Finance Report: Corporate Governance, Investment Appraisal, CVP

VerifiedAdded on 2023/06/15

|14

|4087

|398

Report

AI Summary

This finance report delves into key aspects of corporate finance, starting with an examination of the 'comply or explain' model of corporate governance and its implications for organizations. It proceeds to analyze investment appraisal techniques, including the calculation of payback periods and accounting rates of return for different projects, evaluating their strengths and weaknesses. Furthermore, the report discusses the concept of contribution and its significance in Cost-Volume-Profit (CVP) analysis, alongside its application in decision-making scenarios such as dropping a product or service and evaluating special contracts. Finally, the report includes a practical component involving the preparation of an opening statement of financial position and a monthly forecasted cash flow statement for a hypothetical business, providing a comprehensive overview of financial analysis and planning. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

TO FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question: 1.......................................................................................................................................3

a. ‘comply or explain’ model of corporate governance..............................................................3

(B)...............................................................................................................................................4

Question: 2.......................................................................................................................................4

a. Calculation of payback period for two contracts.....................................................................4

b. Calculation of accounting rate of return for Edinburgh and Newcastle upon Tyne contract. 5

(C)...............................................................................................................................................6

(D)...............................................................................................................................................7

Question: 3.......................................................................................................................................7

a. Concept of contribution and its importance in CVP technique...............................................7

b. Nature of decisions 'dropping a product or service' and 'special contracts'............................8

c. Critical evaluation of CVP technique and its limitations........................................................9

Question : 4....................................................................................................................................10

a. Preparation of Opening statement of financial position for Fashion Clothing at the start of

July 2015...................................................................................................................................10

b. Preparation of monthly forecasted cash flow statement.......................................................10

c)................................................................................................................................................11

REFERENCES..............................................................................................................................13

Question: 1.......................................................................................................................................3

a. ‘comply or explain’ model of corporate governance..............................................................3

(B)...............................................................................................................................................4

Question: 2.......................................................................................................................................4

a. Calculation of payback period for two contracts.....................................................................4

b. Calculation of accounting rate of return for Edinburgh and Newcastle upon Tyne contract. 5

(C)...............................................................................................................................................6

(D)...............................................................................................................................................7

Question: 3.......................................................................................................................................7

a. Concept of contribution and its importance in CVP technique...............................................7

b. Nature of decisions 'dropping a product or service' and 'special contracts'............................8

c. Critical evaluation of CVP technique and its limitations........................................................9

Question : 4....................................................................................................................................10

a. Preparation of Opening statement of financial position for Fashion Clothing at the start of

July 2015...................................................................................................................................10

b. Preparation of monthly forecasted cash flow statement.......................................................10

c)................................................................................................................................................11

REFERENCES..............................................................................................................................13

Question: 1

a. ‘comply or explain’ model of corporate governance

In modern times, it has been seen that major contribution towards the economy is made

by the economic activities of large corporations. In a company form of business organization, the

ownership and management is being separated from each other which gives rise to principal

agent relationship and subsequently, conflict of interests arises due to differing goals of

shareholders and management (Khaddafi, Aryani and Heikal, 2021). Therefore, a system known

as corporate governance came into existence which is meant for controlling and directing the

way companies are running their operations. Initially, corporate governance has been developed

to ensure that management are not engaged in activities that results in disadvantageous position

for the shareholders.

There is another approach to corporate governance known as 'comply or explain'

approach which varies from the general approach adopted by SOX significantly. Under this

approach, it has been mandated for the corporations to comply with corporate governance code,

failing which demands for explanation of reasons for not complying with the code. The model is

described as a voluntary compliance without any compelling efforts made by a regulatory body.

In modern times, it has been seen that major contribution towards the economy is made

by the economic activities of large corporations. In a company form of business organization, the

ownership and management is being separated from each other which gives rise to principal

agent relationship and subsequently, conflict of interests arises due to differing goals of

shareholders and management. Therefore, a system known as corporate governance came into

existence which is meant for controlling and directing the way companies are running their

operations. Initially, corporate governance has been developed to ensure that management are

not engaged in activities that results in disadvantageous position for the shareholders.

There is another approach to corporate governance known as 'comply or explain'

approach which varies from the general approach adopted by SOX significantly. Under this

approach, it has been mandated for the corporations to comply with corporate governance code,

failing which demands for explanation of reasons for not complying with the code. The model is

described as a voluntary compliance without any compelling efforts made by a regulatory body.

a. ‘comply or explain’ model of corporate governance

In modern times, it has been seen that major contribution towards the economy is made

by the economic activities of large corporations. In a company form of business organization, the

ownership and management is being separated from each other which gives rise to principal

agent relationship and subsequently, conflict of interests arises due to differing goals of

shareholders and management (Khaddafi, Aryani and Heikal, 2021). Therefore, a system known

as corporate governance came into existence which is meant for controlling and directing the

way companies are running their operations. Initially, corporate governance has been developed

to ensure that management are not engaged in activities that results in disadvantageous position

for the shareholders.

There is another approach to corporate governance known as 'comply or explain'

approach which varies from the general approach adopted by SOX significantly. Under this

approach, it has been mandated for the corporations to comply with corporate governance code,

failing which demands for explanation of reasons for not complying with the code. The model is

described as a voluntary compliance without any compelling efforts made by a regulatory body.

In modern times, it has been seen that major contribution towards the economy is made

by the economic activities of large corporations. In a company form of business organization, the

ownership and management is being separated from each other which gives rise to principal

agent relationship and subsequently, conflict of interests arises due to differing goals of

shareholders and management. Therefore, a system known as corporate governance came into

existence which is meant for controlling and directing the way companies are running their

operations. Initially, corporate governance has been developed to ensure that management are

not engaged in activities that results in disadvantageous position for the shareholders.

There is another approach to corporate governance known as 'comply or explain'

approach which varies from the general approach adopted by SOX significantly. Under this

approach, it has been mandated for the corporations to comply with corporate governance code,

failing which demands for explanation of reasons for not complying with the code. The model is

described as a voluntary compliance without any compelling efforts made by a regulatory body.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Complying with the model of corporate governance is necessary for all the corporate.

This is the responsibility of the organisation and commercial institutions to deal with all different

regulations and code of conducts associated with the corporate governance. Corporate

governance support companies to drive all its operations in the best way possible. The

implication of all different rule and regulation is wisely depending upon the nature of

organisation (Madaan and Singh, 2019). These compliances clarify about all the mandatory

requirement that organisation need to adjust in process to execute the business operations. The

compliance of the regulatory requirement is necessary and mandatory for al the companies

irrespective to the nature of operations. In case of any failure in order to comply with the

regulations than mandatory charges will deduct from the company. Corporate governance as a

model needs to incorporate by the company in process to operate regular operations of venture.

(B)

The approach that is taken to fill the financial statement by Plc incorporates in United

Kingdom. The approach is diversified and allows the companies to maintain all the regulatory

requirements in the best way possible. The paper work is less and allows the organisation to

efficiently incorporate the entire processing in the best way possible. The financial statement

must be completely prepared with all implication of various accounting regulations. All the

books of accounts must comply with accounting standards. Any adjustment that is made must be

mentioned with the special notes so that reader of the financial statement makes itself aware with

the situation. Filling up financial statement require the complete details about all the transaction

that is included in the financial record of the venture (Tao and et.al., 2021). All documents must

be submitted by the venture so that all the key details and information that is used and explored

while preparing the financial statement can verify by the stakeholders. Further, the modification

in the financial stamen must also be made timely manner so that all requirements can overcome

by the stakeholders. The mandatory audit must also be required so that proper verification of all

different adjustment that is made by the professional.

Question: 2

a. Calculation of payback period for two contracts

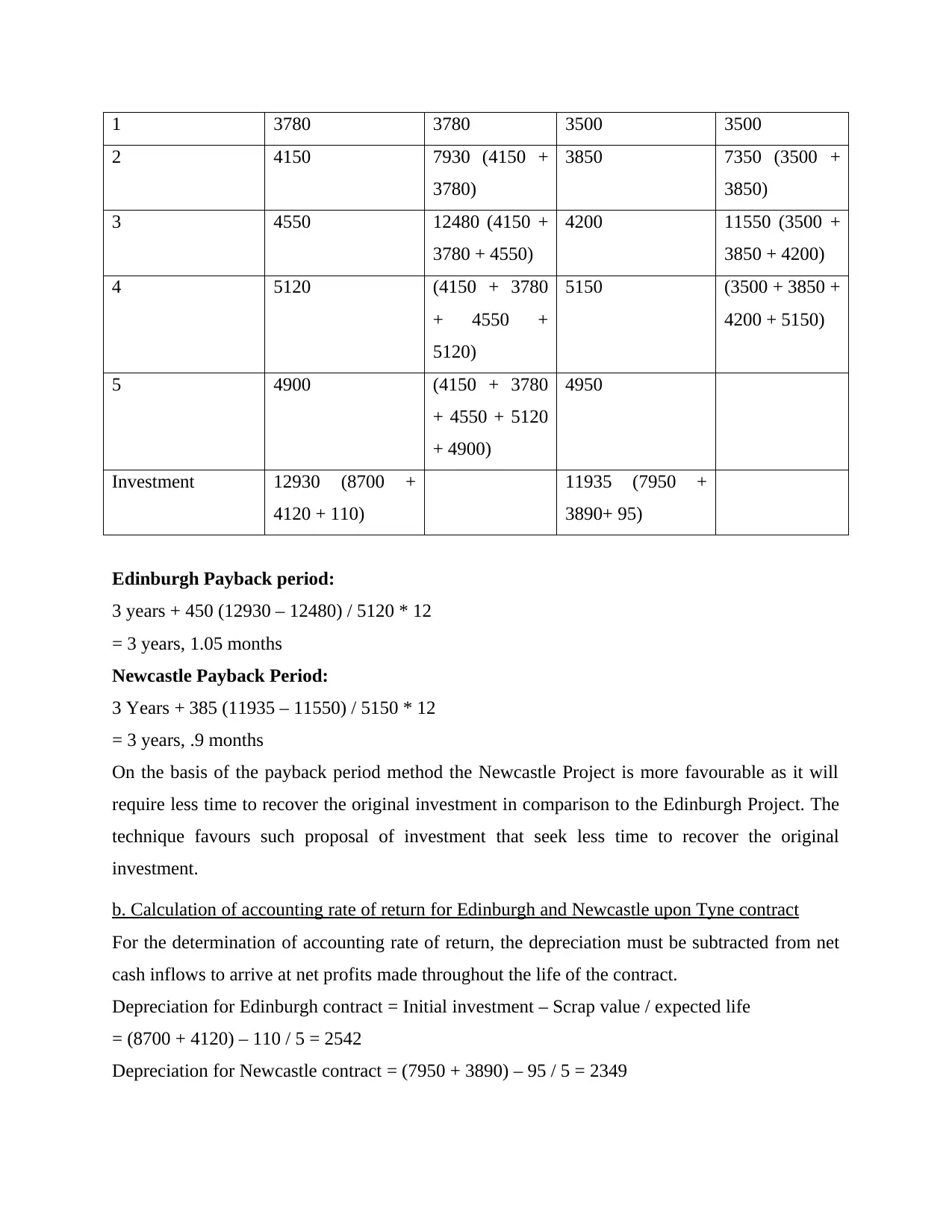

Year Edinburgh Newcastle

This is the responsibility of the organisation and commercial institutions to deal with all different

regulations and code of conducts associated with the corporate governance. Corporate

governance support companies to drive all its operations in the best way possible. The

implication of all different rule and regulation is wisely depending upon the nature of

organisation (Madaan and Singh, 2019). These compliances clarify about all the mandatory

requirement that organisation need to adjust in process to execute the business operations. The

compliance of the regulatory requirement is necessary and mandatory for al the companies

irrespective to the nature of operations. In case of any failure in order to comply with the

regulations than mandatory charges will deduct from the company. Corporate governance as a

model needs to incorporate by the company in process to operate regular operations of venture.

(B)

The approach that is taken to fill the financial statement by Plc incorporates in United

Kingdom. The approach is diversified and allows the companies to maintain all the regulatory

requirements in the best way possible. The paper work is less and allows the organisation to

efficiently incorporate the entire processing in the best way possible. The financial statement

must be completely prepared with all implication of various accounting regulations. All the

books of accounts must comply with accounting standards. Any adjustment that is made must be

mentioned with the special notes so that reader of the financial statement makes itself aware with

the situation. Filling up financial statement require the complete details about all the transaction

that is included in the financial record of the venture (Tao and et.al., 2021). All documents must

be submitted by the venture so that all the key details and information that is used and explored

while preparing the financial statement can verify by the stakeholders. Further, the modification

in the financial stamen must also be made timely manner so that all requirements can overcome

by the stakeholders. The mandatory audit must also be required so that proper verification of all

different adjustment that is made by the professional.

Question: 2

a. Calculation of payback period for two contracts

Year Edinburgh Newcastle

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 3780 3780 3500 3500

2 4150 7930 (4150 +

3780)

3850 7350 (3500 +

3850)

3 4550 12480 (4150 +

3780 + 4550)

4200 11550 (3500 +

3850 + 4200)

4 5120 (4150 + 3780

+ 4550 +

5120)

5150 (3500 + 3850 +

4200 + 5150)

5 4900 (4150 + 3780

+ 4550 + 5120

+ 4900)

4950

Investment 12930 (8700 +

4120 + 110)

11935 (7950 +

3890+ 95)

Edinburgh Payback period:

3 years + 450 (12930 – 12480) / 5120 * 12

= 3 years, 1.05 months

Newcastle Payback Period:

3 Years + 385 (11935 – 11550) / 5150 * 12

= 3 years, .9 months

On the basis of the payback period method the Newcastle Project is more favourable as it will

require less time to recover the original investment in comparison to the Edinburgh Project. The

technique favours such proposal of investment that seek less time to recover the original

investment.

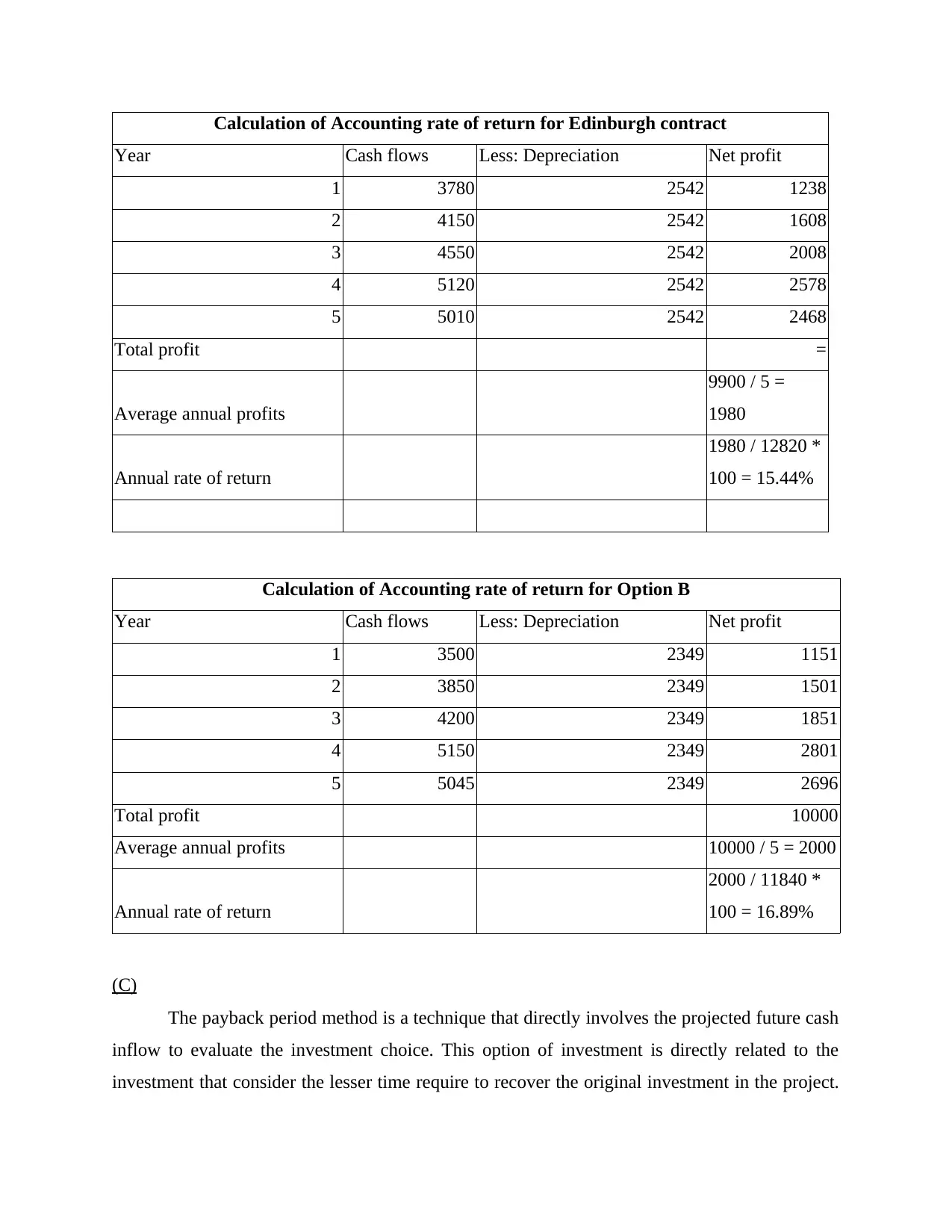

b. Calculation of accounting rate of return for Edinburgh and Newcastle upon Tyne contract

For the determination of accounting rate of return, the depreciation must be subtracted from net

cash inflows to arrive at net profits made throughout the life of the contract.

Depreciation for Edinburgh contract = Initial investment – Scrap value / expected life

= (8700 + 4120) – 110 / 5 = 2542

Depreciation for Newcastle contract = (7950 + 3890) – 95 / 5 = 2349

2 4150 7930 (4150 +

3780)

3850 7350 (3500 +

3850)

3 4550 12480 (4150 +

3780 + 4550)

4200 11550 (3500 +

3850 + 4200)

4 5120 (4150 + 3780

+ 4550 +

5120)

5150 (3500 + 3850 +

4200 + 5150)

5 4900 (4150 + 3780

+ 4550 + 5120

+ 4900)

4950

Investment 12930 (8700 +

4120 + 110)

11935 (7950 +

3890+ 95)

Edinburgh Payback period:

3 years + 450 (12930 – 12480) / 5120 * 12

= 3 years, 1.05 months

Newcastle Payback Period:

3 Years + 385 (11935 – 11550) / 5150 * 12

= 3 years, .9 months

On the basis of the payback period method the Newcastle Project is more favourable as it will

require less time to recover the original investment in comparison to the Edinburgh Project. The

technique favours such proposal of investment that seek less time to recover the original

investment.

b. Calculation of accounting rate of return for Edinburgh and Newcastle upon Tyne contract

For the determination of accounting rate of return, the depreciation must be subtracted from net

cash inflows to arrive at net profits made throughout the life of the contract.

Depreciation for Edinburgh contract = Initial investment – Scrap value / expected life

= (8700 + 4120) – 110 / 5 = 2542

Depreciation for Newcastle contract = (7950 + 3890) – 95 / 5 = 2349

Calculation of Accounting rate of return for Edinburgh contract

Year Cash flows Less: Depreciation Net profit

1 3780 2542 1238

2 4150 2542 1608

3 4550 2542 2008

4 5120 2542 2578

5 5010 2542 2468

Total profit =

Average annual profits

9900 / 5 =

1980

Annual rate of return

1980 / 12820 *

100 = 15.44%

Calculation of Accounting rate of return for Option B

Year Cash flows Less: Depreciation Net profit

1 3500 2349 1151

2 3850 2349 1501

3 4200 2349 1851

4 5150 2349 2801

5 5045 2349 2696

Total profit 10000

Average annual profits 10000 / 5 = 2000

Annual rate of return

2000 / 11840 *

100 = 16.89%

(C)

The payback period method is a technique that directly involves the projected future cash

inflow to evaluate the investment choice. This option of investment is directly related to the

investment that consider the lesser time require to recover the original investment in the project.

Year Cash flows Less: Depreciation Net profit

1 3780 2542 1238

2 4150 2542 1608

3 4550 2542 2008

4 5120 2542 2578

5 5010 2542 2468

Total profit =

Average annual profits

9900 / 5 =

1980

Annual rate of return

1980 / 12820 *

100 = 15.44%

Calculation of Accounting rate of return for Option B

Year Cash flows Less: Depreciation Net profit

1 3500 2349 1151

2 3850 2349 1501

3 4200 2349 1851

4 5150 2349 2801

5 5045 2349 2696

Total profit 10000

Average annual profits 10000 / 5 = 2000

Annual rate of return

2000 / 11840 *

100 = 16.89%

(C)

The payback period method is a technique that directly involves the projected future cash

inflow to evaluate the investment choice. This option of investment is directly related to the

investment that consider the lesser time require to recover the original investment in the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This technique is critical as it do not provide the best possible results out of the investment

decision making is taken. This technique only involve the future expected cash inflow but do not

involve the time value of money factor. This technique directly includes the expected cash

inflow but not consider the time value of money that would eventually deduct the overall price

(Azmat, Jain and Michaux, 2021). Hence, it can state clearly that this technique is not a

favourable option to select when it comes to identify the significance of investment proposal.

Further, this method or technique is more like hypothetical. As there is not any clear basis to

calculate the future cash inflow. This is all expected to assume that the organisation will be able

to derive this much amount of funds but in reality this do not sound fruitful to assume the cash

inflow. This method is critical as even after using this technique investor would have a huge

doubt in the mind about the investment decision that is made by the stakeholders. This is

important to adopt the clear method or approach to approach the investment decision. This

technique is found risky in nature when it comes to taking the investment decision as there is not

any clear mode of identifying the expected future cash inflow.

(D)

On the basis to the investment appraisal decision the option Newcastle project look more

favourable in nature. This project is deriving the better position to the organisation for recovering

the original investment cost and further supporting the organisation to generate the better

possibilities to maximise business growth (Nguyen, Gallery and Newton, 2019). Investment

appraisal decisions are usually based on how effectively and early company is capable to recover

the original investment and further to maximize the profits. The proposal will support the

organisation to generate better return against the investment is made.

Advantage of IRR:

This technique allows investor to make a suitable investment decision.

This method considers the expected cash inflow and the original investment to identify

the feasibility of investment decision making.

This technique do not influence with the size of the project.

Disadvantage of IRR:

It ignores the future cost that might involve with the project.

Opportunity cost also ignore by this method.

Reinvestment rate also ignore in this option.

decision making is taken. This technique only involve the future expected cash inflow but do not

involve the time value of money factor. This technique directly includes the expected cash

inflow but not consider the time value of money that would eventually deduct the overall price

(Azmat, Jain and Michaux, 2021). Hence, it can state clearly that this technique is not a

favourable option to select when it comes to identify the significance of investment proposal.

Further, this method or technique is more like hypothetical. As there is not any clear basis to

calculate the future cash inflow. This is all expected to assume that the organisation will be able

to derive this much amount of funds but in reality this do not sound fruitful to assume the cash

inflow. This method is critical as even after using this technique investor would have a huge

doubt in the mind about the investment decision that is made by the stakeholders. This is

important to adopt the clear method or approach to approach the investment decision. This

technique is found risky in nature when it comes to taking the investment decision as there is not

any clear mode of identifying the expected future cash inflow.

(D)

On the basis to the investment appraisal decision the option Newcastle project look more

favourable in nature. This project is deriving the better position to the organisation for recovering

the original investment cost and further supporting the organisation to generate the better

possibilities to maximise business growth (Nguyen, Gallery and Newton, 2019). Investment

appraisal decisions are usually based on how effectively and early company is capable to recover

the original investment and further to maximize the profits. The proposal will support the

organisation to generate better return against the investment is made.

Advantage of IRR:

This technique allows investor to make a suitable investment decision.

This method considers the expected cash inflow and the original investment to identify

the feasibility of investment decision making.

This technique do not influence with the size of the project.

Disadvantage of IRR:

It ignores the future cost that might involve with the project.

Opportunity cost also ignore by this method.

Reinvestment rate also ignore in this option.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Many time this method provide the complicated result hence even after using this

technique there is a doubt would always remain in the mind of investor about feasibility

of investment choice.

Question: 3

a. Concept of contribution and its importance in CVP technique

The concept of contribution has a very special and significant meaning in CVP technique.

It is calculated by considering a certain level of production where the variable costs of a product

or service has been deducted from the selling price associated with that product or service

(Thom, 2019). Thus, the formula of contribution is as follows:

Contribution = Selling price per unit of a product or service – variable costs per unit of a prouct

or service.

The meaning of contribution can be described in terms of how much contribution each of

the unit produced and sold is making towards covering fixed costs of the operations and also

towards generating profits.

For instance, if the selling price per unit of the product(x) is equivalent to £21 and

variable costs per unit include £7 direct material, £5 direct labour, £3 direct expenses and £3 as

variable overheads. Therefore, to determine the contribution made by each unit of x sold towards

fixed costs and profit would be calculated as follows:

Contribution = Selling price per unit (21) – variable cost per unit (7 + 5 + 3 + 3) = £3

Importance in CVP technique

Within CVP technique, it is determined that how much minimum sales must be made of a

product to recover the fixed costs associated with that product to identify the level at which

business will break – even (Irena and Mariana, 2017). The profitability of the business can be

ensured by comparing fixed costs and contribution margin of the business as the former must be

lower than the latter. The CVP technique takes into account three major factors that is, cost,

volume and profit. It helps in determining the movement in costs and profit at different level of

volume. As a result, an optimum output can be determined for the business that leads to

maximum profits and minimum costs. The contribution here helps in deciding how much a

product is contributing towards the fixed costs and subsequently towards the profit of the

business to determine whether to continue with the production or not.

technique there is a doubt would always remain in the mind of investor about feasibility

of investment choice.

Question: 3

a. Concept of contribution and its importance in CVP technique

The concept of contribution has a very special and significant meaning in CVP technique.

It is calculated by considering a certain level of production where the variable costs of a product

or service has been deducted from the selling price associated with that product or service

(Thom, 2019). Thus, the formula of contribution is as follows:

Contribution = Selling price per unit of a product or service – variable costs per unit of a prouct

or service.

The meaning of contribution can be described in terms of how much contribution each of

the unit produced and sold is making towards covering fixed costs of the operations and also

towards generating profits.

For instance, if the selling price per unit of the product(x) is equivalent to £21 and

variable costs per unit include £7 direct material, £5 direct labour, £3 direct expenses and £3 as

variable overheads. Therefore, to determine the contribution made by each unit of x sold towards

fixed costs and profit would be calculated as follows:

Contribution = Selling price per unit (21) – variable cost per unit (7 + 5 + 3 + 3) = £3

Importance in CVP technique

Within CVP technique, it is determined that how much minimum sales must be made of a

product to recover the fixed costs associated with that product to identify the level at which

business will break – even (Irena and Mariana, 2017). The profitability of the business can be

ensured by comparing fixed costs and contribution margin of the business as the former must be

lower than the latter. The CVP technique takes into account three major factors that is, cost,

volume and profit. It helps in determining the movement in costs and profit at different level of

volume. As a result, an optimum output can be determined for the business that leads to

maximum profits and minimum costs. The contribution here helps in deciding how much a

product is contributing towards the fixed costs and subsequently towards the profit of the

business to determine whether to continue with the production or not.

b. Nature of decisions 'dropping a product or service' and 'special contracts'

CVP technique is useful for many reasons and also helps in making major decision

related to business which include how to optimize the level of output, whether to continue with

the same product or drop it or make modifications, how much should be the selling price of the

product, minimum sales necessary to be made for ensuring business profitability, etc. Here, the

nature of two major decisions (dropping a product or service and entering into a special contract)

that are facilitated by CVP technique will be discussed, which is as follows:

Dropping a product or service: One of the most important decision that can be made with the

help of CVP technique is to evaluate whether the department or a product or service required to

be discontinued or not (MUKTIADJI and et.al., 2020). This decision is made on the basis of

costs involved in the process of making that product available to the final consumers and

comparing it with the final profit remained with the business. When the costs outweigh the

revenues generated and the business is not able to recover its costs, then it is necessary to drop

them. CVP technique facilitates this type of decision – making where if the results shows that at

no level of output the costs of operations can be recovered, then such product should be dropped

at the earliest.

Special contracts: During the business operations, it may occur that a special order can be

received for the sale of product which is not budgeted for. In such case, there is an opportunity to

increase the sales revenue but the contract is accompanied by a request for selling it at a lower

than the price it is being currently available (Zhang and Zhu, 2020). At this moment, it is must

for the business to consider whether the product is still profitable or not if the lower price

contract has been executed. For such evaluation and decision-making, it is necessary to have

knowledge of CVP technique to arrive at a decision whether the special order should be accepted

or not.

c. Critical evaluation of CVP technique and its limitations

CVP techniques is used for many purposes such as for setting the optimal and competitive

selling price of the product, determining appropriate product mix, maximizing the usage of

production facilities and finally it helps in evaluating the effect of volume and costs on the final

profit of the concern. However, there are certain limitations to this technique that is:

Limitations offered by economist's model

CVP technique is useful for many reasons and also helps in making major decision

related to business which include how to optimize the level of output, whether to continue with

the same product or drop it or make modifications, how much should be the selling price of the

product, minimum sales necessary to be made for ensuring business profitability, etc. Here, the

nature of two major decisions (dropping a product or service and entering into a special contract)

that are facilitated by CVP technique will be discussed, which is as follows:

Dropping a product or service: One of the most important decision that can be made with the

help of CVP technique is to evaluate whether the department or a product or service required to

be discontinued or not (MUKTIADJI and et.al., 2020). This decision is made on the basis of

costs involved in the process of making that product available to the final consumers and

comparing it with the final profit remained with the business. When the costs outweigh the

revenues generated and the business is not able to recover its costs, then it is necessary to drop

them. CVP technique facilitates this type of decision – making where if the results shows that at

no level of output the costs of operations can be recovered, then such product should be dropped

at the earliest.

Special contracts: During the business operations, it may occur that a special order can be

received for the sale of product which is not budgeted for. In such case, there is an opportunity to

increase the sales revenue but the contract is accompanied by a request for selling it at a lower

than the price it is being currently available (Zhang and Zhu, 2020). At this moment, it is must

for the business to consider whether the product is still profitable or not if the lower price

contract has been executed. For such evaluation and decision-making, it is necessary to have

knowledge of CVP technique to arrive at a decision whether the special order should be accepted

or not.

c. Critical evaluation of CVP technique and its limitations

CVP techniques is used for many purposes such as for setting the optimal and competitive

selling price of the product, determining appropriate product mix, maximizing the usage of

production facilities and finally it helps in evaluating the effect of volume and costs on the final

profit of the concern. However, there are certain limitations to this technique that is:

Limitations offered by economist's model

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable cost per unit declines initially with the expansion in production which indicates

labour efficiency as they learn production techniques (Yuniningsih, Pertiwi and

Purwanto, 2019). Also, there would be higher returns to scale due to achieving economies

of scale resulting from bulk buying. Subsequently, rise in variable costs experienced with

the output approaching capacity which results in breakdowns and bottlenecks. Therefore,

CVP technique fails to generate results in such scenarios. Selling price of the product required to be lower down for achieving higher sales and

can't be kept constant.

Other limitations of CVP technique

It is not normally true where the units produced gets sold in the same decision period.

In practice, it is not easy to accurately categorize fixed and variable costs.

Fixed cost do not change from the relevant range during the same decision period.

CVP technique takes into account only a single product or service while in reality, there

are multiple products in which business deals (Caruana and et.al., 2019). Therefore, there

is always an impact of performance of products on one another which is not considered

by CVP technique.

Question : 4

a. Preparation of Opening statement of financial position for Fashion Clothing at the start of July

2015

Statement of financial position as at July 2015

Particulars Amount in £

Tangible Non current assets 150000

Current assets

Bank balance 50000

Total Assets 200000

Liabilities and capital

Capital 200000

labour efficiency as they learn production techniques (Yuniningsih, Pertiwi and

Purwanto, 2019). Also, there would be higher returns to scale due to achieving economies

of scale resulting from bulk buying. Subsequently, rise in variable costs experienced with

the output approaching capacity which results in breakdowns and bottlenecks. Therefore,

CVP technique fails to generate results in such scenarios. Selling price of the product required to be lower down for achieving higher sales and

can't be kept constant.

Other limitations of CVP technique

It is not normally true where the units produced gets sold in the same decision period.

In practice, it is not easy to accurately categorize fixed and variable costs.

Fixed cost do not change from the relevant range during the same decision period.

CVP technique takes into account only a single product or service while in reality, there

are multiple products in which business deals (Caruana and et.al., 2019). Therefore, there

is always an impact of performance of products on one another which is not considered

by CVP technique.

Question : 4

a. Preparation of Opening statement of financial position for Fashion Clothing at the start of July

2015

Statement of financial position as at July 2015

Particulars Amount in £

Tangible Non current assets 150000

Current assets

Bank balance 50000

Total Assets 200000

Liabilities and capital

Capital 200000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

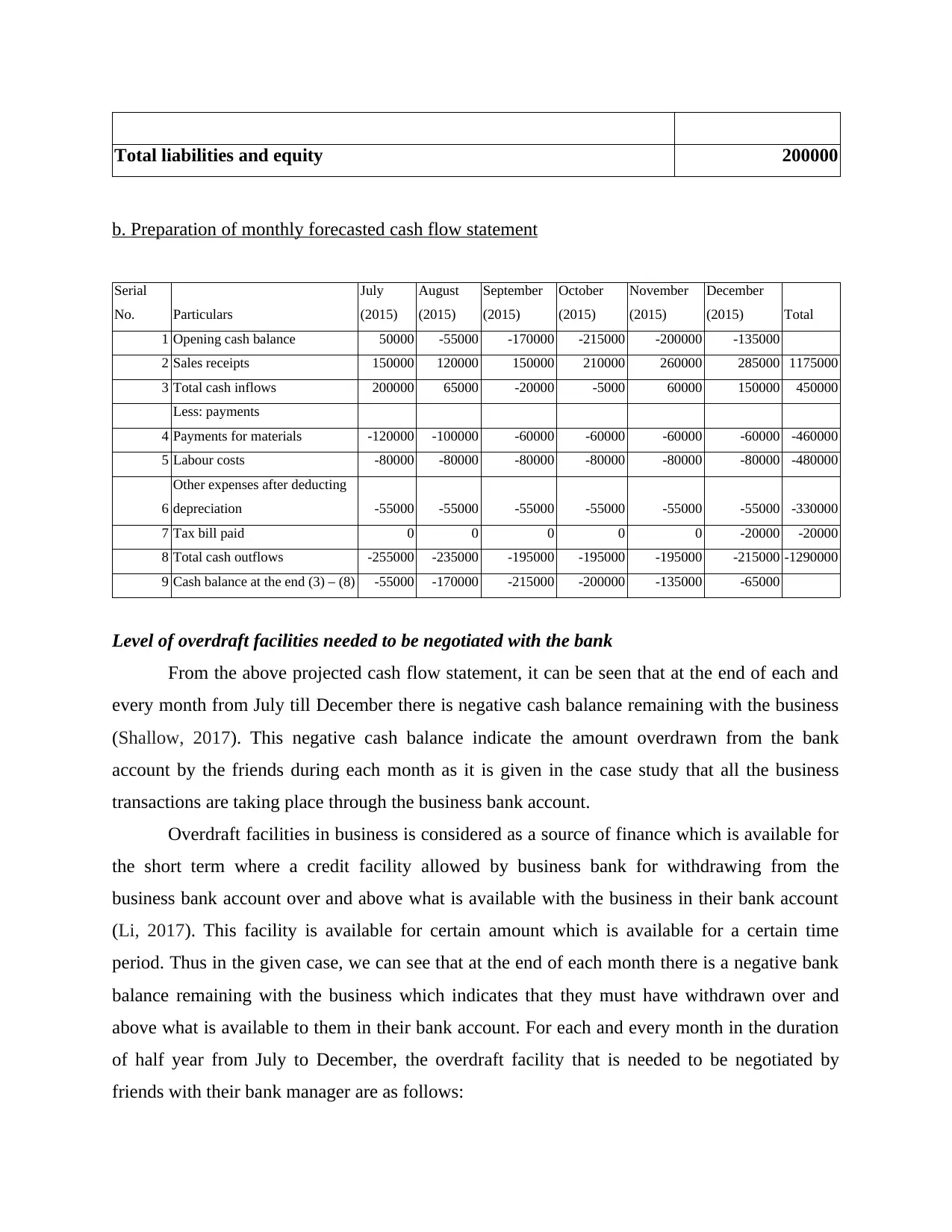

Total liabilities and equity 200000

b. Preparation of monthly forecasted cash flow statement

Serial

No. Particulars

July

(2015)

August

(2015)

September

(2015)

October

(2015)

November

(2015)

December

(2015) Total

1 Opening cash balance 50000 -55000 -170000 -215000 -200000 -135000

2 Sales receipts 150000 120000 150000 210000 260000 285000 1175000

3 Total cash inflows 200000 65000 -20000 -5000 60000 150000 450000

Less: payments

4 Payments for materials -120000 -100000 -60000 -60000 -60000 -60000 -460000

5 Labour costs -80000 -80000 -80000 -80000 -80000 -80000 -480000

6

Other expenses after deducting

depreciation -55000 -55000 -55000 -55000 -55000 -55000 -330000

7 Tax bill paid 0 0 0 0 0 -20000 -20000

8 Total cash outflows -255000 -235000 -195000 -195000 -195000 -215000 -1290000

9 Cash balance at the end (3) – (8) -55000 -170000 -215000 -200000 -135000 -65000

Level of overdraft facilities needed to be negotiated with the bank

From the above projected cash flow statement, it can be seen that at the end of each and

every month from July till December there is negative cash balance remaining with the business

(Shallow, 2017). This negative cash balance indicate the amount overdrawn from the bank

account by the friends during each month as it is given in the case study that all the business

transactions are taking place through the business bank account.

Overdraft facilities in business is considered as a source of finance which is available for

the short term where a credit facility allowed by business bank for withdrawing from the

business bank account over and above what is available with the business in their bank account

(Li, 2017). This facility is available for certain amount which is available for a certain time

period. Thus in the given case, we can see that at the end of each month there is a negative bank

balance remaining with the business which indicates that they must have withdrawn over and

above what is available to them in their bank account. For each and every month in the duration

of half year from July to December, the overdraft facility that is needed to be negotiated by

friends with their bank manager are as follows:

b. Preparation of monthly forecasted cash flow statement

Serial

No. Particulars

July

(2015)

August

(2015)

September

(2015)

October

(2015)

November

(2015)

December

(2015) Total

1 Opening cash balance 50000 -55000 -170000 -215000 -200000 -135000

2 Sales receipts 150000 120000 150000 210000 260000 285000 1175000

3 Total cash inflows 200000 65000 -20000 -5000 60000 150000 450000

Less: payments

4 Payments for materials -120000 -100000 -60000 -60000 -60000 -60000 -460000

5 Labour costs -80000 -80000 -80000 -80000 -80000 -80000 -480000

6

Other expenses after deducting

depreciation -55000 -55000 -55000 -55000 -55000 -55000 -330000

7 Tax bill paid 0 0 0 0 0 -20000 -20000

8 Total cash outflows -255000 -235000 -195000 -195000 -195000 -215000 -1290000

9 Cash balance at the end (3) – (8) -55000 -170000 -215000 -200000 -135000 -65000

Level of overdraft facilities needed to be negotiated with the bank

From the above projected cash flow statement, it can be seen that at the end of each and

every month from July till December there is negative cash balance remaining with the business

(Shallow, 2017). This negative cash balance indicate the amount overdrawn from the bank

account by the friends during each month as it is given in the case study that all the business

transactions are taking place through the business bank account.

Overdraft facilities in business is considered as a source of finance which is available for

the short term where a credit facility allowed by business bank for withdrawing from the

business bank account over and above what is available with the business in their bank account

(Li, 2017). This facility is available for certain amount which is available for a certain time

period. Thus in the given case, we can see that at the end of each month there is a negative bank

balance remaining with the business which indicates that they must have withdrawn over and

above what is available to them in their bank account. For each and every month in the duration

of half year from July to December, the overdraft facility that is needed to be negotiated by

friends with their bank manager are as follows:

At the end of July 2015 = £50000 is needed to be negotiated with the bank manager. In

the same way at the end of August 2015 negotiation would be £170000, for the month of

September 2015 it would be £215000, for the month of October £200000, November £135000

and at the end of December £65000 needed to be negotiated with the bank manager to avail

overdraft facilities.

Therefore, projected cash flow has been drawn to determine the amount by which

shortfalls would be occurred for the upcoming six months (Caruana and et.al., 2019.). So that,

short term financing can be arranged with the bank in terms of overdraft facility to finance such

liquidity shortfalls in advance.

c)

Overdraft facilities when negotiated with the bank always results in additional costs for the

business. Therefore, an interest charges must be taken into account by business's management

team which they required to pay for availing overdraft facility (Irena and Mariana, 2017). The

charges applied are quite lower than other short term sources of finance and business needed to

pay such charges just for the duration for which the amount remains outstanding. In the given

case, it can be seen that overdraft facilities are needed to be availed at the end of each month and

this will results in additional interest charges (at a rate fixed by business's bank) for the duration

for which it will remain negative.

the same way at the end of August 2015 negotiation would be £170000, for the month of

September 2015 it would be £215000, for the month of October £200000, November £135000

and at the end of December £65000 needed to be negotiated with the bank manager to avail

overdraft facilities.

Therefore, projected cash flow has been drawn to determine the amount by which

shortfalls would be occurred for the upcoming six months (Caruana and et.al., 2019.). So that,

short term financing can be arranged with the bank in terms of overdraft facility to finance such

liquidity shortfalls in advance.

c)

Overdraft facilities when negotiated with the bank always results in additional costs for the

business. Therefore, an interest charges must be taken into account by business's management

team which they required to pay for availing overdraft facility (Irena and Mariana, 2017). The

charges applied are quite lower than other short term sources of finance and business needed to

pay such charges just for the duration for which the amount remains outstanding. In the given

case, it can be seen that overdraft facilities are needed to be availed at the end of each month and

this will results in additional interest charges (at a rate fixed by business's bank) for the duration

for which it will remain negative.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.