Finance Report: Financial Analysis of Present Value, Bonds and Equity

VerifiedAdded on 2020/07/22

|9

|1112

|60

Report

AI Summary

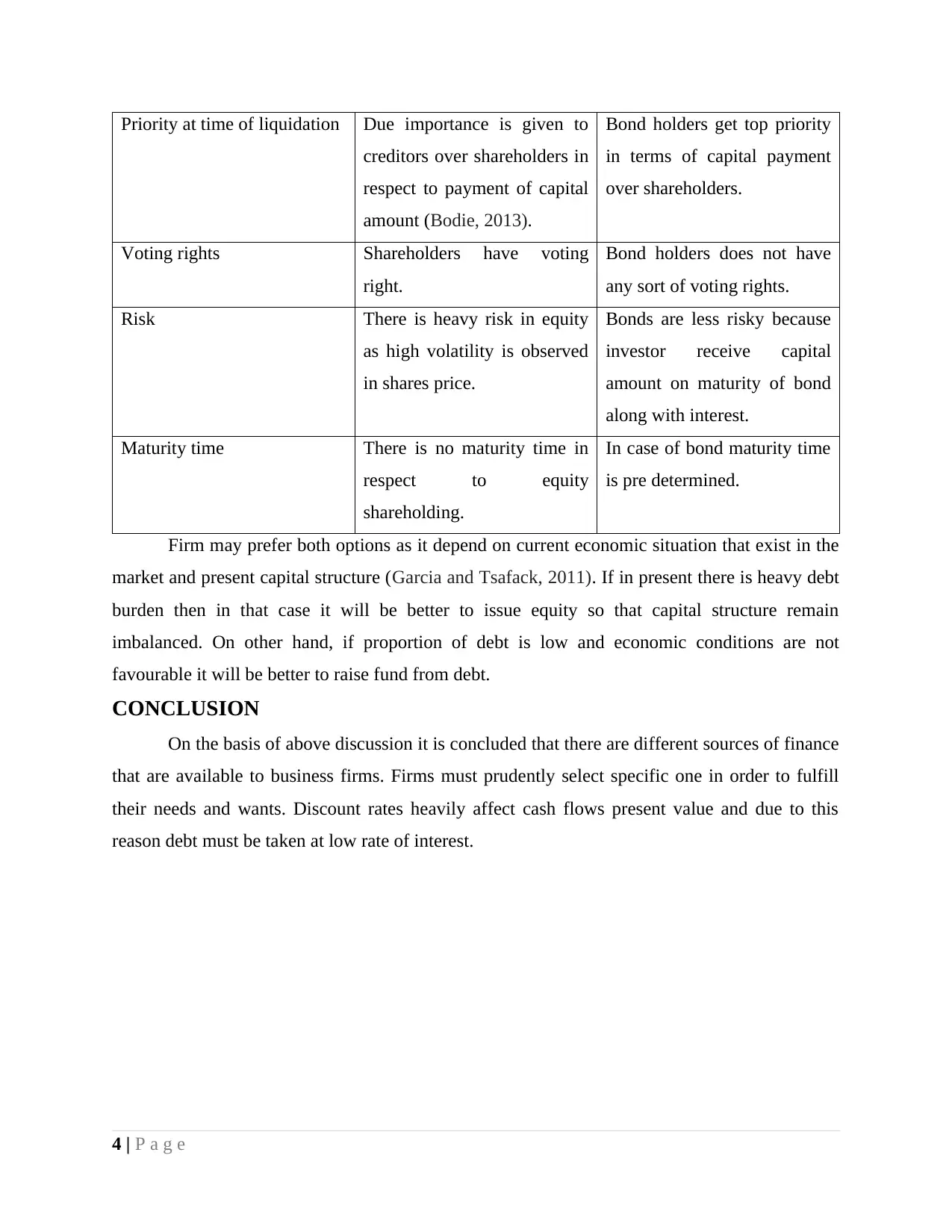

This finance report provides a comprehensive analysis of various financial concepts. It begins with the calculation of present value under different scenarios, demonstrating how discount rates impact future values. The report then delves into bond valuation, exploring the relationship between yield to maturity (YTM) and bond prices, as well as the calculation of YTM. Furthermore, the report covers equity valuation, including the determination of the required rate of return and the value of shares based on dividends and growth rates. Finally, the report compares the characteristics of bonds and equity, highlighting their differences in terms of priority during liquidation, voting rights, risk, and maturity time. The conclusion emphasizes the importance of selecting appropriate financing sources based on specific business needs and market conditions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.