Finance in Hospitality: Cost Analysis, Variance, and Ratio Evaluation

VerifiedAdded on 2020/06/06

|13

|2978

|45

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hospitality industry. It begins by exploring various sources of funding for new and existing businesses, differentiating between personal investment, venture capital, bank loans, debentures, and retained earnings, and their respective advantages and disadvantages. The report then delves into income generation methods such as sales promotion, sub-letting, and sponsorship. A detailed examination of cost elements, including material, direct labor, and indirect expenses, is followed by an analysis of gross profit percentages, selling price determination, and methods for controlling stock and cash. The report further covers the creation and evaluation of trial balances, including adjustments for machinery costs and incorrect salary entries, alongside the preparation of trading and income statements. Budgetary control processes and their purposes are discussed, along with the calculation of variable cost variance. Finally, the report analyzes financial ratios, including sales growth, gross profit margin, net profit margin, stock turnover, and liquidity ratios, offering recommendations based on the findings. The report concludes with a review of cost categorization and contribution per unit calculations, justifying short-term management decisions based on the financial analysis.

Finance in Hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of funding to new and existing business .................................................................3

1.2 Contribution of different range of methods of generating income.......................................4

TASK 2............................................................................................................................................4

2.1 cost.......................................................................................................................................4

(a) Elements of cost ....................................................................................................................4

(b) Gross profit percentages and selling price.............................................................................5

2.2 Methods of controlling stock and cash..................................................................................5

TASK 3............................................................................................................................................6

3.1: Source of trail balance..........................................................................................................6

3.2: Evaluating business account ...............................................................................................7

3.3: Process and purpose of budgetary control ..........................................................................9

3.4: Calculation of variable cost variance...................................................................................9

TASK 4..........................................................................................................................................10

4.1: Calculation and evaluation of ratios...................................................................................10

4.2: Recommendation ..............................................................................................................10

TASK 5..........................................................................................................................................11

5.1: Making categories of various costs....................................................................................11

5.2: Calculation of Contribution per units.................................................................................11

5.3: Justification of short-term management decision .............................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of funding to new and existing business .................................................................3

1.2 Contribution of different range of methods of generating income.......................................4

TASK 2............................................................................................................................................4

2.1 cost.......................................................................................................................................4

(a) Elements of cost ....................................................................................................................4

(b) Gross profit percentages and selling price.............................................................................5

2.2 Methods of controlling stock and cash..................................................................................5

TASK 3............................................................................................................................................6

3.1: Source of trail balance..........................................................................................................6

3.2: Evaluating business account ...............................................................................................7

3.3: Process and purpose of budgetary control ..........................................................................9

3.4: Calculation of variable cost variance...................................................................................9

TASK 4..........................................................................................................................................10

4.1: Calculation and evaluation of ratios...................................................................................10

4.2: Recommendation ..............................................................................................................10

TASK 5..........................................................................................................................................11

5.1: Making categories of various costs....................................................................................11

5.2: Calculation of Contribution per units.................................................................................11

5.3: Justification of short-term management decision .............................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Finance is an essential aspects which would help business to manage and operate their

overall business operations in effective manner. The primary role of managers is to collect

various information which would assist them to gain maximum competitive advantages over

other companies. As in hospitality sector which is related with finance in order to play an

effective role in managing better service and operations (Altinay, Paraskevas and Jang, 2015).

The primary aspects of this project is focusing different sources of finance and its

implications on hospitality sectors. Financial management would be more essential concepts that

is being analyse under this report. On the basis of various various data collection some valuable

recommendation is been done in more effective manner toward hospitality sectors.

TASK 1

1.1 Sources of funding to new and existing business

There are large number of sources of funds for new and existing business which are

mentioned below:

New businesses

Personal Investment: One of the major source of fund is personal investment in their

own new business with the help of their own cash and collateral on your assets.

Advantages: It provides the message to the investors and bankers that having long term

commitment with projects and ready to take high risks.

Disadvantage: Lack of professional investment advice.

Venture capital: It is a type of private equity which provides funds to small and

emerging firms which have potential to earn large number of profits and having high growth

opportunities.

Advantages: It helps the entrepreneur to build their company with OPM through

specialist investor support.

Disadvantage: Loss of control over operations (Bar-Tal, 2012).

Existing business

Bank loan: One of the effective source through large number of funds are raised.

Advantages: Easy to raise finance

Disadvantage: Have to pay high interest rates

3

Finance is an essential aspects which would help business to manage and operate their

overall business operations in effective manner. The primary role of managers is to collect

various information which would assist them to gain maximum competitive advantages over

other companies. As in hospitality sector which is related with finance in order to play an

effective role in managing better service and operations (Altinay, Paraskevas and Jang, 2015).

The primary aspects of this project is focusing different sources of finance and its

implications on hospitality sectors. Financial management would be more essential concepts that

is being analyse under this report. On the basis of various various data collection some valuable

recommendation is been done in more effective manner toward hospitality sectors.

TASK 1

1.1 Sources of funding to new and existing business

There are large number of sources of funds for new and existing business which are

mentioned below:

New businesses

Personal Investment: One of the major source of fund is personal investment in their

own new business with the help of their own cash and collateral on your assets.

Advantages: It provides the message to the investors and bankers that having long term

commitment with projects and ready to take high risks.

Disadvantage: Lack of professional investment advice.

Venture capital: It is a type of private equity which provides funds to small and

emerging firms which have potential to earn large number of profits and having high growth

opportunities.

Advantages: It helps the entrepreneur to build their company with OPM through

specialist investor support.

Disadvantage: Loss of control over operations (Bar-Tal, 2012).

Existing business

Bank loan: One of the effective source through large number of funds are raised.

Advantages: Easy to raise finance

Disadvantage: Have to pay high interest rates

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debentures: Another source which helps to raise money from public.

Advantages: Control is not surrendered to investors

Disadvantage: Need to pay interest even run in loss

Retained earnings: Out of the profit which is not paid as dividend

Advantages: Provides financial stability

Disadvantage: Improper utilisation of funds

1.2 Contribution of different range of methods of generating income

There are different methods which helps the business to earn large number of profits are

defined below:

Sales promotion: It is important promotional mix element which helps to bring

awareness among the customers about diversified business products and services. It includes the

use of media and non-media marketing communications which helps to increase demand,

improved quality of product and stimulate market demand. The major benefits of this method are

attraction of new customers, retention of old customers, drive their competitors out of the market

etc (Bowie, Buttle and Brookes, 2016).

Sub-Letting: It includes the process of leasing of the property or machine to use by some

other person. It provides the opportunity to the management of business is to earn profit in the

form of rent or interest.

Sponsorship: It refers to the providence of support by the business regarding

performance of any act, event, activity or organisation. Such support is provided by the

organisation in financial and any other form. It helps to earn large number of profits through

diversified activities.

TASK 2

2.1 cost

(a) Elements of cost

Cost: It is an amount which is paid by the organisation regarding production of their

products and services. The monetary valuation of every aspect is included in cost like material,

labour, efforts, opportunity cost etc.

The major three elements of cost are defined below:

4

Advantages: Control is not surrendered to investors

Disadvantage: Need to pay interest even run in loss

Retained earnings: Out of the profit which is not paid as dividend

Advantages: Provides financial stability

Disadvantage: Improper utilisation of funds

1.2 Contribution of different range of methods of generating income

There are different methods which helps the business to earn large number of profits are

defined below:

Sales promotion: It is important promotional mix element which helps to bring

awareness among the customers about diversified business products and services. It includes the

use of media and non-media marketing communications which helps to increase demand,

improved quality of product and stimulate market demand. The major benefits of this method are

attraction of new customers, retention of old customers, drive their competitors out of the market

etc (Bowie, Buttle and Brookes, 2016).

Sub-Letting: It includes the process of leasing of the property or machine to use by some

other person. It provides the opportunity to the management of business is to earn profit in the

form of rent or interest.

Sponsorship: It refers to the providence of support by the business regarding

performance of any act, event, activity or organisation. Such support is provided by the

organisation in financial and any other form. It helps to earn large number of profits through

diversified activities.

TASK 2

2.1 cost

(a) Elements of cost

Cost: It is an amount which is paid by the organisation regarding production of their

products and services. The monetary valuation of every aspect is included in cost like material,

labour, efforts, opportunity cost etc.

The major three elements of cost are defined below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material: It can be of two types direct or indirect. The materials which are directly used

in the production of finished product is called as direct material. For ex., wood in

furniture and leather in shoes. The supporting material which is used in production is

known as indirect material. For ex., nails in shoes or furniture (Hoque, 2013).

Direct labour: It includes about the wages which are paid to workers which provides

their function in production process is called direct labour. For ex., supervision,

maintenance, transaction of material which is converted into final product etc.

Indirect Expenses: It is also known as overheads. It includes the expenses which are

incurred on material and labour. It can be classified as:

- Production or manufacturing overheads

- Administrative expenses

- Selling expenses

- Distribution expenses

(b) Gross profit percentages and selling price

Gross profit percentages: It is the ratio which provides the relationship of organisational

profit as percentage of sales. It helps in comparison of profits of two companies.

GPP= Gross profit/ Total sales*100

Selling price + COGS + Mark up

The net profit is attained by the organisation after subtraction of all the expenses like rent,

salaries and taxes from gross profit.

2.2 Methods of controlling stock and cash

Cash control method

Implementation of cash handling policies: It includes about determination of the

strategies which helps in maintenance of cash in organisation.

Accountability form: It includes preparation of cash accounting forms which is further

used to overcome from losses.

Set cash flow target: Forecast about requirement of cash in organisation for effective

control

Stock controlling methods

Just in time: It helps in ordering of the actual quantity of stock. It provides the

opportunity regarding reduction of unnecessary costs.

5

in the production of finished product is called as direct material. For ex., wood in

furniture and leather in shoes. The supporting material which is used in production is

known as indirect material. For ex., nails in shoes or furniture (Hoque, 2013).

Direct labour: It includes about the wages which are paid to workers which provides

their function in production process is called direct labour. For ex., supervision,

maintenance, transaction of material which is converted into final product etc.

Indirect Expenses: It is also known as overheads. It includes the expenses which are

incurred on material and labour. It can be classified as:

- Production or manufacturing overheads

- Administrative expenses

- Selling expenses

- Distribution expenses

(b) Gross profit percentages and selling price

Gross profit percentages: It is the ratio which provides the relationship of organisational

profit as percentage of sales. It helps in comparison of profits of two companies.

GPP= Gross profit/ Total sales*100

Selling price + COGS + Mark up

The net profit is attained by the organisation after subtraction of all the expenses like rent,

salaries and taxes from gross profit.

2.2 Methods of controlling stock and cash

Cash control method

Implementation of cash handling policies: It includes about determination of the

strategies which helps in maintenance of cash in organisation.

Accountability form: It includes preparation of cash accounting forms which is further

used to overcome from losses.

Set cash flow target: Forecast about requirement of cash in organisation for effective

control

Stock controlling methods

Just in time: It helps in ordering of the actual quantity of stock. It provides the

opportunity regarding reduction of unnecessary costs.

5

Formulation of inventory budget: Preparation of budget in advance about material,

logistics, operational and other costs.

Perpetual inventory system: It helps to track over quantity and value of stock.

TASK 3

3.1: Source of trail balance

Trial balance: It is the document which provides the information regarding expenses and

income which is incurred by the organisation during specified period of time. The balances are

complied into debit and credit columns. All the information which is present in trail balance is

taken from the ledger accounts.

Format of Trail Balance as per year ended XXXX

Particulars Debit Amount Credit Amount

Cash and Bank XXX

Bills payable XXX

Office supplies XXX

Salaries XXX

Bank loan XXX

Accounts receivable XXX

Rent Expenses XXX

Common stock XXX

Office equipments XXX

Enquire Revenue XXX

Supplies XXX

Other expenses XXX

TOTAL

3.2: Evaluating business account

In management accounting, trail balance is said to be primary object which is being used

for the purpose of formulating final accounts (Moutinho, 2011). This would eliminate a lot of

6

logistics, operational and other costs.

Perpetual inventory system: It helps to track over quantity and value of stock.

TASK 3

3.1: Source of trail balance

Trial balance: It is the document which provides the information regarding expenses and

income which is incurred by the organisation during specified period of time. The balances are

complied into debit and credit columns. All the information which is present in trail balance is

taken from the ledger accounts.

Format of Trail Balance as per year ended XXXX

Particulars Debit Amount Credit Amount

Cash and Bank XXX

Bills payable XXX

Office supplies XXX

Salaries XXX

Bank loan XXX

Accounts receivable XXX

Rent Expenses XXX

Common stock XXX

Office equipments XXX

Enquire Revenue XXX

Supplies XXX

Other expenses XXX

TOTAL

3.2: Evaluating business account

In management accounting, trail balance is said to be primary object which is being used

for the purpose of formulating final accounts (Moutinho, 2011). This would eliminate a lot of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

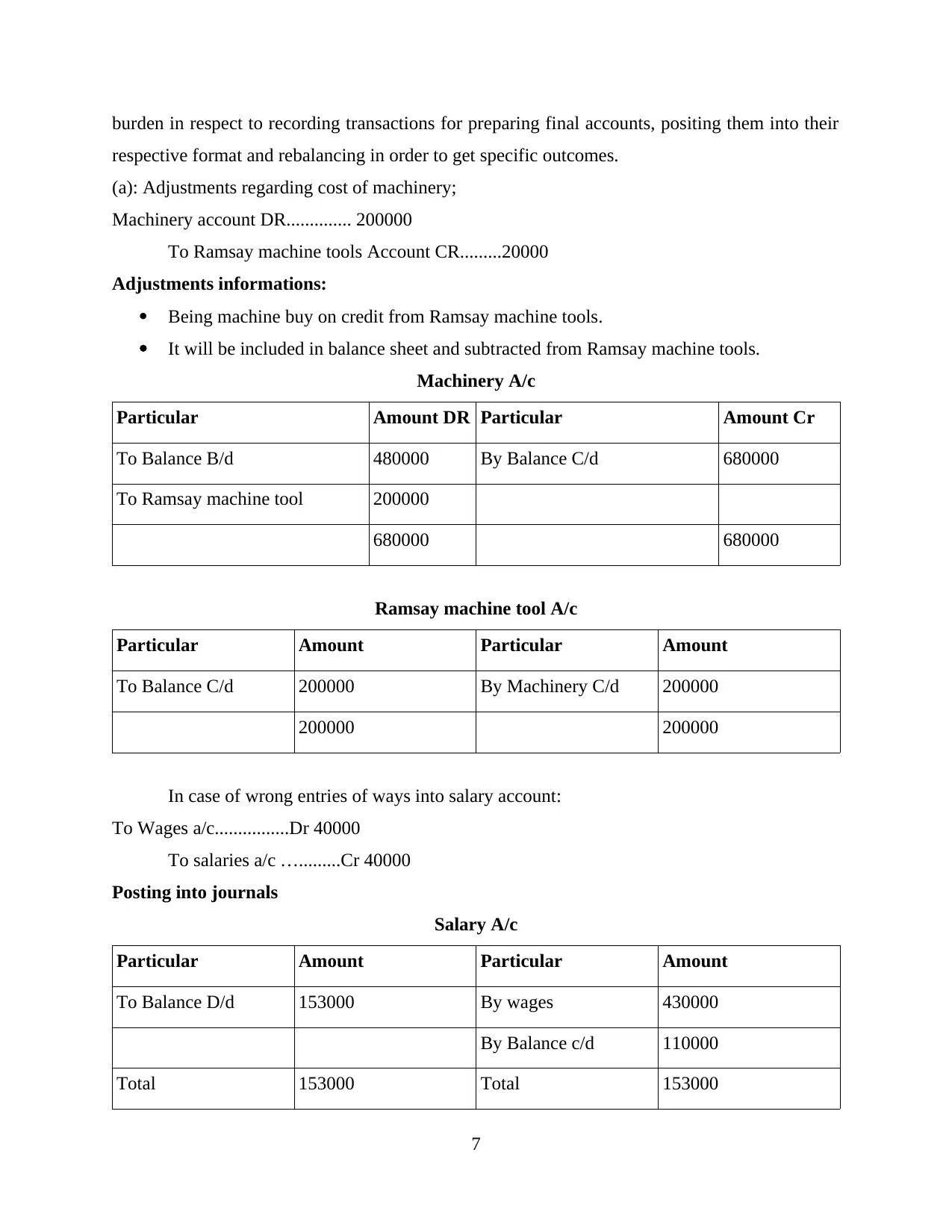

burden in respect to recording transactions for preparing final accounts, positing them into their

respective format and rebalancing in order to get specific outcomes.

(a): Adjustments regarding cost of machinery;

Machinery account DR.............. 200000

To Ramsay machine tools Account CR.........20000

Adjustments informations:

Being machine buy on credit from Ramsay machine tools.

It will be included in balance sheet and subtracted from Ramsay machine tools.

Machinery A/c

Particular Amount DR Particular Amount Cr

To Balance B/d 480000 By Balance C/d 680000

To Ramsay machine tool 200000

680000 680000

Ramsay machine tool A/c

Particular Amount Particular Amount

To Balance C/d 200000 By Machinery C/d 200000

200000 200000

In case of wrong entries of ways into salary account:

To Wages a/c................Dr 40000

To salaries a/c ….........Cr 40000

Posting into journals

Salary A/c

Particular Amount Particular Amount

To Balance D/d 153000 By wages 430000

By Balance c/d 110000

Total 153000 Total 153000

7

respective format and rebalancing in order to get specific outcomes.

(a): Adjustments regarding cost of machinery;

Machinery account DR.............. 200000

To Ramsay machine tools Account CR.........20000

Adjustments informations:

Being machine buy on credit from Ramsay machine tools.

It will be included in balance sheet and subtracted from Ramsay machine tools.

Machinery A/c

Particular Amount DR Particular Amount Cr

To Balance B/d 480000 By Balance C/d 680000

To Ramsay machine tool 200000

680000 680000

Ramsay machine tool A/c

Particular Amount Particular Amount

To Balance C/d 200000 By Machinery C/d 200000

200000 200000

In case of wrong entries of ways into salary account:

To Wages a/c................Dr 40000

To salaries a/c ….........Cr 40000

Posting into journals

Salary A/c

Particular Amount Particular Amount

To Balance D/d 153000 By wages 430000

By Balance c/d 110000

Total 153000 Total 153000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

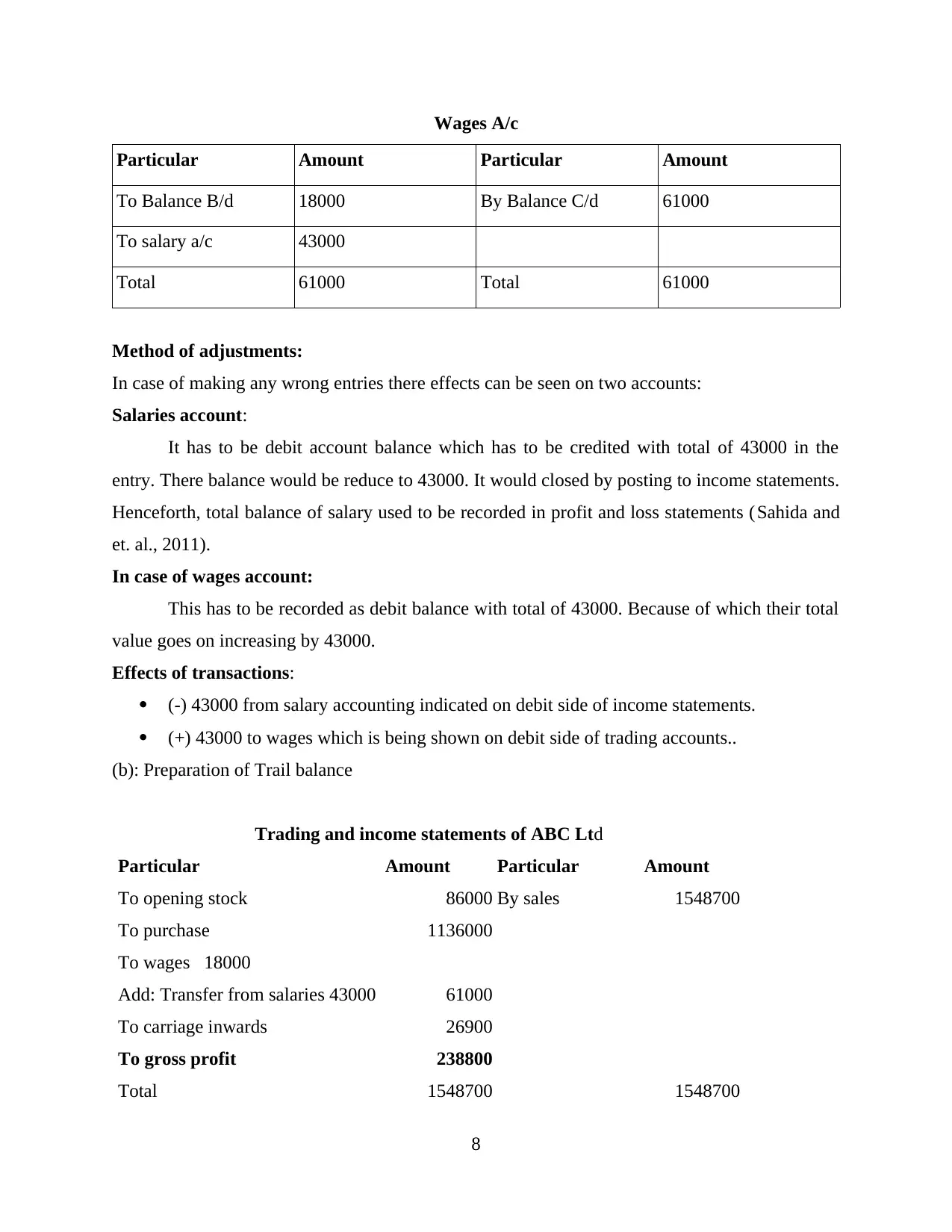

Wages A/c

Particular Amount Particular Amount

To Balance B/d 18000 By Balance C/d 61000

To salary a/c 43000

Total 61000 Total 61000

Method of adjustments:

In case of making any wrong entries there effects can be seen on two accounts:

Salaries account:

It has to be debit account balance which has to be credited with total of 43000 in the

entry. There balance would be reduce to 43000. It would closed by posting to income statements.

Henceforth, total balance of salary used to be recorded in profit and loss statements (Sahida and

et. al., 2011).

In case of wages account:

This has to be recorded as debit balance with total of 43000. Because of which their total

value goes on increasing by 43000.

Effects of transactions:

(-) 43000 from salary accounting indicated on debit side of income statements.

(+) 43000 to wages which is being shown on debit side of trading accounts..

(b): Preparation of Trail balance

Trading and income statements of ABC Ltd

Particular Amount Particular Amount

To opening stock 86000 By sales 1548700

To purchase 1136000

To wages 18000

Add: Transfer from salaries 43000 61000

To carriage inwards 26900

To gross profit 238800

Total 1548700 1548700

8

Particular Amount Particular Amount

To Balance B/d 18000 By Balance C/d 61000

To salary a/c 43000

Total 61000 Total 61000

Method of adjustments:

In case of making any wrong entries there effects can be seen on two accounts:

Salaries account:

It has to be debit account balance which has to be credited with total of 43000 in the

entry. There balance would be reduce to 43000. It would closed by posting to income statements.

Henceforth, total balance of salary used to be recorded in profit and loss statements (Sahida and

et. al., 2011).

In case of wages account:

This has to be recorded as debit balance with total of 43000. Because of which their total

value goes on increasing by 43000.

Effects of transactions:

(-) 43000 from salary accounting indicated on debit side of income statements.

(+) 43000 to wages which is being shown on debit side of trading accounts..

(b): Preparation of Trail balance

Trading and income statements of ABC Ltd

Particular Amount Particular Amount

To opening stock 86000 By sales 1548700

To purchase 1136000

To wages 18000

Add: Transfer from salaries 43000 61000

To carriage inwards 26900

To gross profit 238800

Total 1548700 1548700

8

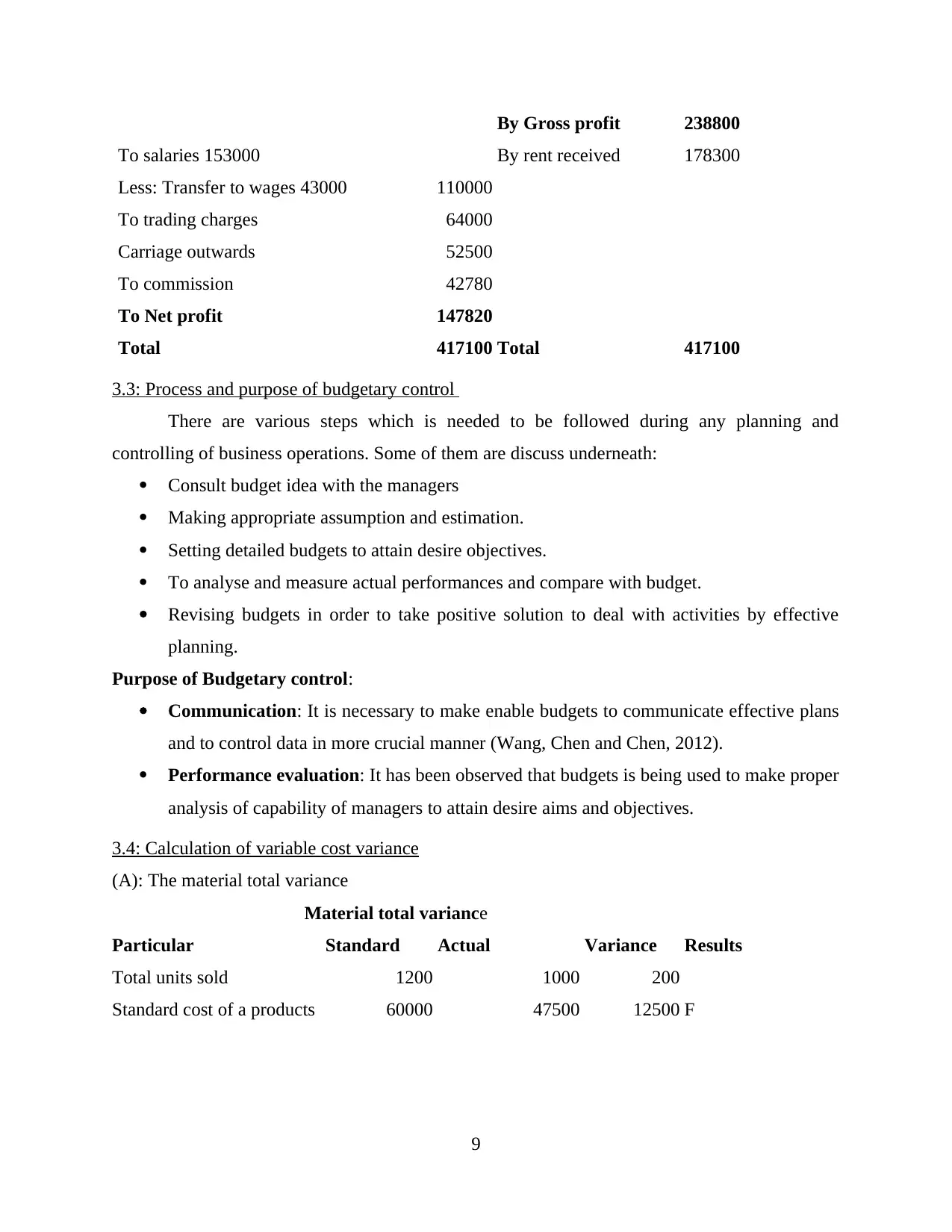

By Gross profit 238800

To salaries 153000 By rent received 178300

Less: Transfer to wages 43000 110000

To trading charges 64000

Carriage outwards 52500

To commission 42780

To Net profit 147820

Total 417100 Total 417100

3.3: Process and purpose of budgetary control

There are various steps which is needed to be followed during any planning and

controlling of business operations. Some of them are discuss underneath:

Consult budget idea with the managers

Making appropriate assumption and estimation.

Setting detailed budgets to attain desire objectives.

To analyse and measure actual performances and compare with budget.

Revising budgets in order to take positive solution to deal with activities by effective

planning.

Purpose of Budgetary control:

Communication: It is necessary to make enable budgets to communicate effective plans

and to control data in more crucial manner (Wang, Chen and Chen, 2012).

Performance evaluation: It has been observed that budgets is being used to make proper

analysis of capability of managers to attain desire aims and objectives.

3.4: Calculation of variable cost variance

(A): The material total variance

Material total variance

Particular Standard Actual Variance Results

Total units sold 1200 1000 200

Standard cost of a products 60000 47500 12500 F

9

To salaries 153000 By rent received 178300

Less: Transfer to wages 43000 110000

To trading charges 64000

Carriage outwards 52500

To commission 42780

To Net profit 147820

Total 417100 Total 417100

3.3: Process and purpose of budgetary control

There are various steps which is needed to be followed during any planning and

controlling of business operations. Some of them are discuss underneath:

Consult budget idea with the managers

Making appropriate assumption and estimation.

Setting detailed budgets to attain desire objectives.

To analyse and measure actual performances and compare with budget.

Revising budgets in order to take positive solution to deal with activities by effective

planning.

Purpose of Budgetary control:

Communication: It is necessary to make enable budgets to communicate effective plans

and to control data in more crucial manner (Wang, Chen and Chen, 2012).

Performance evaluation: It has been observed that budgets is being used to make proper

analysis of capability of managers to attain desire aims and objectives.

3.4: Calculation of variable cost variance

(A): The material total variance

Material total variance

Particular Standard Actual Variance Results

Total units sold 1200 1000 200

Standard cost of a products 60000 47500 12500 F

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

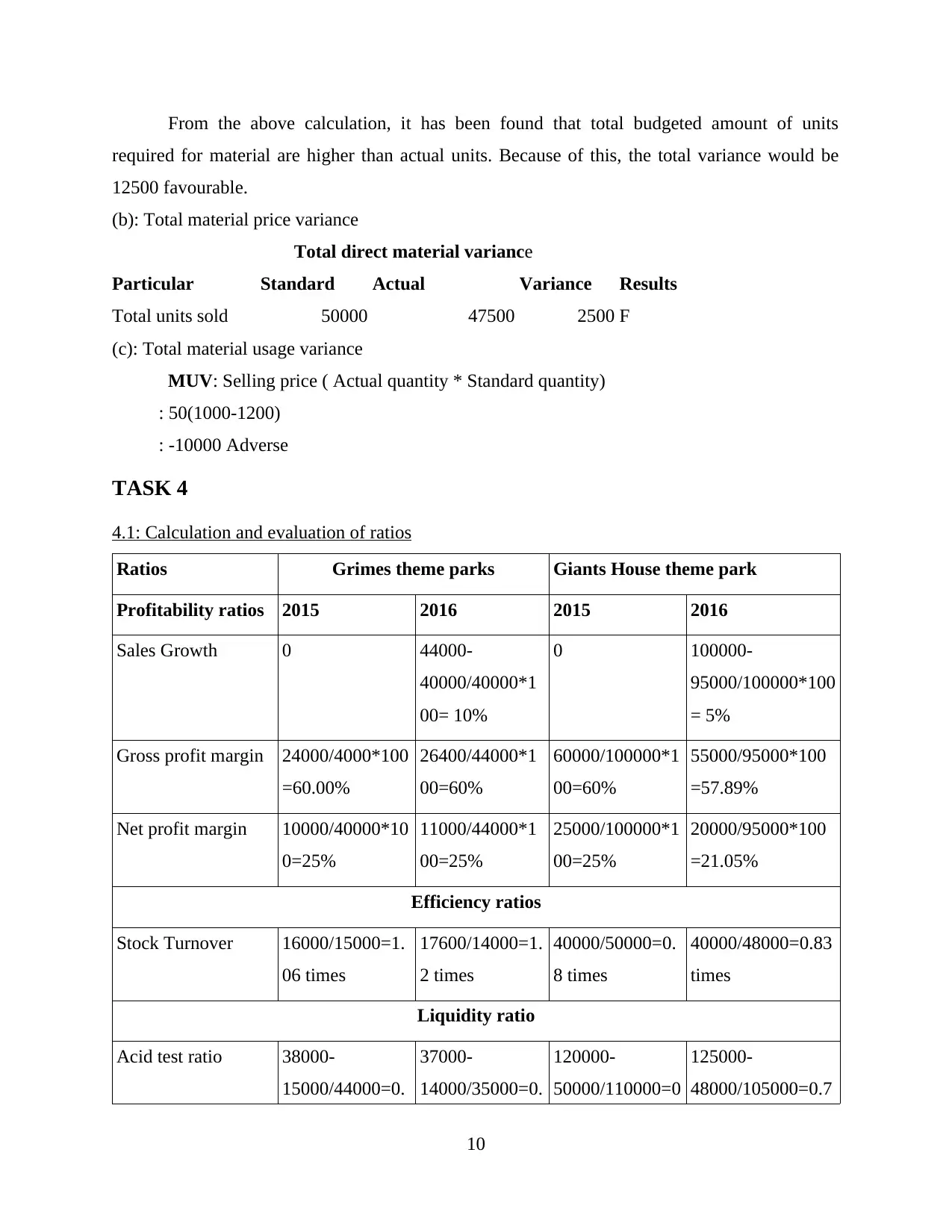

From the above calculation, it has been found that total budgeted amount of units

required for material are higher than actual units. Because of this, the total variance would be

12500 favourable.

(b): Total material price variance

Total direct material variance

Particular Standard Actual Variance Results

Total units sold 50000 47500 2500 F

(c): Total material usage variance

MUV: Selling price ( Actual quantity * Standard quantity)

: 50(1000-1200)

: -10000 Adverse

TASK 4

4.1: Calculation and evaluation of ratios

Ratios Grimes theme parks Giants House theme park

Profitability ratios 2015 2016 2015 2016

Sales Growth 0 44000-

40000/40000*1

00= 10%

0 100000-

95000/100000*100

= 5%

Gross profit margin 24000/4000*100

=60.00%

26400/44000*1

00=60%

60000/100000*1

00=60%

55000/95000*100

=57.89%

Net profit margin 10000/40000*10

0=25%

11000/44000*1

00=25%

25000/100000*1

00=25%

20000/95000*100

=21.05%

Efficiency ratios

Stock Turnover 16000/15000=1.

06 times

17600/14000=1.

2 times

40000/50000=0.

8 times

40000/48000=0.83

times

Liquidity ratio

Acid test ratio 38000-

15000/44000=0.

37000-

14000/35000=0.

120000-

50000/110000=0

125000-

48000/105000=0.7

10

required for material are higher than actual units. Because of this, the total variance would be

12500 favourable.

(b): Total material price variance

Total direct material variance

Particular Standard Actual Variance Results

Total units sold 50000 47500 2500 F

(c): Total material usage variance

MUV: Selling price ( Actual quantity * Standard quantity)

: 50(1000-1200)

: -10000 Adverse

TASK 4

4.1: Calculation and evaluation of ratios

Ratios Grimes theme parks Giants House theme park

Profitability ratios 2015 2016 2015 2016

Sales Growth 0 44000-

40000/40000*1

00= 10%

0 100000-

95000/100000*100

= 5%

Gross profit margin 24000/4000*100

=60.00%

26400/44000*1

00=60%

60000/100000*1

00=60%

55000/95000*100

=57.89%

Net profit margin 10000/40000*10

0=25%

11000/44000*1

00=25%

25000/100000*1

00=25%

20000/95000*100

=21.05%

Efficiency ratios

Stock Turnover 16000/15000=1.

06 times

17600/14000=1.

2 times

40000/50000=0.

8 times

40000/48000=0.83

times

Liquidity ratio

Acid test ratio 38000-

15000/44000=0.

37000-

14000/35000=0.

120000-

50000/110000=0

125000-

48000/105000=0.7

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

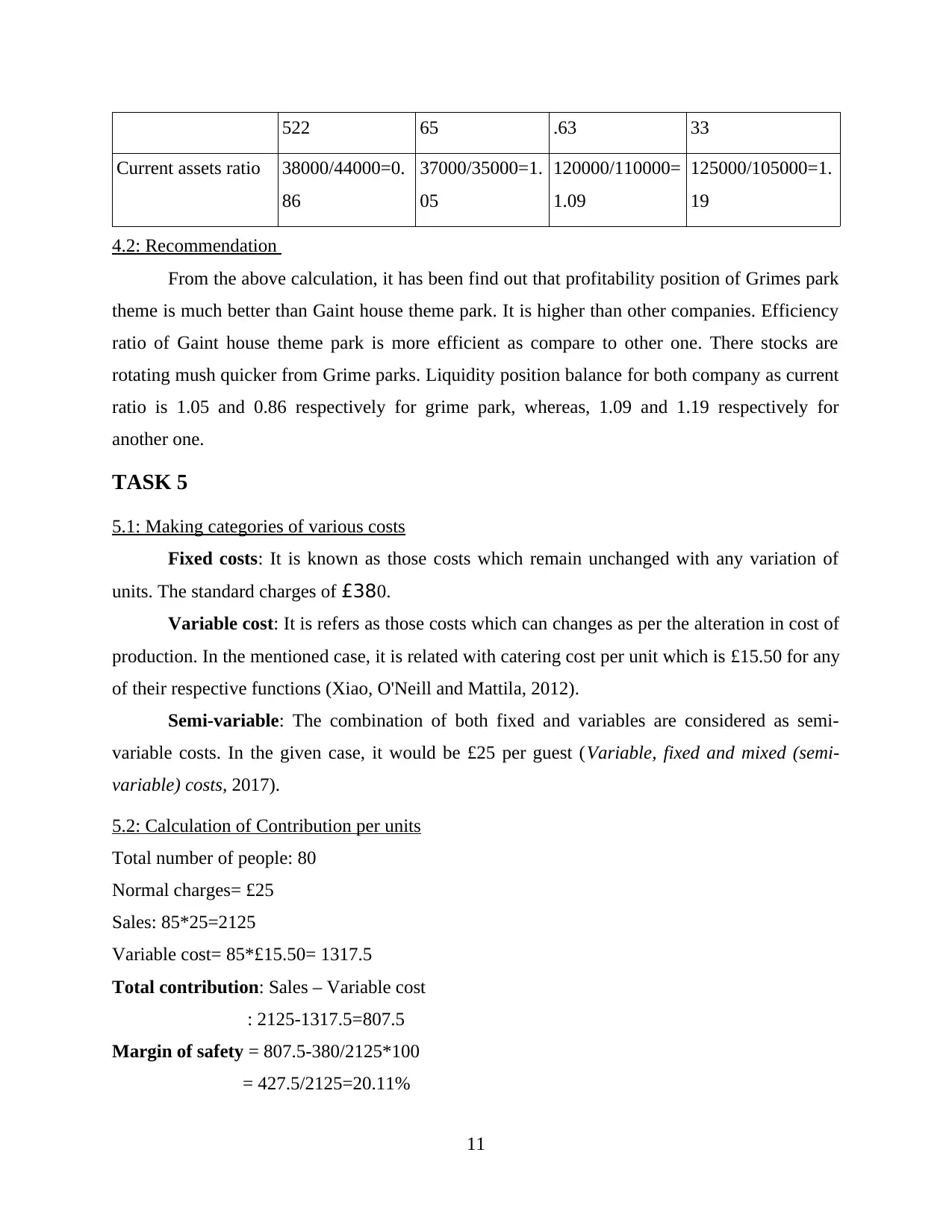

522 65 .63 33

Current assets ratio 38000/44000=0.

86

37000/35000=1.

05

120000/110000=

1.09

125000/105000=1.

19

4.2: Recommendation

From the above calculation, it has been find out that profitability position of Grimes park

theme is much better than Gaint house theme park. It is higher than other companies. Efficiency

ratio of Gaint house theme park is more efficient as compare to other one. There stocks are

rotating mush quicker from Grime parks. Liquidity position balance for both company as current

ratio is 1.05 and 0.86 respectively for grime park, whereas, 1.09 and 1.19 respectively for

another one.

TASK 5

5.1: Making categories of various costs

Fixed costs: It is known as those costs which remain unchanged with any variation of

units. The standard charges of £380.

Variable cost: It is refers as those costs which can changes as per the alteration in cost of

production. In the mentioned case, it is related with catering cost per unit which is £15.50 for any

of their respective functions (Xiao, O'Neill and Mattila, 2012).

Semi-variable: The combination of both fixed and variables are considered as semi-

variable costs. In the given case, it would be £25 per guest (Variable, fixed and mixed (semi-

variable) costs, 2017).

5.2: Calculation of Contribution per units

Total number of people: 80

Normal charges= £25

Sales: 85*25=2125

Variable cost= 85*£15.50= 1317.5

Total contribution: Sales – Variable cost

: 2125-1317.5=807.5

Margin of safety = 807.5-380/2125*100

= 427.5/2125=20.11%

11

Current assets ratio 38000/44000=0.

86

37000/35000=1.

05

120000/110000=

1.09

125000/105000=1.

19

4.2: Recommendation

From the above calculation, it has been find out that profitability position of Grimes park

theme is much better than Gaint house theme park. It is higher than other companies. Efficiency

ratio of Gaint house theme park is more efficient as compare to other one. There stocks are

rotating mush quicker from Grime parks. Liquidity position balance for both company as current

ratio is 1.05 and 0.86 respectively for grime park, whereas, 1.09 and 1.19 respectively for

another one.

TASK 5

5.1: Making categories of various costs

Fixed costs: It is known as those costs which remain unchanged with any variation of

units. The standard charges of £380.

Variable cost: It is refers as those costs which can changes as per the alteration in cost of

production. In the mentioned case, it is related with catering cost per unit which is £15.50 for any

of their respective functions (Xiao, O'Neill and Mattila, 2012).

Semi-variable: The combination of both fixed and variables are considered as semi-

variable costs. In the given case, it would be £25 per guest (Variable, fixed and mixed (semi-

variable) costs, 2017).

5.2: Calculation of Contribution per units

Total number of people: 80

Normal charges= £25

Sales: 85*25=2125

Variable cost= 85*£15.50= 1317.5

Total contribution: Sales – Variable cost

: 2125-1317.5=807.5

Margin of safety = 807.5-380/2125*100

= 427.5/2125=20.11%

11

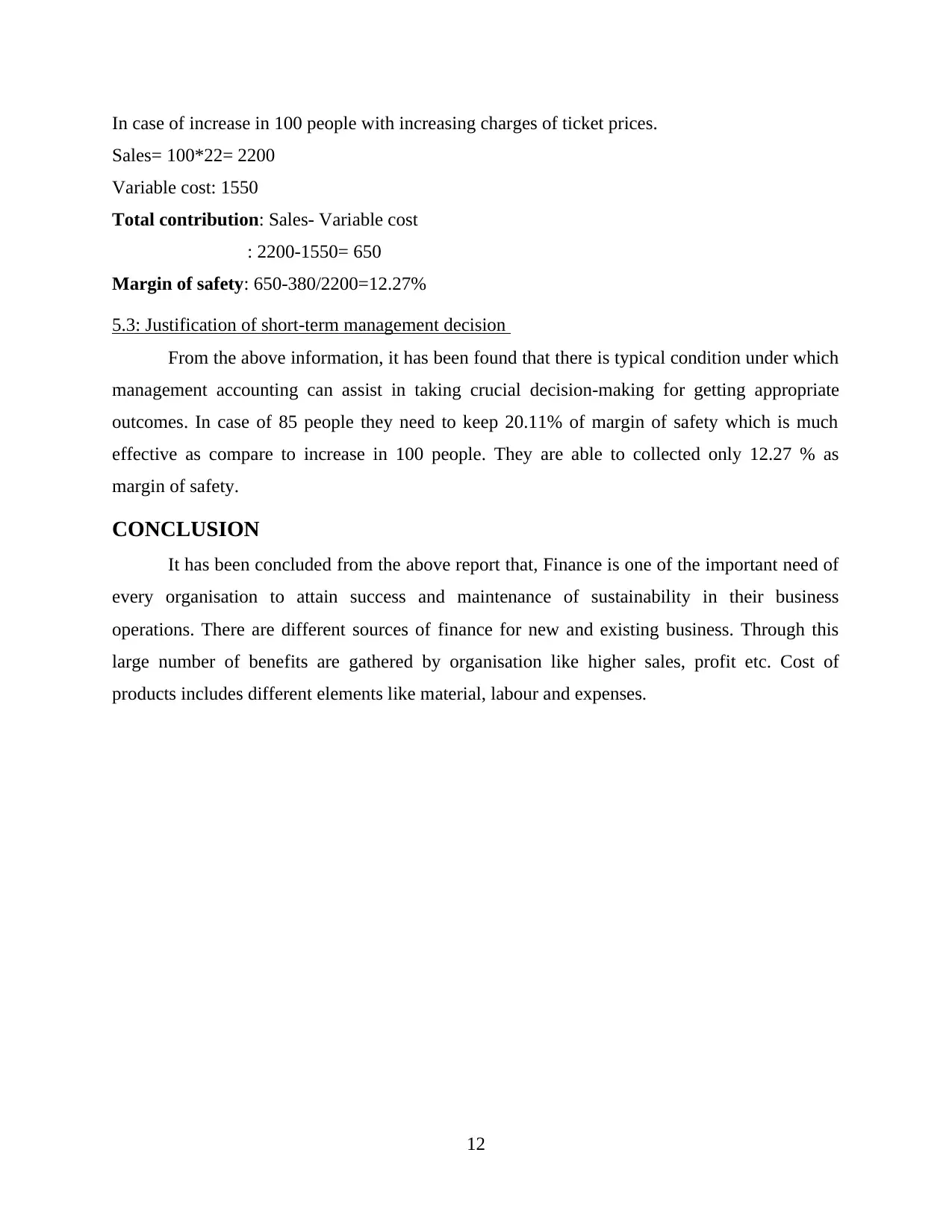

In case of increase in 100 people with increasing charges of ticket prices.

Sales= 100*22= 2200

Variable cost: 1550

Total contribution: Sales- Variable cost

: 2200-1550= 650

Margin of safety: 650-380/2200=12.27%

5.3: Justification of short-term management decision

From the above information, it has been found that there is typical condition under which

management accounting can assist in taking crucial decision-making for getting appropriate

outcomes. In case of 85 people they need to keep 20.11% of margin of safety which is much

effective as compare to increase in 100 people. They are able to collected only 12.27 % as

margin of safety.

CONCLUSION

It has been concluded from the above report that, Finance is one of the important need of

every organisation to attain success and maintenance of sustainability in their business

operations. There are different sources of finance for new and existing business. Through this

large number of benefits are gathered by organisation like higher sales, profit etc. Cost of

products includes different elements like material, labour and expenses.

12

Sales= 100*22= 2200

Variable cost: 1550

Total contribution: Sales- Variable cost

: 2200-1550= 650

Margin of safety: 650-380/2200=12.27%

5.3: Justification of short-term management decision

From the above information, it has been found that there is typical condition under which

management accounting can assist in taking crucial decision-making for getting appropriate

outcomes. In case of 85 people they need to keep 20.11% of margin of safety which is much

effective as compare to increase in 100 people. They are able to collected only 12.27 % as

margin of safety.

CONCLUSION

It has been concluded from the above report that, Finance is one of the important need of

every organisation to attain success and maintenance of sustainability in their business

operations. There are different sources of finance for new and existing business. Through this

large number of benefits are gathered by organisation like higher sales, profit etc. Cost of

products includes different elements like material, labour and expenses.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.