MA514 Business Finance Report: Housing Price Analysis and Loan Options

VerifiedAdded on 2023/06/11

|11

|2161

|403

Report

AI Summary

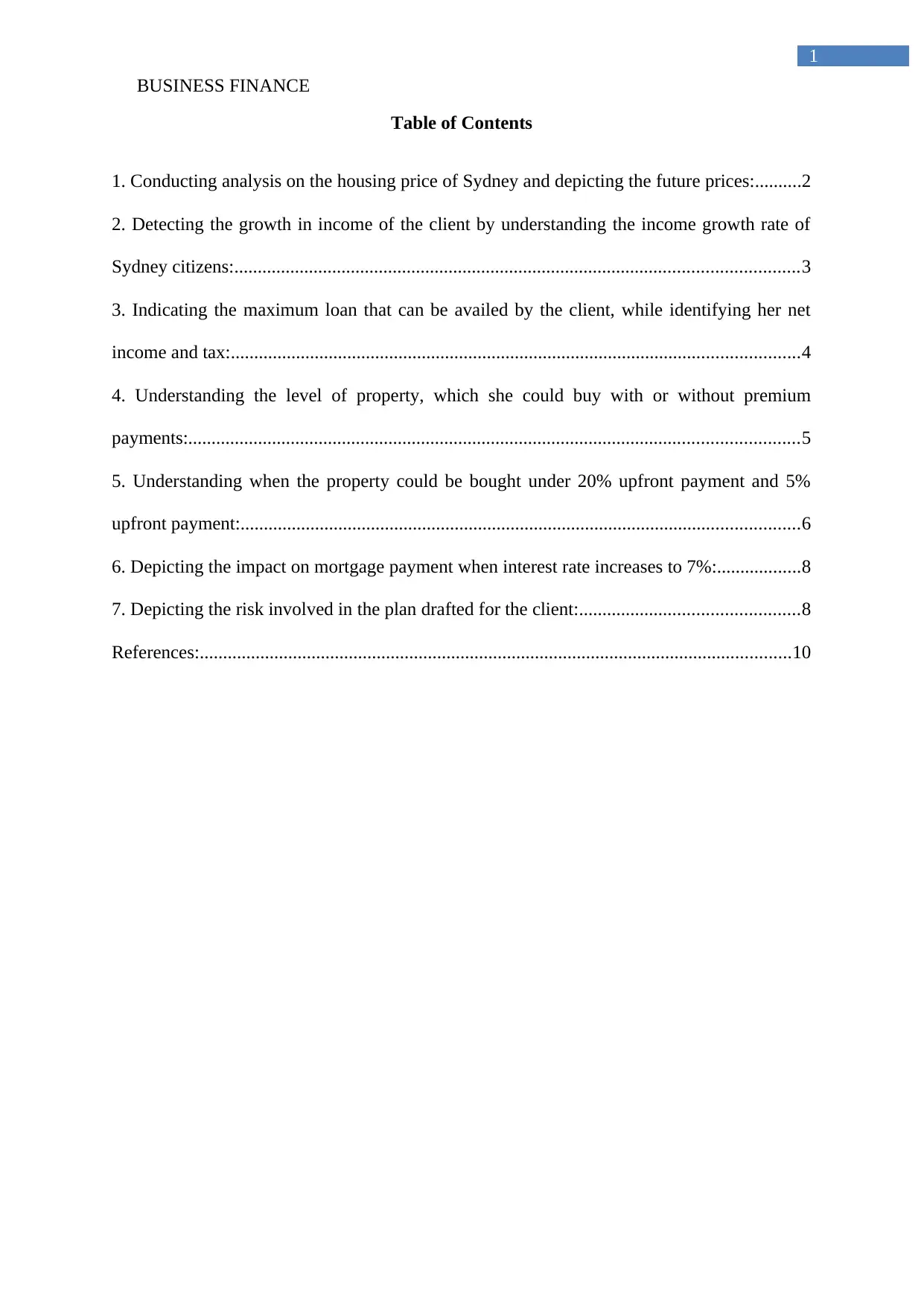

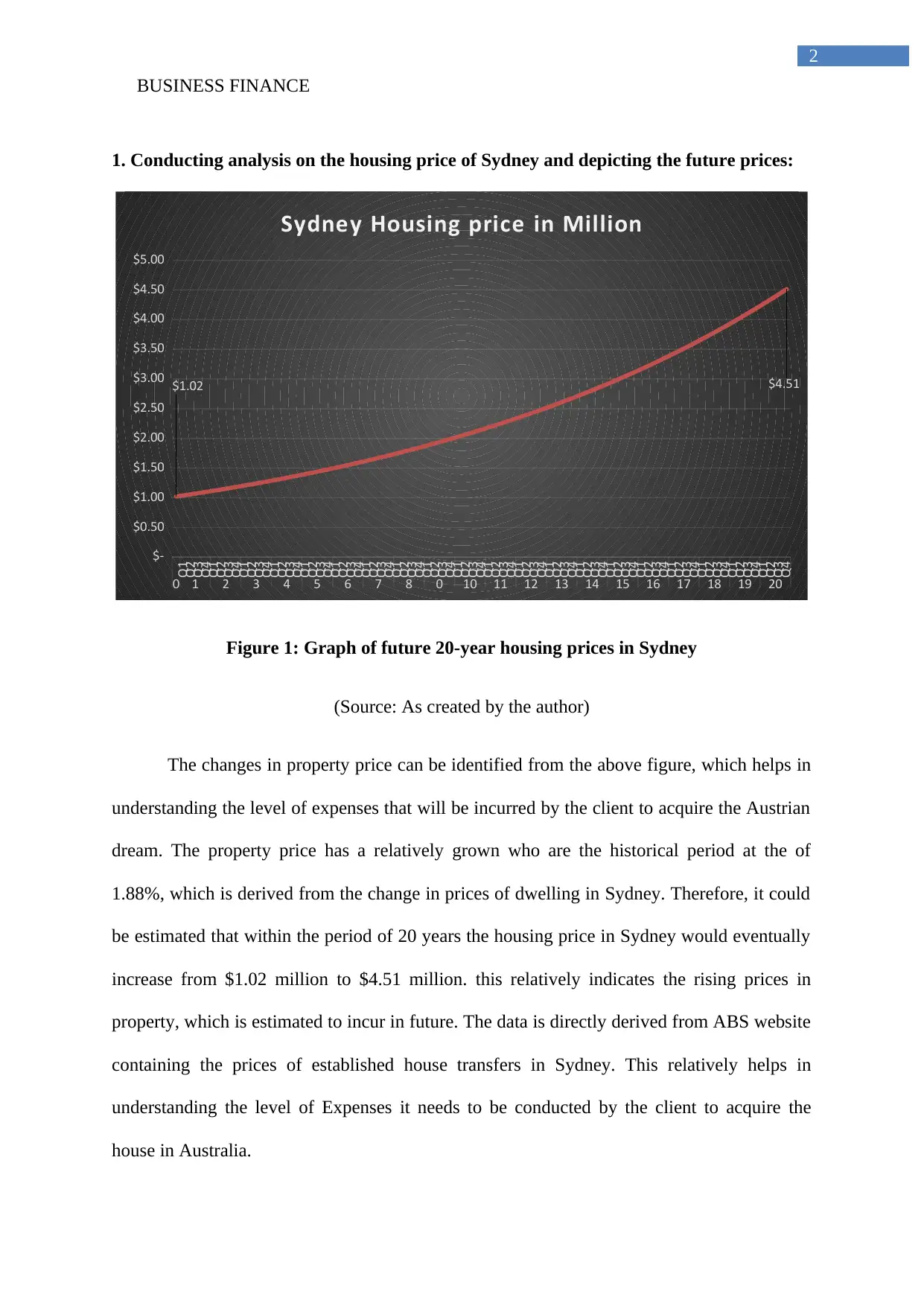

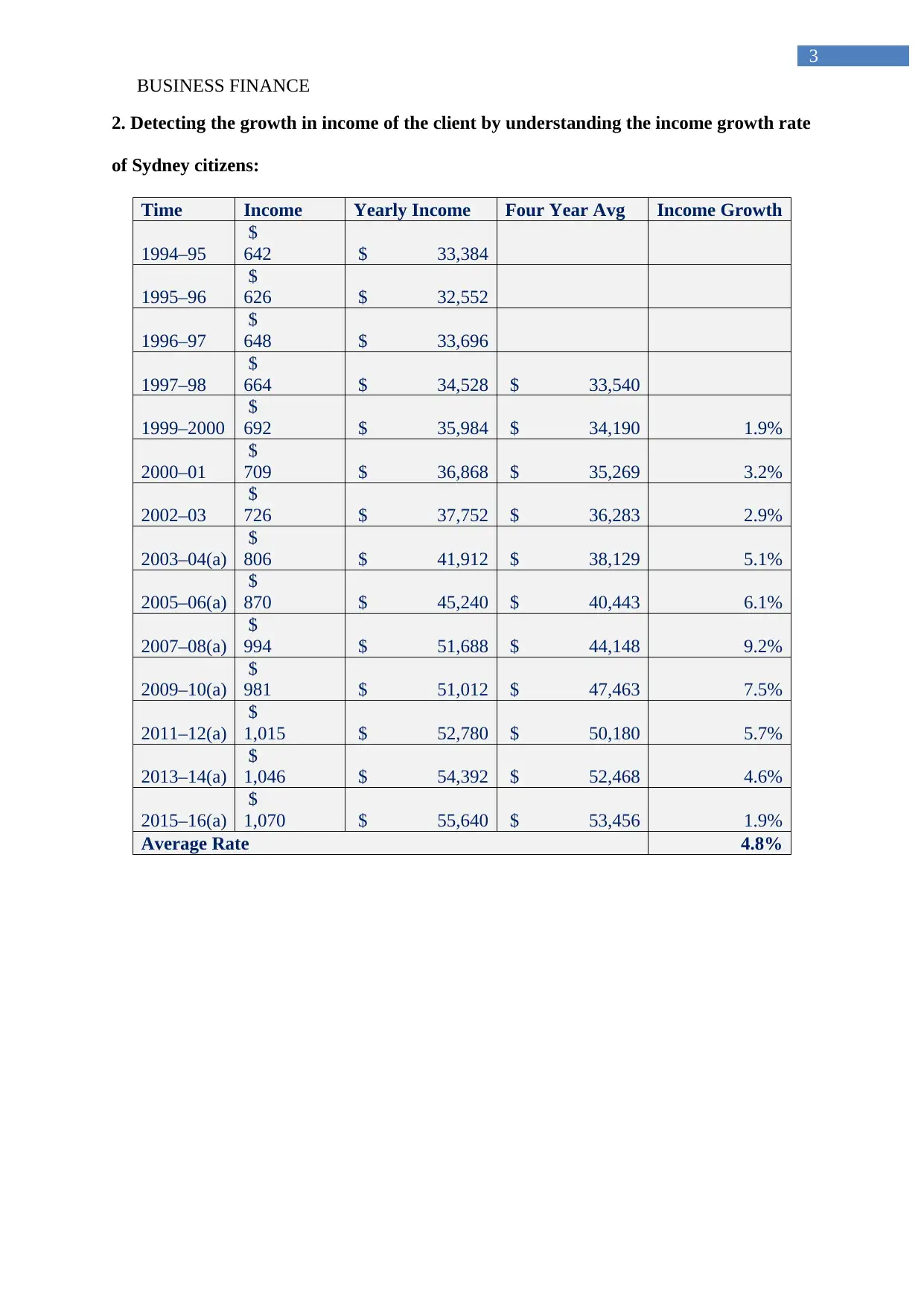

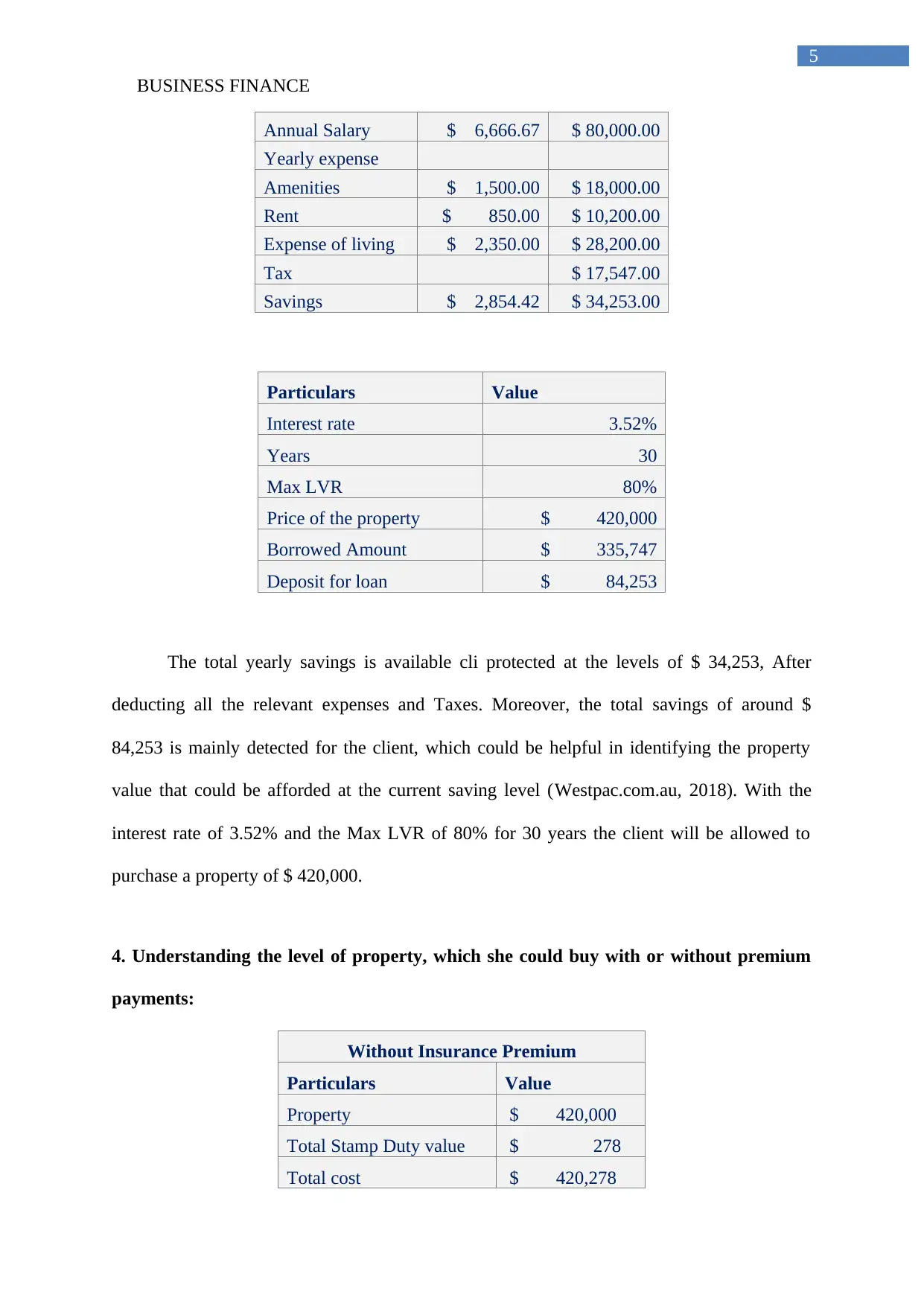

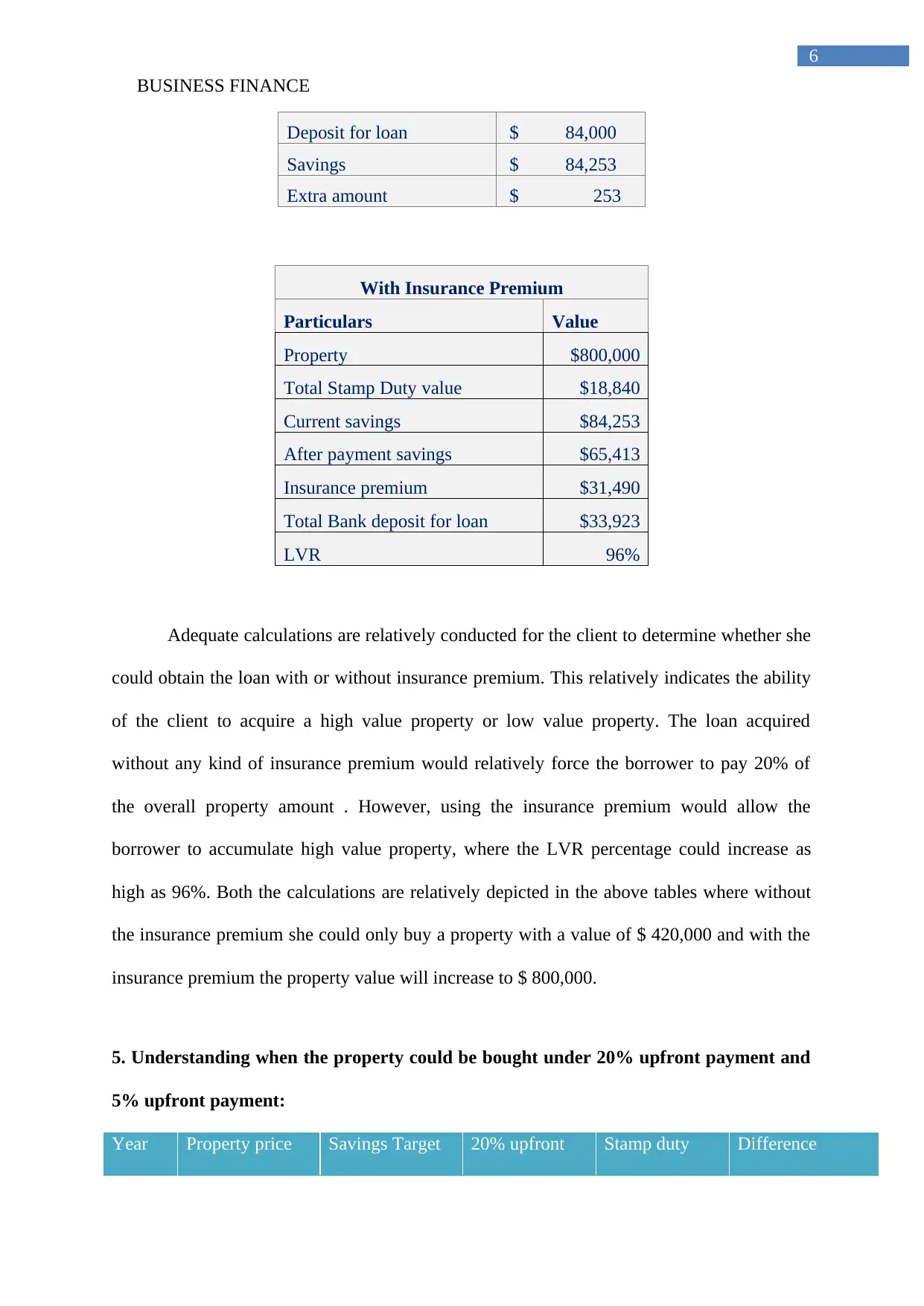

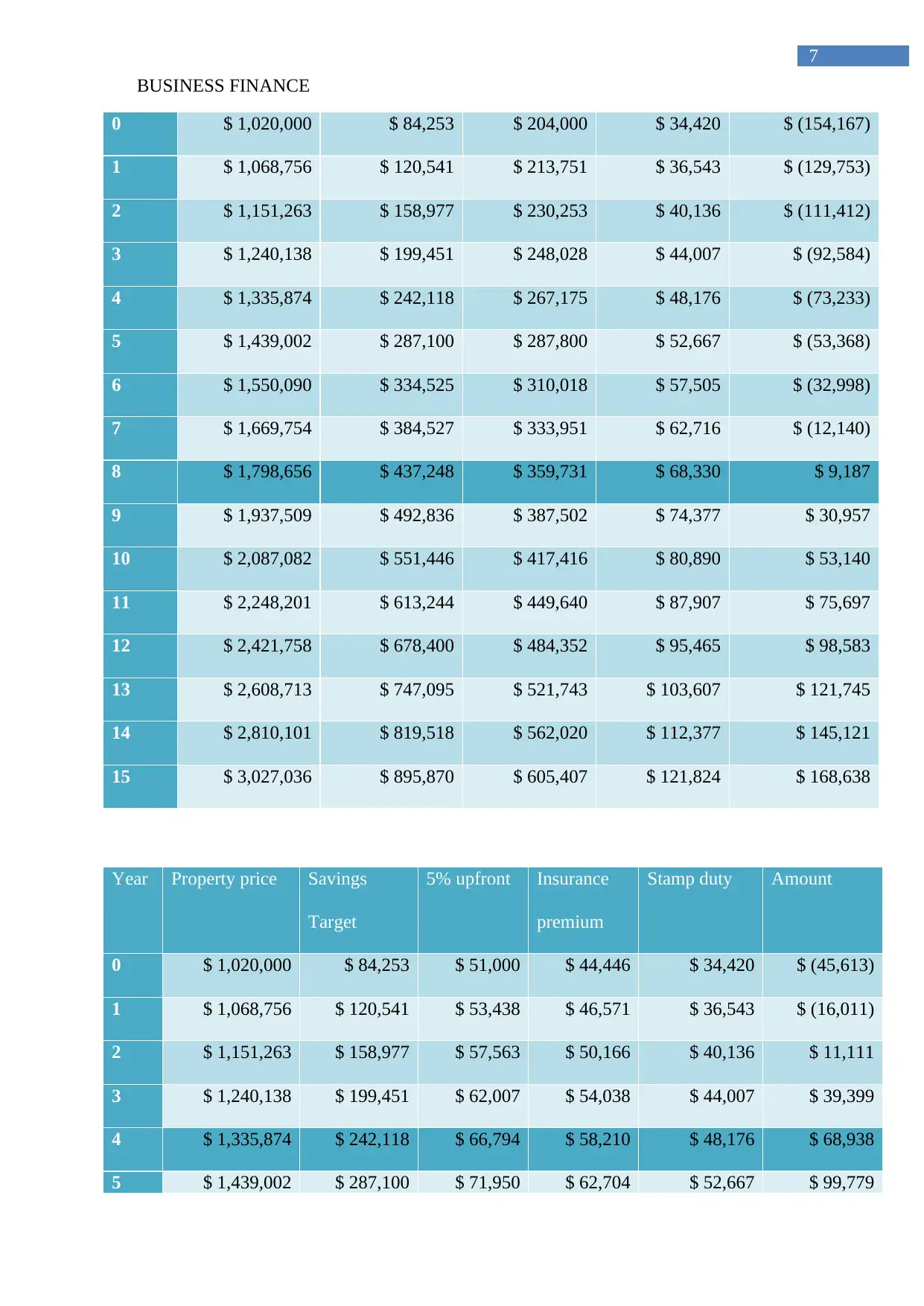

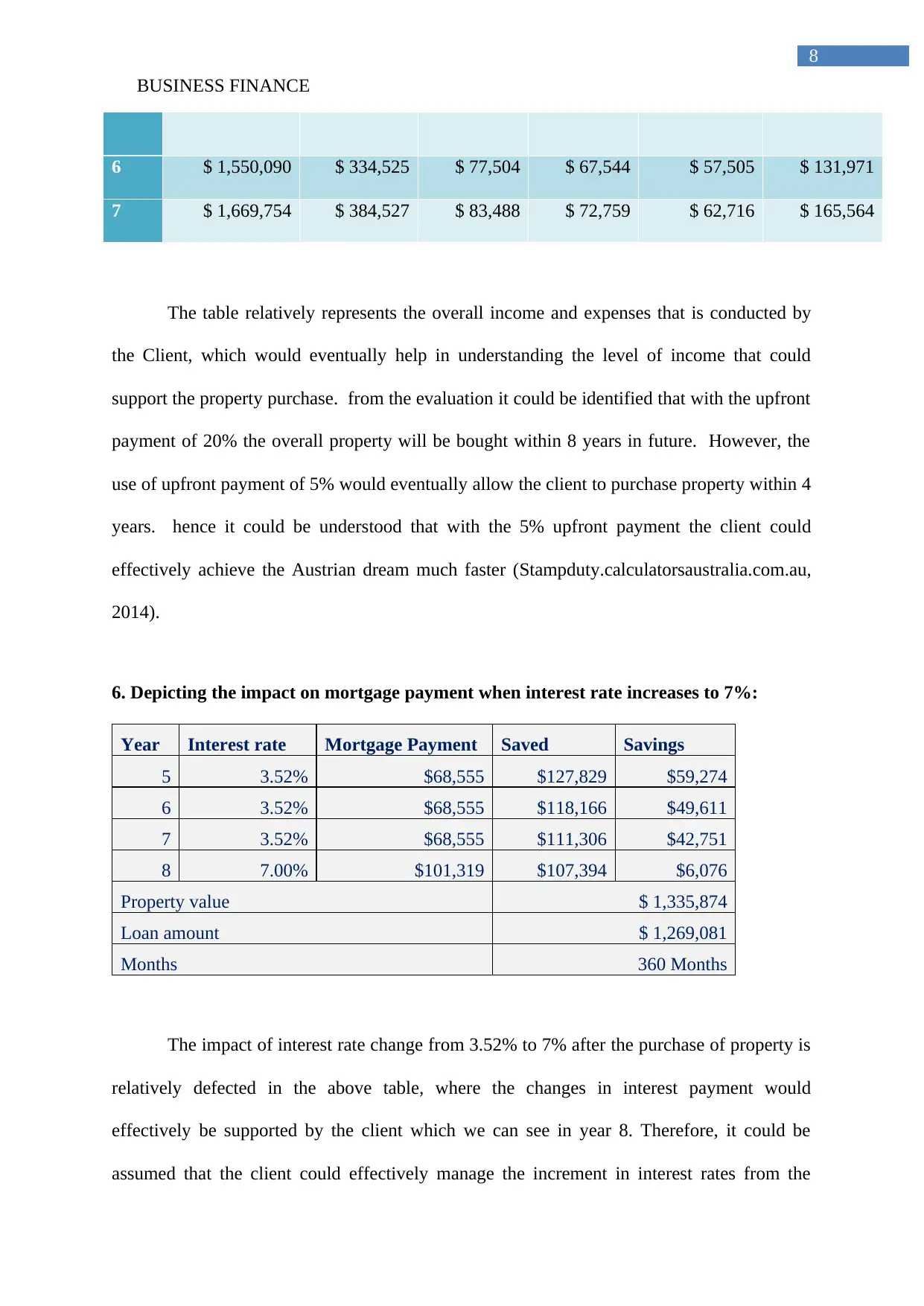

This business finance report provides a detailed analysis of housing prices in Sydney, predicting future trends based on historical data from the ABS website. It assesses a client's income growth over a 10-year period, estimating an average growth rate of 4.8%. The report then determines the maximum loan amount the client can avail, considering net income, taxes, and living expenses, and evaluates the property value she can afford with and without insurance premiums. Furthermore, it calculates the time required to purchase a property with 20% and 5% upfront payments and examines the impact of a potential interest rate increase to 7% on mortgage payments. The report concludes by outlining the risks involved in the financial plan, particularly concerning income stability and potential interest rate hikes, while providing relevant references from sources like Westpac and Domain. Access this and other solved assignments on Desklib.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.