Business Finance: Analysis of Concepts and Mediterranean Delights Ltd

VerifiedAdded on 2023/01/13

|11

|3166

|58

Report

AI Summary

This report delves into key business finance concepts, examining profit, cash flow, working capital, accounts receivable, and accounts payable. Part 1 applies these concepts to Mediterranean Delights Ltd, analyzing its financial situation, including receivables, inventories, and payables, and offering recommendations for improved cash flow management, such as analyzing costs, managing borrowings, and resolving disputes. Part 2 shifts focus to budgeting, discussing its purpose and the advantages and disadvantages of traditional and alternative budgeting approaches, particularly for Second Sight Plc. The report aims to provide a comprehensive understanding of financial management principles and their practical application in real-world business scenarios. The report also offers recommendations for improving cash flow and overall financial performance.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

PART 1...................................................................................................................................3

1. Explanation about following terms:...................................................................................3

a..............................................................................................................................................3

b..............................................................................................................................................4

2. Application of above discussed concepts in context of Mediterranean Delights Ltd:.......4

3. Analysis and Recommendations:.......................................................................................6

PART 2...................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................7

1..............................................................................................................................................7

2..............................................................................................................................................9

3..............................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

EXECUTIVE SUMMARY.............................................................................................................3

PART 1...................................................................................................................................3

1. Explanation about following terms:...................................................................................3

a..............................................................................................................................................3

b..............................................................................................................................................4

2. Application of above discussed concepts in context of Mediterranean Delights Ltd:.......4

3. Analysis and Recommendations:.......................................................................................6

PART 2...................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................7

1..............................................................................................................................................7

2..............................................................................................................................................9

3..............................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

EXECUTIVE SUMMARY

The concept of Business Finance refers to the resources, monies, investments and

obligations involved in business processes. The key role for managers and business operator is to

control employed resources and to use resources efficiently in business (Cole, 2013). The study

as a whole has two sections, the first providing a detailed review on multiple business concepts

such as accounts receivable, accounts payable, cash flows and profit in context of Mediterranean

Delights Ltd.

PART 1

1. Explanation about following terms:

a.

Profit: It is also termed as the “net income,” as the amount of earning that exceeds cost in an

accounting period. Profit is a measure of profitability which is the owner's major interest in the

income through market production. Profit is one of the major sources of economic well-being

because it means incomes and opportunities to develop production. It is the reward generated by

business owners for their initial investment. Profit is further classified in three parts are as

follows- gross profit, operating profit and net profit (Hussain and Scott, 2015).

Cash Flow: It is the financial statement that provides aggregate data regarding of all cash inflow

(amount received) and cash outflow (amount paid) of an organisation during an accounting

period. It is essential to summarize the amount of cash and cash equivalent entering and leaving

a company. It is believed to be the most effective among all financial statements as it is helpful

in operations, investment and financing cash flow. This statement of cash flow acts as a bridge

between the income statement and balance sheet by showing the movement of money in a

business.

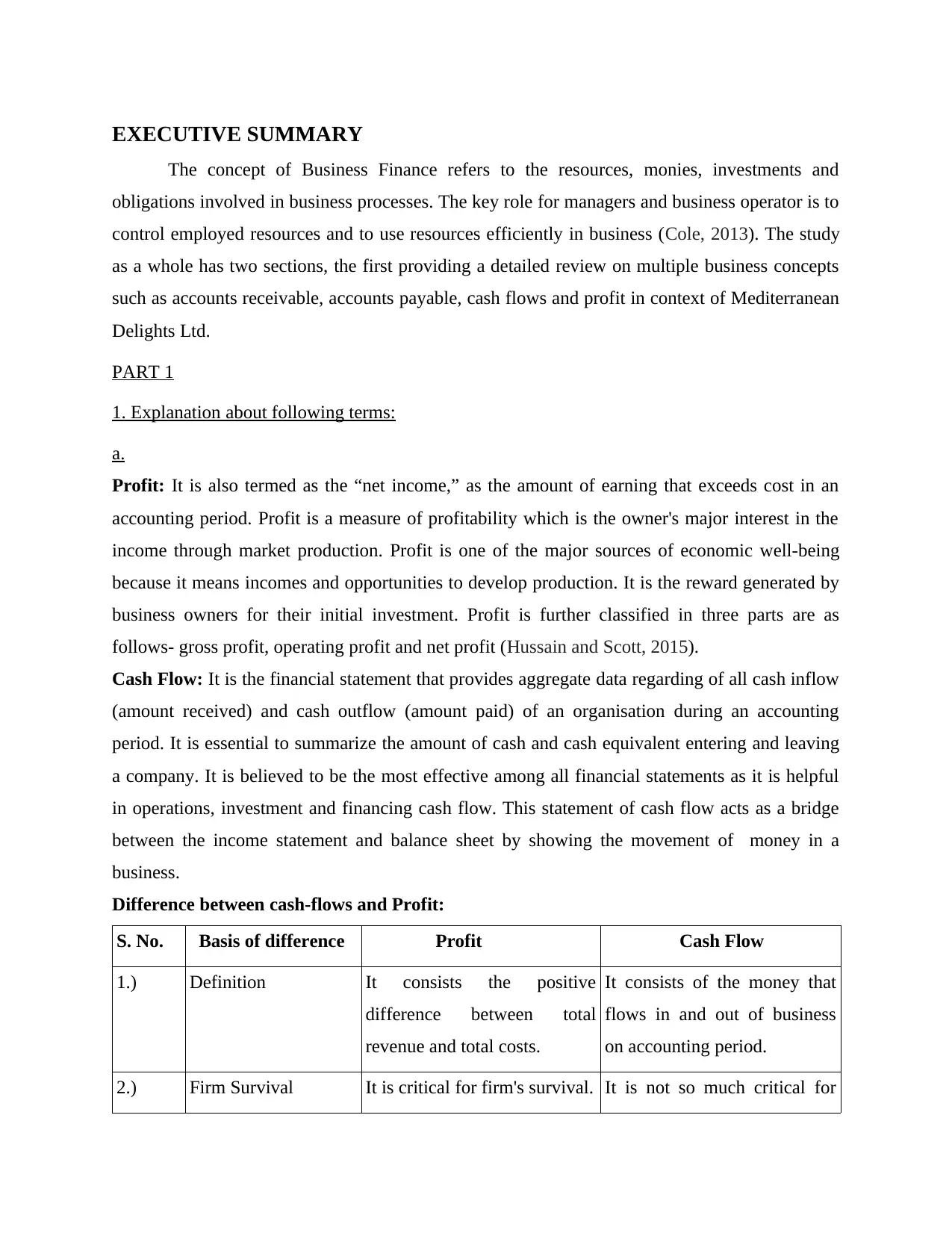

Difference between cash-flows and Profit:

S. No. Basis of difference Profit Cash Flow

1.) Definition It consists the positive

difference between total

revenue and total costs.

It consists of the money that

flows in and out of business

on accounting period.

2.) Firm Survival It is critical for firm's survival. It is not so much critical for

The concept of Business Finance refers to the resources, monies, investments and

obligations involved in business processes. The key role for managers and business operator is to

control employed resources and to use resources efficiently in business (Cole, 2013). The study

as a whole has two sections, the first providing a detailed review on multiple business concepts

such as accounts receivable, accounts payable, cash flows and profit in context of Mediterranean

Delights Ltd.

PART 1

1. Explanation about following terms:

a.

Profit: It is also termed as the “net income,” as the amount of earning that exceeds cost in an

accounting period. Profit is a measure of profitability which is the owner's major interest in the

income through market production. Profit is one of the major sources of economic well-being

because it means incomes and opportunities to develop production. It is the reward generated by

business owners for their initial investment. Profit is further classified in three parts are as

follows- gross profit, operating profit and net profit (Hussain and Scott, 2015).

Cash Flow: It is the financial statement that provides aggregate data regarding of all cash inflow

(amount received) and cash outflow (amount paid) of an organisation during an accounting

period. It is essential to summarize the amount of cash and cash equivalent entering and leaving

a company. It is believed to be the most effective among all financial statements as it is helpful

in operations, investment and financing cash flow. This statement of cash flow acts as a bridge

between the income statement and balance sheet by showing the movement of money in a

business.

Difference between cash-flows and Profit:

S. No. Basis of difference Profit Cash Flow

1.) Definition It consists the positive

difference between total

revenue and total costs.

It consists of the money that

flows in and out of business

on accounting period.

2.) Firm Survival It is critical for firm's survival. It is not so much critical for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the firm to survive as compare

to profit.

In business entity may also face a situation where it earned profits but also has negative

cash flows. Thus it is clear that profit shows company's profitability level while cash-flows

shows short-term liquidity situation of corporation (Jansen, 2016).

b.

Working Capital: It is also termed as Net Working Capital (NWC). It means the difference

between current assets and current liabilities. If these assets are less than these liabilities, its

working capital deficiency. The increase in assets from liabilities leads to working capital

inefficiency. This refers to an indicator of short-term financial position of an organisation and

also measures its overall efficiency (Wilson, 2016).

Receivables: The account receivables are the balance of money due to firm for goods and

services delivered to customers, still to be paid in future. It is any amount of money owed by

customers for purchases made on credit. Companies record account receivables as assets on their

balance sheets as its legal obligation for customer to pay debt. It is one of a series of accounting

transactions dealing with the billing of customer for goods and services that they have ordered to

be paid in future.

Inventories: It is also termed as merchandise. The inventory is an accounting terms refers to

goods (raw materials, work-in-progress and finished products) which are ready to be sold at

profit- margin. It can be measured through valuation method by First In First Out (FIFO), Last In

First Out (LIFO) and Average Cost (AVCO).

Payables: The account payables are the amount due to vendors or suppliers form goods and

services received are not yet paid. It is the money owed by business to its suppliers, shown as

liability on company's balance sheet. These are distinct from notes payable liabilities, which are

debts created by formal legal instrument documents (Keuper and Lueg, 2015).

2. Application of above discussed concepts in context of Mediterranean Delights Ltd:

Profit:

Mediterranean Delights Ltd has reported business's operating profit figures of amounting

£5million that reflects that net sum earned by company from business before providing any sum

of tax and loan or debt interests. This positive sum amount of business operating profit is

to profit.

In business entity may also face a situation where it earned profits but also has negative

cash flows. Thus it is clear that profit shows company's profitability level while cash-flows

shows short-term liquidity situation of corporation (Jansen, 2016).

b.

Working Capital: It is also termed as Net Working Capital (NWC). It means the difference

between current assets and current liabilities. If these assets are less than these liabilities, its

working capital deficiency. The increase in assets from liabilities leads to working capital

inefficiency. This refers to an indicator of short-term financial position of an organisation and

also measures its overall efficiency (Wilson, 2016).

Receivables: The account receivables are the balance of money due to firm for goods and

services delivered to customers, still to be paid in future. It is any amount of money owed by

customers for purchases made on credit. Companies record account receivables as assets on their

balance sheets as its legal obligation for customer to pay debt. It is one of a series of accounting

transactions dealing with the billing of customer for goods and services that they have ordered to

be paid in future.

Inventories: It is also termed as merchandise. The inventory is an accounting terms refers to

goods (raw materials, work-in-progress and finished products) which are ready to be sold at

profit- margin. It can be measured through valuation method by First In First Out (FIFO), Last In

First Out (LIFO) and Average Cost (AVCO).

Payables: The account payables are the amount due to vendors or suppliers form goods and

services received are not yet paid. It is the money owed by business to its suppliers, shown as

liability on company's balance sheet. These are distinct from notes payable liabilities, which are

debts created by formal legal instrument documents (Keuper and Lueg, 2015).

2. Application of above discussed concepts in context of Mediterranean Delights Ltd:

Profit:

Mediterranean Delights Ltd has reported business's operating profit figures of amounting

£5million that reflects that net sum earned by company from business before providing any sum

of tax and loan or debt interests. This positive sum amount of business operating profit is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indication that company is able to generate profits from its operations. Here if there is negative

amount of net profit after considering interest and taxes then it will not be a favourable sign for

corporation.

Cash-flow:

A net cash-flow amount of any organization is normally assessed on cash-concept basis

thus such a amount is ascertained merely by subtracting all expenses incurred in cash out of all

cash receipts and earnings. As MDL has stated cash flows (inflow) from additional debts of £ 2

million and here also an outflow as of payment of £ 8 million advance pay-off for exclusive

using rights of designs. Moreover, in case if entire turnover is assumed to be regarded as cash

sales only, then cash-flows resulting from sales is pound 50 million. Although owed to

inadequacy of data of actual sum of cash flows it is not possible to determine net sum of cash-

flows but a positive amount of cash-flows is important to deflect any upcoming unfavourable

position. As negative figure of cash flow is indication that corporation is facing

adverse/unpleasant liquidity situation (Kraemer-Eis and et.al., 2019).

Receivables: As per case study, MDL has crucial trade receivables titled: Delios Ltd and San

Pedro Ltd. This is also provided that corporation will get amounting £1.5 million as against an

purchase order placed by Delios Ltd. However sum of £2 million to be received through San

Pedro which is withheld as a consequence of undergoing dispute. Moreover, this is also a

noteworthy issue that this sum of £2 million is based on contingency thus it can't be regarded as

as sum of receivables balance in heading current assets.

Inventories:

It consists of sum balance of value of stock/inventories held for manufacturing, processing,

trading and resale purposes. No information about inventories was given herein the case

scenario, but here this is a significant fact that, because as consequence of dispute with San

Pedro as well as suspension of working involved, large quantities of raw items, materials and

processes goods are kept at company's London Site. This inventories items at such place would

be maintained or stored until the settlement of said dispute. Thus such inventories items can't be

reported in books due to this fact.

Payables: Trade-payables are a current liabilities, essential factors in working capital valuation.

Here, in the provided case situation of MDL, no clear trade-payable data has been provided, but

amount of net profit after considering interest and taxes then it will not be a favourable sign for

corporation.

Cash-flow:

A net cash-flow amount of any organization is normally assessed on cash-concept basis

thus such a amount is ascertained merely by subtracting all expenses incurred in cash out of all

cash receipts and earnings. As MDL has stated cash flows (inflow) from additional debts of £ 2

million and here also an outflow as of payment of £ 8 million advance pay-off for exclusive

using rights of designs. Moreover, in case if entire turnover is assumed to be regarded as cash

sales only, then cash-flows resulting from sales is pound 50 million. Although owed to

inadequacy of data of actual sum of cash flows it is not possible to determine net sum of cash-

flows but a positive amount of cash-flows is important to deflect any upcoming unfavourable

position. As negative figure of cash flow is indication that corporation is facing

adverse/unpleasant liquidity situation (Kraemer-Eis and et.al., 2019).

Receivables: As per case study, MDL has crucial trade receivables titled: Delios Ltd and San

Pedro Ltd. This is also provided that corporation will get amounting £1.5 million as against an

purchase order placed by Delios Ltd. However sum of £2 million to be received through San

Pedro which is withheld as a consequence of undergoing dispute. Moreover, this is also a

noteworthy issue that this sum of £2 million is based on contingency thus it can't be regarded as

as sum of receivables balance in heading current assets.

Inventories:

It consists of sum balance of value of stock/inventories held for manufacturing, processing,

trading and resale purposes. No information about inventories was given herein the case

scenario, but here this is a significant fact that, because as consequence of dispute with San

Pedro as well as suspension of working involved, large quantities of raw items, materials and

processes goods are kept at company's London Site. This inventories items at such place would

be maintained or stored until the settlement of said dispute. Thus such inventories items can't be

reported in books due to this fact.

Payables: Trade-payables are a current liabilities, essential factors in working capital valuation.

Here, in the provided case situation of MDL, no clear trade-payable data has been provided, but

debts estimates are provided, if all liabilities are believed to be current in nature, then such

number should be reported under heading of trade-payable (Kopnina and Blewitt, 2018).

Working Capital:

This is a valuable factor in operating business since it defines the overall operating level and

performance of the enterprise. In this case the sum of working capital of WILL Ltd may be

determined by subtracting the trade-payables balance from the accumulated cash and accounts

receivable amount. A negative sum of WC implies that an enterprise does not conduct its daily

business activities effectively.

3. Analysis and Recommendations:

From the above analysis of case study, the managers of MDL company can improve cash

flow through proper working capital management by the following steps, which are as described

under:-

Analyse Fixed and Variable Cost:- This analysis helps to manage working capital by

reducing the unwanted expense on these cost, as it improves liquidity for working capital.

It is also beneficial for the manager of MDL company in the changes of operating cash

flow.

Ensure proper usage of borrowings and loans funds: Here to improve cash-flows

company should ensure proper usage of loans and borrowings like short term borrowings

are used for fulfilment of short-term objectives and long-term debts should be utilised for

long term organisational goals (Minsky, 2016).

Selecting vendors offering discount:- The managers of MDL company has to maintain

good relationships with vendors as they offers discount. It is essential for managers in

cash flow crunch, as this relationship will have long way in receiving some leniency.

Monitoring account receivables and payables:- The managers of MDL company may

imply this track of inflow and outflow of cash, have strong collection of team to chase the

delinquent customers.

Resolve disputes with customers and vendors:- It is very important for managers of

MDL company to resolve the dispute of customers and vendors as soon as possible.

Receivables held up because of disputes are a major cause for many companies.

Use Up- to- date Financial Information:- It plays a very key role in managing the

current data and reports of financial information. The managers of MDL company has to

number should be reported under heading of trade-payable (Kopnina and Blewitt, 2018).

Working Capital:

This is a valuable factor in operating business since it defines the overall operating level and

performance of the enterprise. In this case the sum of working capital of WILL Ltd may be

determined by subtracting the trade-payables balance from the accumulated cash and accounts

receivable amount. A negative sum of WC implies that an enterprise does not conduct its daily

business activities effectively.

3. Analysis and Recommendations:

From the above analysis of case study, the managers of MDL company can improve cash

flow through proper working capital management by the following steps, which are as described

under:-

Analyse Fixed and Variable Cost:- This analysis helps to manage working capital by

reducing the unwanted expense on these cost, as it improves liquidity for working capital.

It is also beneficial for the manager of MDL company in the changes of operating cash

flow.

Ensure proper usage of borrowings and loans funds: Here to improve cash-flows

company should ensure proper usage of loans and borrowings like short term borrowings

are used for fulfilment of short-term objectives and long-term debts should be utilised for

long term organisational goals (Minsky, 2016).

Selecting vendors offering discount:- The managers of MDL company has to maintain

good relationships with vendors as they offers discount. It is essential for managers in

cash flow crunch, as this relationship will have long way in receiving some leniency.

Monitoring account receivables and payables:- The managers of MDL company may

imply this track of inflow and outflow of cash, have strong collection of team to chase the

delinquent customers.

Resolve disputes with customers and vendors:- It is very important for managers of

MDL company to resolve the dispute of customers and vendors as soon as possible.

Receivables held up because of disputes are a major cause for many companies.

Use Up- to- date Financial Information:- It plays a very key role in managing the

current data and reports of financial information. The managers of MDL company has to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maintain solvency, liquidity and profitability ratios on the periodic basis, to identify the

stability of firm in competitive market.

PART 2

EXECUTIVE SUMMARY

Second section of this study-report covers discussion on aims of framing various budgets

as well as analysis of appropriateness of traditional and alternative budgetary systems with

regards to Second Sight Plc. This section discusses primarily the value and usage of various

budgets strategies together with advantages and disadvantages.

1.

Purpose of framing budgets:

Budgets are quantitative and fiscal statement which provides detail summery of

organisations plans and policies for specific future period of time. In other words, budget is a

financial plan which is prepared for the purpose of analysing income and expense of an

organisation for specific period of time. It is a tool of financial accounting which helps

managers in decision making, planning process, and performance appraisal of their employees.

The process of preparing budget is known as budgeting (Sodeyfi, 2016). The main purpose of

preparation of budgets within in enterprise is to outline the performance and operational tasks of

enterprise as well as define short-term and long term targets, aims and business objectives. It

allows for an assessment of real financial results against projected operating results. This also

encourages an efficient comparison of the operating level of the organization with the focused or

budget level. Managers uses two type of approaches which are given as follows for the purpose

of making budget:

Traditional approach: This is a central and ordinary technique related to framing budgets for a

specific time frame used by business organisations. In this type of approach managers prepare

budget on the basis of last year's data. They set targets and built plans and polices on the basis of

last year budget.

Benefit: Key advantages of traditional budgeting is to provide strong framework to

business entity,it is easy for managers to make budget they did not need to waste their time on

researching new ideas or market plans. It is easy and quick process of preparing framework of

budget through traditional budgeting approach.

stability of firm in competitive market.

PART 2

EXECUTIVE SUMMARY

Second section of this study-report covers discussion on aims of framing various budgets

as well as analysis of appropriateness of traditional and alternative budgetary systems with

regards to Second Sight Plc. This section discusses primarily the value and usage of various

budgets strategies together with advantages and disadvantages.

1.

Purpose of framing budgets:

Budgets are quantitative and fiscal statement which provides detail summery of

organisations plans and policies for specific future period of time. In other words, budget is a

financial plan which is prepared for the purpose of analysing income and expense of an

organisation for specific period of time. It is a tool of financial accounting which helps

managers in decision making, planning process, and performance appraisal of their employees.

The process of preparing budget is known as budgeting (Sodeyfi, 2016). The main purpose of

preparation of budgets within in enterprise is to outline the performance and operational tasks of

enterprise as well as define short-term and long term targets, aims and business objectives. It

allows for an assessment of real financial results against projected operating results. This also

encourages an efficient comparison of the operating level of the organization with the focused or

budget level. Managers uses two type of approaches which are given as follows for the purpose

of making budget:

Traditional approach: This is a central and ordinary technique related to framing budgets for a

specific time frame used by business organisations. In this type of approach managers prepare

budget on the basis of last year's data. They set targets and built plans and polices on the basis of

last year budget.

Benefit: Key advantages of traditional budgeting is to provide strong framework to

business entity,it is easy for managers to make budget they did not need to waste their time on

researching new ideas or market plans. It is easy and quick process of preparing framework of

budget through traditional budgeting approach.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantage: It is not a reliable process of budgeting as plans are prepared on past

experiences. Budget are prepared on rigid basis thus manager unable to allocate resources to

each department (Shoup, 2017).

Modern or alternative approach of preparing budget: This involves set of techniques which

are used by organisations as per their specific and unique requirements and objectives. These are

also regarded as alternative budgeting approaches which enables managers to deal with different

circumstances and project performances in different terms. Followings are the methods of

preparing budget by applying modern alternative approaches, as follows:

Zero based budget: In this method managers preparing budget from initial level. They did not

consider past data for preparing budget. They started from zero level they analysis and research

overall environment then built budget on the basis of their study.

Advantage: They started with zero level thus budget provides accurate and reliable

information.

It provides flexibility manager can change their policies with changes in environment conditions.

Disadvantage: It is very expensive and time consuming process.

It is very risky process as success of budget is totally depends on how well expertise make

polices after any sing market condition.

Activity based budget: It is a method in which budgets are prepared after considering cost

incurred of each activity .It is tool of management accounting in which budgets are prepared on

the basis of allocation of resource.

Advantage: This method is useful for newly developed companies because their ration of

materials changes frequently. It will helps in cost cutting and proper utilization of resources.

Disadvantage: There is no clear basis has been defined under this approach to classify

activities so often times it generates ambiguous results (Soros, 2015).

Rolling budget: In this method budgets are prepared for short period of time . Production and

sales department use this method for preparing sales and purchase budget.

Advantage: This method is used to analysis performance of departments.

It provides flexibility as they are prepared for short term period and changes can be implement

easily.

experiences. Budget are prepared on rigid basis thus manager unable to allocate resources to

each department (Shoup, 2017).

Modern or alternative approach of preparing budget: This involves set of techniques which

are used by organisations as per their specific and unique requirements and objectives. These are

also regarded as alternative budgeting approaches which enables managers to deal with different

circumstances and project performances in different terms. Followings are the methods of

preparing budget by applying modern alternative approaches, as follows:

Zero based budget: In this method managers preparing budget from initial level. They did not

consider past data for preparing budget. They started from zero level they analysis and research

overall environment then built budget on the basis of their study.

Advantage: They started with zero level thus budget provides accurate and reliable

information.

It provides flexibility manager can change their policies with changes in environment conditions.

Disadvantage: It is very expensive and time consuming process.

It is very risky process as success of budget is totally depends on how well expertise make

polices after any sing market condition.

Activity based budget: It is a method in which budgets are prepared after considering cost

incurred of each activity .It is tool of management accounting in which budgets are prepared on

the basis of allocation of resource.

Advantage: This method is useful for newly developed companies because their ration of

materials changes frequently. It will helps in cost cutting and proper utilization of resources.

Disadvantage: There is no clear basis has been defined under this approach to classify

activities so often times it generates ambiguous results (Soros, 2015).

Rolling budget: In this method budgets are prepared for short period of time . Production and

sales department use this method for preparing sales and purchase budget.

Advantage: This method is used to analysis performance of departments.

It provides flexibility as they are prepared for short term period and changes can be implement

easily.

Disadvantage: Employees get demotivated due to changes of budget constantly. It is

very hard process it require expertise skills in individual because it is not easy to understand

causes of derivatives in producing product.

2.

As provided in case scenario of corporation Second Sight Plc is using traditional

approaches of budgeting that offers several limitations and besides that this has not so much

relevancy in dealing with business's different issues and problems. In this regard following is

discussion on multiple practical applications and impactions of above budgets, as below:

Rolling Budget: Enterprise Second Sight plc has achieved a revenue of amounting pound250

million that display that entity's operating scale is wider and have large number of business

functions. Therefore corporation is needed to project more reliable and relevant figures for

operating at such as a wider scale. This kind of budget enable corporation more updated, reliable

and relatable figure.

Zero-based Budget: Second Sight can apply this budget approach is used in for taking

momentous and quick decisions since it regard only current year values and figures. Managing

officials in corporation can employ this approach to form short-term targets and objectives (Van

Zon, 2016).

Activity based budget: The organization also uses this budget towards internal assessment as

well as appraisal by categorizing tasks such as Marketing, Accounting, Administration, HR etc.

Often, when working on quite a massive scale, the organization can identify any unnecessary

cost-making including non-cost-efficient operations through variances in activities budgets more

comprehensively.

3.

According to above analysis of various budget approaches and use of such methods in

company sense Second Sight it was found that both systems (i.e. conventional and

alternative/modern) can be implemented concurrently by the company. Traditional budgeting

framework allow organization to form estimations regarding aggregate performance and results

during particular period whereas alternative approaches provide assistance to managing staff to

enhance decision-making, controlling and strategical planning. Further use of various alternative

approaches/methods can lead to increase the relevancy and accuracy of projections within yearly

very hard process it require expertise skills in individual because it is not easy to understand

causes of derivatives in producing product.

2.

As provided in case scenario of corporation Second Sight Plc is using traditional

approaches of budgeting that offers several limitations and besides that this has not so much

relevancy in dealing with business's different issues and problems. In this regard following is

discussion on multiple practical applications and impactions of above budgets, as below:

Rolling Budget: Enterprise Second Sight plc has achieved a revenue of amounting pound250

million that display that entity's operating scale is wider and have large number of business

functions. Therefore corporation is needed to project more reliable and relevant figures for

operating at such as a wider scale. This kind of budget enable corporation more updated, reliable

and relatable figure.

Zero-based Budget: Second Sight can apply this budget approach is used in for taking

momentous and quick decisions since it regard only current year values and figures. Managing

officials in corporation can employ this approach to form short-term targets and objectives (Van

Zon, 2016).

Activity based budget: The organization also uses this budget towards internal assessment as

well as appraisal by categorizing tasks such as Marketing, Accounting, Administration, HR etc.

Often, when working on quite a massive scale, the organization can identify any unnecessary

cost-making including non-cost-efficient operations through variances in activities budgets more

comprehensively.

3.

According to above analysis of various budget approaches and use of such methods in

company sense Second Sight it was found that both systems (i.e. conventional and

alternative/modern) can be implemented concurrently by the company. Traditional budgeting

framework allow organization to form estimations regarding aggregate performance and results

during particular period whereas alternative approaches provide assistance to managing staff to

enhance decision-making, controlling and strategical planning. Further use of various alternative

approaches/methods can lead to increase the relevancy and accuracy of projections within yearly

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fiscal budget framed as per ordinary traditional approach. Moreover, these alternative budgets

can be used to resolve business issues and handle financial outcomes.

CONCLUSION

It's been outlined from the above report that business financing is essential in the

organizational sense as it includes various activities related to the distribution of funds. Having

various budgets within company causes an improvement in it's organizational and fiscal

performances.

can be used to resolve business issues and handle financial outcomes.

CONCLUSION

It's been outlined from the above report that business financing is essential in the

organizational sense as it includes various activities related to the distribution of funds. Having

various budgets within company causes an improvement in it's organizational and fiscal

performances.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Cole, R.A., 2013. What do we know about the capital structure of privately held US firms?

Evidence from the surveys of small business finance. Financial Management. 42(4), pp.

777-813.

Hussain, J. G. and Scott, J .M. eds., 2015. Research handbook on entrepreneurial finance.

Edward Elgar Publishing.

Jansen, K., 2016. External finance in Thailand’s development: An interpretation of Thailand’s

growth boom. Springer.

Keuper, F. and Lueg, K.E., 2015. Finance bundling and finance transformation. Springer

Gabler.

Kopnina, H. and Blewitt, J., 2018. Sustainable business: Key issues. Routledge.

Kraemer-Eis, and et.al., 2019. European Small Business Finance Outlook: December 2019 (No.

2019/61). EIF working paper.

Minsky, H., 2016. Can it happen again?: Essays on instability and finance. Routledge.

Shoup, C., 2017. Public finance. Routledge.

Sodeyfi, S., 2016. Review of literature on the nexus of financial leverage, product quality, &

business conditions. Journal of Economic & Management Perspectives. 10(2). pp.146-

150.

Soros, G., 2015. The alchemy of finance. John Wiley & Sons.

Van Zon, H., 2016. Globalized finance and varieties of capitalism. Basingstoke: Palgrave

Macmillan.

Wilson, N., 2016. ESOPs: their role in corporate finance and performance. Springer.

Books and Journals:

Cole, R.A., 2013. What do we know about the capital structure of privately held US firms?

Evidence from the surveys of small business finance. Financial Management. 42(4), pp.

777-813.

Hussain, J. G. and Scott, J .M. eds., 2015. Research handbook on entrepreneurial finance.

Edward Elgar Publishing.

Jansen, K., 2016. External finance in Thailand’s development: An interpretation of Thailand’s

growth boom. Springer.

Keuper, F. and Lueg, K.E., 2015. Finance bundling and finance transformation. Springer

Gabler.

Kopnina, H. and Blewitt, J., 2018. Sustainable business: Key issues. Routledge.

Kraemer-Eis, and et.al., 2019. European Small Business Finance Outlook: December 2019 (No.

2019/61). EIF working paper.

Minsky, H., 2016. Can it happen again?: Essays on instability and finance. Routledge.

Shoup, C., 2017. Public finance. Routledge.

Sodeyfi, S., 2016. Review of literature on the nexus of financial leverage, product quality, &

business conditions. Journal of Economic & Management Perspectives. 10(2). pp.146-

150.

Soros, G., 2015. The alchemy of finance. John Wiley & Sons.

Van Zon, H., 2016. Globalized finance and varieties of capitalism. Basingstoke: Palgrave

Macmillan.

Wilson, N., 2016. ESOPs: their role in corporate finance and performance. Springer.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.