Finance for Business Assignment: Valuation and Financial Analysis

VerifiedAdded on 2021/04/16

|6

|847

|26

Homework Assignment

AI Summary

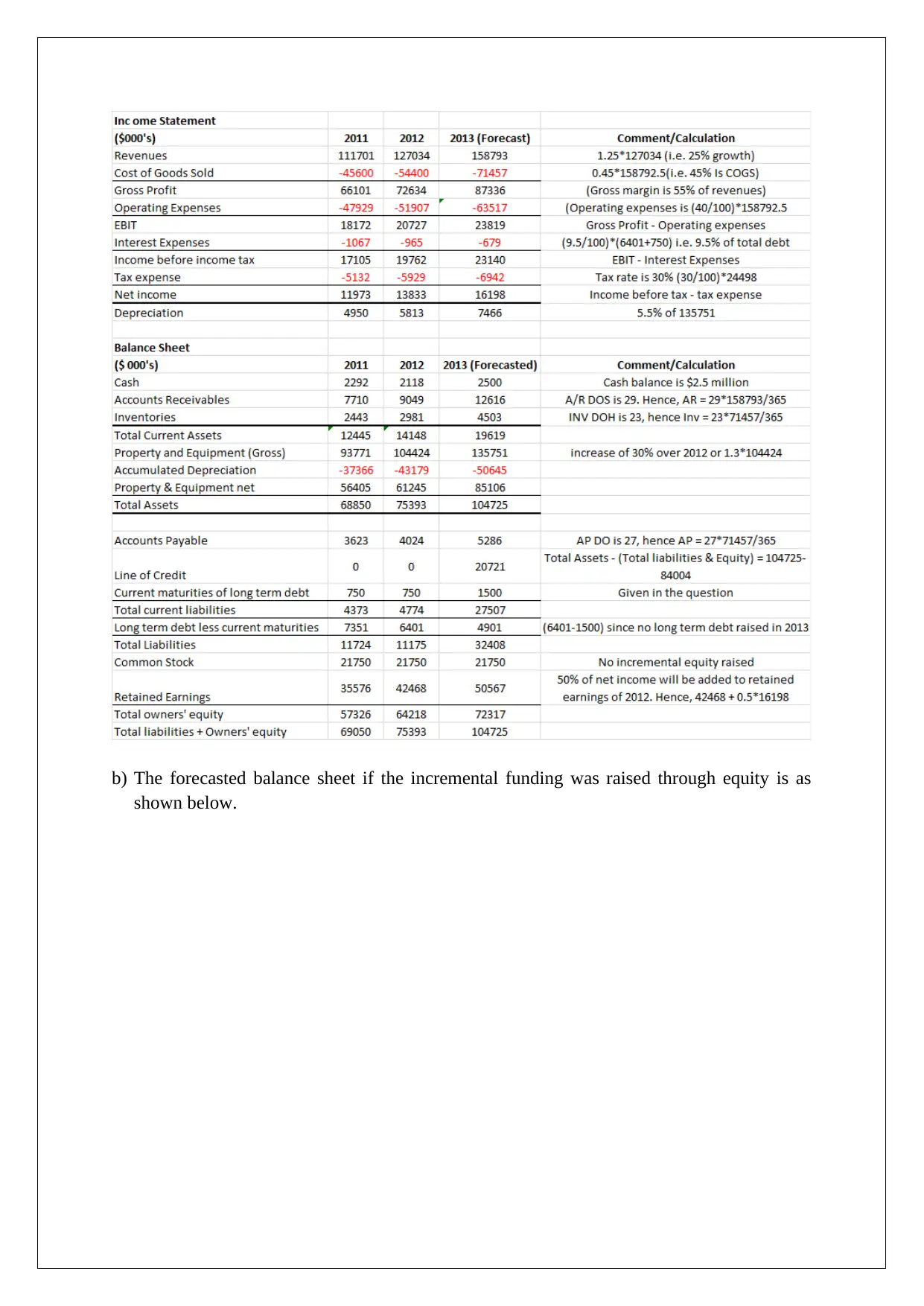

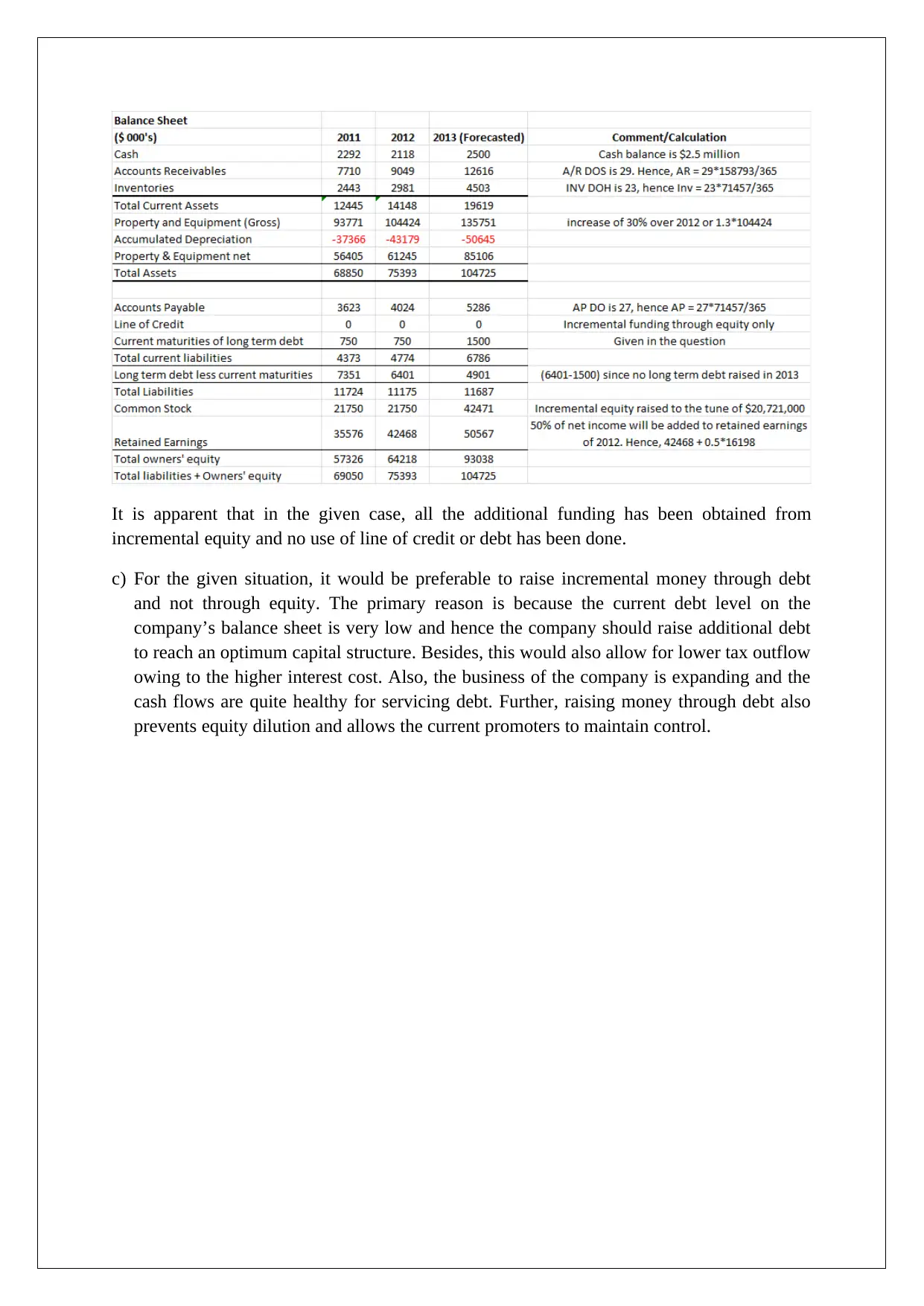

This document presents a comprehensive solution to a finance assignment, addressing key concepts such as Free Cash Flow (FCF) calculation, valuation methods, and financial analysis. The solution meticulously computes FCF for 2016 and 2017, calculates terminal value, and determines the present value of a firm. It explores various valuation multiples, including P/E, P/BV, and Market Capitalization/Revenue, to estimate the intrinsic value per share. The assignment also covers the analysis of Accounts Receivable Days Sales Outstanding (DSO), Accounts Payable Days Outstanding (AP DO), and Inventory Days on Hand (INV DOH). Furthermore, it provides a comparative analysis of debt versus equity financing options, recommending debt financing based on the company's financial position and expansion plans. The document concludes with a discussion on optimal capital structure and its implications for tax outflow and equity dilution.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.