Financial Decision-Making Report: Skanska PLC, BM414, Bucks Uni

VerifiedAdded on 2022/12/26

|11

|3325

|26

Report

AI Summary

This report analyzes financial decision-making within the context of Skanska PLC, a UK-based construction and engineering company. The introduction provides background information on Skanska, including its expansion plans and market position. Task 1 delves into the importance, functions, duties, and roles of both the accounting and finance departments, highlighting their significance in managing inventories, treasury operations, bookkeeping, cash flows, financial reporting, investments, strategic decisions, budgeting, and risk management. The analysis emphasizes how these departments support Skanska's growth. Task 2 focuses on ratio computation and analysis, calculating ROCE, net profit margin, current ratio, debtors collection period, and creditors payment period for 2018 and 2019. The report interprets these ratios, discussing trends and their implications for Skanska's financial health and performance, including potential reasons for declining ROCE and net profit margins, and the impact on the company's ability to secure funding and maximize value.

Financial Decision-Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial decision-making relates to set of activities that allows a business's management

to take a variety of decisions quickly and appropriately. This enables them to assure that

organisations are prepared to learn how to interpret and view fiscal analytical estimates, and

information in order to make a variety of short, mid, and long-term decisions. When it comes to

the use of money, fiscal decision-making is practice of weighing the benefits and drawbacks

of decision. Efficient fiscal decision-making is requirement for financial wellbeing (Valaskova,

Bartosova and Kubala, 2019). This report focuses on the Skanska PLC, which is UK-based

Constructions and Engineering Organization situated in the Hertfordshire, UK. Over the next ten

years, the company intends to expand into European countries and grow its market position.

This research will go into great detail on determining the worth of accounting and finance

activities. A systematic analysis of the different ratios will also be undertaken out as part

of study.

TASK 1

Importance of Accounting and Finance functions, duties and roles:

The Finance department is trained team of employees who manage a company 's financial

functions. Not every representative of the team will be a professional accountant, they would all

be qualified in reporting processes and guidelines. A organization can help to guarantee full

accountability of its financial dealings by creating an accounting section, while also providing

advanced, streamlined aid to other divisions and executives. The accounting staff will contribute

to the company's long-term viability. A corporation 's accounting division provides financial and

monetary support to the organization. This division holds trading receivables and payable,

inventory, salaries, investment securities, and other monetary facets. Bookkeepers in this

department review each division's records to determine corporation's fiscal position and any

changes needed to properly administer the organization (Klačmer Čalopa, 2017).

Accounting is the foundation of the business's finance unit. This department is in control

of both reporting, accruals, and deferred revenue, and also balance sheet preparation, banking

details, cash-flow reports, and daily operations bookkeeping and oversight. External assessments

and protections, as well as taxes and transparency, are both regulated and supervised by this

3

Financial decision-making relates to set of activities that allows a business's management

to take a variety of decisions quickly and appropriately. This enables them to assure that

organisations are prepared to learn how to interpret and view fiscal analytical estimates, and

information in order to make a variety of short, mid, and long-term decisions. When it comes to

the use of money, fiscal decision-making is practice of weighing the benefits and drawbacks

of decision. Efficient fiscal decision-making is requirement for financial wellbeing (Valaskova,

Bartosova and Kubala, 2019). This report focuses on the Skanska PLC, which is UK-based

Constructions and Engineering Organization situated in the Hertfordshire, UK. Over the next ten

years, the company intends to expand into European countries and grow its market position.

This research will go into great detail on determining the worth of accounting and finance

activities. A systematic analysis of the different ratios will also be undertaken out as part

of study.

TASK 1

Importance of Accounting and Finance functions, duties and roles:

The Finance department is trained team of employees who manage a company 's financial

functions. Not every representative of the team will be a professional accountant, they would all

be qualified in reporting processes and guidelines. A organization can help to guarantee full

accountability of its financial dealings by creating an accounting section, while also providing

advanced, streamlined aid to other divisions and executives. The accounting staff will contribute

to the company's long-term viability. A corporation 's accounting division provides financial and

monetary support to the organization. This division holds trading receivables and payable,

inventory, salaries, investment securities, and other monetary facets. Bookkeepers in this

department review each division's records to determine corporation's fiscal position and any

changes needed to properly administer the organization (Klačmer Čalopa, 2017).

Accounting is the foundation of the business's finance unit. This department is in control

of both reporting, accruals, and deferred revenue, and also balance sheet preparation, banking

details, cash-flow reports, and daily operations bookkeeping and oversight. External assessments

and protections, as well as taxes and transparency, are both regulated and supervised by this

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

agency. It guarantees that the corporation is in good financial standing and conforms with all

relevant legislations (Alderman, Forsyth and Walton, 2017).

Both depts are important divisions in every company. As a consequence, it is required of

businesses to use it consistently and correctly to determine their financial situation. Skanska

management must analyse the different roles of both departments in attempt to make productive

decisions while the company expects to expand into European countries over coming 10 years.

The foregoing is an analysis of the significance, functions, and responsibilities of Accounting

and Finance-division in background of SKANSA Corporation:

Managing the Inventories: The accounting and finances department may in charge of keeping

track of and overseeing the corporation 's inventories and materials. Almost no division, apart

from the finance section, is well trained to work for stockholdings. A range of computational

formulas are used to log and control the inventories. Particularly unique approaches are

employed to monitor and maintain the inventory quantities that define the financing department's

comparative benefit. The accounting and financing division of the SKANSKA company must be

capable of adequately managing and monitoring inventory processes. Stock preparation will help

SKANSKA PLC determine if restocking is required or whether inventory levels are running low.

This will also assure that items have the right leading duration as they are required (Andjelic and

Vesic, 2017).

Treasury management tasks: Both employees who deal in money or money equivalents are

subjected to a treasury administration plan established by accounting and finance division.

Treasury preparation includes information on the amount of risk that the business will carry on

at specified period. The finance/accounting administrator oversees treasury operations, while

the chief financial officer oversees financial reporting.

Handling Bookkeeping Process: This is the most basic feature of the finances and accounting

unit. In a regular basis this includes the reporting, analysis, and interpretation of a business's

fiscal operations This will include tracking all expenditures (investment funds, purchases and so

forth) and also finalised product transactions. In a business, this job is usually held

by bookkeeper, however as the company grows and expands, it may be occupied by more

competent employees.

Managing business cash flows: The accounting and financial division is in charge of overseeing

all free cash flows in and out of firm, and also making sure that adequate funds are adequate to

4

relevant legislations (Alderman, Forsyth and Walton, 2017).

Both depts are important divisions in every company. As a consequence, it is required of

businesses to use it consistently and correctly to determine their financial situation. Skanska

management must analyse the different roles of both departments in attempt to make productive

decisions while the company expects to expand into European countries over coming 10 years.

The foregoing is an analysis of the significance, functions, and responsibilities of Accounting

and Finance-division in background of SKANSA Corporation:

Managing the Inventories: The accounting and finances department may in charge of keeping

track of and overseeing the corporation 's inventories and materials. Almost no division, apart

from the finance section, is well trained to work for stockholdings. A range of computational

formulas are used to log and control the inventories. Particularly unique approaches are

employed to monitor and maintain the inventory quantities that define the financing department's

comparative benefit. The accounting and financing division of the SKANSKA company must be

capable of adequately managing and monitoring inventory processes. Stock preparation will help

SKANSKA PLC determine if restocking is required or whether inventory levels are running low.

This will also assure that items have the right leading duration as they are required (Andjelic and

Vesic, 2017).

Treasury management tasks: Both employees who deal in money or money equivalents are

subjected to a treasury administration plan established by accounting and finance division.

Treasury preparation includes information on the amount of risk that the business will carry on

at specified period. The finance/accounting administrator oversees treasury operations, while

the chief financial officer oversees financial reporting.

Handling Bookkeeping Process: This is the most basic feature of the finances and accounting

unit. In a regular basis this includes the reporting, analysis, and interpretation of a business's

fiscal operations This will include tracking all expenditures (investment funds, purchases and so

forth) and also finalised product transactions. In a business, this job is usually held

by bookkeeper, however as the company grows and expands, it may be occupied by more

competent employees.

Managing business cash flows: The accounting and financial division is in charge of overseeing

all free cash flows in and out of firm, and also making sure that adequate funds are adequate to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

meet the company's day-to-day requires. This section also oversees the company's credits and

payments activities, which ensure that customers and vendors are billed on schedule and

correctly, and that organisation is compensated on schedule and appropriately.

Financial Reporting analysis: The purpose of financial monitoring and assessment is to

translate raw accounting inputs into appropriate, readable, and comparable financial reports. The

financing and accounting division drives organizational success by regularly reviewing and

reporting critical statistics critical to the organisation's results. This would almost definitely

provide a summary of all financing streams, investments, and funds put aside for future use

(excepting those set aside and intended for the present phase and also any non-financial details.

They are usually introduced to managers in a fair and intuitive way (Vitale and Cull, 2018).

Managing Company’s Investments: The accounting and finance section is usually in charge of

managing the firm's existing assets as well as updating and selecting new assets/investments.

Aside from fixed investments, the finance division should focus on liquid assets. Since it has a

greater impact on an organisation's liquidity than its financial assets, operating capital must be

managed adequately in addition to maximize profitability relative to the total amount of funds

bound up.

Help executives in major strategic decisions: The financing and accounts team delivers

information to organizational executives to assist them in making financial decisions such as

which sectors or projects to enter, repayment schedules for massive capital acquisitions,

determining how much of organisation's profits can be distributed as dividend payouts and how

percent would be recouped in the enterprise, and determining the best funding strategy that

would generate the firm's profitability.

Budgeting Processes: Budgeting act as crucial part of every company. This should be

accomplished efficiently because the organization 's long viability is largely contingent on how

adequately budgets are formulated. The finance accounting section is often in charge of

budgeting because they have access to the whole list of statistics in the business. Only the

accounting department is capable of reviewing figures in order to determine the entity's current

position Budgets allow customers to imagine the potential, so the department must be profitable

sufficiently to do so. Budgeting is relevant for all organizations, big and medium and SKANSKA

Limited, as a well-known large enterprise, needs a substantial degree of strategic preparation to

address the demands of the sector. In terms of current industry evaluations as well as the position

5

payments activities, which ensure that customers and vendors are billed on schedule and

correctly, and that organisation is compensated on schedule and appropriately.

Financial Reporting analysis: The purpose of financial monitoring and assessment is to

translate raw accounting inputs into appropriate, readable, and comparable financial reports. The

financing and accounting division drives organizational success by regularly reviewing and

reporting critical statistics critical to the organisation's results. This would almost definitely

provide a summary of all financing streams, investments, and funds put aside for future use

(excepting those set aside and intended for the present phase and also any non-financial details.

They are usually introduced to managers in a fair and intuitive way (Vitale and Cull, 2018).

Managing Company’s Investments: The accounting and finance section is usually in charge of

managing the firm's existing assets as well as updating and selecting new assets/investments.

Aside from fixed investments, the finance division should focus on liquid assets. Since it has a

greater impact on an organisation's liquidity than its financial assets, operating capital must be

managed adequately in addition to maximize profitability relative to the total amount of funds

bound up.

Help executives in major strategic decisions: The financing and accounts team delivers

information to organizational executives to assist them in making financial decisions such as

which sectors or projects to enter, repayment schedules for massive capital acquisitions,

determining how much of organisation's profits can be distributed as dividend payouts and how

percent would be recouped in the enterprise, and determining the best funding strategy that

would generate the firm's profitability.

Budgeting Processes: Budgeting act as crucial part of every company. This should be

accomplished efficiently because the organization 's long viability is largely contingent on how

adequately budgets are formulated. The finance accounting section is often in charge of

budgeting because they have access to the whole list of statistics in the business. Only the

accounting department is capable of reviewing figures in order to determine the entity's current

position Budgets allow customers to imagine the potential, so the department must be profitable

sufficiently to do so. Budgeting is relevant for all organizations, big and medium and SKANSKA

Limited, as a well-known large enterprise, needs a substantial degree of strategic preparation to

address the demands of the sector. In terms of current industry evaluations as well as the position

5

of rival firms, SKANSKA Organization must determine what targets can be established. Without

appropriate budgeting plans, no accurate forecast can be made.

Advising and arrange sources of longer-term finance: Financing and accounts dept's job is to

guide enterprises about the best funding combination for all of them including to facilitate them

in securing longer-term capital at lowest possible cost in retaining an adequate liquidity base.

Handling Tax Issue: Taxation are indeed an inevitable part of running a company, and the

financing division has responsibility of coping with these. This includes developing good

business relationships with the authorities by disbursing PAYE to proper authority, as well as

ensuring that tax concerns are resolved in line with current regulations (Chhapra, Kashif, Rehan

and Bai 2018.).

Handling Business Risks: Risk control/management is also handled by the enterprise's finance

and accounting unit. They are accountable for defining assessing, setting priorities, and reducing

the threats that the organization faces. The finance unit predicts external changes for a particular

model that isn't doing well enough. They represent global events including the recession of the

economic system, currency fluctuations, and so forth. They use most of their powers and abilities

to minimize the consequences while keeping a close watch on the circumstance for potential

changes. Through anticipating and being knowledgeable of market trends and investment

opportunities, risks management further aids in the maximising of venture outcomes.

Capital Budgeting Processes: This is activity of studying and identifying programs and

opportunities in the economy which are worthwhile to participate in. Property, sales,

restructurings, and the purchase of fixed assets are all examples of its use. The whole definition

of market capital budgeting centers around the ultimate objective of increasing profitability.

They continue to boost profits in attempt to sustain the business's wealth growing.

The accounting and finance unit of SKANSKA business will have several benefits to the

corporation. The unit would be more likely to persuade investors if it presented the best portrait

of financial sustainability. Furthermore, the organization will be able to create a proper balance

between risks and benefit value creation. The fiscal management principle also assists the

organization in making systematic and well-organized choices. SKANSKA Group can also gain

a competitive advantage by being able to easily respond to any financial-related issues. Among

the most important factors for the unit's operational practices to run seamlessly is the influx of

funding to better cover the unit's expenditures (Kourtis, Kourtis and Curtis, 2019).

6

appropriate budgeting plans, no accurate forecast can be made.

Advising and arrange sources of longer-term finance: Financing and accounts dept's job is to

guide enterprises about the best funding combination for all of them including to facilitate them

in securing longer-term capital at lowest possible cost in retaining an adequate liquidity base.

Handling Tax Issue: Taxation are indeed an inevitable part of running a company, and the

financing division has responsibility of coping with these. This includes developing good

business relationships with the authorities by disbursing PAYE to proper authority, as well as

ensuring that tax concerns are resolved in line with current regulations (Chhapra, Kashif, Rehan

and Bai 2018.).

Handling Business Risks: Risk control/management is also handled by the enterprise's finance

and accounting unit. They are accountable for defining assessing, setting priorities, and reducing

the threats that the organization faces. The finance unit predicts external changes for a particular

model that isn't doing well enough. They represent global events including the recession of the

economic system, currency fluctuations, and so forth. They use most of their powers and abilities

to minimize the consequences while keeping a close watch on the circumstance for potential

changes. Through anticipating and being knowledgeable of market trends and investment

opportunities, risks management further aids in the maximising of venture outcomes.

Capital Budgeting Processes: This is activity of studying and identifying programs and

opportunities in the economy which are worthwhile to participate in. Property, sales,

restructurings, and the purchase of fixed assets are all examples of its use. The whole definition

of market capital budgeting centers around the ultimate objective of increasing profitability.

They continue to boost profits in attempt to sustain the business's wealth growing.

The accounting and finance unit of SKANSKA business will have several benefits to the

corporation. The unit would be more likely to persuade investors if it presented the best portrait

of financial sustainability. Furthermore, the organization will be able to create a proper balance

between risks and benefit value creation. The fiscal management principle also assists the

organization in making systematic and well-organized choices. SKANSKA Group can also gain

a competitive advantage by being able to easily respond to any financial-related issues. Among

the most important factors for the unit's operational practices to run seamlessly is the influx of

funding to better cover the unit's expenditures (Kourtis, Kourtis and Curtis, 2019).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

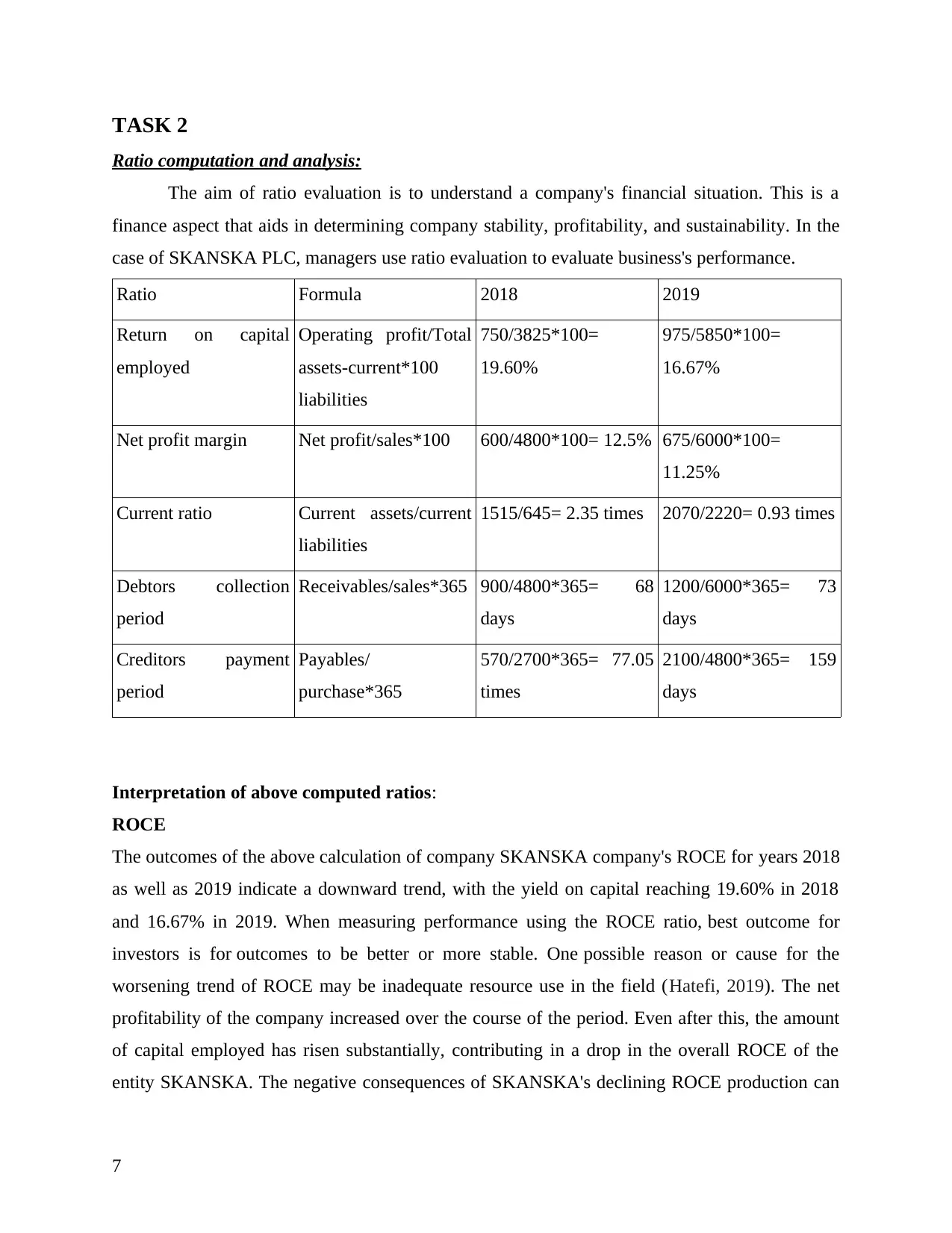

TASK 2

Ratio computation and analysis:

The aim of ratio evaluation is to understand a company's financial situation. This is a

finance aspect that aids in determining company stability, profitability, and sustainability. In the

case of SKANSKA PLC, managers use ratio evaluation to evaluate business's performance.

Ratio Formula 2018 2019

Return on capital

employed

Operating profit/Total

assets-current*100

liabilities

750/3825*100=

19.60%

975/5850*100=

16.67%

Net profit margin Net profit/sales*100 600/4800*100= 12.5% 675/6000*100=

11.25%

Current ratio Current assets/current

liabilities

1515/645= 2.35 times 2070/2220= 0.93 times

Debtors collection

period

Receivables/sales*365 900/4800*365= 68

days

1200/6000*365= 73

days

Creditors payment

period

Payables/

purchase*365

570/2700*365= 77.05

times

2100/4800*365= 159

days

Interpretation of above computed ratios:

ROCE

The outcomes of the above calculation of company SKANSKA company's ROCE for years 2018

as well as 2019 indicate a downward trend, with the yield on capital reaching 19.60% in 2018

and 16.67% in 2019. When measuring performance using the ROCE ratio, best outcome for

investors is for outcomes to be better or more stable. One possible reason or cause for the

worsening trend of ROCE may be inadequate resource use in the field (Hatefi, 2019). The net

profitability of the company increased over the course of the period. Even after this, the amount

of capital employed has risen substantially, contributing in a drop in the overall ROCE of the

entity SKANSKA. The negative consequences of SKANSKA's declining ROCE production can

7

Ratio computation and analysis:

The aim of ratio evaluation is to understand a company's financial situation. This is a

finance aspect that aids in determining company stability, profitability, and sustainability. In the

case of SKANSKA PLC, managers use ratio evaluation to evaluate business's performance.

Ratio Formula 2018 2019

Return on capital

employed

Operating profit/Total

assets-current*100

liabilities

750/3825*100=

19.60%

975/5850*100=

16.67%

Net profit margin Net profit/sales*100 600/4800*100= 12.5% 675/6000*100=

11.25%

Current ratio Current assets/current

liabilities

1515/645= 2.35 times 2070/2220= 0.93 times

Debtors collection

period

Receivables/sales*365 900/4800*365= 68

days

1200/6000*365= 73

days

Creditors payment

period

Payables/

purchase*365

570/2700*365= 77.05

times

2100/4800*365= 159

days

Interpretation of above computed ratios:

ROCE

The outcomes of the above calculation of company SKANSKA company's ROCE for years 2018

as well as 2019 indicate a downward trend, with the yield on capital reaching 19.60% in 2018

and 16.67% in 2019. When measuring performance using the ROCE ratio, best outcome for

investors is for outcomes to be better or more stable. One possible reason or cause for the

worsening trend of ROCE may be inadequate resource use in the field (Hatefi, 2019). The net

profitability of the company increased over the course of the period. Even after this, the amount

of capital employed has risen substantially, contributing in a drop in the overall ROCE of the

entity SKANSKA. The negative consequences of SKANSKA's declining ROCE production can

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be important. The downward pattern of ROCE proportion reduces consumer demand since it

produces a detrimental impression of inefficient resource utilization. A decline of equity

resources would also lead to a scarcity of capital sources, restricting the business's potential to

receive funding assistance.

Net-profit Margin:

According to the aforementioned percentage figures, the net profitability ratio in

timespan 2018 is 12.5 percent, whereas the percentage in 2019 is 11.25 percent. This indicates a

declining trend that is harmful to the company. The primary trigger of this downwards tendency

could be a lack of control over overhead costs. Regardless of fact that sales and net

profitability are still up significantly. Even so, the increase in running expenses exceeds the

increase in sales and gross margin. A large increase in sales is meaningless if the corporation

cannot manage its expenses. The declining net profit ratios would have an effect on the firm's

prosperity. Profit margins are transformed into retained earnings which increases the firm's net

equity. Even so, if earnings are affected, it would have a negative effect on cash, putting the

business's profit maximising objective in jeopardy even further. That wouldn't be possible to

achieve the goal of value maximization (Subalakshmi and Manikandan, 2018).

Current Ratio:

According to the findings of current ratio estimate, ratio were 2.35:1 in 2018 and 0.932:1

in 2019, reflecting a continuing declining trajectory in financial situation. Current assets keep

growing rapidly, but liabilities are rising much faster, adversely impacting the corporation's

overall results. Even though current assets being transformed to money the proceeds would not

be enough to offset the obligations. That as the amount owed rises, some changes in liquidity

ratio will cause the organization to experience liquidity problems. The company owes them

money yet it would be unable to repay them. The company owes them funds but this is incapable

to repay them. Meeting covenants will put the business's ability to continue as going concern in

risk.

Debtors collection period

Based on the aforementioned ratio matrices, it has been determined that the cumulative

receivables periods for the year 2018 are approximately 68 days, while the figure for the year

2019 is approximately 73 days. The rise in duration is negative since it means that the

corporation would have to wait longer to receive revenue from accounts receivables. The overall

8

produces a detrimental impression of inefficient resource utilization. A decline of equity

resources would also lead to a scarcity of capital sources, restricting the business's potential to

receive funding assistance.

Net-profit Margin:

According to the aforementioned percentage figures, the net profitability ratio in

timespan 2018 is 12.5 percent, whereas the percentage in 2019 is 11.25 percent. This indicates a

declining trend that is harmful to the company. The primary trigger of this downwards tendency

could be a lack of control over overhead costs. Regardless of fact that sales and net

profitability are still up significantly. Even so, the increase in running expenses exceeds the

increase in sales and gross margin. A large increase in sales is meaningless if the corporation

cannot manage its expenses. The declining net profit ratios would have an effect on the firm's

prosperity. Profit margins are transformed into retained earnings which increases the firm's net

equity. Even so, if earnings are affected, it would have a negative effect on cash, putting the

business's profit maximising objective in jeopardy even further. That wouldn't be possible to

achieve the goal of value maximization (Subalakshmi and Manikandan, 2018).

Current Ratio:

According to the findings of current ratio estimate, ratio were 2.35:1 in 2018 and 0.932:1

in 2019, reflecting a continuing declining trajectory in financial situation. Current assets keep

growing rapidly, but liabilities are rising much faster, adversely impacting the corporation's

overall results. Even though current assets being transformed to money the proceeds would not

be enough to offset the obligations. That as the amount owed rises, some changes in liquidity

ratio will cause the organization to experience liquidity problems. The company owes them

money yet it would be unable to repay them. The company owes them funds but this is incapable

to repay them. Meeting covenants will put the business's ability to continue as going concern in

risk.

Debtors collection period

Based on the aforementioned ratio matrices, it has been determined that the cumulative

receivables periods for the year 2018 are approximately 68 days, while the figure for the year

2019 is approximately 73 days. The rise in duration is negative since it means that the

corporation would have to wait longer to receive revenue from accounts receivables. The overall

8

compilation period in 2018 is shorter, implying that total amount of collection being completed

in a shorter period of duration. As per 2019 data, the no. of days have increased, causing a delay

in payment collection. The principal consequence for this surge is that trade debtors are either

reluctant or unwilling to settle their debts. The impact of an increasing number of days is that the

risk of trade debtors default increases, causing an increase in bad-debts expense on income

statement. Since total efficiency will be harmed as a result of these consequences, overall

profitability would decline. If payment defaults increase, the likelihood of no repayment

increases, and those account receivables become more prone to defaults (Hilkevics and

Semakina, 2019).

Creditors collection period:

According to the calculations in the figure, the total payable span in 2018 was

approximately 77 days, and in 2019 it was approximately 159 days. Both figures indicate a large

disparity. The larger the damage, the longer the pay-out duration. The main reason for the

increase in payables days is that the company does not have adequate cash to repay its vendors.

This demonstrates that the company is having difficulty paying its vendors due to a lack of

revenue. The effect of the increase for multiple days would've been negative, since the

corporation will face increased cash flow issues as result of inadequate revenue, making it

difficult for the company to fulfil all of its commitments and investments at same period. A lack

of supplier reputation may also be a function of longer overall payment period A company's

value or credibility will be doubted in the eyes of suppliers. The vendors would be reluctant to

supply any additional goods in order to avoid losing their money. Suppliers are the backbone of

every enterprise, and breaching their terms would have a negative impact on the whole selling

string.

CONCLUSION

From the aforementioned report this has been articulated that Accounting and finance are

critical aspects of an entity's management. Businesses compete for profitability and funds at the

completion of each day, and when cash is mishandled, the organization as a result is

unsustainable. By efficiently handling the accounts and finances of the corporation's

expenditures and earnings, the flow of funds could be controlled and calculated, thereby steering

the corporation in the right direction. To develop a successful financial strategy that supports the

9

in a shorter period of duration. As per 2019 data, the no. of days have increased, causing a delay

in payment collection. The principal consequence for this surge is that trade debtors are either

reluctant or unwilling to settle their debts. The impact of an increasing number of days is that the

risk of trade debtors default increases, causing an increase in bad-debts expense on income

statement. Since total efficiency will be harmed as a result of these consequences, overall

profitability would decline. If payment defaults increase, the likelihood of no repayment

increases, and those account receivables become more prone to defaults (Hilkevics and

Semakina, 2019).

Creditors collection period:

According to the calculations in the figure, the total payable span in 2018 was

approximately 77 days, and in 2019 it was approximately 159 days. Both figures indicate a large

disparity. The larger the damage, the longer the pay-out duration. The main reason for the

increase in payables days is that the company does not have adequate cash to repay its vendors.

This demonstrates that the company is having difficulty paying its vendors due to a lack of

revenue. The effect of the increase for multiple days would've been negative, since the

corporation will face increased cash flow issues as result of inadequate revenue, making it

difficult for the company to fulfil all of its commitments and investments at same period. A lack

of supplier reputation may also be a function of longer overall payment period A company's

value or credibility will be doubted in the eyes of suppliers. The vendors would be reluctant to

supply any additional goods in order to avoid losing their money. Suppliers are the backbone of

every enterprise, and breaching their terms would have a negative impact on the whole selling

string.

CONCLUSION

From the aforementioned report this has been articulated that Accounting and finance are

critical aspects of an entity's management. Businesses compete for profitability and funds at the

completion of each day, and when cash is mishandled, the organization as a result is

unsustainable. By efficiently handling the accounts and finances of the corporation's

expenditures and earnings, the flow of funds could be controlled and calculated, thereby steering

the corporation in the right direction. To develop a successful financial strategy that supports the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company's priorities, finance managers or managers must take into account and grasp every

component of the organisation 's strategic goals.

10

component of the organisation 's strategic goals.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Alderman, J., Forsyth, J. and Walton, R., 2017. How religious beliefs influence financial

decision-making. 2017 Volume 20 Issue 3, (3).

Andjelic, S. and Vesic, T., 2017. The importance of financial analysis for business decision

making. In Book of proceedings from Sixth International Scientific Conference

Employment, Education and Entrepreneurship (pp. 9-25).

Chhapra, I.U., Kashif, M., Rehan, R. and Bai, A., 2018. An empirical investigation of investors

behavioral biases on financial decision making. Asian Journal of Empirical

Research, 8(3), pp.99-109.

Hatefi, M.A., 2019. Indifference threshold-based attribute ratio analysis: A method for assigning

the weights to the attributes in multiple attribute decision making. Applied Soft

Computing, 74, pp.643-651.

Hilkevics, S. and Semakina, V., 2019. The classification and comparison of business ratios

analysis methods. Insights into Regional Development, 1(1), pp.47-56.

Klačmer Čalopa, M., 2017. Business owner and manager’s attitudes towards financial decision-

making and strategic planning: Evidence from Croatian SMEs. Management: journal of

contemporary management issues, 22(1), pp.103-116.

Kourtis, E., Kourtis, G. and Curtis, P., 2019. Αn Integrated Financial Ratio Analysis as a

Navigation Compass through the Fraudulent Reporting Conundrum: Α Case

Study. International Journal of Finance, Insurance and Risk Management, 9(1-2), pp.3-

20.

Subalakshmi, S. and Manikandan, M., 2018. Financial Ratio Analysis of SBI [2009-

2016]. ICTACT Journal on Management Studies, 4(01), pp.2395-1664.

Valaskova, K., Bartosova, V. and Kubala, P., 2019. Behavioural aspects of the financial

decision-making. Organizacija, 52(1), pp.22-31.

Vitale, C. and Cull, M., 2018. Modelling the influence of CEO values and leadership styles on

financial decision making. The Journal of New Business Ideas & Trends, 16(1), pp.16-

30.

11

Books and Journals:

Alderman, J., Forsyth, J. and Walton, R., 2017. How religious beliefs influence financial

decision-making. 2017 Volume 20 Issue 3, (3).

Andjelic, S. and Vesic, T., 2017. The importance of financial analysis for business decision

making. In Book of proceedings from Sixth International Scientific Conference

Employment, Education and Entrepreneurship (pp. 9-25).

Chhapra, I.U., Kashif, M., Rehan, R. and Bai, A., 2018. An empirical investigation of investors

behavioral biases on financial decision making. Asian Journal of Empirical

Research, 8(3), pp.99-109.

Hatefi, M.A., 2019. Indifference threshold-based attribute ratio analysis: A method for assigning

the weights to the attributes in multiple attribute decision making. Applied Soft

Computing, 74, pp.643-651.

Hilkevics, S. and Semakina, V., 2019. The classification and comparison of business ratios

analysis methods. Insights into Regional Development, 1(1), pp.47-56.

Klačmer Čalopa, M., 2017. Business owner and manager’s attitudes towards financial decision-

making and strategic planning: Evidence from Croatian SMEs. Management: journal of

contemporary management issues, 22(1), pp.103-116.

Kourtis, E., Kourtis, G. and Curtis, P., 2019. Αn Integrated Financial Ratio Analysis as a

Navigation Compass through the Fraudulent Reporting Conundrum: Α Case

Study. International Journal of Finance, Insurance and Risk Management, 9(1-2), pp.3-

20.

Subalakshmi, S. and Manikandan, M., 2018. Financial Ratio Analysis of SBI [2009-

2016]. ICTACT Journal on Management Studies, 4(01), pp.2395-1664.

Valaskova, K., Bartosova, V. and Kubala, P., 2019. Behavioural aspects of the financial

decision-making. Organizacija, 52(1), pp.22-31.

Vitale, C. and Cull, M., 2018. Modelling the influence of CEO values and leadership styles on

financial decision making. The Journal of New Business Ideas & Trends, 16(1), pp.16-

30.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.