Introduction to Finance: EOQ, Investment Appraisal and Ratios

VerifiedAdded on 2023/01/06

|16

|4047

|43

Homework Assignment

AI Summary

This finance assignment solution comprehensively addresses key concepts in finance. It begins with an introduction to finance, followed by detailed answers to four questions. The first question focuses on the Economic Order Quantity (EOQ) model, including its calculation, application, and managerial implications for optimizing inventory costs. The second question delves into investment appraisal techniques, including payback period and Accounting Rate of Return (ARR), comparing two investment options and evaluating the merits and demerits of the Internal Rate of Return (IRR) method. The third question involves the calculation and interpretation of various financial ratios, such as gross profit margin, current ratio, and debt-to-equity ratio, providing insights into a company's financial health. Finally, the assignment underscores the importance of audience considerations in financial statement analysis. The solution provides a well-structured and in-depth analysis of the financial topics covered.

Introduction to Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2........................................................................................................................................5

Question 3..................................................................................................................................10

Question 4..................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2........................................................................................................................................5

Question 3..................................................................................................................................10

Question 4..................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Finance is general term encompassing fiscal, debt or financing, economic, commodity

markets, assets, and investment operations. Finance effectively represents the management of

funding and the mechanism for the necessary funds to be raised (Bernards and Campbell-

Verduyn, 2019). The role of funding is to ensure that ample finances are available to continue

operating and that the enterprise is equipped to maintain and preserve capital funds. This

evaluation is focused on four main forms of considerations pertaining to sources of financing, the

evaluation of the estimates for measurement of the corporation 's financial results and the

application of techniques of investment appraisal/analysis to evaluate the viability of the

different solutions. Moreover, position and function of a variety of different regulatory structure

bodies is defined as well as roles of the auditing board is discussed.

MAIN BODY

Question 1

(a) Measurement of EOQ-

Economic ordering quantity: √2*annual usage*Ordering cost/Carrying or holding cost

Annual usage: 27000 KG

Carrying or holding cost: $1.75 @ per KG of year

Ordering cost: $0.9

Hence,

EOQ: √2*27000*0.9/1.75

= √48600/1.75

= √27771.43

= 166.65 Or 167

(b) Calculation of annual cost-

Finance is general term encompassing fiscal, debt or financing, economic, commodity

markets, assets, and investment operations. Finance effectively represents the management of

funding and the mechanism for the necessary funds to be raised (Bernards and Campbell-

Verduyn, 2019). The role of funding is to ensure that ample finances are available to continue

operating and that the enterprise is equipped to maintain and preserve capital funds. This

evaluation is focused on four main forms of considerations pertaining to sources of financing, the

evaluation of the estimates for measurement of the corporation 's financial results and the

application of techniques of investment appraisal/analysis to evaluate the viability of the

different solutions. Moreover, position and function of a variety of different regulatory structure

bodies is defined as well as roles of the auditing board is discussed.

MAIN BODY

Question 1

(a) Measurement of EOQ-

Economic ordering quantity: √2*annual usage*Ordering cost/Carrying or holding cost

Annual usage: 27000 KG

Carrying or holding cost: $1.75 @ per KG of year

Ordering cost: $0.9

Hence,

EOQ: √2*27000*0.9/1.75

= √48600/1.75

= √27771.43

= 166.65 Or 167

(b) Calculation of annual cost-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Buying cost: 27000Kg @ 0.90

= $24300

Ordering cost: Annual demand*per unit ordering cost/EOQ = (27000*0.90/167)

= $145.50

Holding cost: Holding Cost per unit*EOQ/2 = (1.75*657/2)

= $146.12

Hence,

Annual cost: $24300+$145.5+$146.12

= $ 24591.5

(c) Evaluation of decision to use EOQ model.

Managers commonly applies the EOQ method in regard to the company Touchdown

Sports to determine the optimum order volume that substantially decreases net cost or

satisfies customer demand. EOQ can be around 657, reducing costs or causing the

profitability to be improved by Touchdown Sports. Decision of the corporation to use

this technique is based on that this will enable them to to optimize stock or inventory

expenses and decide how much inventory retention as well as re-ordering level should be

considered by the corporation. In attempt to take greater advantages of decreased bulk

prices and lowered ordering rates, this method can also consider purchasing a bigger

volume with less orders. Additionally, if they are large as well as order volumes are

usually smaller, they can prefer to more further orders for several products to reduce

operational costs (Booth, Cleary and Rakita, 2020).

(d) Suggestion to Touchdown plc.

The adoption of inventory controls has been suggested to company Touchdown

Sports' senior management team in order to reduce/optimize total expense related

to inventory handling and storage as well as and, with the assistance of EOQ

= $24300

Ordering cost: Annual demand*per unit ordering cost/EOQ = (27000*0.90/167)

= $145.50

Holding cost: Holding Cost per unit*EOQ/2 = (1.75*657/2)

= $146.12

Hence,

Annual cost: $24300+$145.5+$146.12

= $ 24591.5

(c) Evaluation of decision to use EOQ model.

Managers commonly applies the EOQ method in regard to the company Touchdown

Sports to determine the optimum order volume that substantially decreases net cost or

satisfies customer demand. EOQ can be around 657, reducing costs or causing the

profitability to be improved by Touchdown Sports. Decision of the corporation to use

this technique is based on that this will enable them to to optimize stock or inventory

expenses and decide how much inventory retention as well as re-ordering level should be

considered by the corporation. In attempt to take greater advantages of decreased bulk

prices and lowered ordering rates, this method can also consider purchasing a bigger

volume with less orders. Additionally, if they are large as well as order volumes are

usually smaller, they can prefer to more further orders for several products to reduce

operational costs (Booth, Cleary and Rakita, 2020).

(d) Suggestion to Touchdown plc.

The adoption of inventory controls has been suggested to company Touchdown

Sports' senior management team in order to reduce/optimize total expense related

to inventory handling and storage as well as and, with the assistance of EOQ

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

technique model, managers are enabled to lessen it by optimizing orders or maintaining

costs that minimise the costs of goods which either satisfy customer demand or satisfy the

firm's goal of increasing their profits. Keeping control over expenditures related to the

management of inventories which are not usable. Both costs, together with cost of

acquisition as well as cost of shortages, are also component of overall cost of the item.

The costs of running a corporation covers the cost of lost or defective items, and also

storage facilities, employees and insurances. It is also recognized that when market

demand is weak, Just-In-Time solution is more suitable, however EOQ is much more

acceptable in the context of company Touchdown Sports is the leading producer of sports

safety apparels having excessive demand. wIn addition to lessen the overall costs and

then identify the maximum level of quantity necessary to order in event of limited storage

and holding position, it is very important for organization to effectively implement EOQ

model.

Question 2

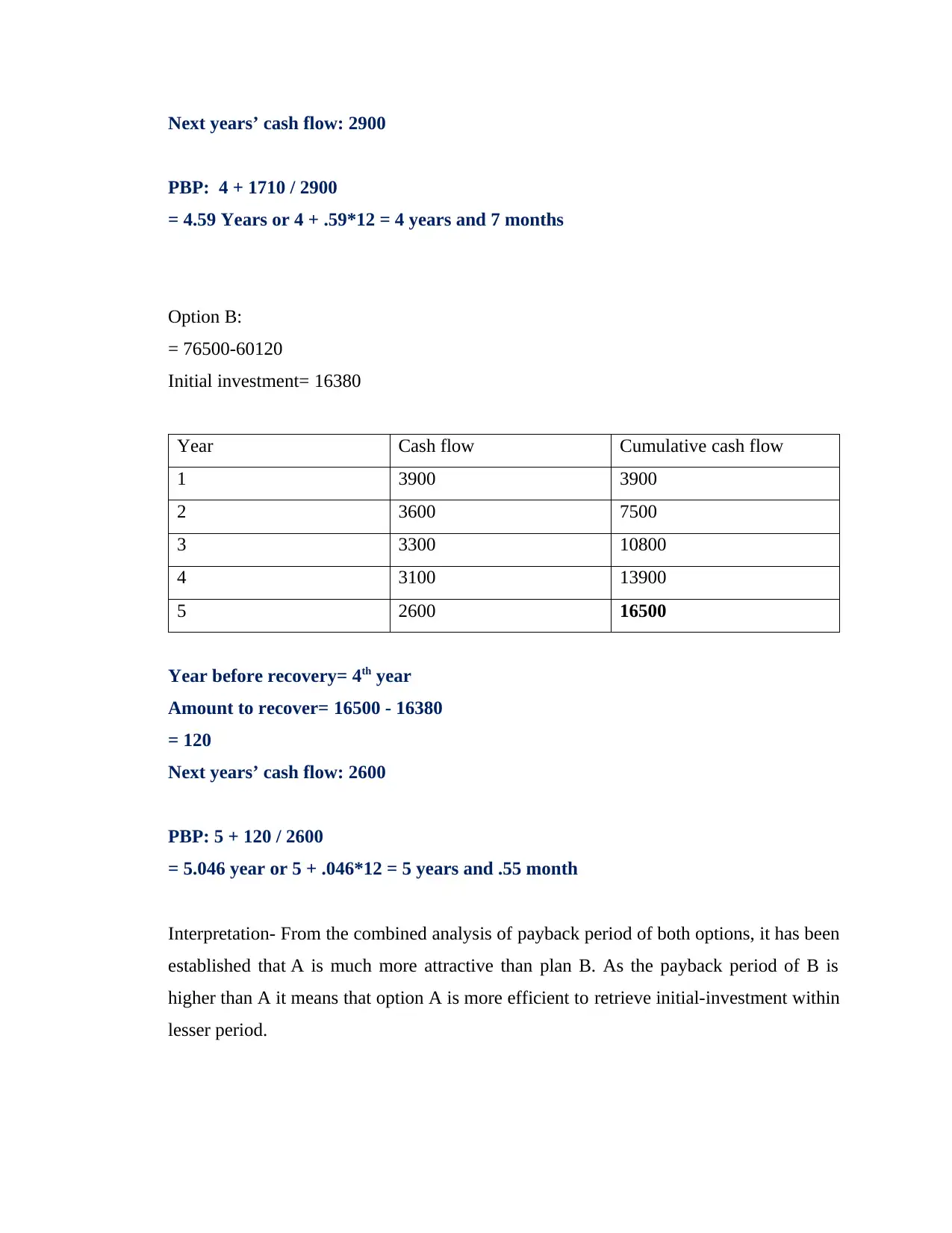

(a) Payback period:

Formula: Year before recovery + amount to be recover/next years’ cash flow

Investment: Cost-Scrap value

Option A:

= 51000-40110

Initial investment= 10890

Year Cash flow Cumulative cash flow

1 3200 3200

2 3300 6500

3 3100 9600

4 3000 12600

5 2900 15500

Year before recovery= 3rd year

Amount to recover= 12600 – 10890 = 1710

costs that minimise the costs of goods which either satisfy customer demand or satisfy the

firm's goal of increasing their profits. Keeping control over expenditures related to the

management of inventories which are not usable. Both costs, together with cost of

acquisition as well as cost of shortages, are also component of overall cost of the item.

The costs of running a corporation covers the cost of lost or defective items, and also

storage facilities, employees and insurances. It is also recognized that when market

demand is weak, Just-In-Time solution is more suitable, however EOQ is much more

acceptable in the context of company Touchdown Sports is the leading producer of sports

safety apparels having excessive demand. wIn addition to lessen the overall costs and

then identify the maximum level of quantity necessary to order in event of limited storage

and holding position, it is very important for organization to effectively implement EOQ

model.

Question 2

(a) Payback period:

Formula: Year before recovery + amount to be recover/next years’ cash flow

Investment: Cost-Scrap value

Option A:

= 51000-40110

Initial investment= 10890

Year Cash flow Cumulative cash flow

1 3200 3200

2 3300 6500

3 3100 9600

4 3000 12600

5 2900 15500

Year before recovery= 3rd year

Amount to recover= 12600 – 10890 = 1710

Next years’ cash flow: 2900

PBP: 4 + 1710 / 2900

= 4.59 Years or 4 + .59*12 = 4 years and 7 months

Option B:

= 76500-60120

Initial investment= 16380

Year Cash flow Cumulative cash flow

1 3900 3900

2 3600 7500

3 3300 10800

4 3100 13900

5 2600 16500

Year before recovery= 4th year

Amount to recover= 16500 - 16380

= 120

Next years’ cash flow: 2600

PBP: 5 + 120 / 2600

= 5.046 year or 5 + .046*12 = 5 years and .55 month

Interpretation- From the combined analysis of payback period of both options, it has been

established that A is much more attractive than plan B. As the payback period of B is

higher than A it means that option A is more efficient to retrieve initial-investment within

lesser period.

PBP: 4 + 1710 / 2900

= 4.59 Years or 4 + .59*12 = 4 years and 7 months

Option B:

= 76500-60120

Initial investment= 16380

Year Cash flow Cumulative cash flow

1 3900 3900

2 3600 7500

3 3300 10800

4 3100 13900

5 2600 16500

Year before recovery= 4th year

Amount to recover= 16500 - 16380

= 120

Next years’ cash flow: 2600

PBP: 5 + 120 / 2600

= 5.046 year or 5 + .046*12 = 5 years and .55 month

Interpretation- From the combined analysis of payback period of both options, it has been

established that A is much more attractive than plan B. As the payback period of B is

higher than A it means that option A is more efficient to retrieve initial-investment within

lesser period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) ARR:

Option A-

Year Cash flow Depreciation (Actual

cost-Scrap value/life

of assets)

Net cash flow

1 3200 2178 1022

2 3300 2178 1122

3 3100 2178 922

4 3000 2178 822

5 2900 2178 722

Total net cash flow 4610

Formula: (Average annual profit / Initial investment) * 100

Average annual profit: 4610/5

= 922

= 922/10890*100

= 8.47%

Option B:

Year Cash flow Depreciation (Actual

cost-Scrap value/life

of assets)

Net cash flow

1 3900 3276 624

2 3600 3276 324

3 3300 3276 24

4 3100 3276 -176

5 2600 3276 -676

Total net cash flow 120

Average annual profit: 120/5

= 24

Option A-

Year Cash flow Depreciation (Actual

cost-Scrap value/life

of assets)

Net cash flow

1 3200 2178 1022

2 3300 2178 1122

3 3100 2178 922

4 3000 2178 822

5 2900 2178 722

Total net cash flow 4610

Formula: (Average annual profit / Initial investment) * 100

Average annual profit: 4610/5

= 922

= 922/10890*100

= 8.47%

Option B:

Year Cash flow Depreciation (Actual

cost-Scrap value/life

of assets)

Net cash flow

1 3900 3276 624

2 3600 3276 324

3 3300 3276 24

4 3100 3276 -176

5 2600 3276 -676

Total net cash flow 120

Average annual profit: 120/5

= 24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ARR: 24/16380*100

= 0.15%

Interpretation- From the above calculation, it was assessed that ARR percentage of plan-

A for Touchdown Trips Inc is 8.47 percent while 0.15 % in case of Option B.

Comparatively, A offers more profitability yield as compare to B thus option A would be

more viable for company.

(c) Evaluation of accounting rate of return method.

ARR technique provide indicator in form of percentage that demonstrates the average return

rate/yield of investments or projects occurred due to cash flows relative to their initial

investment. ARR measured as dividing the projected revenue/cash-flows of the

project/investment by initial expenditure in order to quantity of yield that can be anticipated over

all the lifetime of a project. The time value of capital or future cash flows are not

generally considered in ARR, and may be an important aspect of management decisions for

a firm. With the assistance of this appraisal approach , organisations are allowed to evaluate the

viability of each project. To assess the best alternative for spending, this method is used

by managers of company Touchdown Trips Inc.

Two possible investment approaches are being outlined, namely the Gulfstream G650ER

(option- A) and Boeing BBJ Max 7 (option- B). With assistance of ARR evaluation,

management is enabled to make appropriate selections, and Option A is healthier investment

option which produces 28.46 percent yield on investment. This approach has many rewards, such

as measuring and recognizing the turnaround duration is very efficient and easy. It would take

into consideration the net profit or sum earned over the whole life-cycle of an investment. This

model considers net earnings aspect which is amount of net earnings post taxes and depreciation.

This is a key consideration in appraisal of any investment. This approach allows the future

proposal to be compared to competitive essence of cost-reduction plan or other proposals. This

method offers a clear explanation of a project 's feasibility. This approach alone acknowledges

the accounting concept of gains for the estimation of yield or rate of return (DAVALLOU and

MAHMOODI, 2017).

= 0.15%

Interpretation- From the above calculation, it was assessed that ARR percentage of plan-

A for Touchdown Trips Inc is 8.47 percent while 0.15 % in case of Option B.

Comparatively, A offers more profitability yield as compare to B thus option A would be

more viable for company.

(c) Evaluation of accounting rate of return method.

ARR technique provide indicator in form of percentage that demonstrates the average return

rate/yield of investments or projects occurred due to cash flows relative to their initial

investment. ARR measured as dividing the projected revenue/cash-flows of the

project/investment by initial expenditure in order to quantity of yield that can be anticipated over

all the lifetime of a project. The time value of capital or future cash flows are not

generally considered in ARR, and may be an important aspect of management decisions for

a firm. With the assistance of this appraisal approach , organisations are allowed to evaluate the

viability of each project. To assess the best alternative for spending, this method is used

by managers of company Touchdown Trips Inc.

Two possible investment approaches are being outlined, namely the Gulfstream G650ER

(option- A) and Boeing BBJ Max 7 (option- B). With assistance of ARR evaluation,

management is enabled to make appropriate selections, and Option A is healthier investment

option which produces 28.46 percent yield on investment. This approach has many rewards, such

as measuring and recognizing the turnaround duration is very efficient and easy. It would take

into consideration the net profit or sum earned over the whole life-cycle of an investment. This

model considers net earnings aspect which is amount of net earnings post taxes and depreciation.

This is a key consideration in appraisal of any investment. This approach allows the future

proposal to be compared to competitive essence of cost-reduction plan or other proposals. This

method offers a clear explanation of a project 's feasibility. This approach alone acknowledges

the accounting concept of gains for the estimation of yield or rate of return (DAVALLOU and

MAHMOODI, 2017).

(d) Merits and demerit points of the approach of IRR.

Option A of investment is selected on the grounds of the above-mentioned analysis, that has

a better recovery period and a higher ARR. Furthermore, with the assistance of investment

analysis techniques, Touchdown Trips Inc. executives will be able to make feasible decisions.

Techniques to investment evaluation have certain characteristics that have a broader

importance as discussed below:

• Evaluation of the sum of projected gains received relative to the extent of consistent

investment.

• It envisages the future costs, risks and benefits to be occurred throughout the

project’s life cycle.

• An investment or project's feasibility in terms of expected return, pay-back duration as

well as profitability can be measured to support decision making and making effective

comparison of projects/investments.

• Useful life of a project and how project will retrieve initial investment within project's

useful life can be determined.

• Outcomes of these techniques are based on projected data hence allow managers to take

long term decisions.

Beside all these techniques there is also a crucial technique named IRR, which is discounting

cash flow approach that offers rate of returning which an investment receives. IRR can be

defined/referred as discount rate that equates to nil for an overall initial outlay including

discounted cash-inflows (Endrijaitis, 2020). It is, in simple words, discount rate at which current

net value would be equivalent to 0. Here certain key merits and demerits of IRR, listed below:

Merits: The IRR makes it very easy to make choices. One just require to equate the proportion

of IRR to one can get by spending elsewhere or any other targets determined by management.

This approach would offer an unfavourable/negative percentage to project that is not capable of

getting that investment returned. The primary merit of IRR of project assessment is that

this clearly shows in percentage figures what project in question will produce. The appraiser now

just has to determine which percentage to contrast with. One do not require a hurdle percentage

to be determined in advance. Outcome of this approach would not be influenced by an error in

determining the hurdle threshold (Hiferding, 2019).

Option A of investment is selected on the grounds of the above-mentioned analysis, that has

a better recovery period and a higher ARR. Furthermore, with the assistance of investment

analysis techniques, Touchdown Trips Inc. executives will be able to make feasible decisions.

Techniques to investment evaluation have certain characteristics that have a broader

importance as discussed below:

• Evaluation of the sum of projected gains received relative to the extent of consistent

investment.

• It envisages the future costs, risks and benefits to be occurred throughout the

project’s life cycle.

• An investment or project's feasibility in terms of expected return, pay-back duration as

well as profitability can be measured to support decision making and making effective

comparison of projects/investments.

• Useful life of a project and how project will retrieve initial investment within project's

useful life can be determined.

• Outcomes of these techniques are based on projected data hence allow managers to take

long term decisions.

Beside all these techniques there is also a crucial technique named IRR, which is discounting

cash flow approach that offers rate of returning which an investment receives. IRR can be

defined/referred as discount rate that equates to nil for an overall initial outlay including

discounted cash-inflows (Endrijaitis, 2020). It is, in simple words, discount rate at which current

net value would be equivalent to 0. Here certain key merits and demerits of IRR, listed below:

Merits: The IRR makes it very easy to make choices. One just require to equate the proportion

of IRR to one can get by spending elsewhere or any other targets determined by management.

This approach would offer an unfavourable/negative percentage to project that is not capable of

getting that investment returned. The primary merit of IRR of project assessment is that

this clearly shows in percentage figures what project in question will produce. The appraiser now

just has to determine which percentage to contrast with. One do not require a hurdle percentage

to be determined in advance. Outcome of this approach would not be influenced by an error in

determining the hurdle threshold (Hiferding, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Demerits: When someone compare mutually exclusive projects/investments, a IRR technique is

typically not the appropriate measurement to employ. This implies manager can't consider other

one if they plan to support one of projects/investments. Managers have to project initial costs in

attempt to employ the IRR estimation. This could be hard to define and could cause the equation

to become distorted.

Question 3

Calculations of following ratios:

In attempt to assess its financial status, liquidity level, profitability status, risk, financial

stability, performance, and operational efficacy, ratio calculations and analysis is significant for

the organization and the appropriate use of resources, and also shows the pattern or correlation of

financial outcomes that can be beneficial for the corporation 's stakeholders to make financial

decisions (Kristanti and Herwany, 2017). In this regard here are computation of different

financial ratios based on the data of financial statements of Agro Company, as follows:

Gross profit margin:

Gross profit margin = Gross profit / Revenue * 100

= 1313 / 3495 * 100

= 37.56%

Assets turnover ratio:

Assets turnover ratio = Net Sales / Total assets

= 3495 / 2898

= 1.20 times

Current ratio:

Current ratio = Current assets / Current liabilities

= 1687 / 744

= 2.26 times

Acid test ratio:

Acid test ratio = Quick assets / Current liabilities

= 1537 / 744

= 2.06 times

Working Notes:

Quick assets = Current assets – Inventory

typically not the appropriate measurement to employ. This implies manager can't consider other

one if they plan to support one of projects/investments. Managers have to project initial costs in

attempt to employ the IRR estimation. This could be hard to define and could cause the equation

to become distorted.

Question 3

Calculations of following ratios:

In attempt to assess its financial status, liquidity level, profitability status, risk, financial

stability, performance, and operational efficacy, ratio calculations and analysis is significant for

the organization and the appropriate use of resources, and also shows the pattern or correlation of

financial outcomes that can be beneficial for the corporation 's stakeholders to make financial

decisions (Kristanti and Herwany, 2017). In this regard here are computation of different

financial ratios based on the data of financial statements of Agro Company, as follows:

Gross profit margin:

Gross profit margin = Gross profit / Revenue * 100

= 1313 / 3495 * 100

= 37.56%

Assets turnover ratio:

Assets turnover ratio = Net Sales / Total assets

= 3495 / 2898

= 1.20 times

Current ratio:

Current ratio = Current assets / Current liabilities

= 1687 / 744

= 2.26 times

Acid test ratio:

Acid test ratio = Quick assets / Current liabilities

= 1537 / 744

= 2.06 times

Working Notes:

Quick assets = Current assets – Inventory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 1687 – 150

= 1537

Inventories turnover period:

Inventories turnover period = Cost of Goods Sold (COGS) / Average Inventory

= 2182 / 126

= 17.31

Working Notes:

Average inventory = (Opening stock + Closing stock) / 2

= (102 + 150) / 2

= 252 / 2

= 126

Debt to Equity ratio:

Debt to Equity ratio = Total liabilities / Total shareholder’s equity

= 914 / 2898

= 0.31

Critically explaining major importance of considering audience for financial statement

analysis:

Analysis of financial statements considered as method of evaluating and analysing the

corporation's financial statements for making informed financial choices. In simple terms by

creating a strategic alliance among balance sheet elements, the income statement, and several

other financial reports, the method of assessing the financial assets and deficiencies of an

organization. The word 'analysis' indicates effective simplification of fiscal information by

methodical sorting of the information presented under financial statements,' interpretation'

implies,' describing the purpose and importance of the details so condensed (La Soa, 2019).

However, these are interconnected as well as complementary. The top executives are obsessed

about the firm 's future outlook. Financial analysis allows them to analyse the investment options

in order to judge the company's profit prospects. The estimation and estimation of default and the

risk of company loss could be attained with the aid of the financial statement analysis.

FS analysis tends to determine whether or not credit will be offered to the business by financial

= 1537

Inventories turnover period:

Inventories turnover period = Cost of Goods Sold (COGS) / Average Inventory

= 2182 / 126

= 17.31

Working Notes:

Average inventory = (Opening stock + Closing stock) / 2

= (102 + 150) / 2

= 252 / 2

= 126

Debt to Equity ratio:

Debt to Equity ratio = Total liabilities / Total shareholder’s equity

= 914 / 2898

= 0.31

Critically explaining major importance of considering audience for financial statement

analysis:

Analysis of financial statements considered as method of evaluating and analysing the

corporation's financial statements for making informed financial choices. In simple terms by

creating a strategic alliance among balance sheet elements, the income statement, and several

other financial reports, the method of assessing the financial assets and deficiencies of an

organization. The word 'analysis' indicates effective simplification of fiscal information by

methodical sorting of the information presented under financial statements,' interpretation'

implies,' describing the purpose and importance of the details so condensed (La Soa, 2019).

However, these are interconnected as well as complementary. The top executives are obsessed

about the firm 's future outlook. Financial analysis allows them to analyse the investment options

in order to judge the company's profit prospects. The estimation and estimation of default and the

risk of company loss could be attained with the aid of the financial statement analysis.

FS analysis tends to determine whether or not credit will be offered to the business by financial

companies, lending agencies & lenders. It allows them to assess the default risks, if approved,

decide the contract terms of lending, interest rates, maturity period etc. Audience are key aspect

in analysis of financial statements as these are main personnel which are users as well as

influencer as their decision affects company’s performance. Here are certain targeted audience to

be considered in financial-statement analysis, as discussed below:

Trade-payable/Creditors: Importance of analysis of financial statements as follows:

• Assessing the business's capacity to fulfil its shorter - term commitments

• Assessing the possibility of the company's continuing willingness to satisfy all its

financial commitments in the coming years.

• The willingness of the company to resolve creditors' demands within a relatively

shorter period of time.

• Assessment of the financial situation and the potential to paying off the issues.

Lenders

Long-term debt providers are obsessed with the longer-term financial viability and sustainability

of the business. They analyse company's financial statements:

• To determine the organisation 's viability over specific time period,

• To assess the capacity of a corporation to raise capital, to incur interest and reimburse

principal sum,

• Assessing the connection between different sources of funding (i.e. relations with the

capital framework)

• To evaluate and perceive financial statements containing data on historical results as a

foundation for predicting potential rates of return including risks assessment.

• Determine terms and conditions attached with a loan if held liable, interest rates, and

maturity period etc. to assess credit risk (Schwichtenberg, 2019).

Investors

Investors that have allocated their cash in the securities of the corporation are concerned in the

performance and potential sustainability of the company. Analysing financial statements aids

them in estimating the risk of default and loss of business companies. Investors should take

proactive steps to avoid / minimise losses after becoming conscious of the possible failure

(Silvant and Arrupe, 2020).

Top Management

decide the contract terms of lending, interest rates, maturity period etc. Audience are key aspect

in analysis of financial statements as these are main personnel which are users as well as

influencer as their decision affects company’s performance. Here are certain targeted audience to

be considered in financial-statement analysis, as discussed below:

Trade-payable/Creditors: Importance of analysis of financial statements as follows:

• Assessing the business's capacity to fulfil its shorter - term commitments

• Assessing the possibility of the company's continuing willingness to satisfy all its

financial commitments in the coming years.

• The willingness of the company to resolve creditors' demands within a relatively

shorter period of time.

• Assessment of the financial situation and the potential to paying off the issues.

Lenders

Long-term debt providers are obsessed with the longer-term financial viability and sustainability

of the business. They analyse company's financial statements:

• To determine the organisation 's viability over specific time period,

• To assess the capacity of a corporation to raise capital, to incur interest and reimburse

principal sum,

• Assessing the connection between different sources of funding (i.e. relations with the

capital framework)

• To evaluate and perceive financial statements containing data on historical results as a

foundation for predicting potential rates of return including risks assessment.

• Determine terms and conditions attached with a loan if held liable, interest rates, and

maturity period etc. to assess credit risk (Schwichtenberg, 2019).

Investors

Investors that have allocated their cash in the securities of the corporation are concerned in the

performance and potential sustainability of the company. Analysing financial statements aids

them in estimating the risk of default and loss of business companies. Investors should take

proactive steps to avoid / minimise losses after becoming conscious of the possible failure

(Silvant and Arrupe, 2020).

Top Management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.