Finance Report: Analyzing Financial Objectives and Challenges

VerifiedAdded on 2022/12/28

|23

|5143

|74

Report

AI Summary

This report delves into the core aspects of financial management, beginning with an introduction to the subject and its significance. It examines the intricate relationships between financial functions and other functional areas within organizations, highlighting the importance of coordination. The report then analyzes the impact of financial objectives, such as revenue, cost, profit, cash flow, and capital structure, on decision-making processes, including financing, investment, and dividend decisions. It differentiates between management accounting and financial accounting, outlining their distinct characteristics and purposes. Furthermore, the report investigates the influence of organizational and regulatory frameworks on financial management approaches, emphasizing the need for adherence to policies and procedures. It also explores the financial challenges faced by organizations, particularly small businesses, such as lack of cash flow and capital, and differentiates between budget setting and financial forecasting. The report concludes by discussing corrective actions for budgetary variances and reporting procedures, providing a comprehensive understanding of financial management practices.

MANAGING FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

Relationship between financial and other functional areas within organizations........................4

Impact of financial objectives on decision-making.....................................................................6

Difference between management accounting and financial accounting......................................7

Impact of organizational and regulatory frameworks on financial management approaches.....8

Financial challenges faced by the organization...........................................................................9

The differences between budget setting and financial forecasting............................................10

Evaluations of budget methods used by the organizations........................................................12

Formulation and justification of budget for an area of management responsibility..................14

Analysing the impact of different factors on budget management............................................16

Corrective actions in response to budgetary variance................................................................17

Reporting procedures for authorizing corrective actions to a budget........................................18

CONCLUSION..............................................................................................................................19

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

Relationship between financial and other functional areas within organizations........................4

Impact of financial objectives on decision-making.....................................................................6

Difference between management accounting and financial accounting......................................7

Impact of organizational and regulatory frameworks on financial management approaches.....8

Financial challenges faced by the organization...........................................................................9

The differences between budget setting and financial forecasting............................................10

Evaluations of budget methods used by the organizations........................................................12

Formulation and justification of budget for an area of management responsibility..................14

Analysing the impact of different factors on budget management............................................16

Corrective actions in response to budgetary variance................................................................17

Reporting procedures for authorizing corrective actions to a budget........................................18

CONCLUSION..............................................................................................................................19

REFERENCES................................................................................................................................1

INTRODUCTION

Preparing budgets of different departments in order to know the expected income and

expenses is the prime role of the responsible person of that department. In this report, we will

understand the relationship between financial function with other functional area. This report

will also state the differences between management accounting and financial accounting or

budget setting and financial forecasting. This report will also include the impact of financial

objectives on decision-making and organizational and regulatory frameworks on approaches of

financial management. Nowadays, organizations are facing financial challenges and mostly small

organizations in UK. This report also includes evaluation of different budgets along with

formulation and justification of budgets in order to cope with the financial challenges. This

report will also state the impact of different factors on budget management. The report will study

the corrective actions in case of budget variance in order to minimize and eliminate the budget

variance if any. This report will also understand the reporting procedures for authorizing

corrective actions to a budget.

MAIN BODY

» LEARNER EVIDENCE

1.1 Analyse the relationship between the financial function and other functional areas

within organisations

Preparing budgets of different departments in order to know the expected income and

expenses is the prime role of the responsible person of that department. In this report, we will

understand the relationship between financial function with other functional area. This report

will also state the differences between management accounting and financial accounting or

budget setting and financial forecasting. This report will also include the impact of financial

objectives on decision-making and organizational and regulatory frameworks on approaches of

financial management. Nowadays, organizations are facing financial challenges and mostly small

organizations in UK. This report also includes evaluation of different budgets along with

formulation and justification of budgets in order to cope with the financial challenges. This

report will also state the impact of different factors on budget management. The report will study

the corrective actions in case of budget variance in order to minimize and eliminate the budget

variance if any. This report will also understand the reporting procedures for authorizing

corrective actions to a budget.

MAIN BODY

» LEARNER EVIDENCE

1.1 Analyse the relationship between the financial function and other functional areas

within organisations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Relationship between financial and other functional areas within organisations

Finance management is a part of management indulge in planning, organizing and controlling

the financial resources of the organization. For this purpose, every organization hires finance

managers. The relation between finance function and other functional areas (such as

production function, human resources function and marketing function) states maintaining

coordination among the departments in order to utilize the resources. (Nawaz, and Koç, 2019).

For example, Sainsbury company always focus towards maintaining flexible relationship

between all departmental managers in order to achieve the goals and objectives of the

organization.

Relationship with production management: In organizations, the role of production

manager is to analyse and monitor the production and development process of the

product and services. For this purpose, they have to stay connected with inventory and

sales manager to know about the stock availability and sales quantity. In this respect,

production manager has to coordinate with the finance manager to provide information

about the cost of production of product. So, after receiving and analysing the

information related to the cost of production, finance manager choose an appropriate

investment plan out of various alternatives in order to arrange capital for converting

the raw material into finished goods.

Relationship with HR management: The role of human resources management is to

organize, control and motivate the employees of the organization. To motivate the

employees includes various incentive policies, HR managers also look out the pensions

of retired employees (Monden, 2019). So for all this purpose, there is a requirement of

funds which is going to be arranged by finance mangers. Finance manager and HR

manager are interrelated with each other in order to arrange and conduct training and

incentives plan.

Relationship with marketing management: The role of marketing manager is to

analyse the demand of the product in the market by conducting various surveys. Due to

continuously increase in competitions, finance managers and marketing managers have

to work together in order to increase the market share of the company. To increase the

profit of the company, marketing managers have to promote the products of the

company into the market. Promotion and marketing activity required funds to further

Finance management is a part of management indulge in planning, organizing and controlling

the financial resources of the organization. For this purpose, every organization hires finance

managers. The relation between finance function and other functional areas (such as

production function, human resources function and marketing function) states maintaining

coordination among the departments in order to utilize the resources. (Nawaz, and Koç, 2019).

For example, Sainsbury company always focus towards maintaining flexible relationship

between all departmental managers in order to achieve the goals and objectives of the

organization.

Relationship with production management: In organizations, the role of production

manager is to analyse and monitor the production and development process of the

product and services. For this purpose, they have to stay connected with inventory and

sales manager to know about the stock availability and sales quantity. In this respect,

production manager has to coordinate with the finance manager to provide information

about the cost of production of product. So, after receiving and analysing the

information related to the cost of production, finance manager choose an appropriate

investment plan out of various alternatives in order to arrange capital for converting

the raw material into finished goods.

Relationship with HR management: The role of human resources management is to

organize, control and motivate the employees of the organization. To motivate the

employees includes various incentive policies, HR managers also look out the pensions

of retired employees (Monden, 2019). So for all this purpose, there is a requirement of

funds which is going to be arranged by finance mangers. Finance manager and HR

manager are interrelated with each other in order to arrange and conduct training and

incentives plan.

Relationship with marketing management: The role of marketing manager is to

analyse the demand of the product in the market by conducting various surveys. Due to

continuously increase in competitions, finance managers and marketing managers have

to work together in order to increase the market share of the company. To increase the

profit of the company, marketing managers have to promote the products of the

company into the market. Promotion and marketing activity required funds to further

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

proceed. This indicates that how marketing and finance managers are working together

to increase the profitability of the company.

1.2 Examine the impact of financial objectives on decision making within

organisations

to increase the profitability of the company.

1.2 Examine the impact of financial objectives on decision making within

organisations

Impact of financial objectives on decision-making

Generally, there are various financial objectives of the organizations but the main financial

objectives of all the organization is revenue, cost, profit, cash flow and capital structure

objective. The impact of all the financial objective on decision-making of the organizations

such as Sainsbury company is that the finance managers have to take three important decisions

(Kumar, and et.al., 2017). The three decisions such as financing, investment and dividend

decisions help the finance manager to maximize the profit and wealth of the company.

Financing decision: Financing decision involves the decision related to selection of the

best alternative to acquire funds from the market for investment and managing working

capital purpose. There are various sources of finance is available to the managers of the

company. Selecting the alternatives keeping in mind the objective of low cost of

acquisitions is a crucial decision taken by the managers.

Investment decision: It involves the decision relating to selection of the best project in

order to earn the higher returns. Finance manager can use different investment appraisal

techniques to know the best investment plans. The decision of selection of plans of

finance manager is based upon the objective that the return from funds invested is

higher than the cost of funds. They must take all decisions keeping in mind the

financial objectives.

Dividend decision: It involves the decision of finance manager i.e. whether to

distribute the earnings available for equity shareholders between them or to retained it

for the purpose of future development or both (Roychowdhury, Shroff, and Verdi,

2019). Taking the appropriate decision keeping in mind the objectives of finance

management is must for finance managers to increase wealth of the company.

1.3 Differentiate between management accounting and financial accounting

Generally, there are various financial objectives of the organizations but the main financial

objectives of all the organization is revenue, cost, profit, cash flow and capital structure

objective. The impact of all the financial objective on decision-making of the organizations

such as Sainsbury company is that the finance managers have to take three important decisions

(Kumar, and et.al., 2017). The three decisions such as financing, investment and dividend

decisions help the finance manager to maximize the profit and wealth of the company.

Financing decision: Financing decision involves the decision related to selection of the

best alternative to acquire funds from the market for investment and managing working

capital purpose. There are various sources of finance is available to the managers of the

company. Selecting the alternatives keeping in mind the objective of low cost of

acquisitions is a crucial decision taken by the managers.

Investment decision: It involves the decision relating to selection of the best project in

order to earn the higher returns. Finance manager can use different investment appraisal

techniques to know the best investment plans. The decision of selection of plans of

finance manager is based upon the objective that the return from funds invested is

higher than the cost of funds. They must take all decisions keeping in mind the

financial objectives.

Dividend decision: It involves the decision of finance manager i.e. whether to

distribute the earnings available for equity shareholders between them or to retained it

for the purpose of future development or both (Roychowdhury, Shroff, and Verdi,

2019). Taking the appropriate decision keeping in mind the objectives of finance

management is must for finance managers to increase wealth of the company.

1.3 Differentiate between management accounting and financial accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

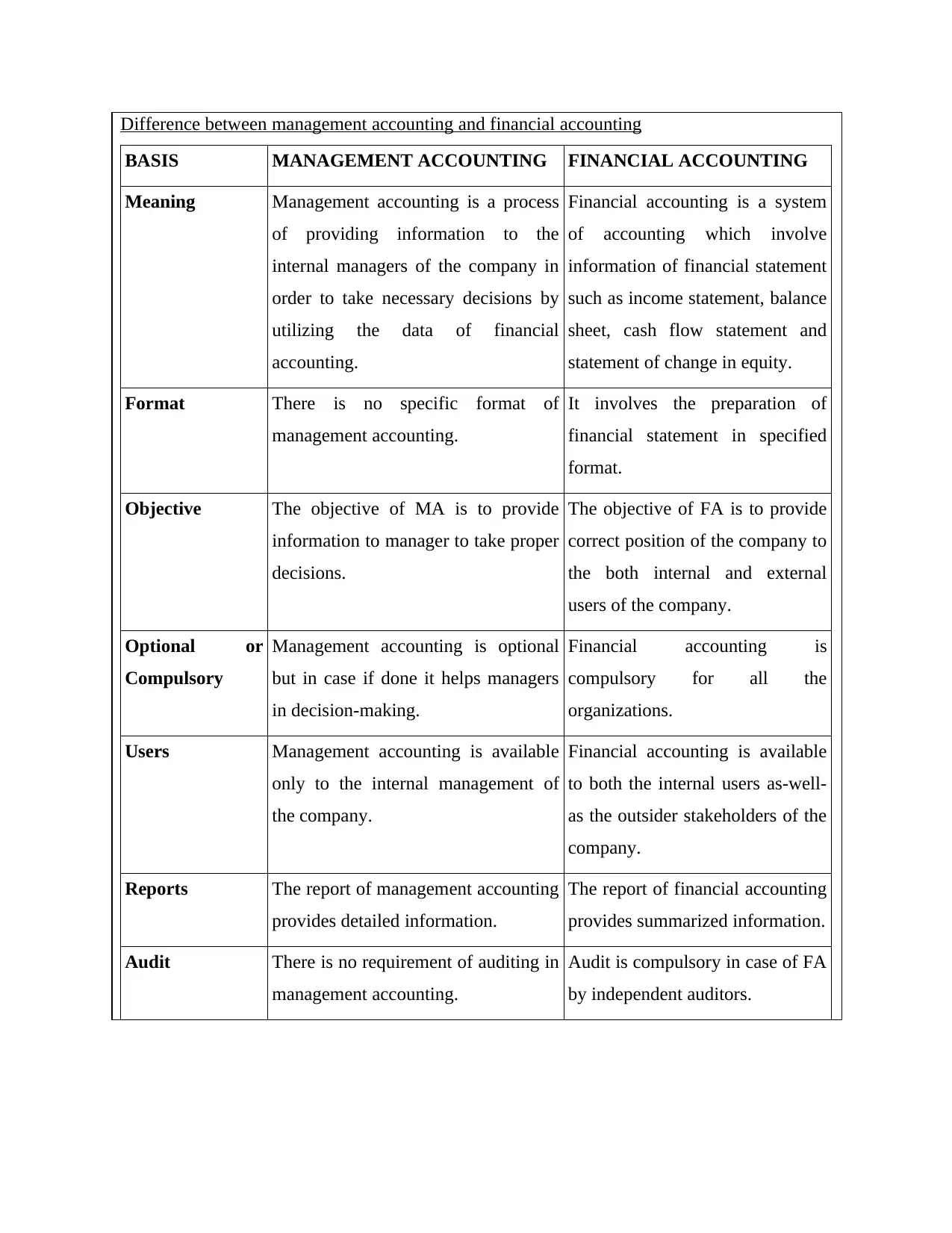

Difference between management accounting and financial accounting

BASIS MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

Meaning Management accounting is a process

of providing information to the

internal managers of the company in

order to take necessary decisions by

utilizing the data of financial

accounting.

Financial accounting is a system

of accounting which involve

information of financial statement

such as income statement, balance

sheet, cash flow statement and

statement of change in equity.

Format There is no specific format of

management accounting.

It involves the preparation of

financial statement in specified

format.

Objective The objective of MA is to provide

information to manager to take proper

decisions.

The objective of FA is to provide

correct position of the company to

the both internal and external

users of the company.

Optional or

Compulsory

Management accounting is optional

but in case if done it helps managers

in decision-making.

Financial accounting is

compulsory for all the

organizations.

Users Management accounting is available

only to the internal management of

the company.

Financial accounting is available

to both the internal users as-well-

as the outsider stakeholders of the

company.

Reports The report of management accounting

provides detailed information.

The report of financial accounting

provides summarized information.

Audit There is no requirement of auditing in

management accounting.

Audit is compulsory in case of FA

by independent auditors.

BASIS MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

Meaning Management accounting is a process

of providing information to the

internal managers of the company in

order to take necessary decisions by

utilizing the data of financial

accounting.

Financial accounting is a system

of accounting which involve

information of financial statement

such as income statement, balance

sheet, cash flow statement and

statement of change in equity.

Format There is no specific format of

management accounting.

It involves the preparation of

financial statement in specified

format.

Objective The objective of MA is to provide

information to manager to take proper

decisions.

The objective of FA is to provide

correct position of the company to

the both internal and external

users of the company.

Optional or

Compulsory

Management accounting is optional

but in case if done it helps managers

in decision-making.

Financial accounting is

compulsory for all the

organizations.

Users Management accounting is available

only to the internal management of

the company.

Financial accounting is available

to both the internal users as-well-

as the outsider stakeholders of the

company.

Reports The report of management accounting

provides detailed information.

The report of financial accounting

provides summarized information.

Audit There is no requirement of auditing in

management accounting.

Audit is compulsory in case of FA

by independent auditors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Time frame Management accounting reports is

prepared as per the needs of the

organizations.

Financial accounting is prepared

at the end of every financial year.

1.4 Analyse the impact of organisational and regulatory frameworks on an

organisation’s approach to financial management

prepared as per the needs of the

organizations.

Financial accounting is prepared

at the end of every financial year.

1.4 Analyse the impact of organisational and regulatory frameworks on an

organisation’s approach to financial management

Impact of organizational and regulatory frameworks on financial management approaches

The approaches of financial management are procurement of fund and utilization of fund in the

best manner possible. For this purpose, financial managers of the company take three most

important decisions such as Financing decision, investment decision and dividend decision.

Organizational frameworks consist of legislation, policies and procedures in order to prepare

the financial statement, budgets and report in a structured way. Regulatory frameworks states

that the financial statement are prepared by following the provision of acts such as companies

act, SEBI, direct and indirect tax, Foreign exchange regulation etc. In order to take the decision

of the company, managers have to follow the structure. Organizational and regulatory

frameworks help to ensure that the behaviour of the company and directors are good towards

the customer in order to attract the customer. In case if managers are focusing on acquiring the

funds from the international market they have to take decision in the same purpose only. In that

case following the provisions of foreign exchange regulation is beneficial in the decision-

making of the managers (Ameen, Ahmed, and Abd Hafez, 2018). It also helps in increasing the

confidence of the users of the company towards the process of financial reporting. They

believe on the decision of the company if they prepare financial statement, budgets and reports

in the proper structure. In case of acquiring the funds from the market in the form of equity and

debt. It is beneficial for the managers to follow the provisions and procedures set by the

Securities exchange board of India. It also helps the managers to invest the fund into the best

project after analysing the legal and market regulations. In order to take financial decision and

achieve objective of the company, following the policies and procedures of financial reporting

frameworks is not only sufficient but it shows the accurate financial statement. It is also

beneficial for the manager to involve legal and market regulations into decision-making.

1.5 Analyse the challenges organisations face accessing finance

The approaches of financial management are procurement of fund and utilization of fund in the

best manner possible. For this purpose, financial managers of the company take three most

important decisions such as Financing decision, investment decision and dividend decision.

Organizational frameworks consist of legislation, policies and procedures in order to prepare

the financial statement, budgets and report in a structured way. Regulatory frameworks states

that the financial statement are prepared by following the provision of acts such as companies

act, SEBI, direct and indirect tax, Foreign exchange regulation etc. In order to take the decision

of the company, managers have to follow the structure. Organizational and regulatory

frameworks help to ensure that the behaviour of the company and directors are good towards

the customer in order to attract the customer. In case if managers are focusing on acquiring the

funds from the international market they have to take decision in the same purpose only. In that

case following the provisions of foreign exchange regulation is beneficial in the decision-

making of the managers (Ameen, Ahmed, and Abd Hafez, 2018). It also helps in increasing the

confidence of the users of the company towards the process of financial reporting. They

believe on the decision of the company if they prepare financial statement, budgets and reports

in the proper structure. In case of acquiring the funds from the market in the form of equity and

debt. It is beneficial for the managers to follow the provisions and procedures set by the

Securities exchange board of India. It also helps the managers to invest the fund into the best

project after analysing the legal and market regulations. In order to take financial decision and

achieve objective of the company, following the policies and procedures of financial reporting

frameworks is not only sufficient but it shows the accurate financial statement. It is also

beneficial for the manager to involve legal and market regulations into decision-making.

1.5 Analyse the challenges organisations face accessing finance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

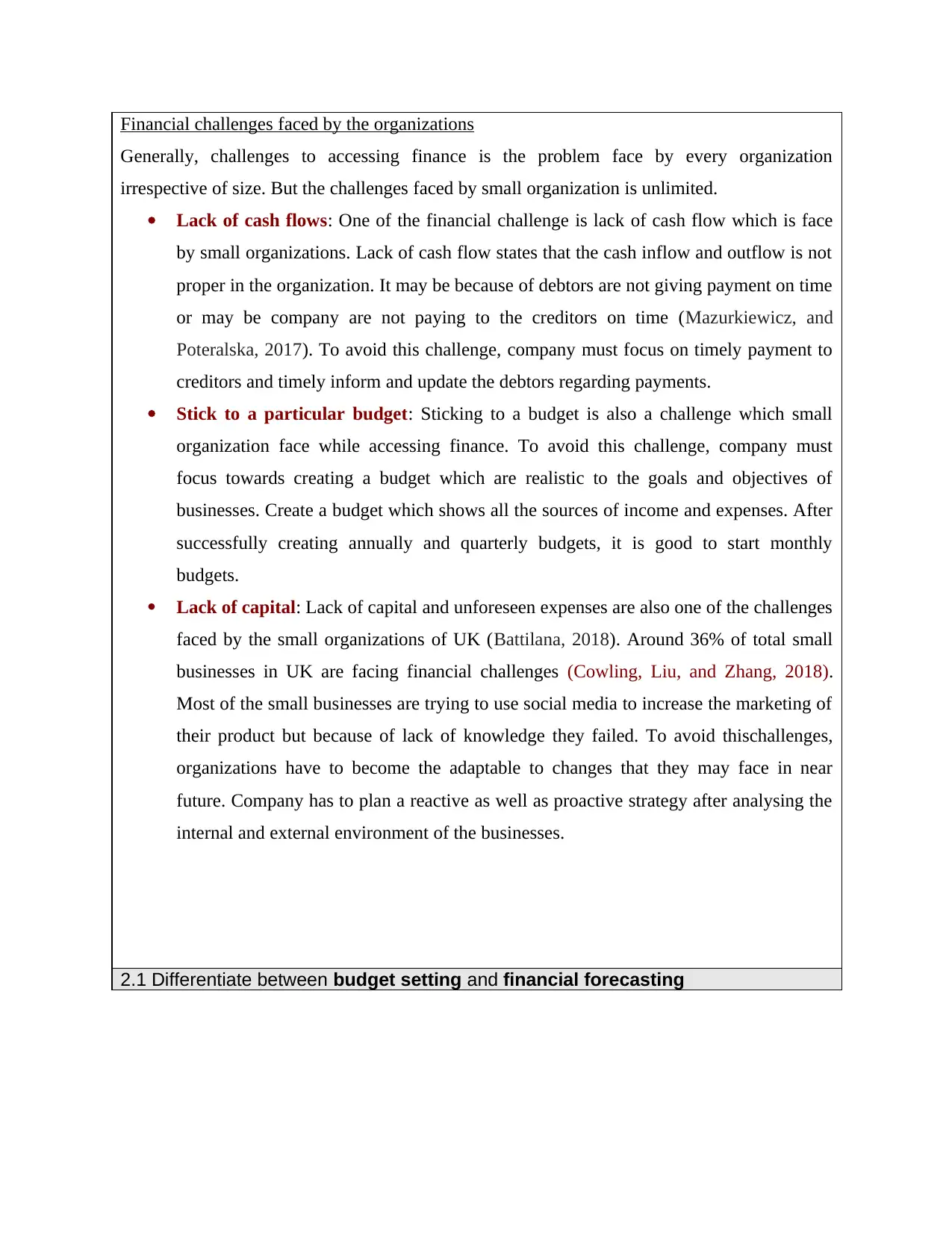

Financial challenges faced by the organizations

Generally, challenges to accessing finance is the problem face by every organization

irrespective of size. But the challenges faced by small organization is unlimited.

Lack of cash flows: One of the financial challenge is lack of cash flow which is face

by small organizations. Lack of cash flow states that the cash inflow and outflow is not

proper in the organization. It may be because of debtors are not giving payment on time

or may be company are not paying to the creditors on time (Mazurkiewicz, and

Poteralska, 2017). To avoid this challenge, company must focus on timely payment to

creditors and timely inform and update the debtors regarding payments.

Stick to a particular budget: Sticking to a budget is also a challenge which small

organization face while accessing finance. To avoid this challenge, company must

focus towards creating a budget which are realistic to the goals and objectives of

businesses. Create a budget which shows all the sources of income and expenses. After

successfully creating annually and quarterly budgets, it is good to start monthly

budgets.

Lack of capital: Lack of capital and unforeseen expenses are also one of the challenges

faced by the small organizations of UK (Battilana, 2018). Around 36% of total small

businesses in UK are facing financial challenges (Cowling, Liu, and Zhang, 2018).

Most of the small businesses are trying to use social media to increase the marketing of

their product but because of lack of knowledge they failed. To avoid thischallenges,

organizations have to become the adaptable to changes that they may face in near

future. Company has to plan a reactive as well as proactive strategy after analysing the

internal and external environment of the businesses.

2.1 Differentiate between budget setting and financial forecasting

Generally, challenges to accessing finance is the problem face by every organization

irrespective of size. But the challenges faced by small organization is unlimited.

Lack of cash flows: One of the financial challenge is lack of cash flow which is face

by small organizations. Lack of cash flow states that the cash inflow and outflow is not

proper in the organization. It may be because of debtors are not giving payment on time

or may be company are not paying to the creditors on time (Mazurkiewicz, and

Poteralska, 2017). To avoid this challenge, company must focus on timely payment to

creditors and timely inform and update the debtors regarding payments.

Stick to a particular budget: Sticking to a budget is also a challenge which small

organization face while accessing finance. To avoid this challenge, company must

focus towards creating a budget which are realistic to the goals and objectives of

businesses. Create a budget which shows all the sources of income and expenses. After

successfully creating annually and quarterly budgets, it is good to start monthly

budgets.

Lack of capital: Lack of capital and unforeseen expenses are also one of the challenges

faced by the small organizations of UK (Battilana, 2018). Around 36% of total small

businesses in UK are facing financial challenges (Cowling, Liu, and Zhang, 2018).

Most of the small businesses are trying to use social media to increase the marketing of

their product but because of lack of knowledge they failed. To avoid thischallenges,

organizations have to become the adaptable to changes that they may face in near

future. Company has to plan a reactive as well as proactive strategy after analysing the

internal and external environment of the businesses.

2.1 Differentiate between budget setting and financial forecasting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

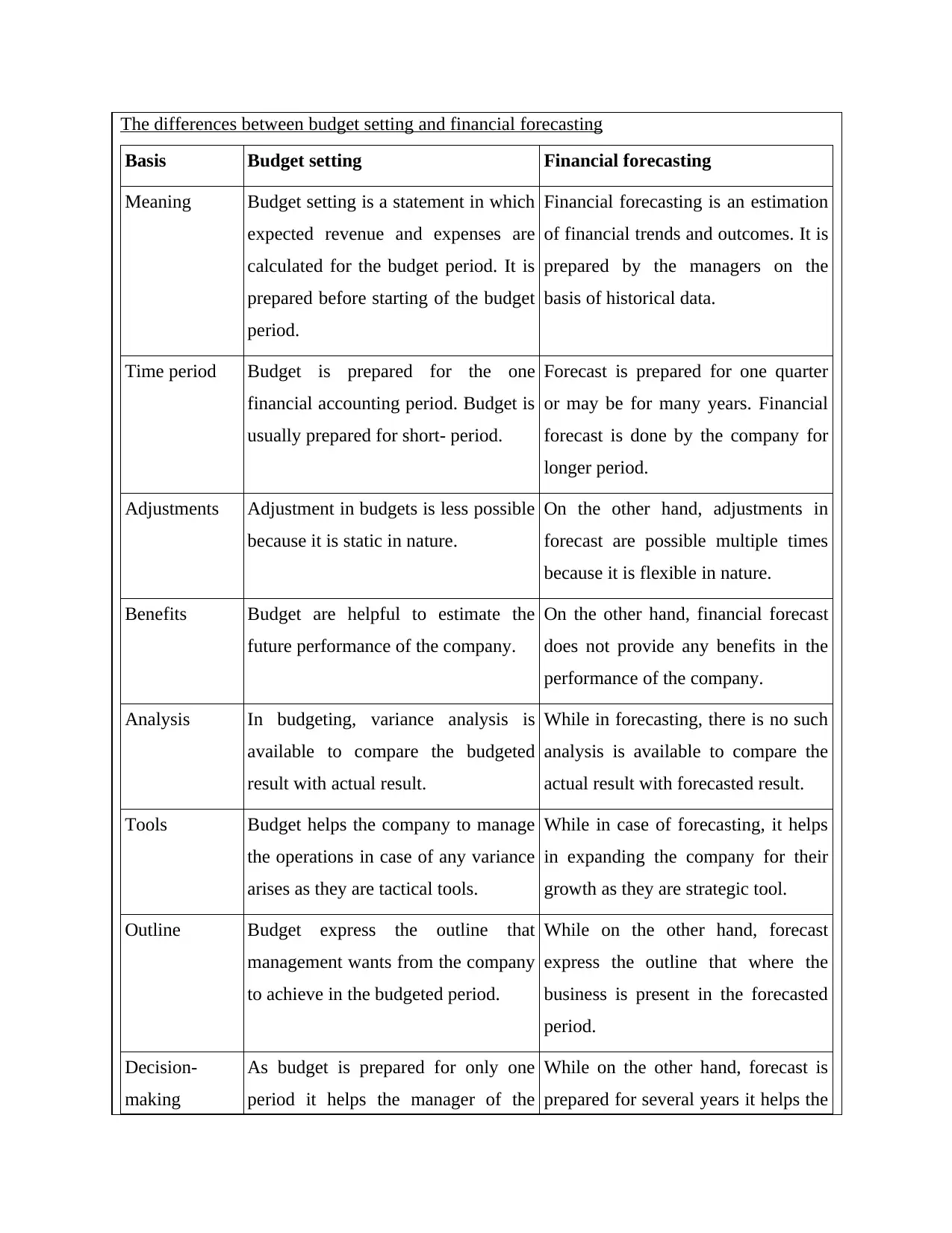

The differences between budget setting and financial forecasting

Basis Budget setting Financial forecasting

Meaning Budget setting is a statement in which

expected revenue and expenses are

calculated for the budget period. It is

prepared before starting of the budget

period.

Financial forecasting is an estimation

of financial trends and outcomes. It is

prepared by the managers on the

basis of historical data.

Time period Budget is prepared for the one

financial accounting period. Budget is

usually prepared for short- period.

Forecast is prepared for one quarter

or may be for many years. Financial

forecast is done by the company for

longer period.

Adjustments Adjustment in budgets is less possible

because it is static in nature.

On the other hand, adjustments in

forecast are possible multiple times

because it is flexible in nature.

Benefits Budget are helpful to estimate the

future performance of the company.

On the other hand, financial forecast

does not provide any benefits in the

performance of the company.

Analysis In budgeting, variance analysis is

available to compare the budgeted

result with actual result.

While in forecasting, there is no such

analysis is available to compare the

actual result with forecasted result.

Tools Budget helps the company to manage

the operations in case of any variance

arises as they are tactical tools.

While in case of forecasting, it helps

in expanding the company for their

growth as they are strategic tool.

Outline Budget express the outline that

management wants from the company

to achieve in the budgeted period.

While on the other hand, forecast

express the outline that where the

business is present in the forecasted

period.

Decision-

making

As budget is prepared for only one

period it helps the manager of the

While on the other hand, forecast is

prepared for several years it helps the

Basis Budget setting Financial forecasting

Meaning Budget setting is a statement in which

expected revenue and expenses are

calculated for the budget period. It is

prepared before starting of the budget

period.

Financial forecasting is an estimation

of financial trends and outcomes. It is

prepared by the managers on the

basis of historical data.

Time period Budget is prepared for the one

financial accounting period. Budget is

usually prepared for short- period.

Forecast is prepared for one quarter

or may be for many years. Financial

forecast is done by the company for

longer period.

Adjustments Adjustment in budgets is less possible

because it is static in nature.

On the other hand, adjustments in

forecast are possible multiple times

because it is flexible in nature.

Benefits Budget are helpful to estimate the

future performance of the company.

On the other hand, financial forecast

does not provide any benefits in the

performance of the company.

Analysis In budgeting, variance analysis is

available to compare the budgeted

result with actual result.

While in forecasting, there is no such

analysis is available to compare the

actual result with forecasted result.

Tools Budget helps the company to manage

the operations in case of any variance

arises as they are tactical tools.

While in case of forecasting, it helps

in expanding the company for their

growth as they are strategic tool.

Outline Budget express the outline that

management wants from the company

to achieve in the budgeted period.

While on the other hand, forecast

express the outline that where the

business is present in the forecasted

period.

Decision-

making

As budget is prepared for only one

period it helps the manager of the

While on the other hand, forecast is

prepared for several years it helps the

company in decision-making for one

period only. Budget helps the

managers to take the operational

decisions of the business.

managers of the company in decision-

making for more than one year.

Forecast helps the managers to take

the strategic decisions of the

business.

2.2 Evaluate budget setting approaches used by organizations

period only. Budget helps the

managers to take the operational

decisions of the business.

managers of the company in decision-

making for more than one year.

Forecast helps the managers to take

the strategic decisions of the

business.

2.2 Evaluate budget setting approaches used by organizations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.