Accounting and Finance Report: University of Derby, Accounting Module

VerifiedAdded on 2023/01/10

|10

|2560

|52

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles, addressing key aspects of financial management and control. Part 1 focuses on the preparation of profit and loss statements for different divisions, highlighting the impact of transfer pricing policies and potential profit enhancements through increased production capacity. It includes calculations related to retail sales and the implications of shifting transfer pricing from cost-plus to opportunity cost. Part 2 critically evaluates the use of capital controls in the banking industry, examining arguments for and against their implementation, particularly in the context of the 2007-2008 global financial crisis. The report explores the benefits of capital controls in maintaining economic stability and managing exchange rate volatility, while also acknowledging the potential downsides, such as market inefficiencies and difficulties in enforcement. The study draws upon the case of Iceland and the United Kingdom, to illustrate the impacts of capital controls on the banking sector and the broader economy.

Accounting and Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

PART 2............................................................................................................................................5

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

PART 2............................................................................................................................................5

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION

Accounting and finance are major aspect within business environment. Accounting relates to

systematically recording all fiscal and related events in books to assess the aggregate financial

performance. While finance is related to arranging funds and support business managers

decisions with aim to boost business performance. Organisation should control overall tasks of

accounting and finance which enable managers to achieve organisational goals and tasks

(Loughran and McDonald, 2016). The study report covers preparation of systematic profit and

losses statements which shows profit of each division, separating external sales and inter-

divisional transfers. Further it covers evaluation of case study related to regulations emphasized

on controlling of systemic risks by capital controls.

PART 1

(a). Three-page PowerPoint presentation:

Covered in PPT:(b). Report:

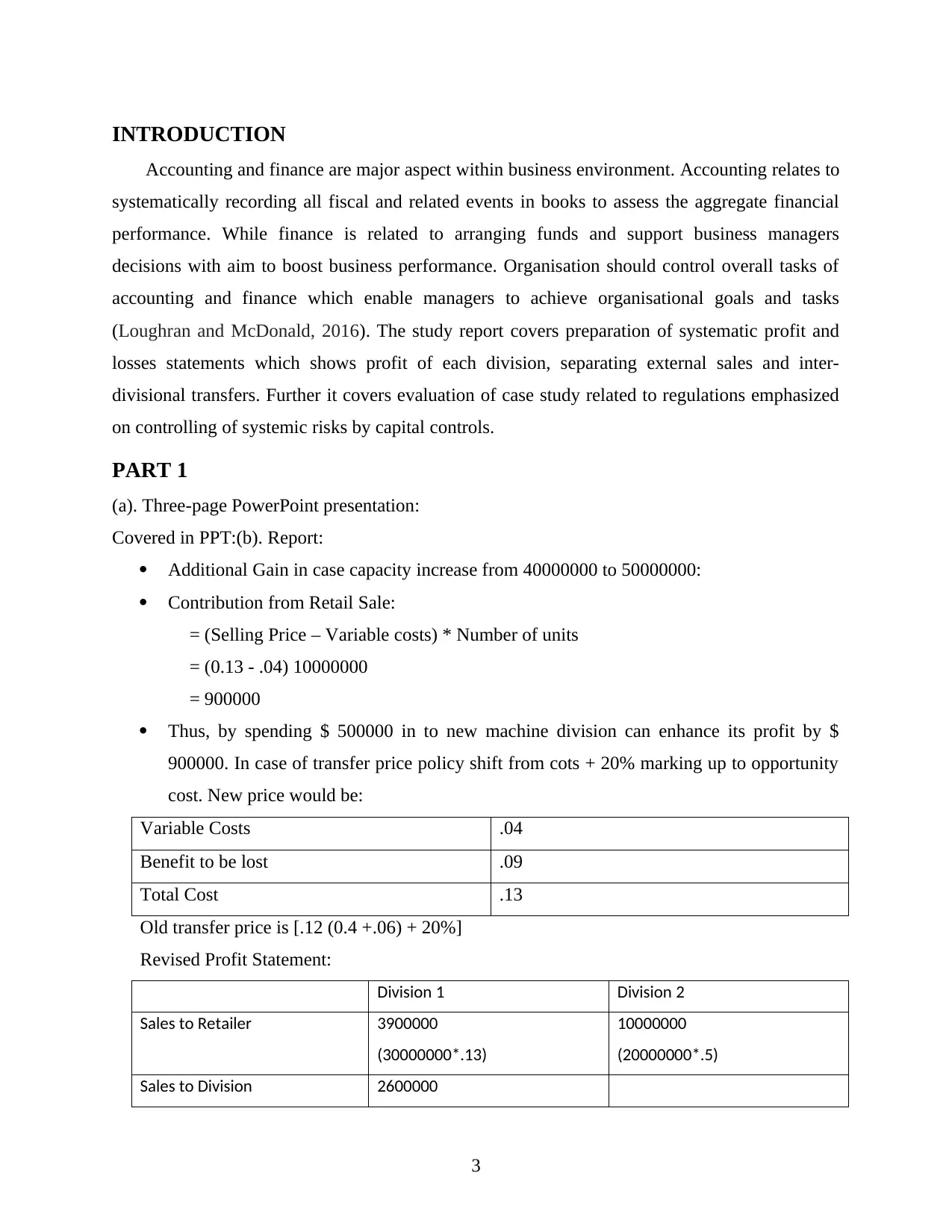

Additional Gain in case capacity increase from 40000000 to 50000000:

Contribution from Retail Sale:

= (Selling Price – Variable costs) * Number of units

= (0.13 - .04) 10000000

= 900000

Thus, by spending $ 500000 in to new machine division can enhance its profit by $

900000. In case of transfer price policy shift from cots + 20% marking up to opportunity

cost. New price would be:

Variable Costs .04

Benefit to be lost .09

Total Cost .13

Old transfer price is [.12 (0.4 +.06) + 20%]

Revised Profit Statement:

Division 1 Division 2

Sales to Retailer 3900000

(30000000*.13)

10000000

(20000000*.5)

Sales to Division 2600000

3

Accounting and finance are major aspect within business environment. Accounting relates to

systematically recording all fiscal and related events in books to assess the aggregate financial

performance. While finance is related to arranging funds and support business managers

decisions with aim to boost business performance. Organisation should control overall tasks of

accounting and finance which enable managers to achieve organisational goals and tasks

(Loughran and McDonald, 2016). The study report covers preparation of systematic profit and

losses statements which shows profit of each division, separating external sales and inter-

divisional transfers. Further it covers evaluation of case study related to regulations emphasized

on controlling of systemic risks by capital controls.

PART 1

(a). Three-page PowerPoint presentation:

Covered in PPT:(b). Report:

Additional Gain in case capacity increase from 40000000 to 50000000:

Contribution from Retail Sale:

= (Selling Price – Variable costs) * Number of units

= (0.13 - .04) 10000000

= 900000

Thus, by spending $ 500000 in to new machine division can enhance its profit by $

900000. In case of transfer price policy shift from cots + 20% marking up to opportunity

cost. New price would be:

Variable Costs .04

Benefit to be lost .09

Total Cost .13

Old transfer price is [.12 (0.4 +.06) + 20%]

Revised Profit Statement:

Division 1 Division 2

Sales to Retailer 3900000

(30000000*.13)

10000000

(20000000*.5)

Sales to Division 2600000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

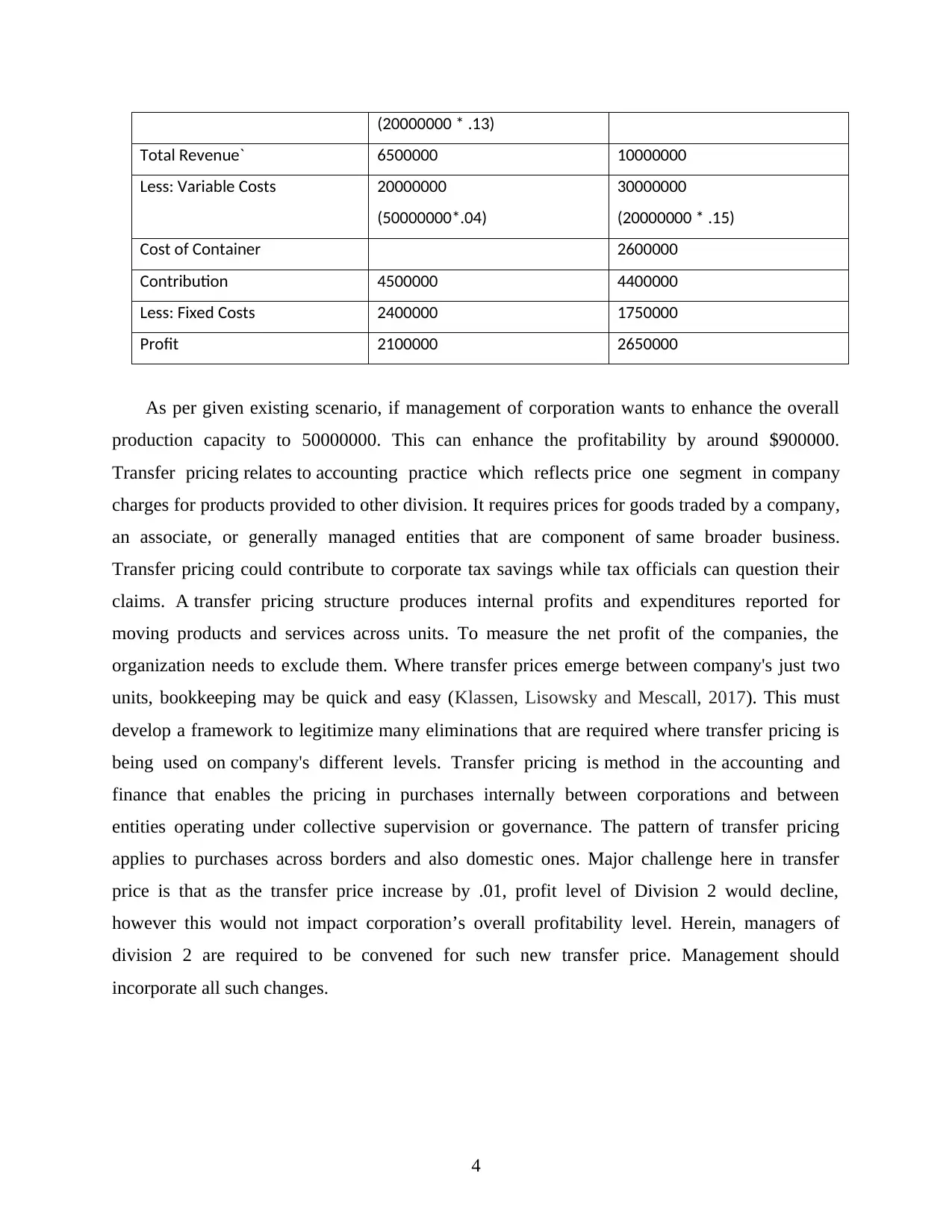

(20000000 * .13)

Total Revenue` 6500000 10000000

Less: Variable Costs 20000000

(50000000*.04)

30000000

(20000000 * .15)

Cost of Container 2600000

Contribution 4500000 4400000

Less: Fixed Costs 2400000 1750000

Profit 2100000 2650000

As per given existing scenario, if management of corporation wants to enhance the overall

production capacity to 50000000. This can enhance the profitability by around $900000.

Transfer pricing relates to accounting practice which reflects price one segment in company

charges for products provided to other division. It requires prices for goods traded by a company,

an associate, or generally managed entities that are component of same broader business.

Transfer pricing could contribute to corporate tax savings while tax officials can question their

claims. A transfer pricing structure produces internal profits and expenditures reported for

moving products and services across units. To measure the net profit of the companies, the

organization needs to exclude them. Where transfer prices emerge between company's just two

units, bookkeeping may be quick and easy (Klassen, Lisowsky and Mescall, 2017). This must

develop a framework to legitimize many eliminations that are required where transfer pricing is

being used on company's different levels. Transfer pricing is method in the accounting and

finance that enables the pricing in purchases internally between corporations and between

entities operating under collective supervision or governance. The pattern of transfer pricing

applies to purchases across borders and also domestic ones. Major challenge here in transfer

price is that as the transfer price increase by .01, profit level of Division 2 would decline,

however this would not impact corporation’s overall profitability level. Herein, managers of

division 2 are required to be convened for such new transfer price. Management should

incorporate all such changes.

4

Total Revenue` 6500000 10000000

Less: Variable Costs 20000000

(50000000*.04)

30000000

(20000000 * .15)

Cost of Container 2600000

Contribution 4500000 4400000

Less: Fixed Costs 2400000 1750000

Profit 2100000 2650000

As per given existing scenario, if management of corporation wants to enhance the overall

production capacity to 50000000. This can enhance the profitability by around $900000.

Transfer pricing relates to accounting practice which reflects price one segment in company

charges for products provided to other division. It requires prices for goods traded by a company,

an associate, or generally managed entities that are component of same broader business.

Transfer pricing could contribute to corporate tax savings while tax officials can question their

claims. A transfer pricing structure produces internal profits and expenditures reported for

moving products and services across units. To measure the net profit of the companies, the

organization needs to exclude them. Where transfer prices emerge between company's just two

units, bookkeeping may be quick and easy (Klassen, Lisowsky and Mescall, 2017). This must

develop a framework to legitimize many eliminations that are required where transfer pricing is

being used on company's different levels. Transfer pricing is method in the accounting and

finance that enables the pricing in purchases internally between corporations and between

entities operating under collective supervision or governance. The pattern of transfer pricing

applies to purchases across borders and also domestic ones. Major challenge here in transfer

price is that as the transfer price increase by .01, profit level of Division 2 would decline,

however this would not impact corporation’s overall profitability level. Herein, managers of

division 2 are required to be convened for such new transfer price. Management should

incorporate all such changes.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

Critically evaluate the case for and against the use of capital controls in the banking industry.

Overview- The given case is based on global financial crisis 2007 in which banking sector

focused on controlling risk by managing their capital. As a result, most of banks focused on not

to provide loan to needed firms because it was risky for them.

Capital control- Capital controls are residence permit-based measures, such as structure of

capital, other boundaries or absolute restrictions that the government of a country may use to

restrict flows from financial system to and from the money supply of a region. Such

interventions can be fiscal, sector-specific (generally the banking sector) or industry-specific

(e.g. "strategic" businesses). These can refer to both flows, or they may distinguish by form or

length of stream (debt, stock, direct investment; short-term vs. moderate-and long-term). Forms

of capital control include export taxes that help stop or restrict the buying and selling of a

floating currency at a market price, brackets mostly on quantity permitted for global buying or

selling of a range of payment assets, payment taxes such as the suggested Tobin tax on money

transfers, minimum service needs, compulsory get a, or even limits on the number of capital

control. There have been many differences in perception as to how capital controls are effective

and in what conditions they can be included (Siddiqui and Armstrong, 2018). In the 2008 global

financial crisis, Iceland (which is a part of a European Free Trade Region but not of the euro

zone) introduced banking regulations owing to the breakdown of its banking industry. Iceland

national government said in June 2015 that it scheduled to lift them – but, given that the

introduced legislation should include a tax on investment withdrawal from the nation, it is likely

that they still actually constitutes capital controls. The Icelandic government has declared that its

capital controls had been removed on 12 March 2017. The University of California analyst Jón

Steinsson said in 2017 that they initially supported the implementation of banking regulations in

Iceland before the recession, but that his observation in Iceland initially made him change his

views: "The country had to manage very significant deficits. The application of banking

regulations locked up a significant amount of international capital in the region. During financial

crisis 2007, most of the banks in the United Kingdom focused on applying this policy of capital

control that is as follows:

Importance of capital control for banking industry-

5

Critically evaluate the case for and against the use of capital controls in the banking industry.

Overview- The given case is based on global financial crisis 2007 in which banking sector

focused on controlling risk by managing their capital. As a result, most of banks focused on not

to provide loan to needed firms because it was risky for them.

Capital control- Capital controls are residence permit-based measures, such as structure of

capital, other boundaries or absolute restrictions that the government of a country may use to

restrict flows from financial system to and from the money supply of a region. Such

interventions can be fiscal, sector-specific (generally the banking sector) or industry-specific

(e.g. "strategic" businesses). These can refer to both flows, or they may distinguish by form or

length of stream (debt, stock, direct investment; short-term vs. moderate-and long-term). Forms

of capital control include export taxes that help stop or restrict the buying and selling of a

floating currency at a market price, brackets mostly on quantity permitted for global buying or

selling of a range of payment assets, payment taxes such as the suggested Tobin tax on money

transfers, minimum service needs, compulsory get a, or even limits on the number of capital

control. There have been many differences in perception as to how capital controls are effective

and in what conditions they can be included (Siddiqui and Armstrong, 2018). In the 2008 global

financial crisis, Iceland (which is a part of a European Free Trade Region but not of the euro

zone) introduced banking regulations owing to the breakdown of its banking industry. Iceland

national government said in June 2015 that it scheduled to lift them – but, given that the

introduced legislation should include a tax on investment withdrawal from the nation, it is likely

that they still actually constitutes capital controls. The Icelandic government has declared that its

capital controls had been removed on 12 March 2017. The University of California analyst Jón

Steinsson said in 2017 that they initially supported the implementation of banking regulations in

Iceland before the recession, but that his observation in Iceland initially made him change his

views: "The country had to manage very significant deficits. The application of banking

regulations locked up a significant amount of international capital in the region. During financial

crisis 2007, most of the banks in the United Kingdom focused on applying this policy of capital

control that is as follows:

Importance of capital control for banking industry-

5

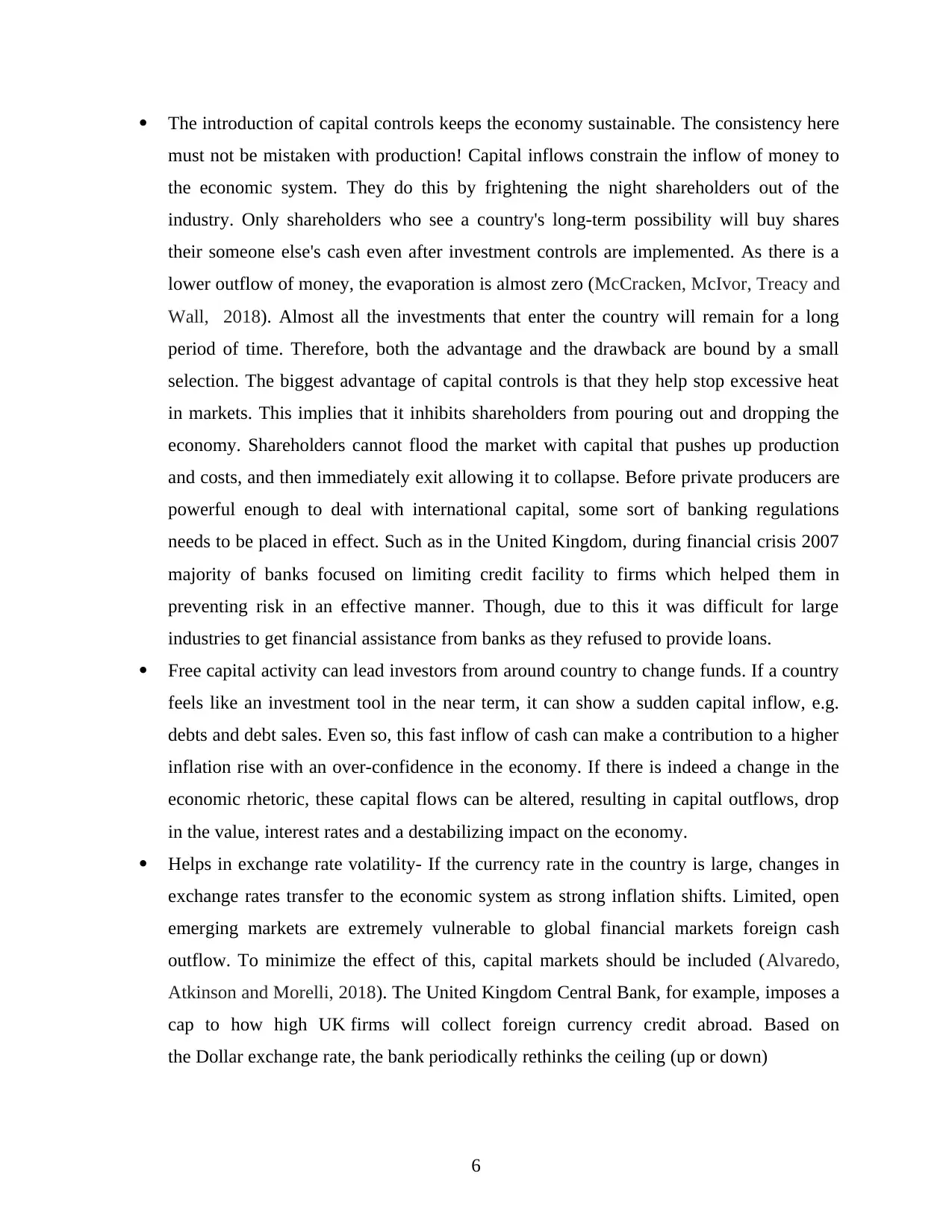

The introduction of capital controls keeps the economy sustainable. The consistency here

must not be mistaken with production! Capital inflows constrain the inflow of money to

the economic system. They do this by frightening the night shareholders out of the

industry. Only shareholders who see a country's long-term possibility will buy shares

their someone else's cash even after investment controls are implemented. As there is a

lower outflow of money, the evaporation is almost zero (McCracken, McIvor, Treacy and

Wall, 2018). Almost all the investments that enter the country will remain for a long

period of time. Therefore, both the advantage and the drawback are bound by a small

selection. The biggest advantage of capital controls is that they help stop excessive heat

in markets. This implies that it inhibits shareholders from pouring out and dropping the

economy. Shareholders cannot flood the market with capital that pushes up production

and costs, and then immediately exit allowing it to collapse. Before private producers are

powerful enough to deal with international capital, some sort of banking regulations

needs to be placed in effect. Such as in the United Kingdom, during financial crisis 2007

majority of banks focused on limiting credit facility to firms which helped them in

preventing risk in an effective manner. Though, due to this it was difficult for large

industries to get financial assistance from banks as they refused to provide loans.

Free capital activity can lead investors from around country to change funds. If a country

feels like an investment tool in the near term, it can show a sudden capital inflow, e.g.

debts and debt sales. Even so, this fast inflow of cash can make a contribution to a higher

inflation rise with an over-confidence in the economy. If there is indeed a change in the

economic rhetoric, these capital flows can be altered, resulting in capital outflows, drop

in the value, interest rates and a destabilizing impact on the economy.

Helps in exchange rate volatility- If the currency rate in the country is large, changes in

exchange rates transfer to the economic system as strong inflation shifts. Limited, open

emerging markets are extremely vulnerable to global financial markets foreign cash

outflow. To minimize the effect of this, capital markets should be included (Alvaredo,

Atkinson and Morelli, 2018). The United Kingdom Central Bank, for example, imposes a

cap to how high UK firms will collect foreign currency credit abroad. Based on

the Dollar exchange rate, the bank periodically rethinks the ceiling (up or down)

6

must not be mistaken with production! Capital inflows constrain the inflow of money to

the economic system. They do this by frightening the night shareholders out of the

industry. Only shareholders who see a country's long-term possibility will buy shares

their someone else's cash even after investment controls are implemented. As there is a

lower outflow of money, the evaporation is almost zero (McCracken, McIvor, Treacy and

Wall, 2018). Almost all the investments that enter the country will remain for a long

period of time. Therefore, both the advantage and the drawback are bound by a small

selection. The biggest advantage of capital controls is that they help stop excessive heat

in markets. This implies that it inhibits shareholders from pouring out and dropping the

economy. Shareholders cannot flood the market with capital that pushes up production

and costs, and then immediately exit allowing it to collapse. Before private producers are

powerful enough to deal with international capital, some sort of banking regulations

needs to be placed in effect. Such as in the United Kingdom, during financial crisis 2007

majority of banks focused on limiting credit facility to firms which helped them in

preventing risk in an effective manner. Though, due to this it was difficult for large

industries to get financial assistance from banks as they refused to provide loans.

Free capital activity can lead investors from around country to change funds. If a country

feels like an investment tool in the near term, it can show a sudden capital inflow, e.g.

debts and debt sales. Even so, this fast inflow of cash can make a contribution to a higher

inflation rise with an over-confidence in the economy. If there is indeed a change in the

economic rhetoric, these capital flows can be altered, resulting in capital outflows, drop

in the value, interest rates and a destabilizing impact on the economy.

Helps in exchange rate volatility- If the currency rate in the country is large, changes in

exchange rates transfer to the economic system as strong inflation shifts. Limited, open

emerging markets are extremely vulnerable to global financial markets foreign cash

outflow. To minimize the effect of this, capital markets should be included (Alvaredo,

Atkinson and Morelli, 2018). The United Kingdom Central Bank, for example, imposes a

cap to how high UK firms will collect foreign currency credit abroad. Based on

the Dollar exchange rate, the bank periodically rethinks the ceiling (up or down)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Downside of capital control for banking sector-

There are also many statisticians who oppose banking regulations. This is because they think this

is against the ability to function of a market economy. Something that is contradictory to the

workings of a free market system cannot be maintained for a long time. As a consequence,

capital controls lead to large-scale avoidance and bribery. Firms that would like to start taking

their money overseas do so by the certain means whatsoever. There are unlawful outlets here.

They are most sometimes assisted by officials who support them design the correct product

invoice or the right accounting entry that will escape the strong reach of the legislation. Capital

control did turn out to be an inefficient, long and laborious exercise, often driven by political

reasons rather than sensible financial ones. As in the above case, banks focused on reducing limit

of credit to large business entities. Due to which various kinds of obstacles had been occurred

(Bennister, Worthy and Hart, 2017). This is so because large companies were unable to get

financial assistance from banks and investment ruined. Along with, not only banking sector in

the UK but also some other sectors also focused on capital control which leads to lower growth

of GDP rate in the United Kingdom.

The problem with banking regulations is that economies are able to find ways to deal

with them. Investors are able to side up conventional laws with new internet payments

systems, for example. Such as in the United Kingdom, their banks can face the issue of

regulation of different kinds of aspects regards to capital control.

Free capital movement that contribute in developing countries to large foreign

investments that enable them to achieve a high economic growth rate and to "move

ahead" with the industrialized world. It is argued that higher constraints slow it down this

reach parity rate.

Free markets believe that the stream of wealth where it is most financially viable and

effective is prevented through banking regulations. The effect is a lower rate of capital

gain for domestic companies and a reduced number of profits.

Difficult to enforce- A considerable amount of money and time is used by the control

board to enforce and tune these but even then "leaks" are not easily prevented (Kim and

Kim, 2016). Such as in the United Kingdom, this can be difficult for banks to implement

capital control for various kinds of aspects.

7

There are also many statisticians who oppose banking regulations. This is because they think this

is against the ability to function of a market economy. Something that is contradictory to the

workings of a free market system cannot be maintained for a long time. As a consequence,

capital controls lead to large-scale avoidance and bribery. Firms that would like to start taking

their money overseas do so by the certain means whatsoever. There are unlawful outlets here.

They are most sometimes assisted by officials who support them design the correct product

invoice or the right accounting entry that will escape the strong reach of the legislation. Capital

control did turn out to be an inefficient, long and laborious exercise, often driven by political

reasons rather than sensible financial ones. As in the above case, banks focused on reducing limit

of credit to large business entities. Due to which various kinds of obstacles had been occurred

(Bennister, Worthy and Hart, 2017). This is so because large companies were unable to get

financial assistance from banks and investment ruined. Along with, not only banking sector in

the UK but also some other sectors also focused on capital control which leads to lower growth

of GDP rate in the United Kingdom.

The problem with banking regulations is that economies are able to find ways to deal

with them. Investors are able to side up conventional laws with new internet payments

systems, for example. Such as in the United Kingdom, their banks can face the issue of

regulation of different kinds of aspects regards to capital control.

Free capital movement that contribute in developing countries to large foreign

investments that enable them to achieve a high economic growth rate and to "move

ahead" with the industrialized world. It is argued that higher constraints slow it down this

reach parity rate.

Free markets believe that the stream of wealth where it is most financially viable and

effective is prevented through banking regulations. The effect is a lower rate of capital

gain for domestic companies and a reduced number of profits.

Difficult to enforce- A considerable amount of money and time is used by the control

board to enforce and tune these but even then "leaks" are not easily prevented (Kim and

Kim, 2016). Such as in the United Kingdom, this can be difficult for banks to implement

capital control for various kinds of aspects.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Throughout the midst of capital controls policymakers will follow extremely unwise

fiscal plans without caring about investor response for quite a while. Central banks can

follow inflationary policies, state can run rising, long term government spending and

compel domestic entities to purchase government is given etc. Private producers and

firms couldn't do much about this. In the context of United Kingdom, during financial

crisis, this might be difficult for banks to norm the policies of central banks. This is so

because central banks enforce to provide huge amount of financial assistance but due to

capital control they refused this policy that created various kinds of issues.

Bad for domestic investors and firms- In the lack of banking regulations, private

producers can broaden their investments, participate in foreign markets and (in theory)

earn better risk-adjusted returns. Firms may benefit from lower funding costs on foreign

markets. This is so because in the UK, during financial crisis it was tough for different

investors and firms to have proper financial assistance due to capital control.

8

fiscal plans without caring about investor response for quite a while. Central banks can

follow inflationary policies, state can run rising, long term government spending and

compel domestic entities to purchase government is given etc. Private producers and

firms couldn't do much about this. In the context of United Kingdom, during financial

crisis, this might be difficult for banks to norm the policies of central banks. This is so

because central banks enforce to provide huge amount of financial assistance but due to

capital control they refused this policy that created various kinds of issues.

Bad for domestic investors and firms- In the lack of banking regulations, private

producers can broaden their investments, participate in foreign markets and (in theory)

earn better risk-adjusted returns. Firms may benefit from lower funding costs on foreign

markets. This is so because in the UK, during financial crisis it was tough for different

investors and firms to have proper financial assistance due to capital control.

8

CONCLUSION

From above study report it has been articulated that finance and accounting interrelated and

interdependent tasks which require detailed information about business. These both aspects assist

managing officials to take relevant business decisions and identify potential risks to business.

Managers are key personnel who handles finance related tasks while accounting personnel are

responsible for all the accounting tasks like recording, summarising and reporting financial

information to stakeholders.

9

From above study report it has been articulated that finance and accounting interrelated and

interdependent tasks which require detailed information about business. These both aspects assist

managing officials to take relevant business decisions and identify potential risks to business.

Managers are key personnel who handles finance related tasks while accounting personnel are

responsible for all the accounting tasks like recording, summarising and reporting financial

information to stakeholders.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2017. Transfer pricing: Strategies, practices, and tax

minimization. Contemporary Accounting Research, 34(1), pp.455-493.

Siddiqui, K. and Armstrong, P., 2018. Capital control reconsidered: financialisation and

economic policy. International Review of Applied Economics, 32(6), pp.713-731.

McCracken, M., McIvor, R., Treacy, R. and Wall, T., 2018, March. A study of human capital

reporting in the United Kingdom. In Accounting Forum (Vol. 42, No. 1, pp. 130-141).

Taylor & Francis.

Alvaredo, F., Atkinson, A.B. and Morelli, S., 2018. Top wealth shares in the UK over more than

a century. Journal of Public Economics, 162, pp.26-47.

Bennister, M., Worthy, B. and Hart, P.T. eds., 2017. The leadership capital index: a new

perspective on political leadership. Oxford University Press.

Kim, B.U., Kim, O., Kim, H.C. and Kim, S., 2016. Influence of fossil-fuel power plant emissions

on the surface fine particulate matter in the Seoul Capital Area, South Korea. Journal of

the Air & Waste Management Association, 66(9), pp.863-873.

10

Books and Journals:

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2017. Transfer pricing: Strategies, practices, and tax

minimization. Contemporary Accounting Research, 34(1), pp.455-493.

Siddiqui, K. and Armstrong, P., 2018. Capital control reconsidered: financialisation and

economic policy. International Review of Applied Economics, 32(6), pp.713-731.

McCracken, M., McIvor, R., Treacy, R. and Wall, T., 2018, March. A study of human capital

reporting in the United Kingdom. In Accounting Forum (Vol. 42, No. 1, pp. 130-141).

Taylor & Francis.

Alvaredo, F., Atkinson, A.B. and Morelli, S., 2018. Top wealth shares in the UK over more than

a century. Journal of Public Economics, 162, pp.26-47.

Bennister, M., Worthy, B. and Hart, P.T. eds., 2017. The leadership capital index: a new

perspective on political leadership. Oxford University Press.

Kim, B.U., Kim, O., Kim, H.C. and Kim, S., 2016. Influence of fossil-fuel power plant emissions

on the surface fine particulate matter in the Seoul Capital Area, South Korea. Journal of

the Air & Waste Management Association, 66(9), pp.863-873.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.