Finance Exam Solution: Valuation, Project Appraisal, and Production

VerifiedAdded on 2023/01/07

|14

|1668

|36

Homework Assignment

AI Summary

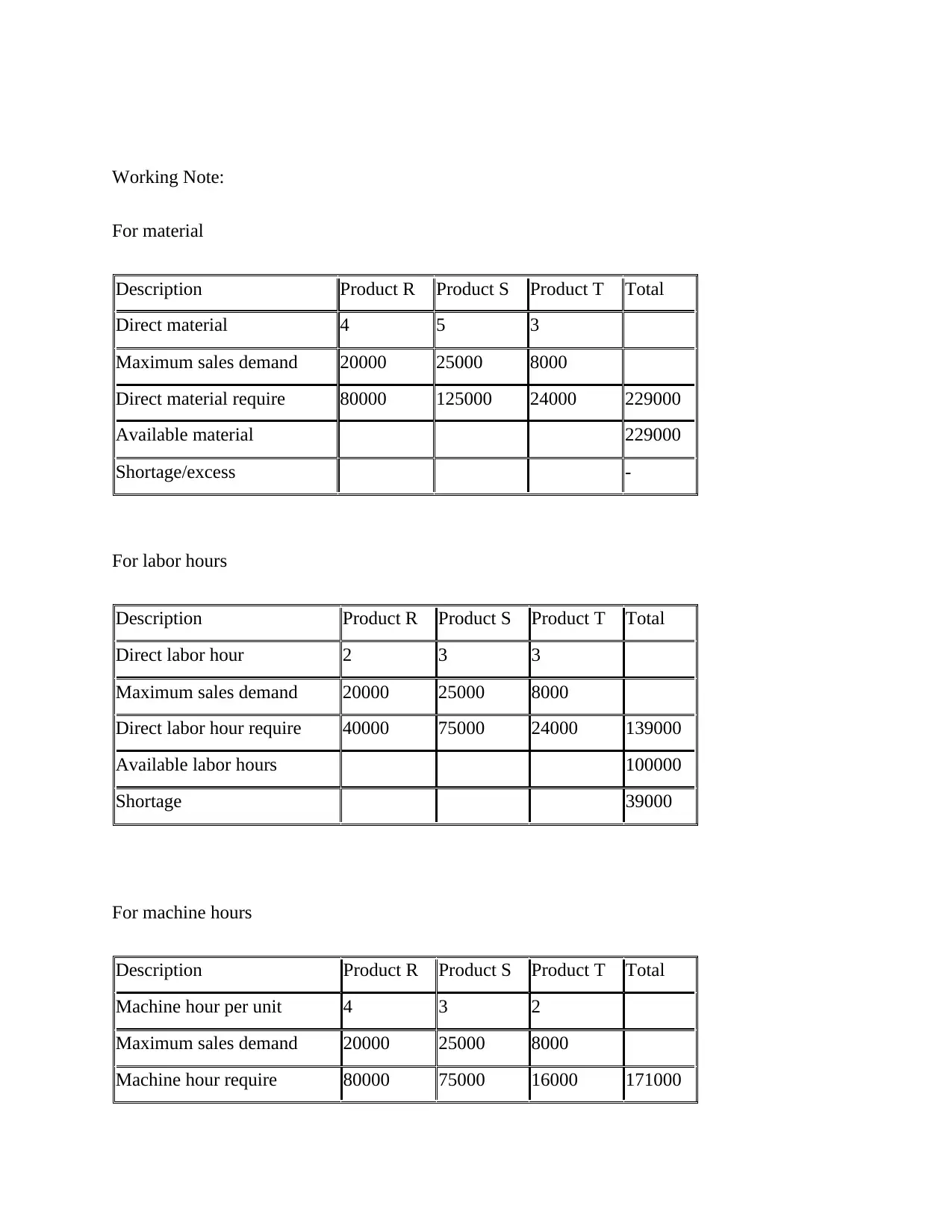

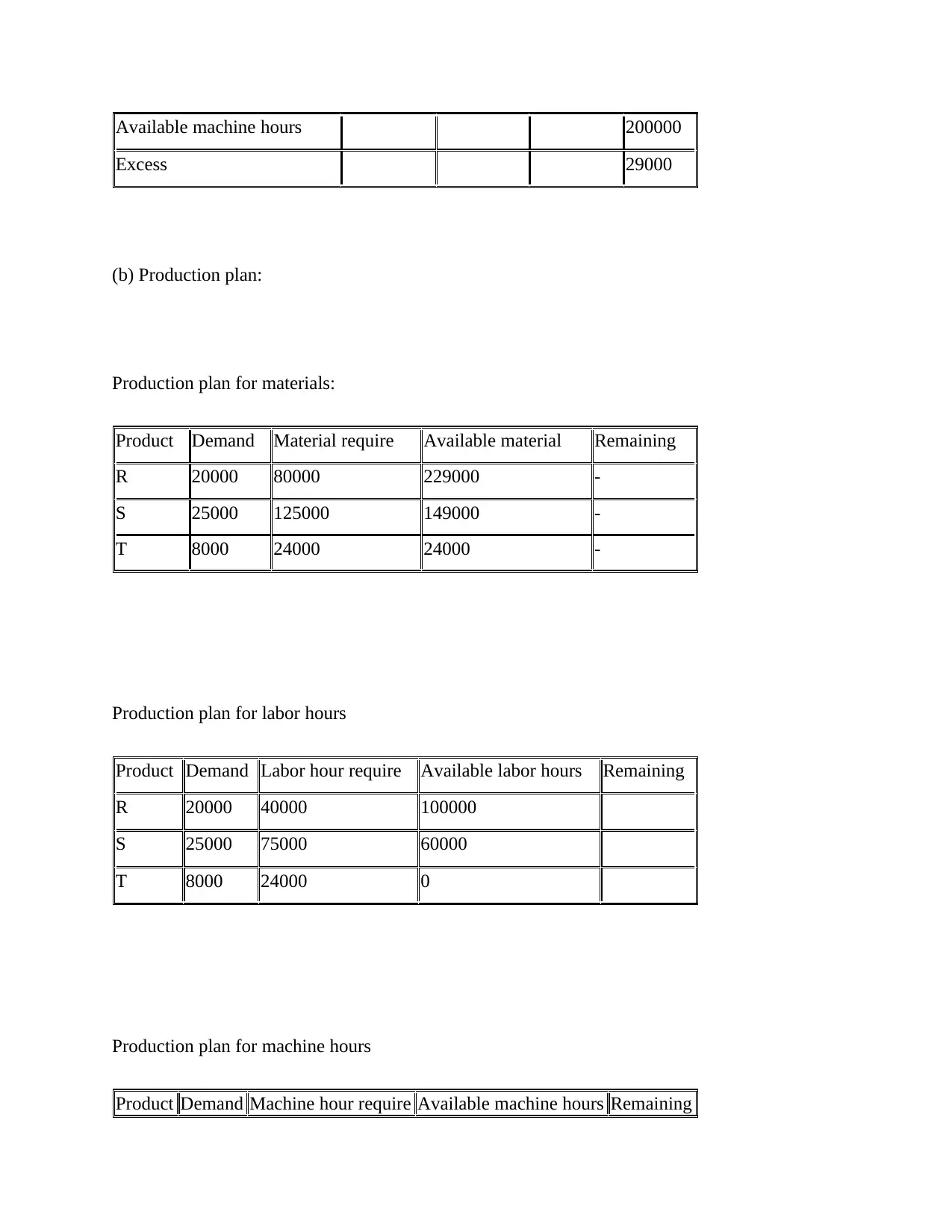

This document provides a comprehensive solution to a finance exam, addressing three key questions. The first question focuses on company valuation, utilizing the P/E ratio and the dividend growth model to estimate the value of Stellar Ltd, along with a discussion of the limitations of each method. The second question delves into project appraisal, calculating the Net Present Value (NPV) and Internal Rate of Return (IRR) for a proposed investment in new machinery by Lennon Plc, and then recommending whether the investment should proceed. The final question examines production decisions, identifying the limiting factor in production based on constraints in labor and machine hours and determining the optimal production plan to maximize contribution, followed by a breakeven point calculation for a specific product. The solution includes detailed workings, calculations, and explanations for each part of the exam.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.