Financial Analysis: Sources & Distribution of Funds in Tourism

VerifiedAdded on 2024/04/24

|40

|6021

|127

Report

AI Summary

This report provides an analysis of finance and funding within the travel and tourism sector, emphasizing the importance of cost, volume, and profit (CVP) analysis for management decision-making. It explores various pricing methods used in the industry, factors influencing profitability, and different types of management accounting information (MAI) with a case study of Dalata Hotel Group plc. The report interprets the financial accounts of Dalata Hotel Group plc for the year ended 2016, assessing their performance over two years, and analyzes sources and distribution of funding for capital projects associated with tourism development. The document highlights the significance of cost behavior, volume analysis, and pricing strategies in maintaining competitiveness and achieving financial sustainability in the travel and tourism industry.

Finance and funding in the travel and tourism

sector

sector

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:....................................................................................................................................4

TASK 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)...........................................................4

LO1 Understand the importance of costs, volume and profit for management decision making in

travel and tourism:...........................................................................................................................4

1.1 Explain the importance of costs and volume in financial management of travel and tourism

businesses.....................................................................................................................................4

1.2 Analyse pricing methods used in the travel and tourism sector................................................9

1.3 analyse factors influencing profit for travel and tourism businesses...................................10

Task2 (LO2, AC2.1, 2.2, M1, M2, M3, D1, D2, D3)....................................................................12

LO2- Understand the use of management accounting information as a decision-making tool in

travel and tourism businesses........................................................................................................12

P2.1 explain different types of management accounting information that could be used in

travel and tourism businesses using Dalata Hotel Group plc as your case study......................12

P2.2 assesses the use of management accounting information as a decision-making tool for

Dalata Hotel Group plc..............................................................................................................12

Task3 (LO3, AC3.1, M1, M2, M3, D1, D2, D3)...........................................................................23

LO3 be able to interpret financial accounts to assist decision making in travel and tourism

businesses:.....................................................................................................................................23

3.1 Interpret financial accounts of Dalata Hotel Group plc for the year ended 31st

December 2016 showing at least two years performance:.........................................................23

Task 4 (LO4, AC4.1, M1, M2, M3, D1, D2, D3)..........................................................................31

Introduction:....................................................................................................................................4

TASK 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)...........................................................4

LO1 Understand the importance of costs, volume and profit for management decision making in

travel and tourism:...........................................................................................................................4

1.1 Explain the importance of costs and volume in financial management of travel and tourism

businesses.....................................................................................................................................4

1.2 Analyse pricing methods used in the travel and tourism sector................................................9

1.3 analyse factors influencing profit for travel and tourism businesses...................................10

Task2 (LO2, AC2.1, 2.2, M1, M2, M3, D1, D2, D3)....................................................................12

LO2- Understand the use of management accounting information as a decision-making tool in

travel and tourism businesses........................................................................................................12

P2.1 explain different types of management accounting information that could be used in

travel and tourism businesses using Dalata Hotel Group plc as your case study......................12

P2.2 assesses the use of management accounting information as a decision-making tool for

Dalata Hotel Group plc..............................................................................................................12

Task3 (LO3, AC3.1, M1, M2, M3, D1, D2, D3)...........................................................................23

LO3 be able to interpret financial accounts to assist decision making in travel and tourism

businesses:.....................................................................................................................................23

3.1 Interpret financial accounts of Dalata Hotel Group plc for the year ended 31st

December 2016 showing at least two years performance:.........................................................23

Task 4 (LO4, AC4.1, M1, M2, M3, D1, D2, D3)..........................................................................31

LO4 – Understand sources and distribution of funding for public and non-public tourism

development...................................................................................................................................31

4.1 analyse sources and distribution of funding for the development of capital projects

associated with tourism..............................................................................................................31

Conclusion:....................................................................................................................................37

References:....................................................................................................................................38

development...................................................................................................................................31

4.1 analyse sources and distribution of funding for the development of capital projects

associated with tourism..............................................................................................................31

Conclusion:....................................................................................................................................37

References:....................................................................................................................................38

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

This report introduces about various feature of management accounting information &

significance of MAI as decision making tools. This report also describes about various method of

pricing in travel and tourism sector to emphasise actual economic situation to perfect & alternate

pricing strategy. This assignment will also dictate about cost volume & profit analysis and

relation to describe flexibility & feasibility of financial performance of Carnival Corporation Plc.

group. PowerPoint presentation is also included in it to provide deep discussion on MAI and

decision-making tool.

This report introduces about various feature of management accounting information &

significance of MAI as decision making tools. This report also describes about various method of

pricing in travel and tourism sector to emphasise actual economic situation to perfect & alternate

pricing strategy. This assignment will also dictate about cost volume & profit analysis and

relation to describe flexibility & feasibility of financial performance of Carnival Corporation Plc.

group. PowerPoint presentation is also included in it to provide deep discussion on MAI and

decision-making tool.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1 (LO1, AC1.1, 1.2, 1.3, M1, M2, M3, D1, D2, D3)

Report:

LO1 Understand the importance of costs, volume and profit for management decision

making in travel and tourism:

Introduction:

Working as a trainee business advisor in the Carnival plc London England, proper observation

and analysis of various career chances and opportunity in travel and tourism industry becomes

important & essential. Such analysis provides good acknowledgment and understanding of

different kinds of pricing methodologies, cost-profit volume relation & implication of

management and costing applications in the organisation for the betterment of management

could be evaluated easily. This report will introduce from importance of cost, profit and volume

relation and CVP analysis in tourism businesses entity (Hanifi and Taleei, 2016).

1.1 Explain the importance of costs and volume in financial management of travel and

tourism businesses

Solution:

Relation of cost volume and profit behaviour is known as Cost Volume & Profit analysis or CVP

analysis. Such kinds of cost and volume analysis are useful in making additional adjustment and

taking financial decision in travel and tourism sector for long term development. Cost behaviour

and its effective categorisation provide managers opportunities to understand actual requirements

to survive and run their business in precise way. Travelling sector are allowed to know their

requirement of funds for their future production and to maintain the level of profitability by cost

and volume analysis (Navaneetha & Punitha, 2017).

CVP analysis provides a platform to the travel agency to make strong insights regarding

proficiency and efficiency level of provided products and services. Cost and volume

classification are listed below:

Cost categorisation: Cost can be classified according to their nature and behaviour which

affects the output by the changes in the state of production activity.

Report:

LO1 Understand the importance of costs, volume and profit for management decision

making in travel and tourism:

Introduction:

Working as a trainee business advisor in the Carnival plc London England, proper observation

and analysis of various career chances and opportunity in travel and tourism industry becomes

important & essential. Such analysis provides good acknowledgment and understanding of

different kinds of pricing methodologies, cost-profit volume relation & implication of

management and costing applications in the organisation for the betterment of management

could be evaluated easily. This report will introduce from importance of cost, profit and volume

relation and CVP analysis in tourism businesses entity (Hanifi and Taleei, 2016).

1.1 Explain the importance of costs and volume in financial management of travel and

tourism businesses

Solution:

Relation of cost volume and profit behaviour is known as Cost Volume & Profit analysis or CVP

analysis. Such kinds of cost and volume analysis are useful in making additional adjustment and

taking financial decision in travel and tourism sector for long term development. Cost behaviour

and its effective categorisation provide managers opportunities to understand actual requirements

to survive and run their business in precise way. Travelling sector are allowed to know their

requirement of funds for their future production and to maintain the level of profitability by cost

and volume analysis (Navaneetha & Punitha, 2017).

CVP analysis provides a platform to the travel agency to make strong insights regarding

proficiency and efficiency level of provided products and services. Cost and volume

classification are listed below:

Cost categorisation: Cost can be classified according to their nature and behaviour which

affects the output by the changes in the state of production activity.

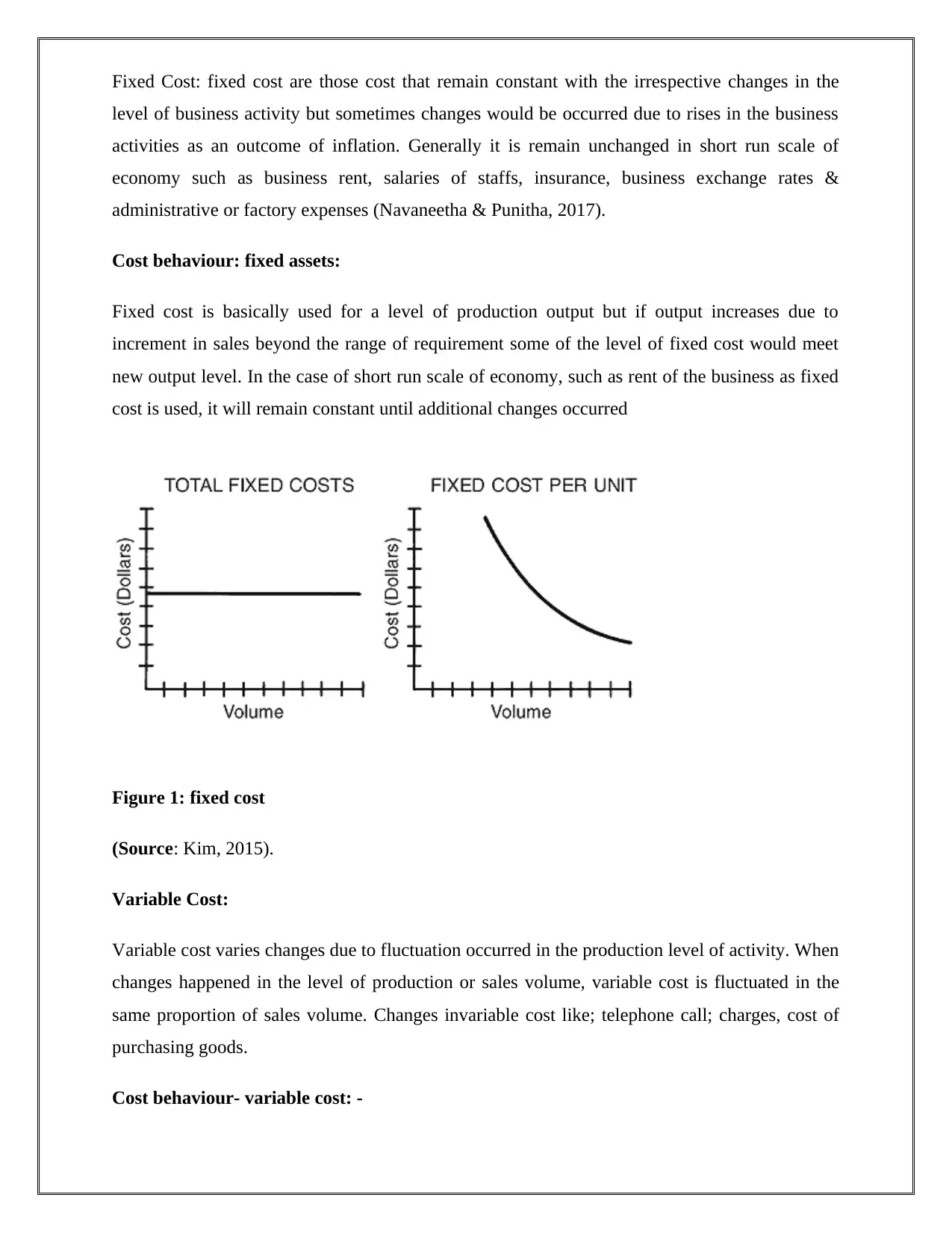

Fixed Cost: fixed cost are those cost that remain constant with the irrespective changes in the

level of business activity but sometimes changes would be occurred due to rises in the business

activities as an outcome of inflation. Generally it is remain unchanged in short run scale of

economy such as business rent, salaries of staffs, insurance, business exchange rates &

administrative or factory expenses (Navaneetha & Punitha, 2017).

Cost behaviour: fixed assets:

Fixed cost is basically used for a level of production output but if output increases due to

increment in sales beyond the range of requirement some of the level of fixed cost would meet

new output level. In the case of short run scale of economy, such as rent of the business as fixed

cost is used, it will remain constant until additional changes occurred

Figure 1: fixed cost

(Source: Kim, 2015).

Variable Cost:

Variable cost varies changes due to fluctuation occurred in the production level of activity. When

changes happened in the level of production or sales volume, variable cost is fluctuated in the

same proportion of sales volume. Changes invariable cost like; telephone call; charges, cost of

purchasing goods.

Cost behaviour- variable cost: -

level of business activity but sometimes changes would be occurred due to rises in the business

activities as an outcome of inflation. Generally it is remain unchanged in short run scale of

economy such as business rent, salaries of staffs, insurance, business exchange rates &

administrative or factory expenses (Navaneetha & Punitha, 2017).

Cost behaviour: fixed assets:

Fixed cost is basically used for a level of production output but if output increases due to

increment in sales beyond the range of requirement some of the level of fixed cost would meet

new output level. In the case of short run scale of economy, such as rent of the business as fixed

cost is used, it will remain constant until additional changes occurred

Figure 1: fixed cost

(Source: Kim, 2015).

Variable Cost:

Variable cost varies changes due to fluctuation occurred in the production level of activity. When

changes happened in the level of production or sales volume, variable cost is fluctuated in the

same proportion of sales volume. Changes invariable cost like; telephone call; charges, cost of

purchasing goods.

Cost behaviour- variable cost: -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable cost are those cost are varied with the level of changed in production and sale volume.

For example if Carnival Plc. Company engages in selling more Harbour Cruise ship, that time

company has to focus on additional vessels & variable cost would be fluctuated accordingly.

Company will be needed to enhance the production capacity and cost of raw material would be

increased. Such kinds of high level of business steps would create high lead for the betterment of

purchase pricing which would improvise economies of scale.

Figure 2: Variable cost

(Source: Kim, 2015)

Importance of cost behaviour in the Carnival Corporation & Plc.:-

Cost based analysis & reduction: travel and tourism sector are allowed to maintain the books

and financial records safely through cost behaviour analysis. Cost behaviour analysis is the

concept in which company can easily recognise its future requirement of funds and crucial

factors which helps travel industries in the allocation of financial resources. Cost based analysis

helps the management to survive in the market by maximising profit volume and reduce

wastages of non-values activities.

Future forecasting decision: costs structure is based on common behaviour of direct and

indirect cost. Direct costs are those costs which affect management directly and indirect cost

varies such cost behaviour which cannot directly measured by particular units of production

output. Such cost structure will help Carnival Corporation Plc. company to recognise and

manage overall budgeting resources to make reliable and effective forecasting for future decision

For example if Carnival Plc. Company engages in selling more Harbour Cruise ship, that time

company has to focus on additional vessels & variable cost would be fluctuated accordingly.

Company will be needed to enhance the production capacity and cost of raw material would be

increased. Such kinds of high level of business steps would create high lead for the betterment of

purchase pricing which would improvise economies of scale.

Figure 2: Variable cost

(Source: Kim, 2015)

Importance of cost behaviour in the Carnival Corporation & Plc.:-

Cost based analysis & reduction: travel and tourism sector are allowed to maintain the books

and financial records safely through cost behaviour analysis. Cost behaviour analysis is the

concept in which company can easily recognise its future requirement of funds and crucial

factors which helps travel industries in the allocation of financial resources. Cost based analysis

helps the management to survive in the market by maximising profit volume and reduce

wastages of non-values activities.

Future forecasting decision: costs structure is based on common behaviour of direct and

indirect cost. Direct costs are those costs which affect management directly and indirect cost

varies such cost behaviour which cannot directly measured by particular units of production

output. Such cost structure will help Carnival Corporation Plc. company to recognise and

manage overall budgeting resources to make reliable and effective forecasting for future decision

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making process. Cost behaviour allows travel sector to make services more strong and reliable

by reducing administrative cost to get long term achievements (Kim, 2015).

Importance of Volume:

Volume analysis can be measured by huge number of production activity and services are

provided to customers in the physical sort to attain more potential visitors in the travel agencies.

Volume analysis allows travel industries such as Carnival Corporation Plc. Company to make

effective relation between cost and profit by reducing cost and maximising profit. Importance of

volume analysis can be analysis through following points:

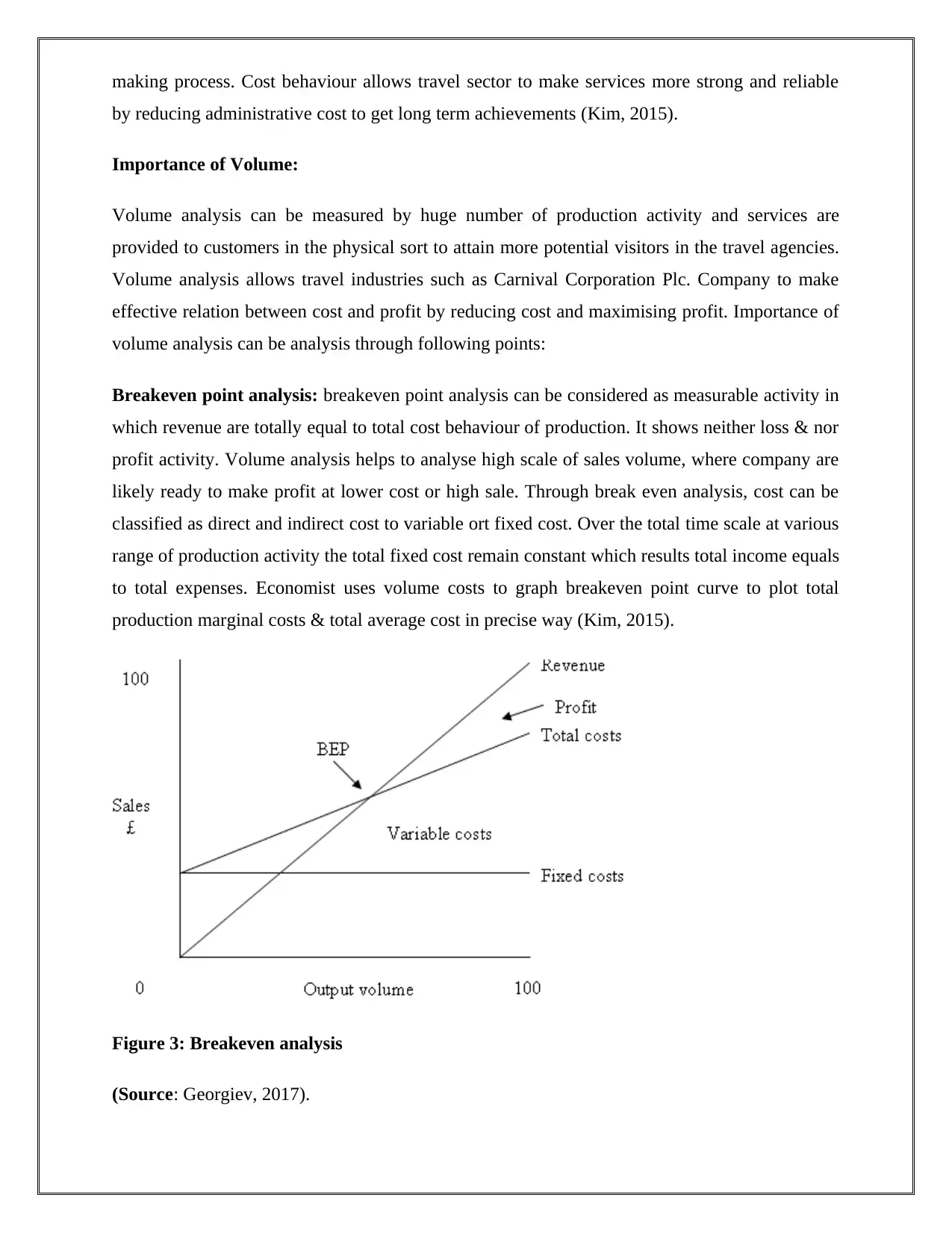

Breakeven point analysis: breakeven point analysis can be considered as measurable activity in

which revenue are totally equal to total cost behaviour of production. It shows neither loss & nor

profit activity. Volume analysis helps to analyse high scale of sales volume, where company are

likely ready to make profit at lower cost or high sale. Through break even analysis, cost can be

classified as direct and indirect cost to variable ort fixed cost. Over the total time scale at various

range of production activity the total fixed cost remain constant which results total income equals

to total expenses. Economist uses volume costs to graph breakeven point curve to plot total

production marginal costs & total average cost in precise way (Kim, 2015).

Figure 3: Breakeven analysis

(Source: Georgiev, 2017).

by reducing administrative cost to get long term achievements (Kim, 2015).

Importance of Volume:

Volume analysis can be measured by huge number of production activity and services are

provided to customers in the physical sort to attain more potential visitors in the travel agencies.

Volume analysis allows travel industries such as Carnival Corporation Plc. Company to make

effective relation between cost and profit by reducing cost and maximising profit. Importance of

volume analysis can be analysis through following points:

Breakeven point analysis: breakeven point analysis can be considered as measurable activity in

which revenue are totally equal to total cost behaviour of production. It shows neither loss & nor

profit activity. Volume analysis helps to analyse high scale of sales volume, where company are

likely ready to make profit at lower cost or high sale. Through break even analysis, cost can be

classified as direct and indirect cost to variable ort fixed cost. Over the total time scale at various

range of production activity the total fixed cost remain constant which results total income equals

to total expenses. Economist uses volume costs to graph breakeven point curve to plot total

production marginal costs & total average cost in precise way (Kim, 2015).

Figure 3: Breakeven analysis

(Source: Georgiev, 2017).

Economies of scale: economies of scale are based on cost and volume analysis. It is the cost

advantages which are obtained by organisation due to size, cost per unit of production which is

basically decreasing from increasing scale as fixed costs. Economies of scale are applied when

organisational and business situation are varied at various business entity level. It has some

limits like optimum design elements where cost per marginal unit starts to increase (Georgiev,

2017).

advantages which are obtained by organisation due to size, cost per unit of production which is

basically decreasing from increasing scale as fixed costs. Economies of scale are applied when

organisational and business situation are varied at various business entity level. It has some

limits like optimum design elements where cost per marginal unit starts to increase (Georgiev,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 Analyse pricing methods used in the travel and tourism sector

Effective and reliable moves related to pricing and its determination can help Carnival

Corporation travel industry to know reliable changes and fluctuation occurred in outside the

business entity. Proper pricing strategies can allow the company to stay competitive and

smoothly in market. Following are the various kinds of pricing methods:

1. Penetration pricing: it is technique of fixing price of relative products and service at initial and

low level entry price. Even it is determined at lower level comparatively to eventual market

value. It is way or strategy to attract new potential customers (Navaneetha & Punitha, 2017).

2. Marginal cost pricing: it is taken as fluctuation in the total cost which is arisen when the

quantity of produced services are changed per unit. It is cost pricing which is based in one more

additional cost of additional production. At each stage of production marginal pricing involves

additional pricing or cost.

3. Price skimming: price skimming is a method of setting a subjective higher prices of relative

products and services and declined the price over the time according to market demand. It is

methodology of capturing market actual consumer surplus.

4. Absorption pricing: is that method of pricing in which all cost is easily recovered through cost

based behaviour. This pricing strategy involves variable cost related to each items as per

proportionate amount of the fixed cost.

5. Cost plus pricing: cost plus pricing is the most relevant and effective pricing strategy for travel

and tourism agency to recover market surplus and attract more potential customers. It is better

and perfect technique for small sized enterprises to introduce their market competiveness and

additional economic requirements (Maguire, 2017).

Effective and reliable moves related to pricing and its determination can help Carnival

Corporation travel industry to know reliable changes and fluctuation occurred in outside the

business entity. Proper pricing strategies can allow the company to stay competitive and

smoothly in market. Following are the various kinds of pricing methods:

1. Penetration pricing: it is technique of fixing price of relative products and service at initial and

low level entry price. Even it is determined at lower level comparatively to eventual market

value. It is way or strategy to attract new potential customers (Navaneetha & Punitha, 2017).

2. Marginal cost pricing: it is taken as fluctuation in the total cost which is arisen when the

quantity of produced services are changed per unit. It is cost pricing which is based in one more

additional cost of additional production. At each stage of production marginal pricing involves

additional pricing or cost.

3. Price skimming: price skimming is a method of setting a subjective higher prices of relative

products and services and declined the price over the time according to market demand. It is

methodology of capturing market actual consumer surplus.

4. Absorption pricing: is that method of pricing in which all cost is easily recovered through cost

based behaviour. This pricing strategy involves variable cost related to each items as per

proportionate amount of the fixed cost.

5. Cost plus pricing: cost plus pricing is the most relevant and effective pricing strategy for travel

and tourism agency to recover market surplus and attract more potential customers. It is better

and perfect technique for small sized enterprises to introduce their market competiveness and

additional economic requirements (Maguire, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 analyse factors influencing profit for travel and tourism businesses

Profit is a very economic and justified concept for travel and tourism. It is a financial and

expected return for the small enterprises which appreciate entities to achieve desired goals after

avoiding risk. Profit is focused as important sources as a reward to provide finance and relative

finding through justified elements. Retained profits are essential sources which are used in the

business to describe actual financial position of company (Georgiev, 2017).

Factor influencing profit:

Seasonality: tourism profit is basically affected by seasonal business types in almost field of the

world which creates unique challenges both in operational norms and operational management of

tourism business. Off season packages, holiday booking are affected by seasonality of business

in travel and tourism agency. Such changes create opposite reaction on customers mind and

profit gets reduced in off seasons (Georgiev, 2017).

Political environment: profitability of business entity is based on consumers spending and

preferences. Sometimes changes in the rules and regulation of political environment may create

negative or positive fluctuation upon business entity. Company fail and face difficulties in

interpreting its actual business situation and external changes occurred in the environment. Such

fluctuation in governmental rules and other political disturbance create negative influence upon

profit generation activity.

Economic environment: economic factor are relate to changes in economic environment which

affects the business profit through its regulations, access of profit and credit & demand of goods

and services regarding technological betterments of economic market demand. High interest

rates, exchange rate, inflation are the factor that affects the profit.

Production and inventory level: travel and tourism agencies need to maintain their sensible

inventory level to manage their inventory level and increase the gross profit in business entity. If

company is engaged in selling their production unit in a small amount in a total given period of

time, the cost of sales would be overweighed by total sales (Georgiev, 2017).

Profit is a very economic and justified concept for travel and tourism. It is a financial and

expected return for the small enterprises which appreciate entities to achieve desired goals after

avoiding risk. Profit is focused as important sources as a reward to provide finance and relative

finding through justified elements. Retained profits are essential sources which are used in the

business to describe actual financial position of company (Georgiev, 2017).

Factor influencing profit:

Seasonality: tourism profit is basically affected by seasonal business types in almost field of the

world which creates unique challenges both in operational norms and operational management of

tourism business. Off season packages, holiday booking are affected by seasonality of business

in travel and tourism agency. Such changes create opposite reaction on customers mind and

profit gets reduced in off seasons (Georgiev, 2017).

Political environment: profitability of business entity is based on consumers spending and

preferences. Sometimes changes in the rules and regulation of political environment may create

negative or positive fluctuation upon business entity. Company fail and face difficulties in

interpreting its actual business situation and external changes occurred in the environment. Such

fluctuation in governmental rules and other political disturbance create negative influence upon

profit generation activity.

Economic environment: economic factor are relate to changes in economic environment which

affects the business profit through its regulations, access of profit and credit & demand of goods

and services regarding technological betterments of economic market demand. High interest

rates, exchange rate, inflation are the factor that affects the profit.

Production and inventory level: travel and tourism agencies need to maintain their sensible

inventory level to manage their inventory level and increase the gross profit in business entity. If

company is engaged in selling their production unit in a small amount in a total given period of

time, the cost of sales would be overweighed by total sales (Georgiev, 2017).

Conclusion:

This report has been explained about relation between cost volume and profit analysis. Various

uses of prices determination are also included in it to describe significance of pricing strategies

in travel and tourism business. This reading has also involved a deep explanation on profit and

various factors affecting profit (Chaperon, 2017).

This report has been explained about relation between cost volume and profit analysis. Various

uses of prices determination are also included in it to describe significance of pricing strategies

in travel and tourism business. This reading has also involved a deep explanation on profit and

various factors affecting profit (Chaperon, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 40

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.