Finance and Funding in TTM: Analysis and Report on Akaglo Tours

VerifiedAdded on 2020/11/23

|17

|4406

|306

Report

AI Summary

This report provides a comprehensive analysis of financial management principles and practices within the travel and tourism sector, specifically focusing on Akaglo Tours. It begins by examining the concept of Cost-Volume-Profit (CVP) analysis and its significance in financial management, followed by an assessment of various pricing methods that can be employed by the company. The report then delves into management accounting information, exploring different types and their application, along with an evaluation of investment appraisal techniques as decision-making tools. Furthermore, it includes an interpretation of financial statements through ratio analysis, providing insights into the company's performance. Finally, the report assesses various funding sources that Akaglo Tours could utilize for developing new hotels or expanding its operations. The report covers financial planning, analysis, and strategic decision-making within the context of a travel company.

Finance and Funding in TTM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a. Examining the concept of CVP analysis and assessing its importance in financial

management.................................................................................................................................3

b. Presenting pricing methods which can be used by Akaglo Tours company...........................5

TASK 2............................................................................................................................................7

a. Explaining different types of management accounting information which can be used by

ATC.............................................................................................................................................7

b. Assessing the use of investment appraisal techniques as a decision making tool...................8

TASK 3..........................................................................................................................................10

a. Interpreting financial statements of TUI travel through ratio analysis..................................10

TASK 4..........................................................................................................................................14

a. Assessing funding sources which can be undertaken by the company for developing new

hotel...........................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a. Examining the concept of CVP analysis and assessing its importance in financial

management.................................................................................................................................3

b. Presenting pricing methods which can be used by Akaglo Tours company...........................5

TASK 2............................................................................................................................................7

a. Explaining different types of management accounting information which can be used by

ATC.............................................................................................................................................7

b. Assessing the use of investment appraisal techniques as a decision making tool...................8

TASK 3..........................................................................................................................................10

a. Interpreting financial statements of TUI travel through ratio analysis..................................10

TASK 4..........................................................................................................................................14

a. Assessing funding sources which can be undertaken by the company for developing new

hotel...........................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

In the current times, travel and tourism sector is growing with the very high pace. Now,

with the motive to make the vacations memorable individuals prefer to contract travel companies

which in turn provides them with attractive tour packages. In UK, there are several companies

which involved in planning specific packages as per the wants and expectation of customers. The

present report is based on Akaglo Tours Company which is planning to offer excusive summer

holiday trips to the customers. In this, report will provide deeper insight about the aspects of

financial management. Besides this, it also depicts the manner through which prices of the travel

packages can be determined by ATC. Report also entails how investment appraisal tools and

techniques aid in decision making aspects. Further, it also highlights the extent to which

profitability, liquidity and solvency position of the company is good. In this, internal and

external funding sources will also be described which firm can use for the new establishment.

TASK 1

a. Examining the concept of CVP analysis and assessing its importance in financial management

In the context of ATC, cost, volume and profit assessment is highly significant which

makes vital contribution in the aspect of financial management.

Cost: It implies for the sum of expenses incurred by the firm for offering travel packages

to the customers. Hence, ATC can distinguish expenses in terms of fixed, and variable and

thereby would become able to determine overall cost level.

Fixed cost: Expenses which are not affected from the number of units produced or

offered considered as fixed cost (Bulgurcu, 2012). Main examples of fixed cost in the context of

ATC include salaries of personnel etc.

Variable cost: Unlike fixed, variable cost affects from the number of units produced or

services offered to the customers. Hence, according to the units variable costs are affected to a

great extent. Variable expenses include insurance, electricity expenses etc.

Total cost: Fixed + Variable

In the current times, travel and tourism sector is growing with the very high pace. Now,

with the motive to make the vacations memorable individuals prefer to contract travel companies

which in turn provides them with attractive tour packages. In UK, there are several companies

which involved in planning specific packages as per the wants and expectation of customers. The

present report is based on Akaglo Tours Company which is planning to offer excusive summer

holiday trips to the customers. In this, report will provide deeper insight about the aspects of

financial management. Besides this, it also depicts the manner through which prices of the travel

packages can be determined by ATC. Report also entails how investment appraisal tools and

techniques aid in decision making aspects. Further, it also highlights the extent to which

profitability, liquidity and solvency position of the company is good. In this, internal and

external funding sources will also be described which firm can use for the new establishment.

TASK 1

a. Examining the concept of CVP analysis and assessing its importance in financial management

In the context of ATC, cost, volume and profit assessment is highly significant which

makes vital contribution in the aspect of financial management.

Cost: It implies for the sum of expenses incurred by the firm for offering travel packages

to the customers. Hence, ATC can distinguish expenses in terms of fixed, and variable and

thereby would become able to determine overall cost level.

Fixed cost: Expenses which are not affected from the number of units produced or

offered considered as fixed cost (Bulgurcu, 2012). Main examples of fixed cost in the context of

ATC include salaries of personnel etc.

Variable cost: Unlike fixed, variable cost affects from the number of units produced or

services offered to the customers. Hence, according to the units variable costs are affected to a

great extent. Variable expenses include insurance, electricity expenses etc.

Total cost: Fixed + Variable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: Variable cost, 2018)

Volume: It has assessed from evaluation that volume plays a vital role in financial

management. Moreover, when firm offers services to the large number of customers then it gets

high economies of scale (Hall and Page, 2014). In this, by doing BEP analysis, ATC can assess

the number of customers which it needs to serve for attaining the situation of no profit no loss

BEP Graph

`

(Source: Break-even point analysis, 2018)

Profit: High volume and low cost positively contributes in the profit margin generated

by the firm. High economies of scale offer cost advantages to the firm and thereby enhances

profit level. In addition to this, using BEP tool business entity of ATC can identify the number of

tourists to whom travel packages need to be offered for getting the desired level of profit margin.

Volume: It has assessed from evaluation that volume plays a vital role in financial

management. Moreover, when firm offers services to the large number of customers then it gets

high economies of scale (Hall and Page, 2014). In this, by doing BEP analysis, ATC can assess

the number of customers which it needs to serve for attaining the situation of no profit no loss

BEP Graph

`

(Source: Break-even point analysis, 2018)

Profit: High volume and low cost positively contributes in the profit margin generated

by the firm. High economies of scale offer cost advantages to the firm and thereby enhances

profit level. In addition to this, using BEP tool business entity of ATC can identify the number of

tourists to whom travel packages need to be offered for getting the desired level of profit margin.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

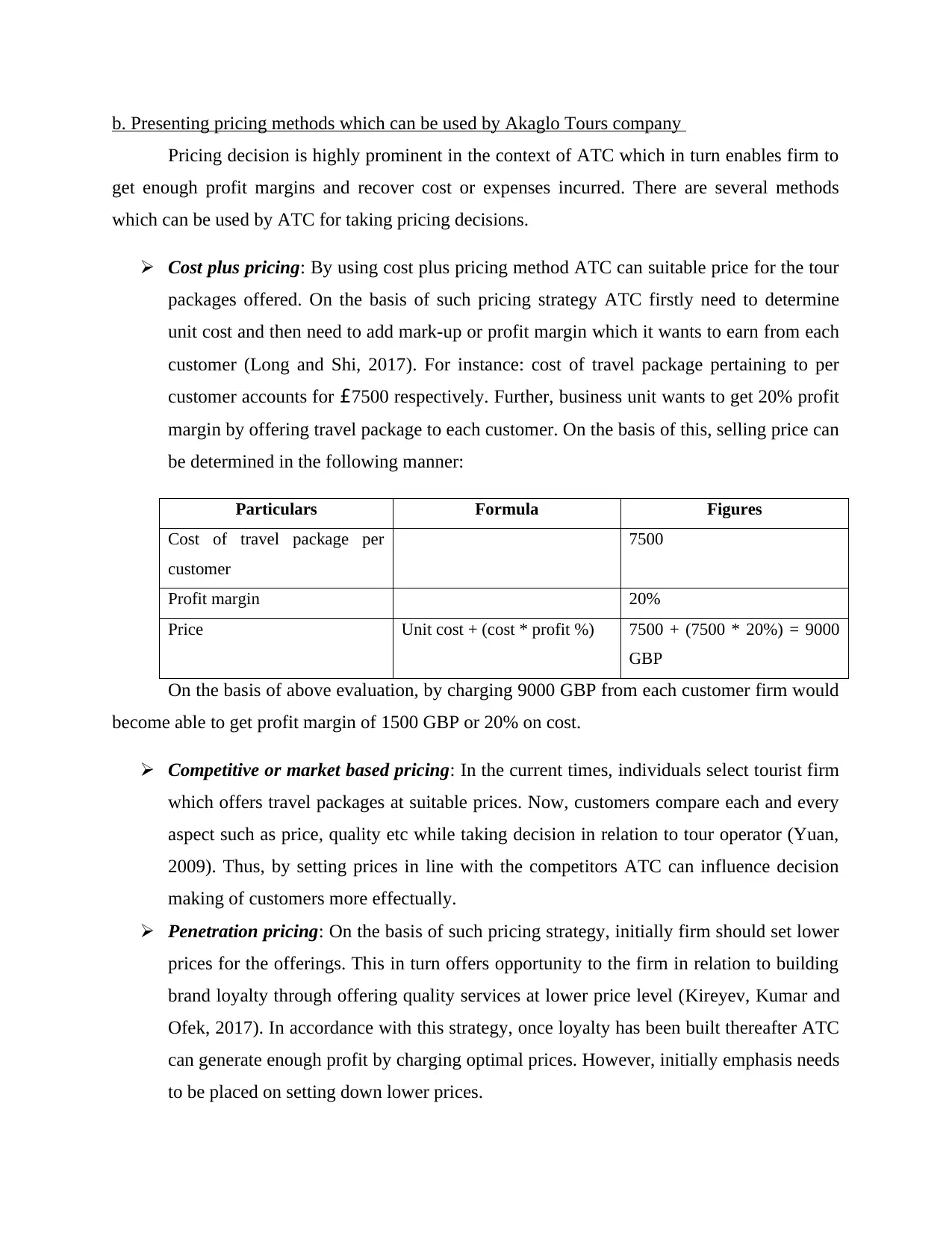

b. Presenting pricing methods which can be used by Akaglo Tours company

Pricing decision is highly prominent in the context of ATC which in turn enables firm to

get enough profit margins and recover cost or expenses incurred. There are several methods

which can be used by ATC for taking pricing decisions.

Cost plus pricing: By using cost plus pricing method ATC can suitable price for the tour

packages offered. On the basis of such pricing strategy ATC firstly need to determine

unit cost and then need to add mark-up or profit margin which it wants to earn from each

customer (Long and Shi, 2017). For instance: cost of travel package pertaining to per

customer accounts for £7500 respectively. Further, business unit wants to get 20% profit

margin by offering travel package to each customer. On the basis of this, selling price can

be determined in the following manner:

Particulars Formula Figures

Cost of travel package per

customer

7500

Profit margin 20%

Price Unit cost + (cost * profit %) 7500 + (7500 * 20%) = 9000

GBP

On the basis of above evaluation, by charging 9000 GBP from each customer firm would

become able to get profit margin of 1500 GBP or 20% on cost.

Competitive or market based pricing: In the current times, individuals select tourist firm

which offers travel packages at suitable prices. Now, customers compare each and every

aspect such as price, quality etc while taking decision in relation to tour operator (Yuan,

2009). Thus, by setting prices in line with the competitors ATC can influence decision

making of customers more effectually.

Penetration pricing: On the basis of such pricing strategy, initially firm should set lower

prices for the offerings. This in turn offers opportunity to the firm in relation to building

brand loyalty through offering quality services at lower price level (Kireyev, Kumar and

Ofek, 2017). In accordance with this strategy, once loyalty has been built thereafter ATC

can generate enough profit by charging optimal prices. However, initially emphasis needs

to be placed on setting down lower prices.

Pricing decision is highly prominent in the context of ATC which in turn enables firm to

get enough profit margins and recover cost or expenses incurred. There are several methods

which can be used by ATC for taking pricing decisions.

Cost plus pricing: By using cost plus pricing method ATC can suitable price for the tour

packages offered. On the basis of such pricing strategy ATC firstly need to determine

unit cost and then need to add mark-up or profit margin which it wants to earn from each

customer (Long and Shi, 2017). For instance: cost of travel package pertaining to per

customer accounts for £7500 respectively. Further, business unit wants to get 20% profit

margin by offering travel package to each customer. On the basis of this, selling price can

be determined in the following manner:

Particulars Formula Figures

Cost of travel package per

customer

7500

Profit margin 20%

Price Unit cost + (cost * profit %) 7500 + (7500 * 20%) = 9000

GBP

On the basis of above evaluation, by charging 9000 GBP from each customer firm would

become able to get profit margin of 1500 GBP or 20% on cost.

Competitive or market based pricing: In the current times, individuals select tourist firm

which offers travel packages at suitable prices. Now, customers compare each and every

aspect such as price, quality etc while taking decision in relation to tour operator (Yuan,

2009). Thus, by setting prices in line with the competitors ATC can influence decision

making of customers more effectually.

Penetration pricing: On the basis of such pricing strategy, initially firm should set lower

prices for the offerings. This in turn offers opportunity to the firm in relation to building

brand loyalty through offering quality services at lower price level (Kireyev, Kumar and

Ofek, 2017). In accordance with this strategy, once loyalty has been built thereafter ATC

can generate enough profit by charging optimal prices. However, initially emphasis needs

to be placed on setting down lower prices.

c. Analyzing factors which have an impact profit margin of ATC

In travel & tourism sector, there are numerous factors which closely influence profit

margin of business units including ATC such as:

Seasonal variations: Individuals prefer to visit different places during holidays and

specific season when weather is pleasant. Hence, seasonality trends or variations highly

impact growth and firm’s profitability. During non-peak season for enticing sales firm

make focus on offering special discounts to the customers. Thus, discounting aspects

influence profitability.

Changing trends and customers preferences: Through evaluation, it has identified that

now taste and preferences of customers are changing with the very high pace. Now,

visitors prefer to deal with the firm which provide them with attractive tour packages and

make their holidays memorable (Bekaert and Hodrick, 2017). Hence, non-compliance

with the changing trends has significant impact on the customer’s decision making and

thereby sales as well as margin of firm.

Bad debt: In ATC, level of bad debt has influence on organizational profitability. For

enhancing sales ATC focuses on offering travel packages to other institutions or firm on

credit basis. Hence, default which is made by the debtors in repayment has an impact on

organizational profit margin.

Lack of effective planning and competent staff: Competent planning is the key of

organizational growth and success. In the case of ineffective planning ATC would not

become able to make optimum use of financial resources and thereby get profit margin.

In the service sector, skills and abilities of personnel have greater impact on the

satisfaction level of customers (Drehmann and Nikolaou, 2013). Hence, profitability of

ATC will be affected negatively in the case of having less skilled as well as competent

staff.

D1

Particulars Figures (in £)

Fixed cost 500000

Desired profit margin 100000

In travel & tourism sector, there are numerous factors which closely influence profit

margin of business units including ATC such as:

Seasonal variations: Individuals prefer to visit different places during holidays and

specific season when weather is pleasant. Hence, seasonality trends or variations highly

impact growth and firm’s profitability. During non-peak season for enticing sales firm

make focus on offering special discounts to the customers. Thus, discounting aspects

influence profitability.

Changing trends and customers preferences: Through evaluation, it has identified that

now taste and preferences of customers are changing with the very high pace. Now,

visitors prefer to deal with the firm which provide them with attractive tour packages and

make their holidays memorable (Bekaert and Hodrick, 2017). Hence, non-compliance

with the changing trends has significant impact on the customer’s decision making and

thereby sales as well as margin of firm.

Bad debt: In ATC, level of bad debt has influence on organizational profitability. For

enhancing sales ATC focuses on offering travel packages to other institutions or firm on

credit basis. Hence, default which is made by the debtors in repayment has an impact on

organizational profit margin.

Lack of effective planning and competent staff: Competent planning is the key of

organizational growth and success. In the case of ineffective planning ATC would not

become able to make optimum use of financial resources and thereby get profit margin.

In the service sector, skills and abilities of personnel have greater impact on the

satisfaction level of customers (Drehmann and Nikolaou, 2013). Hence, profitability of

ATC will be affected negatively in the case of having less skilled as well as competent

staff.

D1

Particulars Figures (in £)

Fixed cost 500000

Desired profit margin 100000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

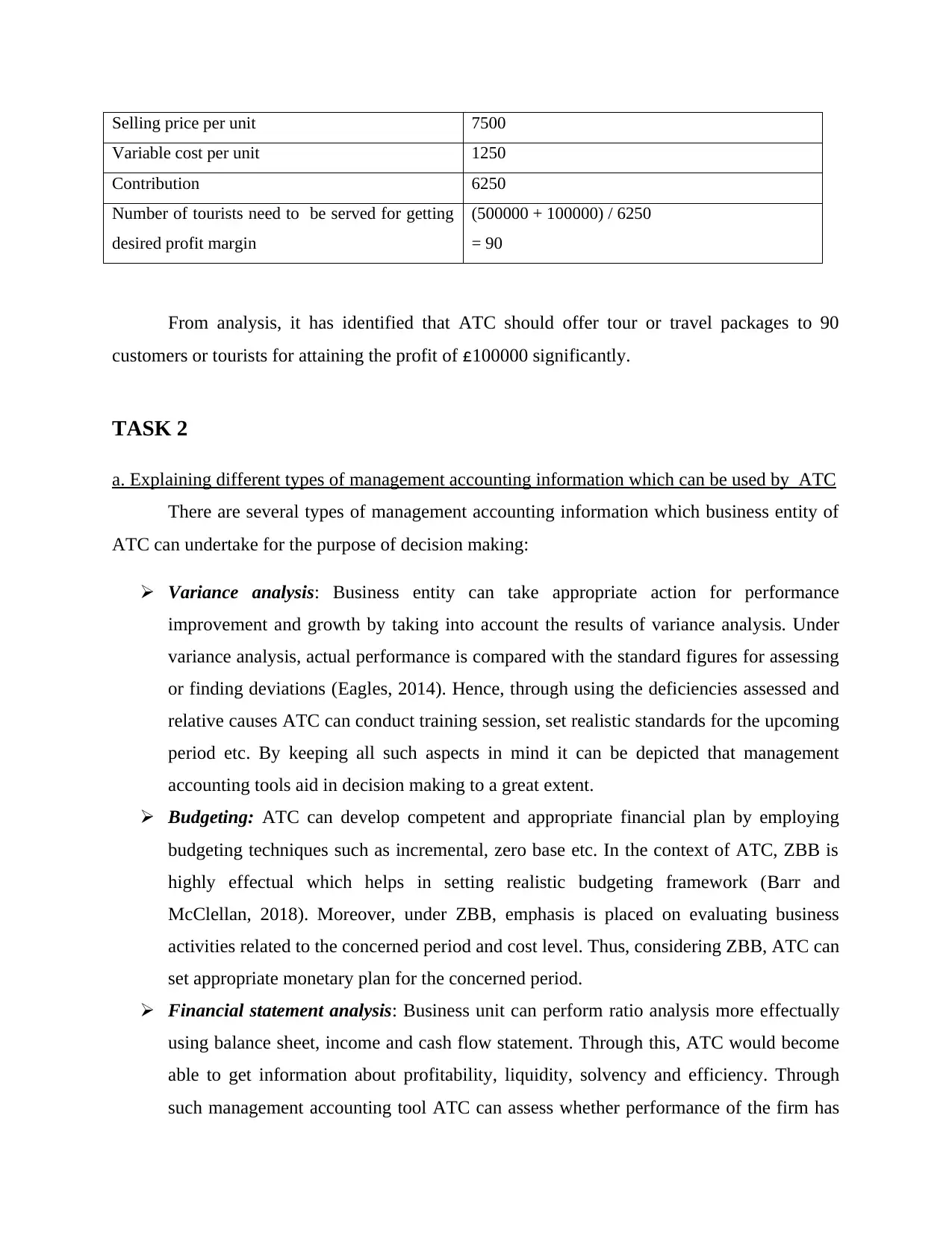

Selling price per unit 7500

Variable cost per unit 1250

Contribution 6250

Number of tourists need to be served for getting

desired profit margin

(500000 + 100000) / 6250

= 90

From analysis, it has identified that ATC should offer tour or travel packages to 90

customers or tourists for attaining the profit of £100000 significantly.

TASK 2

a. Explaining different types of management accounting information which can be used by ATC

There are several types of management accounting information which business entity of

ATC can undertake for the purpose of decision making:

Variance analysis: Business entity can take appropriate action for performance

improvement and growth by taking into account the results of variance analysis. Under

variance analysis, actual performance is compared with the standard figures for assessing

or finding deviations (Eagles, 2014). Hence, through using the deficiencies assessed and

relative causes ATC can conduct training session, set realistic standards for the upcoming

period etc. By keeping all such aspects in mind it can be depicted that management

accounting tools aid in decision making to a great extent.

Budgeting: ATC can develop competent and appropriate financial plan by employing

budgeting techniques such as incremental, zero base etc. In the context of ATC, ZBB is

highly effectual which helps in setting realistic budgeting framework (Barr and

McClellan, 2018). Moreover, under ZBB, emphasis is placed on evaluating business

activities related to the concerned period and cost level. Thus, considering ZBB, ATC can

set appropriate monetary plan for the concerned period.

Financial statement analysis: Business unit can perform ratio analysis more effectually

using balance sheet, income and cash flow statement. Through this, ATC would become

able to get information about profitability, liquidity, solvency and efficiency. Through

such management accounting tool ATC can assess whether performance of the firm has

Variable cost per unit 1250

Contribution 6250

Number of tourists need to be served for getting

desired profit margin

(500000 + 100000) / 6250

= 90

From analysis, it has identified that ATC should offer tour or travel packages to 90

customers or tourists for attaining the profit of £100000 significantly.

TASK 2

a. Explaining different types of management accounting information which can be used by ATC

There are several types of management accounting information which business entity of

ATC can undertake for the purpose of decision making:

Variance analysis: Business entity can take appropriate action for performance

improvement and growth by taking into account the results of variance analysis. Under

variance analysis, actual performance is compared with the standard figures for assessing

or finding deviations (Eagles, 2014). Hence, through using the deficiencies assessed and

relative causes ATC can conduct training session, set realistic standards for the upcoming

period etc. By keeping all such aspects in mind it can be depicted that management

accounting tools aid in decision making to a great extent.

Budgeting: ATC can develop competent and appropriate financial plan by employing

budgeting techniques such as incremental, zero base etc. In the context of ATC, ZBB is

highly effectual which helps in setting realistic budgeting framework (Barr and

McClellan, 2018). Moreover, under ZBB, emphasis is placed on evaluating business

activities related to the concerned period and cost level. Thus, considering ZBB, ATC can

set appropriate monetary plan for the concerned period.

Financial statement analysis: Business unit can perform ratio analysis more effectually

using balance sheet, income and cash flow statement. Through this, ATC would become

able to get information about profitability, liquidity, solvency and efficiency. Through

such management accounting tool ATC can assess whether performance of the firm has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

improved or deteriorated over the time frame. Hence, through analyzing financial

statements and thereby performance ATC can develop sound strategic & policy

framework which makes contribution in the organizational growth.

b. Assessing the use of investment appraisal techniques as a decision making tool

On the basis of given case scenario, ATC wants to improve decision making aspects by

taking into account or employing modern management accounting techniques. Hence,

investment appraisal techniques of management accounting are highly effectual which helps in

evaluating the viability of proposal in monetary terms. Tools of investment appraisal includes

payback, net present value and internal rate of return which helps in assessing whether long term

capital project will aid in the growth of business unit or not.

Payback method of investment appraisal helps in ascertaining time period within which

firm will recoup initial investment. In other words, payback assists in assessing time after which

firm will start making profit (Fraser, Bhaumik and Wright, 2015). However, on the critical note,

it can be stated that payback method avoids time value of money concept which in turn affects its

significance level. Under this, while taking decision business unit should give priority to the

project has less payback period.

Further, NPV method clearly entails return in the monetary form which ATC will

generate over the time frame and initial investment. Such method of investment appraisal has

high level of importance in the modern era as it presents solution considering time value of

money concept. In accordance with this, firm should select and invest money in the project

which offers higher NPV.

Internal rate of return method comes under discounting tools, which helps in identifying

profitability in terms of percentage. On the critical note, it can be presented IRR and NPV tool

does not help in comparing two mutually exclusive projects (Higgins, 2012). Hence, using

investment appraisal tools ATC can select most profitable proposal out of two or more.

For instance: ATC has two investment proposals with the similar initial investment such as

£200000

Payback period

statements and thereby performance ATC can develop sound strategic & policy

framework which makes contribution in the organizational growth.

b. Assessing the use of investment appraisal techniques as a decision making tool

On the basis of given case scenario, ATC wants to improve decision making aspects by

taking into account or employing modern management accounting techniques. Hence,

investment appraisal techniques of management accounting are highly effectual which helps in

evaluating the viability of proposal in monetary terms. Tools of investment appraisal includes

payback, net present value and internal rate of return which helps in assessing whether long term

capital project will aid in the growth of business unit or not.

Payback method of investment appraisal helps in ascertaining time period within which

firm will recoup initial investment. In other words, payback assists in assessing time after which

firm will start making profit (Fraser, Bhaumik and Wright, 2015). However, on the critical note,

it can be stated that payback method avoids time value of money concept which in turn affects its

significance level. Under this, while taking decision business unit should give priority to the

project has less payback period.

Further, NPV method clearly entails return in the monetary form which ATC will

generate over the time frame and initial investment. Such method of investment appraisal has

high level of importance in the modern era as it presents solution considering time value of

money concept. In accordance with this, firm should select and invest money in the project

which offers higher NPV.

Internal rate of return method comes under discounting tools, which helps in identifying

profitability in terms of percentage. On the critical note, it can be presented IRR and NPV tool

does not help in comparing two mutually exclusive projects (Higgins, 2012). Hence, using

investment appraisal tools ATC can select most profitable proposal out of two or more.

For instance: ATC has two investment proposals with the similar initial investment such as

£200000

Payback period

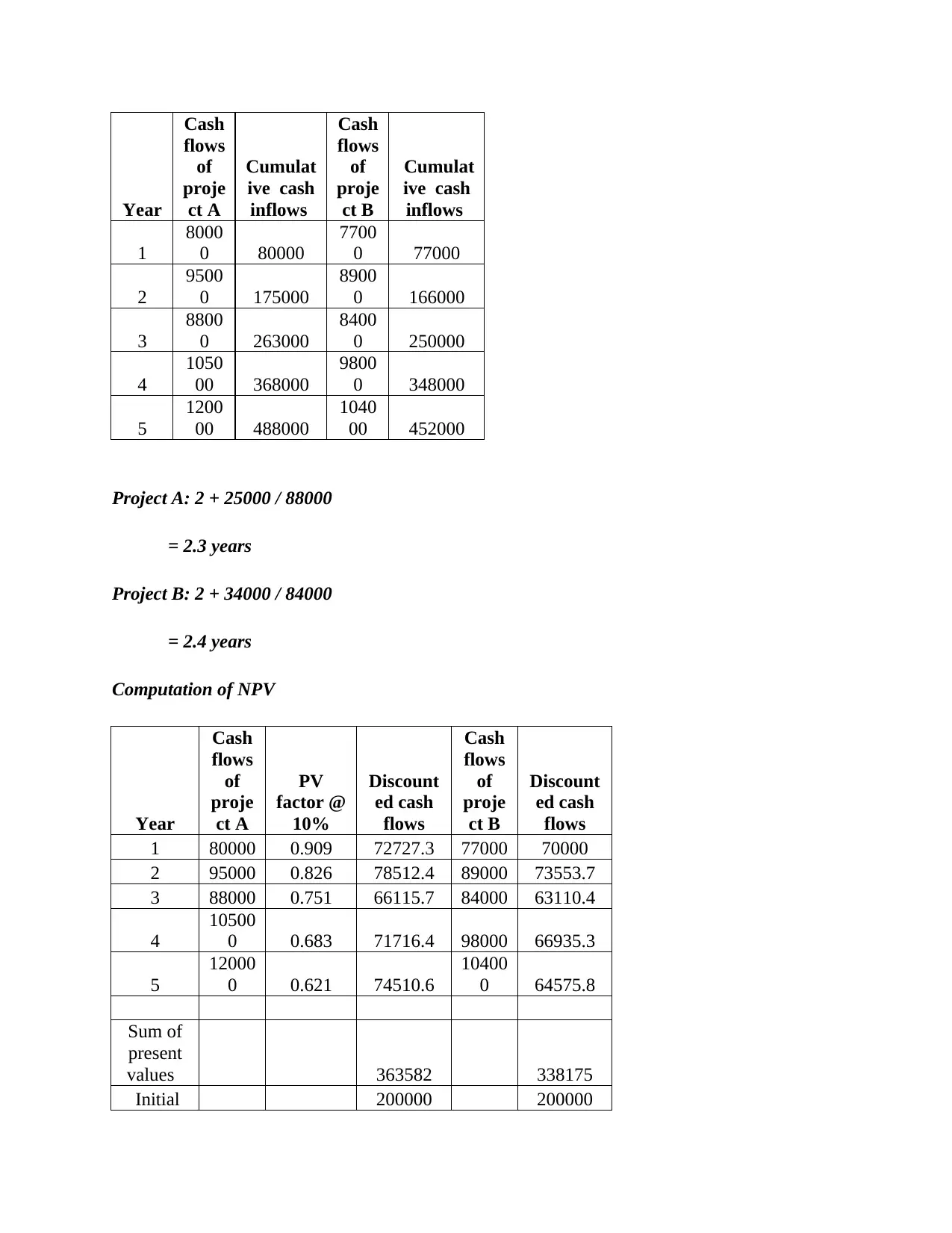

Year

Cash

flows

of

proje

ct A

Cumulat

ive cash

inflows

Cash

flows

of

proje

ct B

Cumulat

ive cash

inflows

1

8000

0 80000

7700

0 77000

2

9500

0 175000

8900

0 166000

3

8800

0 263000

8400

0 250000

4

1050

00 368000

9800

0 348000

5

1200

00 488000

1040

00 452000

Project A: 2 + 25000 / 88000

= 2.3 years

Project B: 2 + 34000 / 84000

= 2.4 years

Computation of NPV

Year

Cash

flows

of

proje

ct A

PV

factor @

10%

Discount

ed cash

flows

Cash

flows

of

proje

ct B

Discount

ed cash

flows

1 80000 0.909 72727.3 77000 70000

2 95000 0.826 78512.4 89000 73553.7

3 88000 0.751 66115.7 84000 63110.4

4

10500

0 0.683 71716.4 98000 66935.3

5

12000

0 0.621 74510.6

10400

0 64575.8

Sum of

present

values 363582 338175

Initial 200000 200000

Cash

flows

of

proje

ct A

Cumulat

ive cash

inflows

Cash

flows

of

proje

ct B

Cumulat

ive cash

inflows

1

8000

0 80000

7700

0 77000

2

9500

0 175000

8900

0 166000

3

8800

0 263000

8400

0 250000

4

1050

00 368000

9800

0 348000

5

1200

00 488000

1040

00 452000

Project A: 2 + 25000 / 88000

= 2.3 years

Project B: 2 + 34000 / 84000

= 2.4 years

Computation of NPV

Year

Cash

flows

of

proje

ct A

PV

factor @

10%

Discount

ed cash

flows

Cash

flows

of

proje

ct B

Discount

ed cash

flows

1 80000 0.909 72727.3 77000 70000

2 95000 0.826 78512.4 89000 73553.7

3 88000 0.751 66115.7 84000 63110.4

4

10500

0 0.683 71716.4 98000 66935.3

5

12000

0 0.621 74510.6

10400

0 64575.8

Sum of

present

values 363582 338175

Initial 200000 200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investme

nt

Net

present

value 163582 138175

Computation of IRR

Year Cash flows of project A Cash flows of project B

0 -200000 -200000

1 80000 77000

2 95000 89000

3 88000 84000

4 105000 98000

5 120000 104000

IRR 36% 33%

Outcome of investment appraisal presents that ATC will get high profit margin by

investing money in project A over B. Moreover, payback period of proposal is less in

comparison to B. Hence, in the case of project A business unit will start to get profit one month

earlier in against to B. Furthermore, NPV and IRR of project A are higher as compared to B.

Thus, by investing money in proposal A, ATC becomes able to get high profit margin over

others. This aspect clearly shows that investment appraisal tools help in taking profitable

decisions.

TASK 3

a. Interpreting financial statements of TUI travel through ratio analysis

Ratio analysis implies for the financial tool which helps in summarizing and evaluating

financial performance from several perspectives such as profitability, liquidity, efficiency as well

as investment (Financial ratio analysis, 2018). In this, for assessing the extent to which financial

position of TUI Group, a leading travel & tourism group, is good ratio analysis has been done.

nt

Net

present

value 163582 138175

Computation of IRR

Year Cash flows of project A Cash flows of project B

0 -200000 -200000

1 80000 77000

2 95000 89000

3 88000 84000

4 105000 98000

5 120000 104000

IRR 36% 33%

Outcome of investment appraisal presents that ATC will get high profit margin by

investing money in project A over B. Moreover, payback period of proposal is less in

comparison to B. Hence, in the case of project A business unit will start to get profit one month

earlier in against to B. Furthermore, NPV and IRR of project A are higher as compared to B.

Thus, by investing money in proposal A, ATC becomes able to get high profit margin over

others. This aspect clearly shows that investment appraisal tools help in taking profitable

decisions.

TASK 3

a. Interpreting financial statements of TUI travel through ratio analysis

Ratio analysis implies for the financial tool which helps in summarizing and evaluating

financial performance from several perspectives such as profitability, liquidity, efficiency as well

as investment (Financial ratio analysis, 2018). In this, for assessing the extent to which financial

position of TUI Group, a leading travel & tourism group, is good ratio analysis has been done.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

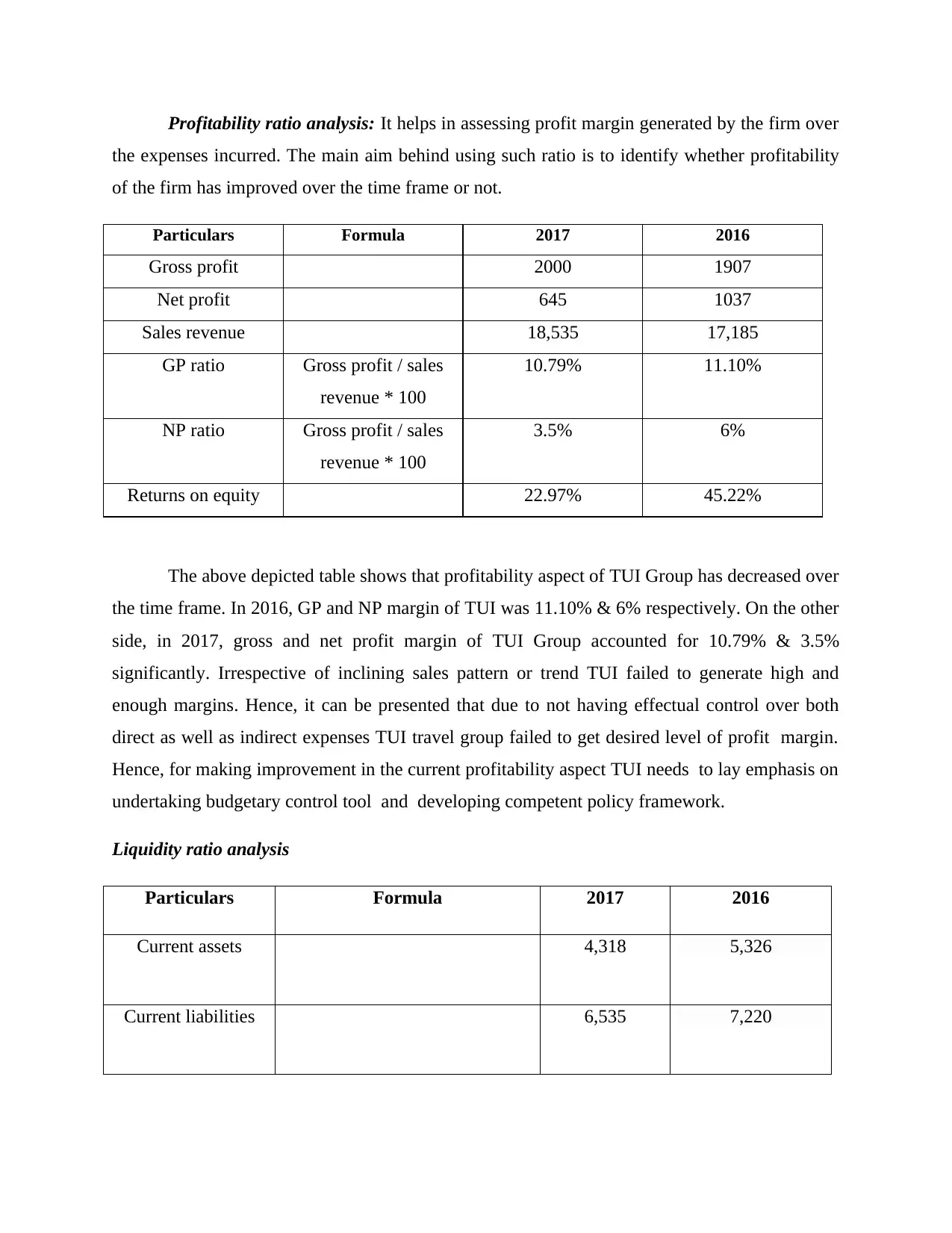

Profitability ratio analysis: It helps in assessing profit margin generated by the firm over

the expenses incurred. The main aim behind using such ratio is to identify whether profitability

of the firm has improved over the time frame or not.

Particulars Formula 2017 2016

Gross profit 2000 1907

Net profit 645 1037

Sales revenue 18,535 17,185

GP ratio Gross profit / sales

revenue * 100

10.79% 11.10%

NP ratio Gross profit / sales

revenue * 100

3.5% 6%

Returns on equity 22.97% 45.22%

The above depicted table shows that profitability aspect of TUI Group has decreased over

the time frame. In 2016, GP and NP margin of TUI was 11.10% & 6% respectively. On the other

side, in 2017, gross and net profit margin of TUI Group accounted for 10.79% & 3.5%

significantly. Irrespective of inclining sales pattern or trend TUI failed to generate high and

enough margins. Hence, it can be presented that due to not having effectual control over both

direct as well as indirect expenses TUI travel group failed to get desired level of profit margin.

Hence, for making improvement in the current profitability aspect TUI needs to lay emphasis on

undertaking budgetary control tool and developing competent policy framework.

Liquidity ratio analysis

Particulars Formula 2017 2016

Current assets 4,318 5,326

Current liabilities 6,535 7,220

the expenses incurred. The main aim behind using such ratio is to identify whether profitability

of the firm has improved over the time frame or not.

Particulars Formula 2017 2016

Gross profit 2000 1907

Net profit 645 1037

Sales revenue 18,535 17,185

GP ratio Gross profit / sales

revenue * 100

10.79% 11.10%

NP ratio Gross profit / sales

revenue * 100

3.5% 6%

Returns on equity 22.97% 45.22%

The above depicted table shows that profitability aspect of TUI Group has decreased over

the time frame. In 2016, GP and NP margin of TUI was 11.10% & 6% respectively. On the other

side, in 2017, gross and net profit margin of TUI Group accounted for 10.79% & 3.5%

significantly. Irrespective of inclining sales pattern or trend TUI failed to generate high and

enough margins. Hence, it can be presented that due to not having effectual control over both

direct as well as indirect expenses TUI travel group failed to get desired level of profit margin.

Hence, for making improvement in the current profitability aspect TUI needs to lay emphasis on

undertaking budgetary control tool and developing competent policy framework.

Liquidity ratio analysis

Particulars Formula 2017 2016

Current assets 4,318 5,326

Current liabilities 6,535 7,220

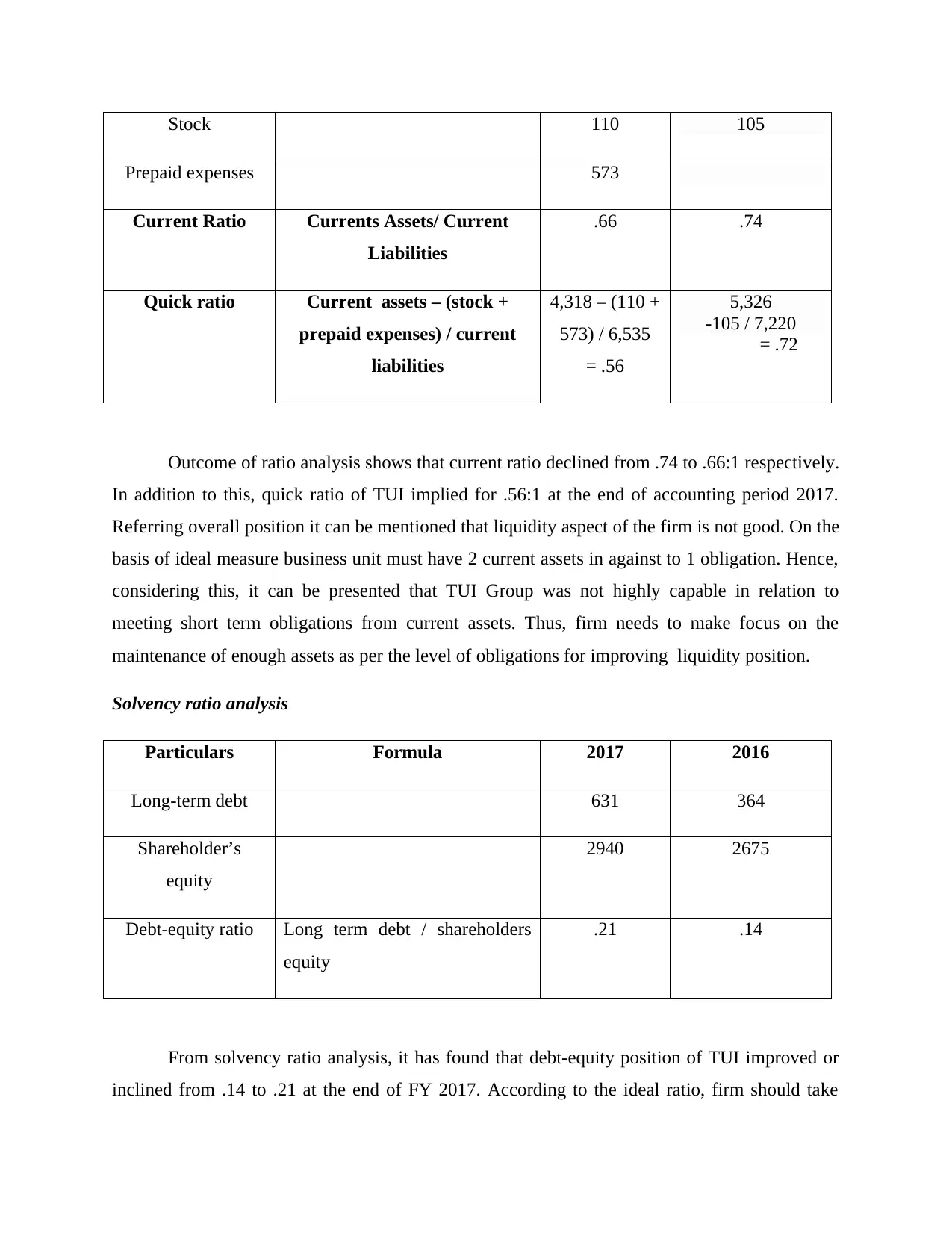

Stock 110 105

Prepaid expenses 573

Current Ratio Currents Assets/ Current

Liabilities

.66 .74

Quick ratio Current assets – (stock +

prepaid expenses) / current

liabilities

4,318 – (110 +

573) / 6,535

= .56

5,326

-105 / 7,220

= .72

Outcome of ratio analysis shows that current ratio declined from .74 to .66:1 respectively.

In addition to this, quick ratio of TUI implied for .56:1 at the end of accounting period 2017.

Referring overall position it can be mentioned that liquidity aspect of the firm is not good. On the

basis of ideal measure business unit must have 2 current assets in against to 1 obligation. Hence,

considering this, it can be presented that TUI Group was not highly capable in relation to

meeting short term obligations from current assets. Thus, firm needs to make focus on the

maintenance of enough assets as per the level of obligations for improving liquidity position.

Solvency ratio analysis

Particulars Formula 2017 2016

Long-term debt 631 364

Shareholder’s

equity

2940 2675

Debt-equity ratio Long term debt / shareholders

equity

.21 .14

From solvency ratio analysis, it has found that debt-equity position of TUI improved or

inclined from .14 to .21 at the end of FY 2017. According to the ideal ratio, firm should take

Prepaid expenses 573

Current Ratio Currents Assets/ Current

Liabilities

.66 .74

Quick ratio Current assets – (stock +

prepaid expenses) / current

liabilities

4,318 – (110 +

573) / 6,535

= .56

5,326

-105 / 7,220

= .72

Outcome of ratio analysis shows that current ratio declined from .74 to .66:1 respectively.

In addition to this, quick ratio of TUI implied for .56:1 at the end of accounting period 2017.

Referring overall position it can be mentioned that liquidity aspect of the firm is not good. On the

basis of ideal measure business unit must have 2 current assets in against to 1 obligation. Hence,

considering this, it can be presented that TUI Group was not highly capable in relation to

meeting short term obligations from current assets. Thus, firm needs to make focus on the

maintenance of enough assets as per the level of obligations for improving liquidity position.

Solvency ratio analysis

Particulars Formula 2017 2016

Long-term debt 631 364

Shareholder’s

equity

2940 2675

Debt-equity ratio Long term debt / shareholders

equity

.21 .14

From solvency ratio analysis, it has found that debt-equity position of TUI improved or

inclined from .14 to .21 at the end of FY 2017. According to the ideal ratio, firm should take

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.