Comprehensive Analysis of Decision Support Tools in Finance

VerifiedAdded on 2020/11/23

|18

|2599

|500

Homework Assignment

AI Summary

This assignment delves into the application of various decision support tools within a financial context. It begins with an exploration of decision analysis, including assessing utility functions and standard gamble techniques to evaluate investment scenarios in the share market. The assignment then covers the value of information, analyzing prior and posterior probabilities to determine expected net gains and losses from market research. Monte Carlo simulation and regression analysis are also employed to evaluate different financial models. Furthermore, the assignment uses CVP (Cost-Volume-Profit) analysis to determine break-even points and contribution margins for different products. The solution provides detailed calculations and explanations for each section, offering a comprehensive understanding of these crucial financial decision-making tools.

Decision Support Tools

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1: DECISION ANALYSIS.........................................................................................4

A. Assessing the utility function as well as standard gamble which helps in determining utility

value.............................................................................................................................................4

B. Investing primarily in share market........................................................................................4

1...................................................................................................................................................4

2...................................................................................................................................................5

3...................................................................................................................................................5

4...................................................................................................................................................5

5...................................................................................................................................................5

6...................................................................................................................................................5

QUESTION 2: VALUE OF INFORMATION................................................................................6

a....................................................................................................................................................6

B. Analyzing the prior probability...............................................................................................6

C. Posterior probability................................................................................................................7

D. Expected net gain and loss after conducting the market research..........................................7

QUESTION 3 MONTE CARLO SIMULATION...........................................................................7

a....................................................................................................................................................7

b...................................................................................................................................................7

QUESTION 4 REGRESSION ANALYSIS....................................................................................8

a....................................................................................................................................................8

b...................................................................................................................................................8

c..................................................................................................................................................12

d.................................................................................................................................................12

QUESTION 5: CVP ANALYSIS..................................................................................................13

QUESTION 1: DECISION ANALYSIS.........................................................................................4

A. Assessing the utility function as well as standard gamble which helps in determining utility

value.............................................................................................................................................4

B. Investing primarily in share market........................................................................................4

1...................................................................................................................................................4

2...................................................................................................................................................5

3...................................................................................................................................................5

4...................................................................................................................................................5

5...................................................................................................................................................5

6...................................................................................................................................................5

QUESTION 2: VALUE OF INFORMATION................................................................................6

a....................................................................................................................................................6

B. Analyzing the prior probability...............................................................................................6

C. Posterior probability................................................................................................................7

D. Expected net gain and loss after conducting the market research..........................................7

QUESTION 3 MONTE CARLO SIMULATION...........................................................................7

a....................................................................................................................................................7

b...................................................................................................................................................7

QUESTION 4 REGRESSION ANALYSIS....................................................................................8

a....................................................................................................................................................8

b...................................................................................................................................................8

c..................................................................................................................................................12

d.................................................................................................................................................12

QUESTION 5: CVP ANALYSIS..................................................................................................13

a..................................................................................................................................................13

b.................................................................................................................................................13

c..................................................................................................................................................14

d.................................................................................................................................................14

D (i)............................................................................................................................................14

D (ii)...........................................................................................................................................14

b.................................................................................................................................................13

c..................................................................................................................................................14

d.................................................................................................................................................14

D (i)............................................................................................................................................14

D (ii)...........................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

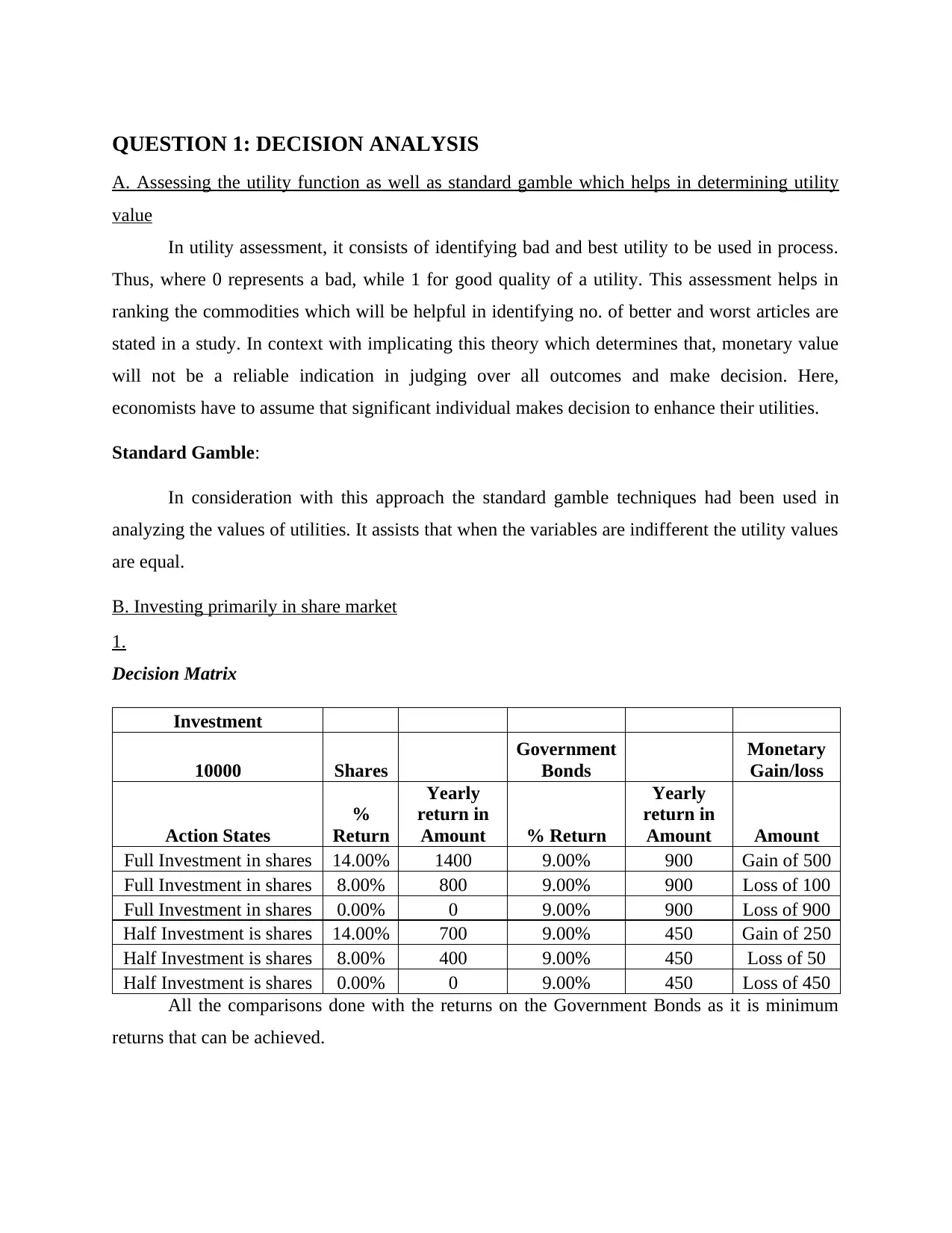

QUESTION 1: DECISION ANALYSIS

A. Assessing the utility function as well as standard gamble which helps in determining utility

value

In utility assessment, it consists of identifying bad and best utility to be used in process.

Thus, where 0 represents a bad, while 1 for good quality of a utility. This assessment helps in

ranking the commodities which will be helpful in identifying no. of better and worst articles are

stated in a study. In context with implicating this theory which determines that, monetary value

will not be a reliable indication in judging over all outcomes and make decision. Here,

economists have to assume that significant individual makes decision to enhance their utilities.

Standard Gamble:

In consideration with this approach the standard gamble techniques had been used in

analyzing the values of utilities. It assists that when the variables are indifferent the utility values

are equal.

B. Investing primarily in share market

1.

Decision Matrix

Investment

10000 Shares

Government

Bonds

Monetary

Gain/loss

Action States

%

Return

Yearly

return in

Amount % Return

Yearly

return in

Amount Amount

Full Investment in shares 14.00% 1400 9.00% 900 Gain of 500

Full Investment in shares 8.00% 800 9.00% 900 Loss of 100

Full Investment in shares 0.00% 0 9.00% 900 Loss of 900

Half Investment is shares 14.00% 700 9.00% 450 Gain of 250

Half Investment is shares 8.00% 400 9.00% 450 Loss of 50

Half Investment is shares 0.00% 0 9.00% 450 Loss of 450

All the comparisons done with the returns on the Government Bonds as it is minimum

returns that can be achieved.

A. Assessing the utility function as well as standard gamble which helps in determining utility

value

In utility assessment, it consists of identifying bad and best utility to be used in process.

Thus, where 0 represents a bad, while 1 for good quality of a utility. This assessment helps in

ranking the commodities which will be helpful in identifying no. of better and worst articles are

stated in a study. In context with implicating this theory which determines that, monetary value

will not be a reliable indication in judging over all outcomes and make decision. Here,

economists have to assume that significant individual makes decision to enhance their utilities.

Standard Gamble:

In consideration with this approach the standard gamble techniques had been used in

analyzing the values of utilities. It assists that when the variables are indifferent the utility values

are equal.

B. Investing primarily in share market

1.

Decision Matrix

Investment

10000 Shares

Government

Bonds

Monetary

Gain/loss

Action States

%

Return

Yearly

return in

Amount % Return

Yearly

return in

Amount Amount

Full Investment in shares 14.00% 1400 9.00% 900 Gain of 500

Full Investment in shares 8.00% 800 9.00% 900 Loss of 100

Full Investment in shares 0.00% 0 9.00% 900 Loss of 900

Half Investment is shares 14.00% 700 9.00% 450 Gain of 250

Half Investment is shares 8.00% 400 9.00% 450 Loss of 50

Half Investment is shares 0.00% 0 9.00% 450 Loss of 450

All the comparisons done with the returns on the Government Bonds as it is minimum

returns that can be achieved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

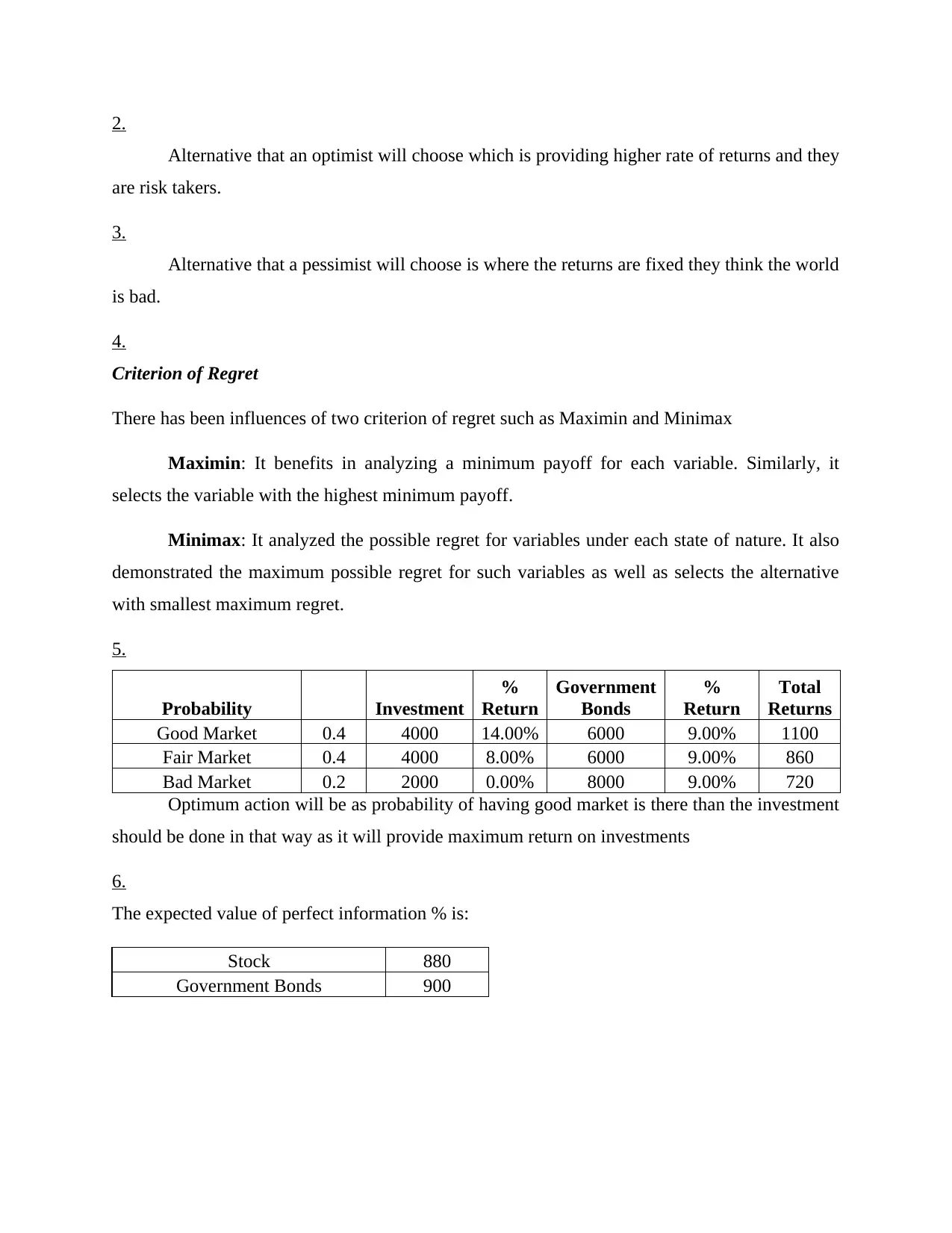

2.

Alternative that an optimist will choose which is providing higher rate of returns and they

are risk takers.

3.

Alternative that a pessimist will choose is where the returns are fixed they think the world

is bad.

4.

Criterion of Regret

There has been influences of two criterion of regret such as Maximin and Minimax

Maximin: It benefits in analyzing a minimum payoff for each variable. Similarly, it

selects the variable with the highest minimum payoff.

Minimax: It analyzed the possible regret for variables under each state of nature. It also

demonstrated the maximum possible regret for such variables as well as selects the alternative

with smallest maximum regret.

5.

Probability Investment

%

Return

Government

Bonds

%

Return

Total

Returns

Good Market 0.4 4000 14.00% 6000 9.00% 1100

Fair Market 0.4 4000 8.00% 6000 9.00% 860

Bad Market 0.2 2000 0.00% 8000 9.00% 720

Optimum action will be as probability of having good market is there than the investment

should be done in that way as it will provide maximum return on investments

6.

The expected value of perfect information % is:

Stock 880

Government Bonds 900

Alternative that an optimist will choose which is providing higher rate of returns and they

are risk takers.

3.

Alternative that a pessimist will choose is where the returns are fixed they think the world

is bad.

4.

Criterion of Regret

There has been influences of two criterion of regret such as Maximin and Minimax

Maximin: It benefits in analyzing a minimum payoff for each variable. Similarly, it

selects the variable with the highest minimum payoff.

Minimax: It analyzed the possible regret for variables under each state of nature. It also

demonstrated the maximum possible regret for such variables as well as selects the alternative

with smallest maximum regret.

5.

Probability Investment

%

Return

Government

Bonds

%

Return

Total

Returns

Good Market 0.4 4000 14.00% 6000 9.00% 1100

Fair Market 0.4 4000 8.00% 6000 9.00% 860

Bad Market 0.2 2000 0.00% 8000 9.00% 720

Optimum action will be as probability of having good market is there than the investment

should be done in that way as it will provide maximum return on investments

6.

The expected value of perfect information % is:

Stock 880

Government Bonds 900

As the maximum of expectation is in Government Bonds. As not knowing the directions

where will be the market go we expect the most of returns from government bonds thus EMV

=900

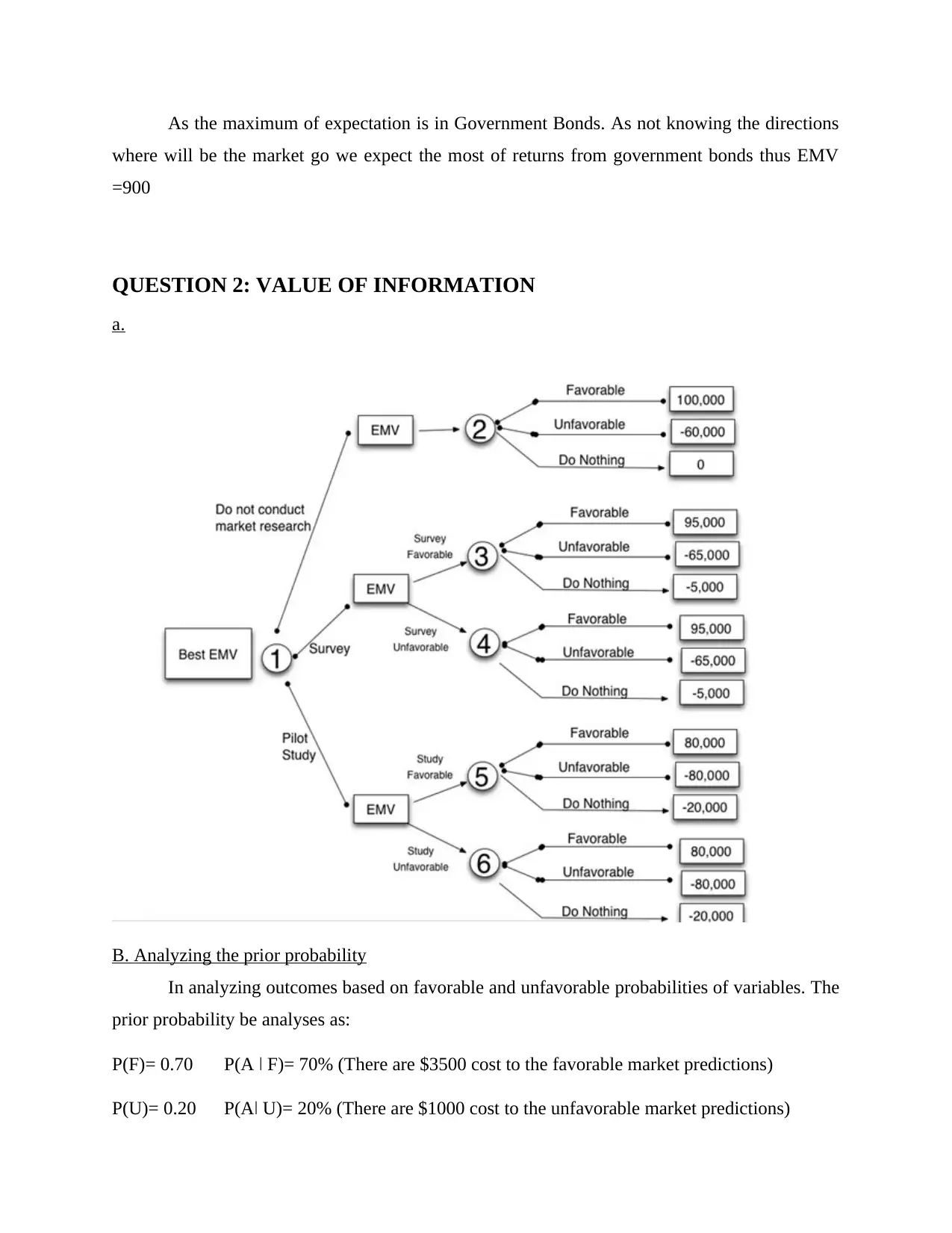

QUESTION 2: VALUE OF INFORMATION

a.

B. Analyzing the prior probability

In analyzing outcomes based on favorable and unfavorable probabilities of variables. The

prior probability be analyses as:

P(F)= 0.70 P(A ǀ F)= 70% (There are $3500 cost to the favorable market predictions)

P(U)= 0.20 P(Aǀ U)= 20% (There are $1000 cost to the unfavorable market predictions)

where will be the market go we expect the most of returns from government bonds thus EMV

=900

QUESTION 2: VALUE OF INFORMATION

a.

B. Analyzing the prior probability

In analyzing outcomes based on favorable and unfavorable probabilities of variables. The

prior probability be analyses as:

P(F)= 0.70 P(A ǀ F)= 70% (There are $3500 cost to the favorable market predictions)

P(U)= 0.20 P(Aǀ U)= 20% (There are $1000 cost to the unfavorable market predictions)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

C. Posterior probability

P(A) = P(A ǀ F) P(F) + P(A ǀ U) P(U)

P(F ǀ A) = P(F ∩ A)/P(A) = P(A ǀ F) P(F)/P(A ǀ F) P(M) + P(A ǀ U) P(U)

= 3500*0.7 / (3500*0.7) + (1000*0.2)

= 0.924

P(U ǀ A) = P(U ∩ A)/ P(A) = P(A ǀ U) P(U)/ P(A ǀ F) P(F) + P(A ǀ U) P(U)

1000* 0.20/ (3500*0.7)+ (1000*0.2)

= 0.075

D. Expected net gain and loss after conducting the market research

Probability of having favorable outcomes = 3500

Probability of having unfavorable outcomes are = 1000

Therefore,

=3500-1000

= 2500

There will be gain of 2500 which insist that the market research will be helpful in bringing the

suitable gains.

QUESTION 3 MONTE CARLO SIMULATION

a.

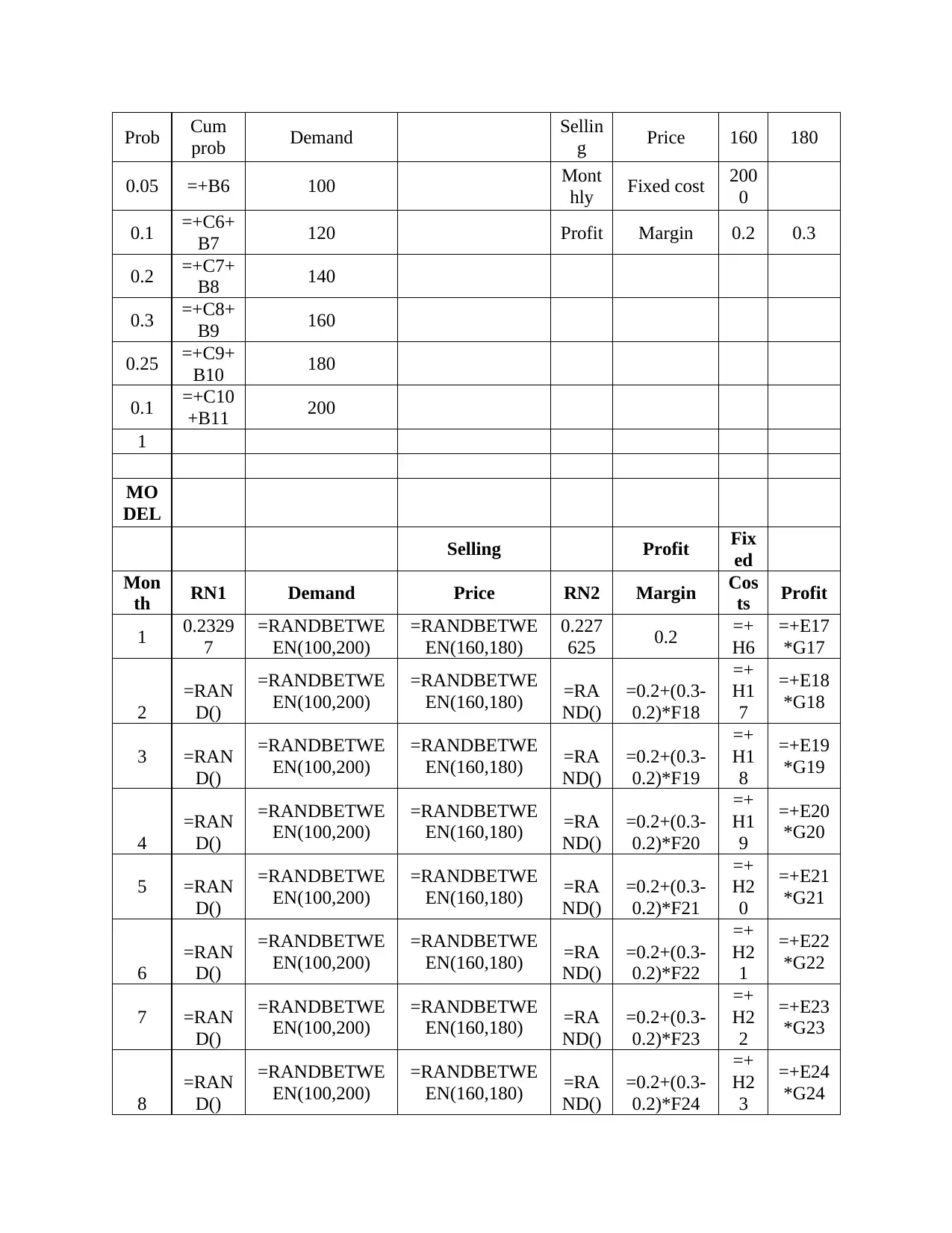

Average monthly profit to Ajax Tyres over the period of 12 months are as follows:

Ajax Tyres

DATA

Prob Cum

prob Demand Selling Price $160 $180

0.05 0.05 100 Monthly Fixed

cost $2,000

P(A) = P(A ǀ F) P(F) + P(A ǀ U) P(U)

P(F ǀ A) = P(F ∩ A)/P(A) = P(A ǀ F) P(F)/P(A ǀ F) P(M) + P(A ǀ U) P(U)

= 3500*0.7 / (3500*0.7) + (1000*0.2)

= 0.924

P(U ǀ A) = P(U ∩ A)/ P(A) = P(A ǀ U) P(U)/ P(A ǀ F) P(F) + P(A ǀ U) P(U)

1000* 0.20/ (3500*0.7)+ (1000*0.2)

= 0.075

D. Expected net gain and loss after conducting the market research

Probability of having favorable outcomes = 3500

Probability of having unfavorable outcomes are = 1000

Therefore,

=3500-1000

= 2500

There will be gain of 2500 which insist that the market research will be helpful in bringing the

suitable gains.

QUESTION 3 MONTE CARLO SIMULATION

a.

Average monthly profit to Ajax Tyres over the period of 12 months are as follows:

Ajax Tyres

DATA

Prob Cum

prob Demand Selling Price $160 $180

0.05 0.05 100 Monthly Fixed

cost $2,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.1 0.15 120 Profit Margin 20% 30%

0.2 0.35 140

0.3 0.65 160

0.25 0.9 180

0.1 1 200

1

MODE

L

Sellin

g Profit Fixed

Month RN1 Deman

d Price RN2 Margi

n Costs Profit

1 0.2329

7 199 $173 0.2276

3 0.2 $2,00

0 34.6

2 0.822 164 $173 0.1330

7 0.21

$2,00

0

36.902

1

3 0.966 159 $172 0.8388

4 0.28

$2,00

0 48.828

4 0.028 157 $173 0.1857

7 0.22

$2,00

0

37.813

8

5 0.511 104 $164 0.8110

4 0.28

$2,00

0

46.101

1

6 0.810 131 $168 0.8309

2 0.28

$2,00

0

47.559

5

7 0.066 179 $170 0.6692

4 0.27

$2,00

0

45.377

1

8 0.655 175 $177 0.7726

4 0.28

$2,00

0

49.075

8

9 0.943 182 $165 0.0978

2 0.21

$2,00

0 34.614

10 0.635 132 $164 0.2095

4 0.22

$2,00

0

36.236

4

11 0.736 171 $171 0.7680

3 0.28

$2,00

0

47.333

3

12 0.657 196 $161 0.5075

1 0.25

$2,00

0 40.371

Ajax Tyres

DAT

A

0.2 0.35 140

0.3 0.65 160

0.25 0.9 180

0.1 1 200

1

MODE

L

Sellin

g Profit Fixed

Month RN1 Deman

d Price RN2 Margi

n Costs Profit

1 0.2329

7 199 $173 0.2276

3 0.2 $2,00

0 34.6

2 0.822 164 $173 0.1330

7 0.21

$2,00

0

36.902

1

3 0.966 159 $172 0.8388

4 0.28

$2,00

0 48.828

4 0.028 157 $173 0.1857

7 0.22

$2,00

0

37.813

8

5 0.511 104 $164 0.8110

4 0.28

$2,00

0

46.101

1

6 0.810 131 $168 0.8309

2 0.28

$2,00

0

47.559

5

7 0.066 179 $170 0.6692

4 0.27

$2,00

0

45.377

1

8 0.655 175 $177 0.7726

4 0.28

$2,00

0

49.075

8

9 0.943 182 $165 0.0978

2 0.21

$2,00

0 34.614

10 0.635 132 $164 0.2095

4 0.22

$2,00

0

36.236

4

11 0.736 171 $171 0.7680

3 0.28

$2,00

0

47.333

3

12 0.657 196 $161 0.5075

1 0.25

$2,00

0 40.371

Ajax Tyres

DAT

A

Prob Cum

prob Demand Sellin

g Price 160 180

0.05 =+B6 100 Mont

hly Fixed cost 200

0

0.1 =+C6+

B7 120 Profit Margin 0.2 0.3

0.2 =+C7+

B8 140

0.3 =+C8+

B9 160

0.25 =+C9+

B10 180

0.1 =+C10

+B11 200

1

MO

DEL

Selling Profit Fix

ed

Mon

th RN1 Demand Price RN2 Margin Cos

ts Profit

1 0.2329

7

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180)

0.227

625 0.2 =+

H6

=+E17

*G17

2

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F18

=+

H1

7

=+E18

*G18

3 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F19

=+

H1

8

=+E19

*G19

4

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F20

=+

H1

9

=+E20

*G20

5 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F21

=+

H2

0

=+E21

*G21

6

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F22

=+

H2

1

=+E22

*G22

7 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F23

=+

H2

2

=+E23

*G23

8

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F24

=+

H2

3

=+E24

*G24

prob Demand Sellin

g Price 160 180

0.05 =+B6 100 Mont

hly Fixed cost 200

0

0.1 =+C6+

B7 120 Profit Margin 0.2 0.3

0.2 =+C7+

B8 140

0.3 =+C8+

B9 160

0.25 =+C9+

B10 180

0.1 =+C10

+B11 200

1

MO

DEL

Selling Profit Fix

ed

Mon

th RN1 Demand Price RN2 Margin Cos

ts Profit

1 0.2329

7

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180)

0.227

625 0.2 =+

H6

=+E17

*G17

2

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F18

=+

H1

7

=+E18

*G18

3 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F19

=+

H1

8

=+E19

*G19

4

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F20

=+

H1

9

=+E20

*G20

5 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F21

=+

H2

0

=+E21

*G21

6

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F22

=+

H2

1

=+E22

*G22

7 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F23

=+

H2

2

=+E23

*G23

8

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F24

=+

H2

3

=+E24

*G24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F25

=+

H2

4

=+E25

*G25

10

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F26

=+

H2

5

=+E26

*G26

11 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F27

=+

H2

6

=+E27

*G27

12

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F28

=+

H2

7

=+E28

*G28

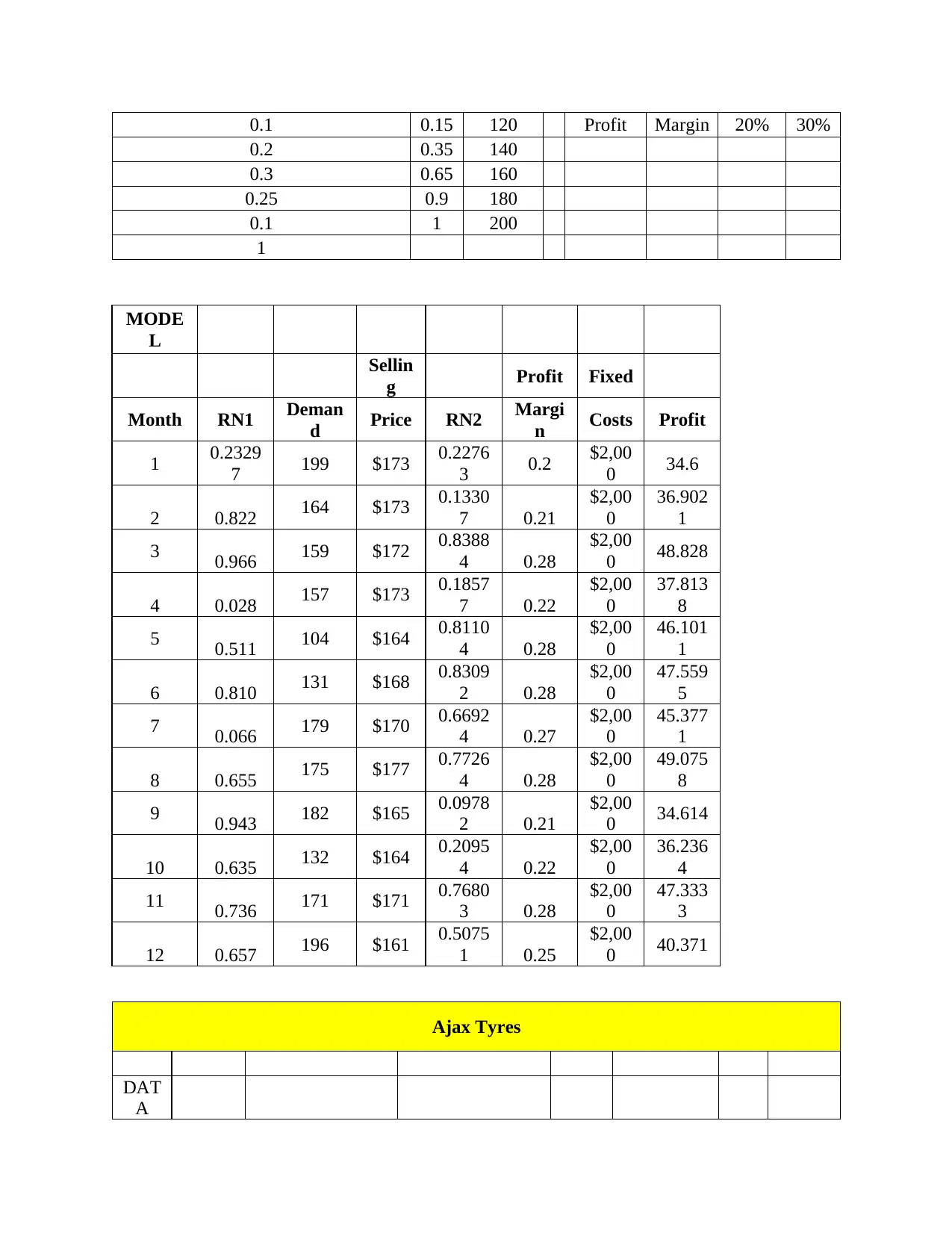

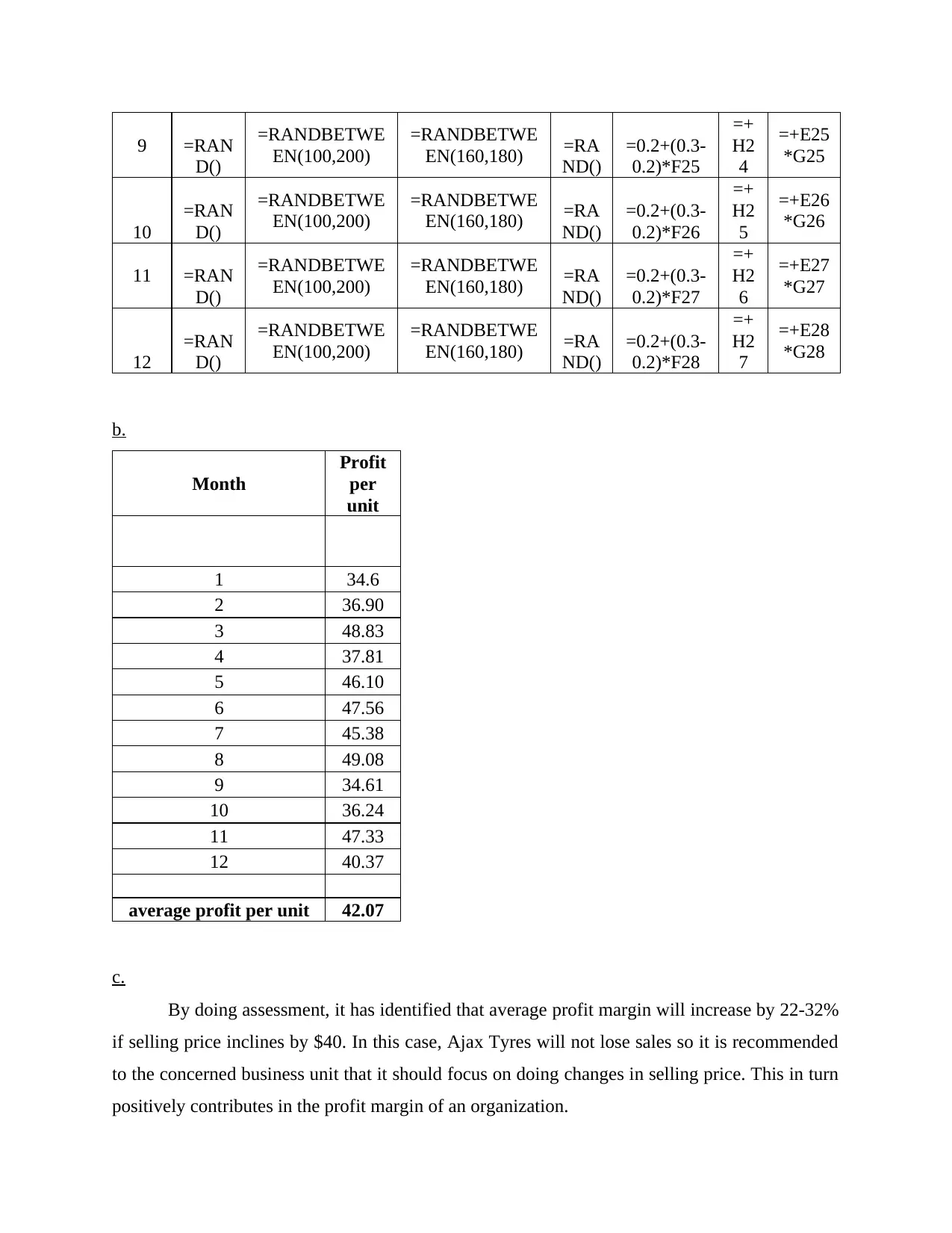

b.

Month

Profit

per

unit

1 34.6

2 36.90

3 48.83

4 37.81

5 46.10

6 47.56

7 45.38

8 49.08

9 34.61

10 36.24

11 47.33

12 40.37

average profit per unit 42.07

c.

By doing assessment, it has identified that average profit margin will increase by 22-32%

if selling price inclines by $40. In this case, Ajax Tyres will not lose sales so it is recommended

to the concerned business unit that it should focus on doing changes in selling price. This in turn

positively contributes in the profit margin of an organization.

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F25

=+

H2

4

=+E25

*G25

10

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F26

=+

H2

5

=+E26

*G26

11 =RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F27

=+

H2

6

=+E27

*G27

12

=RAN

D()

=RANDBETWE

EN(100,200)

=RANDBETWE

EN(160,180) =RA

ND()

=0.2+(0.3-

0.2)*F28

=+

H2

7

=+E28

*G28

b.

Month

Profit

per

unit

1 34.6

2 36.90

3 48.83

4 37.81

5 46.10

6 47.56

7 45.38

8 49.08

9 34.61

10 36.24

11 47.33

12 40.37

average profit per unit 42.07

c.

By doing assessment, it has identified that average profit margin will increase by 22-32%

if selling price inclines by $40. In this case, Ajax Tyres will not lose sales so it is recommended

to the concerned business unit that it should focus on doing changes in selling price. This in turn

positively contributes in the profit margin of an organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

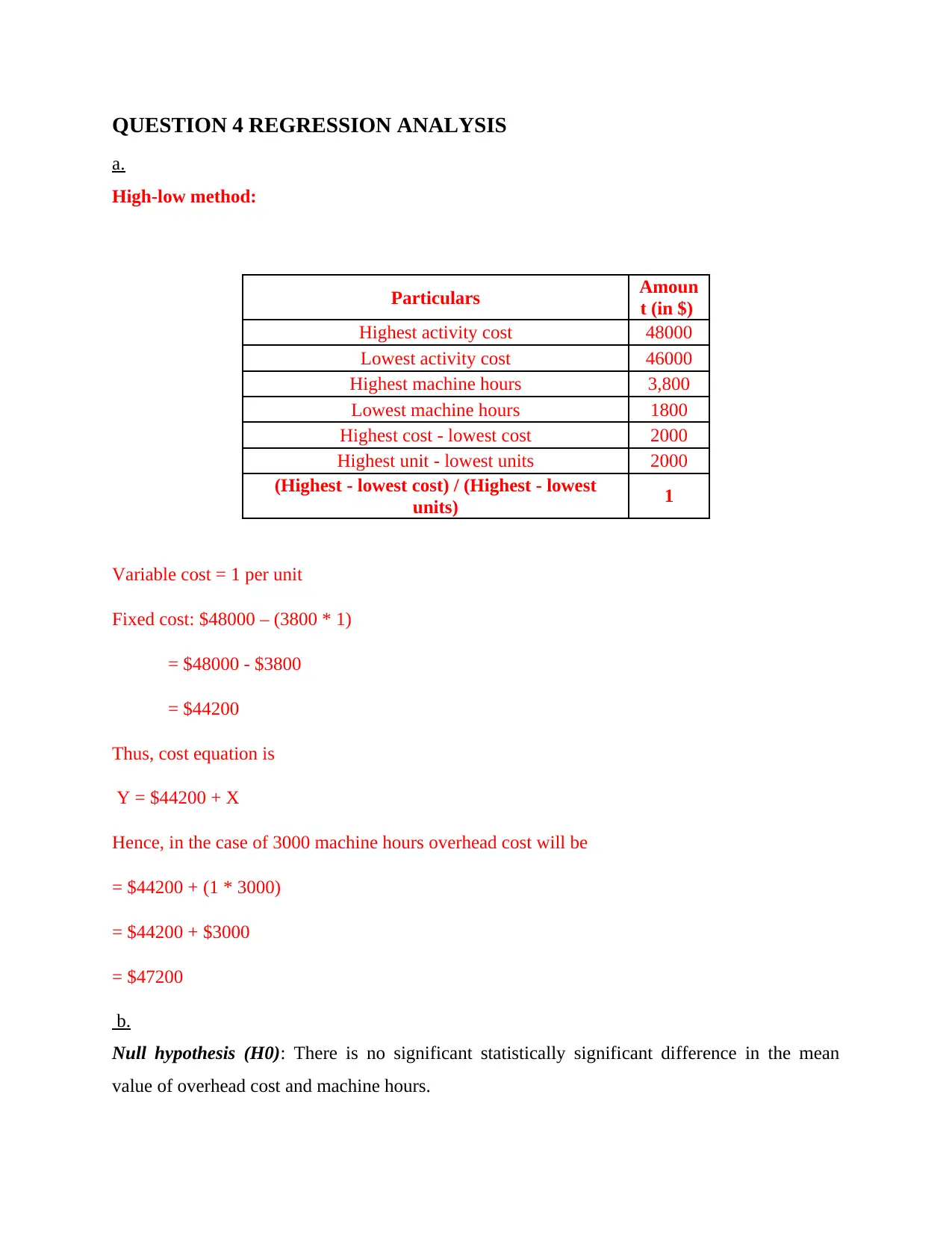

QUESTION 4 REGRESSION ANALYSIS

a.

High-low method:

Particulars Amoun

t (in $)

Highest activity cost 48000

Lowest activity cost 46000

Highest machine hours 3,800

Lowest machine hours 1800

Highest cost - lowest cost 2000

Highest unit - lowest units 2000

(Highest - lowest cost) / (Highest - lowest

units) 1

Variable cost = 1 per unit

Fixed cost: $48000 – (3800 * 1)

= $48000 - $3800

= $44200

Thus, cost equation is

Y = $44200 + X

Hence, in the case of 3000 machine hours overhead cost will be

= $44200 + (1 * 3000)

= $44200 + $3000

= $47200

b.

Null hypothesis (H0): There is no significant statistically significant difference in the mean

value of overhead cost and machine hours.

a.

High-low method:

Particulars Amoun

t (in $)

Highest activity cost 48000

Lowest activity cost 46000

Highest machine hours 3,800

Lowest machine hours 1800

Highest cost - lowest cost 2000

Highest unit - lowest units 2000

(Highest - lowest cost) / (Highest - lowest

units) 1

Variable cost = 1 per unit

Fixed cost: $48000 – (3800 * 1)

= $48000 - $3800

= $44200

Thus, cost equation is

Y = $44200 + X

Hence, in the case of 3000 machine hours overhead cost will be

= $44200 + (1 * 3000)

= $44200 + $3000

= $47200

b.

Null hypothesis (H0): There is no significant statistically significant difference in the mean

value of overhead cost and machine hours.

Alternative hypothesis (H1): There is a statistically significant difference in the mean value of

overhead cost and machine hours.

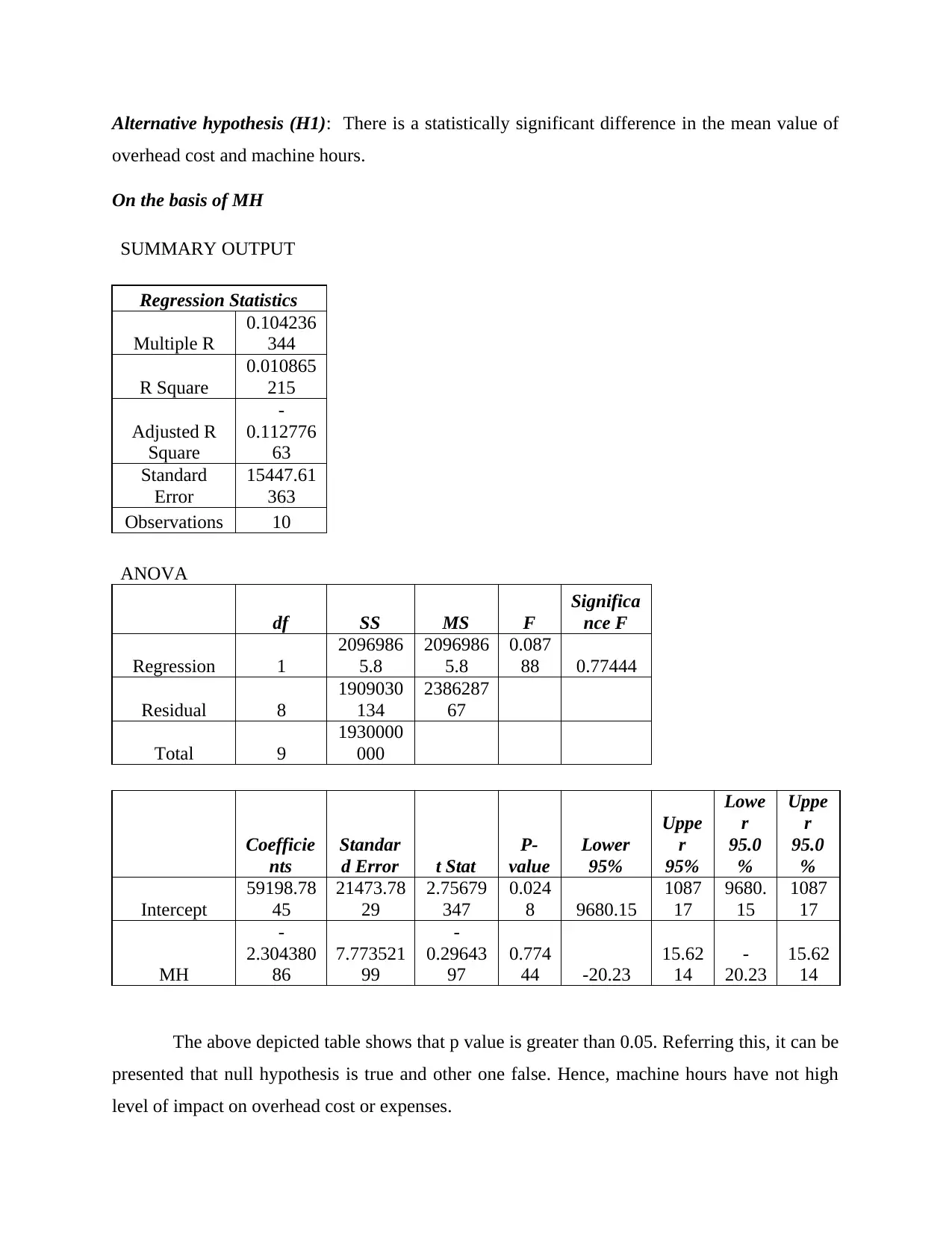

On the basis of MH

SUMMARY OUTPUT

Regression Statistics

Multiple R

0.104236

344

R Square

0.010865

215

Adjusted R

Square

-

0.112776

63

Standard

Error

15447.61

363

Observations 10

ANOVA

df SS MS F

Significa

nce F

Regression 1

2096986

5.8

2096986

5.8

0.087

88 0.77444

Residual 8

1909030

134

2386287

67

Total 9

1930000

000

Coefficie

nts

Standar

d Error t Stat

P-

value

Lower

95%

Uppe

r

95%

Lowe

r

95.0

%

Uppe

r

95.0

%

Intercept

59198.78

45

21473.78

29

2.75679

347

0.024

8 9680.15

1087

17

9680.

15

1087

17

MH

-

2.304380

86

7.773521

99

-

0.29643

97

0.774

44 -20.23

15.62

14

-

20.23

15.62

14

The above depicted table shows that p value is greater than 0.05. Referring this, it can be

presented that null hypothesis is true and other one false. Hence, machine hours have not high

level of impact on overhead cost or expenses.

overhead cost and machine hours.

On the basis of MH

SUMMARY OUTPUT

Regression Statistics

Multiple R

0.104236

344

R Square

0.010865

215

Adjusted R

Square

-

0.112776

63

Standard

Error

15447.61

363

Observations 10

ANOVA

df SS MS F

Significa

nce F

Regression 1

2096986

5.8

2096986

5.8

0.087

88 0.77444

Residual 8

1909030

134

2386287

67

Total 9

1930000

000

Coefficie

nts

Standar

d Error t Stat

P-

value

Lower

95%

Uppe

r

95%

Lowe

r

95.0

%

Uppe

r

95.0

%

Intercept

59198.78

45

21473.78

29

2.75679

347

0.024

8 9680.15

1087

17

9680.

15

1087

17

MH

-

2.304380

86

7.773521

99

-

0.29643

97

0.774

44 -20.23

15.62

14

-

20.23

15.62

14

The above depicted table shows that p value is greater than 0.05. Referring this, it can be

presented that null hypothesis is true and other one false. Hence, machine hours have not high

level of impact on overhead cost or expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.