Finance Report: Bank Roles, Debt Finance, Basel III, and Crisis

VerifiedAdded on 2020/05/28

|7

|1631

|70

Report

AI Summary

This finance report critically examines the key roles of banks in contributing to a country's financial system, focusing on credit and liquidity provisions. It evaluates the problems associated with debt finance for financial deficit units and discusses the impact of Basel III regulations on capital adequacy, liquidity, and leverage. The report explains the process of asset securitization and its benefits for banks, while also analyzing the implications of the global financial crisis on bank performance and the measures taken by different countries to mitigate the crisis, including Singapore, the UK, and the USA, with specific examples from OCBC Bank, Barclays Bank, and Citigroup. The report uses financial data to support the analysis.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

1

Table of Contents

1. Identifying and critically discussing 2 key roles of bank in terms of contribution to country

financial system:.........................................................................................................................2

2. Critically evaluating the problems associated with relying on debt finance being provided

by bank with those parties who are a financial surplus unit to those who are a financial deficit

unit:............................................................................................................................................2

3. Critically changing the capital adequacy, liquidity and leverage as stipulated by Basel III

and discussing the impact of these changes in banks financial condition:................................3

4. Critically explaining the process of asset securitization and why banks may wish to

securitize:...................................................................................................................................4

5. Critically discussing the implication of global crisis on banks financial shortly after the

crisis and discussing the measure used by the country to calm the crisis:.................................5

Reference and Bibliography:......................................................................................................6

1

Table of Contents

1. Identifying and critically discussing 2 key roles of bank in terms of contribution to country

financial system:.........................................................................................................................2

2. Critically evaluating the problems associated with relying on debt finance being provided

by bank with those parties who are a financial surplus unit to those who are a financial deficit

unit:............................................................................................................................................2

3. Critically changing the capital adequacy, liquidity and leverage as stipulated by Basel III

and discussing the impact of these changes in banks financial condition:................................3

4. Critically explaining the process of asset securitization and why banks may wish to

securitize:...................................................................................................................................4

5. Critically discussing the implication of global crisis on banks financial shortly after the

crisis and discussing the measure used by the country to calm the crisis:.................................5

Reference and Bibliography:......................................................................................................6

FINANCE

2

1. Identifying and critically discussing 2 key roles of bank in terms of contribution to

country financial system:

There are certain roles that is played by OCBC Bank in Singapore, Barclays Bank in

UK and Citigroup in USA, which directly helps in smoothing the functioning of financial

system in the country. The identified organisations mainly contribute to the distribution of

monetary system in their country, which efficiently helps in improving financial operations.

The credit provision and liquidity provision is effectively conducted by OCBC Bank in

Singapore, Barclays Bank in UK and Citigroup in USA, which helps in supporting the

financial system of the country. The increment in credit provisions could directly fuel the

economic activity of the country, where business could flourish and generate higher cash

flow. This credit provision could fuel economic activities, where investment beyond cash on

hand is conducted (Ocbc.com 2018). This helps in increasing homes purchase without

savings the entire cost in advance and government to smooth their spending for investing in

infrastructure projects. Liquidity provisions are also conducted by OCBC, Barclays Bank and

Citigroup, which allows both demand deposits and credit provisions. These banks directly

conduct financial market services such as buying and selling securities, which help in

supporting financial requirements of organisations. The banks are the main provider of

liquidity to the organisation and customers in their respective countries.

2. Critically evaluating the problems associated with relying on debt finance being

provided by bank with those parties who are a financial surplus unit to those who are a

financial deficit unit:

There is different level of problems that arises from debt finances, which needs to be

accommodated by banks before providing finance to companies. In addition, banks support

the companies with financial surplus rather than financial deficit, as they have higher

capability to repay the financing amount with interest. The main problem associated with the

2

1. Identifying and critically discussing 2 key roles of bank in terms of contribution to

country financial system:

There are certain roles that is played by OCBC Bank in Singapore, Barclays Bank in

UK and Citigroup in USA, which directly helps in smoothing the functioning of financial

system in the country. The identified organisations mainly contribute to the distribution of

monetary system in their country, which efficiently helps in improving financial operations.

The credit provision and liquidity provision is effectively conducted by OCBC Bank in

Singapore, Barclays Bank in UK and Citigroup in USA, which helps in supporting the

financial system of the country. The increment in credit provisions could directly fuel the

economic activity of the country, where business could flourish and generate higher cash

flow. This credit provision could fuel economic activities, where investment beyond cash on

hand is conducted (Ocbc.com 2018). This helps in increasing homes purchase without

savings the entire cost in advance and government to smooth their spending for investing in

infrastructure projects. Liquidity provisions are also conducted by OCBC, Barclays Bank and

Citigroup, which allows both demand deposits and credit provisions. These banks directly

conduct financial market services such as buying and selling securities, which help in

supporting financial requirements of organisations. The banks are the main provider of

liquidity to the organisation and customers in their respective countries.

2. Critically evaluating the problems associated with relying on debt finance being

provided by bank with those parties who are a financial surplus unit to those who are a

financial deficit unit:

There is different level of problems that arises from debt finances, which needs to be

accommodated by banks before providing finance to companies. In addition, banks support

the companies with financial surplus rather than financial deficit, as they have higher

capability to repay the financing amount with interest. The main problem associated with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

3

financing companies with financial deficit is the increasing accumulation of interest payment,

which cannot be conducted with the existing revenue stream. The company with increased

debt accumulation could lead to insolvency, which might hamper the repayment of banks

finances. For example, Lehman Brothers increased debt accumulation before the crisis, where

banks did not support the company due to its excessive financial deficit. Thus, it could be

understood that banks do not support companies with extra debt financing if they have

financial deficit. The problems in repayment and chances of default by the company having

financial deficit is very strong, which could hinder actual financial condition of the bank.

3. Critically changing the capital adequacy, liquidity and leverage as stipulated by Basel

III and discussing the impact of these changes in banks financial condition:

The Basel III was mainly drafted after the financial crisis of 2008, which mainly

liquidated financial sector of the world. The extensive debt accumulation conducted by banks

was mainly reduced with the help of Basel III, as it could help in smoothing the function of

banks. The new capital requirement directly represents tighter equity definition maintained by

banks. In addition, the common equity requirement under Basel III mainly increased from 2%

to 4.5% in 2015 with the increment in mandatory reserve from 4% to 6%. Moreover, under

leverage ratio the banks need to be maintain a 3% leverage all time, which could help in

thickening the cushion of cash reserves. Moreover, the liquidity coverage ratio needs to be no

lower than 100% under Basel III, which could help in reducing the chances of default by a

bank (Angelini et al. 2015). Net Funding Stability Ratio (NFSR) needs to be maintained by

banks, which could help in maintaining capital stability. Furthermore, the liquidity needs to

be maintained by banks for 30-day time horizon under acute liquidity stress scenario. These

changes could help in strengthening the financial position of banks during any kind of

financial crisis.

3

financing companies with financial deficit is the increasing accumulation of interest payment,

which cannot be conducted with the existing revenue stream. The company with increased

debt accumulation could lead to insolvency, which might hamper the repayment of banks

finances. For example, Lehman Brothers increased debt accumulation before the crisis, where

banks did not support the company due to its excessive financial deficit. Thus, it could be

understood that banks do not support companies with extra debt financing if they have

financial deficit. The problems in repayment and chances of default by the company having

financial deficit is very strong, which could hinder actual financial condition of the bank.

3. Critically changing the capital adequacy, liquidity and leverage as stipulated by Basel

III and discussing the impact of these changes in banks financial condition:

The Basel III was mainly drafted after the financial crisis of 2008, which mainly

liquidated financial sector of the world. The extensive debt accumulation conducted by banks

was mainly reduced with the help of Basel III, as it could help in smoothing the function of

banks. The new capital requirement directly represents tighter equity definition maintained by

banks. In addition, the common equity requirement under Basel III mainly increased from 2%

to 4.5% in 2015 with the increment in mandatory reserve from 4% to 6%. Moreover, under

leverage ratio the banks need to be maintain a 3% leverage all time, which could help in

thickening the cushion of cash reserves. Moreover, the liquidity coverage ratio needs to be no

lower than 100% under Basel III, which could help in reducing the chances of default by a

bank (Angelini et al. 2015). Net Funding Stability Ratio (NFSR) needs to be maintained by

banks, which could help in maintaining capital stability. Furthermore, the liquidity needs to

be maintained by banks for 30-day time horizon under acute liquidity stress scenario. These

changes could help in strengthening the financial position of banks during any kind of

financial crisis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

4

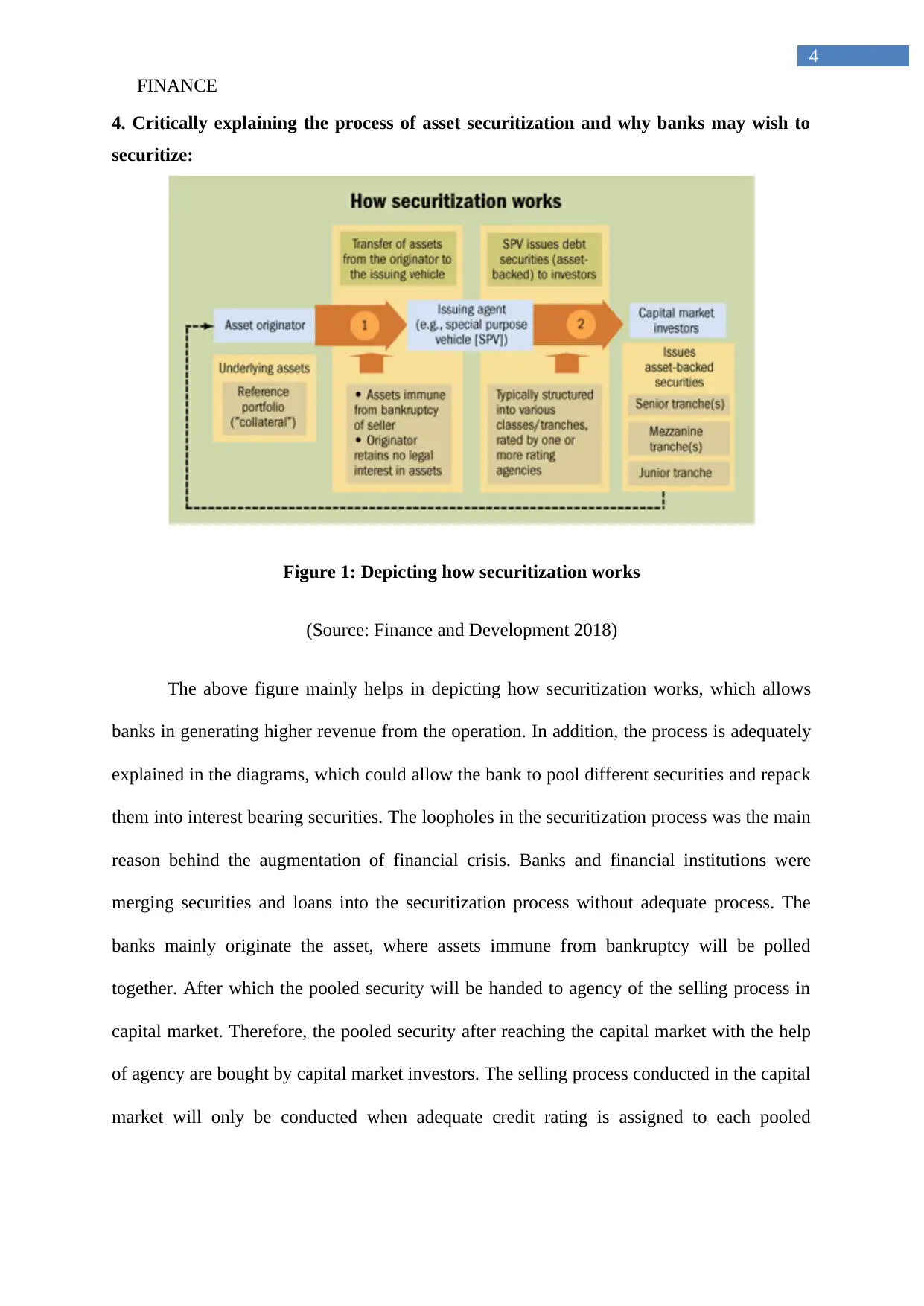

4. Critically explaining the process of asset securitization and why banks may wish to

securitize:

Figure 1: Depicting how securitization works

(Source: Finance and Development 2018)

The above figure mainly helps in depicting how securitization works, which allows

banks in generating higher revenue from the operation. In addition, the process is adequately

explained in the diagrams, which could allow the bank to pool different securities and repack

them into interest bearing securities. The loopholes in the securitization process was the main

reason behind the augmentation of financial crisis. Banks and financial institutions were

merging securities and loans into the securitization process without adequate process. The

banks mainly originate the asset, where assets immune from bankruptcy will be polled

together. After which the pooled security will be handed to agency of the selling process in

capital market. Therefore, the pooled security after reaching the capital market with the help

of agency are bought by capital market investors. The selling process conducted in the capital

market will only be conducted when adequate credit rating is assigned to each pooled

4

4. Critically explaining the process of asset securitization and why banks may wish to

securitize:

Figure 1: Depicting how securitization works

(Source: Finance and Development 2018)

The above figure mainly helps in depicting how securitization works, which allows

banks in generating higher revenue from the operation. In addition, the process is adequately

explained in the diagrams, which could allow the bank to pool different securities and repack

them into interest bearing securities. The loopholes in the securitization process was the main

reason behind the augmentation of financial crisis. Banks and financial institutions were

merging securities and loans into the securitization process without adequate process. The

banks mainly originate the asset, where assets immune from bankruptcy will be polled

together. After which the pooled security will be handed to agency of the selling process in

capital market. Therefore, the pooled security after reaching the capital market with the help

of agency are bought by capital market investors. The selling process conducted in the capital

market will only be conducted when adequate credit rating is assigned to each pooled

FINANCE

5

security. Therefore, banks wish to securitise for attaining flow of cash after providing loans to

its borrower.

5. Critically discussing the implication of global crisis on banks financial shortly after

the crisis and discussing the measure used by the country to calm the crisis:

During the financial crisis the profit of OCBC bank mainly declined from the level of

2,183,240,000 to 1,860,010,000 in 2008 as compared from 2007 (Eresources.nlb.gov.sg

2018). This mainly indicates the incapability of the company to attain higher profitability

after the financial crisis. However, Singapore mainly pledged S$2.9 billion in 2008 and

S$20.5 billion in 2009 for reducing the impact of financial crisis on banking operations.

On the other hand, performance of Barclays Bank in UK increased from 2008 to 2009

from 5,249,000,000 to 10,289,000,000, which indicates high end performance conducted by

the company (Home.barclays 2018). Moreover, the UK government mainly used £39 billion

as their bailout package to reduce the impact of financial crisis. In addition, merger of HBOS

and Lloyds was nationalised, where £200 billion was available for new debt issue under the

special liquidity scheme. Lastly, the guarantee of the depositors was raised from £35,000 to

£50,000, while Bank of England cut the interest rate in half to reduce the problems portrayed

by financial crisis.

Furthermore, performance of Citigroup in USA mainly declined during financial

crisis, where the group earned net loss from 2008 to 2009. The net loss in 2008 was at

27,684,000,000, while the loss declined in 2009 to 1,606,000,000 (Citigroup.com 2018). The

US government conducted the largest government intervene in the financial crisis, where

$700 billion bailout programme was conducted to support banking industry. In addition, the

bank deposits were raised from $100,000 to $250,000 by the end of 2009.moreover, the FED

also cut interest rate to 1.5%, which helped in creating liquidity into the market.

5

security. Therefore, banks wish to securitise for attaining flow of cash after providing loans to

its borrower.

5. Critically discussing the implication of global crisis on banks financial shortly after

the crisis and discussing the measure used by the country to calm the crisis:

During the financial crisis the profit of OCBC bank mainly declined from the level of

2,183,240,000 to 1,860,010,000 in 2008 as compared from 2007 (Eresources.nlb.gov.sg

2018). This mainly indicates the incapability of the company to attain higher profitability

after the financial crisis. However, Singapore mainly pledged S$2.9 billion in 2008 and

S$20.5 billion in 2009 for reducing the impact of financial crisis on banking operations.

On the other hand, performance of Barclays Bank in UK increased from 2008 to 2009

from 5,249,000,000 to 10,289,000,000, which indicates high end performance conducted by

the company (Home.barclays 2018). Moreover, the UK government mainly used £39 billion

as their bailout package to reduce the impact of financial crisis. In addition, merger of HBOS

and Lloyds was nationalised, where £200 billion was available for new debt issue under the

special liquidity scheme. Lastly, the guarantee of the depositors was raised from £35,000 to

£50,000, while Bank of England cut the interest rate in half to reduce the problems portrayed

by financial crisis.

Furthermore, performance of Citigroup in USA mainly declined during financial

crisis, where the group earned net loss from 2008 to 2009. The net loss in 2008 was at

27,684,000,000, while the loss declined in 2009 to 1,606,000,000 (Citigroup.com 2018). The

US government conducted the largest government intervene in the financial crisis, where

$700 billion bailout programme was conducted to support banking industry. In addition, the

bank deposits were raised from $100,000 to $250,000 by the end of 2009.moreover, the FED

also cut interest rate to 1.5%, which helped in creating liquidity into the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

6

Reference and Bibliography:

Angelini, P., Clerc, L., Cúrdia, V., Gambacorta, L., Gerali, A., Locarno, A., Motto, R.,

Roeger, W., Van den Heuvel, S. and Vlček, J., 2015. Basel III: Long‐term Impact on

Economic Performance and Fluctuations. The Manchester School, 83(2), pp.217-251.

Citigroup.com. (2018). [online] Available at:

http://www.citigroup.com/citi/investor/quarterly/2010/ar09c_en.pdf?ieNocache=157

[Accessed 12 Jan. 2018].

Eresources.nlb.gov.sg. (2018). Singapore is first East Asian country to slip into recession -

Singapore History. [online] Available at:

http://eresources.nlb.gov.sg/history/events/3cacf256-82cc-4776-b7f8-83757723b502

[Accessed 11 Jan. 2018].

Finance and Development | F&D. (2018). Finance and Development. [online] Available at:

http://www.imf.org/external/pubs/ft/fandd/2008/09/basics.htm [Accessed 11 Jan. 2018].

Home.barclays. (2018). [online] Available at:

https://www.home.barclays/content/dam/barclayspublic/docs/InvestorRelations/

AnnualReports/AR2009/2009-barclays-bank-plc-annual-report.pdf [Accessed 12 Jan. 2018].

Ocbc.com. (2018). OCBC - Investors - Annual Reports. [online] Available at:

https://www.ocbc.com/group/investors/annual-reports.html [Accessed 11 Jan. 2018].

6

Reference and Bibliography:

Angelini, P., Clerc, L., Cúrdia, V., Gambacorta, L., Gerali, A., Locarno, A., Motto, R.,

Roeger, W., Van den Heuvel, S. and Vlček, J., 2015. Basel III: Long‐term Impact on

Economic Performance and Fluctuations. The Manchester School, 83(2), pp.217-251.

Citigroup.com. (2018). [online] Available at:

http://www.citigroup.com/citi/investor/quarterly/2010/ar09c_en.pdf?ieNocache=157

[Accessed 12 Jan. 2018].

Eresources.nlb.gov.sg. (2018). Singapore is first East Asian country to slip into recession -

Singapore History. [online] Available at:

http://eresources.nlb.gov.sg/history/events/3cacf256-82cc-4776-b7f8-83757723b502

[Accessed 11 Jan. 2018].

Finance and Development | F&D. (2018). Finance and Development. [online] Available at:

http://www.imf.org/external/pubs/ft/fandd/2008/09/basics.htm [Accessed 11 Jan. 2018].

Home.barclays. (2018). [online] Available at:

https://www.home.barclays/content/dam/barclayspublic/docs/InvestorRelations/

AnnualReports/AR2009/2009-barclays-bank-plc-annual-report.pdf [Accessed 12 Jan. 2018].

Ocbc.com. (2018). OCBC - Investors - Annual Reports. [online] Available at:

https://www.ocbc.com/group/investors/annual-reports.html [Accessed 11 Jan. 2018].

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.