MOD003319 Business Finance: Case Study & Budgeting Report

VerifiedAdded on 2023/01/12

|10

|3124

|47

Case Study

AI Summary

This assignment presents a comprehensive financial analysis and budgeting report. Part A focuses on Mediterranean Delights Ltd (MDL), examining its financial difficulties, profit and cash flow differences, working capital components, and the impact of working capital changes on cash flow. Recommendations are made to improve MDL's cash flows through effective working capital management. Part B shifts to Second Sight corporation and explores the purpose of budgeting, traditional and alternative budgeting methods (rolling, zero-based, activity-based), and their application to the company's expansion plans, advocating for the use of rolling budgets to support growth opportunities. The report concludes with an evaluation of traditional versus alternative budgetary systems.

Making a report after a

case study

(Business Finance)

case study

(Business Finance)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

PART A...........................................................................................................................................3

Executive summary................................................................................................................3

Explaining financial analysis concepts...................................................................................3

Applying financial analysis concepts to Mediterranean Delights Ltd (MDL).......................4

Recommendation to improve company’s cash flows through working capital management 5

PART B............................................................................................................................................6

Executive summary................................................................................................................6

Understanding purpose to preparation of budget...................................................................6

Application of methods and cost management.......................................................................8

Evaluation of traditional or alternative budgetary system......................................................8

REEFRENCES..............................................................................................................................10

PART A...........................................................................................................................................3

Executive summary................................................................................................................3

Explaining financial analysis concepts...................................................................................3

Applying financial analysis concepts to Mediterranean Delights Ltd (MDL).......................4

Recommendation to improve company’s cash flows through working capital management 5

PART B............................................................................................................................................6

Executive summary................................................................................................................6

Understanding purpose to preparation of budget...................................................................6

Application of methods and cost management.......................................................................8

Evaluation of traditional or alternative budgetary system......................................................8

REEFRENCES..............................................................................................................................10

PART A

Executive summary

Section A of this article, focused on Mediterranean Delights Ltd (MDL), summarizes that

this business is experiencing financial difficulties as it will need to gain sufficient income and its

liabilities are constantly rising. It has outlined from this study that this business will receive its

due valuation from the consumers and allow efforts to preserve its healthy working capital

(Kettner, Moroney and Martin, 2013).

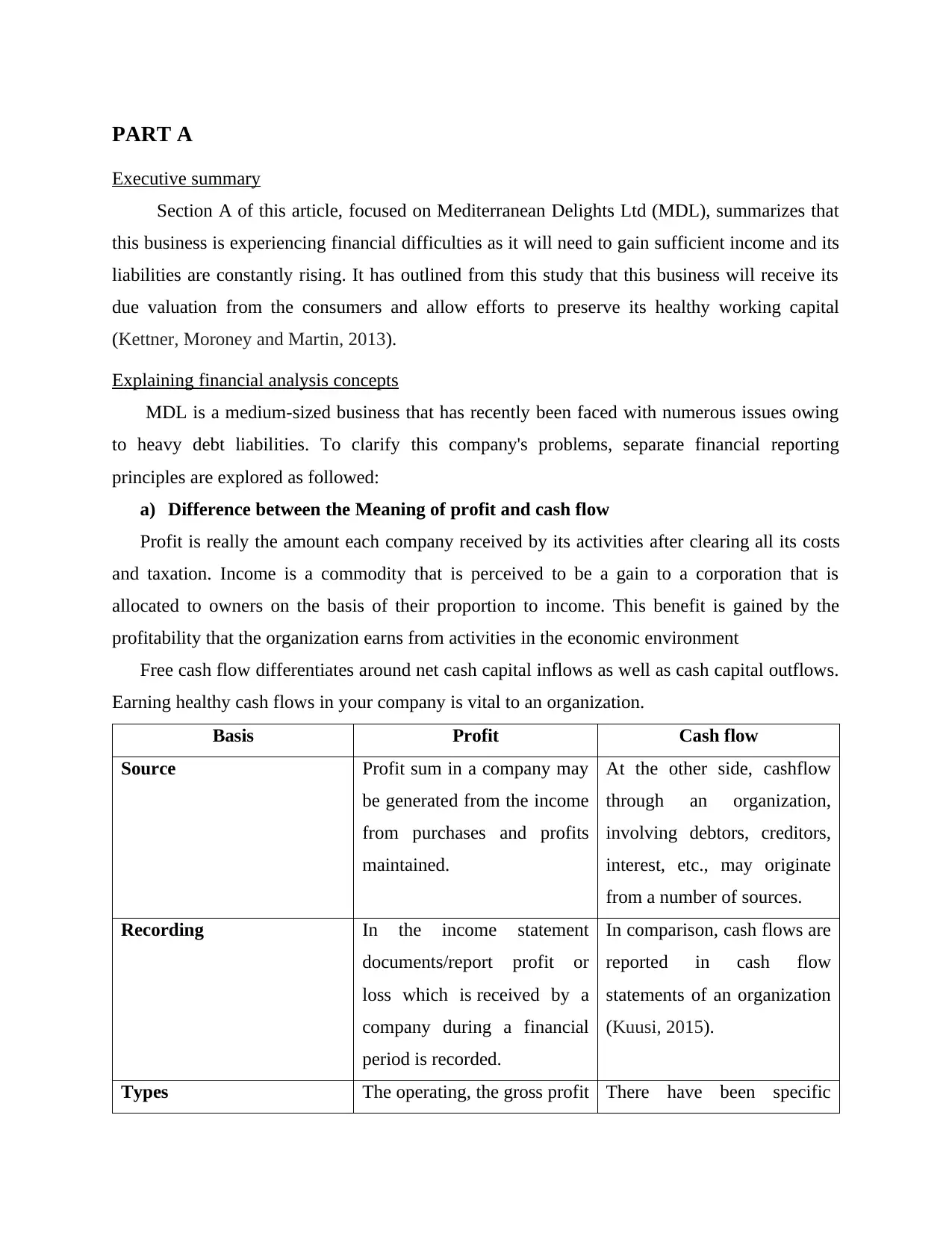

Explaining financial analysis concepts

MDL is a medium-sized business that has recently been faced with numerous issues owing

to heavy debt liabilities. To clarify this company's problems, separate financial reporting

principles are explored as followed:

a) Difference between the Meaning of profit and cash flow

Profit is really the amount each company received by its activities after clearing all its costs

and taxation. Income is a commodity that is perceived to be a gain to a corporation that is

allocated to owners on the basis of their proportion to income. This benefit is gained by the

profitability that the organization earns from activities in the economic environment

Free cash flow differentiates around net cash capital inflows as well as cash capital outflows.

Earning healthy cash flows in your company is vital to an organization.

Basis Profit Cash flow

Source Profit sum in a company may

be generated from the income

from purchases and profits

maintained.

At the other side, cashflow

through an organization,

involving debtors, creditors,

interest, etc., may originate

from a number of sources.

Recording In the income statement

documents/report profit or

loss which is received by a

company during a financial

period is recorded.

In comparison, cash flows are

reported in cash flow

statements of an organization

(Kuusi, 2015).

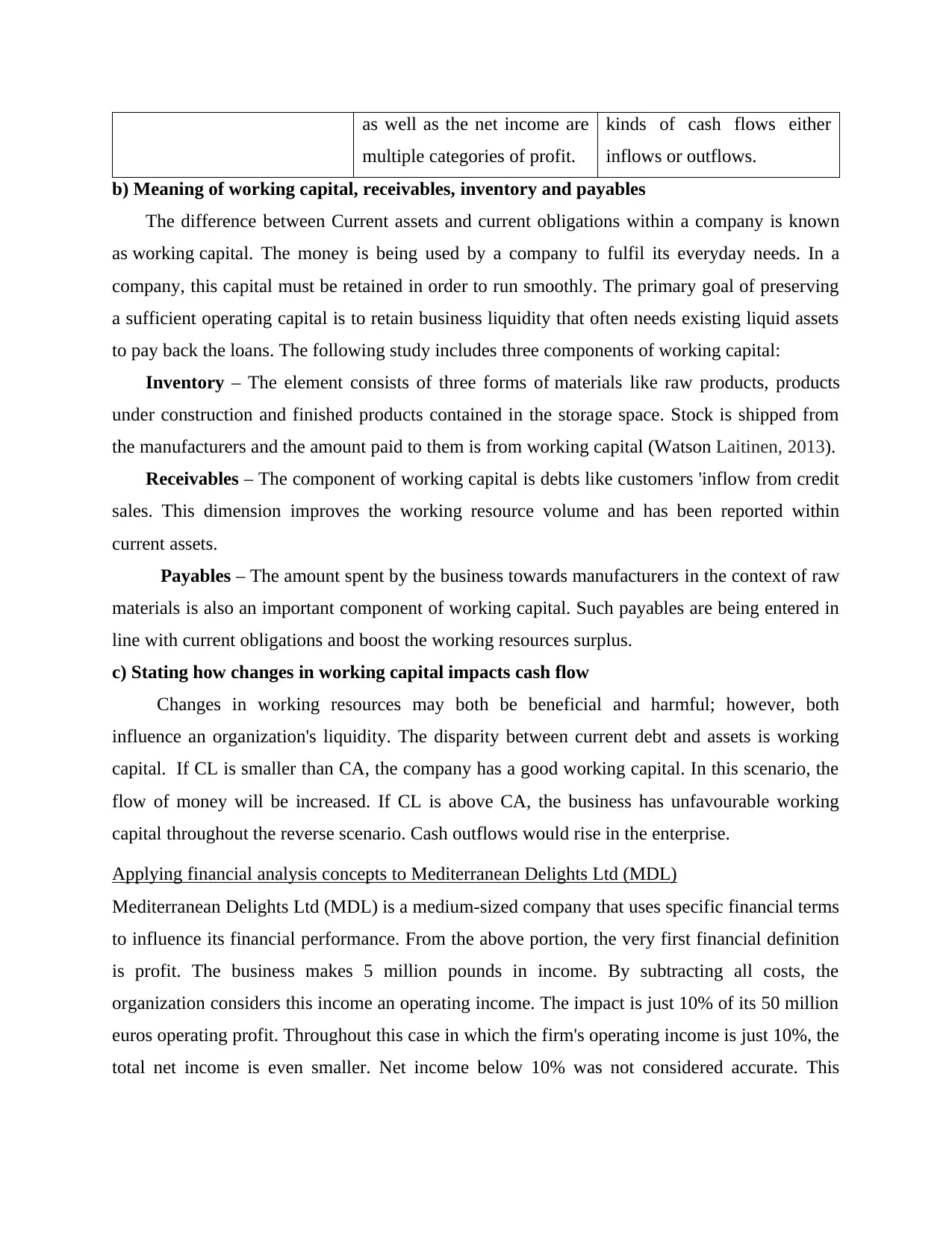

Types The operating, the gross profit There have been specific

Executive summary

Section A of this article, focused on Mediterranean Delights Ltd (MDL), summarizes that

this business is experiencing financial difficulties as it will need to gain sufficient income and its

liabilities are constantly rising. It has outlined from this study that this business will receive its

due valuation from the consumers and allow efforts to preserve its healthy working capital

(Kettner, Moroney and Martin, 2013).

Explaining financial analysis concepts

MDL is a medium-sized business that has recently been faced with numerous issues owing

to heavy debt liabilities. To clarify this company's problems, separate financial reporting

principles are explored as followed:

a) Difference between the Meaning of profit and cash flow

Profit is really the amount each company received by its activities after clearing all its costs

and taxation. Income is a commodity that is perceived to be a gain to a corporation that is

allocated to owners on the basis of their proportion to income. This benefit is gained by the

profitability that the organization earns from activities in the economic environment

Free cash flow differentiates around net cash capital inflows as well as cash capital outflows.

Earning healthy cash flows in your company is vital to an organization.

Basis Profit Cash flow

Source Profit sum in a company may

be generated from the income

from purchases and profits

maintained.

At the other side, cashflow

through an organization,

involving debtors, creditors,

interest, etc., may originate

from a number of sources.

Recording In the income statement

documents/report profit or

loss which is received by a

company during a financial

period is recorded.

In comparison, cash flows are

reported in cash flow

statements of an organization

(Kuusi, 2015).

Types The operating, the gross profit There have been specific

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as well as the net income are

multiple categories of profit.

kinds of cash flows either

inflows or outflows.

b) Meaning of working capital, receivables, inventory and payables

The difference between Current assets and current obligations within a company is known

as working capital. The money is being used by a company to fulfil its everyday needs. In a

company, this capital must be retained in order to run smoothly. The primary goal of preserving

a sufficient operating capital is to retain business liquidity that often needs existing liquid assets

to pay back the loans. The following study includes three components of working capital:

Inventory – The element consists of three forms of materials like raw products, products

under construction and finished products contained in the storage space. Stock is shipped from

the manufacturers and the amount paid to them is from working capital (Watson Laitinen, 2013).

Receivables – The component of working capital is debts like customers 'inflow from credit

sales. This dimension improves the working resource volume and has been reported within

current assets.

Payables – The amount spent by the business towards manufacturers in the context of raw

materials is also an important component of working capital. Such payables are being entered in

line with current obligations and boost the working resources surplus.

c) Stating how changes in working capital impacts cash flow

Changes in working resources may both be beneficial and harmful; however, both

influence an organization's liquidity. The disparity between current debt and assets is working

capital. If CL is smaller than CA, the company has a good working capital. In this scenario, the

flow of money will be increased. If CL is above CA, the business has unfavourable working

capital throughout the reverse scenario. Cash outflows would rise in the enterprise.

Applying financial analysis concepts to Mediterranean Delights Ltd (MDL)

Mediterranean Delights Ltd (MDL) is a medium-sized company that uses specific financial terms

to influence its financial performance. From the above portion, the very first financial definition

is profit. The business makes 5 million pounds in income. By subtracting all costs, the

organization considers this income an operating income. The impact is just 10% of its 50 million

euros operating profit. Throughout this case in which the firm's operating income is just 10%, the

total net income is even smaller. Net income below 10% was not considered accurate. This

multiple categories of profit.

kinds of cash flows either

inflows or outflows.

b) Meaning of working capital, receivables, inventory and payables

The difference between Current assets and current obligations within a company is known

as working capital. The money is being used by a company to fulfil its everyday needs. In a

company, this capital must be retained in order to run smoothly. The primary goal of preserving

a sufficient operating capital is to retain business liquidity that often needs existing liquid assets

to pay back the loans. The following study includes three components of working capital:

Inventory – The element consists of three forms of materials like raw products, products

under construction and finished products contained in the storage space. Stock is shipped from

the manufacturers and the amount paid to them is from working capital (Watson Laitinen, 2013).

Receivables – The component of working capital is debts like customers 'inflow from credit

sales. This dimension improves the working resource volume and has been reported within

current assets.

Payables – The amount spent by the business towards manufacturers in the context of raw

materials is also an important component of working capital. Such payables are being entered in

line with current obligations and boost the working resources surplus.

c) Stating how changes in working capital impacts cash flow

Changes in working resources may both be beneficial and harmful; however, both

influence an organization's liquidity. The disparity between current debt and assets is working

capital. If CL is smaller than CA, the company has a good working capital. In this scenario, the

flow of money will be increased. If CL is above CA, the business has unfavourable working

capital throughout the reverse scenario. Cash outflows would rise in the enterprise.

Applying financial analysis concepts to Mediterranean Delights Ltd (MDL)

Mediterranean Delights Ltd (MDL) is a medium-sized company that uses specific financial terms

to influence its financial performance. From the above portion, the very first financial definition

is profit. The business makes 5 million pounds in income. By subtracting all costs, the

organization considers this income an operating income. The impact is just 10% of its 50 million

euros operating profit. Throughout this case in which the firm's operating income is just 10%, the

total net income is even smaller. Net income below 10% was not considered accurate. This

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

strategy has led to reducing productivity performance for businesses with large business

expenses (Mazikana, 2019).

Cash flow is yet another financial term discussed above case study. The Mediterranean

Delights Ltd (MDL) revealed that the firm was experiencing an adverse cash flow condition, as

its main clients sold the loan to Delios Limited 1.5 million euros and Sam Pedro Limited 2

million lbs. The firm's method of supplying their clients with higher credit sales has resulted in

weak working capital economic performance.

Working capital is considered to be an important components financial element defined in MDL

case study. The Mediterranean Delights Ltd (MDL) case studies have shown that claims are

available in the business but the payment sum is fairly growing. Also, after the liability raise,

from 16 million to 18 million euros, this company continues to lease its goods and as a

financial result are unfavourable working capital and heavy current obligations. This way of

funding the credit policies would also affect on the business's sustainability, and insolvency is

sure to follow in nearby time (Ofei-Mensah and Bennett, 2013).

Recommendation to improve company’s cash flows through working capital management

The functional administration of resources is the way to handle the strategies and

approaches of the business that improve credit supply and acceptance. Mediterranean Delights

Ltd (MDL) may use this method to boost cash inflows for their business. The working capital

planning process or approach comprises the following 3 proportions: working capital ratio, the

inventory ratio as well the average collection period.

Mediterranean Delights Ltd (MDL) is advised to compensate its liabilities as well as

increase its current assets in order to sustain a healthy working capital percentage. The above

business will make every effort to ensure its people pay their owing amounts as Delios Limited

has been provided with 1.5 million pounds of credit and Sam Pedro Limited 2 million pounds by

MDL. The average collection proportion is also needed to be improved by the company. As in

current scenarios the company’s collection percentage is weak, since they have to collected huge

amount for the existing market which they are unable to do the same. For this reason, it is

advisable to modify this company's recovery policies for setting total loan duration of 60 days,

under which each borrower shall pay the sum due less than 2 months.

The last suggestion is to retain its inventory ratio. The cost of production produced and the total

inventory shall be measured accordingly (Weetman, 2010). This is why the company spends

expenses (Mazikana, 2019).

Cash flow is yet another financial term discussed above case study. The Mediterranean

Delights Ltd (MDL) revealed that the firm was experiencing an adverse cash flow condition, as

its main clients sold the loan to Delios Limited 1.5 million euros and Sam Pedro Limited 2

million lbs. The firm's method of supplying their clients with higher credit sales has resulted in

weak working capital economic performance.

Working capital is considered to be an important components financial element defined in MDL

case study. The Mediterranean Delights Ltd (MDL) case studies have shown that claims are

available in the business but the payment sum is fairly growing. Also, after the liability raise,

from 16 million to 18 million euros, this company continues to lease its goods and as a

financial result are unfavourable working capital and heavy current obligations. This way of

funding the credit policies would also affect on the business's sustainability, and insolvency is

sure to follow in nearby time (Ofei-Mensah and Bennett, 2013).

Recommendation to improve company’s cash flows through working capital management

The functional administration of resources is the way to handle the strategies and

approaches of the business that improve credit supply and acceptance. Mediterranean Delights

Ltd (MDL) may use this method to boost cash inflows for their business. The working capital

planning process or approach comprises the following 3 proportions: working capital ratio, the

inventory ratio as well the average collection period.

Mediterranean Delights Ltd (MDL) is advised to compensate its liabilities as well as

increase its current assets in order to sustain a healthy working capital percentage. The above

business will make every effort to ensure its people pay their owing amounts as Delios Limited

has been provided with 1.5 million pounds of credit and Sam Pedro Limited 2 million pounds by

MDL. The average collection proportion is also needed to be improved by the company. As in

current scenarios the company’s collection percentage is weak, since they have to collected huge

amount for the existing market which they are unable to do the same. For this reason, it is

advisable to modify this company's recovery policies for setting total loan duration of 60 days,

under which each borrower shall pay the sum due less than 2 months.

The last suggestion is to retain its inventory ratio. The cost of production produced and the total

inventory shall be measured accordingly (Weetman, 2010). This is why the company spends

only an appropriate amount on this expense of sold goods which corresponds to its estimated

inventory, to ensure the maintenance of this proportion. This company will generate a large

profit and therefore will increase its profitability by 10%.

For Mediterranean Delights Ltd (MDL), almost all of the measures and processes discussed

above are relevant, as this business will help to obtain its appropriate amount from its buyers and

it will able to maintain better profits in future time (Head, 2016).

PART B

Executive summary

Second Sight corporation is a multinational corporation that advocates use of rolling budgets.

This has been evaluated that this corporation has increased growth opportunities as a result of

which they should avoid their conventional budgeting method and implement rolling budget.

Understanding purpose to preparation of budget

A budget regards to plan that anticipates all the spending and incomes that an entity may in

future spends or receive. Budget is implying to a report formulated to fulfil an objective. There

are different budget planning and preparation objectives which are listed and discussed as below:

The primary aim of budget is to facilitate effective decision-making process. A budget

offers a mechanism for estimating receipts and spending. An entity can depend on a

budget to make correct decisions (Aktas, Croci and Petmeza, 2015).

Another significant budgetary aim is to offer a baseline for actual operations under way.

The budget also seeks to establish a consistent balance of control and accountability by

establishing pre-determined targets that should be met.

a) Traditional budgeting approaches

These approaches to budgeting utilize a traditional framework whereby a budget is designed

using financial reports or facts of the past year. The approach is focused purely on previous

year's fiscal results, which excludes any additional problems which variables. There are multiple

advantages of this approach which involves the fact because it is simple to adopt, it provides

flexibility in features and it also gives the potential to merge multiple projects within a specific

one (Atrill, 2014).

inventory, to ensure the maintenance of this proportion. This company will generate a large

profit and therefore will increase its profitability by 10%.

For Mediterranean Delights Ltd (MDL), almost all of the measures and processes discussed

above are relevant, as this business will help to obtain its appropriate amount from its buyers and

it will able to maintain better profits in future time (Head, 2016).

PART B

Executive summary

Second Sight corporation is a multinational corporation that advocates use of rolling budgets.

This has been evaluated that this corporation has increased growth opportunities as a result of

which they should avoid their conventional budgeting method and implement rolling budget.

Understanding purpose to preparation of budget

A budget regards to plan that anticipates all the spending and incomes that an entity may in

future spends or receive. Budget is implying to a report formulated to fulfil an objective. There

are different budget planning and preparation objectives which are listed and discussed as below:

The primary aim of budget is to facilitate effective decision-making process. A budget

offers a mechanism for estimating receipts and spending. An entity can depend on a

budget to make correct decisions (Aktas, Croci and Petmeza, 2015).

Another significant budgetary aim is to offer a baseline for actual operations under way.

The budget also seeks to establish a consistent balance of control and accountability by

establishing pre-determined targets that should be met.

a) Traditional budgeting approaches

These approaches to budgeting utilize a traditional framework whereby a budget is designed

using financial reports or facts of the past year. The approach is focused purely on previous

year's fiscal results, which excludes any additional problems which variables. There are multiple

advantages of this approach which involves the fact because it is simple to adopt, it provides

flexibility in features and it also gives the potential to merge multiple projects within a specific

one (Atrill, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Compared to any technique, this strategy also has few drawbacks that are its stiffness and

dependency on data from prior year. This sort of budget is tough to change and causes confusion

between work and uncertainty.

b) Alternative budget methods

Rolling budget – It is kind of modern budget that incorporates a revolutionary method to

continuous budget creation. The operations are periodically checked within this budget, as well

as any adjustments may be made if needed. This style of budget has many advantages including

lower uncertainty, flexibility as well as ability to adapt. There’re also some drawbacks of

such budget that prohibit businesses from adopting it. Such drawbacks are that this form of

budget is beneficial for projects in short term. There are still no goals in this program, owing to

which personnel lack support and inspiration (Atrill, 2015).

Zero based budget – Those kinds of budgets are developed from scratch or zero and are not

cantered on annual statements or budgets of previous year. Both expenditures and profits are

estimated applying external environment and there's no connection between budget for the 2

periods. This strategy takes a different approach, since it has several strengths and weaknesses.

This method's advantages include precision and reliance on present situation as a result of which

contingencies are which. Demerit points of this strategy are that this form of budget is ideal for

programs with restricted time periods and not unrestricted time frames for organizations.

Activity based budget – Each form of spending involves overheads on a per operation basis. This

budgetary strategy is known to be one of most effective, since it contributes to the evaluation of

costs linked with increasing operation (Blaak, Openjuru and Zeelen, 2013). This method has

multiple advantages and demerits that involve the following:

This method benefits from the ability of a company to distinguish costs related with each

operation. This approach also aims to achieve a strategic advantage by contrasting the effects of

their operations with those of other organizations. This method also has several demerits that

cover dynamic nature because it is not easy to cost computing against each operation/activity.

There is a broad disparity between conventional and modern forms of budgeting as

analysed from the aforementioned analysis. Alternative budget methods are useful for

contemporary entities like Second Sight corporation.

dependency on data from prior year. This sort of budget is tough to change and causes confusion

between work and uncertainty.

b) Alternative budget methods

Rolling budget – It is kind of modern budget that incorporates a revolutionary method to

continuous budget creation. The operations are periodically checked within this budget, as well

as any adjustments may be made if needed. This style of budget has many advantages including

lower uncertainty, flexibility as well as ability to adapt. There’re also some drawbacks of

such budget that prohibit businesses from adopting it. Such drawbacks are that this form of

budget is beneficial for projects in short term. There are still no goals in this program, owing to

which personnel lack support and inspiration (Atrill, 2015).

Zero based budget – Those kinds of budgets are developed from scratch or zero and are not

cantered on annual statements or budgets of previous year. Both expenditures and profits are

estimated applying external environment and there's no connection between budget for the 2

periods. This strategy takes a different approach, since it has several strengths and weaknesses.

This method's advantages include precision and reliance on present situation as a result of which

contingencies are which. Demerit points of this strategy are that this form of budget is ideal for

programs with restricted time periods and not unrestricted time frames for organizations.

Activity based budget – Each form of spending involves overheads on a per operation basis. This

budgetary strategy is known to be one of most effective, since it contributes to the evaluation of

costs linked with increasing operation (Blaak, Openjuru and Zeelen, 2013). This method has

multiple advantages and demerits that involve the following:

This method benefits from the ability of a company to distinguish costs related with each

operation. This approach also aims to achieve a strategic advantage by contrasting the effects of

their operations with those of other organizations. This method also has several demerits that

cover dynamic nature because it is not easy to cost computing against each operation/activity.

There is a broad disparity between conventional and modern forms of budgeting as

analysed from the aforementioned analysis. Alternative budget methods are useful for

contemporary entities like Second Sight corporation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Application of methods and cost management

Second sight plc is a multinational corporation that actually makes use of conventional budgeting

approaches. This business is involved in the manufacture of prescription spectacles and

accessories for numerous leading firms. This company has plans for future of building a new

plant in Netherlands for that they intend to form joint venture with Indian corporation. In this

situation, evaluating which budgetary strategy would support this business is significant. In the

background of this enterprise, the approach of all budgets is discussed below as along with

analysis of how goods and procedures should be planned for this enterprise (Brown, A.M.,

2015).

Traditional budgeting systems – This method is employed by the organization under which

they create a budget plan based on budget estimate from a previous year. When the corporation

begins with joint venture, this will no longer be allowed to use this method. The system includes

reports and expenditures from last year so this organization would not be able to utilize this

method in absence of last year's budget plan as joint venture would be newly formed enterprise.

Alternative budgeting systems – Usage of alternate budgetary methods is strongly

recommended for this organization. If this company wants to choose rolling schedule, instead

they can continue to manage their expenses. They can make changes anytime they want. If

businesses prefer zero base budgeting, they must schedule their upcoming annual expense

control. Each year, such organization will form new budget and each framed budget has no

connection with the budget of the previous year. The organization must monitor its projected

expenses in the case of task-based expenditures by assessing and defining costs linked with each

operation or activity (Drury, 2016).

Evaluation of traditional or alternative budgetary system

Traditional and alternate budgetary frameworks are two terms of separate existence. Both work

differently as per their characteristics. Traditional is used only in older times and also has

significance in case of routine or continuous in nature activities. The unusual improvements can

be easily recognized by the use of traditional budgetary framework process. More changes in

environmental events or variables are the primary reason for its use in past. It has the least

impact on an organization's overall operation, including the efficiency of various divisions. Now,

switch the situation (Finger and El Benni, 2014). Organizations are globalized and there is a

great deal of change in the international world that has an immense impact on activities. Owing

Second sight plc is a multinational corporation that actually makes use of conventional budgeting

approaches. This business is involved in the manufacture of prescription spectacles and

accessories for numerous leading firms. This company has plans for future of building a new

plant in Netherlands for that they intend to form joint venture with Indian corporation. In this

situation, evaluating which budgetary strategy would support this business is significant. In the

background of this enterprise, the approach of all budgets is discussed below as along with

analysis of how goods and procedures should be planned for this enterprise (Brown, A.M.,

2015).

Traditional budgeting systems – This method is employed by the organization under which

they create a budget plan based on budget estimate from a previous year. When the corporation

begins with joint venture, this will no longer be allowed to use this method. The system includes

reports and expenditures from last year so this organization would not be able to utilize this

method in absence of last year's budget plan as joint venture would be newly formed enterprise.

Alternative budgeting systems – Usage of alternate budgetary methods is strongly

recommended for this organization. If this company wants to choose rolling schedule, instead

they can continue to manage their expenses. They can make changes anytime they want. If

businesses prefer zero base budgeting, they must schedule their upcoming annual expense

control. Each year, such organization will form new budget and each framed budget has no

connection with the budget of the previous year. The organization must monitor its projected

expenses in the case of task-based expenditures by assessing and defining costs linked with each

operation or activity (Drury, 2016).

Evaluation of traditional or alternative budgetary system

Traditional and alternate budgetary frameworks are two terms of separate existence. Both work

differently as per their characteristics. Traditional is used only in older times and also has

significance in case of routine or continuous in nature activities. The unusual improvements can

be easily recognized by the use of traditional budgetary framework process. More changes in

environmental events or variables are the primary reason for its use in past. It has the least

impact on an organization's overall operation, including the efficiency of various divisions. Now,

switch the situation (Finger and El Benni, 2014). Organizations are globalized and there is a

great deal of change in the international world that has an immense impact on activities. Owing

to the lack of understanding of other considerations, the strength of the conventional method of

budgeting is inadequate in this context. The end result of this would be calculated in the forms of

adverse consequences and unfounded forecasts which are not accurate for possible choices to be

made. Here, the alternate budgeting method is the right way to follow in keeping with today's

environment. This is a method that involves the integration of multiple financial strategies that

can aid in the estimation of potential operations, taking into account both the relevant external as

well as internal variables.

Every decision has its own preference. It will also offer an incentive to pick one that is

ideally suited to the individual departments functioning structure. A company must in future

determine the value of reducing threats, implementing integration initiatives and building a

robust internal operating climate. Overall, this gives confidence to all different teams that are

able to meet the operational objectives within a defined timeline.

budgeting is inadequate in this context. The end result of this would be calculated in the forms of

adverse consequences and unfounded forecasts which are not accurate for possible choices to be

made. Here, the alternate budgeting method is the right way to follow in keeping with today's

environment. This is a method that involves the integration of multiple financial strategies that

can aid in the estimation of potential operations, taking into account both the relevant external as

well as internal variables.

Every decision has its own preference. It will also offer an incentive to pick one that is

ideally suited to the individual departments functioning structure. A company must in future

determine the value of reducing threats, implementing integration initiatives and building a

robust internal operating climate. Overall, this gives confidence to all different teams that are

able to meet the operational objectives within a defined timeline.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REEFRENCES

Books and Journals

Aktas, Croci, Petmeza, 2015. Is working capital management value-enchancing. Journal of

Corporate Finance 30, pp. 98-113.pdf

Atrill 2014. Financial Management for Decision Makers. 7th ed. London FT Prentice Hall.

Chapter 10 - Working Capital.pdf

Atrill, 2015. Management Accounting for Decision Makers. 8th ed. London Pearson. Chapter 6

Budgeting.pdf

Blaak, M., Openjuru, G. L. and Zeelen, J., 2013. Non-formal vocational education in Uganda:

Practical empowerment through a workable alternative. International Journal of

Educational Development. 33(1). pp.88-97.

Brown, A.M., 2015, August. The influence of the traditional reporting model on Fijian budgetary

addresses. In Forum of International Development Studies (Vol. 46, No. 7, pp. 1-17).

Drury, 2016. Management Accounting for Business 6th ed. London Cengage. Chapter 9 The

Budgeting Process.pdf

Finger, R. and El Benni, N., 2014. Alternative specifications of reference income levels in the

income stabilization tool. In Agricultural Cooperative Management and Policy (pp. 65-

85). Springer, Cham.

Kettner, P. M., Moroney, R. M. and Martin, L. L., 2013. Designing and managing programs: An

effectiveness-based approach: An effectiveness-based approach. Sage.

Kuusi, T., 2015. Alternatives for measuring structural budgetary position.

Laitinen, E. K., 2013. Financial and non-financial variables in predicting failure of small

business reorganisation. International Journal of Accounting and Finance. 4(1). pp.1-34.

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Ofei-Mensah, A. and Bennett, J., 2013. Transaction costs of alternative greenhouse gas policies

in the Australian transport energy sector. Ecological Economics. 88. pp.214-221.

Watson Head, 2016. Corporate Finance. 7th ed. London Pearson. Chapter 3 - Working

Capital.pdf

Weetman, 2010. Management Accounting. 2nd ed. London FT Prentice Hall. Chapter 13

Preparing a budget.

Books and Journals

Aktas, Croci, Petmeza, 2015. Is working capital management value-enchancing. Journal of

Corporate Finance 30, pp. 98-113.pdf

Atrill 2014. Financial Management for Decision Makers. 7th ed. London FT Prentice Hall.

Chapter 10 - Working Capital.pdf

Atrill, 2015. Management Accounting for Decision Makers. 8th ed. London Pearson. Chapter 6

Budgeting.pdf

Blaak, M., Openjuru, G. L. and Zeelen, J., 2013. Non-formal vocational education in Uganda:

Practical empowerment through a workable alternative. International Journal of

Educational Development. 33(1). pp.88-97.

Brown, A.M., 2015, August. The influence of the traditional reporting model on Fijian budgetary

addresses. In Forum of International Development Studies (Vol. 46, No. 7, pp. 1-17).

Drury, 2016. Management Accounting for Business 6th ed. London Cengage. Chapter 9 The

Budgeting Process.pdf

Finger, R. and El Benni, N., 2014. Alternative specifications of reference income levels in the

income stabilization tool. In Agricultural Cooperative Management and Policy (pp. 65-

85). Springer, Cham.

Kettner, P. M., Moroney, R. M. and Martin, L. L., 2013. Designing and managing programs: An

effectiveness-based approach: An effectiveness-based approach. Sage.

Kuusi, T., 2015. Alternatives for measuring structural budgetary position.

Laitinen, E. K., 2013. Financial and non-financial variables in predicting failure of small

business reorganisation. International Journal of Accounting and Finance. 4(1). pp.1-34.

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Ofei-Mensah, A. and Bennett, J., 2013. Transaction costs of alternative greenhouse gas policies

in the Australian transport energy sector. Ecological Economics. 88. pp.214-221.

Watson Head, 2016. Corporate Finance. 7th ed. London Pearson. Chapter 3 - Working

Capital.pdf

Weetman, 2010. Management Accounting. 2nd ed. London FT Prentice Hall. Chapter 13

Preparing a budget.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.