University Cost Accounting Assignment: UGB 106 Homework

VerifiedAdded on 2023/01/10

|10

|2081

|100

Homework Assignment

AI Summary

This document presents a comprehensive solution to a cost accounting assignment, addressing key concepts such as contribution margin, breakeven analysis, and variance analysis. The solution begins with a detailed calculation of contribution, followed by the determination of breakeven points under different scenarios. The assignment further explores profit calculations based on varying sales volumes and selling prices. It then delves into overhead cost allocation, calculating overhead cost rates for different departments and analyzing the total production costs. The solution also examines standard costing, including the calculation of various variances, such as purchase price variance, material yield variance, labor rate variance, and labor efficiency variance. Finally, it provides an evaluation of a strategic decision and a columnar statement of budgets and variances. The document offers a complete guide to understanding and solving cost accounting problems, with references to relevant academic sources.

UGB 106

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MAIN BODY..................................................................................................................................3

QUESTION 2..................................................................................................................................3

(a).................................................................................................................................................3

(b).................................................................................................................................................3

(c).................................................................................................................................................3

(d).................................................................................................................................................3

(e).................................................................................................................................................4

(f).................................................................................................................................................4

QUESTION 3..................................................................................................................................5

(a).................................................................................................................................................5

(b).................................................................................................................................................6

(c).................................................................................................................................................6

QUESTION 4..................................................................................................................................7

(a) Columnar statement of budgets and variances.......................................................................7

(b).................................................................................................................................................7

(c).................................................................................................................................................8

REFERENCES................................................................................................................................9

MAIN BODY..................................................................................................................................3

QUESTION 2..................................................................................................................................3

(a).................................................................................................................................................3

(b).................................................................................................................................................3

(c).................................................................................................................................................3

(d).................................................................................................................................................3

(e).................................................................................................................................................4

(f).................................................................................................................................................4

QUESTION 3..................................................................................................................................5

(a).................................................................................................................................................5

(b).................................................................................................................................................6

(c).................................................................................................................................................6

QUESTION 4..................................................................................................................................7

(a) Columnar statement of budgets and variances.......................................................................7

(b).................................................................................................................................................7

(c).................................................................................................................................................8

REFERENCES................................................................................................................................9

MAIN BODY

QUESTION 2

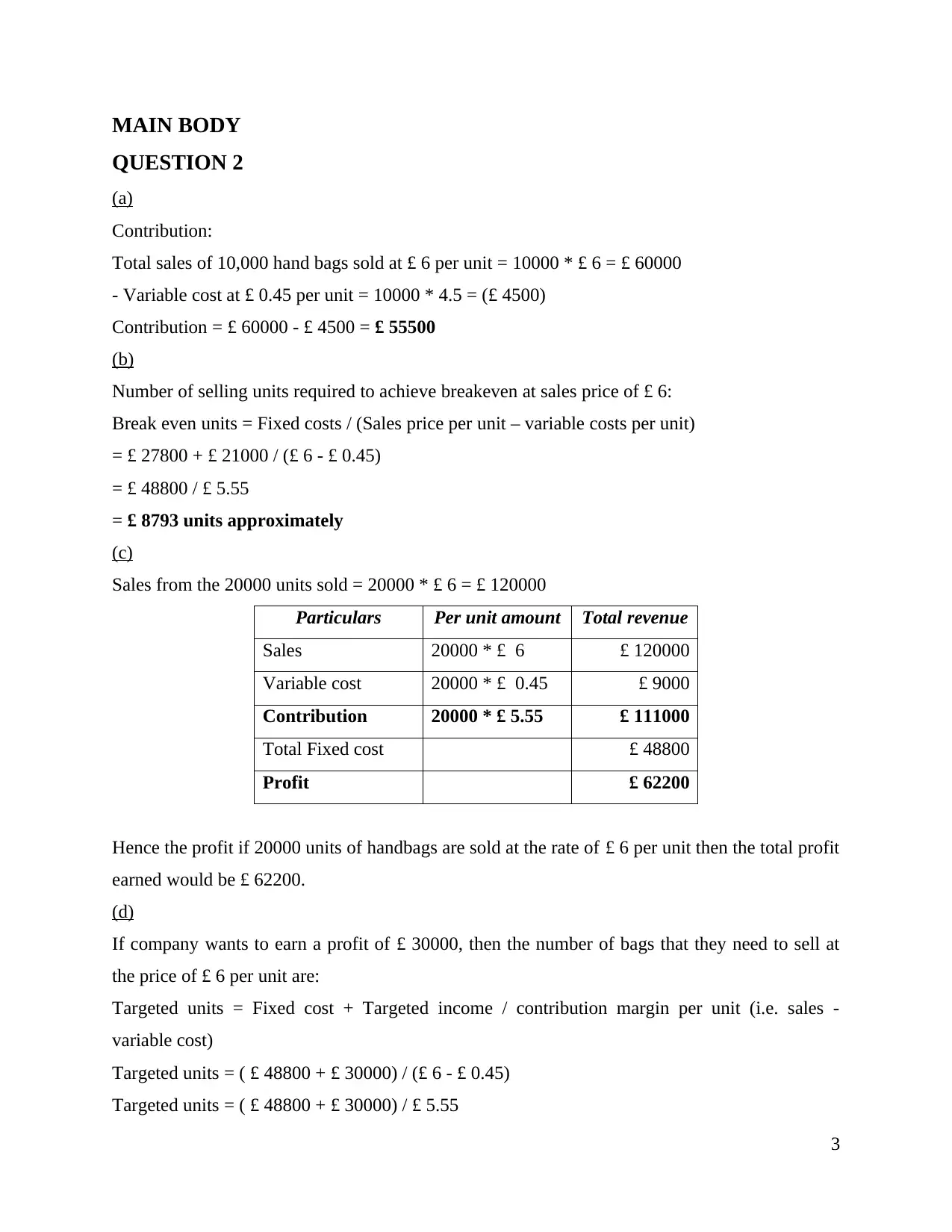

(a)

Contribution:

Total sales of 10,000 hand bags sold at £ 6 per unit = 10000 * £ 6 = £ 60000

- Variable cost at £ 0.45 per unit = 10000 * 4.5 = (£ 4500)

Contribution = £ 60000 - £ 4500 = £ 55500

(b)

Number of selling units required to achieve breakeven at sales price of £ 6:

Break even units = Fixed costs / (Sales price per unit – variable costs per unit)

= £ 27800 + £ 21000 / (£ 6 - £ 0.45)

= £ 48800 / £ 5.55

= £ 8793 units approximately

(c)

Sales from the 20000 units sold = 20000 * £ 6 = £ 120000

Particulars Per unit amount Total revenue

Sales 20000 * £ 6 £ 120000

Variable cost 20000 * £ 0.45 £ 9000

Contribution 20000 * £ 5.55 £ 111000

Total Fixed cost £ 48800

Profit £ 62200

Hence the profit if 20000 units of handbags are sold at the rate of £ 6 per unit then the total profit

earned would be £ 62200.

(d)

If company wants to earn a profit of £ 30000, then the number of bags that they need to sell at

the price of £ 6 per unit are:

Targeted units = Fixed cost + Targeted income / contribution margin per unit (i.e. sales -

variable cost)

Targeted units = ( £ 48800 + £ 30000) / (£ 6 - £ 0.45)

Targeted units = ( £ 48800 + £ 30000) / £ 5.55

3

QUESTION 2

(a)

Contribution:

Total sales of 10,000 hand bags sold at £ 6 per unit = 10000 * £ 6 = £ 60000

- Variable cost at £ 0.45 per unit = 10000 * 4.5 = (£ 4500)

Contribution = £ 60000 - £ 4500 = £ 55500

(b)

Number of selling units required to achieve breakeven at sales price of £ 6:

Break even units = Fixed costs / (Sales price per unit – variable costs per unit)

= £ 27800 + £ 21000 / (£ 6 - £ 0.45)

= £ 48800 / £ 5.55

= £ 8793 units approximately

(c)

Sales from the 20000 units sold = 20000 * £ 6 = £ 120000

Particulars Per unit amount Total revenue

Sales 20000 * £ 6 £ 120000

Variable cost 20000 * £ 0.45 £ 9000

Contribution 20000 * £ 5.55 £ 111000

Total Fixed cost £ 48800

Profit £ 62200

Hence the profit if 20000 units of handbags are sold at the rate of £ 6 per unit then the total profit

earned would be £ 62200.

(d)

If company wants to earn a profit of £ 30000, then the number of bags that they need to sell at

the price of £ 6 per unit are:

Targeted units = Fixed cost + Targeted income / contribution margin per unit (i.e. sales -

variable cost)

Targeted units = ( £ 48800 + £ 30000) / (£ 6 - £ 0.45)

Targeted units = ( £ 48800 + £ 30000) / £ 5.55

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

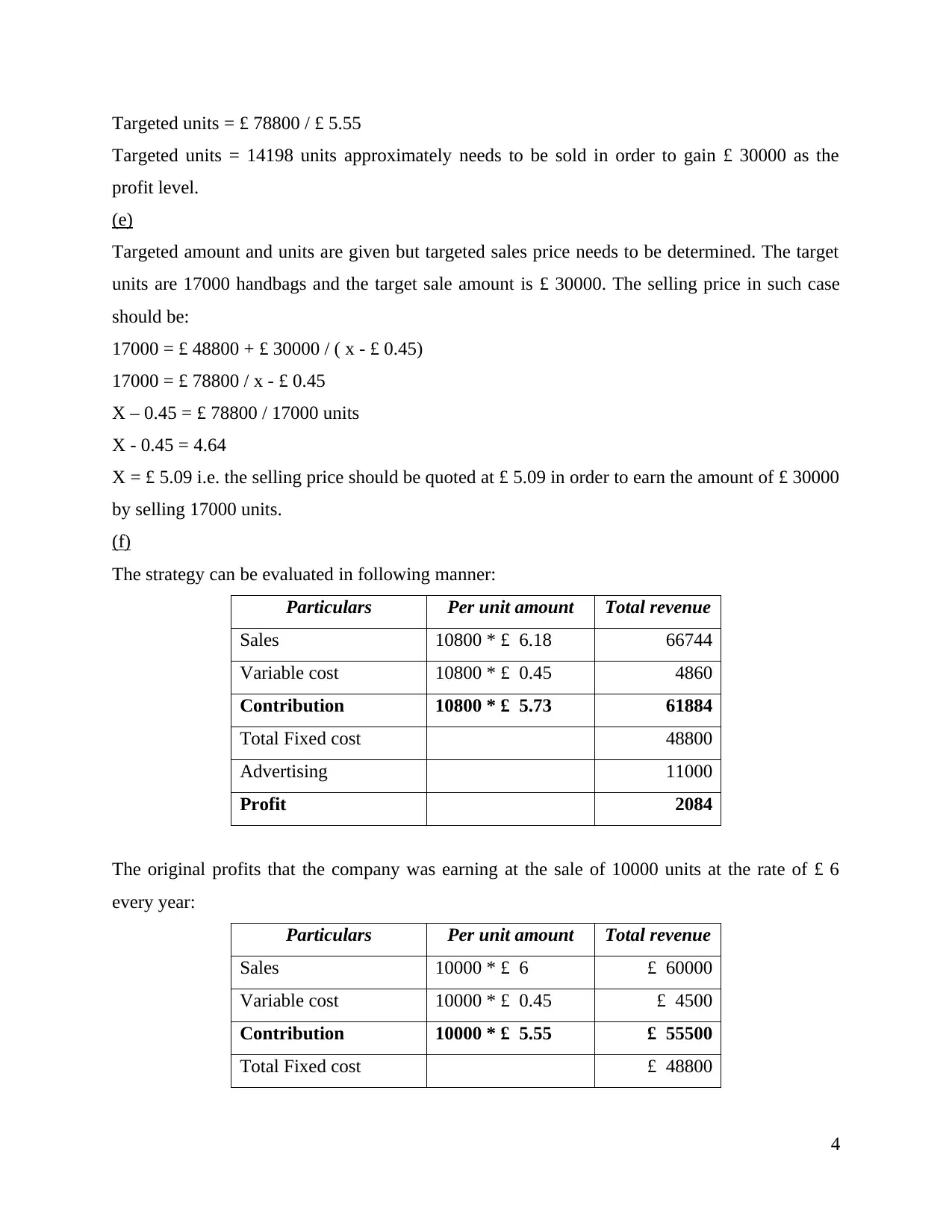

Targeted units = £ 78800 / £ 5.55

Targeted units = 14198 units approximately needs to be sold in order to gain £ 30000 as the

profit level.

(e)

Targeted amount and units are given but targeted sales price needs to be determined. The target

units are 17000 handbags and the target sale amount is £ 30000. The selling price in such case

should be:

17000 = £ 48800 + £ 30000 / ( x - £ 0.45)

17000 = £ 78800 / x - £ 0.45

X – 0.45 = £ 78800 / 17000 units

X - 0.45 = 4.64

X = £ 5.09 i.e. the selling price should be quoted at £ 5.09 in order to earn the amount of £ 30000

by selling 17000 units.

(f)

The strategy can be evaluated in following manner:

Particulars Per unit amount Total revenue

Sales 10800 * £ 6.18 66744

Variable cost 10800 * £ 0.45 4860

Contribution 10800 * £ 5.73 61884

Total Fixed cost 48800

Advertising 11000

Profit 2084

The original profits that the company was earning at the sale of 10000 units at the rate of £ 6

every year:

Particulars Per unit amount Total revenue

Sales 10000 * £ 6 £ 60000

Variable cost 10000 * £ 0.45 £ 4500

Contribution 10000 * £ 5.55 £ 55500

Total Fixed cost £ 48800

4

Targeted units = 14198 units approximately needs to be sold in order to gain £ 30000 as the

profit level.

(e)

Targeted amount and units are given but targeted sales price needs to be determined. The target

units are 17000 handbags and the target sale amount is £ 30000. The selling price in such case

should be:

17000 = £ 48800 + £ 30000 / ( x - £ 0.45)

17000 = £ 78800 / x - £ 0.45

X – 0.45 = £ 78800 / 17000 units

X - 0.45 = 4.64

X = £ 5.09 i.e. the selling price should be quoted at £ 5.09 in order to earn the amount of £ 30000

by selling 17000 units.

(f)

The strategy can be evaluated in following manner:

Particulars Per unit amount Total revenue

Sales 10800 * £ 6.18 66744

Variable cost 10800 * £ 0.45 4860

Contribution 10800 * £ 5.73 61884

Total Fixed cost 48800

Advertising 11000

Profit 2084

The original profits that the company was earning at the sale of 10000 units at the rate of £ 6

every year:

Particulars Per unit amount Total revenue

Sales 10000 * £ 6 £ 60000

Variable cost 10000 * £ 0.45 £ 4500

Contribution 10000 * £ 5.55 £ 55500

Total Fixed cost £ 48800

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

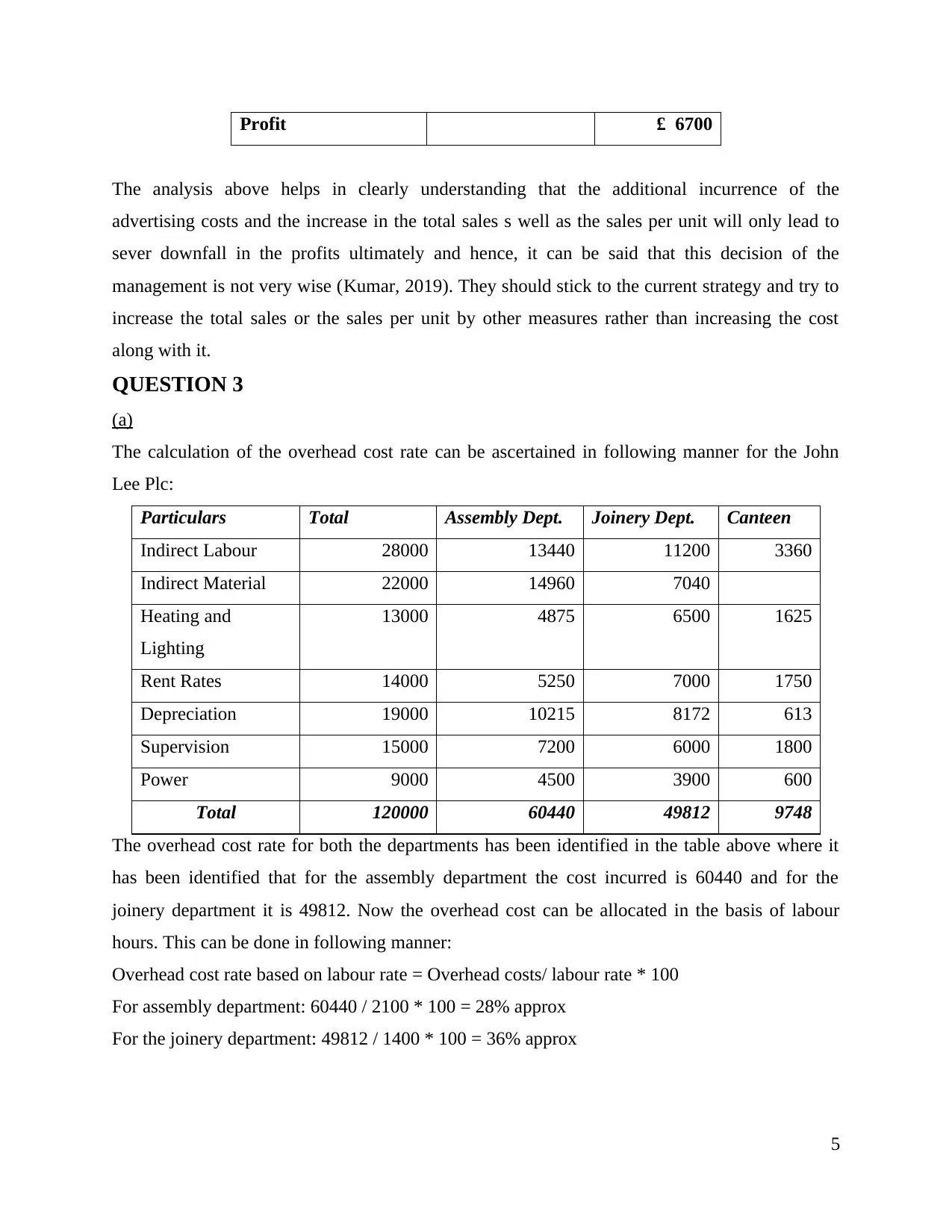

Profit £ 6700

The analysis above helps in clearly understanding that the additional incurrence of the

advertising costs and the increase in the total sales s well as the sales per unit will only lead to

sever downfall in the profits ultimately and hence, it can be said that this decision of the

management is not very wise (Kumar, 2019). They should stick to the current strategy and try to

increase the total sales or the sales per unit by other measures rather than increasing the cost

along with it.

QUESTION 3

(a)

The calculation of the overhead cost rate can be ascertained in following manner for the John

Lee Plc:

Particulars Total Assembly Dept. Joinery Dept. Canteen

Indirect Labour 28000 13440 11200 3360

Indirect Material 22000 14960 7040

Heating and

Lighting

13000 4875 6500 1625

Rent Rates 14000 5250 7000 1750

Depreciation 19000 10215 8172 613

Supervision 15000 7200 6000 1800

Power 9000 4500 3900 600

Total 120000 60440 49812 9748

The overhead cost rate for both the departments has been identified in the table above where it

has been identified that for the assembly department the cost incurred is 60440 and for the

joinery department it is 49812. Now the overhead cost can be allocated in the basis of labour

hours. This can be done in following manner:

Overhead cost rate based on labour rate = Overhead costs/ labour rate * 100

For assembly department: 60440 / 2100 * 100 = 28% approx

For the joinery department: 49812 / 1400 * 100 = 36% approx

5

The analysis above helps in clearly understanding that the additional incurrence of the

advertising costs and the increase in the total sales s well as the sales per unit will only lead to

sever downfall in the profits ultimately and hence, it can be said that this decision of the

management is not very wise (Kumar, 2019). They should stick to the current strategy and try to

increase the total sales or the sales per unit by other measures rather than increasing the cost

along with it.

QUESTION 3

(a)

The calculation of the overhead cost rate can be ascertained in following manner for the John

Lee Plc:

Particulars Total Assembly Dept. Joinery Dept. Canteen

Indirect Labour 28000 13440 11200 3360

Indirect Material 22000 14960 7040

Heating and

Lighting

13000 4875 6500 1625

Rent Rates 14000 5250 7000 1750

Depreciation 19000 10215 8172 613

Supervision 15000 7200 6000 1800

Power 9000 4500 3900 600

Total 120000 60440 49812 9748

The overhead cost rate for both the departments has been identified in the table above where it

has been identified that for the assembly department the cost incurred is 60440 and for the

joinery department it is 49812. Now the overhead cost can be allocated in the basis of labour

hours. This can be done in following manner:

Overhead cost rate based on labour rate = Overhead costs/ labour rate * 100

For assembly department: 60440 / 2100 * 100 = 28% approx

For the joinery department: 49812 / 1400 * 100 = 36% approx

5

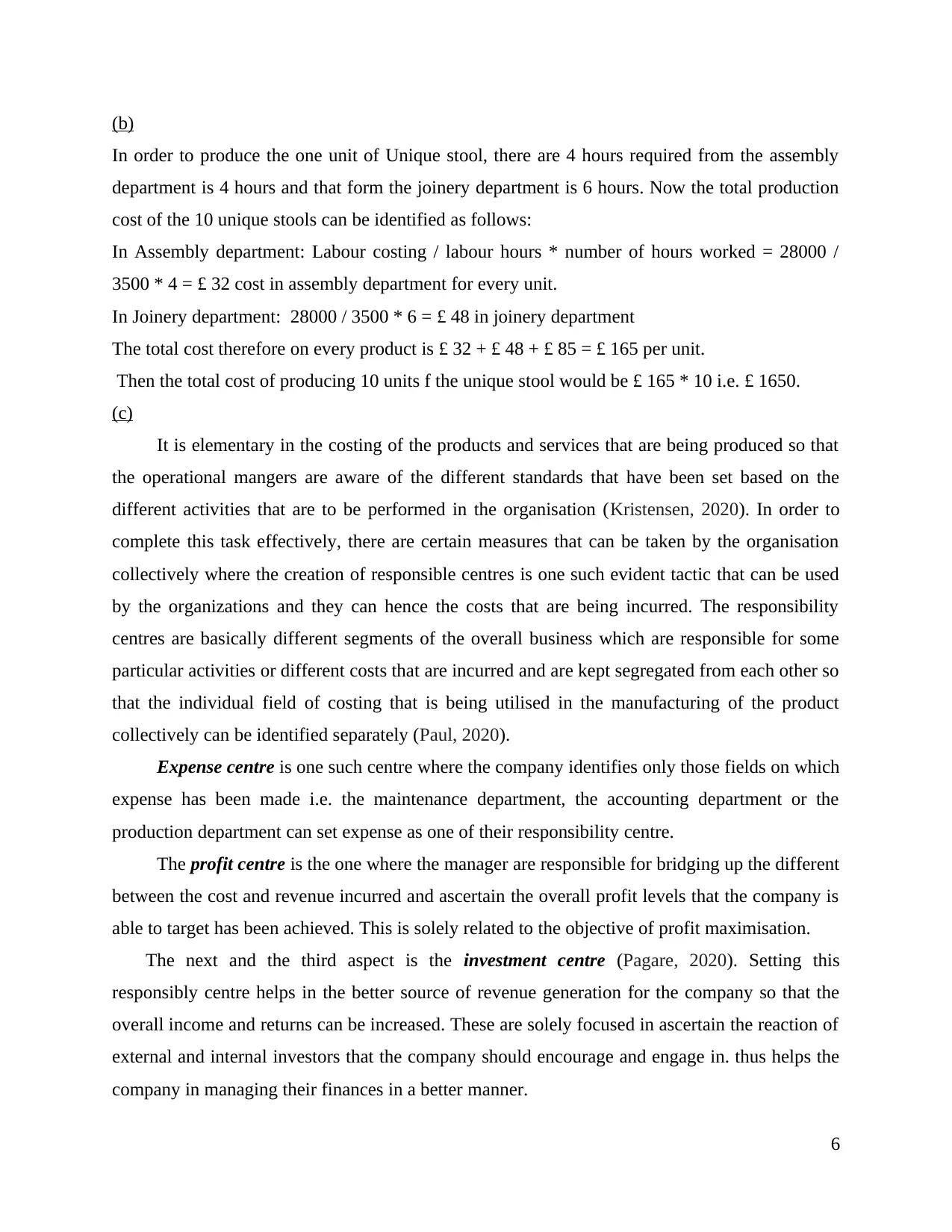

(b)

In order to produce the one unit of Unique stool, there are 4 hours required from the assembly

department is 4 hours and that form the joinery department is 6 hours. Now the total production

cost of the 10 unique stools can be identified as follows:

In Assembly department: Labour costing / labour hours * number of hours worked = 28000 /

3500 * 4 = £ 32 cost in assembly department for every unit.

In Joinery department: 28000 / 3500 * 6 = £ 48 in joinery department

The total cost therefore on every product is £ 32 + £ 48 + £ 85 = £ 165 per unit.

Then the total cost of producing 10 units f the unique stool would be £ 165 * 10 i.e. £ 1650.

(c)

It is elementary in the costing of the products and services that are being produced so that

the operational mangers are aware of the different standards that have been set based on the

different activities that are to be performed in the organisation (Kristensen, 2020). In order to

complete this task effectively, there are certain measures that can be taken by the organisation

collectively where the creation of responsible centres is one such evident tactic that can be used

by the organizations and they can hence the costs that are being incurred. The responsibility

centres are basically different segments of the overall business which are responsible for some

particular activities or different costs that are incurred and are kept segregated from each other so

that the individual field of costing that is being utilised in the manufacturing of the product

collectively can be identified separately (Paul, 2020).

Expense centre is one such centre where the company identifies only those fields on which

expense has been made i.e. the maintenance department, the accounting department or the

production department can set expense as one of their responsibility centre.

The profit centre is the one where the manager are responsible for bridging up the different

between the cost and revenue incurred and ascertain the overall profit levels that the company is

able to target has been achieved. This is solely related to the objective of profit maximisation.

The next and the third aspect is the investment centre (Pagare, 2020). Setting this

responsibly centre helps in the better source of revenue generation for the company so that the

overall income and returns can be increased. These are solely focused in ascertain the reaction of

external and internal investors that the company should encourage and engage in. thus helps the

company in managing their finances in a better manner.

6

In order to produce the one unit of Unique stool, there are 4 hours required from the assembly

department is 4 hours and that form the joinery department is 6 hours. Now the total production

cost of the 10 unique stools can be identified as follows:

In Assembly department: Labour costing / labour hours * number of hours worked = 28000 /

3500 * 4 = £ 32 cost in assembly department for every unit.

In Joinery department: 28000 / 3500 * 6 = £ 48 in joinery department

The total cost therefore on every product is £ 32 + £ 48 + £ 85 = £ 165 per unit.

Then the total cost of producing 10 units f the unique stool would be £ 165 * 10 i.e. £ 1650.

(c)

It is elementary in the costing of the products and services that are being produced so that

the operational mangers are aware of the different standards that have been set based on the

different activities that are to be performed in the organisation (Kristensen, 2020). In order to

complete this task effectively, there are certain measures that can be taken by the organisation

collectively where the creation of responsible centres is one such evident tactic that can be used

by the organizations and they can hence the costs that are being incurred. The responsibility

centres are basically different segments of the overall business which are responsible for some

particular activities or different costs that are incurred and are kept segregated from each other so

that the individual field of costing that is being utilised in the manufacturing of the product

collectively can be identified separately (Paul, 2020).

Expense centre is one such centre where the company identifies only those fields on which

expense has been made i.e. the maintenance department, the accounting department or the

production department can set expense as one of their responsibility centre.

The profit centre is the one where the manager are responsible for bridging up the different

between the cost and revenue incurred and ascertain the overall profit levels that the company is

able to target has been achieved. This is solely related to the objective of profit maximisation.

The next and the third aspect is the investment centre (Pagare, 2020). Setting this

responsibly centre helps in the better source of revenue generation for the company so that the

overall income and returns can be increased. These are solely focused in ascertain the reaction of

external and internal investors that the company should encourage and engage in. thus helps the

company in managing their finances in a better manner.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

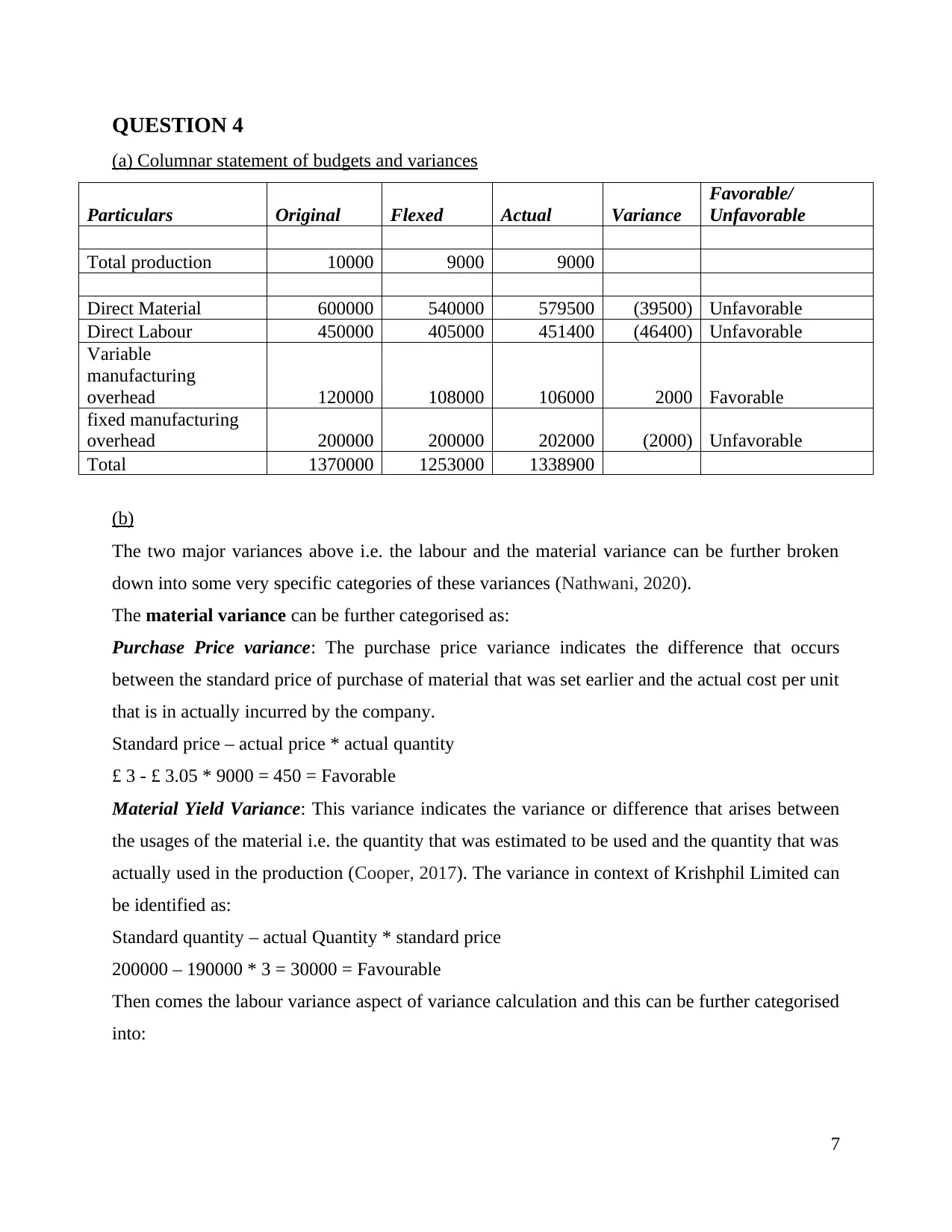

QUESTION 4

(a) Columnar statement of budgets and variances

Particulars Original Flexed Actual Variance

Favorable/

Unfavorable

Total production 10000 9000 9000

Direct Material 600000 540000 579500 (39500) Unfavorable

Direct Labour 450000 405000 451400 (46400) Unfavorable

Variable

manufacturing

overhead 120000 108000 106000 2000 Favorable

fixed manufacturing

overhead 200000 200000 202000 (2000) Unfavorable

Total 1370000 1253000 1338900

(b)

The two major variances above i.e. the labour and the material variance can be further broken

down into some very specific categories of these variances (Nathwani, 2020).

The material variance can be further categorised as:

Purchase Price variance: The purchase price variance indicates the difference that occurs

between the standard price of purchase of material that was set earlier and the actual cost per unit

that is in actually incurred by the company.

Standard price – actual price * actual quantity

£ 3 - £ 3.05 * 9000 = 450 = Favorable

Material Yield Variance: This variance indicates the variance or difference that arises between

the usages of the material i.e. the quantity that was estimated to be used and the quantity that was

actually used in the production (Cooper, 2017). The variance in context of Krishphil Limited can

be identified as:

Standard quantity – actual Quantity * standard price

200000 – 190000 * 3 = 30000 = Favourable

Then comes the labour variance aspect of variance calculation and this can be further categorised

into:

7

(a) Columnar statement of budgets and variances

Particulars Original Flexed Actual Variance

Favorable/

Unfavorable

Total production 10000 9000 9000

Direct Material 600000 540000 579500 (39500) Unfavorable

Direct Labour 450000 405000 451400 (46400) Unfavorable

Variable

manufacturing

overhead 120000 108000 106000 2000 Favorable

fixed manufacturing

overhead 200000 200000 202000 (2000) Unfavorable

Total 1370000 1253000 1338900

(b)

The two major variances above i.e. the labour and the material variance can be further broken

down into some very specific categories of these variances (Nathwani, 2020).

The material variance can be further categorised as:

Purchase Price variance: The purchase price variance indicates the difference that occurs

between the standard price of purchase of material that was set earlier and the actual cost per unit

that is in actually incurred by the company.

Standard price – actual price * actual quantity

£ 3 - £ 3.05 * 9000 = 450 = Favorable

Material Yield Variance: This variance indicates the variance or difference that arises between

the usages of the material i.e. the quantity that was estimated to be used and the quantity that was

actually used in the production (Cooper, 2017). The variance in context of Krishphil Limited can

be identified as:

Standard quantity – actual Quantity * standard price

200000 – 190000 * 3 = 30000 = Favourable

Then comes the labour variance aspect of variance calculation and this can be further categorised

into:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

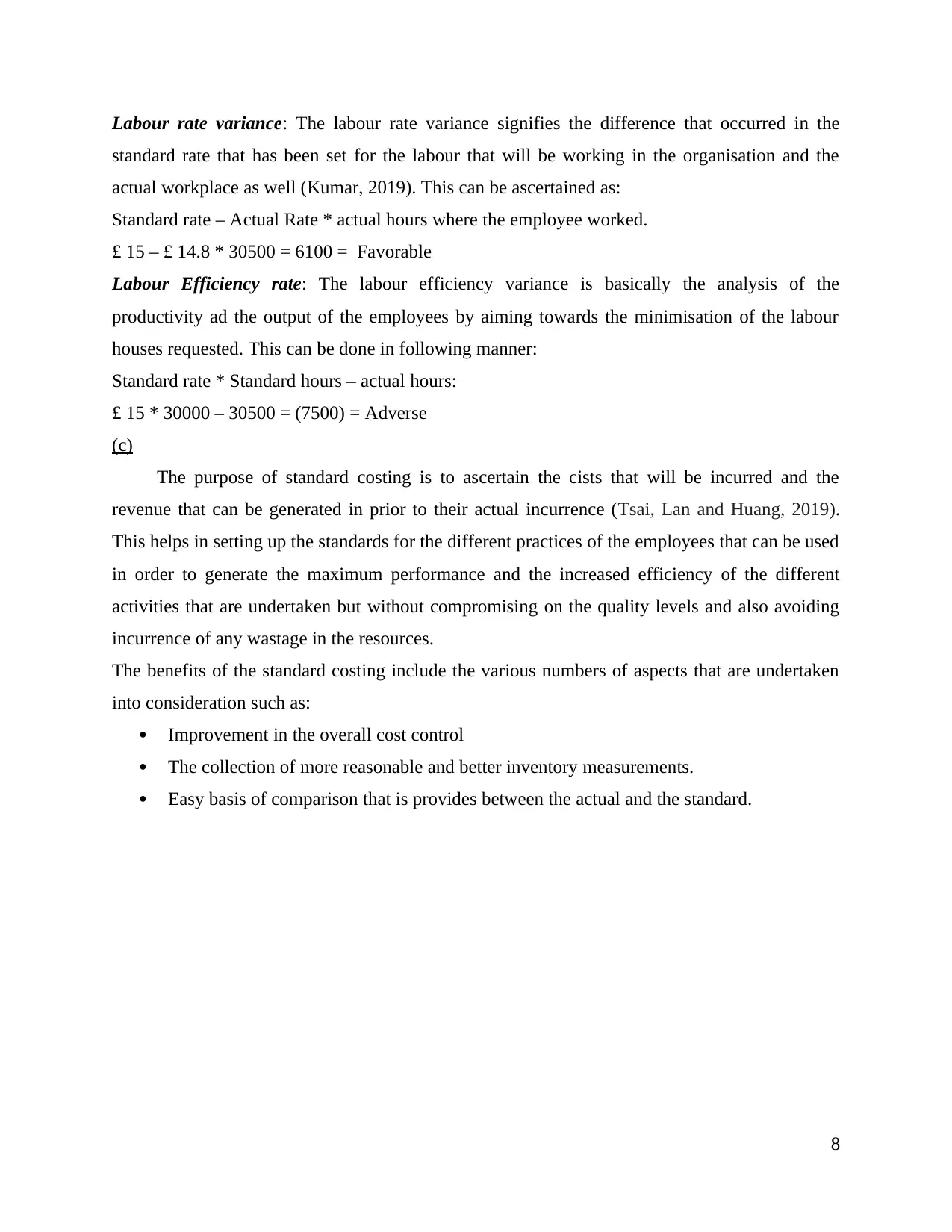

Labour rate variance: The labour rate variance signifies the difference that occurred in the

standard rate that has been set for the labour that will be working in the organisation and the

actual workplace as well (Kumar, 2019). This can be ascertained as:

Standard rate – Actual Rate * actual hours where the employee worked.

£ 15 – £ 14.8 * 30500 = 6100 = Favorable

Labour Efficiency rate: The labour efficiency variance is basically the analysis of the

productivity ad the output of the employees by aiming towards the minimisation of the labour

houses requested. This can be done in following manner:

Standard rate * Standard hours – actual hours:

£ 15 * 30000 – 30500 = (7500) = Adverse

(c)

The purpose of standard costing is to ascertain the cists that will be incurred and the

revenue that can be generated in prior to their actual incurrence (Tsai, Lan and Huang, 2019).

This helps in setting up the standards for the different practices of the employees that can be used

in order to generate the maximum performance and the increased efficiency of the different

activities that are undertaken but without compromising on the quality levels and also avoiding

incurrence of any wastage in the resources.

The benefits of the standard costing include the various numbers of aspects that are undertaken

into consideration such as:

Improvement in the overall cost control

The collection of more reasonable and better inventory measurements.

Easy basis of comparison that is provides between the actual and the standard.

8

standard rate that has been set for the labour that will be working in the organisation and the

actual workplace as well (Kumar, 2019). This can be ascertained as:

Standard rate – Actual Rate * actual hours where the employee worked.

£ 15 – £ 14.8 * 30500 = 6100 = Favorable

Labour Efficiency rate: The labour efficiency variance is basically the analysis of the

productivity ad the output of the employees by aiming towards the minimisation of the labour

houses requested. This can be done in following manner:

Standard rate * Standard hours – actual hours:

£ 15 * 30000 – 30500 = (7500) = Adverse

(c)

The purpose of standard costing is to ascertain the cists that will be incurred and the

revenue that can be generated in prior to their actual incurrence (Tsai, Lan and Huang, 2019).

This helps in setting up the standards for the different practices of the employees that can be used

in order to generate the maximum performance and the increased efficiency of the different

activities that are undertaken but without compromising on the quality levels and also avoiding

incurrence of any wastage in the resources.

The benefits of the standard costing include the various numbers of aspects that are undertaken

into consideration such as:

Improvement in the overall cost control

The collection of more reasonable and better inventory measurements.

Easy basis of comparison that is provides between the actual and the standard.

8

REFERENCES

Books and Journals

Cooper, R., 2017. Target costing and value engineering. Routledge.

Kristensen, T.B., 2020. Enabling use of standard variable costing in lean production. Production

Planning & Control, pp.1-16.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Kumar, A., 2019. Standard Costing And Material Cost Variance. The Management Accountant

Journal. 54(1). pp.82-85.

Nathwani, D., 2020. Standard Costing.

Pagare, S., 2020. Standard Costing.

Paul, D.D., 2020. STANDARD COSTING AND ABC: A COEXISTENCE. Strategic

Finance. 101(11). pp.32-39.

Tsai, W.H., Lan, S.H. and Huang, C.T., 2019. Activity-Based Standard Costing Product-Mix

Decision in the Future Digital Era: Green Recycling Steel-Scrap Material for Steel

Industry. Sustainability. 11(3). p.899.

9

Books and Journals

Cooper, R., 2017. Target costing and value engineering. Routledge.

Kristensen, T.B., 2020. Enabling use of standard variable costing in lean production. Production

Planning & Control, pp.1-16.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Kumar, A., 2019. Standard Costing And Material Cost Variance. The Management Accountant

Journal. 54(1). pp.82-85.

Nathwani, D., 2020. Standard Costing.

Pagare, S., 2020. Standard Costing.

Paul, D.D., 2020. STANDARD COSTING AND ABC: A COEXISTENCE. Strategic

Finance. 101(11). pp.32-39.

Tsai, W.H., Lan, S.H. and Huang, C.T., 2019. Activity-Based Standard Costing Product-Mix

Decision in the Future Digital Era: Green Recycling Steel-Scrap Material for Steel

Industry. Sustainability. 11(3). p.899.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.