Final Assignment: MCO201 Finance Case Study on Medical Inc. Project

VerifiedAdded on 2022/08/26

|6

|950

|13

Case Study

AI Summary

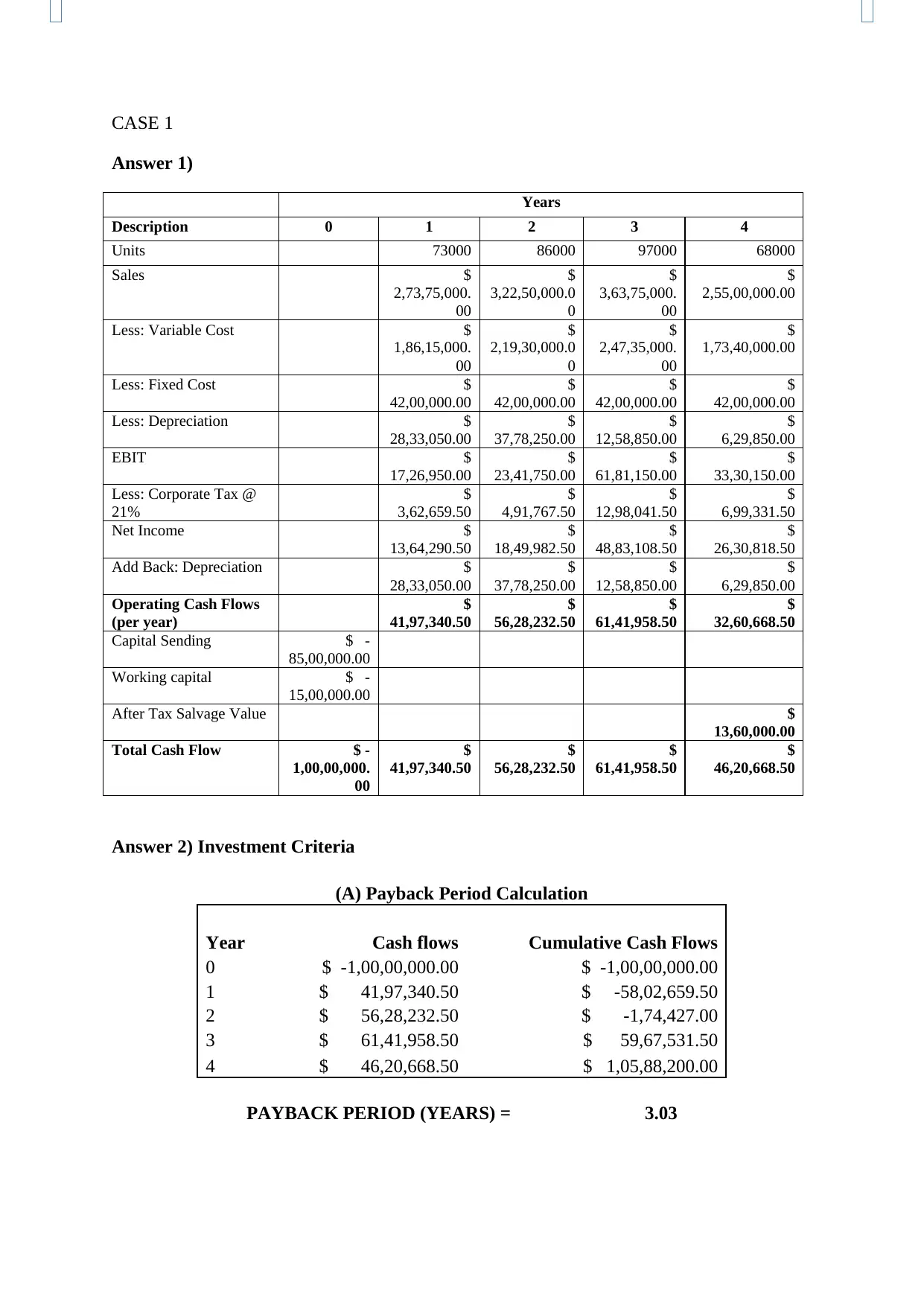

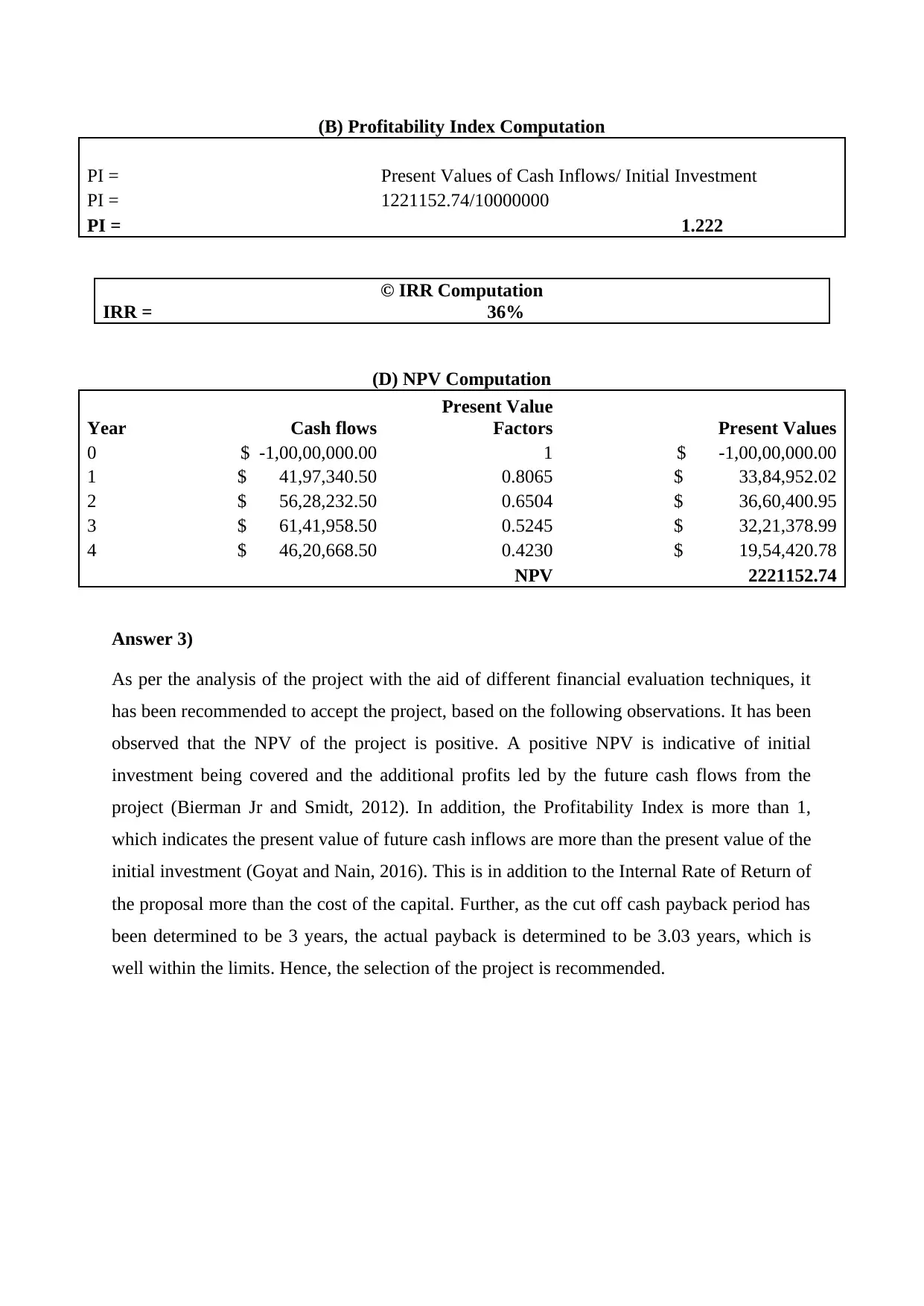

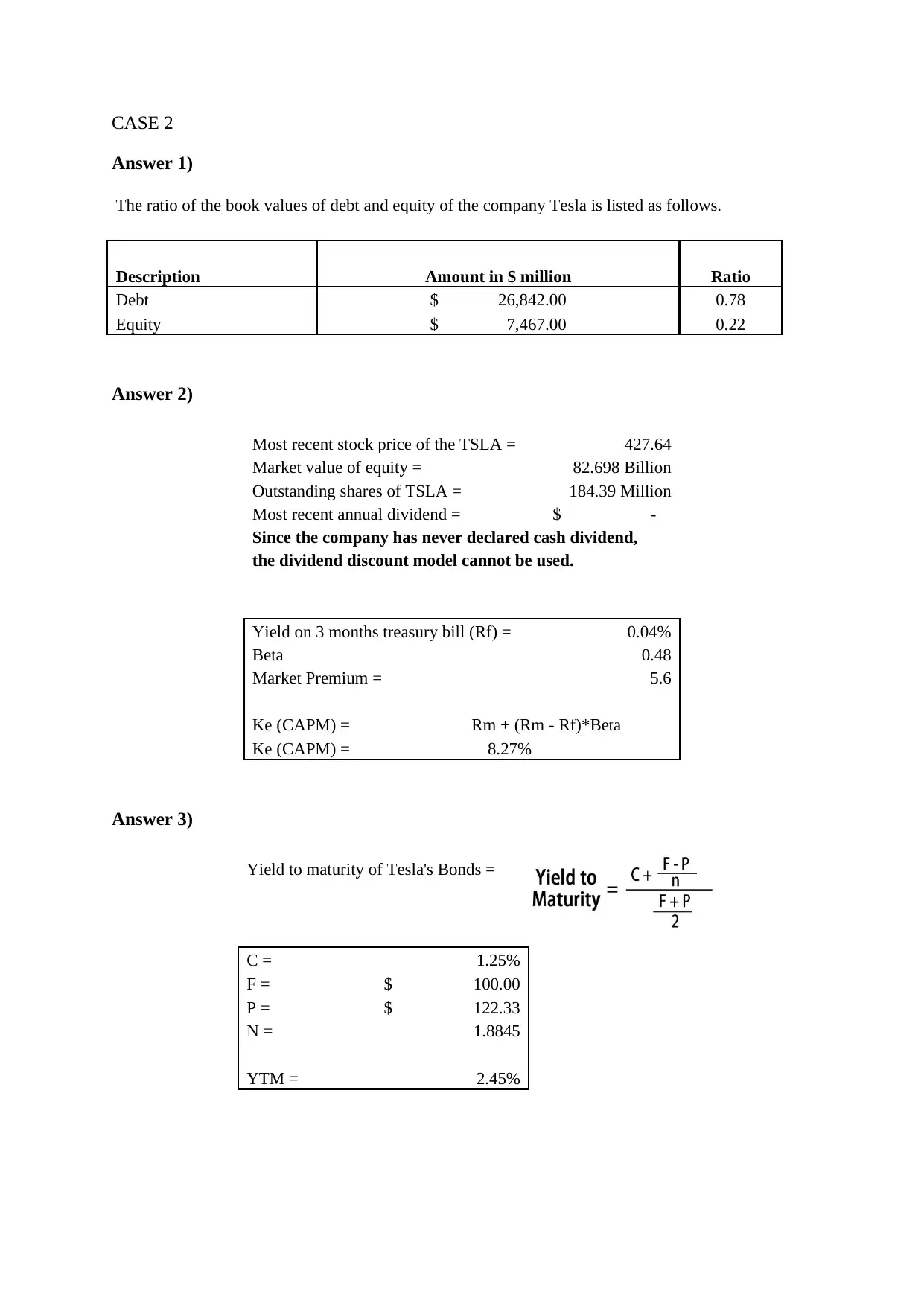

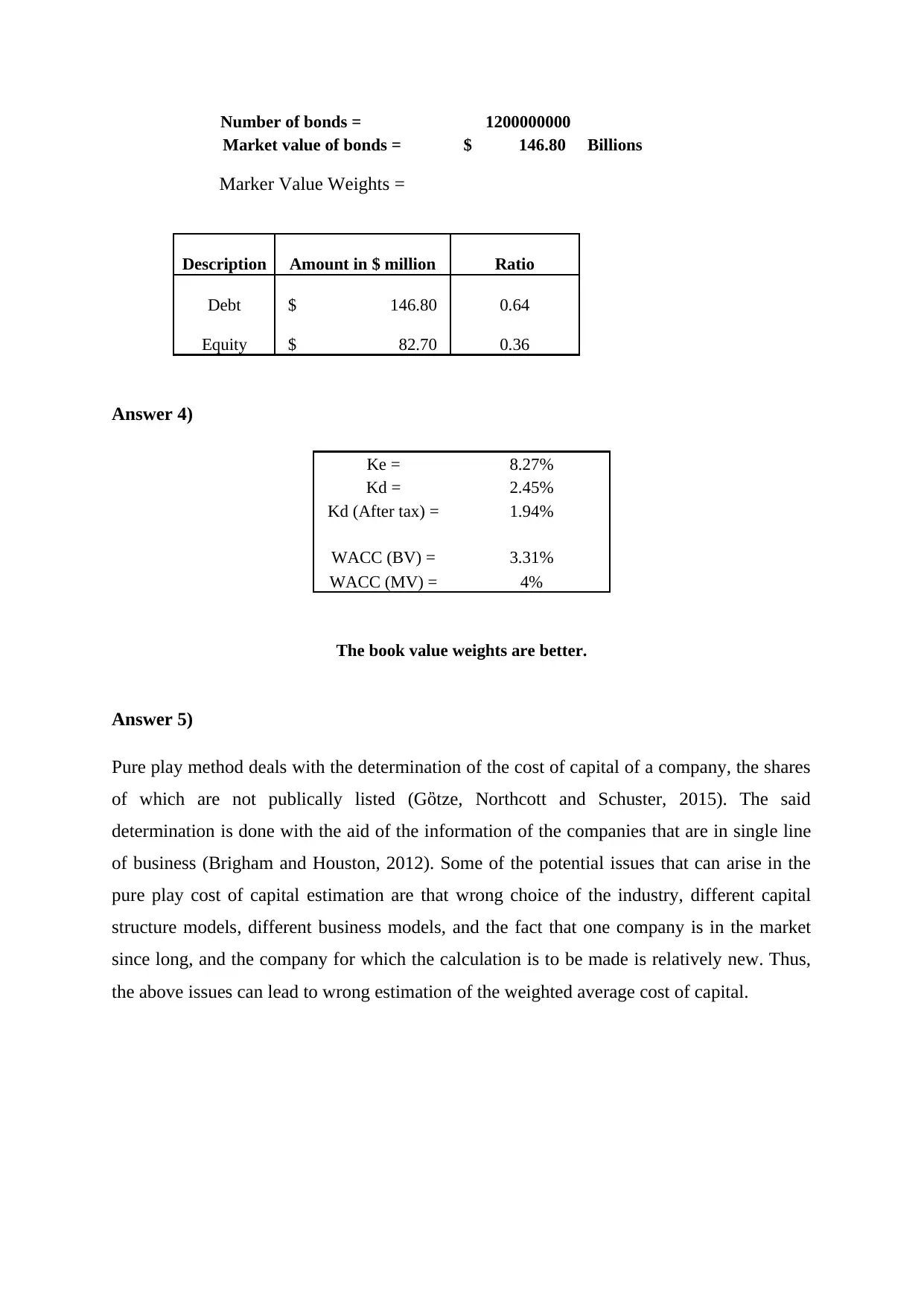

This document presents a comprehensive analysis of two finance case studies. Case 1 focuses on Medical Inc., evaluating a new dental implant project using capital budgeting techniques. It calculates cash flows, payback period, profitability index, NPV, and IRR to determine the project's financial viability, recommending acceptance based on positive NPV and other favorable metrics. Case 2 analyzes Tesla's financial structure, calculating the debt-to-equity ratio, market value of equity, and cost of capital. It determines the cost of equity using CAPM, yield to maturity, and WACC using both book and market value weights. The document also addresses the pure play method, discussing potential issues in determining the cost of capital for companies with limited publicly available information. The analysis provides detailed calculations and recommendations based on financial principles.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.