Business Finance Report: MDL and Budgeting Approaches

VerifiedAdded on 2023/01/13

|15

|3665

|90

Report

AI Summary

This report provides a comprehensive analysis of business finance, covering key concepts such as profit and cash flow, working capital management, and budgeting approaches. Part 1 focuses on Mediterranean Delights Ltd (MDL), examining its profit and loss statement, balance sheet, cash flow statement, and working capital. It explains the differences between profit and cash flow, the impact of working capital adjustments, and strategies to improve cash flow through better working capital management. Part 2 shifts to budgeting, discussing traditional and alternative approaches, including zero-based budgeting, using Second Sight plc as a case study. The report highlights the purpose of budgeting, explores various budgeting methods, and provides recommendations for financial planning and cost management. The analysis includes detailed calculations, interpretations of financial statements, and practical steps to enhance financial performance and decision-making.

B07591

BUSINESS

FINANCE

BUSINESS

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report consists of two parts; in first part the report focuses on profit and loss

statement, balance sheet, cash flow statement and working capital. These concepts

have been explained with specific formula and calculations. Also the affect of working

capital adjustments on cash flow statements is discussed. In first part the case study of

Mediterranean Delights Ltd (“MDL”) is taken, it owns and operates 30 delicatessens

throughout the South of England. The core activity of this company is delivering food

items to various restaurants of South England.

This report consists of two parts; in first part the report focuses on profit and loss

statement, balance sheet, cash flow statement and working capital. These concepts

have been explained with specific formula and calculations. Also the affect of working

capital adjustments on cash flow statements is discussed. In first part the case study of

Mediterranean Delights Ltd (“MDL”) is taken, it owns and operates 30 delicatessens

throughout the South of England. The core activity of this company is delivering food

items to various restaurants of South England.

PART 1

1. Concept of Profit and Cashflow and difference between profit and cashflow:...........4

2. Concepts of working capital, receivables, inventory and payables:...........................5

3. Affect of changes in working capital on cash flows:...................................................6

4. Affect of Mediterranean Delights Ltd (“MDL”) management on its financial results:. .7

5. Steps to improve Mediterranean Delights Ltd (“MDL”) cash flow through better

working capital:..................................................................................................................9

PART 2

1. Concept of budgeting and its purpose of preparing:.................................................11

2. Application of traditional and alternative budgeting approach for planning cost of

Second sight plc:.............................................................................................................13

3. Analysis of best approach:........................................................................................14

BIBILOGRAPHY..............................................................................................................15

1. Concept of Profit and Cashflow and difference between profit and cashflow:...........4

2. Concepts of working capital, receivables, inventory and payables:...........................5

3. Affect of changes in working capital on cash flows:...................................................6

4. Affect of Mediterranean Delights Ltd (“MDL”) management on its financial results:. .7

5. Steps to improve Mediterranean Delights Ltd (“MDL”) cash flow through better

working capital:..................................................................................................................9

PART 2

1. Concept of budgeting and its purpose of preparing:.................................................11

2. Application of traditional and alternative budgeting approach for planning cost of

Second sight plc:.............................................................................................................13

3. Analysis of best approach:........................................................................................14

BIBILOGRAPHY..............................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 1

1. Concept of Profit and Cashflow and difference between profit and

cashflow:

Profit: It is the remaining amount left with the business after paying all direct and

indirect expenses such as factory overheads, direct labor, direct material, selling

and administrative expenses, fixed overheads and production overheads from

the revenue and incomes (Bendell and Doyle, 2017). To get net profit after

interest and taxes, company needs to deduct same from total profit earned by the

company during a year. It consists of all cash and non cash transactions

occurring during a year. This amount transferred to retained earnings if not

shared among shareholders.

Cashflow: As the name indicates, these statements show how cash is moving

within a business. It separates whole business transactions into three different

activities: Operating activities, Investing activities and Financing activities (Burns

and Dewhurst, 2016). The main reason behind this division is to analyze cash in

and out.

Operating activities shows cash generates or used in operations. This part

consists of net profit.

Under Investing activities; all cash transactions related to buying or selling of

fixed assets or properties considered under this portion, additional to this any

interest or dividend received from investments done in other business also

considered under this activity.

Financing Activities: This part covers only those activities which are related to

shares and equity like generating cash through issuing new shares, paying

dividends and paying long term loans.

1. Concept of Profit and Cashflow and difference between profit and

cashflow:

Profit: It is the remaining amount left with the business after paying all direct and

indirect expenses such as factory overheads, direct labor, direct material, selling

and administrative expenses, fixed overheads and production overheads from

the revenue and incomes (Bendell and Doyle, 2017). To get net profit after

interest and taxes, company needs to deduct same from total profit earned by the

company during a year. It consists of all cash and non cash transactions

occurring during a year. This amount transferred to retained earnings if not

shared among shareholders.

Cashflow: As the name indicates, these statements show how cash is moving

within a business. It separates whole business transactions into three different

activities: Operating activities, Investing activities and Financing activities (Burns

and Dewhurst, 2016). The main reason behind this division is to analyze cash in

and out.

Operating activities shows cash generates or used in operations. This part

consists of net profit.

Under Investing activities; all cash transactions related to buying or selling of

fixed assets or properties considered under this portion, additional to this any

interest or dividend received from investments done in other business also

considered under this activity.

Financing Activities: This part covers only those activities which are related to

shares and equity like generating cash through issuing new shares, paying

dividends and paying long term loans.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

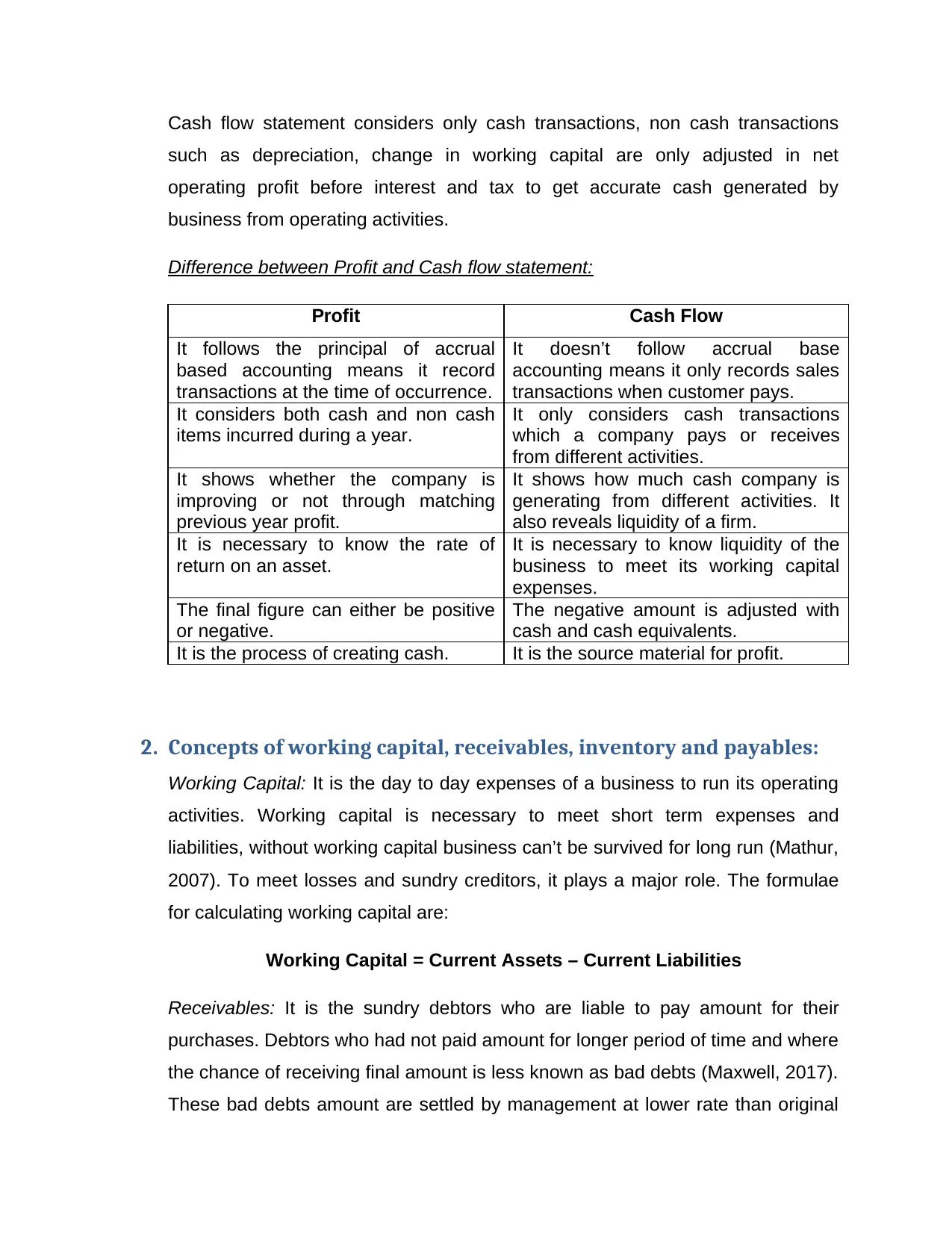

Cash flow statement considers only cash transactions, non cash transactions

such as depreciation, change in working capital are only adjusted in net

operating profit before interest and tax to get accurate cash generated by

business from operating activities.

Difference between Profit and Cash flow statement:

Profit Cash Flow

It follows the principal of accrual

based accounting means it record

transactions at the time of occurrence.

It doesn’t follow accrual base

accounting means it only records sales

transactions when customer pays.

It considers both cash and non cash

items incurred during a year.

It only considers cash transactions

which a company pays or receives

from different activities.

It shows whether the company is

improving or not through matching

previous year profit.

It shows how much cash company is

generating from different activities. It

also reveals liquidity of a firm.

It is necessary to know the rate of

return on an asset.

It is necessary to know liquidity of the

business to meet its working capital

expenses.

The final figure can either be positive

or negative.

The negative amount is adjusted with

cash and cash equivalents.

It is the process of creating cash. It is the source material for profit.

2. Concepts of working capital, receivables, inventory and payables:

Working Capital: It is the day to day expenses of a business to run its operating

activities. Working capital is necessary to meet short term expenses and

liabilities, without working capital business can’t be survived for long run (Mathur,

2007). To meet losses and sundry creditors, it plays a major role. The formulae

for calculating working capital are:

Working Capital = Current Assets – Current Liabilities

Receivables: It is the sundry debtors who are liable to pay amount for their

purchases. Debtors who had not paid amount for longer period of time and where

the chance of receiving final amount is less known as bad debts (Maxwell, 2017).

These bad debts amount are settled by management at lower rate than original

such as depreciation, change in working capital are only adjusted in net

operating profit before interest and tax to get accurate cash generated by

business from operating activities.

Difference between Profit and Cash flow statement:

Profit Cash Flow

It follows the principal of accrual

based accounting means it record

transactions at the time of occurrence.

It doesn’t follow accrual base

accounting means it only records sales

transactions when customer pays.

It considers both cash and non cash

items incurred during a year.

It only considers cash transactions

which a company pays or receives

from different activities.

It shows whether the company is

improving or not through matching

previous year profit.

It shows how much cash company is

generating from different activities. It

also reveals liquidity of a firm.

It is necessary to know the rate of

return on an asset.

It is necessary to know liquidity of the

business to meet its working capital

expenses.

The final figure can either be positive

or negative.

The negative amount is adjusted with

cash and cash equivalents.

It is the process of creating cash. It is the source material for profit.

2. Concepts of working capital, receivables, inventory and payables:

Working Capital: It is the day to day expenses of a business to run its operating

activities. Working capital is necessary to meet short term expenses and

liabilities, without working capital business can’t be survived for long run (Mathur,

2007). To meet losses and sundry creditors, it plays a major role. The formulae

for calculating working capital are:

Working Capital = Current Assets – Current Liabilities

Receivables: It is the sundry debtors who are liable to pay amount for their

purchases. Debtors who had not paid amount for longer period of time and where

the chance of receiving final amount is less known as bad debts (Maxwell, 2017).

These bad debts amount are settled by management at lower rate than original

price of the product. The period taken by debtors to pay their amount purchased

is known as average collection period.

Payables: These are the parties or suppliers from whom business has purchased

raw materials to further productions or to sale it to other. Payables also known as

sundry creditors, company is liable to pay sundry creditors for their purchases.

The period in which company pays creditors or payables is known as average

accounts payable period (Haeger, 2017). Companies try to take shorter period to

pay back its creditors to built strong goodwill in the market, so that it can buy on

credit from the market easily.

Inventory: The important basic pillar of manufacturing companies is its

inventories. Without inventory no business can do trading and earn profits. It is

also known by stock of the company (different from share stock). For proper

inventory management company adopts the EOQ (Economic order quantity)

concept to manage demands of the buyer. These days JIT (Just in time) concept

is become main objective of every company to reduce warehouse costs (Bouma,

Jeucken and Klinkers, 2017).

3. Affect of changes in working capital on cash flows:

Working capital consists indirect cash and non cash transactions so it is adjusted

in net operating profit before working capital adjustments to get pure cash

generated from operating activities. Below is the various affects of working

capital changes on cash flow:

Increase in current assets: This will decrease cash from operations, as

increase in current assets means purchasing of more inventories

(Bhattacharya, 2014). Increase in debtors has to be decrease from cash

from operations because increase in debtor’s means buyers had not paid

the amount of sales revenue and this unearned amount should be

deducted to get actual cash earned from operations.

is known as average collection period.

Payables: These are the parties or suppliers from whom business has purchased

raw materials to further productions or to sale it to other. Payables also known as

sundry creditors, company is liable to pay sundry creditors for their purchases.

The period in which company pays creditors or payables is known as average

accounts payable period (Haeger, 2017). Companies try to take shorter period to

pay back its creditors to built strong goodwill in the market, so that it can buy on

credit from the market easily.

Inventory: The important basic pillar of manufacturing companies is its

inventories. Without inventory no business can do trading and earn profits. It is

also known by stock of the company (different from share stock). For proper

inventory management company adopts the EOQ (Economic order quantity)

concept to manage demands of the buyer. These days JIT (Just in time) concept

is become main objective of every company to reduce warehouse costs (Bouma,

Jeucken and Klinkers, 2017).

3. Affect of changes in working capital on cash flows:

Working capital consists indirect cash and non cash transactions so it is adjusted

in net operating profit before working capital adjustments to get pure cash

generated from operating activities. Below is the various affects of working

capital changes on cash flow:

Increase in current assets: This will decrease cash from operations, as

increase in current assets means purchasing of more inventories

(Bhattacharya, 2014). Increase in debtors has to be decrease from cash

from operations because increase in debtor’s means buyers had not paid

the amount of sales revenue and this unearned amount should be

deducted to get actual cash earned from operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increase in current liabilities: If current liabilities have increased

comparison to previous year, then it should be added to cash from

operations because increase in liabilities indicates in cash items. Increase

in creditors has to be added back to cash from operations because

company hasn’t paid the cash for its purchases.

Decrease in current assets: It should add to cash from operations,

because decrease in inventories means selling and sale generates cash

for the business. On the other hand decrease in debtors means cash

received from debtors (Sagner, 2010).

Decrease in current liabilities: It should be deducted from cash from

operations as decrease in liabilities means paying back companies debts

which reduces cash and fund of the company.

4. Affect of Mediterranean Delights Ltd (“MDL”) management on its

financial results:

Mediterranean Delights Ltd (“MDL”) is a supplier and buyer both, so it needs

warehouse for storing its stock. Company’s management decisions have different

impacts on profit, cash flows, receivables, payables and inventories. This impact

is discussed below:

Impact on profit statement: Company has £50 million pound sales revenue but

talking about its operating profit which is only £5 million pound. This shows

company has spent 90% of its revenue on direct and indirect expenses. That’s

why its net operating income is much less as compared with sales revenue.

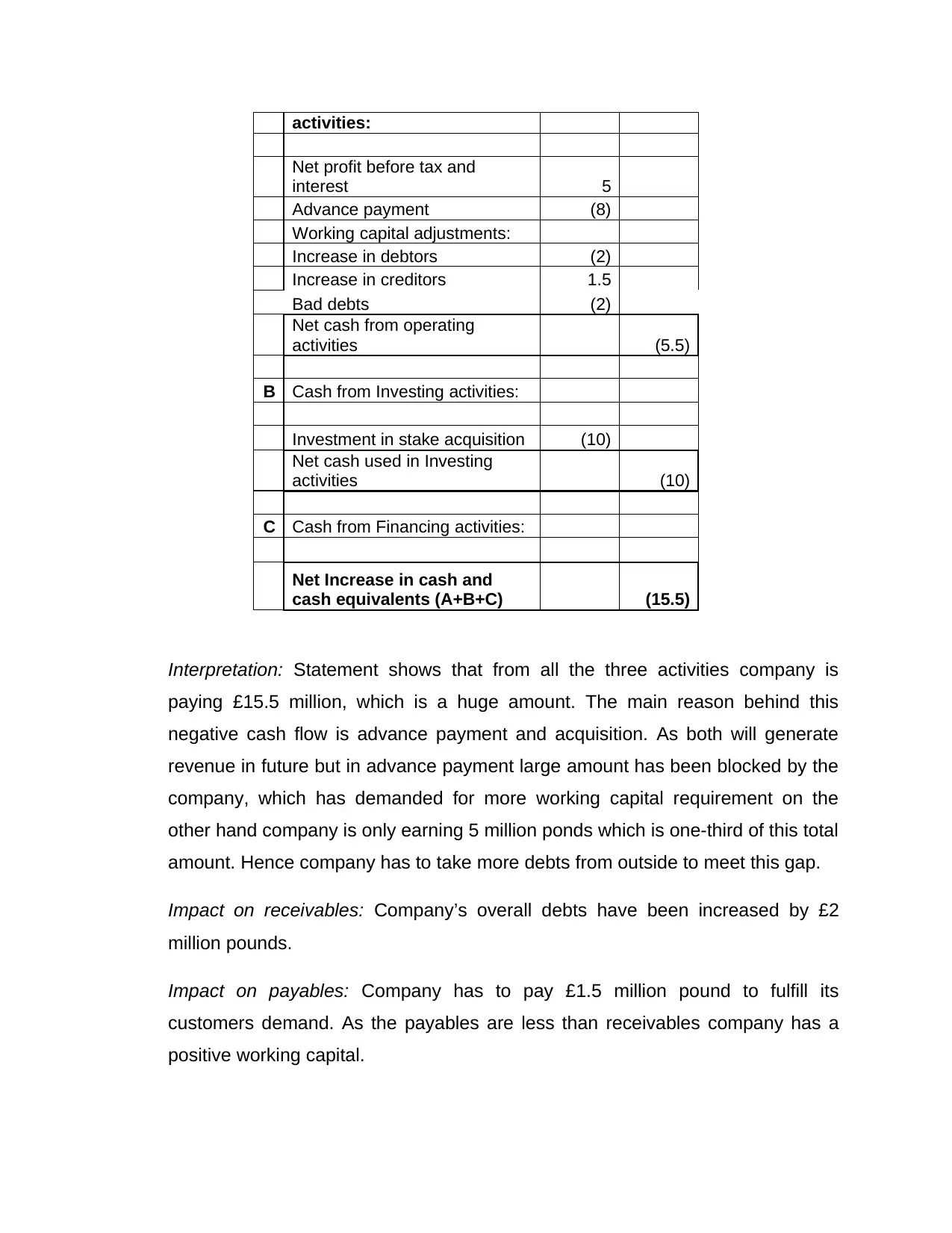

Impact on cash flow statement:

Cash flow statement at the end of the year 2017

Amoun

t (£

Million)

Amoun

t (£

Million)

A Cash from operating

comparison to previous year, then it should be added to cash from

operations because increase in liabilities indicates in cash items. Increase

in creditors has to be added back to cash from operations because

company hasn’t paid the cash for its purchases.

Decrease in current assets: It should add to cash from operations,

because decrease in inventories means selling and sale generates cash

for the business. On the other hand decrease in debtors means cash

received from debtors (Sagner, 2010).

Decrease in current liabilities: It should be deducted from cash from

operations as decrease in liabilities means paying back companies debts

which reduces cash and fund of the company.

4. Affect of Mediterranean Delights Ltd (“MDL”) management on its

financial results:

Mediterranean Delights Ltd (“MDL”) is a supplier and buyer both, so it needs

warehouse for storing its stock. Company’s management decisions have different

impacts on profit, cash flows, receivables, payables and inventories. This impact

is discussed below:

Impact on profit statement: Company has £50 million pound sales revenue but

talking about its operating profit which is only £5 million pound. This shows

company has spent 90% of its revenue on direct and indirect expenses. That’s

why its net operating income is much less as compared with sales revenue.

Impact on cash flow statement:

Cash flow statement at the end of the year 2017

Amoun

t (£

Million)

Amoun

t (£

Million)

A Cash from operating

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activities:

Net profit before tax and

interest 5

Advance payment (8)

Working capital adjustments:

Increase in debtors (2)

Increase in creditors 1.5

Bad debts (2)

Net cash from operating

activities (5.5)

B Cash from Investing activities:

Investment in stake acquisition (10)

Net cash used in Investing

activities (10)

C Cash from Financing activities:

Net Increase in cash and

cash equivalents (A+B+C) (15.5)

Interpretation: Statement shows that from all the three activities company is

paying £15.5 million, which is a huge amount. The main reason behind this

negative cash flow is advance payment and acquisition. As both will generate

revenue in future but in advance payment large amount has been blocked by the

company, which has demanded for more working capital requirement on the

other hand company is only earning 5 million ponds which is one-third of this total

amount. Hence company has to take more debts from outside to meet this gap.

Impact on receivables: Company’s overall debts have been increased by £2

million pounds.

Impact on payables: Company has to pay £1.5 million pound to fulfill its

customers demand. As the payables are less than receivables company has a

positive working capital.

Net profit before tax and

interest 5

Advance payment (8)

Working capital adjustments:

Increase in debtors (2)

Increase in creditors 1.5

Bad debts (2)

Net cash from operating

activities (5.5)

B Cash from Investing activities:

Investment in stake acquisition (10)

Net cash used in Investing

activities (10)

C Cash from Financing activities:

Net Increase in cash and

cash equivalents (A+B+C) (15.5)

Interpretation: Statement shows that from all the three activities company is

paying £15.5 million, which is a huge amount. The main reason behind this

negative cash flow is advance payment and acquisition. As both will generate

revenue in future but in advance payment large amount has been blocked by the

company, which has demanded for more working capital requirement on the

other hand company is only earning 5 million ponds which is one-third of this total

amount. Hence company has to take more debts from outside to meet this gap.

Impact on receivables: Company’s overall debts have been increased by £2

million pounds.

Impact on payables: Company has to pay £1.5 million pound to fulfill its

customers demand. As the payables are less than receivables company has a

positive working capital.

Impact on Inventories: Due to dispute between two parties, company requires to

store additional inventories which increase warehouse expenses.

5. Steps to improve Mediterranean Delights Ltd (“MDL”) cash flow

through better working capital:

Company should take various steps to improve its cash flow, these steps are

given below:

Reduce extra inventory: Company should try to reduce holding cost of

stock. Holding costs are nothing but expenditure on maintenance and

care of stock at warehouse (Michalski, 2014). It should adopt Just In

Time technique to reduce unnecessary warehouse expenses.

Reduce average collection period: Receivables requires some period

of time to pay back amount purchases, this period of time is known as

average collection period. Firm should minimize this period to get

cash on time and this cash could be used in further operations.

Increase average accounts payable period: This period is the time

taken by business to pay back its suppliers or creditors. Company

should try to hold the payment of creditors or it should be more than

average collection period. This will help company in avoid taking extra

debt from the market for the payment to its creditors.

Focus on cash sales: MDL can also improve its cash flow through

focusing more on cash sales rather than credit sales. It should adopt

some policies like cash discount, bonus goods. etc. to increase cash

sales.

EXECUTIVE SUMMARY

store additional inventories which increase warehouse expenses.

5. Steps to improve Mediterranean Delights Ltd (“MDL”) cash flow

through better working capital:

Company should take various steps to improve its cash flow, these steps are

given below:

Reduce extra inventory: Company should try to reduce holding cost of

stock. Holding costs are nothing but expenditure on maintenance and

care of stock at warehouse (Michalski, 2014). It should adopt Just In

Time technique to reduce unnecessary warehouse expenses.

Reduce average collection period: Receivables requires some period

of time to pay back amount purchases, this period of time is known as

average collection period. Firm should minimize this period to get

cash on time and this cash could be used in further operations.

Increase average accounts payable period: This period is the time

taken by business to pay back its suppliers or creditors. Company

should try to hold the payment of creditors or it should be more than

average collection period. This will help company in avoid taking extra

debt from the market for the payment to its creditors.

Focus on cash sales: MDL can also improve its cash flow through

focusing more on cash sales rather than credit sales. It should adopt

some policies like cash discount, bonus goods. etc. to increase cash

sales.

EXECUTIVE SUMMARY

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In this report part 2 is covered, this report focuses on Budgeting approaches. There are

two approaches of budget; Traditional and Alternative, where alternative budget have

different types; rolling, zero based and activity based budgeting. In this part the case

study of Second Sight Plc is taken, this is an international company which produces

prescription glasses and sunglasses for a number of leading international brands. It

wants to open a joint venture with Indian company at Chennai employing 800 staff. This

report will explain why adopting zero based budgeting is best approach for the

company.

two approaches of budget; Traditional and Alternative, where alternative budget have

different types; rolling, zero based and activity based budgeting. In this part the case

study of Second Sight Plc is taken, this is an international company which produces

prescription glasses and sunglasses for a number of leading international brands. It

wants to open a joint venture with Indian company at Chennai employing 800 staff. This

report will explain why adopting zero based budgeting is best approach for the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

1. Concept of budgeting and its purpose of preparing:

Budget: Also known as budgeting is the process of estimating, forecasting and

making advance financial reports (Balance sheet and Income statement) to get

information about how much funds is required to get desired sales revenue or

profit. Budgeting works on past data’s and information’s taken from company’s

balance sheet and trading and P&L accounts.

The main purpose behind preparing budget is to meet with future expenses

especially working capital required for expansion of business and to find sources

to meet this fund requirement (Tomkin, 2016). Budget is necessary not only at

company level but at national level also. It is the part of planning and controlling

because without planning budget cannot be formed and without controlling

budget can’t be execute, so both are required for budgeting process.

There are various approaches used for preparing budgets, these approaches are

discussed below:

a) Traditional budget approach: In this approach budget is prepared on

simple concept. For preparing budget by traditional approach, previous

year’s data or information of balance sheet and income statement is taken

as a base and the figures given in financial statement is modified by

estimating inflation rate, future consumer demand, risk if any, competition

level, etc (Wildavsky, 2017). Overall in this method, budget is made for

current year by changing in the previous year’s financial statements.

Strength Weakness

Provides benchmark to every

manager. It becomes easy for

managers to get information in

which direction they have to move.

Inefficient: Uses old tools such as

spreadsheet.

Gives opportunity to adopt

decentralization to meet set

Rigid towards change: once budget

prepared, it’s hard to modify it.

1. Concept of budgeting and its purpose of preparing:

Budget: Also known as budgeting is the process of estimating, forecasting and

making advance financial reports (Balance sheet and Income statement) to get

information about how much funds is required to get desired sales revenue or

profit. Budgeting works on past data’s and information’s taken from company’s

balance sheet and trading and P&L accounts.

The main purpose behind preparing budget is to meet with future expenses

especially working capital required for expansion of business and to find sources

to meet this fund requirement (Tomkin, 2016). Budget is necessary not only at

company level but at national level also. It is the part of planning and controlling

because without planning budget cannot be formed and without controlling

budget can’t be execute, so both are required for budgeting process.

There are various approaches used for preparing budgets, these approaches are

discussed below:

a) Traditional budget approach: In this approach budget is prepared on

simple concept. For preparing budget by traditional approach, previous

year’s data or information of balance sheet and income statement is taken

as a base and the figures given in financial statement is modified by

estimating inflation rate, future consumer demand, risk if any, competition

level, etc (Wildavsky, 2017). Overall in this method, budget is made for

current year by changing in the previous year’s financial statements.

Strength Weakness

Provides benchmark to every

manager. It becomes easy for

managers to get information in

which direction they have to move.

Inefficient: Uses old tools such as

spreadsheet.

Gives opportunity to adopt

decentralization to meet set

Rigid towards change: once budget

prepared, it’s hard to modify it.

objectives.

It is being used by managers for

long period of time; hence it is well

known to them and ease to make

budgets.

Fails to control employees working

towards target.

b) Alternative budget approach: Also known as modern budgeting method,

this approach consists of three different methods and approaches to

prepare budget. These approaches are discussed below:

Rolling budget: In this approach old budget is replaced by new

budget continuously (Drury, 2013). A new budget is prepared

before the ending of old budget; this helps management in

preparing a more than 80 percent accurate budget. It can be

treated as never ended process for a business.

Strength Weakness

Make business more

responsive towards change in

the market.

Only applicable when

circumstances and situations

are constantly changing like

boom, inflation, deflation, etc.

Due to preparing repeatedly, it

allows organization to make

budget which is near to actual.

This approach requires

professionals who charged high

amount which makes it

expensive.

Zero based budget: It is totally different approach of preparing

budget. In this method no base is taken for estimating budget, it

starts by taking all values at zero (Ward, 2012). The main aim of

this approach is to cut unnecessary expenses and costs occurring

at different level of operations. It analysis the complete

information’s about the cost before adding it to budget line.

Strength Weakness

As it take all the expenses from

scratch, it becomes easy to

focus more on how to reduce

costs (Porter and Norton,

2012).

It is time consuming process.

Best method for make or buy Not applicable to small

It is being used by managers for

long period of time; hence it is well

known to them and ease to make

budgets.

Fails to control employees working

towards target.

b) Alternative budget approach: Also known as modern budgeting method,

this approach consists of three different methods and approaches to

prepare budget. These approaches are discussed below:

Rolling budget: In this approach old budget is replaced by new

budget continuously (Drury, 2013). A new budget is prepared

before the ending of old budget; this helps management in

preparing a more than 80 percent accurate budget. It can be

treated as never ended process for a business.

Strength Weakness

Make business more

responsive towards change in

the market.

Only applicable when

circumstances and situations

are constantly changing like

boom, inflation, deflation, etc.

Due to preparing repeatedly, it

allows organization to make

budget which is near to actual.

This approach requires

professionals who charged high

amount which makes it

expensive.

Zero based budget: It is totally different approach of preparing

budget. In this method no base is taken for estimating budget, it

starts by taking all values at zero (Ward, 2012). The main aim of

this approach is to cut unnecessary expenses and costs occurring

at different level of operations. It analysis the complete

information’s about the cost before adding it to budget line.

Strength Weakness

As it take all the expenses from

scratch, it becomes easy to

focus more on how to reduce

costs (Porter and Norton,

2012).

It is time consuming process.

Best method for make or buy Not applicable to small

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.