Finance for Business: Corporate Ethics, Investment Analysis, Dusk Ltd

VerifiedAdded on 2023/06/11

|15

|3279

|183

Report

AI Summary

This report addresses key aspects of finance for business, starting with an analysis of the corporate ethics failure of One.Tel, including prevention strategies and lessons learned. It then delves into financial calculations such as present value and future value of cash flows, and effective annual rates. A comparative analysis of two models for Asian Fusion Restaurant is conducted, advising on the best model based on cash outflow. The report further evaluates an investment project for ElectroTech Ltd, calculating Net Present Value (NPV) and Internal Rate of Return (IRR), ultimately recommending rejection of the project based on financial results. Finally, the report discusses advantages and disadvantages of private equity financing and explores alternative sources of finance, along with calculating the weighted average cost of capital for Dusk Ltd. Desklib provides students with access to similar solved assignments and past papers.

FINANCE FOR BUSINESS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

1)One. Tel limited failed in corporate ethics:..............................................................................3

2)How could it have been prevented by management:................................................................3

3) Lessons learnt and business implication for business commodity:.........................................4

(i) Present Value of Cash Flows..................................................................................................4

(ii) Future Value of Cash Flows...................................................................................................5

(iii) Effective annual rate.............................................................................................................5

Question 3........................................................................................................................................5

(a) Best Model selection..............................................................................................................5

(b).................................................................................................................................................7

(i) Calculation of Net Present Value and Internal Rate of Return of EletroTech Ltd Equipment

......................................................................................................................................................7

(ii) Recommendation...................................................................................................................9

(iii) Factors affecting investment decision...................................................................................9

Question 4........................................................................................................................................9

(a).................................................................................................................................................9

(b)...............................................................................................................................................10

(c)...............................................................................................................................................10

(d)...............................................................................................................................................11

(e) Weighted average cost of capital of Dusk Ltd.....................................................................11

Question 5......................................................................................................................................11

(a)...............................................................................................................................................11

(b)...............................................................................................................................................12

...................................................................................................................................................13

REFERENCES................................................................................................................................1

Question 1........................................................................................................................................3

1)One. Tel limited failed in corporate ethics:..............................................................................3

2)How could it have been prevented by management:................................................................3

3) Lessons learnt and business implication for business commodity:.........................................4

(i) Present Value of Cash Flows..................................................................................................4

(ii) Future Value of Cash Flows...................................................................................................5

(iii) Effective annual rate.............................................................................................................5

Question 3........................................................................................................................................5

(a) Best Model selection..............................................................................................................5

(b).................................................................................................................................................7

(i) Calculation of Net Present Value and Internal Rate of Return of EletroTech Ltd Equipment

......................................................................................................................................................7

(ii) Recommendation...................................................................................................................9

(iii) Factors affecting investment decision...................................................................................9

Question 4........................................................................................................................................9

(a).................................................................................................................................................9

(b)...............................................................................................................................................10

(c)...............................................................................................................................................10

(d)...............................................................................................................................................11

(e) Weighted average cost of capital of Dusk Ltd.....................................................................11

Question 5......................................................................................................................................11

(a)...............................................................................................................................................11

(b)...............................................................................................................................................12

...................................................................................................................................................13

REFERENCES................................................................................................................................1

Question 1

1)One. Tel limited failed in corporate ethics:

One. Tel company is an Australian based telecommunications company. The company

are private limited company which offers the landlines phones, mobile phones and internet

services as well as provides residential and commercial telecommunication services and it is a

market leader in providing network solutions for businesses of all sizes or network solution

provider in the alarm industry. The company was very people focused and focused on market as

corporate business. It was the fourth largest telecommunication company in Australia which had

more than two million customers and operates in eight countries. It was a major corporate

collapse in Australia. One. Tel collapse is a classic case which failed in expectation, strategic

mistakes, wrong pricing policy and its unbridled growth. From various studies, One. Tel

company is failed to manage the corporate ethics in the workplace. Australian computer society

code in the light of the information technologies which is employed by the Australian

telecommunication company One. Tel limited (Chitehwe, 2019). The company was seen failure

in information system, in particular failed in the billing system. This case arise issues of

professional behaviour and ethics of information technology personnel and management at One.

Tel limited.

2)How could it have been prevented by management:

Business ethics can place current technology challenges and it has every thing to do with

management So, Managers must acknowledge their role before shaping business ethics. There

was a lack of diversity of opinions in the board and management does not make full discloser to

the board about the management performance of the firm so, their must be discloser about the

business performance and clearly defined responsibilities between the board and the

management which are vital for effective corporate governance. Non- executive board member

should make their own enquiries into firm strategies and performance thus, non-executive

member should have middle and lower management to ensure transparency of information as

well as large investors in firm must be take active interest in managing the firm. Executives who

ignore the business ethics can run the arise of management and corporate liability in strong legal

environment (Mubaraq and Abdulrasaq, 2019). One. Tel company must relive their new ethics

with new guidelines which helps to recognize the guidelines of organization and managerial root.

1)One. Tel limited failed in corporate ethics:

One. Tel company is an Australian based telecommunications company. The company

are private limited company which offers the landlines phones, mobile phones and internet

services as well as provides residential and commercial telecommunication services and it is a

market leader in providing network solutions for businesses of all sizes or network solution

provider in the alarm industry. The company was very people focused and focused on market as

corporate business. It was the fourth largest telecommunication company in Australia which had

more than two million customers and operates in eight countries. It was a major corporate

collapse in Australia. One. Tel collapse is a classic case which failed in expectation, strategic

mistakes, wrong pricing policy and its unbridled growth. From various studies, One. Tel

company is failed to manage the corporate ethics in the workplace. Australian computer society

code in the light of the information technologies which is employed by the Australian

telecommunication company One. Tel limited (Chitehwe, 2019). The company was seen failure

in information system, in particular failed in the billing system. This case arise issues of

professional behaviour and ethics of information technology personnel and management at One.

Tel limited.

2)How could it have been prevented by management:

Business ethics can place current technology challenges and it has every thing to do with

management So, Managers must acknowledge their role before shaping business ethics. There

was a lack of diversity of opinions in the board and management does not make full discloser to

the board about the management performance of the firm so, their must be discloser about the

business performance and clearly defined responsibilities between the board and the

management which are vital for effective corporate governance. Non- executive board member

should make their own enquiries into firm strategies and performance thus, non-executive

member should have middle and lower management to ensure transparency of information as

well as large investors in firm must be take active interest in managing the firm. Executives who

ignore the business ethics can run the arise of management and corporate liability in strong legal

environment (Mubaraq and Abdulrasaq, 2019). One. Tel company must relive their new ethics

with new guidelines which helps to recognize the guidelines of organization and managerial root.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3) Lessons learnt and business implication for business commodity:

The ethical implication of technology focus on the ways that creative morale and ethical

principles. One. Tel limited technologies studies offers a robust vocabulary for describing where

ethics intersect with technology agency. In the case study of collapse of One. Tel shock to

corporate world while demonstrate that weaknesses in governance practice in relation to control

management system, audit quality, and financial reporting quality so, it has to understand their

business history in terms of the business models, growth, strategies is important for identifying

antecedents to its collapse. Company should work in concert with humans. They must explore

ethics in the classification of future technologies, maintain the ethics relationships between firms

and worker, ethics between firms and other firms and as well as ethical governance of

technology must use with in the organization. One .Tel marketing and advertising campaigns

created an impression that the company was targeting the back packaging community which

helps to sign up new customers which accelerate sales and growth of customers. One. Tel

collapse leave several lessons on corporate strategies, firstly it is not enough to acquire

customers in large scale unless customers must be contributed towards profitable of the firm.

Secondly, sales generation are not enough unless revenues are collected into cash timely and

third, high competitive price only gain the market share which can disastrous consequences.

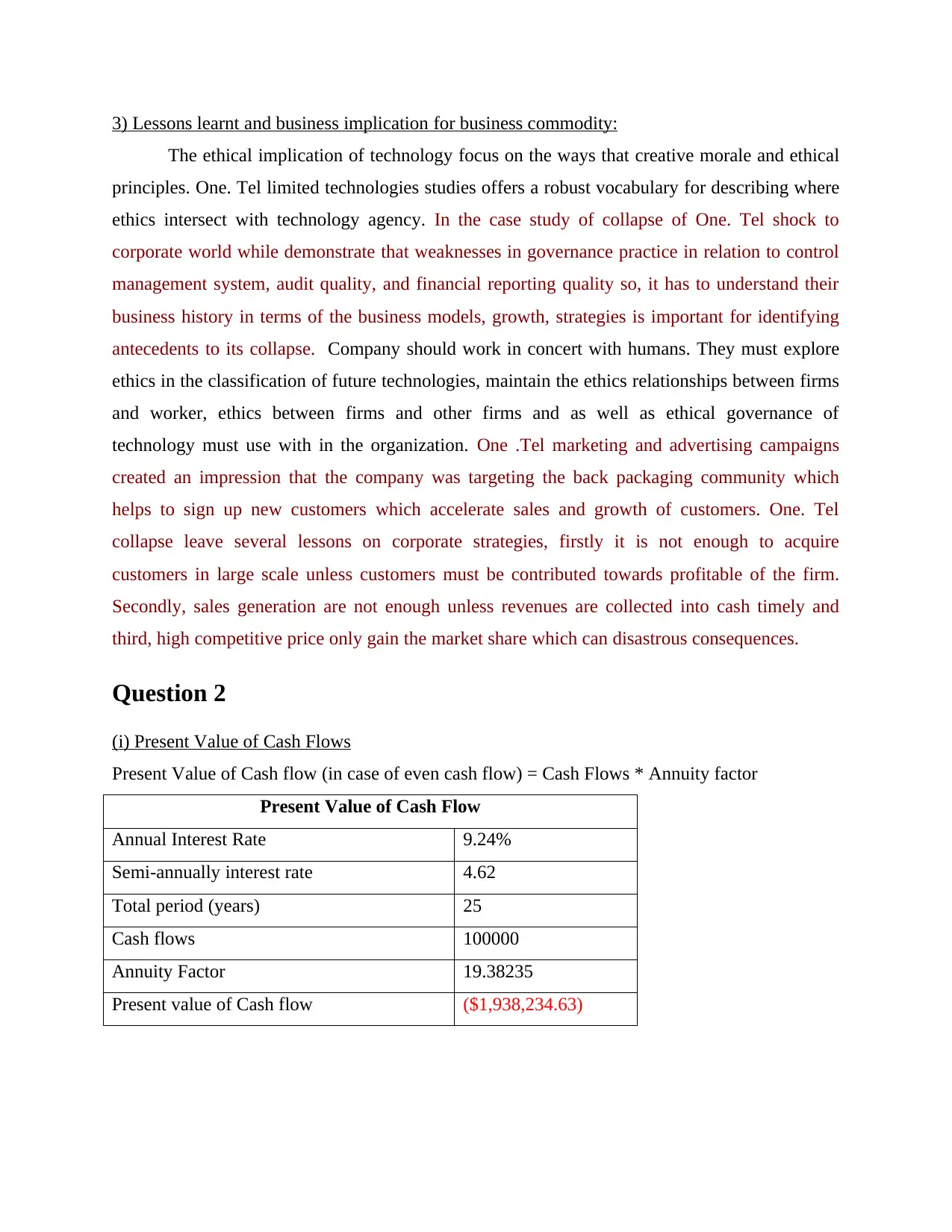

Question 2

(i) Present Value of Cash Flows

Present Value of Cash flow (in case of even cash flow) = Cash Flows * Annuity factor

Present Value of Cash Flow

Annual Interest Rate 9.24%

Semi-annually interest rate 4.62

Total period (years) 25

Cash flows 100000

Annuity Factor 19.38235

Present value of Cash flow ($1,938,234.63)

The ethical implication of technology focus on the ways that creative morale and ethical

principles. One. Tel limited technologies studies offers a robust vocabulary for describing where

ethics intersect with technology agency. In the case study of collapse of One. Tel shock to

corporate world while demonstrate that weaknesses in governance practice in relation to control

management system, audit quality, and financial reporting quality so, it has to understand their

business history in terms of the business models, growth, strategies is important for identifying

antecedents to its collapse. Company should work in concert with humans. They must explore

ethics in the classification of future technologies, maintain the ethics relationships between firms

and worker, ethics between firms and other firms and as well as ethical governance of

technology must use with in the organization. One .Tel marketing and advertising campaigns

created an impression that the company was targeting the back packaging community which

helps to sign up new customers which accelerate sales and growth of customers. One. Tel

collapse leave several lessons on corporate strategies, firstly it is not enough to acquire

customers in large scale unless customers must be contributed towards profitable of the firm.

Secondly, sales generation are not enough unless revenues are collected into cash timely and

third, high competitive price only gain the market share which can disastrous consequences.

Question 2

(i) Present Value of Cash Flows

Present Value of Cash flow (in case of even cash flow) = Cash Flows * Annuity factor

Present Value of Cash Flow

Annual Interest Rate 9.24%

Semi-annually interest rate 4.62

Total period (years) 25

Cash flows 100000

Annuity Factor 19.38235

Present value of Cash flow ($1,938,234.63)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On the basis of above computation, it is identified that the present value of cash flow of $100000

for every six months is $1938234.63. This is computed by converting annual interest to semi-

annually interest rate.

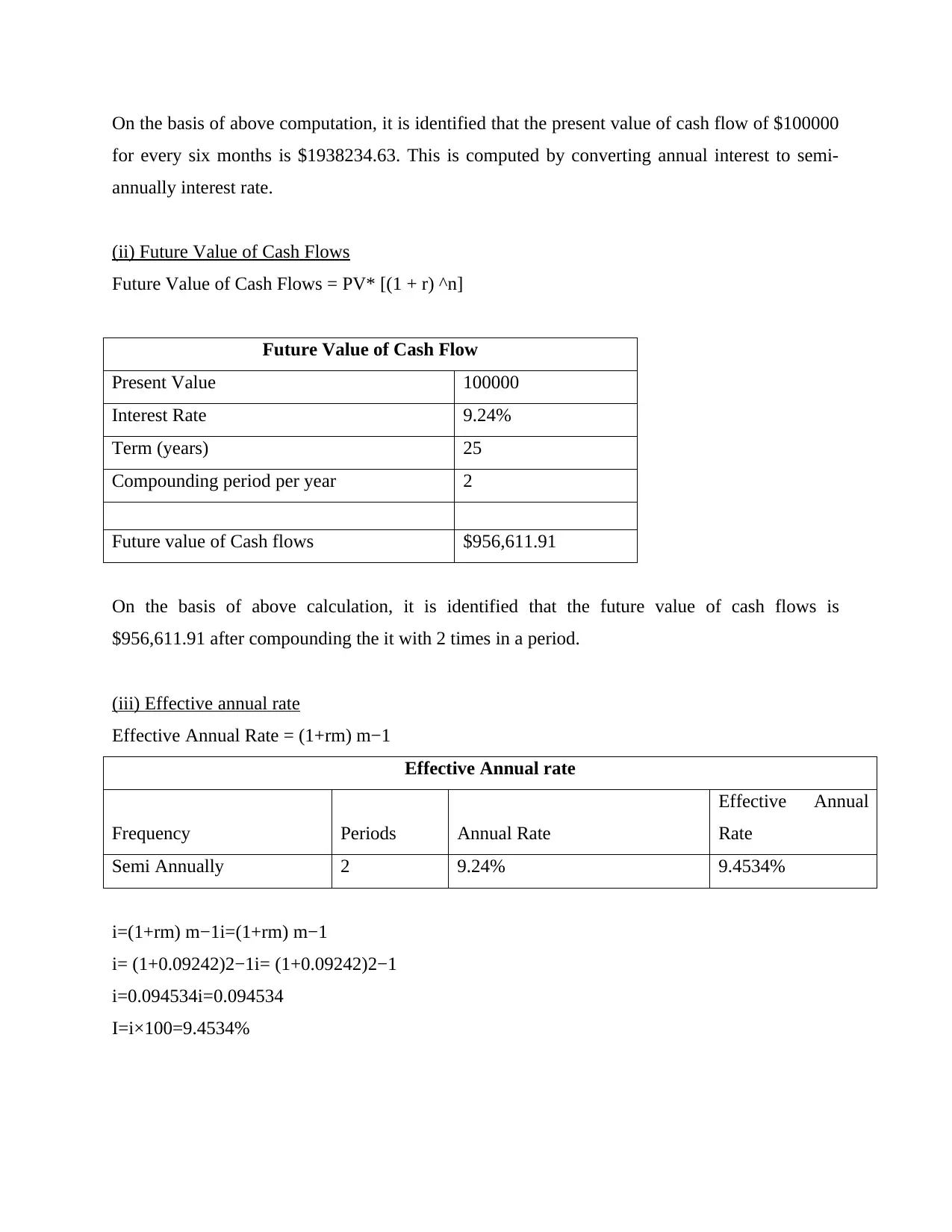

(ii) Future Value of Cash Flows

Future Value of Cash Flows = PV* [(1 + r) ^n]

Future Value of Cash Flow

Present Value 100000

Interest Rate 9.24%

Term (years) 25

Compounding period per year 2

Future value of Cash flows $956,611.91

On the basis of above calculation, it is identified that the future value of cash flows is

$956,611.91 after compounding the it with 2 times in a period.

(iii) Effective annual rate

Effective Annual Rate = (1+rm) m−1

Effective Annual rate

Frequency Periods Annual Rate

Effective Annual

Rate

Semi Annually 2 9.24% 9.4534%

i=(1+rm) m−1i=(1+rm) m−1

i= (1+0.09242)2−1i= (1+0.09242)2−1

i=0.094534i=0.094534

I=i×100=9.4534%

for every six months is $1938234.63. This is computed by converting annual interest to semi-

annually interest rate.

(ii) Future Value of Cash Flows

Future Value of Cash Flows = PV* [(1 + r) ^n]

Future Value of Cash Flow

Present Value 100000

Interest Rate 9.24%

Term (years) 25

Compounding period per year 2

Future value of Cash flows $956,611.91

On the basis of above calculation, it is identified that the future value of cash flows is

$956,611.91 after compounding the it with 2 times in a period.

(iii) Effective annual rate

Effective Annual Rate = (1+rm) m−1

Effective Annual rate

Frequency Periods Annual Rate

Effective Annual

Rate

Semi Annually 2 9.24% 9.4534%

i=(1+rm) m−1i=(1+rm) m−1

i= (1+0.09242)2−1i= (1+0.09242)2−1

i=0.094534i=0.094534

I=i×100=9.4534%

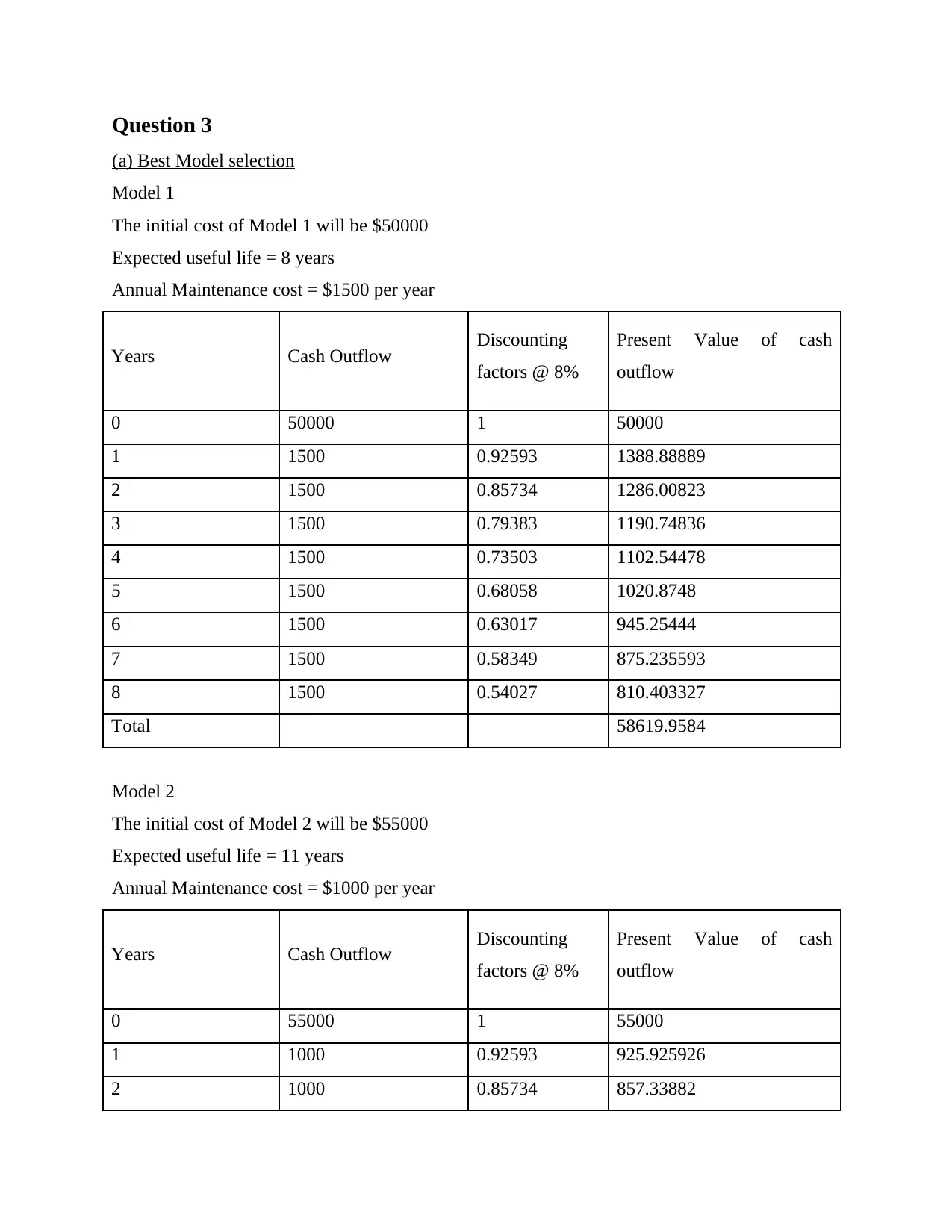

Question 3

(a) Best Model selection

Model 1

The initial cost of Model 1 will be $50000

Expected useful life = 8 years

Annual Maintenance cost = $1500 per year

Years Cash Outflow Discounting

factors @ 8%

Present Value of cash

outflow

0 50000 1 50000

1 1500 0.92593 1388.88889

2 1500 0.85734 1286.00823

3 1500 0.79383 1190.74836

4 1500 0.73503 1102.54478

5 1500 0.68058 1020.8748

6 1500 0.63017 945.25444

7 1500 0.58349 875.235593

8 1500 0.54027 810.403327

Total 58619.9584

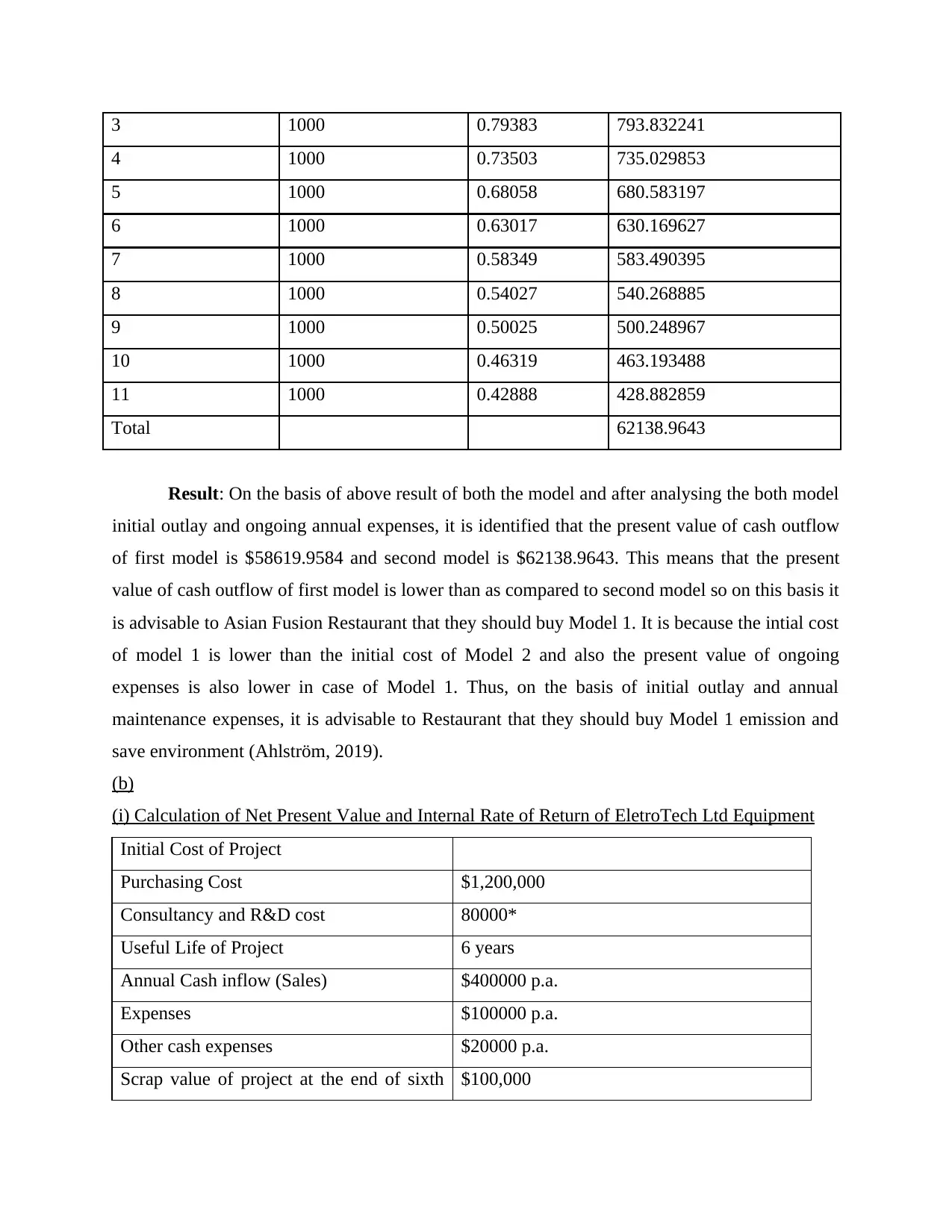

Model 2

The initial cost of Model 2 will be $55000

Expected useful life = 11 years

Annual Maintenance cost = $1000 per year

Years Cash Outflow Discounting

factors @ 8%

Present Value of cash

outflow

0 55000 1 55000

1 1000 0.92593 925.925926

2 1000 0.85734 857.33882

(a) Best Model selection

Model 1

The initial cost of Model 1 will be $50000

Expected useful life = 8 years

Annual Maintenance cost = $1500 per year

Years Cash Outflow Discounting

factors @ 8%

Present Value of cash

outflow

0 50000 1 50000

1 1500 0.92593 1388.88889

2 1500 0.85734 1286.00823

3 1500 0.79383 1190.74836

4 1500 0.73503 1102.54478

5 1500 0.68058 1020.8748

6 1500 0.63017 945.25444

7 1500 0.58349 875.235593

8 1500 0.54027 810.403327

Total 58619.9584

Model 2

The initial cost of Model 2 will be $55000

Expected useful life = 11 years

Annual Maintenance cost = $1000 per year

Years Cash Outflow Discounting

factors @ 8%

Present Value of cash

outflow

0 55000 1 55000

1 1000 0.92593 925.925926

2 1000 0.85734 857.33882

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 1000 0.79383 793.832241

4 1000 0.73503 735.029853

5 1000 0.68058 680.583197

6 1000 0.63017 630.169627

7 1000 0.58349 583.490395

8 1000 0.54027 540.268885

9 1000 0.50025 500.248967

10 1000 0.46319 463.193488

11 1000 0.42888 428.882859

Total 62138.9643

Result: On the basis of above result of both the model and after analysing the both model

initial outlay and ongoing annual expenses, it is identified that the present value of cash outflow

of first model is $58619.9584 and second model is $62138.9643. This means that the present

value of cash outflow of first model is lower than as compared to second model so on this basis it

is advisable to Asian Fusion Restaurant that they should buy Model 1. It is because the intial cost

of model 1 is lower than the initial cost of Model 2 and also the present value of ongoing

expenses is also lower in case of Model 1. Thus, on the basis of initial outlay and annual

maintenance expenses, it is advisable to Restaurant that they should buy Model 1 emission and

save environment (Ahlström, 2019).

(b)

(i) Calculation of Net Present Value and Internal Rate of Return of EletroTech Ltd Equipment

Initial Cost of Project

Purchasing Cost $1,200,000

Consultancy and R&D cost 80000*

Useful Life of Project 6 years

Annual Cash inflow (Sales) $400000 p.a.

Expenses $100000 p.a.

Other cash expenses $20000 p.a.

Scrap value of project at the end of sixth $100,000

4 1000 0.73503 735.029853

5 1000 0.68058 680.583197

6 1000 0.63017 630.169627

7 1000 0.58349 583.490395

8 1000 0.54027 540.268885

9 1000 0.50025 500.248967

10 1000 0.46319 463.193488

11 1000 0.42888 428.882859

Total 62138.9643

Result: On the basis of above result of both the model and after analysing the both model

initial outlay and ongoing annual expenses, it is identified that the present value of cash outflow

of first model is $58619.9584 and second model is $62138.9643. This means that the present

value of cash outflow of first model is lower than as compared to second model so on this basis it

is advisable to Asian Fusion Restaurant that they should buy Model 1. It is because the intial cost

of model 1 is lower than the initial cost of Model 2 and also the present value of ongoing

expenses is also lower in case of Model 1. Thus, on the basis of initial outlay and annual

maintenance expenses, it is advisable to Restaurant that they should buy Model 1 emission and

save environment (Ahlström, 2019).

(b)

(i) Calculation of Net Present Value and Internal Rate of Return of EletroTech Ltd Equipment

Initial Cost of Project

Purchasing Cost $1,200,000

Consultancy and R&D cost 80000*

Useful Life of Project 6 years

Annual Cash inflow (Sales) $400000 p.a.

Expenses $100000 p.a.

Other cash expenses $20000 p.a.

Scrap value of project at the end of sixth $100,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

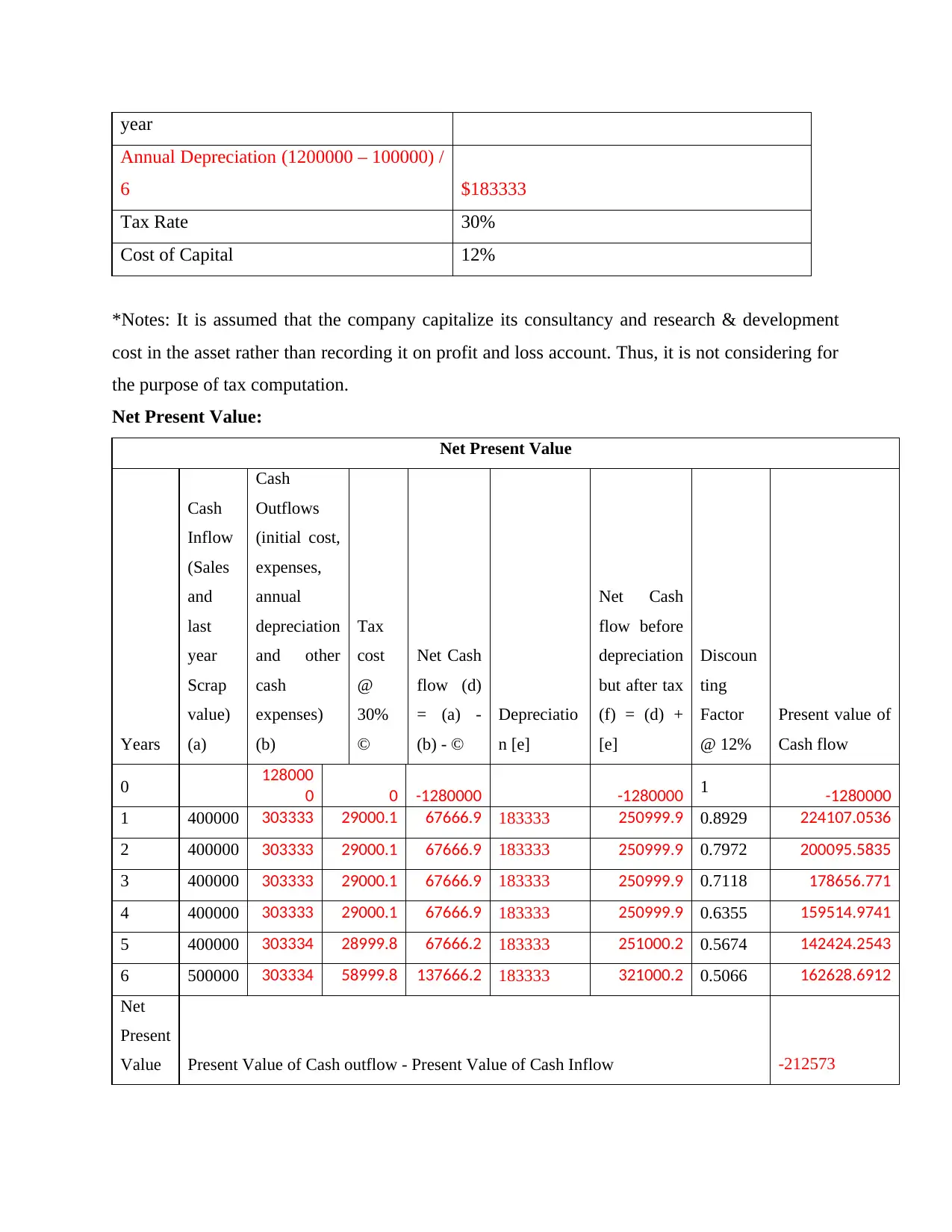

year

Annual Depreciation (1200000 – 100000) /

6 $183333

Tax Rate 30%

Cost of Capital 12%

*Notes: It is assumed that the company capitalize its consultancy and research & development

cost in the asset rather than recording it on profit and loss account. Thus, it is not considering for

the purpose of tax computation.

Net Present Value:

Net Present Value

Years

Cash

Inflow

(Sales

and

last

year

Scrap

value)

(a)

Cash

Outflows

(initial cost,

expenses,

annual

depreciation

and other

cash

expenses)

(b)

Tax

cost

@

30%

©

Net Cash

flow (d)

= (a) -

(b) - ©

Depreciatio

n [e]

Net Cash

flow before

depreciation

but after tax

(f) = (d) +

[e]

Discoun

ting

Factor

@ 12%

Present value of

Cash flow

0 128000

0 0 -1280000 -1280000 1 -1280000

1 400000 303333 29000.1 67666.9 183333 250999.9 0.8929 224107.0536

2 400000 303333 29000.1 67666.9 183333 250999.9 0.7972 200095.5835

3 400000 303333 29000.1 67666.9 183333 250999.9 0.7118 178656.771

4 400000 303333 29000.1 67666.9 183333 250999.9 0.6355 159514.9741

5 400000 303334 28999.8 67666.2 183333 251000.2 0.5674 142424.2543

6 500000 303334 58999.8 137666.2 183333 321000.2 0.5066 162628.6912

Net

Present

Value Present Value of Cash outflow - Present Value of Cash Inflow -212573

Annual Depreciation (1200000 – 100000) /

6 $183333

Tax Rate 30%

Cost of Capital 12%

*Notes: It is assumed that the company capitalize its consultancy and research & development

cost in the asset rather than recording it on profit and loss account. Thus, it is not considering for

the purpose of tax computation.

Net Present Value:

Net Present Value

Years

Cash

Inflow

(Sales

and

last

year

Scrap

value)

(a)

Cash

Outflows

(initial cost,

expenses,

annual

depreciation

and other

cash

expenses)

(b)

Tax

cost

@

30%

©

Net Cash

flow (d)

= (a) -

(b) - ©

Depreciatio

n [e]

Net Cash

flow before

depreciation

but after tax

(f) = (d) +

[e]

Discoun

ting

Factor

@ 12%

Present value of

Cash flow

0 128000

0 0 -1280000 -1280000 1 -1280000

1 400000 303333 29000.1 67666.9 183333 250999.9 0.8929 224107.0536

2 400000 303333 29000.1 67666.9 183333 250999.9 0.7972 200095.5835

3 400000 303333 29000.1 67666.9 183333 250999.9 0.7118 178656.771

4 400000 303333 29000.1 67666.9 183333 250999.9 0.6355 159514.9741

5 400000 303334 28999.8 67666.2 183333 251000.2 0.5674 142424.2543

6 500000 303334 58999.8 137666.2 183333 321000.2 0.5066 162628.6912

Net

Present

Value Present Value of Cash outflow - Present Value of Cash Inflow -212573

Internal Rate of Return:

Internal Rate of Return

Year

Net Cash

Flow

Discounting

Factor @ 12%

Present value of

Cash flow

Discounting

Factor @ 5%

Present value of

Cash flow

0 -1280000 1 -1280000 1 -1280000

1 250999.9 0.8929 224107.05 0.9524 239047.524

2 250999.9 0.7972 200095.58 0.9070 227664.308

3 250999.9 0.7118 178656.77 0.8638 216823.151

4 250999.9 0.6355 159514.97 0.8227 206498.239

5 251000.2 0.5674 142424.25 0.7835 196665.224

6 321000.2 0.5066 162628.69 0.7462 239535.292

-212573 46234

Formula of Internal Rate of Return =

ra = lower discount rate chosen = 5%

rb = Higher discount rate Chosen = 12%

Na = NPV at ra = 46234

Nb = NPV at rb = -212573

= 5% + [46234 / (46234 – - 212573)] * (12% – 5%)

= 5% + [46234 / 258807] * 7%

= 5% + 0.18 * 7%

= 5% + 1.26%

= 6.26%

(ii) Recommendation

On the basis of above NPV and IRR calculation, it is identified that the net present value of

equipment is negative and internal rate of return of equipment is below cost of acquisition (Billio

Internal Rate of Return

Year

Net Cash

Flow

Discounting

Factor @ 12%

Present value of

Cash flow

Discounting

Factor @ 5%

Present value of

Cash flow

0 -1280000 1 -1280000 1 -1280000

1 250999.9 0.8929 224107.05 0.9524 239047.524

2 250999.9 0.7972 200095.58 0.9070 227664.308

3 250999.9 0.7118 178656.77 0.8638 216823.151

4 250999.9 0.6355 159514.97 0.8227 206498.239

5 251000.2 0.5674 142424.25 0.7835 196665.224

6 321000.2 0.5066 162628.69 0.7462 239535.292

-212573 46234

Formula of Internal Rate of Return =

ra = lower discount rate chosen = 5%

rb = Higher discount rate Chosen = 12%

Na = NPV at ra = 46234

Nb = NPV at rb = -212573

= 5% + [46234 / (46234 – - 212573)] * (12% – 5%)

= 5% + [46234 / 258807] * 7%

= 5% + 0.18 * 7%

= 5% + 1.26%

= 6.26%

(ii) Recommendation

On the basis of above NPV and IRR calculation, it is identified that the net present value of

equipment is negative and internal rate of return of equipment is below cost of acquisition (Billio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and Varotto, 2020). So, on this basis it can be analyzed that the ElectroTech Ltd should reject

this project as they unable higher profit return that the cost of acquisition.

(iii) Factors affecting investment decision

Beside return on investment, the risk is also need to be taken into consideration while

making investment related decision.

The period of investment and inflation rate is also need to be consider while making

business decision.

Further, investment volatility factor and liquidity position is also plays vital role in

identifying whether the project is profitable or not.

The change in the internal as well as external business environment is also one of the

factor that should be consider by the company before making any decision (Falchetta and

et.al., 2022).

Question 4

(a)

Advantage of Private Equity financing:

The private equity source of finance adds working capital to the business as it can

provide cash infusion that is best for supporting new and struggling business.

Another advantage of private equity is such that the valuation of private equity is not

affected by the public market and they also need not to move through high-interest loans.

The private equity financing allows more freedom for the growth of the business which

ultimately leads to higher profitability and expansion.

Disadvantages of Private Equity:

It requires upfront funding and also sometime returns are often smaller and less likely to

cover the all project cost.

Acquiring funds from the private equity is lengthy process which ultimately leads to

delay in the targets achievement for which funds are acquired from private equity option.

The private equity may affect the business decision-making process as they are providing

and handing over their shares and part of their control (Falchetta and et.al., 2022).

this project as they unable higher profit return that the cost of acquisition.

(iii) Factors affecting investment decision

Beside return on investment, the risk is also need to be taken into consideration while

making investment related decision.

The period of investment and inflation rate is also need to be consider while making

business decision.

Further, investment volatility factor and liquidity position is also plays vital role in

identifying whether the project is profitable or not.

The change in the internal as well as external business environment is also one of the

factor that should be consider by the company before making any decision (Falchetta and

et.al., 2022).

Question 4

(a)

Advantage of Private Equity financing:

The private equity source of finance adds working capital to the business as it can

provide cash infusion that is best for supporting new and struggling business.

Another advantage of private equity is such that the valuation of private equity is not

affected by the public market and they also need not to move through high-interest loans.

The private equity financing allows more freedom for the growth of the business which

ultimately leads to higher profitability and expansion.

Disadvantages of Private Equity:

It requires upfront funding and also sometime returns are often smaller and less likely to

cover the all project cost.

Acquiring funds from the private equity is lengthy process which ultimately leads to

delay in the targets achievement for which funds are acquired from private equity option.

The private equity may affect the business decision-making process as they are providing

and handing over their shares and part of their control (Falchetta and et.al., 2022).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b)

Beside private equity, debentures is an alternative source of finance that can be adopted by

the company in order raise the funds. Financing through debt is less costly and provides tax

benefits while on the other hand, debt financing is a rigid obligation that enlarge the leverage

ratio. It is because whether the company will earn profit or not, they need to pay fixed interest to

its business. For example, Woolworths is an Australian company that raise debt capital of $607.8

million from JB Hi-Fi JBH:AU and $1.36 billion from Metcash MTS:AU (Pallathadka and et.al.,

2021).

(c)

Alpha Ltd can borrow loan at the prime rate while on the other hand, Beta Ltd, can borrow loan

at prime rate + 4. As the current prime rate is 4.75% so the respective loan of Alpha and Beta are

as follows:

Alpha respective loan rate = 4.75%

Beta respective loan rate = 4.75% + 4 = 4.0475%

(d)

The introduction of tax decreases the value of business it is because due to tax expenses,

the cost of sales of the company increases which ultimately result into the less income of the

business. Thus, it can be said that the introduction of tax should decrease the value of business.

(e) Weighted average cost of capital of Dusk Ltd.

Particulars

Amount

($ In

million) Weights

Cost of

Capital

(after

tax

rate)

Weighted

average

cost of

capital

Debt

Outstanding 25 0.625 8.51 5.31875

Equity

Outstanding 15 0.375 12.00 4.5

Beside private equity, debentures is an alternative source of finance that can be adopted by

the company in order raise the funds. Financing through debt is less costly and provides tax

benefits while on the other hand, debt financing is a rigid obligation that enlarge the leverage

ratio. It is because whether the company will earn profit or not, they need to pay fixed interest to

its business. For example, Woolworths is an Australian company that raise debt capital of $607.8

million from JB Hi-Fi JBH:AU and $1.36 billion from Metcash MTS:AU (Pallathadka and et.al.,

2021).

(c)

Alpha Ltd can borrow loan at the prime rate while on the other hand, Beta Ltd, can borrow loan

at prime rate + 4. As the current prime rate is 4.75% so the respective loan of Alpha and Beta are

as follows:

Alpha respective loan rate = 4.75%

Beta respective loan rate = 4.75% + 4 = 4.0475%

(d)

The introduction of tax decreases the value of business it is because due to tax expenses,

the cost of sales of the company increases which ultimately result into the less income of the

business. Thus, it can be said that the introduction of tax should decrease the value of business.

(e) Weighted average cost of capital of Dusk Ltd.

Particulars

Amount

($ In

million) Weights

Cost of

Capital

(after

tax

rate)

Weighted

average

cost of

capital

Debt

Outstanding 25 0.625 8.51 5.31875

Equity

Outstanding 15 0.375 12.00 4.5

40 1 9.82

Cost of debt after tax = 8.25/ (1-0.03) = 8.51%

Question 5

(a)

On the basis of above chart, it can be stated that the dividend policy adopted by

CryptoKnight Ltd under its investigation period is residual dividend policy. The residual

dividend policy state that companies pays dividend to its shareholders on the basis of amount of

profit are left over after the company has paid for its capital expenditure and working capital

costs. After analyzing the above chart regarding earning per share and dividend per share, it is

identified that the company has distributed 50% of its earning towards the shareholders in the

form of dividend (Boubaker and Nguyen, 2018). The company has employed this particular

policy in order to keep their employee satisfied and happy. Further, it is also helpful for

convincing the shareholders to reinvest the earning or returns again in the company for the future

development of the business.

(b)

Clientele Effect Theory: As per these theory, the change in distribution policy and

incorporating regular cash dividend may result into the loss of some clientele which will chose to

sell their stocks and attract new clientele who will buy stock based on the dividend preferences

(Sari, 2018). Thus, as per this theory, the company should change its dividend distribution policy

and not pay regular cash dividend as it may lead to gain of clientele who purchase stocks based

on dividend preferences.

Dividend Signalling Theory: This theory indicates that the announcement of company’s

change in distribution policy and paying regular dividend payment is an indicator of positive

future prospects. This theory also beliefs that the information available on the company’s

financial health is basically not available to all parties in a market at the same point of time. So,

as per this theory, it is advisable to IT sector of CryptoMax Ltd (Jaara, Alashhab and Jaara,

2018). That they should change its distribution policy and pay a regular cash dividend

Cost of debt after tax = 8.25/ (1-0.03) = 8.51%

Question 5

(a)

On the basis of above chart, it can be stated that the dividend policy adopted by

CryptoKnight Ltd under its investigation period is residual dividend policy. The residual

dividend policy state that companies pays dividend to its shareholders on the basis of amount of

profit are left over after the company has paid for its capital expenditure and working capital

costs. After analyzing the above chart regarding earning per share and dividend per share, it is

identified that the company has distributed 50% of its earning towards the shareholders in the

form of dividend (Boubaker and Nguyen, 2018). The company has employed this particular

policy in order to keep their employee satisfied and happy. Further, it is also helpful for

convincing the shareholders to reinvest the earning or returns again in the company for the future

development of the business.

(b)

Clientele Effect Theory: As per these theory, the change in distribution policy and

incorporating regular cash dividend may result into the loss of some clientele which will chose to

sell their stocks and attract new clientele who will buy stock based on the dividend preferences

(Sari, 2018). Thus, as per this theory, the company should change its dividend distribution policy

and not pay regular cash dividend as it may lead to gain of clientele who purchase stocks based

on dividend preferences.

Dividend Signalling Theory: This theory indicates that the announcement of company’s

change in distribution policy and paying regular dividend payment is an indicator of positive

future prospects. This theory also beliefs that the information available on the company’s

financial health is basically not available to all parties in a market at the same point of time. So,

as per this theory, it is advisable to IT sector of CryptoMax Ltd (Jaara, Alashhab and Jaara,

2018). That they should change its distribution policy and pay a regular cash dividend

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.