Hospitality Finance: Sources of Funding, Cost Control, and Ratios

VerifiedAdded on 2020/06/04

|12

|2914

|33

Report

AI Summary

This report provides a comprehensive overview of financial management within the hospitality industry. It begins by exploring various sources of funding, including personal investment, venture capital, bank loans, and retained earnings, and discusses methods for generating income, such as commission, sales promotion, and sponsorship. The report then delves into cost elements, including material, direct labor, and indirect expenses, and explains gross profit percentages and selling price calculations. Methods for controlling stock and cash are also examined. The report further assesses the structure of a trial balance, measures business accounts, and discusses adjustments and notes. It also covers the process and purpose of budgetary control, including variance analysis. Financial ratios are calculated and analyzed to interpret historical business performance, offering insights into future management strategies. Finally, the report categorizes costs, calculates contribution per product, and discusses short-term management decisions based on profit/loss potential and break-even calculations, ultimately providing a detailed analysis of finance in hospitality.

FINANCE IN HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funding available to business and industries.......................................................1

1.2 Measure the contribution made by a range of methods for generating income....................2

TASK 2............................................................................................................................................2

2.1 Elements of cost, gross profit percentages and selling price for the product........................2

(B) Gross profit percentage and selling price.............................................................................3

2.2 Methods of controlling stock and cash in a business and service environment....................3

TASK 3............................................................................................................................................4

3.1 Assess the sources and structure of the trial balance............................................................4

3.2 measure business accounts, adjustments and notes...............................................................4

3.3 The process and purpose of budgetary control.....................................................................6

3.4 Variance analysis from budgeted and actual figures offering suggestion for future

management................................................................................................................................6

TASK 4............................................................................................................................................7

4.1 calculation and analysis of ratio to offer a consistent interpretation of historical business

performance.................................................................................................................................7

4.2 appropriate Future management strategies for a given business and service operation........7

TASK 5............................................................................................................................................8

5.1 Categorise costs as fixed, variable and semi-variable for a given scenario..........................8

5.2 Calculation of contribution per product/customer and explain the cost profit/ volume

relation.........................................................................................................................................8

5.3 Short term management decision based upon profit loss potential and break-even

calculation...................................................................................................................................8

CONCLUSION................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funding available to business and industries.......................................................1

1.2 Measure the contribution made by a range of methods for generating income....................2

TASK 2............................................................................................................................................2

2.1 Elements of cost, gross profit percentages and selling price for the product........................2

(B) Gross profit percentage and selling price.............................................................................3

2.2 Methods of controlling stock and cash in a business and service environment....................3

TASK 3............................................................................................................................................4

3.1 Assess the sources and structure of the trial balance............................................................4

3.2 measure business accounts, adjustments and notes...............................................................4

3.3 The process and purpose of budgetary control.....................................................................6

3.4 Variance analysis from budgeted and actual figures offering suggestion for future

management................................................................................................................................6

TASK 4............................................................................................................................................7

4.1 calculation and analysis of ratio to offer a consistent interpretation of historical business

performance.................................................................................................................................7

4.2 appropriate Future management strategies for a given business and service operation........7

TASK 5............................................................................................................................................8

5.1 Categorise costs as fixed, variable and semi-variable for a given scenario..........................8

5.2 Calculation of contribution per product/customer and explain the cost profit/ volume

relation.........................................................................................................................................8

5.3 Short term management decision based upon profit loss potential and break-even

calculation...................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is one of the important resources with in organisational context. Management

and control of financial resources is covered in financial management. Concept of financial

resources management is defined in hospitality sector (Xiao, O'Neill and Mattila, 2012). This

project is prepared to explain depth knowledge and practical overview of accounting techniques

which are used to control cost and profit. This helps to understand the control system and income

generation methods. It covers the use of various financial ratios in analysing subject to

interpreter and bifurcate the data.

Methods of pricing and management information are defined in hospitality industry. It

will help to gain a fundamental understanding in the hospitality industry also defined in this

context. Understand the management and operation in order to determine the context.

TASK 1

1.1 Sources of funding available to business and industries

There are type of sources of funds available by which organisation become eligible to

generate funds such as

Funds for New Business:

Personal investment: this is considered a major sources which is invested to generate

funds for personal income and revenues. Funds and cash are invested at initial stage with the as a

capital and utilised for acquiring assets (WangChen and Chen, 2012).

Advantages: there is no any interest charges and expense need to be paid for

externals or long term debts.

Disadvantage: expert knowledge and advise remain lack behind in this source

Venture capital: this is also one of the type of funding which is made by investing

private equity with in small growing and developing organisations and firms. Enhancing profit

capability and revenue structure is major motive of this funding (Sahida and et. al., 2011.).

Advantages: it helps to analyse the entrepreneur skills which build company's

image and investor management support.

Disadvantages: there is a lake of control is found in this source of funding

Funds Existing Business

Bank loan: this is one of the common source of fund which is generally used by business

and organisations.

1

Finance is one of the important resources with in organisational context. Management

and control of financial resources is covered in financial management. Concept of financial

resources management is defined in hospitality sector (Xiao, O'Neill and Mattila, 2012). This

project is prepared to explain depth knowledge and practical overview of accounting techniques

which are used to control cost and profit. This helps to understand the control system and income

generation methods. It covers the use of various financial ratios in analysing subject to

interpreter and bifurcate the data.

Methods of pricing and management information are defined in hospitality industry. It

will help to gain a fundamental understanding in the hospitality industry also defined in this

context. Understand the management and operation in order to determine the context.

TASK 1

1.1 Sources of funding available to business and industries

There are type of sources of funds available by which organisation become eligible to

generate funds such as

Funds for New Business:

Personal investment: this is considered a major sources which is invested to generate

funds for personal income and revenues. Funds and cash are invested at initial stage with the as a

capital and utilised for acquiring assets (WangChen and Chen, 2012).

Advantages: there is no any interest charges and expense need to be paid for

externals or long term debts.

Disadvantage: expert knowledge and advise remain lack behind in this source

Venture capital: this is also one of the type of funding which is made by investing

private equity with in small growing and developing organisations and firms. Enhancing profit

capability and revenue structure is major motive of this funding (Sahida and et. al., 2011.).

Advantages: it helps to analyse the entrepreneur skills which build company's

image and investor management support.

Disadvantages: there is a lake of control is found in this source of funding

Funds Existing Business

Bank loan: this is one of the common source of fund which is generally used by business

and organisations.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages: Procedure of getting loans and advances are find easier.

Disadvantages: high interest rates and expenses is one of the disadvantage of

bank loans

Debentures: this is considered a type of loans which contains a fixed rate of interest.

Advantages: it retain the control and management with in the organisation.

Disadvantage: Organisation has to pay interest on debentures even after not

gaining profits and revenues.

Retain earning: this is considered as a part and share of profit which is utilised by

organisation.

Advantages: It provides stable structure and prevent extra cost of organisation.

Disadvantages: ratio of retain earnings remain differ every year.

1.2 Measure the contribution made by a range of methods for generating income

Various type of methods are used subject to generating income with in organisational

context such as:

Commission: this is one of the essential method which plays vital role in order to

enhance profitability and revenue structure of organisation. Sales person are appointed for

enhancing sales on certain percentage of commission share. Straight commission plans is one o f

the essential method which is used by organisation (Moutinho, 2011).

Sales promotion: this method or techniques helps to emerge the sales and profitability

by distributing free samples, services after sales, free trial services, free gifts and offering

impressive and attracting pricing offers. This is considered one of the effective method subject to

gain more customer attraction and interest.

Sponsorship: this techniques is used by distribution channels and sponsors. This

technique contains various activities such as act, activities, events and campaigns for enhancing

sales records. Sponsors helps to analyse the profitability and revenue of organisation.

TASK 2

2.1 Elements of cost, gross profit percentages and selling price for the product

Cost: In organisational context cost is considered as a sum of money incurred to fulfil

production needs and requirement. This is considered as a cost and expenses made for direct

material, direct labour, direct expenses and overheads (Hoque, 2013).

Major elements of cost are discussed in this context:

2

Disadvantages: high interest rates and expenses is one of the disadvantage of

bank loans

Debentures: this is considered a type of loans which contains a fixed rate of interest.

Advantages: it retain the control and management with in the organisation.

Disadvantage: Organisation has to pay interest on debentures even after not

gaining profits and revenues.

Retain earning: this is considered as a part and share of profit which is utilised by

organisation.

Advantages: It provides stable structure and prevent extra cost of organisation.

Disadvantages: ratio of retain earnings remain differ every year.

1.2 Measure the contribution made by a range of methods for generating income

Various type of methods are used subject to generating income with in organisational

context such as:

Commission: this is one of the essential method which plays vital role in order to

enhance profitability and revenue structure of organisation. Sales person are appointed for

enhancing sales on certain percentage of commission share. Straight commission plans is one o f

the essential method which is used by organisation (Moutinho, 2011).

Sales promotion: this method or techniques helps to emerge the sales and profitability

by distributing free samples, services after sales, free trial services, free gifts and offering

impressive and attracting pricing offers. This is considered one of the effective method subject to

gain more customer attraction and interest.

Sponsorship: this techniques is used by distribution channels and sponsors. This

technique contains various activities such as act, activities, events and campaigns for enhancing

sales records. Sponsors helps to analyse the profitability and revenue of organisation.

TASK 2

2.1 Elements of cost, gross profit percentages and selling price for the product

Cost: In organisational context cost is considered as a sum of money incurred to fulfil

production needs and requirement. This is considered as a cost and expenses made for direct

material, direct labour, direct expenses and overheads (Hoque, 2013).

Major elements of cost are discussed in this context:

2

Material: components, elements and stocks which are considered essential subject to

manufacturing and production units. Direct material is also considered essential in order to

determine enhance productivity of organisation. There are two type of material are found in

organisational context such as indirect material, direct martial. For example petroleum products

are used as raw materiel to make Vaseline (Bowie, Buttle and Brookes, 2016).

Direct labour: it is considered as a physical and mental efforts in consideration of

payment. A labour which is incurred directly with in operations and production of services are

considered as direct labour.

Indirect Expenses: expenses and cost which do not remain the part of manufacturing

and production process is called as indirect expenses. It is also considered as indirect overheads.

Production overheads, selling and administration expenses and distribution expenses are some

examples of indirect expenses.

(B) Gross profit percentage and selling price

Gross profit percentage: this is calculated as gross profit to sales. This is used to

measure profitability of organisation. It is calculated as (GPP = gross profit / total sales)* 100

Selling price + Cost of goods sold + Mark up.

2.2 Methods of controlling stock and cash in a business and service environment

Cash control method

There are two type of methods are majorly used to control cost such as

Implementation of cash handling policies

Accountability form

Set cash flow targets

Stock controlling methods

Just in time: this method is basically used to analyse actual quantity of stock.

Formulation off inventory budgets: Making budgets in order to determine monthly and

yearly requirement of stock.

Perpetual inventory system: it is used to track volume and value of inventory.

3

manufacturing and production units. Direct material is also considered essential in order to

determine enhance productivity of organisation. There are two type of material are found in

organisational context such as indirect material, direct martial. For example petroleum products

are used as raw materiel to make Vaseline (Bowie, Buttle and Brookes, 2016).

Direct labour: it is considered as a physical and mental efforts in consideration of

payment. A labour which is incurred directly with in operations and production of services are

considered as direct labour.

Indirect Expenses: expenses and cost which do not remain the part of manufacturing

and production process is called as indirect expenses. It is also considered as indirect overheads.

Production overheads, selling and administration expenses and distribution expenses are some

examples of indirect expenses.

(B) Gross profit percentage and selling price

Gross profit percentage: this is calculated as gross profit to sales. This is used to

measure profitability of organisation. It is calculated as (GPP = gross profit / total sales)* 100

Selling price + Cost of goods sold + Mark up.

2.2 Methods of controlling stock and cash in a business and service environment

Cash control method

There are two type of methods are majorly used to control cost such as

Implementation of cash handling policies

Accountability form

Set cash flow targets

Stock controlling methods

Just in time: this method is basically used to analyse actual quantity of stock.

Formulation off inventory budgets: Making budgets in order to determine monthly and

yearly requirement of stock.

Perpetual inventory system: it is used to track volume and value of inventory.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

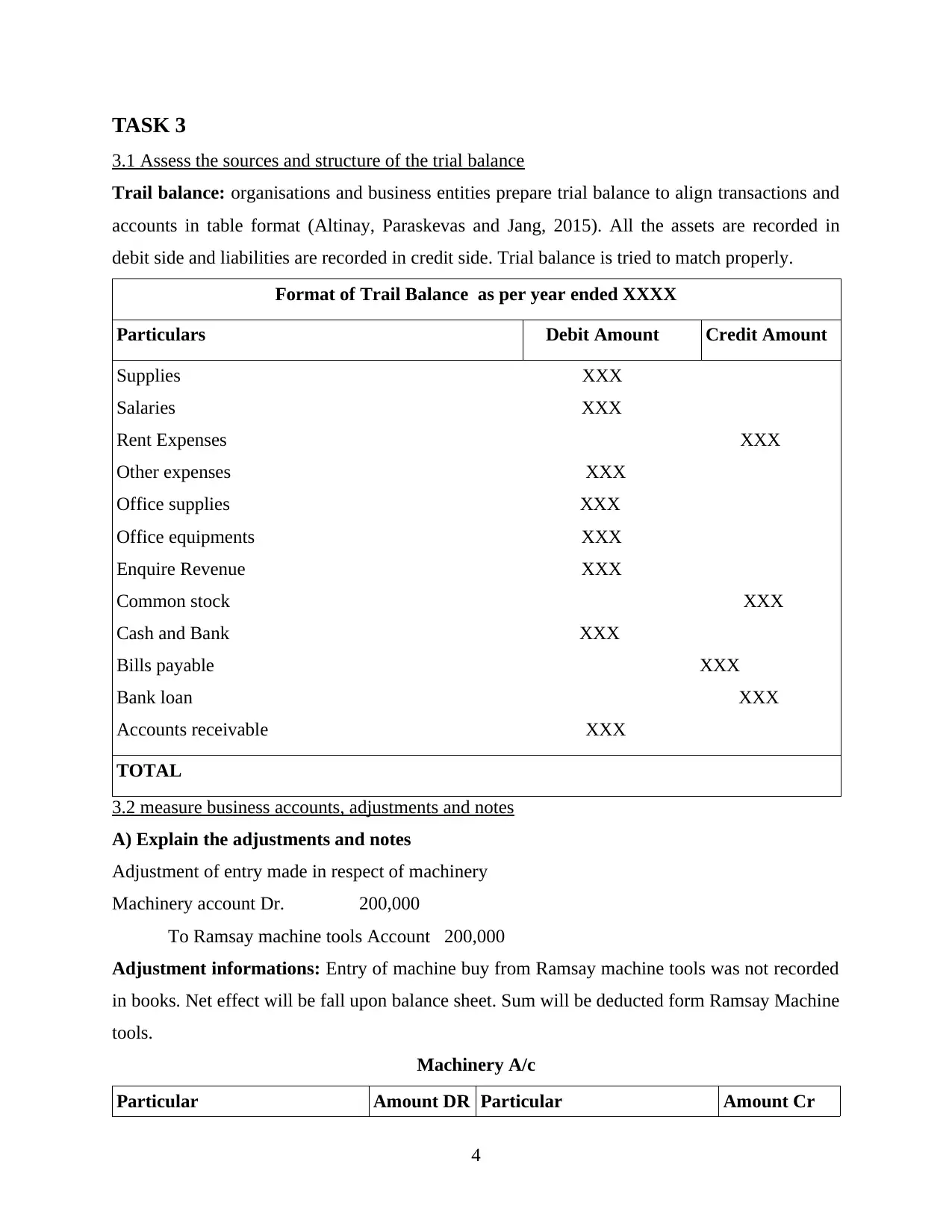

3.1 Assess the sources and structure of the trial balance

Trail balance: organisations and business entities prepare trial balance to align transactions and

accounts in table format (Altinay, Paraskevas and Jang, 2015). All the assets are recorded in

debit side and liabilities are recorded in credit side. Trial balance is tried to match properly.

Format of Trail Balance as per year ended XXXX

Particulars Debit Amount Credit Amount

Supplies XXX

Salaries XXX

Rent Expenses XXX

Other expenses XXX

Office supplies XXX

Office equipments XXX

Enquire Revenue XXX

Common stock XXX

Cash and Bank XXX

Bills payable XXX

Bank loan XXX

Accounts receivable XXX

TOTAL

3.2 measure business accounts, adjustments and notes

A) Explain the adjustments and notes

Adjustment of entry made in respect of machinery

Machinery account Dr. 200,000

To Ramsay machine tools Account 200,000

Adjustment informations: Entry of machine buy from Ramsay machine tools was not recorded

in books. Net effect will be fall upon balance sheet. Sum will be deducted form Ramsay Machine

tools.

Machinery A/c

Particular Amount DR Particular Amount Cr

4

3.1 Assess the sources and structure of the trial balance

Trail balance: organisations and business entities prepare trial balance to align transactions and

accounts in table format (Altinay, Paraskevas and Jang, 2015). All the assets are recorded in

debit side and liabilities are recorded in credit side. Trial balance is tried to match properly.

Format of Trail Balance as per year ended XXXX

Particulars Debit Amount Credit Amount

Supplies XXX

Salaries XXX

Rent Expenses XXX

Other expenses XXX

Office supplies XXX

Office equipments XXX

Enquire Revenue XXX

Common stock XXX

Cash and Bank XXX

Bills payable XXX

Bank loan XXX

Accounts receivable XXX

TOTAL

3.2 measure business accounts, adjustments and notes

A) Explain the adjustments and notes

Adjustment of entry made in respect of machinery

Machinery account Dr. 200,000

To Ramsay machine tools Account 200,000

Adjustment informations: Entry of machine buy from Ramsay machine tools was not recorded

in books. Net effect will be fall upon balance sheet. Sum will be deducted form Ramsay Machine

tools.

Machinery A/c

Particular Amount DR Particular Amount Cr

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

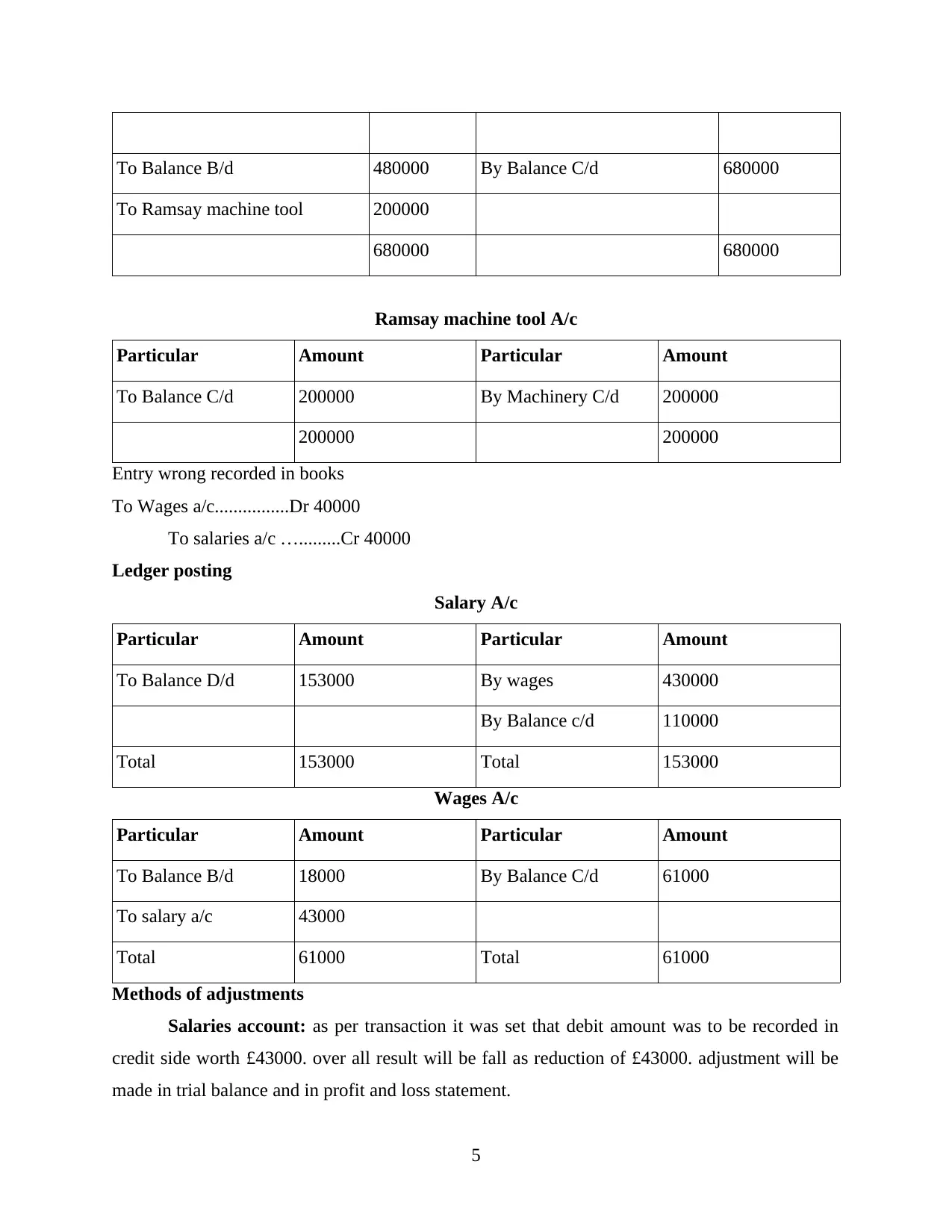

To Balance B/d 480000 By Balance C/d 680000

To Ramsay machine tool 200000

680000 680000

Ramsay machine tool A/c

Particular Amount Particular Amount

To Balance C/d 200000 By Machinery C/d 200000

200000 200000

Entry wrong recorded in books

To Wages a/c................Dr 40000

To salaries a/c ….........Cr 40000

Ledger posting

Salary A/c

Particular Amount Particular Amount

To Balance D/d 153000 By wages 430000

By Balance c/d 110000

Total 153000 Total 153000

Wages A/c

Particular Amount Particular Amount

To Balance B/d 18000 By Balance C/d 61000

To salary a/c 43000

Total 61000 Total 61000

Methods of adjustments

Salaries account: as per transaction it was set that debit amount was to be recorded in

credit side worth £43000. over all result will be fall as reduction of £43000. adjustment will be

made in trial balance and in profit and loss statement.

5

To Ramsay machine tool 200000

680000 680000

Ramsay machine tool A/c

Particular Amount Particular Amount

To Balance C/d 200000 By Machinery C/d 200000

200000 200000

Entry wrong recorded in books

To Wages a/c................Dr 40000

To salaries a/c ….........Cr 40000

Ledger posting

Salary A/c

Particular Amount Particular Amount

To Balance D/d 153000 By wages 430000

By Balance c/d 110000

Total 153000 Total 153000

Wages A/c

Particular Amount Particular Amount

To Balance B/d 18000 By Balance C/d 61000

To salary a/c 43000

Total 61000 Total 61000

Methods of adjustments

Salaries account: as per transaction it was set that debit amount was to be recorded in

credit side worth £43000. over all result will be fall as reduction of £43000. adjustment will be

made in trial balance and in profit and loss statement.

5

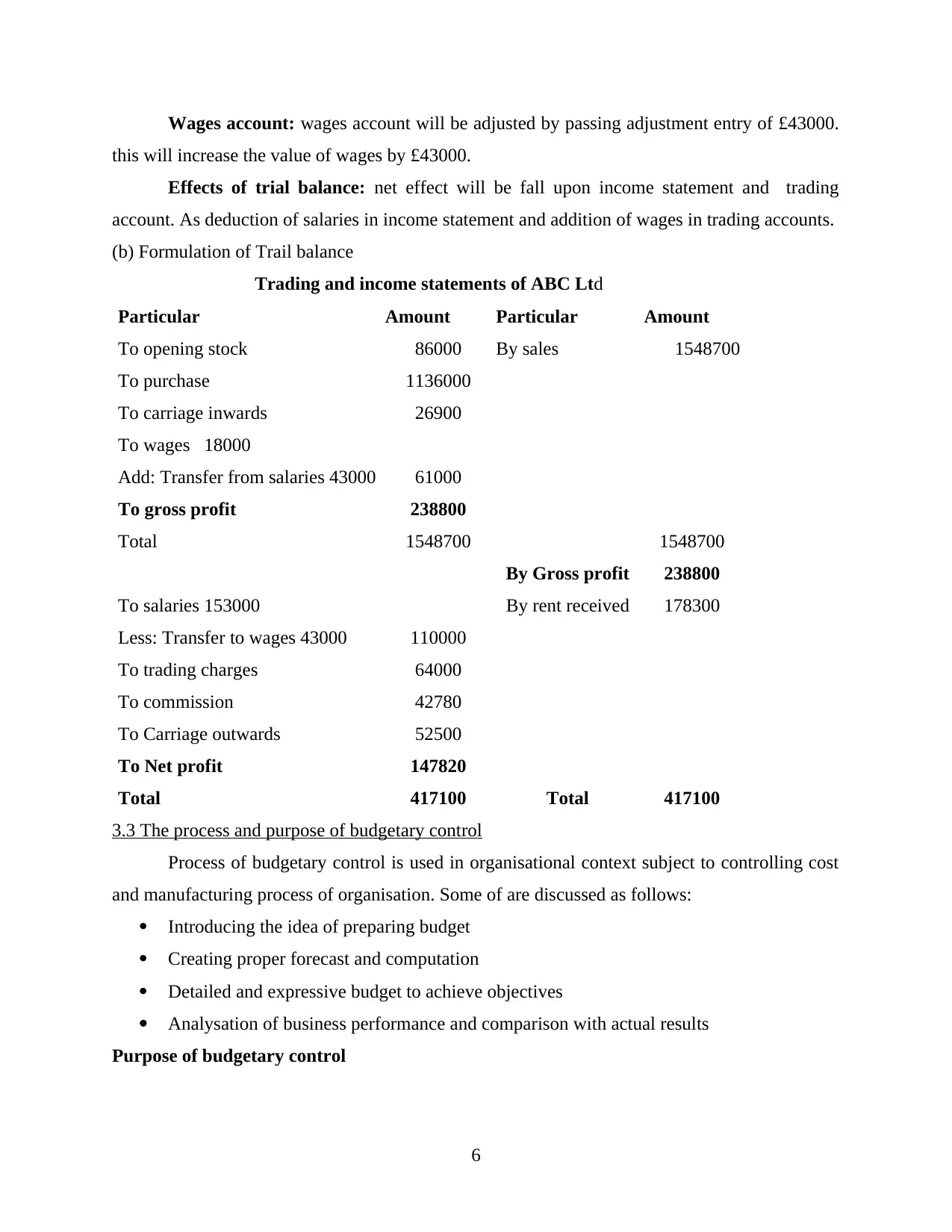

Wages account: wages account will be adjusted by passing adjustment entry of £43000.

this will increase the value of wages by £43000.

Effects of trial balance: net effect will be fall upon income statement and trading

account. As deduction of salaries in income statement and addition of wages in trading accounts.

(b) Formulation of Trail balance

Trading and income statements of ABC Ltd

Particular Amount Particular Amount

To opening stock 86000 By sales 1548700

To purchase 1136000

To carriage inwards 26900

To wages 18000

Add: Transfer from salaries 43000 61000

To gross profit 238800

Total 1548700 1548700

By Gross profit 238800

To salaries 153000 By rent received 178300

Less: Transfer to wages 43000 110000

To trading charges 64000

To commission 42780

To Carriage outwards 52500

To Net profit 147820

Total 417100 Total 417100

3.3 The process and purpose of budgetary control

Process of budgetary control is used in organisational context subject to controlling cost

and manufacturing process of organisation. Some of are discussed as follows:

Introducing the idea of preparing budget

Creating proper forecast and computation

Detailed and expressive budget to achieve objectives

Analysation of business performance and comparison with actual results

Purpose of budgetary control

6

this will increase the value of wages by £43000.

Effects of trial balance: net effect will be fall upon income statement and trading

account. As deduction of salaries in income statement and addition of wages in trading accounts.

(b) Formulation of Trail balance

Trading and income statements of ABC Ltd

Particular Amount Particular Amount

To opening stock 86000 By sales 1548700

To purchase 1136000

To carriage inwards 26900

To wages 18000

Add: Transfer from salaries 43000 61000

To gross profit 238800

Total 1548700 1548700

By Gross profit 238800

To salaries 153000 By rent received 178300

Less: Transfer to wages 43000 110000

To trading charges 64000

To commission 42780

To Carriage outwards 52500

To Net profit 147820

Total 417100 Total 417100

3.3 The process and purpose of budgetary control

Process of budgetary control is used in organisational context subject to controlling cost

and manufacturing process of organisation. Some of are discussed as follows:

Introducing the idea of preparing budget

Creating proper forecast and computation

Detailed and expressive budget to achieve objectives

Analysation of business performance and comparison with actual results

Purpose of budgetary control

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

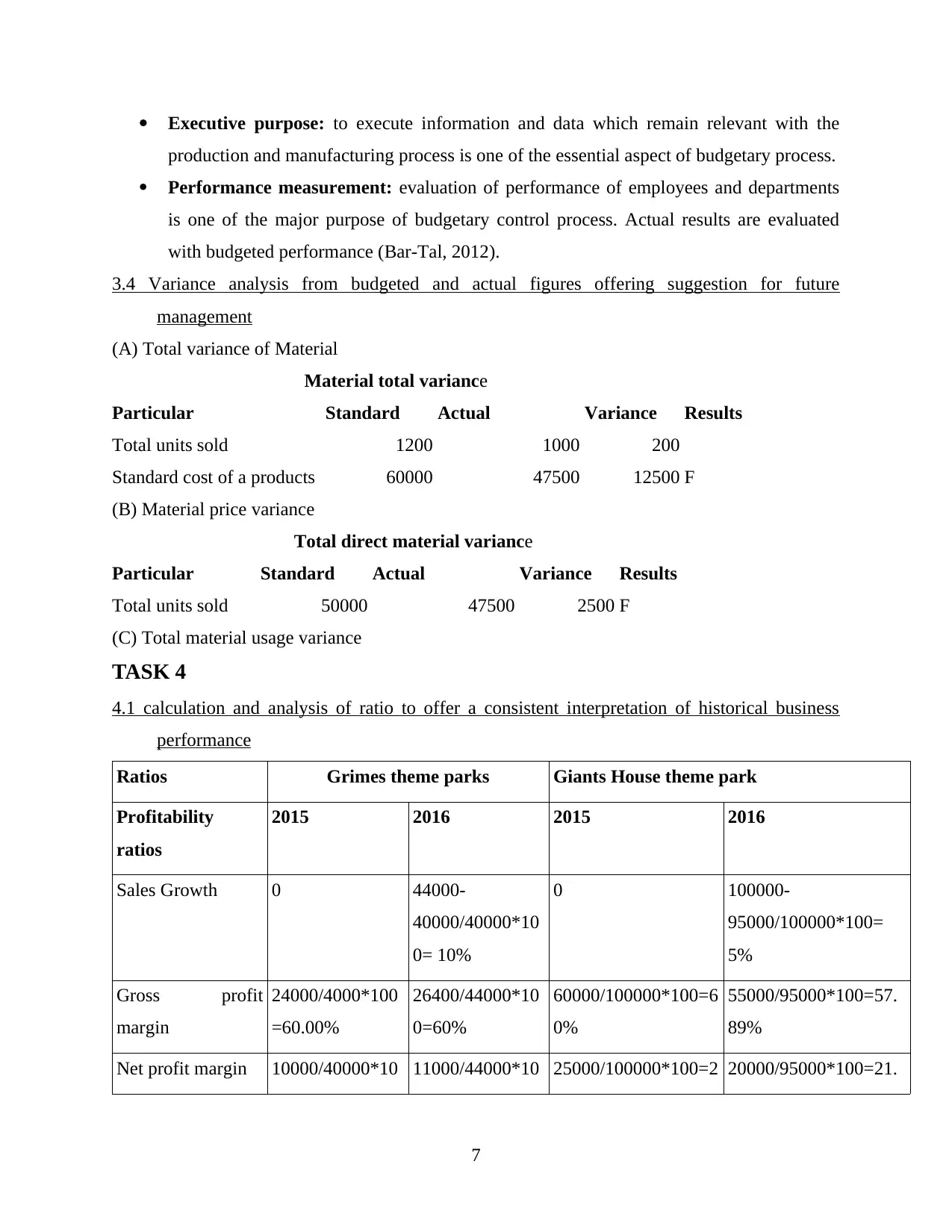

Executive purpose: to execute information and data which remain relevant with the

production and manufacturing process is one of the essential aspect of budgetary process.

Performance measurement: evaluation of performance of employees and departments

is one of the major purpose of budgetary control process. Actual results are evaluated

with budgeted performance (Bar-Tal, 2012).

3.4 Variance analysis from budgeted and actual figures offering suggestion for future

management

(A) Total variance of Material

Material total variance

Particular Standard Actual Variance Results

Total units sold 1200 1000 200

Standard cost of a products 60000 47500 12500 F

(B) Material price variance

Total direct material variance

Particular Standard Actual Variance Results

Total units sold 50000 47500 2500 F

(C) Total material usage variance

TASK 4

4.1 calculation and analysis of ratio to offer a consistent interpretation of historical business

performance

Ratios Grimes theme parks Giants House theme park

Profitability

ratios

2015 2016 2015 2016

Sales Growth 0 44000-

40000/40000*10

0= 10%

0 100000-

95000/100000*100=

5%

Gross profit

margin

24000/4000*100

=60.00%

26400/44000*10

0=60%

60000/100000*100=6

0%

55000/95000*100=57.

89%

Net profit margin 10000/40000*10 11000/44000*10 25000/100000*100=2 20000/95000*100=21.

7

production and manufacturing process is one of the essential aspect of budgetary process.

Performance measurement: evaluation of performance of employees and departments

is one of the major purpose of budgetary control process. Actual results are evaluated

with budgeted performance (Bar-Tal, 2012).

3.4 Variance analysis from budgeted and actual figures offering suggestion for future

management

(A) Total variance of Material

Material total variance

Particular Standard Actual Variance Results

Total units sold 1200 1000 200

Standard cost of a products 60000 47500 12500 F

(B) Material price variance

Total direct material variance

Particular Standard Actual Variance Results

Total units sold 50000 47500 2500 F

(C) Total material usage variance

TASK 4

4.1 calculation and analysis of ratio to offer a consistent interpretation of historical business

performance

Ratios Grimes theme parks Giants House theme park

Profitability

ratios

2015 2016 2015 2016

Sales Growth 0 44000-

40000/40000*10

0= 10%

0 100000-

95000/100000*100=

5%

Gross profit

margin

24000/4000*100

=60.00%

26400/44000*10

0=60%

60000/100000*100=6

0%

55000/95000*100=57.

89%

Net profit margin 10000/40000*10 11000/44000*10 25000/100000*100=2 20000/95000*100=21.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

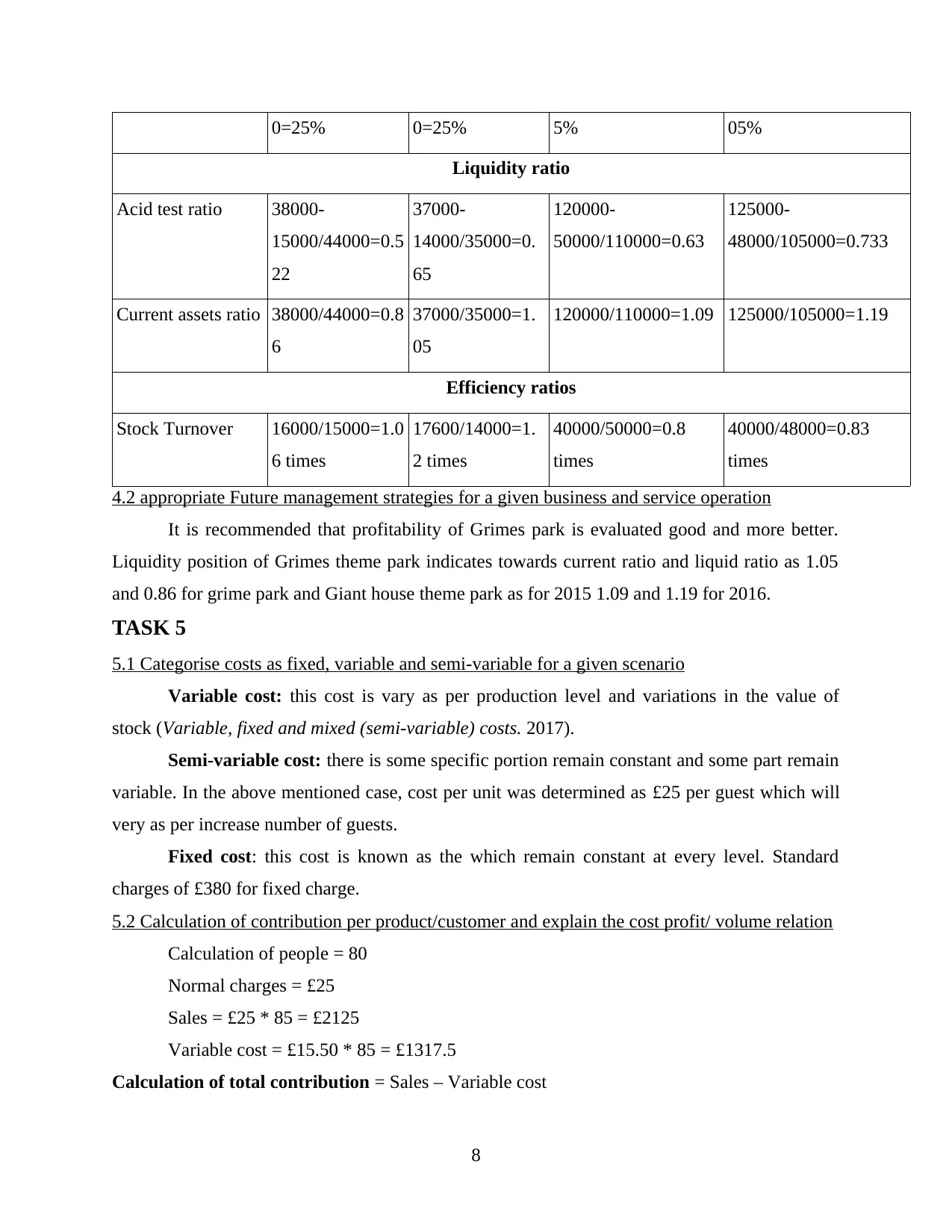

0=25% 0=25% 5% 05%

Liquidity ratio

Acid test ratio 38000-

15000/44000=0.5

22

37000-

14000/35000=0.

65

120000-

50000/110000=0.63

125000-

48000/105000=0.733

Current assets ratio 38000/44000=0.8

6

37000/35000=1.

05

120000/110000=1.09 125000/105000=1.19

Efficiency ratios

Stock Turnover 16000/15000=1.0

6 times

17600/14000=1.

2 times

40000/50000=0.8

times

40000/48000=0.83

times

4.2 appropriate Future management strategies for a given business and service operation

It is recommended that profitability of Grimes park is evaluated good and more better.

Liquidity position of Grimes theme park indicates towards current ratio and liquid ratio as 1.05

and 0.86 for grime park and Giant house theme park as for 2015 1.09 and 1.19 for 2016.

TASK 5

5.1 Categorise costs as fixed, variable and semi-variable for a given scenario

Variable cost: this cost is vary as per production level and variations in the value of

stock (Variable, fixed and mixed (semi-variable) costs. 2017).

Semi-variable cost: there is some specific portion remain constant and some part remain

variable. In the above mentioned case, cost per unit was determined as £25 per guest which will

very as per increase number of guests.

Fixed cost: this cost is known as the which remain constant at every level. Standard

charges of £380 for fixed charge.

5.2 Calculation of contribution per product/customer and explain the cost profit/ volume relation

Calculation of people = 80

Normal charges = £25

Sales = £25 * 85 = £2125

Variable cost = £15.50 * 85 = £1317.5

Calculation of total contribution = Sales – Variable cost

8

Liquidity ratio

Acid test ratio 38000-

15000/44000=0.5

22

37000-

14000/35000=0.

65

120000-

50000/110000=0.63

125000-

48000/105000=0.733

Current assets ratio 38000/44000=0.8

6

37000/35000=1.

05

120000/110000=1.09 125000/105000=1.19

Efficiency ratios

Stock Turnover 16000/15000=1.0

6 times

17600/14000=1.

2 times

40000/50000=0.8

times

40000/48000=0.83

times

4.2 appropriate Future management strategies for a given business and service operation

It is recommended that profitability of Grimes park is evaluated good and more better.

Liquidity position of Grimes theme park indicates towards current ratio and liquid ratio as 1.05

and 0.86 for grime park and Giant house theme park as for 2015 1.09 and 1.19 for 2016.

TASK 5

5.1 Categorise costs as fixed, variable and semi-variable for a given scenario

Variable cost: this cost is vary as per production level and variations in the value of

stock (Variable, fixed and mixed (semi-variable) costs. 2017).

Semi-variable cost: there is some specific portion remain constant and some part remain

variable. In the above mentioned case, cost per unit was determined as £25 per guest which will

very as per increase number of guests.

Fixed cost: this cost is known as the which remain constant at every level. Standard

charges of £380 for fixed charge.

5.2 Calculation of contribution per product/customer and explain the cost profit/ volume relation

Calculation of people = 80

Normal charges = £25

Sales = £25 * 85 = £2125

Variable cost = £15.50 * 85 = £1317.5

Calculation of total contribution = Sales – Variable cost

8

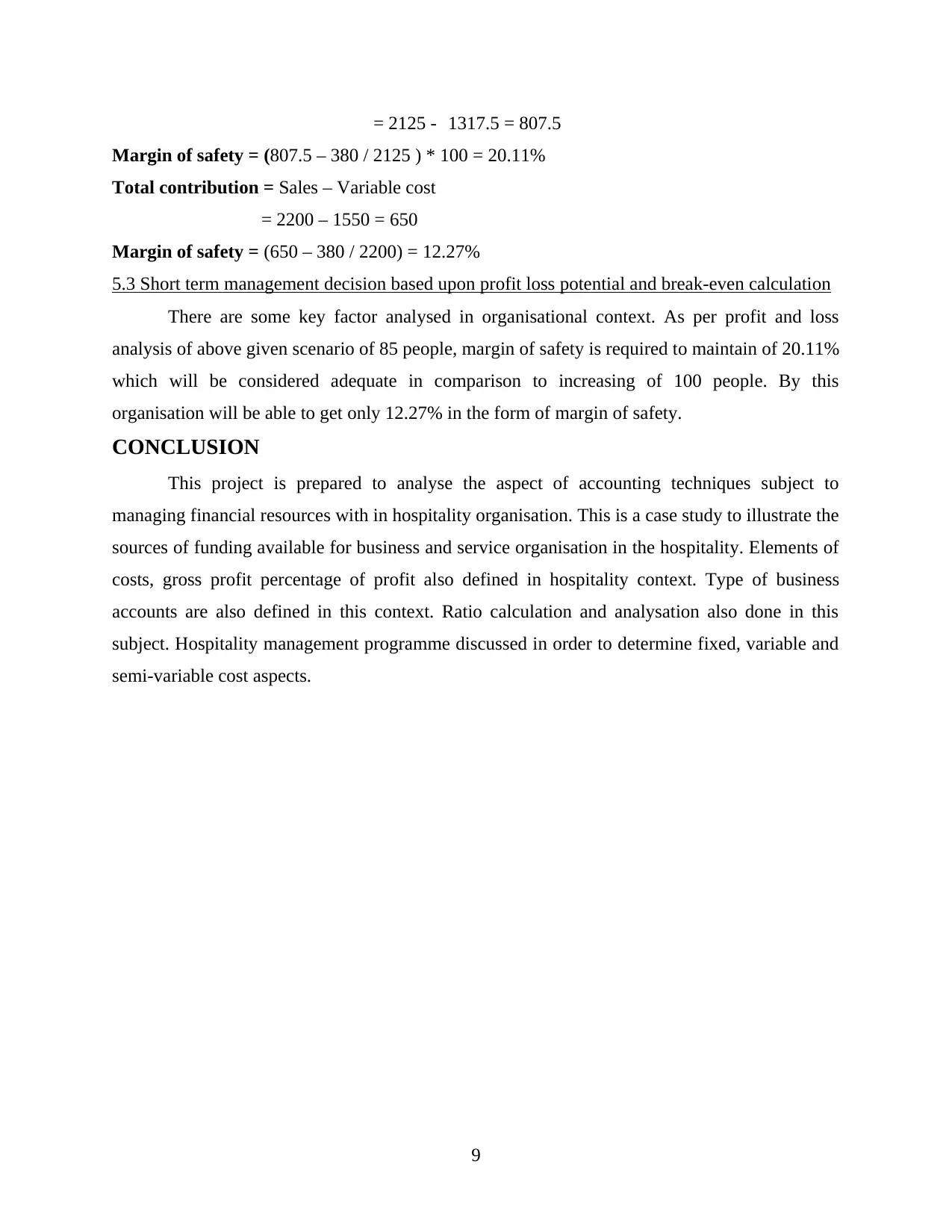

= 2125 - 1317.5 = 807.5

Margin of safety = (807.5 – 380 / 2125 ) * 100 = 20.11%

Total contribution = Sales – Variable cost

= 2200 – 1550 = 650

Margin of safety = (650 – 380 / 2200) = 12.27%

5.3 Short term management decision based upon profit loss potential and break-even calculation

There are some key factor analysed in organisational context. As per profit and loss

analysis of above given scenario of 85 people, margin of safety is required to maintain of 20.11%

which will be considered adequate in comparison to increasing of 100 people. By this

organisation will be able to get only 12.27% in the form of margin of safety.

CONCLUSION

This project is prepared to analyse the aspect of accounting techniques subject to

managing financial resources with in hospitality organisation. This is a case study to illustrate the

sources of funding available for business and service organisation in the hospitality. Elements of

costs, gross profit percentage of profit also defined in hospitality context. Type of business

accounts are also defined in this context. Ratio calculation and analysation also done in this

subject. Hospitality management programme discussed in order to determine fixed, variable and

semi-variable cost aspects.

9

Margin of safety = (807.5 – 380 / 2125 ) * 100 = 20.11%

Total contribution = Sales – Variable cost

= 2200 – 1550 = 650

Margin of safety = (650 – 380 / 2200) = 12.27%

5.3 Short term management decision based upon profit loss potential and break-even calculation

There are some key factor analysed in organisational context. As per profit and loss

analysis of above given scenario of 85 people, margin of safety is required to maintain of 20.11%

which will be considered adequate in comparison to increasing of 100 people. By this

organisation will be able to get only 12.27% in the form of margin of safety.

CONCLUSION

This project is prepared to analyse the aspect of accounting techniques subject to

managing financial resources with in hospitality organisation. This is a case study to illustrate the

sources of funding available for business and service organisation in the hospitality. Elements of

costs, gross profit percentage of profit also defined in hospitality context. Type of business

accounts are also defined in this context. Ratio calculation and analysation also done in this

subject. Hospitality management programme discussed in order to determine fixed, variable and

semi-variable cost aspects.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.