Finance Portfolio Management Report: GSK and RB Performance

VerifiedAdded on 2022/09/08

|22

|4277

|21

Report

AI Summary

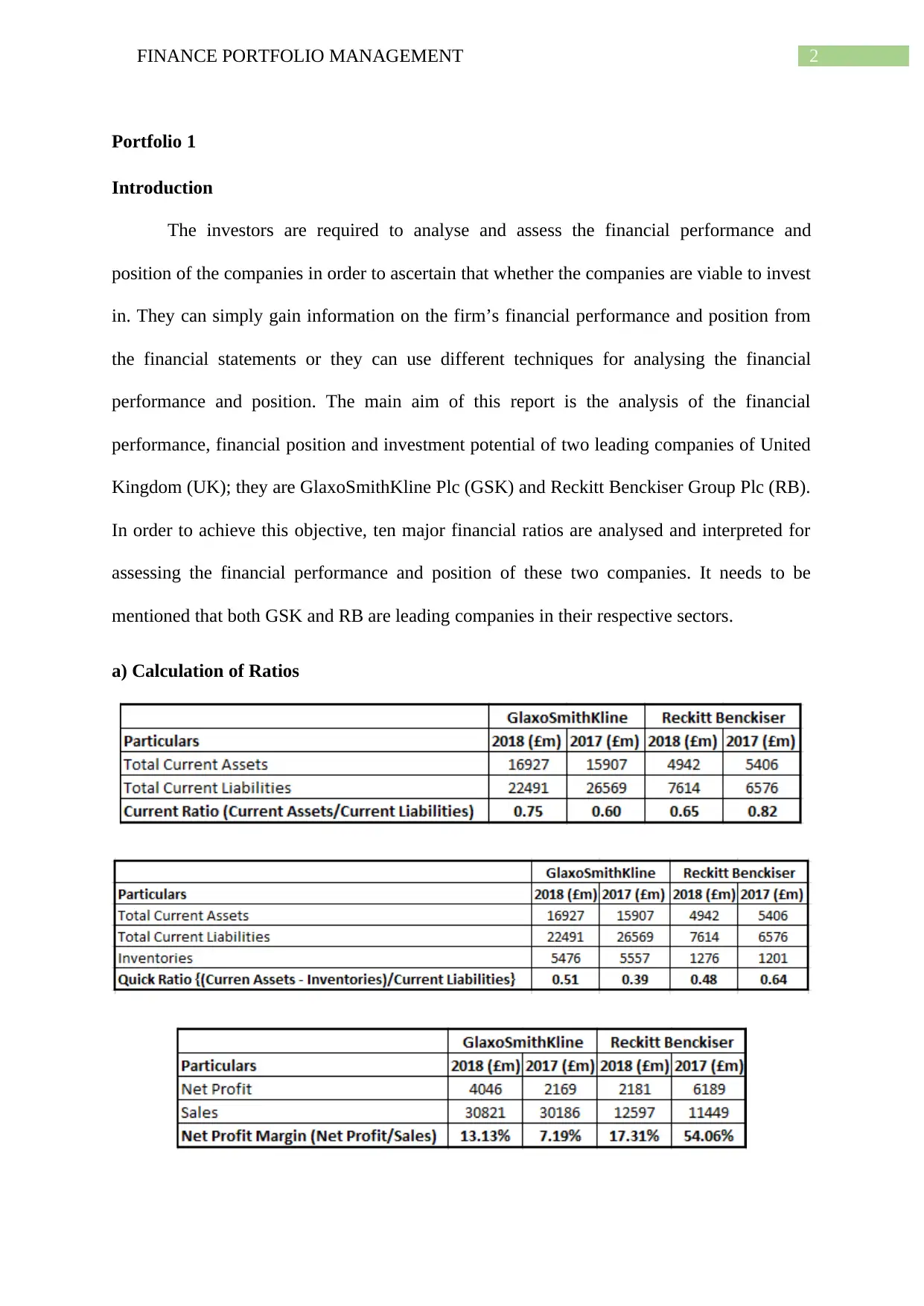

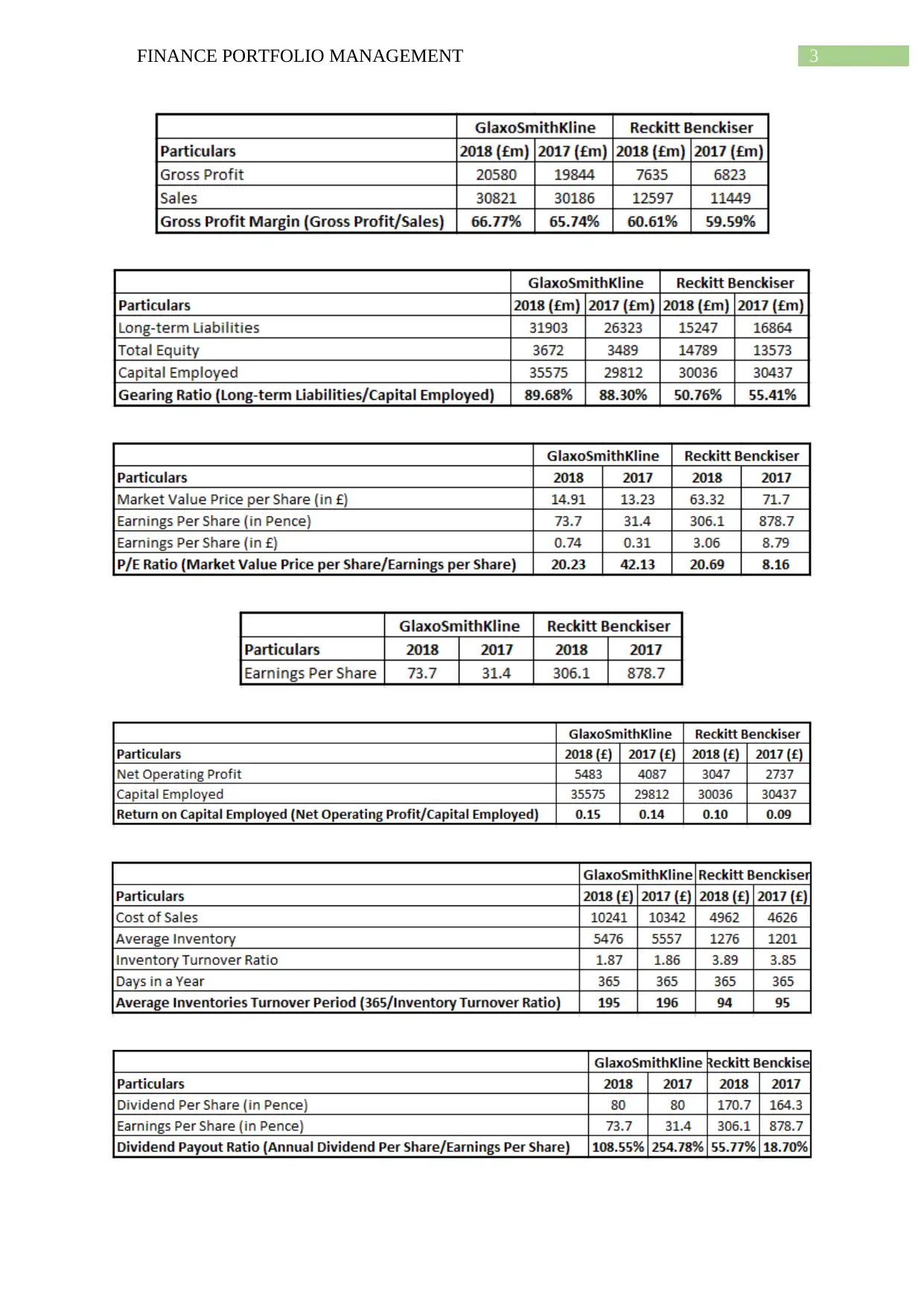

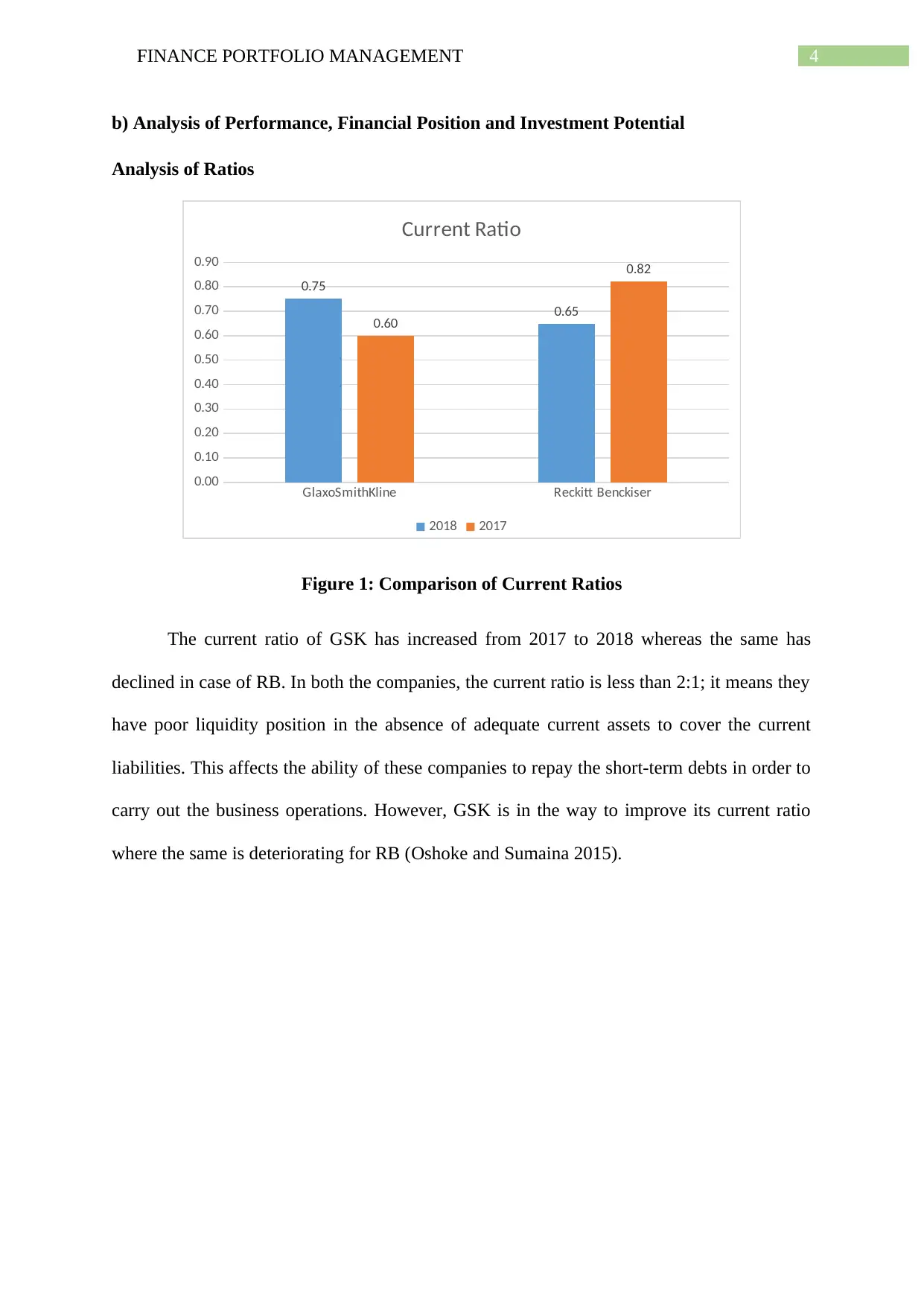

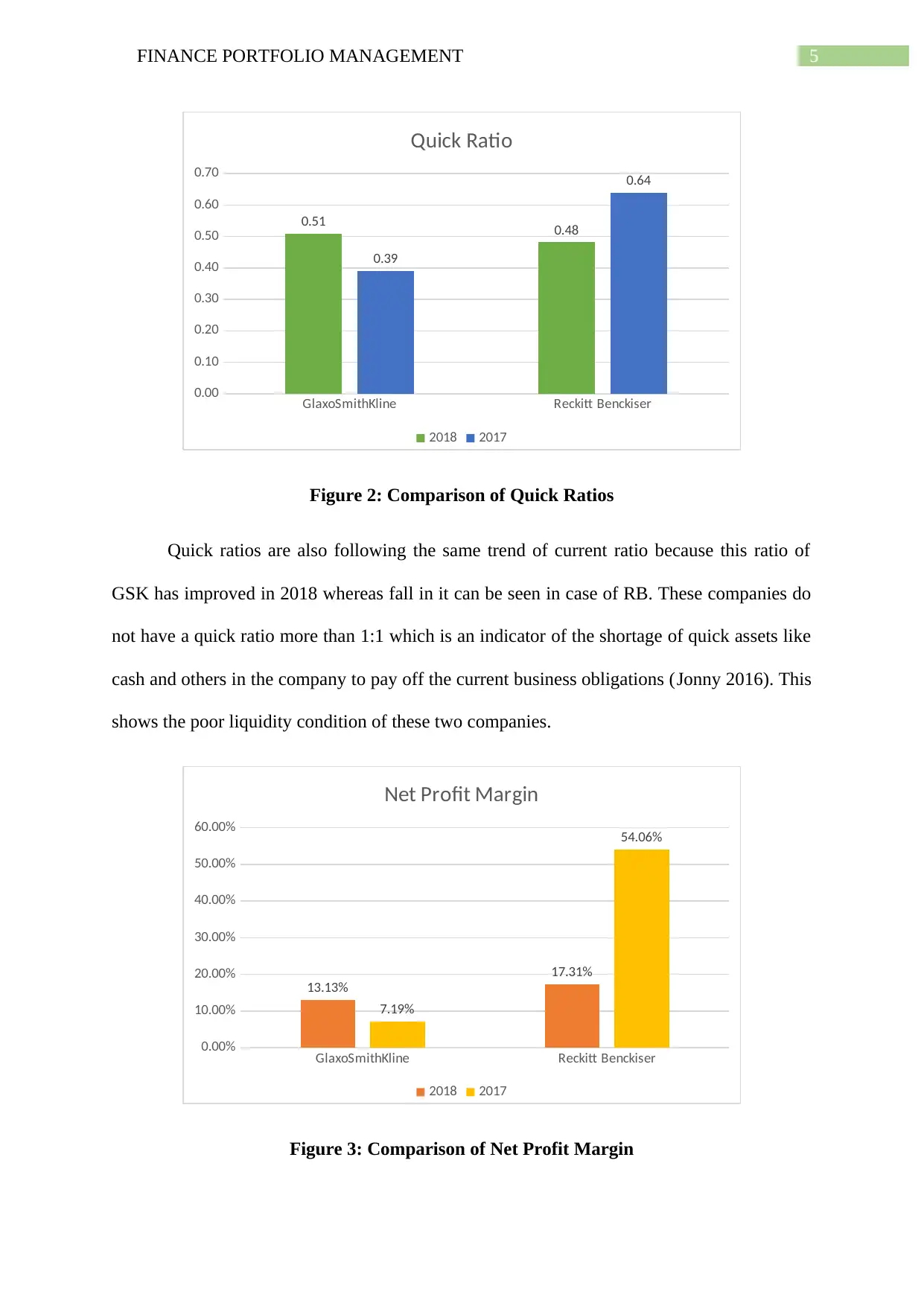

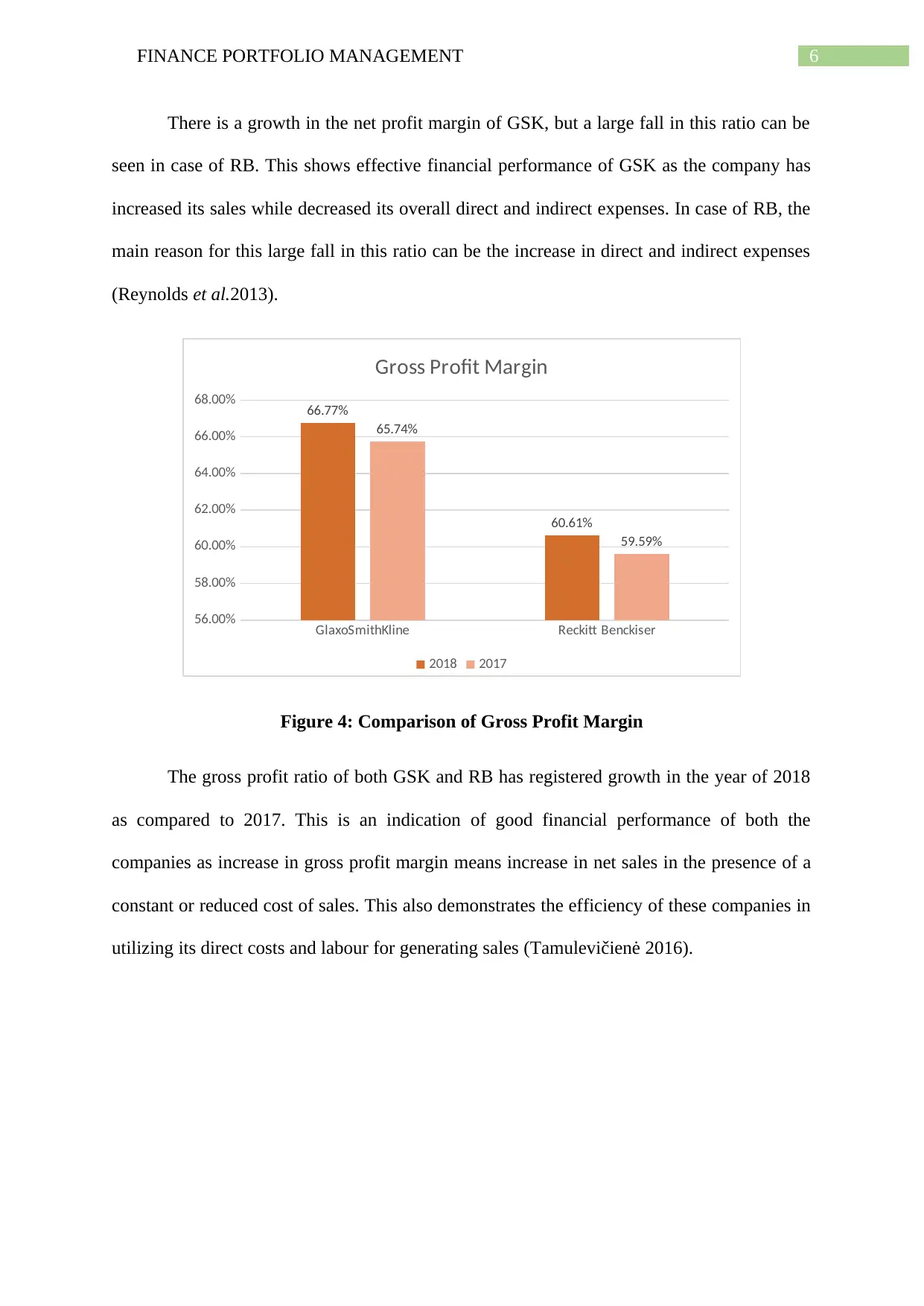

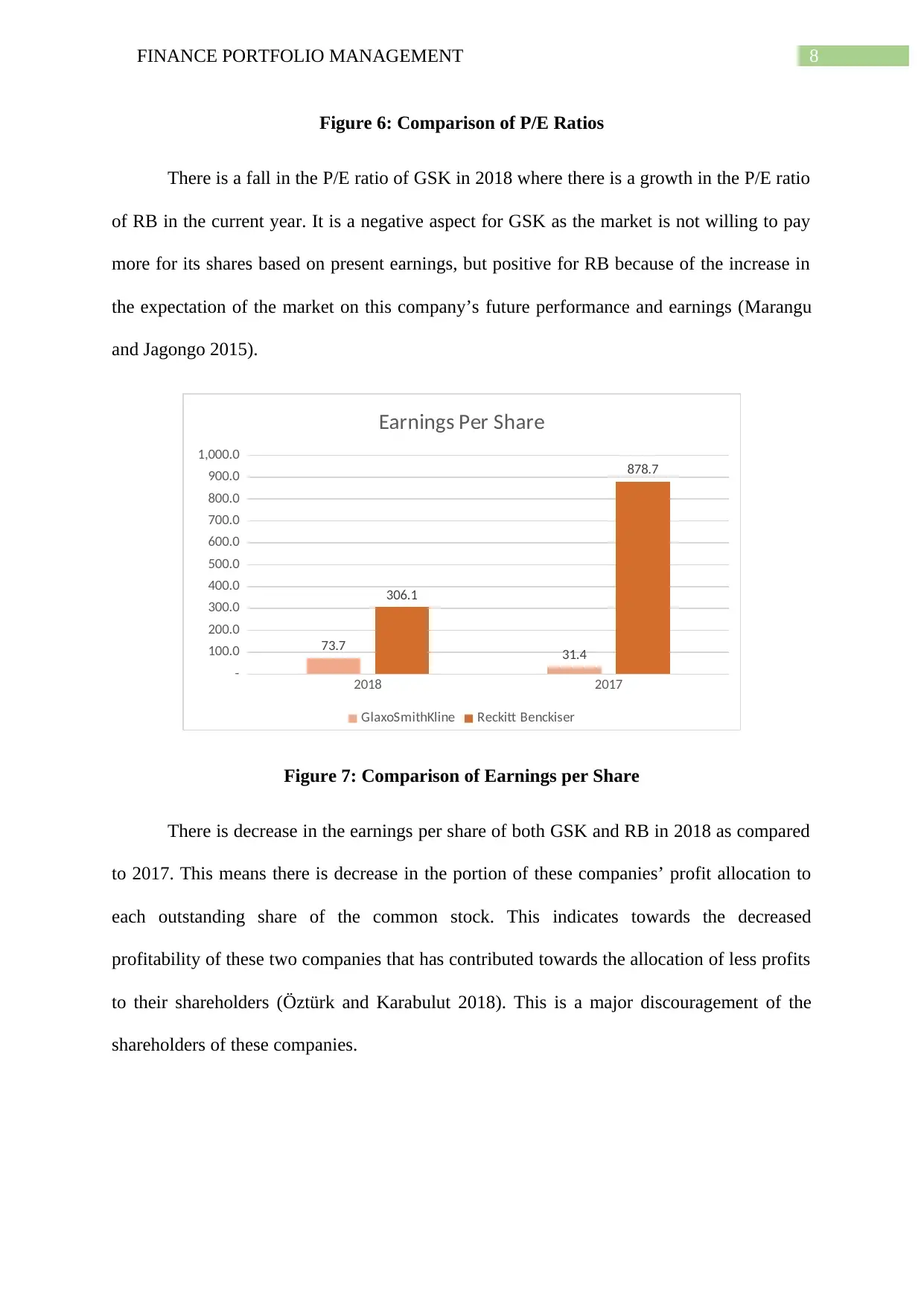

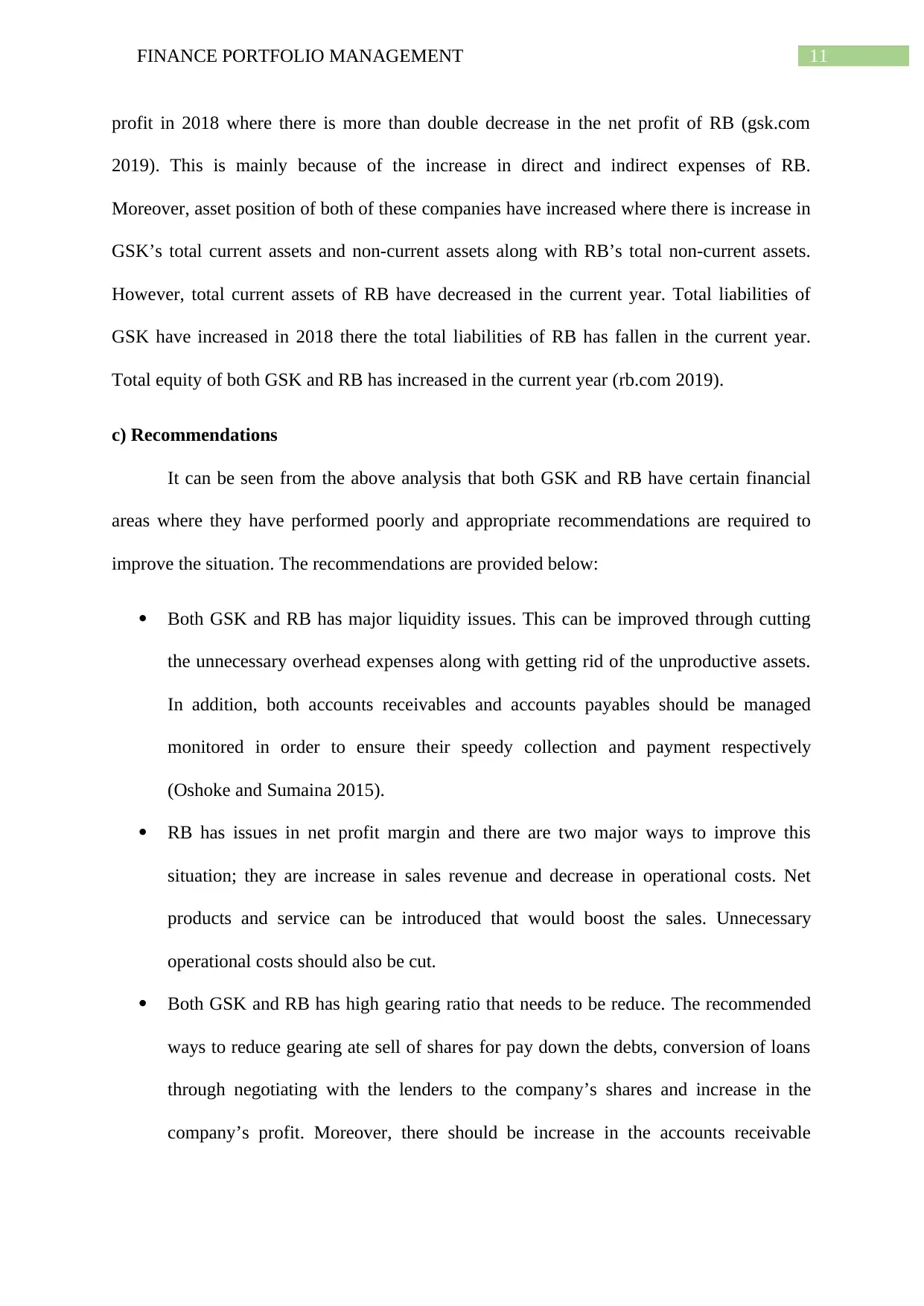

This report provides a comprehensive analysis of the financial performance, financial position, and investment potential of two leading UK companies, GlaxoSmithKline Plc (GSK) and Reckitt Benckiser Group Plc (RB). The analysis involves calculating and interpreting ten major financial ratios to assess liquidity, profitability, and gearing. The report compares the performance of both companies from 2017 to 2018, highlighting trends in current ratios, quick ratios, net profit margin, gross profit margin, gearing ratios, P/E ratios, earnings per share, return on capital employed, average inventories turnover period, and dividend pay-out ratios. Additionally, it reviews audited financial statements and offers recommendations for improvement, focusing on addressing liquidity issues, enhancing net profit margins, reducing gearing ratios, and improving earnings per share. The report also discusses the limitations of relying on financial ratios for company performance interpretation.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.