Comprehensive Cost of Capital Analysis Solution for IBTECH

VerifiedAdded on 2022/09/14

|11

|2270

|9

Homework Assignment

AI Summary

This document presents a comprehensive solution to a cost of capital assignment. It begins by addressing the components of Weighted Average Cost of Capital (WACC), including the cost of debt, equity, and preferred stock, and emphasizes the importance of using market values in the calculation. The solution delves into the specifics of calculating the cost of debt, considering factors like the yield to maturity (YTM), floatation costs, and effective annual rates. It also explores the cost of preferred stock, including calculations for both a standard and a redeemable preference share. Furthermore, the assignment covers the cost of retained earnings, using the Capital Asset Pricing Model (CAPM) and Dividend Discount Model (DDM), and explores the use of T-bills as a risk-free rate and the impact of market risk premium. The solution then discusses the growth rate calculation and uses different methods to determine the cost of retained earnings including bond yield plus risk premium method. Finally, the document concludes by comparing the various approaches and justifying the chosen method, making this a valuable resource for students studying finance and corporate finance.

Running head: COST OF CAPITAL

Cost of Capital

Name of the Student:

Name of the University:

Author Note:

Cost of Capital

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COST OF CAPITAL

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to Question 2:................................................................................................................3

Part a:.....................................................................................................................................3

Part b:.....................................................................................................................................3

Part c:.....................................................................................................................................4

Part d:.....................................................................................................................................4

Answer to Question 3:................................................................................................................5

Part a:.....................................................................................................................................5

Part b:.....................................................................................................................................5

Part c:.....................................................................................................................................5

Part d:.....................................................................................................................................6

Part e:.....................................................................................................................................6

Answer to Question 4:................................................................................................................6

Part a:.....................................................................................................................................6

Part b:.....................................................................................................................................6

Answer to Question 5:................................................................................................................7

Part a:.....................................................................................................................................7

Part b:.....................................................................................................................................7

Part c:.....................................................................................................................................7

Part d:.....................................................................................................................................7

Part e:.....................................................................................................................................8

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to Question 2:................................................................................................................3

Part a:.....................................................................................................................................3

Part b:.....................................................................................................................................3

Part c:.....................................................................................................................................4

Part d:.....................................................................................................................................4

Answer to Question 3:................................................................................................................5

Part a:.....................................................................................................................................5

Part b:.....................................................................................................................................5

Part c:.....................................................................................................................................5

Part d:.....................................................................................................................................6

Part e:.....................................................................................................................................6

Answer to Question 4:................................................................................................................6

Part a:.....................................................................................................................................6

Part b:.....................................................................................................................................6

Answer to Question 5:................................................................................................................7

Part a:.....................................................................................................................................7

Part b:.....................................................................................................................................7

Part c:.....................................................................................................................................7

Part d:.....................................................................................................................................7

Part e:.....................................................................................................................................8

2COST OF CAPITAL

Answer to Question 6:................................................................................................................8

Part a:.....................................................................................................................................8

Part b:.....................................................................................................................................8

Part c:.....................................................................................................................................8

Part 7:.........................................................................................................................................9

Part 8:.........................................................................................................................................9

Part 9:.........................................................................................................................................9

Bibliographies:.........................................................................................................................11

Answer to Question 6:................................................................................................................8

Part a:.....................................................................................................................................8

Part b:.....................................................................................................................................8

Part c:.....................................................................................................................................8

Part 7:.........................................................................................................................................9

Part 8:.........................................................................................................................................9

Part 9:.........................................................................................................................................9

Bibliographies:.........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COST OF CAPITAL

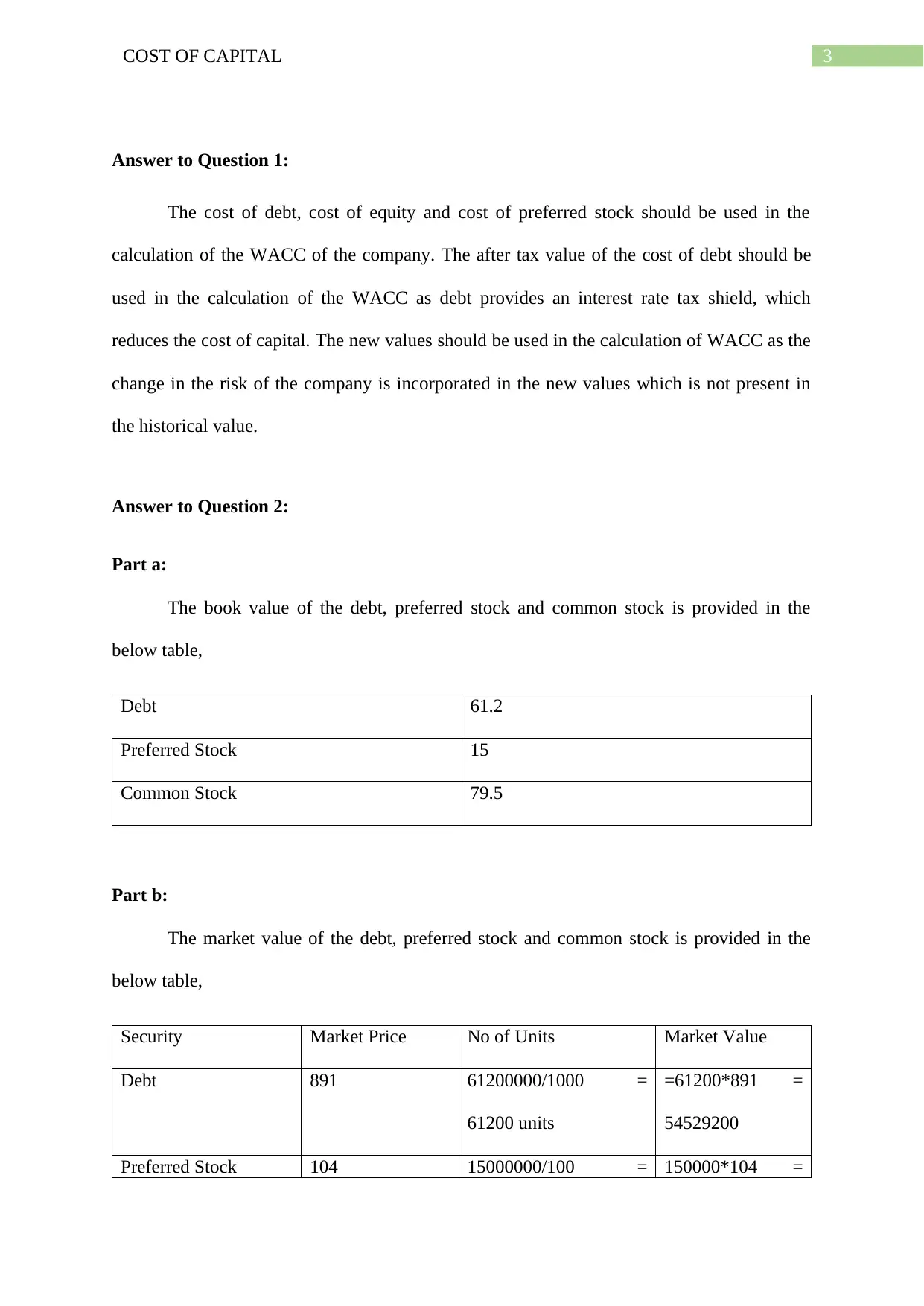

Answer to Question 1:

The cost of debt, cost of equity and cost of preferred stock should be used in the

calculation of the WACC of the company. The after tax value of the cost of debt should be

used in the calculation of the WACC as debt provides an interest rate tax shield, which

reduces the cost of capital. The new values should be used in the calculation of WACC as the

change in the risk of the company is incorporated in the new values which is not present in

the historical value.

Answer to Question 2:

Part a:

The book value of the debt, preferred stock and common stock is provided in the

below table,

Debt 61.2

Preferred Stock 15

Common Stock 79.5

Part b:

The market value of the debt, preferred stock and common stock is provided in the

below table,

Security Market Price No of Units Market Value

Debt 891 61200000/1000 =

61200 units

=61200*891 =

54529200

Preferred Stock 104 15000000/100 = 150000*104 =

Answer to Question 1:

The cost of debt, cost of equity and cost of preferred stock should be used in the

calculation of the WACC of the company. The after tax value of the cost of debt should be

used in the calculation of the WACC as debt provides an interest rate tax shield, which

reduces the cost of capital. The new values should be used in the calculation of WACC as the

change in the risk of the company is incorporated in the new values which is not present in

the historical value.

Answer to Question 2:

Part a:

The book value of the debt, preferred stock and common stock is provided in the

below table,

Debt 61.2

Preferred Stock 15

Common Stock 79.5

Part b:

The market value of the debt, preferred stock and common stock is provided in the

below table,

Security Market Price No of Units Market Value

Debt 891 61200000/1000 =

61200 units

=61200*891 =

54529200

Preferred Stock 104 15000000/100 = 150000*104 =

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COST OF CAPITAL

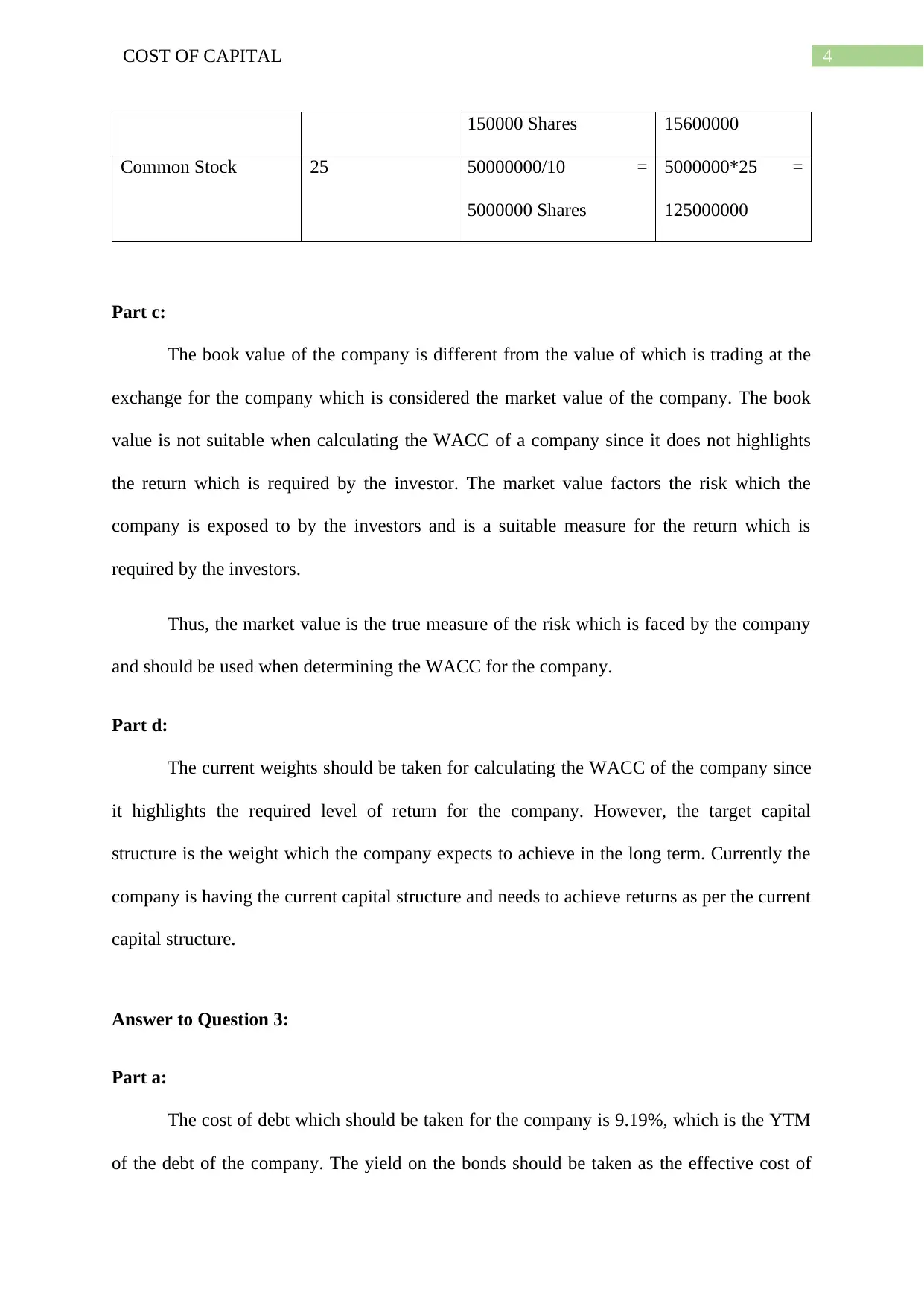

150000 Shares 15600000

Common Stock 25 50000000/10 =

5000000 Shares

5000000*25 =

125000000

Part c:

The book value of the company is different from the value of which is trading at the

exchange for the company which is considered the market value of the company. The book

value is not suitable when calculating the WACC of a company since it does not highlights

the return which is required by the investor. The market value factors the risk which the

company is exposed to by the investors and is a suitable measure for the return which is

required by the investors.

Thus, the market value is the true measure of the risk which is faced by the company

and should be used when determining the WACC for the company.

Part d:

The current weights should be taken for calculating the WACC of the company since

it highlights the required level of return for the company. However, the target capital

structure is the weight which the company expects to achieve in the long term. Currently the

company is having the current capital structure and needs to achieve returns as per the current

capital structure.

Answer to Question 3:

Part a:

The cost of debt which should be taken for the company is 9.19%, which is the YTM

of the debt of the company. The yield on the bonds should be taken as the effective cost of

150000 Shares 15600000

Common Stock 25 50000000/10 =

5000000 Shares

5000000*25 =

125000000

Part c:

The book value of the company is different from the value of which is trading at the

exchange for the company which is considered the market value of the company. The book

value is not suitable when calculating the WACC of a company since it does not highlights

the return which is required by the investor. The market value factors the risk which the

company is exposed to by the investors and is a suitable measure for the return which is

required by the investors.

Thus, the market value is the true measure of the risk which is faced by the company

and should be used when determining the WACC for the company.

Part d:

The current weights should be taken for calculating the WACC of the company since

it highlights the required level of return for the company. However, the target capital

structure is the weight which the company expects to achieve in the long term. Currently the

company is having the current capital structure and needs to achieve returns as per the current

capital structure.

Answer to Question 3:

Part a:

The cost of debt which should be taken for the company is 9.19%, which is the YTM

of the debt of the company. The yield on the bonds should be taken as the effective cost of

5COST OF CAPITAL

debt for the company. It is calculated by taking 4.75% as the coupon rate since the coupon

payment is semi-annual. The number of period is 30 and the current price of the bond is 891.

Thus, the YTM of the bond is 4.59% for half year and for annual year it is 9.19%. This is the

pre-tax cost of debt, while the post-tax cost of debt would be = 9.19% *(1-40%) = 5.51%

Part b:

The floatation cost of debt should be taken in the calculation of the debt, since this is

the cost which would be incurred when raising funds. This charge is a one-time charge which

reduces the amount of funds which is to be raised or increases the cost of capital. This cost

being unavoidable and consists of legal fees, advisory fees, investment banker fees which are

incurred when issuing the debt. Thus, the floatation cost of the debt should be included in the

cost of debt of the company.

Also another treatment of the cost of debt is to reduce from the NPV of the project for

which debt is being raised. The floatation cost which is a one-time charge is considered for

the project and also provides a fair view for the project.

Part c:

The effective annual rate should be considered as the cost of debt for the company.

The nominal cost of debt is less than the effective annual rate as it fails to incorporate the

compounding of the returns. The effective annual rate is higher because the coupons which

are received are assumed to be reinvested at the market rate which makes the effective annual

rate higher and should be considered when using as the cost of debt for a company.

Part d:

Thus to create better proxy for the 30 year cost when the 15 year yield is used, it

should incorporate for the maturity and the liquidity risk which would make the 15 year yield

a better proxy of 30 year yield.

debt for the company. It is calculated by taking 4.75% as the coupon rate since the coupon

payment is semi-annual. The number of period is 30 and the current price of the bond is 891.

Thus, the YTM of the bond is 4.59% for half year and for annual year it is 9.19%. This is the

pre-tax cost of debt, while the post-tax cost of debt would be = 9.19% *(1-40%) = 5.51%

Part b:

The floatation cost of debt should be taken in the calculation of the debt, since this is

the cost which would be incurred when raising funds. This charge is a one-time charge which

reduces the amount of funds which is to be raised or increases the cost of capital. This cost

being unavoidable and consists of legal fees, advisory fees, investment banker fees which are

incurred when issuing the debt. Thus, the floatation cost of the debt should be included in the

cost of debt of the company.

Also another treatment of the cost of debt is to reduce from the NPV of the project for

which debt is being raised. The floatation cost which is a one-time charge is considered for

the project and also provides a fair view for the project.

Part c:

The effective annual rate should be considered as the cost of debt for the company.

The nominal cost of debt is less than the effective annual rate as it fails to incorporate the

compounding of the returns. The effective annual rate is higher because the coupons which

are received are assumed to be reinvested at the market rate which makes the effective annual

rate higher and should be considered when using as the cost of debt for a company.

Part d:

Thus to create better proxy for the 30 year cost when the 15 year yield is used, it

should incorporate for the maturity and the liquidity risk which would make the 15 year yield

a better proxy of 30 year yield.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COST OF CAPITAL

Part e:

Since the bonds of the company have not been recently traded, the method of

calculating the cost of debt would be to divide the interest expense of the company with the

EBIT. This provides a % of debt which is incurred by the company for its debt, however this

amount is pre-tax cost of debt. Hence the post-tax cost of debt would be needed to be

calculated for the same.

Answer to Question 4:

Part a:

The cost of the preferred stock including the floatation cost is provided below,

Cost of preferred stock = Dividend/ Current Price – Floatation Cost = 2.5/ 104-2 = 2.45%

Part b:

The cost of the redeemable preference share is provided below,

Cost of preferred Share = Dividend + (Redemption value – Net Proceeds)/n / (Redemption

value-net proceeds)/2

= 2.5+(( 110 – 104 – 2 )/5) /( 110 - 104 -2 )/2 = 2.5+1.6/ 4 = 1.025%

Answer to Question 5:

Part a:

The retained earnings is the amount which if not retained would had been paid to the

share-holders in the form of dividend. The dividend which would had been received by the

investor would be invested in security and would generate a return. The company has not

paid dividend to the shareholders as it can generate a higher return than the market, thus this

leads to the cost of the retained earnings. If the company cannot use the funds to generate

Part e:

Since the bonds of the company have not been recently traded, the method of

calculating the cost of debt would be to divide the interest expense of the company with the

EBIT. This provides a % of debt which is incurred by the company for its debt, however this

amount is pre-tax cost of debt. Hence the post-tax cost of debt would be needed to be

calculated for the same.

Answer to Question 4:

Part a:

The cost of the preferred stock including the floatation cost is provided below,

Cost of preferred stock = Dividend/ Current Price – Floatation Cost = 2.5/ 104-2 = 2.45%

Part b:

The cost of the redeemable preference share is provided below,

Cost of preferred Share = Dividend + (Redemption value – Net Proceeds)/n / (Redemption

value-net proceeds)/2

= 2.5+(( 110 – 104 – 2 )/5) /( 110 - 104 -2 )/2 = 2.5+1.6/ 4 = 1.025%

Answer to Question 5:

Part a:

The retained earnings is the amount which if not retained would had been paid to the

share-holders in the form of dividend. The dividend which would had been received by the

investor would be invested in security and would generate a return. The company has not

paid dividend to the shareholders as it can generate a higher return than the market, thus this

leads to the cost of the retained earnings. If the company cannot use the funds to generate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COST OF CAPITAL

return it should pay to the shareholders, however return is generated which is the cost of the

retained earnings.

Part b:

The cost of retained earnings using CAPM is provided by the following formula,

Cost of earnings = RF+ (Market Risk Premium)* Beta = 8% + (6%*1.2) = 15.2%

Part c:

The t bond is long term bonds which have an investment horizon of greater than 10

years. The t bill has a horizon of less than a year and hence is a risk free investment with low

volatility. The t bill rates are expected to remain constant and are risk free and serve the true

purpose of the risk free rate. However, t bond are risk free but have long maturity hence face

maturity risk for which the investor is compensated with higher returns. Thus, t bill is a better

measure of the risk free rate.

Part d:

The market risk premium can be calculated from the return of the shares of the

comparable company which can be taken as a proxy for the market return. This return can be

expected to be generated by the company and the market risk premium can be calculated by

deducting the risk free rate. In a similar way, the company historical return can be taken as

the benchmark for market return and can be used to calculate the market risk premium.

Part e:

The cost of retained earnings using CAPM is provided by the following formula,

Cost of earnings = RF+ (Market Risk Premium)* Beta = 8% + (6%*1.2) = 15.2%

return it should pay to the shareholders, however return is generated which is the cost of the

retained earnings.

Part b:

The cost of retained earnings using CAPM is provided by the following formula,

Cost of earnings = RF+ (Market Risk Premium)* Beta = 8% + (6%*1.2) = 15.2%

Part c:

The t bond is long term bonds which have an investment horizon of greater than 10

years. The t bill has a horizon of less than a year and hence is a risk free investment with low

volatility. The t bill rates are expected to remain constant and are risk free and serve the true

purpose of the risk free rate. However, t bond are risk free but have long maturity hence face

maturity risk for which the investor is compensated with higher returns. Thus, t bill is a better

measure of the risk free rate.

Part d:

The market risk premium can be calculated from the return of the shares of the

comparable company which can be taken as a proxy for the market return. This return can be

expected to be generated by the company and the market risk premium can be calculated by

deducting the risk free rate. In a similar way, the company historical return can be taken as

the benchmark for market return and can be used to calculate the market risk premium.

Part e:

The cost of retained earnings using CAPM is provided by the following formula,

Cost of earnings = RF+ (Market Risk Premium)* Beta = 8% + (6%*1.2) = 15.2%

8COST OF CAPITAL

Answer to Question 6:

Part a:

The growth rate can be calculated for the company by multiplying the return on equity

of the company with the retained earnings of the company. This growth rate is called the

sustainable growth rate of the company.

Growth Rate of dividend = ROE * Retained Earnings = 14% * (1-25%) = 10.5%

Part b:

The growth rate of the company using the point to point method is provided below

and is known as compounded annual growth rate,

CAGR = ((1.09 /0.72) ^ (1/5))-1 = 1.5138 ^ (1/5) – 1 = 1.0864 – 1 = 8.647%

Part c:

The cost of retained earnings for the company using the DCF or DDM is provided by

the following formula,

Price of share = Dividend * (1+Growth Rate)/ (Cost of retained earnings – Growth Rate)

Cost of Retained Earnings = Dividend * (1+Growth Rate)/ Price of share + Growth Rate

= 1.09* (1+10.5%)/25 + 10.5% = 1.20/25 +10.5% = 4.82%+10.5% = 15.32%

Part 7:

The cost of retained earnings using the bond yield plus risk premium method is provided by

the following formula,

Cost of retained earnings = Bond yield + market risk premium = 10% + 6% = 16%

Answer to Question 6:

Part a:

The growth rate can be calculated for the company by multiplying the return on equity

of the company with the retained earnings of the company. This growth rate is called the

sustainable growth rate of the company.

Growth Rate of dividend = ROE * Retained Earnings = 14% * (1-25%) = 10.5%

Part b:

The growth rate of the company using the point to point method is provided below

and is known as compounded annual growth rate,

CAGR = ((1.09 /0.72) ^ (1/5))-1 = 1.5138 ^ (1/5) – 1 = 1.0864 – 1 = 8.647%

Part c:

The cost of retained earnings for the company using the DCF or DDM is provided by

the following formula,

Price of share = Dividend * (1+Growth Rate)/ (Cost of retained earnings – Growth Rate)

Cost of Retained Earnings = Dividend * (1+Growth Rate)/ Price of share + Growth Rate

= 1.09* (1+10.5%)/25 + 10.5% = 1.20/25 +10.5% = 4.82%+10.5% = 15.32%

Part 7:

The cost of retained earnings using the bond yield plus risk premium method is provided by

the following formula,

Cost of retained earnings = Bond yield + market risk premium = 10% + 6% = 16%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COST OF CAPITAL

Part 8:

The final estimate of the cost of retained earnings under the three approaches is the

DCF approach. Thus the cost of equity is 15.32% for the company and the reason is provided

in the following points,

In the CAPM approach the risk free rate should had been t bill, however the cost of

retained earnings is calculated using t bonds. This incorporates maturity risk in the

calculation.

The Company has a credit rating of BBB while the bond yield taken is from A rated

bond. The company is facing higher risk but less risky bond is taken for the

calculation of the cost of retained earnings.

Thus, due to these reasons the cost of retained earnings is calculated using the DCF.

Part 9:

The dividend per share is taken as 1.09 while the growth rate is 10.5%. The current

share price is 25 while the floatation cost is 30%. Thus the cost of retained earnings is

provided by the following formula,

Cost of retained earnings = Dividend Next Year/ Price of share *(1- Floatation cost) +

Growth Rate

= 1.20/17.5 + 10.5% = 17.35%

Part 8:

The final estimate of the cost of retained earnings under the three approaches is the

DCF approach. Thus the cost of equity is 15.32% for the company and the reason is provided

in the following points,

In the CAPM approach the risk free rate should had been t bill, however the cost of

retained earnings is calculated using t bonds. This incorporates maturity risk in the

calculation.

The Company has a credit rating of BBB while the bond yield taken is from A rated

bond. The company is facing higher risk but less risky bond is taken for the

calculation of the cost of retained earnings.

Thus, due to these reasons the cost of retained earnings is calculated using the DCF.

Part 9:

The dividend per share is taken as 1.09 while the growth rate is 10.5%. The current

share price is 25 while the floatation cost is 30%. Thus the cost of retained earnings is

provided by the following formula,

Cost of retained earnings = Dividend Next Year/ Price of share *(1- Floatation cost) +

Growth Rate

= 1.20/17.5 + 10.5% = 17.35%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COST OF CAPITAL

Bibliographies:

Andrei, D., Cujean, J. and Wilson, M.I., 2018. The lost capital asset pricing model.

Cook, K.A., Moser, W.J. and Omer, T.C., 2017. Tax avoidance and ex ante cost of

capital. Journal of Business Finance & Accounting, 44(7-8), pp.1109-1136.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of

capital. Journal of Financial Economics, 123(2), pp.415-431.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of

capital. Journal of Financial Economics, 123(2), pp.415-431.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental

responsibility and the cost of capital: International evidence. Journal of Business

Ethics, 149(2), pp.335-361.

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal

of Financial Economics, 119(2), pp.300-315.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Kuehn, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Bibliographies:

Andrei, D., Cujean, J. and Wilson, M.I., 2018. The lost capital asset pricing model.

Cook, K.A., Moser, W.J. and Omer, T.C., 2017. Tax avoidance and ex ante cost of

capital. Journal of Business Finance & Accounting, 44(7-8), pp.1109-1136.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of

capital. Journal of Financial Economics, 123(2), pp.415-431.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of

capital. Journal of Financial Economics, 123(2), pp.415-431.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental

responsibility and the cost of capital: International evidence. Journal of Business

Ethics, 149(2), pp.335-361.

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal

of Financial Economics, 119(2), pp.300-315.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Kuehn, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.