Finance Homework Assignment

VerifiedAdded on 2020/02/24

|5

|446

|218

Homework Assignment

AI Summary

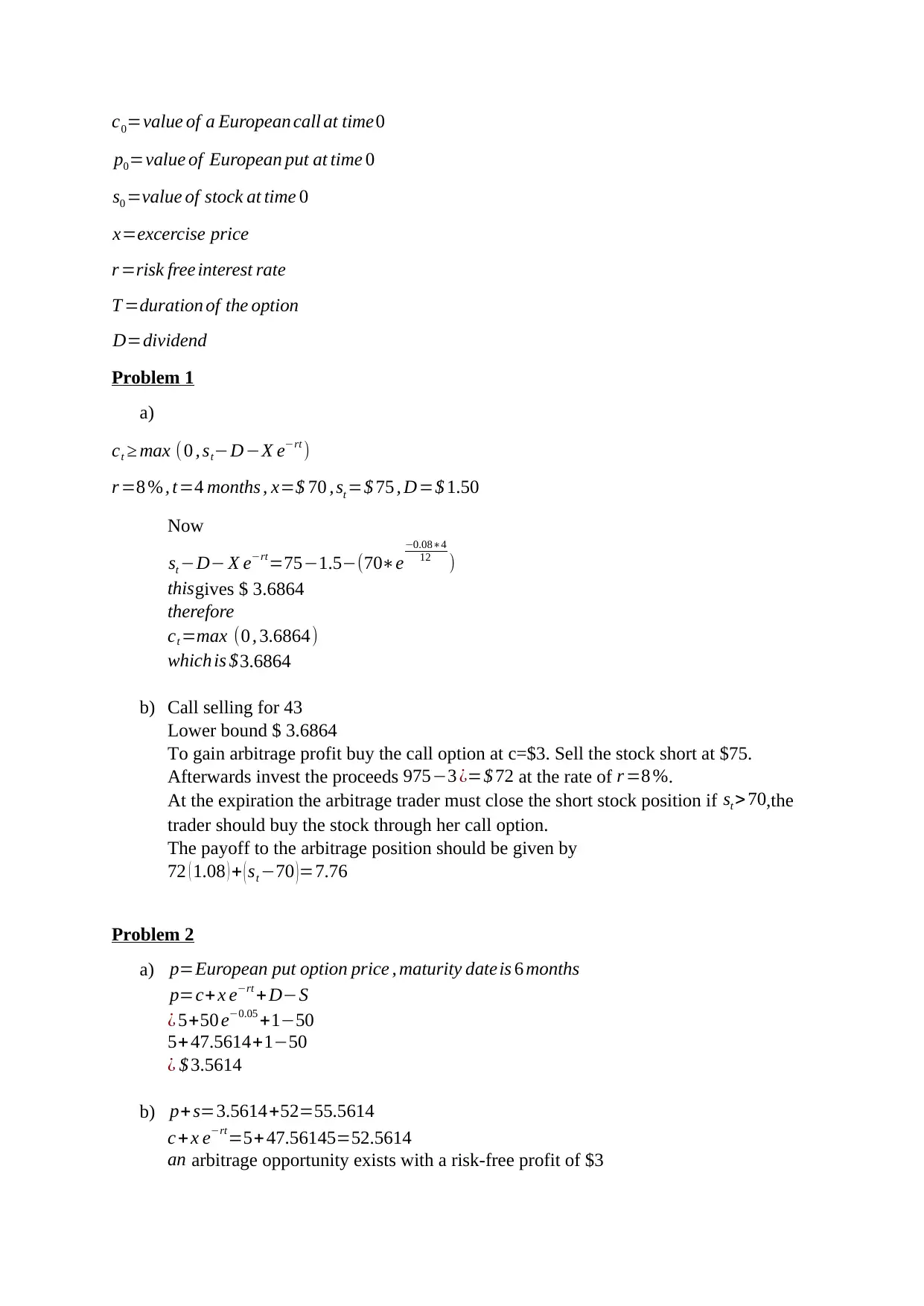

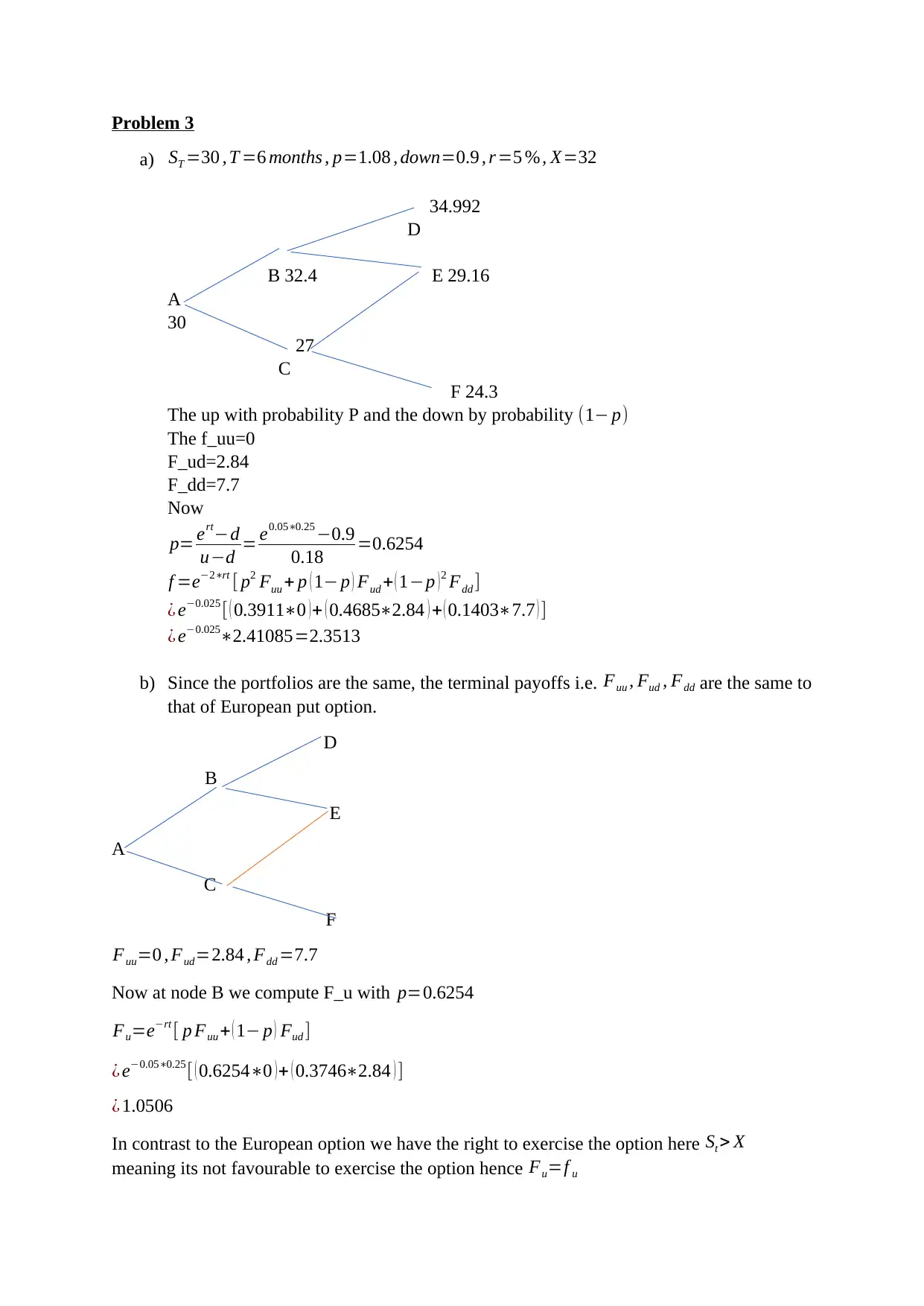

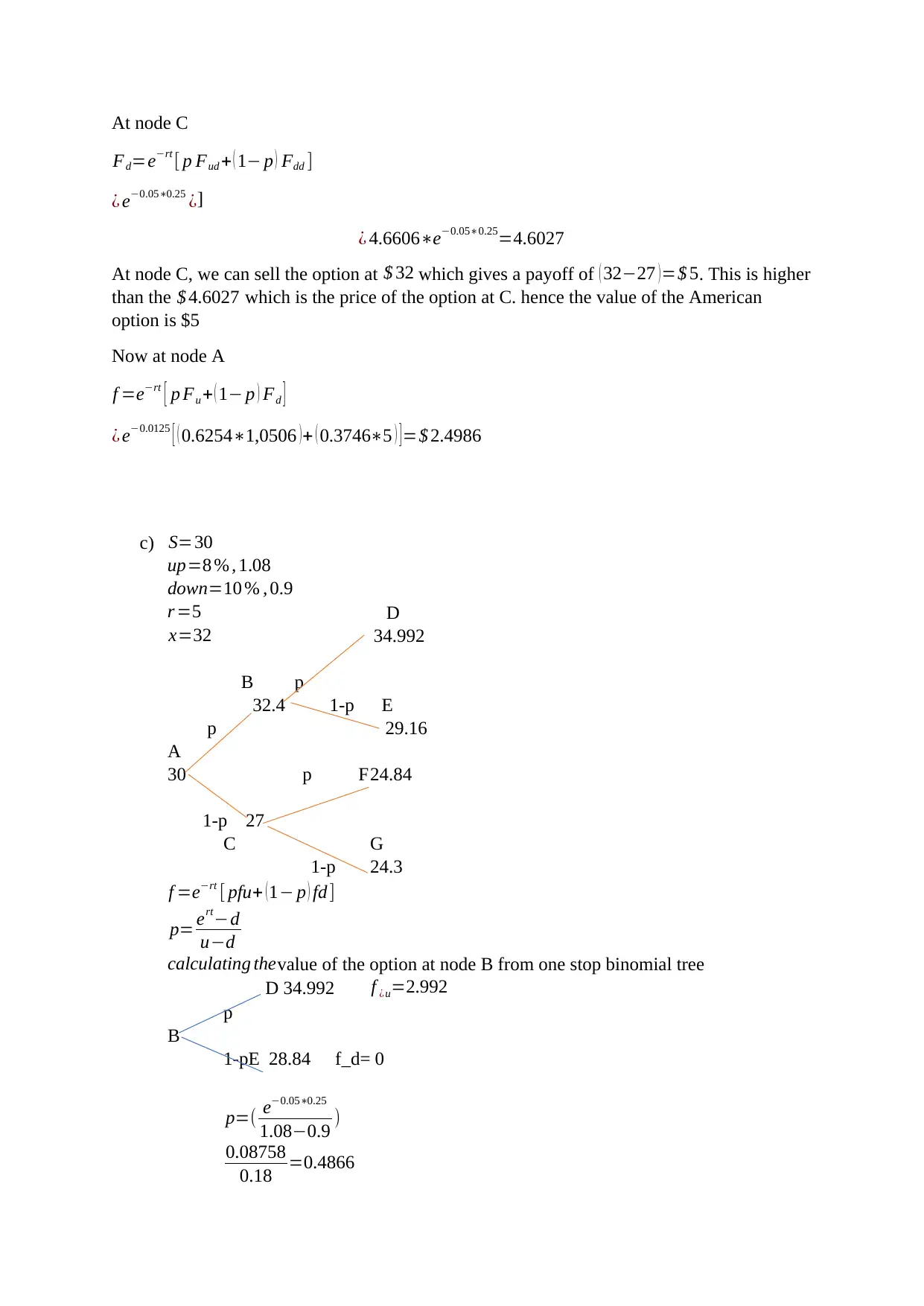

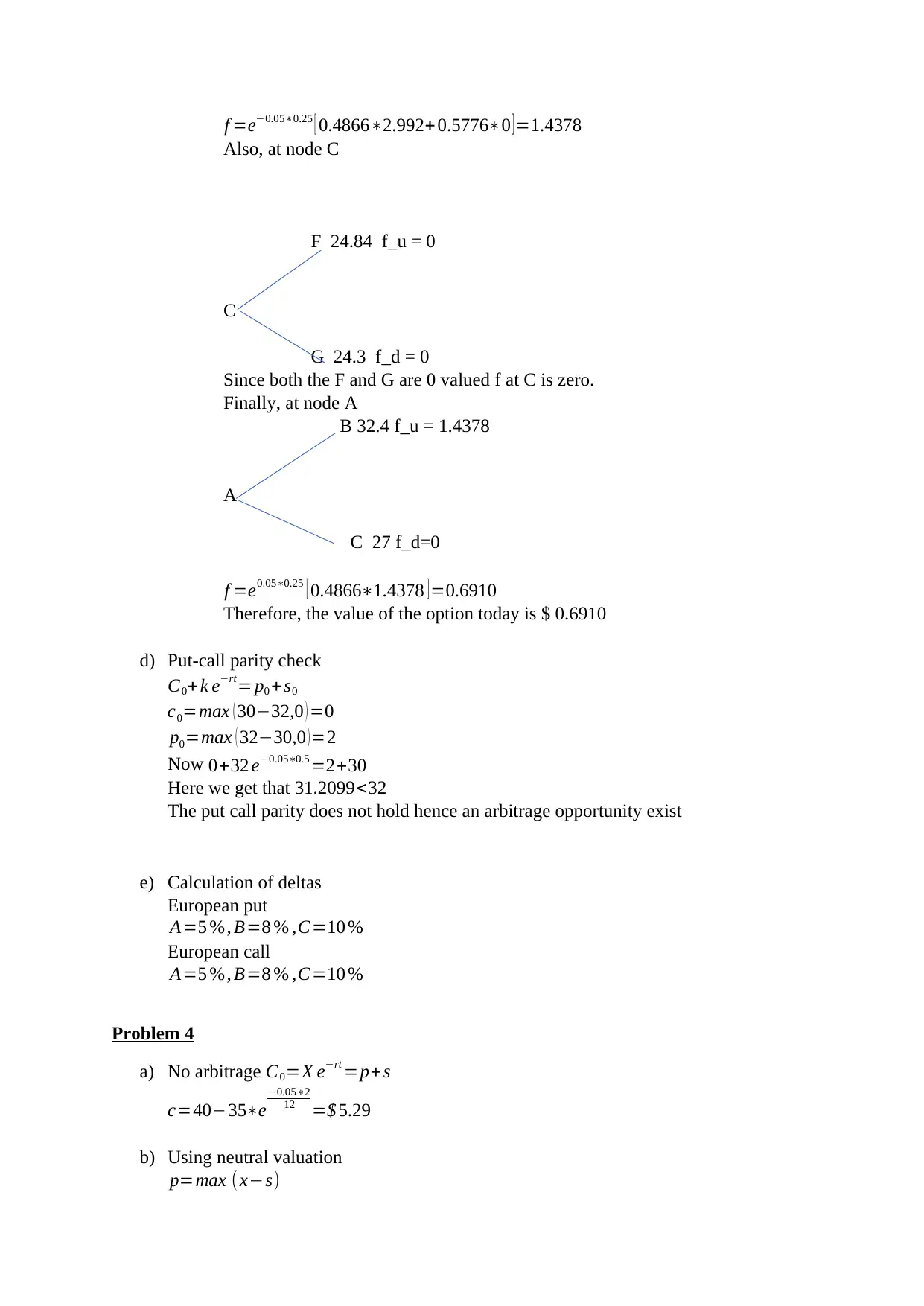

This assignment focuses on various problems related to arbitrage opportunities and option pricing, including European and American options, put-call parity, and the use of Excel for calculations. It emphasizes the importance of understanding financial derivatives and the implications of different pricing strategies.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.