61.536

2 80 0.5917 47.336

3 50 0.4552 22.76

4 40 0.3501 14.004

5 30 0.2693 8.079

TOTAL = 153.715

IRR = 7.03 + 20.75%

6

13.717

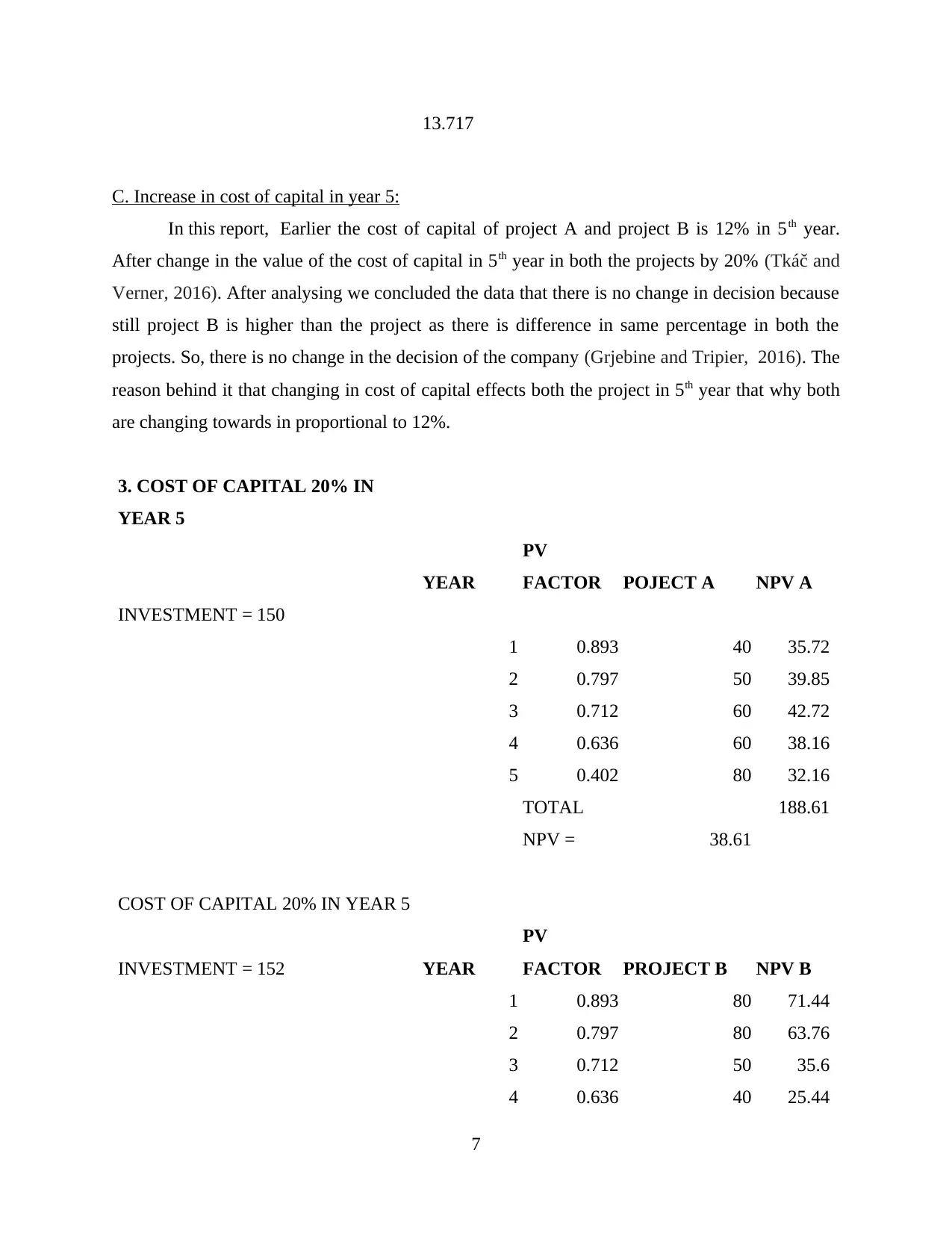

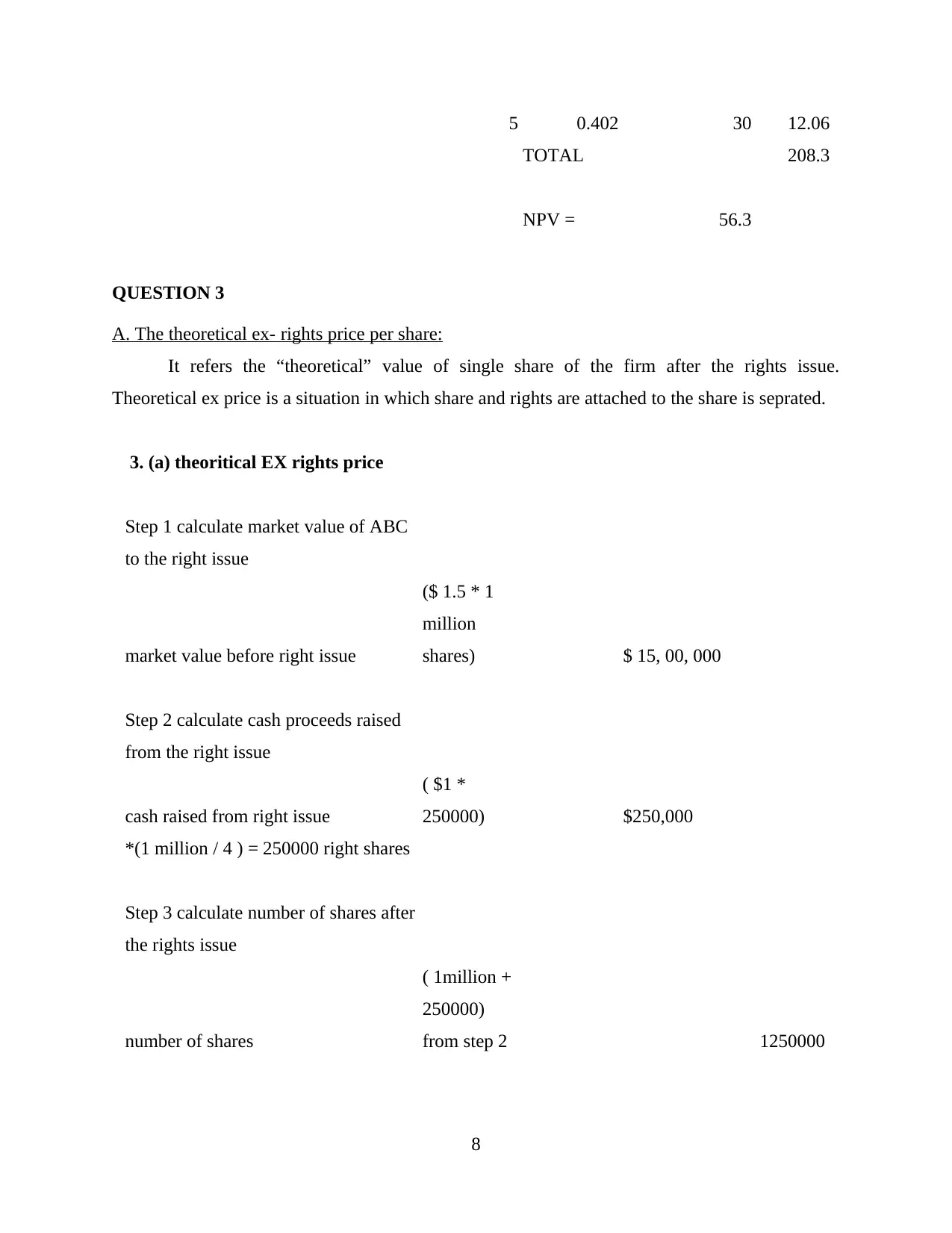

C. Increase in cost of capital in year 5:

In this report, Earlier the cost of capital of project A and project B is 12% in 5th year.

After change in the value of the cost of capital in 5th year in both the projects by 20% (Tkáč and

Verner, 2016). After analysing we concluded the data that there is no change in decision because

still project B is higher than the project as there is difference in same percentage in both the

projects. So, there is no change in the decision of the company (Grjebine and Tripier, 2016). The

reason behind it that changing in cost of capital effects both the project in 5th year that why both

are changing towards in proportional to 12%.

3. COST OF CAPITAL 20% IN

YEAR 5

YEAR

PV

FACTOR POJECT A NPV A

INVESTMENT = 150

1 0.893 40 35.72

2 0.797 50 39.85

3 0.712 60 42.72

4 0.636 60 38.16

5 0.402 80 32.16

TOTAL 188.61

NPV = 38.61

COST OF CAPITAL 20% IN YEAR 5

INVESTMENT = 152 YEAR

PV

FACTOR PROJECT B NPV B

1 0.893 80 71.44

2 0.797 80 63.76

3 0.712 50 35.6

4 0.636 40 25.44

7

C. Increase in cost of capital in year 5:

In this report, Earlier the cost of capital of project A and project B is 12% in 5th year.

After change in the value of the cost of capital in 5th year in both the projects by 20% (Tkáč and

Verner, 2016). After analysing we concluded the data that there is no change in decision because

still project B is higher than the project as there is difference in same percentage in both the

projects. So, there is no change in the decision of the company (Grjebine and Tripier, 2016). The

reason behind it that changing in cost of capital effects both the project in 5th year that why both

are changing towards in proportional to 12%.

3. COST OF CAPITAL 20% IN

YEAR 5

YEAR

PV

FACTOR POJECT A NPV A

INVESTMENT = 150

1 0.893 40 35.72

2 0.797 50 39.85

3 0.712 60 42.72

4 0.636 60 38.16

5 0.402 80 32.16

TOTAL 188.61

NPV = 38.61

COST OF CAPITAL 20% IN YEAR 5

INVESTMENT = 152 YEAR

PV

FACTOR PROJECT B NPV B

1 0.893 80 71.44

2 0.797 80 63.76

3 0.712 50 35.6

4 0.636 40 25.44

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 0.402 30 12.06

TOTAL 208.3

NPV = 56.3

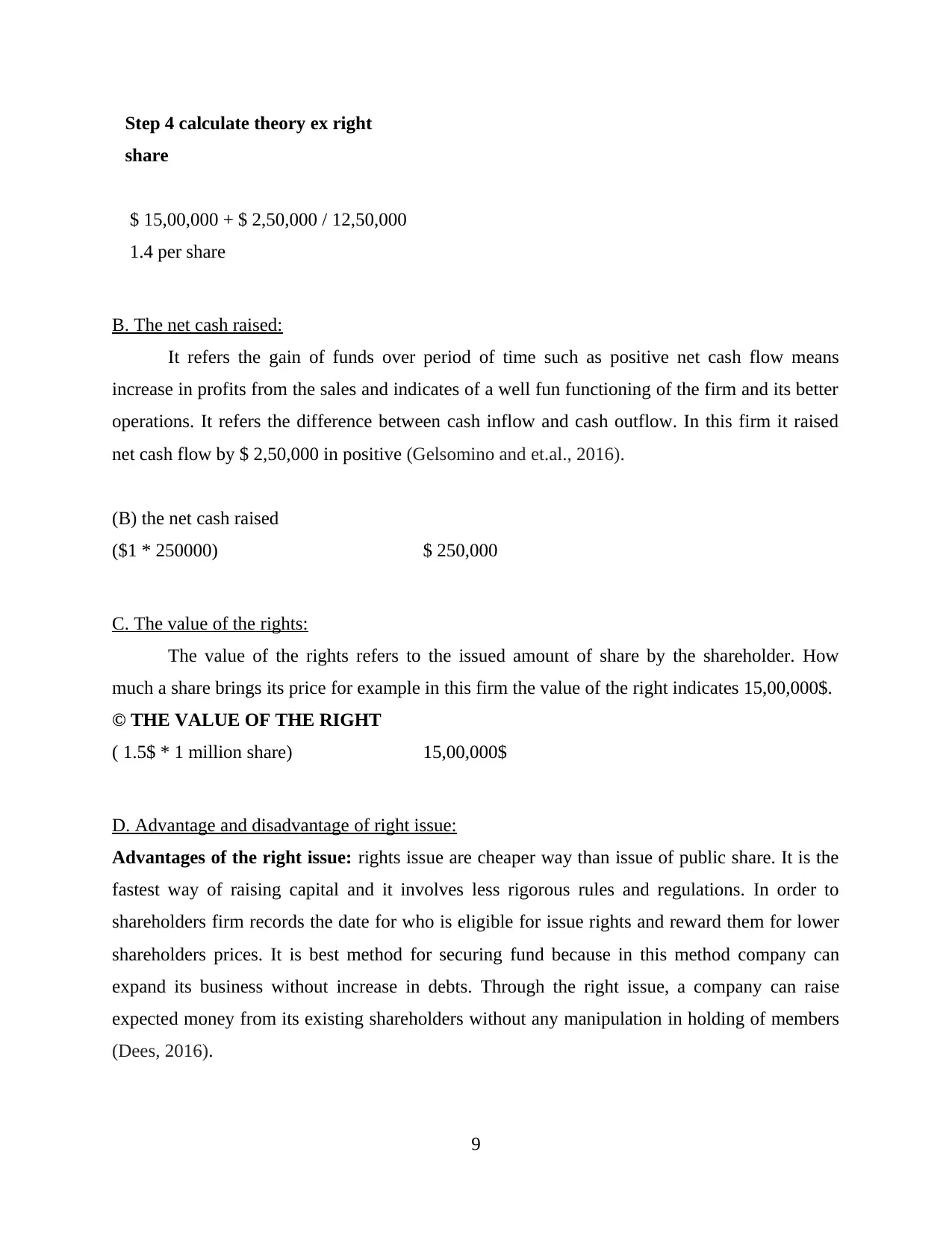

QUESTION 3

A. The theoretical ex- rights price per share:

It refers the “theoretical” value of single share of the firm after the rights issue.

Theoretical ex price is a situation in which share and rights are attached to the share is seprated.

3. (a) theoritical EX rights price

Step 1 calculate market value of ABC

to the right issue

market value before right issue

($ 1.5 * 1

million

shares) $ 15, 00, 000

Step 2 calculate cash proceeds raised

from the right issue

cash raised from right issue

( $1 *

250000) $250,000

*(1 million / 4 ) = 250000 right shares

Step 3 calculate number of shares after

the rights issue

number of shares

( 1million +

250000)

from step 2 1250000

8

TOTAL 208.3

NPV = 56.3

QUESTION 3

A. The theoretical ex- rights price per share:

It refers the “theoretical” value of single share of the firm after the rights issue.

Theoretical ex price is a situation in which share and rights are attached to the share is seprated.

3. (a) theoritical EX rights price

Step 1 calculate market value of ABC

to the right issue

market value before right issue

($ 1.5 * 1

million

shares) $ 15, 00, 000

Step 2 calculate cash proceeds raised

from the right issue

cash raised from right issue

( $1 *

250000) $250,000

*(1 million / 4 ) = 250000 right shares

Step 3 calculate number of shares after

the rights issue

number of shares

( 1million +

250000)

from step 2 1250000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step 4 calculate theory ex right

share

$ 15,00,000 + $ 2,50,000 / 12,50,000

1.4 per share

B. The net cash raised:

It refers the gain of funds over period of time such as positive net cash flow means

increase in profits from the sales and indicates of a well fun functioning of the firm and its better

operations. It refers the difference between cash inflow and cash outflow. In this firm it raised

net cash flow by $ 2,50,000 in positive (Gelsomino and et.al., 2016).

(B) the net cash raised

($1 * 250000) $ 250,000

C. The value of the rights:

The value of the rights refers to the issued amount of share by the shareholder. How

much a share brings its price for example in this firm the value of the right indicates 15,00,000$.

© THE VALUE OF THE RIGHT

( 1.5$ * 1 million share) 15,00,000$

D. Advantage and disadvantage of right issue:

Advantages of the right issue: rights issue are cheaper way than issue of public share. It is the

fastest way of raising capital and it involves less rigorous rules and regulations. In order to

shareholders firm records the date for who is eligible for issue rights and reward them for lower

shareholders prices. It is best method for securing fund because in this method company can

expand its business without increase in debts. Through the right issue, a company can raise

expected money from its existing shareholders without any manipulation in holding of members

(Dees, 2016).

9

share

$ 15,00,000 + $ 2,50,000 / 12,50,000

1.4 per share

B. The net cash raised:

It refers the gain of funds over period of time such as positive net cash flow means

increase in profits from the sales and indicates of a well fun functioning of the firm and its better

operations. It refers the difference between cash inflow and cash outflow. In this firm it raised

net cash flow by $ 2,50,000 in positive (Gelsomino and et.al., 2016).

(B) the net cash raised

($1 * 250000) $ 250,000

C. The value of the rights:

The value of the rights refers to the issued amount of share by the shareholder. How

much a share brings its price for example in this firm the value of the right indicates 15,00,000$.

© THE VALUE OF THE RIGHT

( 1.5$ * 1 million share) 15,00,000$

D. Advantage and disadvantage of right issue:

Advantages of the right issue: rights issue are cheaper way than issue of public share. It is the

fastest way of raising capital and it involves less rigorous rules and regulations. In order to

shareholders firm records the date for who is eligible for issue rights and reward them for lower

shareholders prices. It is best method for securing fund because in this method company can

expand its business without increase in debts. Through the right issue, a company can raise

expected money from its existing shareholders without any manipulation in holding of members

(Dees, 2016).

9

Disadvantages of the right issue: In this company cannot raise its amount in case of initial

public offer. Stock exchange put restrictions on that amount on which a firm raise via right issue.

The limit is generally proportional to the equity value of the firm. Issue of right shares is

indicates the liquidity crisis. If shareholders do not take up their rights, then firm's shareholders

will be diluted.

QUESTION 4

A. The company's weighted average cost of capital using market weightings:

WACC= E/E+D*R^e+D/D+E*R^d*(1-t)

return on equity =R^f+BETA*(R^m-

R^f)

R^f= risk free rate 0.05

R^f-R^m= risk premium 0.091

Beta 1.21

return on equity =R^f+BETA*(R^m-

R^f) 0.16011

equity 200

debt 650

return on debt 0.09

tax rate 0.3

WACC= E/E+D*R^e+D/D+E*R^d*(1-t) 118.6715

10

public offer. Stock exchange put restrictions on that amount on which a firm raise via right issue.

The limit is generally proportional to the equity value of the firm. Issue of right shares is

indicates the liquidity crisis. If shareholders do not take up their rights, then firm's shareholders

will be diluted.

QUESTION 4

A. The company's weighted average cost of capital using market weightings:

WACC= E/E+D*R^e+D/D+E*R^d*(1-t)

return on equity =R^f+BETA*(R^m-

R^f)

R^f= risk free rate 0.05

R^f-R^m= risk premium 0.091

Beta 1.21

return on equity =R^f+BETA*(R^m-

R^f) 0.16011

equity 200

debt 650

return on debt 0.09

tax rate 0.3

WACC= E/E+D*R^e+D/D+E*R^d*(1-t) 118.6715

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.