ACC544, Decision Support Tools: Finance Assignment 3, Semester 2

VerifiedAdded on 2022/10/17

|16

|2727

|7

Homework Assignment

AI Summary

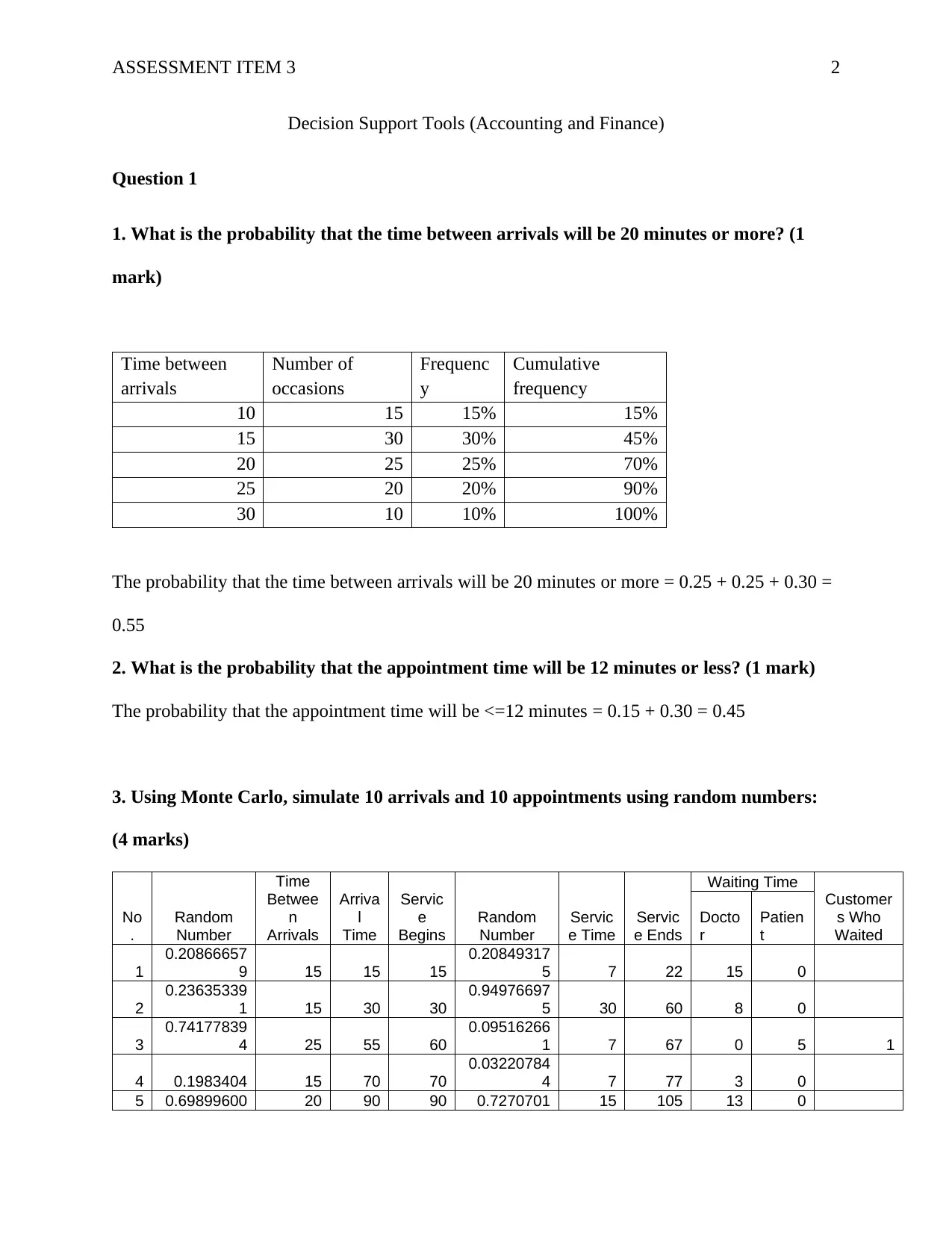

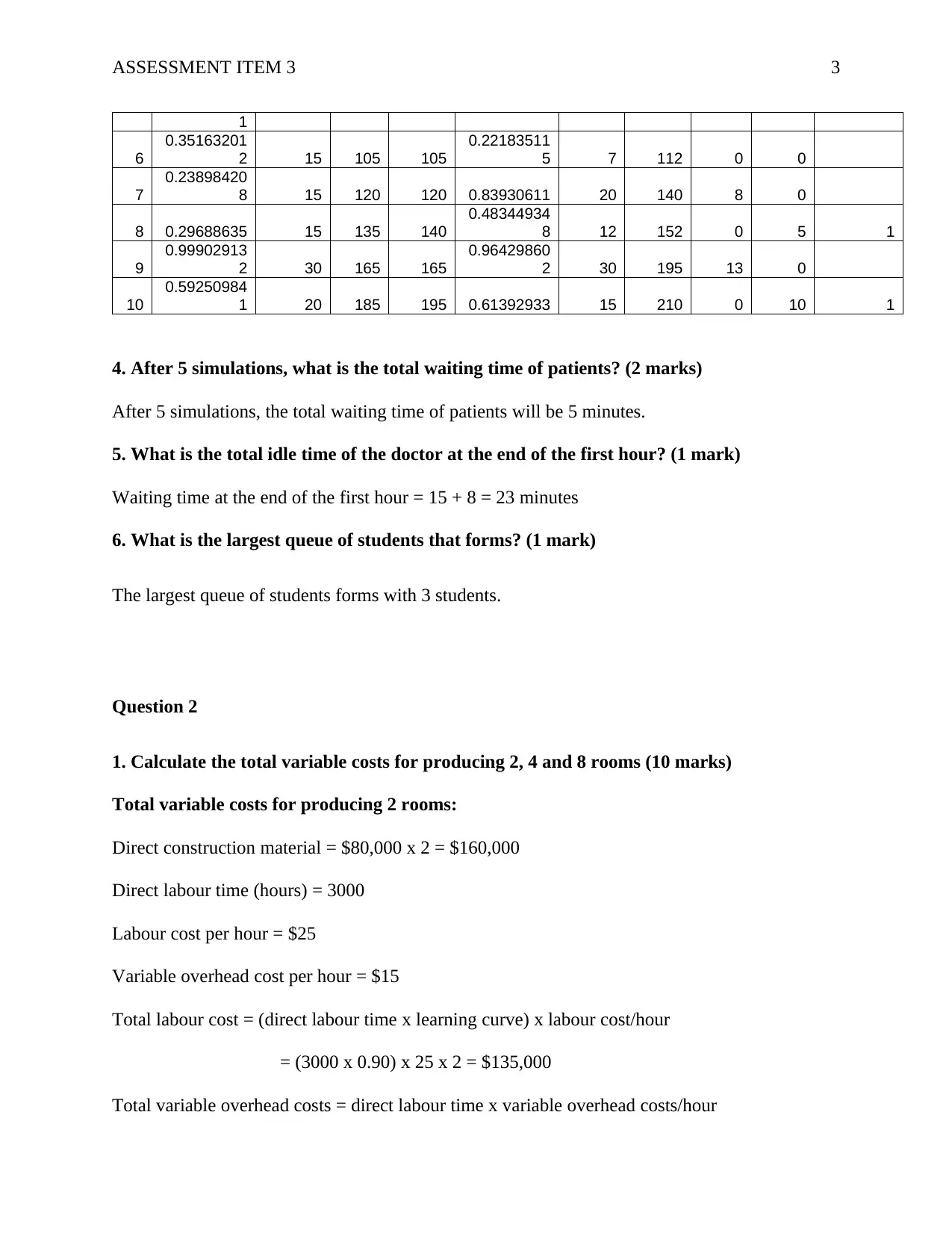

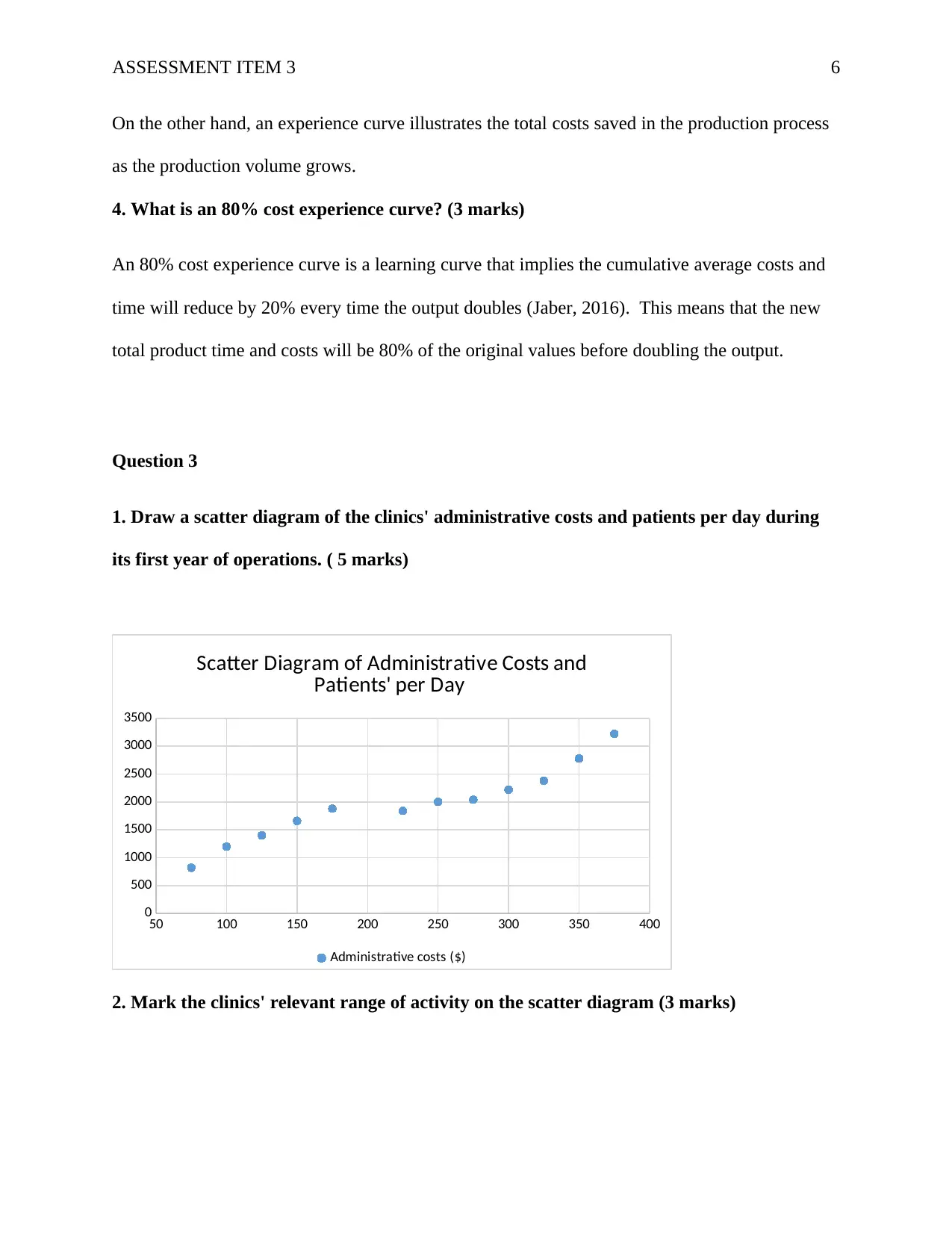

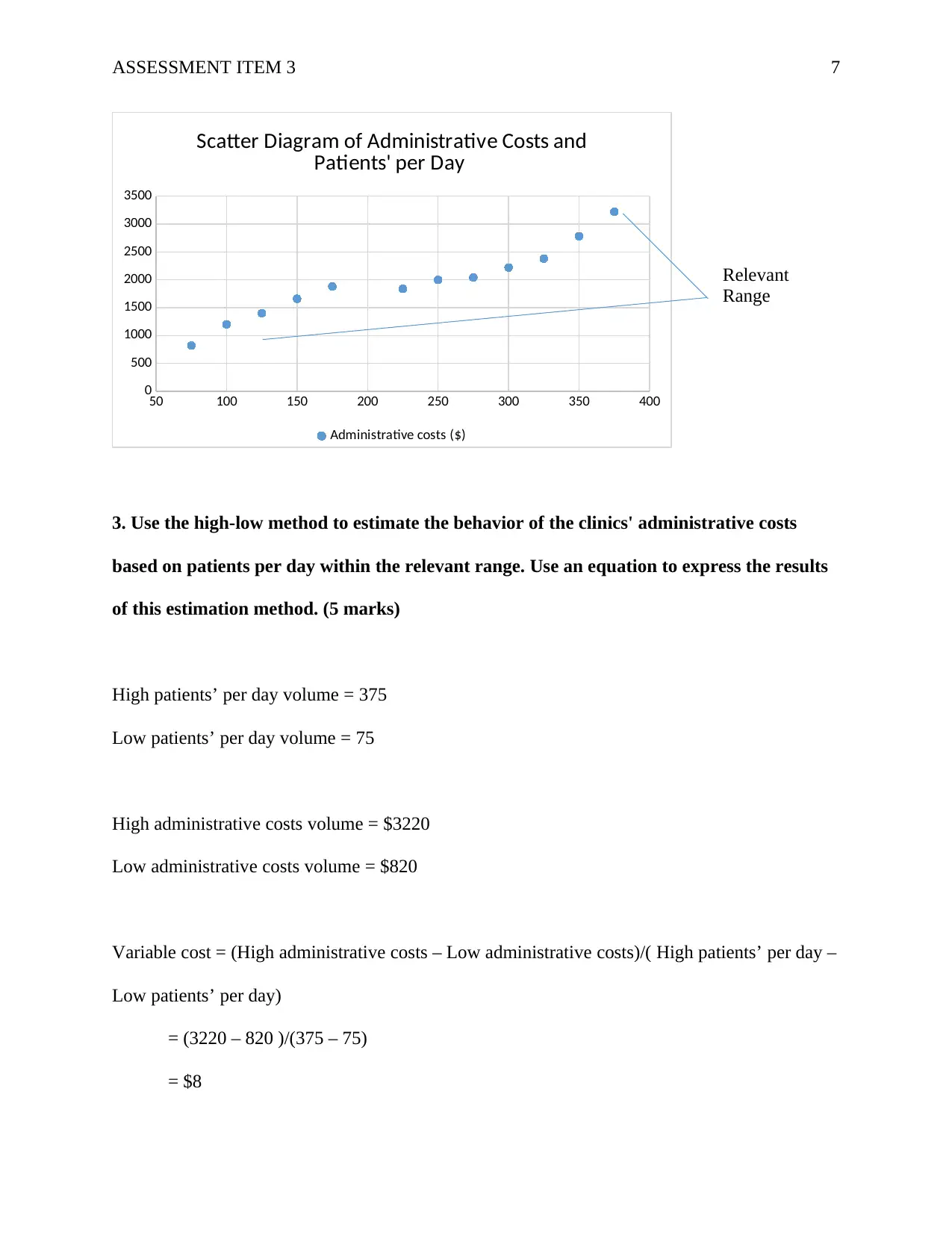

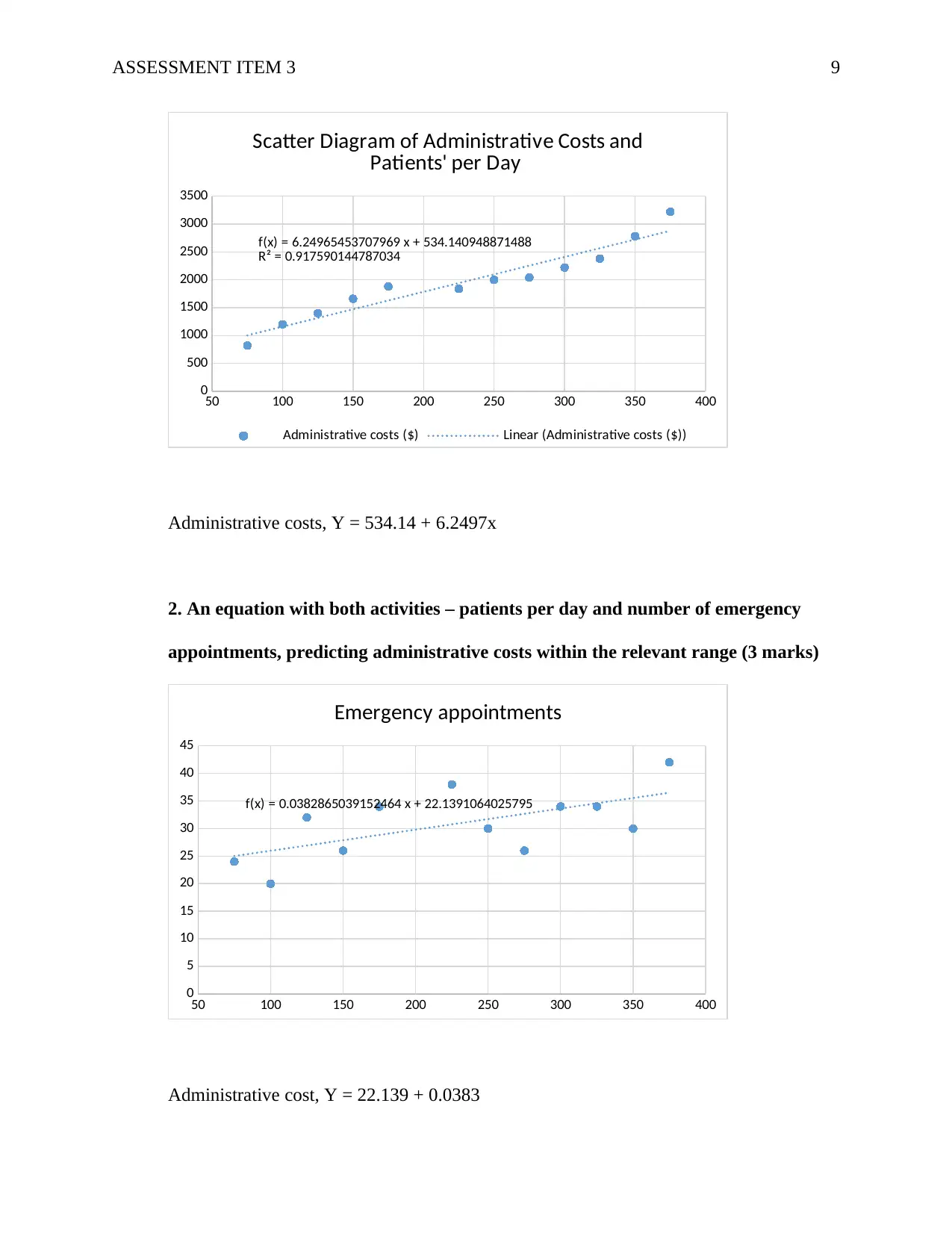

This assignment solution for ACC544, Decision Support Tools, addresses several key areas of finance and decision-making. Question 1 focuses on queuing theory and Monte Carlo simulation, involving probability calculations and simulating arrivals and appointments to analyze waiting times and idle time. Question 2 delves into cost accounting, requiring the calculation of variable costs, an explanation of learning and experience curves, and their role in cost estimation, including an 80% cost experience curve. Question 3 applies regression analysis to estimate administrative costs based on patient volume, employing the high-low method and creating a scatter diagram. It also predicts costs and uses regression models to analyze the impact of additional cost drivers. Question 4 deals with financial planning, including budgeting, break-even analysis, and the impact of changing costs and sales mix on profitability. The solution includes determining a budgeted net profit, calculating break-even points under different scenarios, and providing a memo to management with recommendations. The assignment covers a range of topics including simulation, cost accounting, regression, and financial planning, providing a comprehensive overview of decision support tools in a financial context.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.