Finance Case Study Solutions

VerifiedAdded on 2019/09/22

|8

|1082

|296

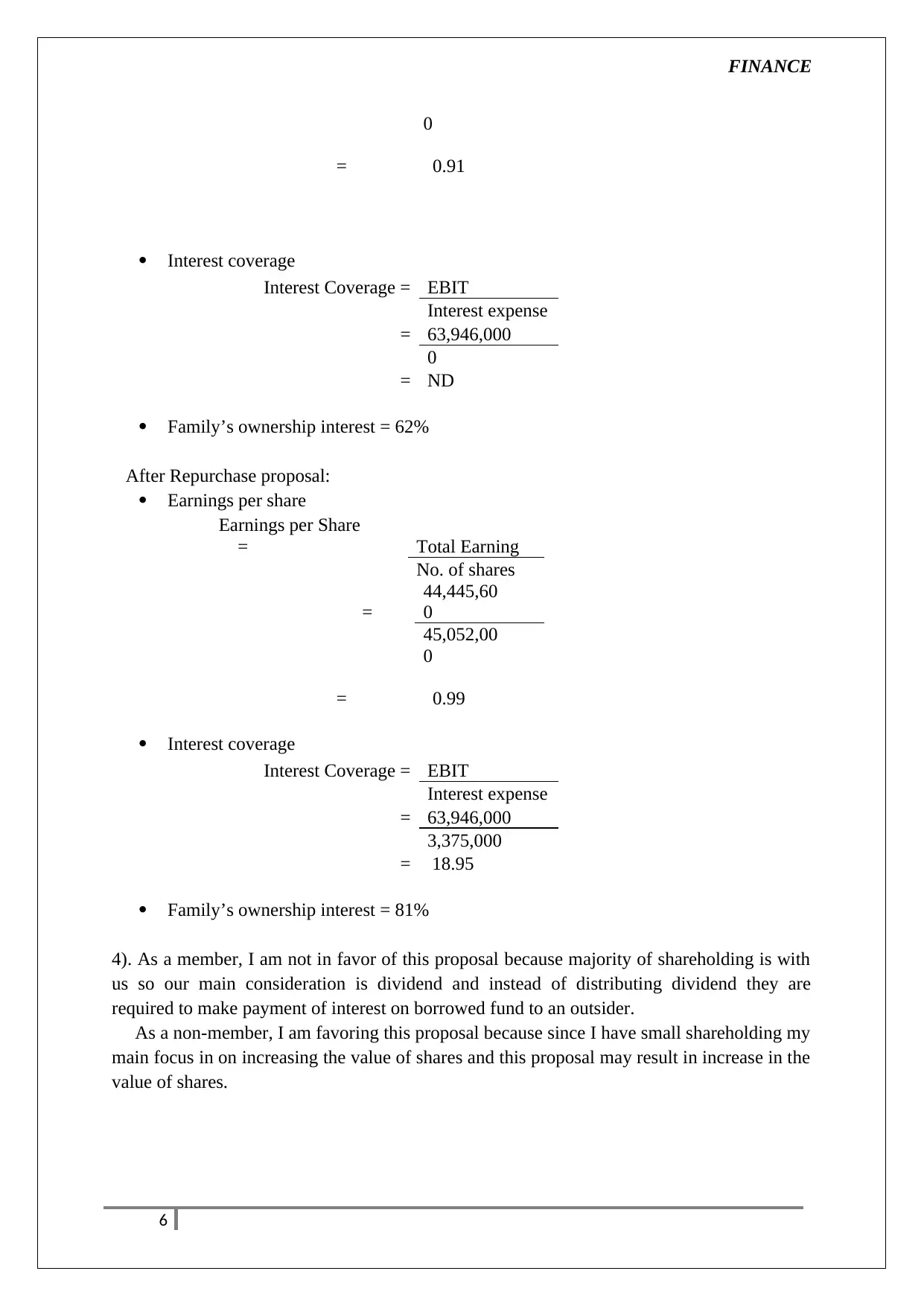

Case Study

AI Summary

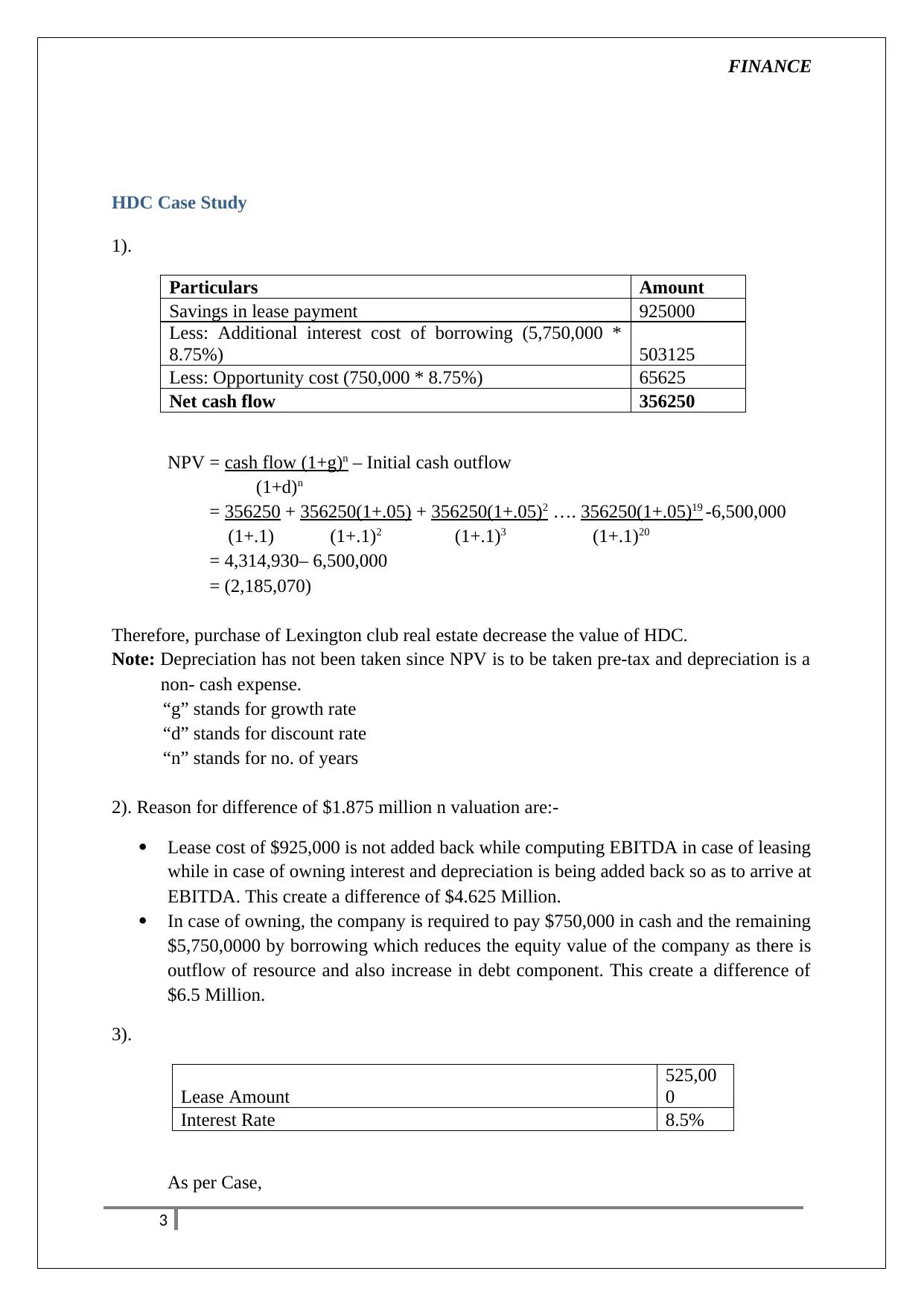

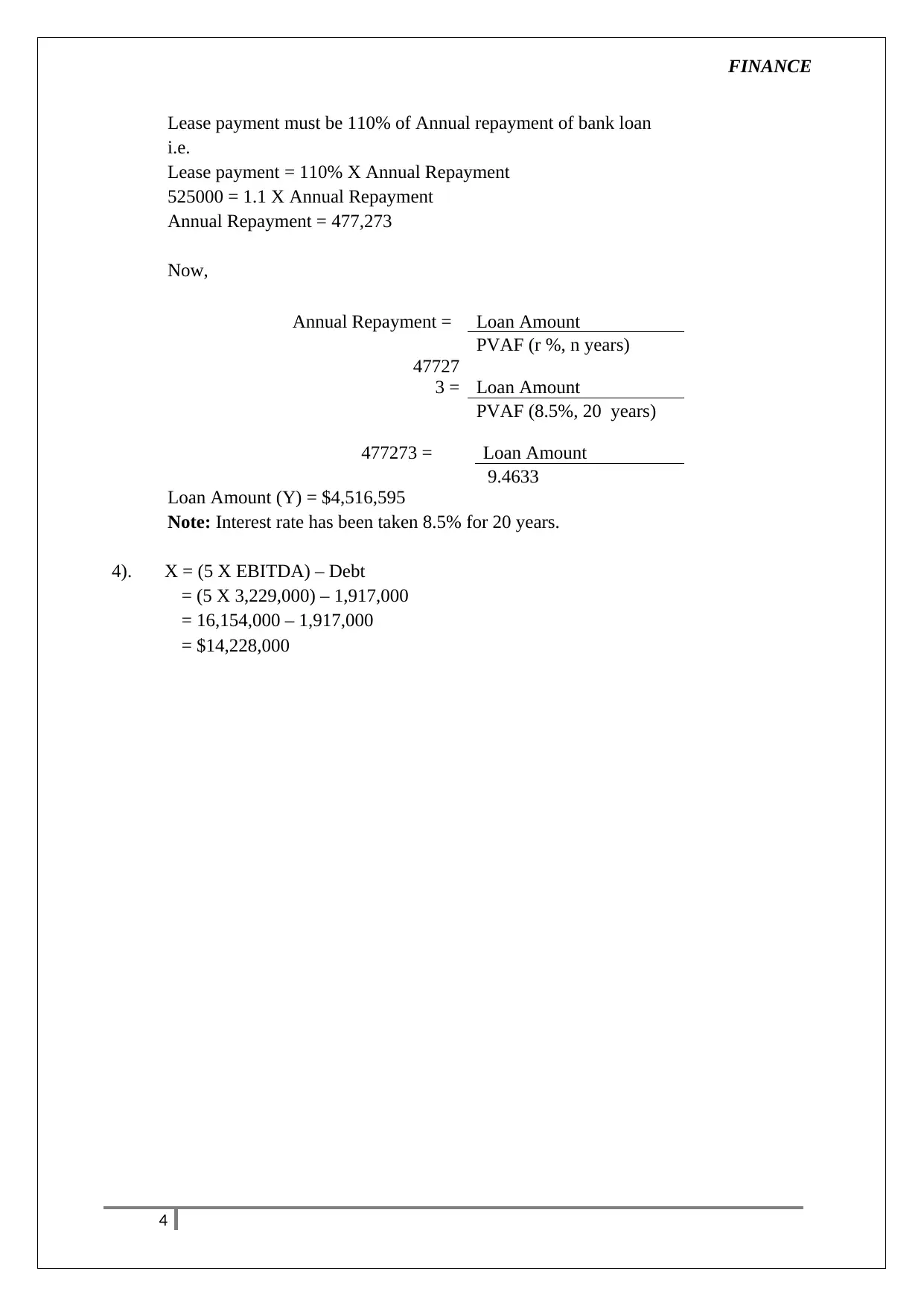

This case study analyzes two companies: HDC and Blaine Kitchenware. For HDC, the analysis focuses on the profitability of a real estate investment using Net Present Value (NPV) calculations. It explores the differences in valuation between leasing and owning the property, considering factors like interest costs, opportunity costs, and depreciation. The Blaine Kitchenware case study examines the company's capital structure, payout policy, and a proposed share repurchase. It evaluates the appropriateness of the current capital structure, the impact of the repurchase on earnings per share (EPS), interest coverage, and family ownership. The analysis considers the advantages and disadvantages of the share repurchase from both majority and minority shareholder perspectives, referencing relevant financial theories like Walter's model and the concept of trading on equity. The document includes detailed calculations and references supporting the analysis.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.