Finance in Hospitality Report

VerifiedAdded on 2020/10/04

|22

|5156

|24

Report

AI Summary

This report discusses the critical role of finance in the hospitality industry, detailing various funding sources, income generation methods for restaurants, and financial management strategies. It includes analyses of financial statements, budgetary control processes, and recommendations for improving profitability in hospitality businesses.

FINANCE IN

HOSPITALITY

HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Finance is the life blood in any organization and hence, is required in order to have

growth and to attain organisational objectives. The present report talks about finance in

hospitality. Hospitality industries are generally service providing industries. Restaurant business,

hotel business, travel and tourism and hospital are few of the example of hospitality industry. In

the present research report various sources available to raise funds for service industries has been

provided along with various techniques that can be used by restaurant business in order to

generate their income. Further, in this report, budgetary control along with its process has been

explained and the same has been enclosed in PPT along with analysing variance between actual

and budgeted results for Cyprian. Financial statements are also prepared for R Rigs after

considering two unrecorded entries along with their analysis using ratio analysis tool. At last

various proposals have been analysed for getting desired profits for R Rigs.

TASK 1

1.1 Available sources of funds in business and service industries

A business cannot grow unless there are sufficient cash reserves that are required to

invest for growth. Growth of a business ultimately increases sales and profit of the firm (Axsäter,

2015). However, for increasing sales business had to increase its current assets and fixed assets

such as inventory, plant and equipment, land and building, etc. Funds in a business are required

in order to carry out business operations, expansion of business, purchasing of fixed assets or for

making investments. There are many different ways from where a small business can raise funds.

Therefore, from following sources a sole a trader can raise funds in context with buying a new

building worth £450,000.

Various Sources of raising funds:

Personal sources:

It is easy for small business traders to finance their business through their personal cash.

This source of fund is most beneficial for small owners along with various other benefits like, a

banker is always keen to know before providing any loan amount that how much own capital is

1

Finance is the life blood in any organization and hence, is required in order to have

growth and to attain organisational objectives. The present report talks about finance in

hospitality. Hospitality industries are generally service providing industries. Restaurant business,

hotel business, travel and tourism and hospital are few of the example of hospitality industry. In

the present research report various sources available to raise funds for service industries has been

provided along with various techniques that can be used by restaurant business in order to

generate their income. Further, in this report, budgetary control along with its process has been

explained and the same has been enclosed in PPT along with analysing variance between actual

and budgeted results for Cyprian. Financial statements are also prepared for R Rigs after

considering two unrecorded entries along with their analysis using ratio analysis tool. At last

various proposals have been analysed for getting desired profits for R Rigs.

TASK 1

1.1 Available sources of funds in business and service industries

A business cannot grow unless there are sufficient cash reserves that are required to

invest for growth. Growth of a business ultimately increases sales and profit of the firm (Axsäter,

2015). However, for increasing sales business had to increase its current assets and fixed assets

such as inventory, plant and equipment, land and building, etc. Funds in a business are required

in order to carry out business operations, expansion of business, purchasing of fixed assets or for

making investments. There are many different ways from where a small business can raise funds.

Therefore, from following sources a sole a trader can raise funds in context with buying a new

building worth £450,000.

Various Sources of raising funds:

Personal sources:

It is easy for small business traders to finance their business through their personal cash.

This source of fund is most beneficial for small owners along with various other benefits like, a

banker is always keen to know before providing any loan amount that how much own capital is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

invested in the business by owner. Personal sources could be like their personal savings, home

equity loan secured by own residential house, cash value life insurance etc.

Finance through Friends and Family:

Another popular source for the growth of small business includes finance through friends

and family (Shenoy and Rosas, 2018). Benefit of friends and family finance is that there is no

need of any guarantor because they already know you along with flexible repayable terms and

lower or no interest rate. However, a written contract presenting the debt amount and liability

may be created between the borrower and lender.

Internally generated funds:

It is the most advantageous source of fund. Under this, finance is raised through retained

earnings of the business. By using retained earnings business only loses the opportunity cost of

interest if it had kept in bank. In order to have growth, ploughing retained earnings back in the

business could be a smart move.

Bank Loans:

Bank loans are easily available to small business trader for investment in property as

papers of that property can be kept as the purpose of security. There is also an option of taking

finance lease from bank (DRURY, 2013). Under this option, asset is purchased by bank and then

owner takes that asset from bank by paying either rent or lease amount. Loan consists of

excessive documentation requirement, as borrower needs to present their financial statement to

inform lenders about their capability of loan repayment. Moreover, debt covenant is designed

that are necessary to be complied and as per this, timely instalments and interest required to be

paid by the firm.

Trade Credit:

Another essential financing tool for small traders is trade credit. Under this credit period

is extended by the suppliers. Credit amount which is to be payable to suppliers is then invested in

business.

Increasing internal cash flow:

2

equity loan secured by own residential house, cash value life insurance etc.

Finance through Friends and Family:

Another popular source for the growth of small business includes finance through friends

and family (Shenoy and Rosas, 2018). Benefit of friends and family finance is that there is no

need of any guarantor because they already know you along with flexible repayable terms and

lower or no interest rate. However, a written contract presenting the debt amount and liability

may be created between the borrower and lender.

Internally generated funds:

It is the most advantageous source of fund. Under this, finance is raised through retained

earnings of the business. By using retained earnings business only loses the opportunity cost of

interest if it had kept in bank. In order to have growth, ploughing retained earnings back in the

business could be a smart move.

Bank Loans:

Bank loans are easily available to small business trader for investment in property as

papers of that property can be kept as the purpose of security. There is also an option of taking

finance lease from bank (DRURY, 2013). Under this option, asset is purchased by bank and then

owner takes that asset from bank by paying either rent or lease amount. Loan consists of

excessive documentation requirement, as borrower needs to present their financial statement to

inform lenders about their capability of loan repayment. Moreover, debt covenant is designed

that are necessary to be complied and as per this, timely instalments and interest required to be

paid by the firm.

Trade Credit:

Another essential financing tool for small traders is trade credit. Under this credit period

is extended by the suppliers. Credit amount which is to be payable to suppliers is then invested in

business.

Increasing internal cash flow:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Need of purchasing a building is often forecasted earlier. Hence, by then, increasing cash

flow within business in the way of increasing profit margin on products and services, cutting cost

of services, managing working capital, selling off old assets or by recovering debts earlier,

business can generate more cash (Sources of funds, 2017).

Issuing share capital:

Issue of share capital, is generally the least favourable sources of finance for small

business traders because brand image of the business is yet in process and thus less public rely

on them. However, there is an option to owner if he wants to raise finance through issuing share

capital.

The best way for raising finance in order to purchase new building for small trader is

using personal source or through bank loan (Jang and Park, 2011). Because using personal

sources will increase capital in the business that will create a good image of the firm and

therefore, bank loan can be easily available.

Government programs:

With the help of government and grants for the financial institutions which in turn helps

in facilitating the adequate funds for the business operations. The most important benefit

associated with the grant is that it does not need any repayment if it is utilized in the mentioned

timeframe and for the purpose for which it is given. Thus, the same is its limitation also as grant

is available for specified time or given objective only. Hence, it cannot be used for any other

purpose.

1.2 Methods for generating income in restaurant business

In the competitive world, making restaurant profitable is a difficult task. In order to

survive in a restaurant industry, making high revenue is a key factor, however, in order to

increase revenue, business cannot use wrong practices like charging high from customers,

reducing average volume, etc. Using such practices can push the customers away from the

restaurant. Below are some tactics that can be used by restaurant business to increase their

revenue and make their restaurant profitable:

3

flow within business in the way of increasing profit margin on products and services, cutting cost

of services, managing working capital, selling off old assets or by recovering debts earlier,

business can generate more cash (Sources of funds, 2017).

Issuing share capital:

Issue of share capital, is generally the least favourable sources of finance for small

business traders because brand image of the business is yet in process and thus less public rely

on them. However, there is an option to owner if he wants to raise finance through issuing share

capital.

The best way for raising finance in order to purchase new building for small trader is

using personal source or through bank loan (Jang and Park, 2011). Because using personal

sources will increase capital in the business that will create a good image of the firm and

therefore, bank loan can be easily available.

Government programs:

With the help of government and grants for the financial institutions which in turn helps

in facilitating the adequate funds for the business operations. The most important benefit

associated with the grant is that it does not need any repayment if it is utilized in the mentioned

timeframe and for the purpose for which it is given. Thus, the same is its limitation also as grant

is available for specified time or given objective only. Hence, it cannot be used for any other

purpose.

1.2 Methods for generating income in restaurant business

In the competitive world, making restaurant profitable is a difficult task. In order to

survive in a restaurant industry, making high revenue is a key factor, however, in order to

increase revenue, business cannot use wrong practices like charging high from customers,

reducing average volume, etc. Using such practices can push the customers away from the

restaurant. Below are some tactics that can be used by restaurant business to increase their

revenue and make their restaurant profitable:

3

Good Ambiance:

It is said that 1st impression is the last impression. The first thing that a customer notices

is the front look of restaurant and its ambiance (Walker, 2016). Having a good look will

definitely attract more customers which in turn will increase volume of sales and good image in

the market. However, along with the ambiance, comfortable sitting area must also be considered.

Knowing target customers:

Before a restaurant starts marketing about your business, it is necessary to identify your

target customers. For example, if the restaurant is in the middle of southern BBQ country, selling

small amount of dish with less variety will not work. Hence, must be created keeping in view the

customers around the restaurant.

Update menu regularly:

Consumers always want something different to try in a restaurant. If there would be same

menu year by year, customer will get bored out of it and will get pushed away from the

restaurant. Therefore, it is necessary to provide different new choices to the customers to make

them retain in your place.

Be known for a signature dish:

Consumer often get attracted to a restaurant if it is popular for a signature dish. Signature

dish in the menu aids to the business value (Park and Jang, 2014). It is something that shapes

how a customer looks at the restaurant.

Good marketing strategy:

Advertising your business is necessary in order to create recognition in the market. Great

marketing plan can be executed such as offering welcome drink and welcome snacks to

customers, opting for social media marketing, TV and radio, etc. However, the best marketing is

the mouth advertising which is done by the customers, so first priority of a restaurant must be

customer satisfaction.

4

It is said that 1st impression is the last impression. The first thing that a customer notices

is the front look of restaurant and its ambiance (Walker, 2016). Having a good look will

definitely attract more customers which in turn will increase volume of sales and good image in

the market. However, along with the ambiance, comfortable sitting area must also be considered.

Knowing target customers:

Before a restaurant starts marketing about your business, it is necessary to identify your

target customers. For example, if the restaurant is in the middle of southern BBQ country, selling

small amount of dish with less variety will not work. Hence, must be created keeping in view the

customers around the restaurant.

Update menu regularly:

Consumers always want something different to try in a restaurant. If there would be same

menu year by year, customer will get bored out of it and will get pushed away from the

restaurant. Therefore, it is necessary to provide different new choices to the customers to make

them retain in your place.

Be known for a signature dish:

Consumer often get attracted to a restaurant if it is popular for a signature dish. Signature

dish in the menu aids to the business value (Park and Jang, 2014). It is something that shapes

how a customer looks at the restaurant.

Good marketing strategy:

Advertising your business is necessary in order to create recognition in the market. Great

marketing plan can be executed such as offering welcome drink and welcome snacks to

customers, opting for social media marketing, TV and radio, etc. However, the best marketing is

the mouth advertising which is done by the customers, so first priority of a restaurant must be

customer satisfaction.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Commission based business: In despite of the above, restaurant can offer different

services and earn commission based revenues to maximize their income level. Running

commission based activities such as taking franchise will enable restaurant chain to get success

in the local as well as international market place.

Sale of unused assets: Assets which are not available for use and categorized as assets

for disposal can be disposed off in the open market to generate income from the same.

Letting/subletting: It is also an opportunity for the restaurant, under which, it can

organize various events like on birthday parties, anniversaries and other occasions and maximize

their sales revenue and net return.

TASK 2

2.1 Discussing various elements of cost, gross profit and sales price

Enclosed in PPT.

2.2 Evaluating different methods of controlling inventory and cash

Enclosed in PPT.

TASK 3

3.3 Purpose of Budgetary control along with its process

Enclosed in PPT.

3.4 Analysing variance between actual and budgeted figures with suggestions

Enclosed in PPT.

TASK 4

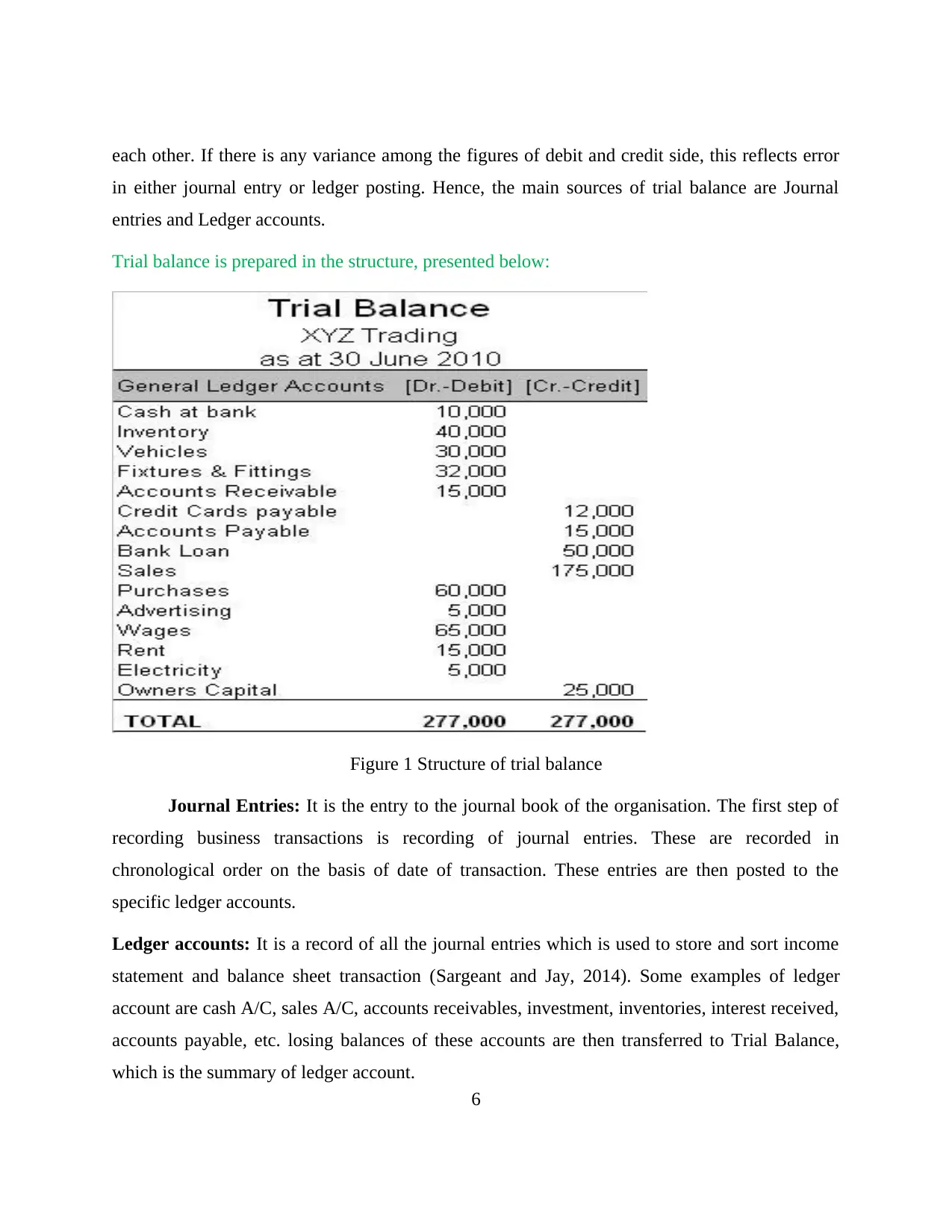

3.1 Assessing several variables of Trial Balance with structure of Trial Balance

Trial balance is a financial statement that is a summary of all debit and credit balances.

Debit side may include balances of either assets or expenses and credit side may include

balances of either income or liability (Arif, Noor-E-Jannat and Anwar, 2016). It is based on

double entry book system. It includes all the closing balances of ledger accounts of a company

which are then considered for the preparation of Income Statement and Statement of Financial

Position. One of the principle of trial balance is that its credit and debit side always match with

5

services and earn commission based revenues to maximize their income level. Running

commission based activities such as taking franchise will enable restaurant chain to get success

in the local as well as international market place.

Sale of unused assets: Assets which are not available for use and categorized as assets

for disposal can be disposed off in the open market to generate income from the same.

Letting/subletting: It is also an opportunity for the restaurant, under which, it can

organize various events like on birthday parties, anniversaries and other occasions and maximize

their sales revenue and net return.

TASK 2

2.1 Discussing various elements of cost, gross profit and sales price

Enclosed in PPT.

2.2 Evaluating different methods of controlling inventory and cash

Enclosed in PPT.

TASK 3

3.3 Purpose of Budgetary control along with its process

Enclosed in PPT.

3.4 Analysing variance between actual and budgeted figures with suggestions

Enclosed in PPT.

TASK 4

3.1 Assessing several variables of Trial Balance with structure of Trial Balance

Trial balance is a financial statement that is a summary of all debit and credit balances.

Debit side may include balances of either assets or expenses and credit side may include

balances of either income or liability (Arif, Noor-E-Jannat and Anwar, 2016). It is based on

double entry book system. It includes all the closing balances of ledger accounts of a company

which are then considered for the preparation of Income Statement and Statement of Financial

Position. One of the principle of trial balance is that its credit and debit side always match with

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

each other. If there is any variance among the figures of debit and credit side, this reflects error

in either journal entry or ledger posting. Hence, the main sources of trial balance are Journal

entries and Ledger accounts.

Trial balance is prepared in the structure, presented below:

Figure 1 Structure of trial balance

Journal Entries: It is the entry to the journal book of the organisation. The first step of

recording business transactions is recording of journal entries. These are recorded in

chronological order on the basis of date of transaction. These entries are then posted to the

specific ledger accounts.

Ledger accounts: It is a record of all the journal entries which is used to store and sort income

statement and balance sheet transaction (Sargeant and Jay, 2014). Some examples of ledger

account are cash A/C, sales A/C, accounts receivables, investment, inventories, interest received,

accounts payable, etc. losing balances of these accounts are then transferred to Trial Balance,

which is the summary of ledger account.

6

in either journal entry or ledger posting. Hence, the main sources of trial balance are Journal

entries and Ledger accounts.

Trial balance is prepared in the structure, presented below:

Figure 1 Structure of trial balance

Journal Entries: It is the entry to the journal book of the organisation. The first step of

recording business transactions is recording of journal entries. These are recorded in

chronological order on the basis of date of transaction. These entries are then posted to the

specific ledger accounts.

Ledger accounts: It is a record of all the journal entries which is used to store and sort income

statement and balance sheet transaction (Sargeant and Jay, 2014). Some examples of ledger

account are cash A/C, sales A/C, accounts receivables, investment, inventories, interest received,

accounts payable, etc. losing balances of these accounts are then transferred to Trial Balance,

which is the summary of ledger account.

6

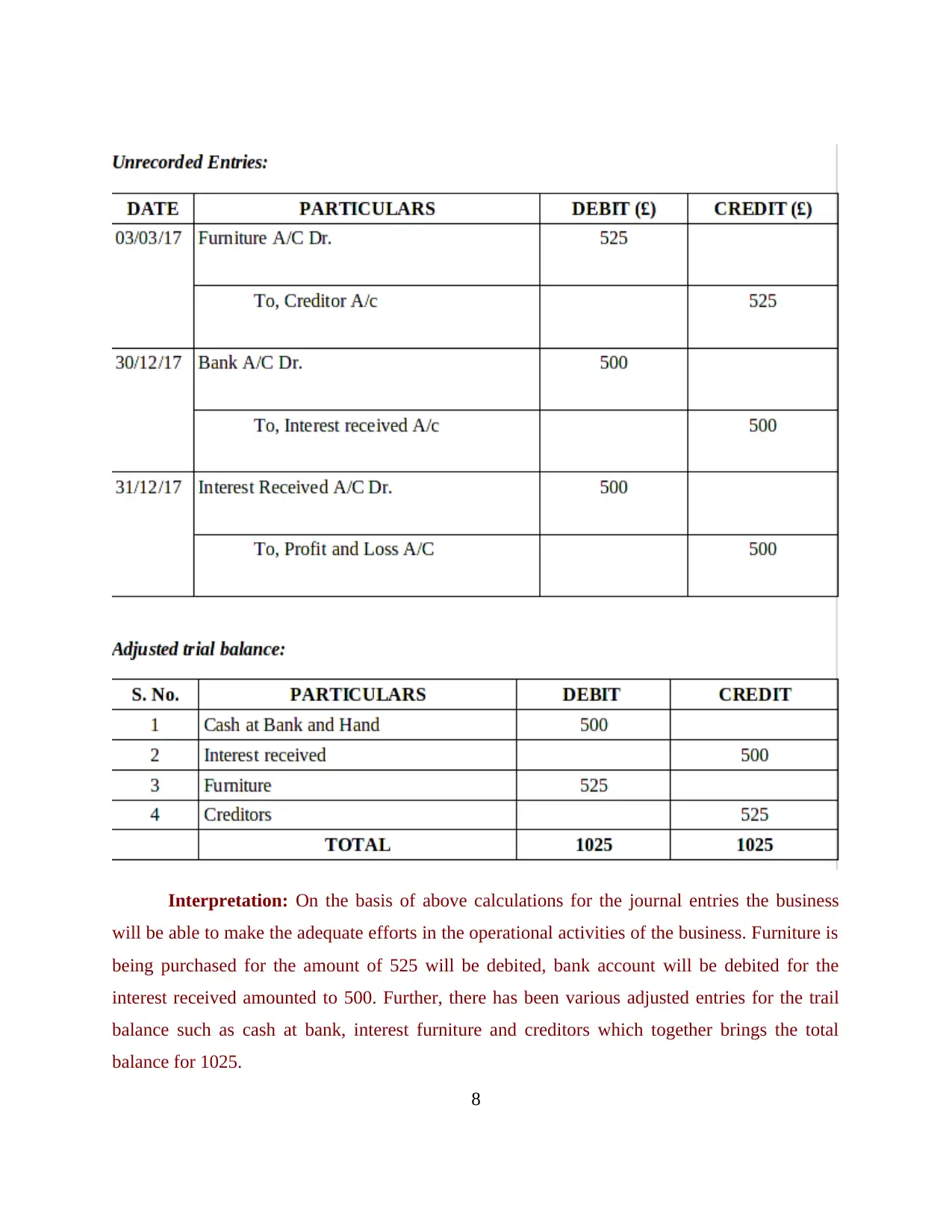

As per the given scenario, R Rigs have not recorded two transactions in its records. The

same are been recorded below:

7

same are been recorded below:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: On the basis of above calculations for the journal entries the business

will be able to make the adequate efforts in the operational activities of the business. Furniture is

being purchased for the amount of 525 will be debited, bank account will be debited for the

interest received amounted to 500. Further, there has been various adjusted entries for the trail

balance such as cash at bank, interest furniture and creditors which together brings the total

balance for 1025.

8

will be able to make the adequate efforts in the operational activities of the business. Furniture is

being purchased for the amount of 525 will be debited, bank account will be debited for the

interest received amounted to 500. Further, there has been various adjusted entries for the trail

balance such as cash at bank, interest furniture and creditors which together brings the total

balance for 1025.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

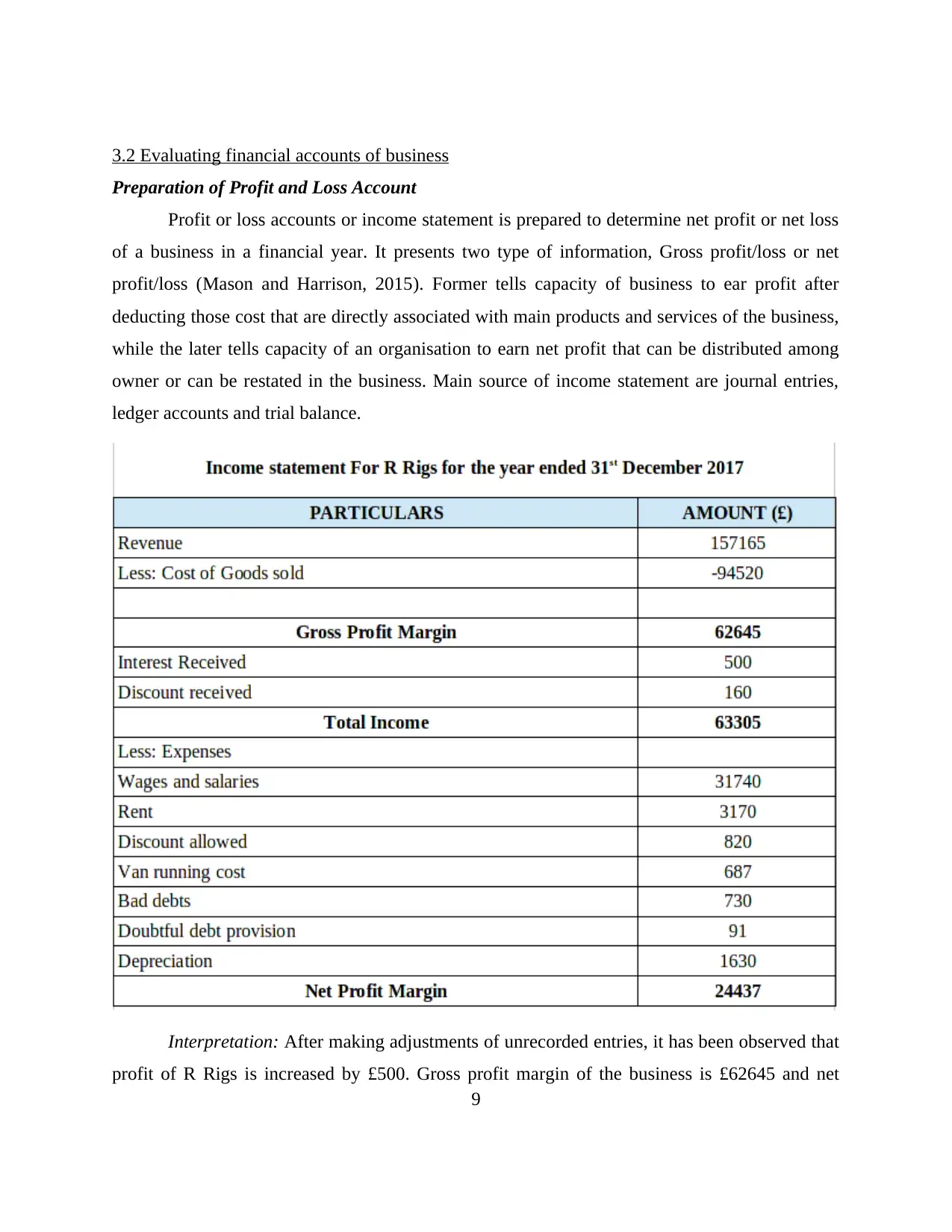

3.2 Evaluating financial accounts of business

Preparation of Profit and Loss Account

Profit or loss accounts or income statement is prepared to determine net profit or net loss

of a business in a financial year. It presents two type of information, Gross profit/loss or net

profit/loss (Mason and Harrison, 2015). Former tells capacity of business to ear profit after

deducting those cost that are directly associated with main products and services of the business,

while the later tells capacity of an organisation to earn net profit that can be distributed among

owner or can be restated in the business. Main source of income statement are journal entries,

ledger accounts and trial balance.

Interpretation: After making adjustments of unrecorded entries, it has been observed that

profit of R Rigs is increased by £500. Gross profit margin of the business is £62645 and net

9

Preparation of Profit and Loss Account

Profit or loss accounts or income statement is prepared to determine net profit or net loss

of a business in a financial year. It presents two type of information, Gross profit/loss or net

profit/loss (Mason and Harrison, 2015). Former tells capacity of business to ear profit after

deducting those cost that are directly associated with main products and services of the business,

while the later tells capacity of an organisation to earn net profit that can be distributed among

owner or can be restated in the business. Main source of income statement are journal entries,

ledger accounts and trial balance.

Interpretation: After making adjustments of unrecorded entries, it has been observed that

profit of R Rigs is increased by £500. Gross profit margin of the business is £62645 and net

9

profit margin of the business is £24437. This means profit earning capacity of business is good

enough but due to its high indirect expenses its net profit comes down to 2/5th level of gross

profit. Therefore, R Rigs is required to control its indirect expenses, specially wages and salary

that are costing to £31740.

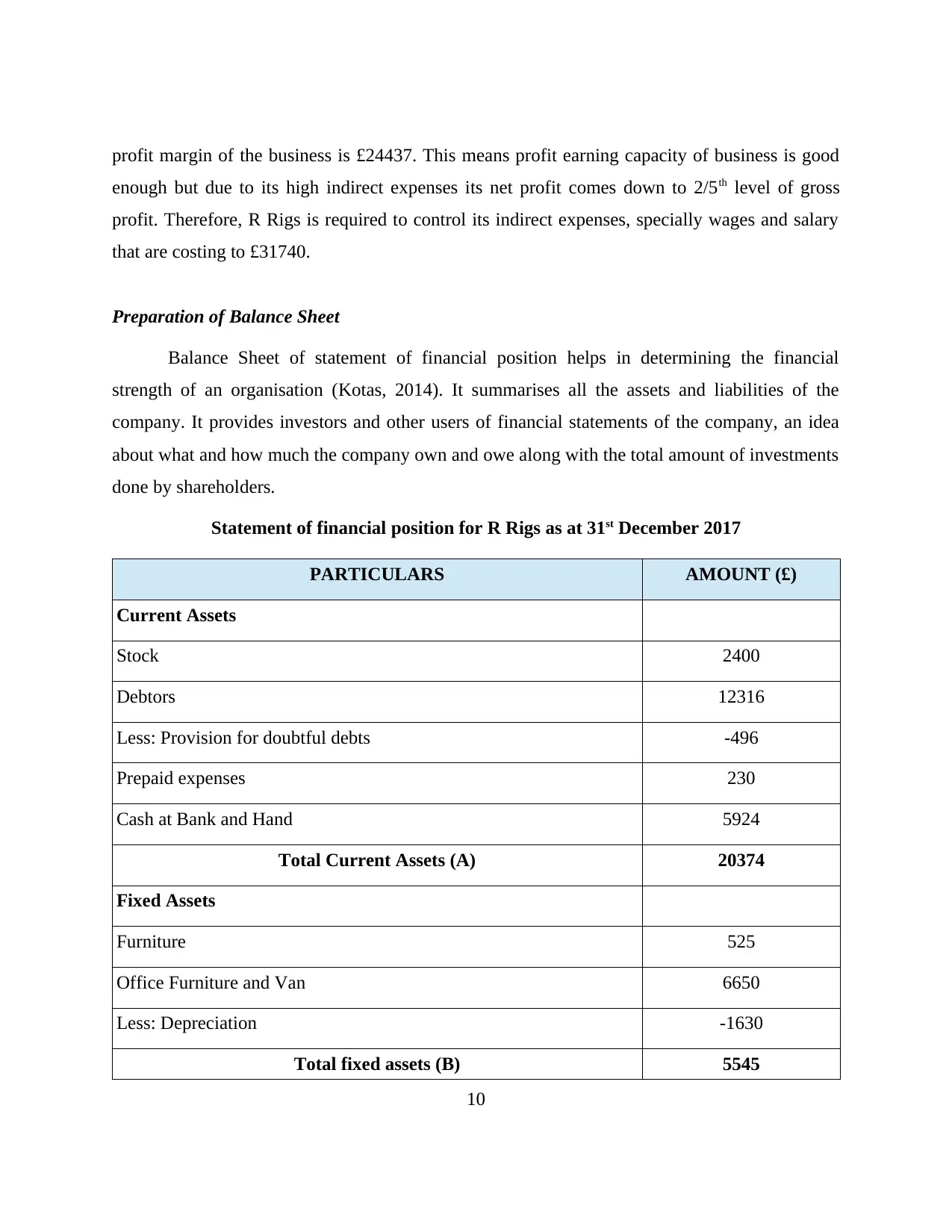

Preparation of Balance Sheet

Balance Sheet of statement of financial position helps in determining the financial

strength of an organisation (Kotas, 2014). It summarises all the assets and liabilities of the

company. It provides investors and other users of financial statements of the company, an idea

about what and how much the company own and owe along with the total amount of investments

done by shareholders.

Statement of financial position for R Rigs as at 31st December 2017

PARTICULARS AMOUNT (£)

Current Assets

Stock 2400

Debtors 12316

Less: Provision for doubtful debts -496

Prepaid expenses 230

Cash at Bank and Hand 5924

Total Current Assets (A) 20374

Fixed Assets

Furniture 525

Office Furniture and Van 6650

Less: Depreciation -1630

Total fixed assets (B) 5545

10

enough but due to its high indirect expenses its net profit comes down to 2/5th level of gross

profit. Therefore, R Rigs is required to control its indirect expenses, specially wages and salary

that are costing to £31740.

Preparation of Balance Sheet

Balance Sheet of statement of financial position helps in determining the financial

strength of an organisation (Kotas, 2014). It summarises all the assets and liabilities of the

company. It provides investors and other users of financial statements of the company, an idea

about what and how much the company own and owe along with the total amount of investments

done by shareholders.

Statement of financial position for R Rigs as at 31st December 2017

PARTICULARS AMOUNT (£)

Current Assets

Stock 2400

Debtors 12316

Less: Provision for doubtful debts -496

Prepaid expenses 230

Cash at Bank and Hand 5924

Total Current Assets (A) 20374

Fixed Assets

Furniture 525

Office Furniture and Van 6650

Less: Depreciation -1630

Total fixed assets (B) 5545

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.