University Finance Assignment: Interest Rate Parity and Swaps Analysis

VerifiedAdded on 2022/08/08

|12

|2649

|21

Homework Assignment

AI Summary

This assignment delves into two key areas of finance: interest rate parity and interest rate swaps. The first question examines interest rate parity, explaining its role in forex markets, calculating forward rates, and identifying arbitrage opportunities. It explores the relationship between spot rates, forward rates, and interest rate differentials, illustrating how deviations from parity can lead to arbitrage profits. The second question focuses on interest rate swaps, analyzing their mechanics, benefits, and risk. It explains how swaps can be used to manage interest rate risk, calculate cost savings, and determine settlement payments. The assignment also discusses the risks associated with swaps, including price and default risk, and how these risks can be mitigated.

Running head: QUESTION AND ANSWERS

Question and Answer

Name of the Student:

Name of the University:

Author Note:

Question and Answer

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1QUESTION AND ANSWERS

Answer to Question 1:

Part 1:

The interest rate parity means the forward rate should be equal to the interest rate

differential between the two countries multiplied by the spot rate. Thus the interest rate parity

highlights that the difference between the forward rate and the spot rate should be equal to the

difference between the interest rate between the two countries. This has an immense role to

play in the forex markets as if the interest rate parity does not hold good then investors can

earn arbitrage profits by taking relevant position in the currency.

Thus as per the question, the spot rate and the forward rates have been provided with

the bid ask rate. The bid rate is the rate at which the investor can sell to the bank and the ask

rate is the rate at which the investor can purchase from the bank. Thus for simplicity of

calculating interest rate parity mid rates are taken for the same.

Mid Spot Rate = 1.2575

Mid Forward Rate = 1.2375

Forward discount Premium = ((1.2375-1.2575)/1.2575)*100 = 1.59%

Interest rate US 3% UK 5%,

Hence interest rate differential = (5-3) % = 2%

Hence arbitrage is possible since the interest rate differential is not equal to the

currency differential. Thus the formula for IRP is given by,

Forward Rate/ spot Rate = (1+US)^N/(1+UK)^N

Forward Rate = 1.2575*((1+0.03)^3/12/(1+0.05)^3/12)

Answer to Question 1:

Part 1:

The interest rate parity means the forward rate should be equal to the interest rate

differential between the two countries multiplied by the spot rate. Thus the interest rate parity

highlights that the difference between the forward rate and the spot rate should be equal to the

difference between the interest rate between the two countries. This has an immense role to

play in the forex markets as if the interest rate parity does not hold good then investors can

earn arbitrage profits by taking relevant position in the currency.

Thus as per the question, the spot rate and the forward rates have been provided with

the bid ask rate. The bid rate is the rate at which the investor can sell to the bank and the ask

rate is the rate at which the investor can purchase from the bank. Thus for simplicity of

calculating interest rate parity mid rates are taken for the same.

Mid Spot Rate = 1.2575

Mid Forward Rate = 1.2375

Forward discount Premium = ((1.2375-1.2575)/1.2575)*100 = 1.59%

Interest rate US 3% UK 5%,

Hence interest rate differential = (5-3) % = 2%

Hence arbitrage is possible since the interest rate differential is not equal to the

currency differential. Thus the formula for IRP is given by,

Forward Rate/ spot Rate = (1+US)^N/(1+UK)^N

Forward Rate = 1.2575*((1+0.03)^3/12/(1+0.05)^3/12)

2QUESTION AND ANSWERS

Forward Rate = 1.251

The Forward parity rate is the rate which should be the exchange rate after the time

period which is equal to the interest rate differential of the two countries multiplied by the

spot rate. If the rate is not equal to the forward rate, then the investor has an opportunity to

generate arbitrage profits. The mid rates from the spot and the forward rates for both the

currency is calculated, which is used in the parity equation. Thus the interest rate for the both

the country is taken and used in the parity equation, which provides the forward rate of $

1.251 per euro. Thus the forward rates of the currency is not equal to the parity forward rate

which is calculated.

Part 2:

The interest rate arbitrage can be defined as borrowing in low yielding currency and

investing in high yielding currency. The arbitrage profit is earned when the interest rate parity

does not hold good and the investor makes more money than it was supposed to from the

investment. Thus the interest rate arbitrage is highlighted in the following steps.

Step 1: The amount which needs to be invest is pound 100000.

Step 2: convert the pound into spot dollars at the exchange rate of 1.255 which is the bid rate.

The dollar which is received is 125500.

Step 3: Invest the dollar which has been converted for 3 months at the US interest rate which

is 3%. Thus the amount after 3 months is 126430.84 dollars.

Step 4: This amount which is received in dollars is converted in pound at ask forward rate of

1.245. Thus the pound which is received is 101550.

Step 5: If the pound 100000 would had been invested at 5% UK rate the pound amount would

had been 101227.22.

Forward Rate = 1.251

The Forward parity rate is the rate which should be the exchange rate after the time

period which is equal to the interest rate differential of the two countries multiplied by the

spot rate. If the rate is not equal to the forward rate, then the investor has an opportunity to

generate arbitrage profits. The mid rates from the spot and the forward rates for both the

currency is calculated, which is used in the parity equation. Thus the interest rate for the both

the country is taken and used in the parity equation, which provides the forward rate of $

1.251 per euro. Thus the forward rates of the currency is not equal to the parity forward rate

which is calculated.

Part 2:

The interest rate arbitrage can be defined as borrowing in low yielding currency and

investing in high yielding currency. The arbitrage profit is earned when the interest rate parity

does not hold good and the investor makes more money than it was supposed to from the

investment. Thus the interest rate arbitrage is highlighted in the following steps.

Step 1: The amount which needs to be invest is pound 100000.

Step 2: convert the pound into spot dollars at the exchange rate of 1.255 which is the bid rate.

The dollar which is received is 125500.

Step 3: Invest the dollar which has been converted for 3 months at the US interest rate which

is 3%. Thus the amount after 3 months is 126430.84 dollars.

Step 4: This amount which is received in dollars is converted in pound at ask forward rate of

1.245. Thus the pound which is received is 101550.

Step 5: If the pound 100000 would had been invested at 5% UK rate the pound amount would

had been 101227.22.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3QUESTION AND ANSWERS

Step 6: Thus arbitrage profit from the transaction is pound 323.65.

Thus since the transaction was covered the effective exchange rate which was locked

by the company from the above transaction is 126430.84/101227.22 = 1.249.

Thus as per the money market mechanism the parity forward rate for the currency pair

is $1.2489. Thus this is not equal to the parity forward rate calculated from the parity

equation. The forward rate as per the money market mechanism implies that if the position in

the foreign currency is left open and not covered the rate which should be present should be

equal to the forward rate of the currency. Thus, it is the effective exchange rate at which the

company can convert its currency, ignoring taxes and transaction cost.

Part 3:

The parity equation takes into account the spot rates, the interest rates for both the

countries when the forward rate is calculated. In the money market mechanism, the forward

rate is calculated by dividing a set amount invested in one currency by the same amount

invested in other currency (Du, Tepper and Verdelhan 2018). The difference which is of

$0.02 is on account of the fact of the effect of the spot rate. In uncovered IRP the spot rate is

the rate for conversion, and gives a specific set of amount which is invested in the market rate

for a specific time period. Thus the amount which earned is not covered and is exchanged on

the day of the investment horizon ends (Han 2018). Thus the difference between the interest

rates and the exchange rates should be equal to avoid arbitrage. However, since the difference

is not equal it gives rise to arbitrage opportunity which is exploited by the investors (Lothian

2016).

Step 6: Thus arbitrage profit from the transaction is pound 323.65.

Thus since the transaction was covered the effective exchange rate which was locked

by the company from the above transaction is 126430.84/101227.22 = 1.249.

Thus as per the money market mechanism the parity forward rate for the currency pair

is $1.2489. Thus this is not equal to the parity forward rate calculated from the parity

equation. The forward rate as per the money market mechanism implies that if the position in

the foreign currency is left open and not covered the rate which should be present should be

equal to the forward rate of the currency. Thus, it is the effective exchange rate at which the

company can convert its currency, ignoring taxes and transaction cost.

Part 3:

The parity equation takes into account the spot rates, the interest rates for both the

countries when the forward rate is calculated. In the money market mechanism, the forward

rate is calculated by dividing a set amount invested in one currency by the same amount

invested in other currency (Du, Tepper and Verdelhan 2018). The difference which is of

$0.02 is on account of the fact of the effect of the spot rate. In uncovered IRP the spot rate is

the rate for conversion, and gives a specific set of amount which is invested in the market rate

for a specific time period. Thus the amount which earned is not covered and is exchanged on

the day of the investment horizon ends (Han 2018). Thus the difference between the interest

rates and the exchange rates should be equal to avoid arbitrage. However, since the difference

is not equal it gives rise to arbitrage opportunity which is exploited by the investors (Lothian

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4QUESTION AND ANSWERS

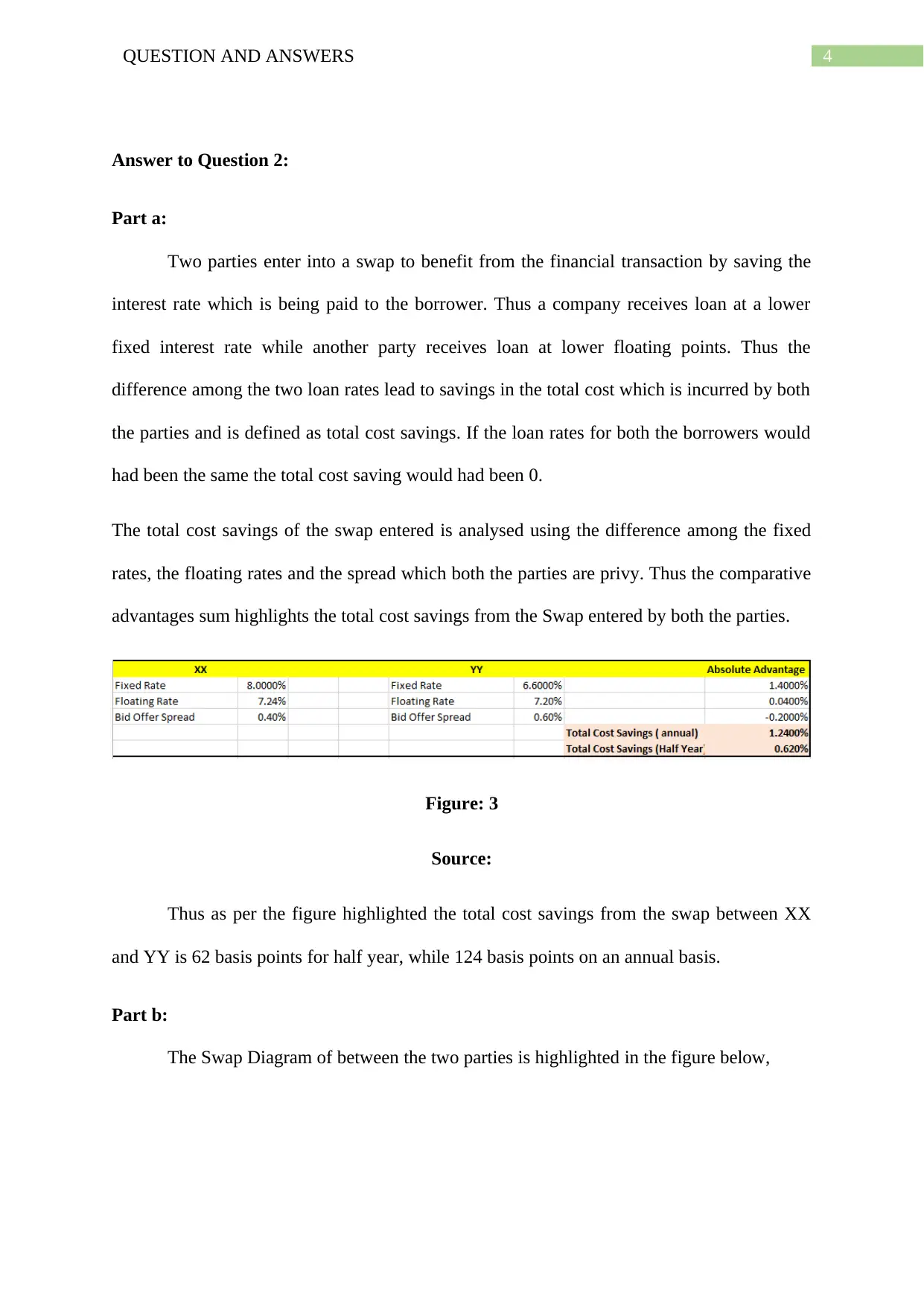

Answer to Question 2:

Part a:

Two parties enter into a swap to benefit from the financial transaction by saving the

interest rate which is being paid to the borrower. Thus a company receives loan at a lower

fixed interest rate while another party receives loan at lower floating points. Thus the

difference among the two loan rates lead to savings in the total cost which is incurred by both

the parties and is defined as total cost savings. If the loan rates for both the borrowers would

had been the same the total cost saving would had been 0.

The total cost savings of the swap entered is analysed using the difference among the fixed

rates, the floating rates and the spread which both the parties are privy. Thus the comparative

advantages sum highlights the total cost savings from the Swap entered by both the parties.

Figure: 3

Source:

Thus as per the figure highlighted the total cost savings from the swap between XX

and YY is 62 basis points for half year, while 124 basis points on an annual basis.

Part b:

The Swap Diagram of between the two parties is highlighted in the figure below,

Answer to Question 2:

Part a:

Two parties enter into a swap to benefit from the financial transaction by saving the

interest rate which is being paid to the borrower. Thus a company receives loan at a lower

fixed interest rate while another party receives loan at lower floating points. Thus the

difference among the two loan rates lead to savings in the total cost which is incurred by both

the parties and is defined as total cost savings. If the loan rates for both the borrowers would

had been the same the total cost saving would had been 0.

The total cost savings of the swap entered is analysed using the difference among the fixed

rates, the floating rates and the spread which both the parties are privy. Thus the comparative

advantages sum highlights the total cost savings from the Swap entered by both the parties.

Figure: 3

Source:

Thus as per the figure highlighted the total cost savings from the swap between XX

and YY is 62 basis points for half year, while 124 basis points on an annual basis.

Part b:

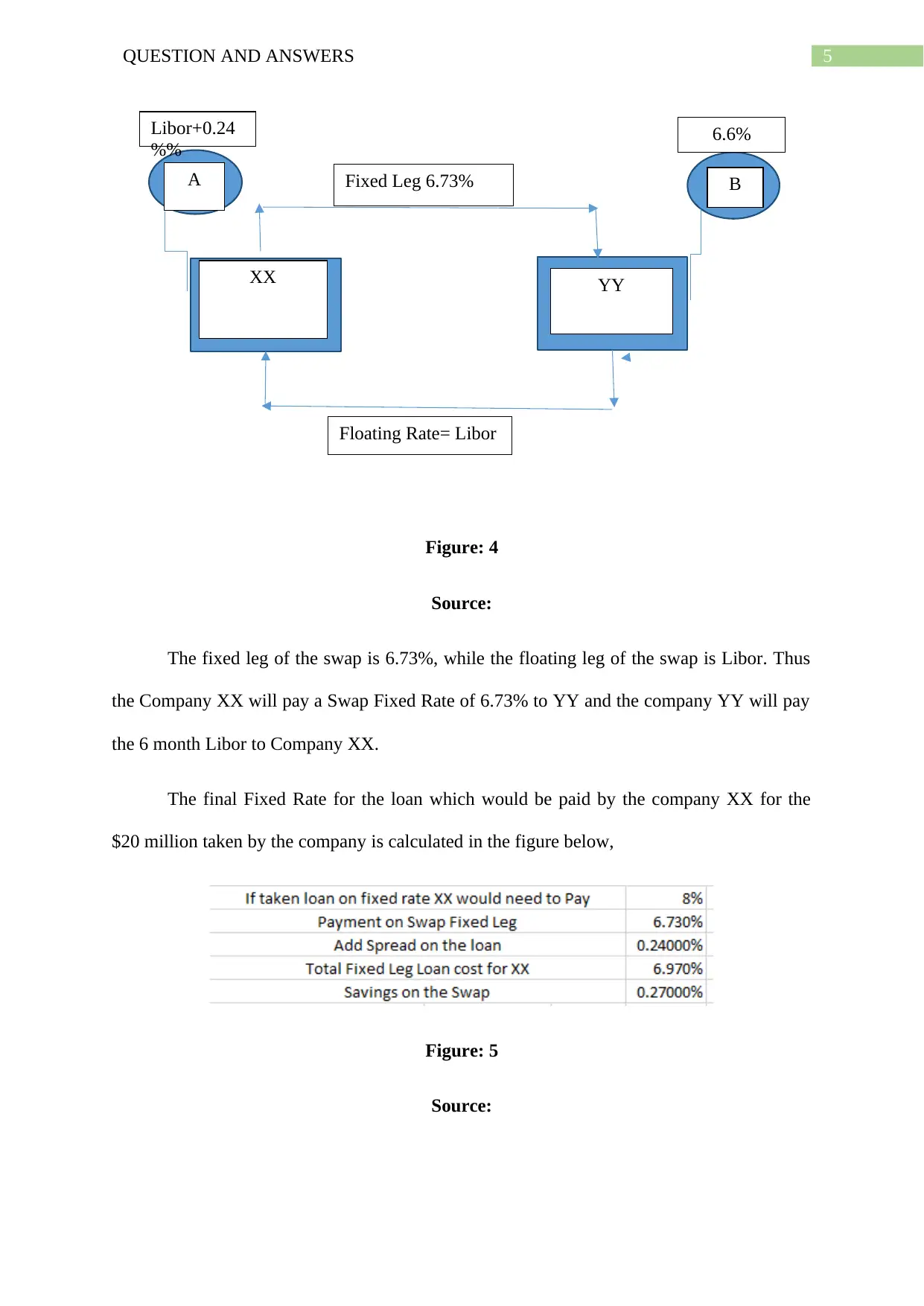

The Swap Diagram of between the two parties is highlighted in the figure below,

5QUESTION AND ANSWERS

XX YY

A BFixed Leg 6.73%

Floating Rate= Libor

Libor+0.24

%% 6.6%

Figure: 4

Source:

The fixed leg of the swap is 6.73%, while the floating leg of the swap is Libor. Thus

the Company XX will pay a Swap Fixed Rate of 6.73% to YY and the company YY will pay

the 6 month Libor to Company XX.

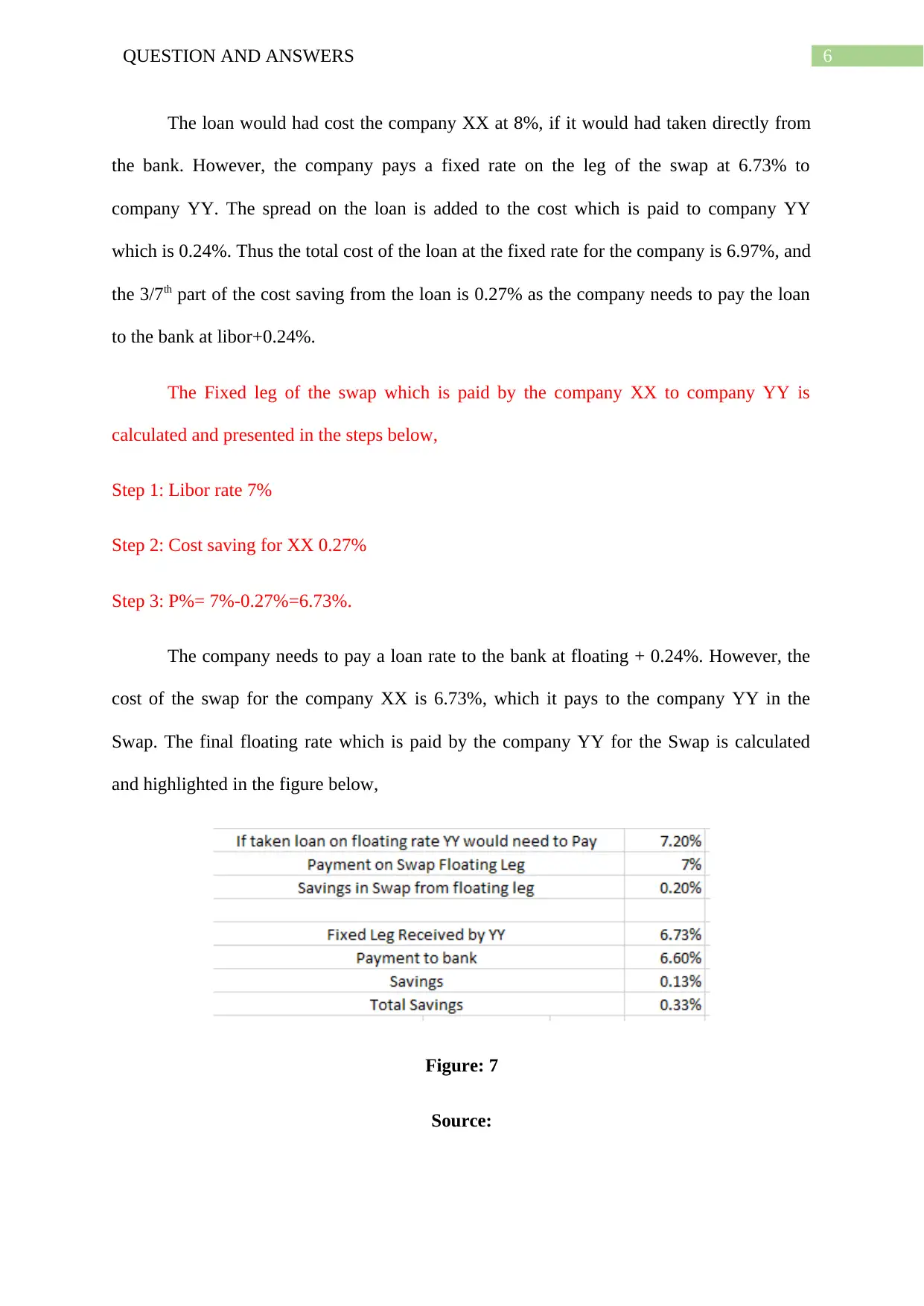

The final Fixed Rate for the loan which would be paid by the company XX for the

$20 million taken by the company is calculated in the figure below,

Figure: 5

Source:

XX YY

A BFixed Leg 6.73%

Floating Rate= Libor

Libor+0.24

%% 6.6%

Figure: 4

Source:

The fixed leg of the swap is 6.73%, while the floating leg of the swap is Libor. Thus

the Company XX will pay a Swap Fixed Rate of 6.73% to YY and the company YY will pay

the 6 month Libor to Company XX.

The final Fixed Rate for the loan which would be paid by the company XX for the

$20 million taken by the company is calculated in the figure below,

Figure: 5

Source:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6QUESTION AND ANSWERS

The loan would had cost the company XX at 8%, if it would had taken directly from

the bank. However, the company pays a fixed rate on the leg of the swap at 6.73% to

company YY. The spread on the loan is added to the cost which is paid to company YY

which is 0.24%. Thus the total cost of the loan at the fixed rate for the company is 6.97%, and

the 3/7th part of the cost saving from the loan is 0.27% as the company needs to pay the loan

to the bank at libor+0.24%.

The Fixed leg of the swap which is paid by the company XX to company YY is

calculated and presented in the steps below,

Step 1: Libor rate 7%

Step 2: Cost saving for XX 0.27%

Step 3: P%= 7%-0.27%=6.73%.

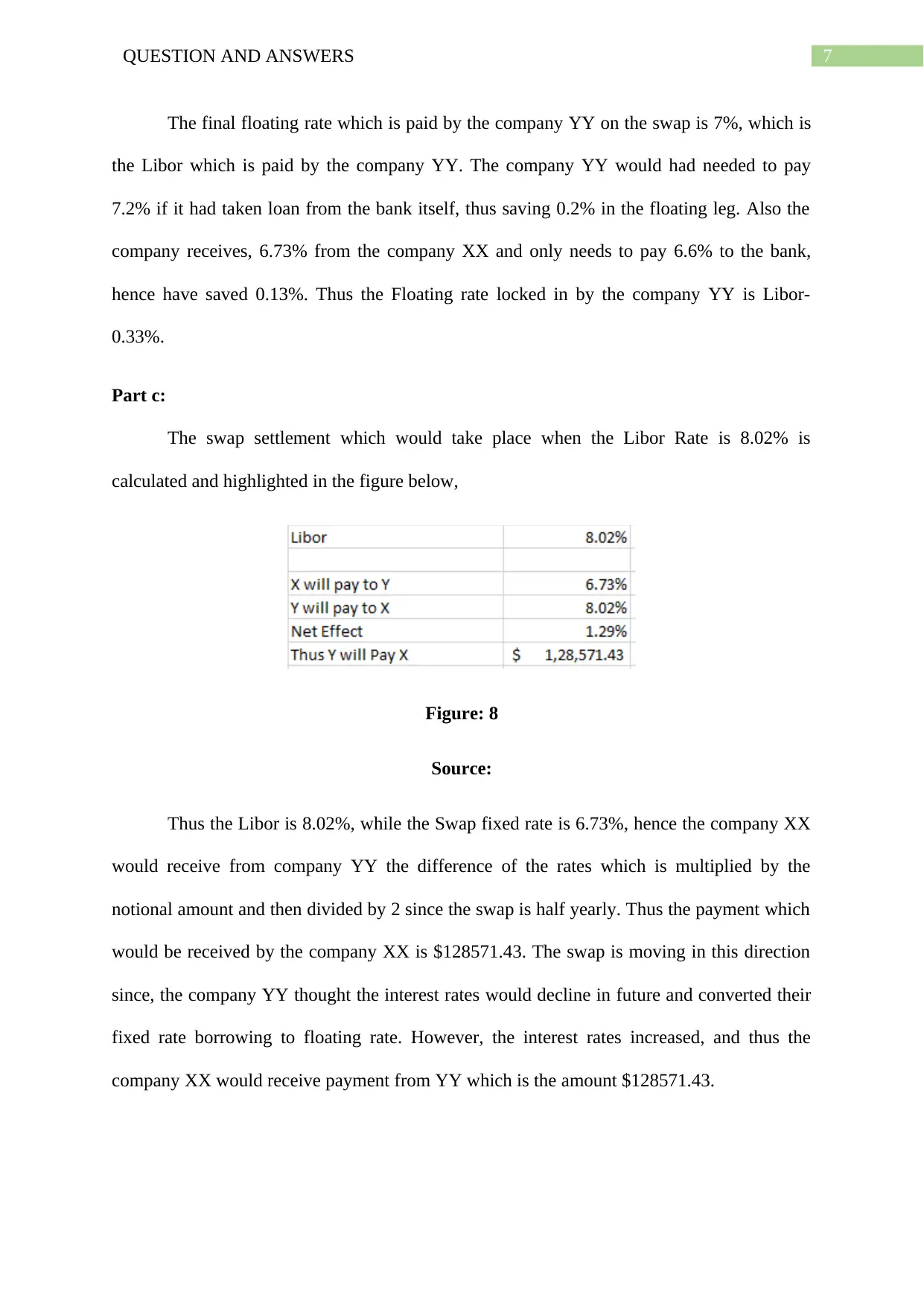

The company needs to pay a loan rate to the bank at floating + 0.24%. However, the

cost of the swap for the company XX is 6.73%, which it pays to the company YY in the

Swap. The final floating rate which is paid by the company YY for the Swap is calculated

and highlighted in the figure below,

Figure: 7

Source:

The loan would had cost the company XX at 8%, if it would had taken directly from

the bank. However, the company pays a fixed rate on the leg of the swap at 6.73% to

company YY. The spread on the loan is added to the cost which is paid to company YY

which is 0.24%. Thus the total cost of the loan at the fixed rate for the company is 6.97%, and

the 3/7th part of the cost saving from the loan is 0.27% as the company needs to pay the loan

to the bank at libor+0.24%.

The Fixed leg of the swap which is paid by the company XX to company YY is

calculated and presented in the steps below,

Step 1: Libor rate 7%

Step 2: Cost saving for XX 0.27%

Step 3: P%= 7%-0.27%=6.73%.

The company needs to pay a loan rate to the bank at floating + 0.24%. However, the

cost of the swap for the company XX is 6.73%, which it pays to the company YY in the

Swap. The final floating rate which is paid by the company YY for the Swap is calculated

and highlighted in the figure below,

Figure: 7

Source:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7QUESTION AND ANSWERS

The final floating rate which is paid by the company YY on the swap is 7%, which is

the Libor which is paid by the company YY. The company YY would had needed to pay

7.2% if it had taken loan from the bank itself, thus saving 0.2% in the floating leg. Also the

company receives, 6.73% from the company XX and only needs to pay 6.6% to the bank,

hence have saved 0.13%. Thus the Floating rate locked in by the company YY is Libor-

0.33%.

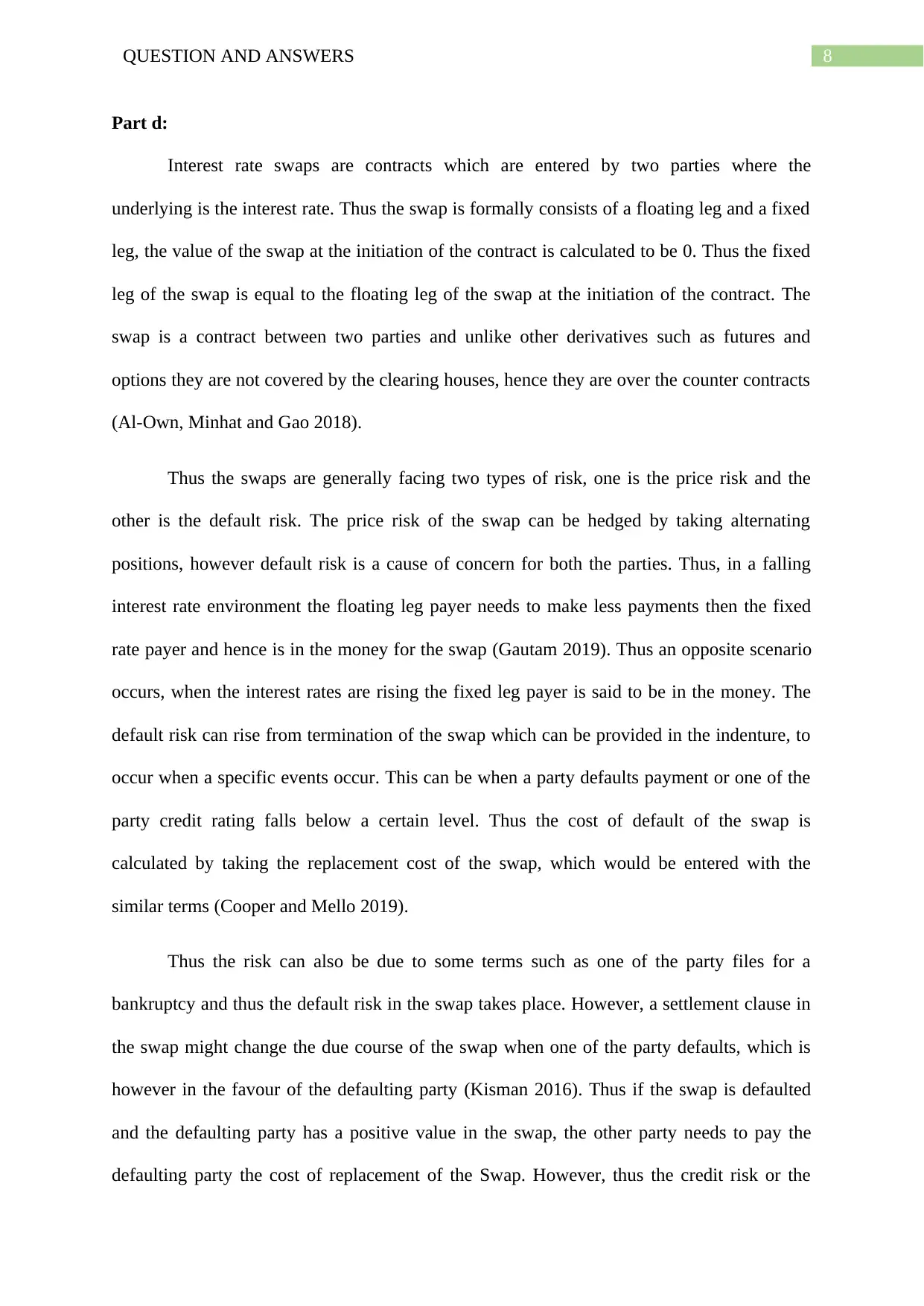

Part c:

The swap settlement which would take place when the Libor Rate is 8.02% is

calculated and highlighted in the figure below,

Figure: 8

Source:

Thus the Libor is 8.02%, while the Swap fixed rate is 6.73%, hence the company XX

would receive from company YY the difference of the rates which is multiplied by the

notional amount and then divided by 2 since the swap is half yearly. Thus the payment which

would be received by the company XX is $128571.43. The swap is moving in this direction

since, the company YY thought the interest rates would decline in future and converted their

fixed rate borrowing to floating rate. However, the interest rates increased, and thus the

company XX would receive payment from YY which is the amount $128571.43.

The final floating rate which is paid by the company YY on the swap is 7%, which is

the Libor which is paid by the company YY. The company YY would had needed to pay

7.2% if it had taken loan from the bank itself, thus saving 0.2% in the floating leg. Also the

company receives, 6.73% from the company XX and only needs to pay 6.6% to the bank,

hence have saved 0.13%. Thus the Floating rate locked in by the company YY is Libor-

0.33%.

Part c:

The swap settlement which would take place when the Libor Rate is 8.02% is

calculated and highlighted in the figure below,

Figure: 8

Source:

Thus the Libor is 8.02%, while the Swap fixed rate is 6.73%, hence the company XX

would receive from company YY the difference of the rates which is multiplied by the

notional amount and then divided by 2 since the swap is half yearly. Thus the payment which

would be received by the company XX is $128571.43. The swap is moving in this direction

since, the company YY thought the interest rates would decline in future and converted their

fixed rate borrowing to floating rate. However, the interest rates increased, and thus the

company XX would receive payment from YY which is the amount $128571.43.

8QUESTION AND ANSWERS

Part d:

Interest rate swaps are contracts which are entered by two parties where the

underlying is the interest rate. Thus the swap is formally consists of a floating leg and a fixed

leg, the value of the swap at the initiation of the contract is calculated to be 0. Thus the fixed

leg of the swap is equal to the floating leg of the swap at the initiation of the contract. The

swap is a contract between two parties and unlike other derivatives such as futures and

options they are not covered by the clearing houses, hence they are over the counter contracts

(Al-Own, Minhat and Gao 2018).

Thus the swaps are generally facing two types of risk, one is the price risk and the

other is the default risk. The price risk of the swap can be hedged by taking alternating

positions, however default risk is a cause of concern for both the parties. Thus, in a falling

interest rate environment the floating leg payer needs to make less payments then the fixed

rate payer and hence is in the money for the swap (Gautam 2019). Thus an opposite scenario

occurs, when the interest rates are rising the fixed leg payer is said to be in the money. The

default risk can rise from termination of the swap which can be provided in the indenture, to

occur when a specific events occur. This can be when a party defaults payment or one of the

party credit rating falls below a certain level. Thus the cost of default of the swap is

calculated by taking the replacement cost of the swap, which would be entered with the

similar terms (Cooper and Mello 2019).

Thus the risk can also be due to some terms such as one of the party files for a

bankruptcy and thus the default risk in the swap takes place. However, a settlement clause in

the swap might change the due course of the swap when one of the party defaults, which is

however in the favour of the defaulting party (Kisman 2016). Thus if the swap is defaulted

and the defaulting party has a positive value in the swap, the other party needs to pay the

defaulting party the cost of replacement of the Swap. However, thus the credit risk or the

Part d:

Interest rate swaps are contracts which are entered by two parties where the

underlying is the interest rate. Thus the swap is formally consists of a floating leg and a fixed

leg, the value of the swap at the initiation of the contract is calculated to be 0. Thus the fixed

leg of the swap is equal to the floating leg of the swap at the initiation of the contract. The

swap is a contract between two parties and unlike other derivatives such as futures and

options they are not covered by the clearing houses, hence they are over the counter contracts

(Al-Own, Minhat and Gao 2018).

Thus the swaps are generally facing two types of risk, one is the price risk and the

other is the default risk. The price risk of the swap can be hedged by taking alternating

positions, however default risk is a cause of concern for both the parties. Thus, in a falling

interest rate environment the floating leg payer needs to make less payments then the fixed

rate payer and hence is in the money for the swap (Gautam 2019). Thus an opposite scenario

occurs, when the interest rates are rising the fixed leg payer is said to be in the money. The

default risk can rise from termination of the swap which can be provided in the indenture, to

occur when a specific events occur. This can be when a party defaults payment or one of the

party credit rating falls below a certain level. Thus the cost of default of the swap is

calculated by taking the replacement cost of the swap, which would be entered with the

similar terms (Cooper and Mello 2019).

Thus the risk can also be due to some terms such as one of the party files for a

bankruptcy and thus the default risk in the swap takes place. However, a settlement clause in

the swap might change the due course of the swap when one of the party defaults, which is

however in the favour of the defaulting party (Kisman 2016). Thus if the swap is defaulted

and the defaulting party has a positive value in the swap, the other party needs to pay the

defaulting party the cost of replacement of the Swap. However, thus the credit risk or the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9QUESTION AND ANSWERS

default risk is extremely high in the swap as the defaulting party could not pay the dues when

the swap defaults, but can collect the payment when they have a positive value (Thalassinos,

Stamatopoulos and Thalassinos 2016).

default risk is extremely high in the swap as the defaulting party could not pay the dues when

the swap defaults, but can collect the payment when they have a positive value (Thalassinos,

Stamatopoulos and Thalassinos 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10QUESTION AND ANSWERS

References:

Ali, I., Gohar, A. and Meharzi, O., 2017. Why do firms change their dividend

policy?. International Journal of Economics and Financial Issues, 7(3), pp.411-422.

Al-Own, B., Minhat, M. and Gao, S., 2018. Stock options and credit default swaps in risk

management. Journal of International Financial Markets, Institutions and Money, 53,

pp.200-214.

Baker, H.K., Kilincarslan, E. and Arsal, A.H., 2018. Dividend policy in Turkey: Survey

evidence from Borsa Istanbul firms. Global Finance Journal, 35, pp.43-57.

Cooper, I. and Mello, A.S., 2019. The default risk of swaps. Institute of Finance and

Accounting.

Du, W., Tepper, A. and Verdelhan, A., 2018. Deviations from covered interest rate

parity. The Journal of Finance, 73(3), pp.915-957.

Gautam, P., 2019. Agency Costs and Dividend Policy: A Review of Theories and Empirical

Evidence. Journal of the Gujarat Research Society, 21(16), pp.1229-1234.

Kisman, Z., 2016. Disappearing Dividend Phenomenon: A Review of Theories and

Evidence. Transylvanian Review, (3).

Lothian, J.R., 2016. Uncovered interest parity: The long and the short of it. Journal of

Empirical Finance, 36, pp.1-7.

Murtaza, M., Iqbal, M.M., Ullah, Z., Rasheed, H. and Basit, A., 2018. An Analytical Review

of Dividend Policy Theories. Journal of Advanced Research in Business and Management

Studies, 11(1), pp.62-76.

References:

Ali, I., Gohar, A. and Meharzi, O., 2017. Why do firms change their dividend

policy?. International Journal of Economics and Financial Issues, 7(3), pp.411-422.

Al-Own, B., Minhat, M. and Gao, S., 2018. Stock options and credit default swaps in risk

management. Journal of International Financial Markets, Institutions and Money, 53,

pp.200-214.

Baker, H.K., Kilincarslan, E. and Arsal, A.H., 2018. Dividend policy in Turkey: Survey

evidence from Borsa Istanbul firms. Global Finance Journal, 35, pp.43-57.

Cooper, I. and Mello, A.S., 2019. The default risk of swaps. Institute of Finance and

Accounting.

Du, W., Tepper, A. and Verdelhan, A., 2018. Deviations from covered interest rate

parity. The Journal of Finance, 73(3), pp.915-957.

Gautam, P., 2019. Agency Costs and Dividend Policy: A Review of Theories and Empirical

Evidence. Journal of the Gujarat Research Society, 21(16), pp.1229-1234.

Kisman, Z., 2016. Disappearing Dividend Phenomenon: A Review of Theories and

Evidence. Transylvanian Review, (3).

Lothian, J.R., 2016. Uncovered interest parity: The long and the short of it. Journal of

Empirical Finance, 36, pp.1-7.

Murtaza, M., Iqbal, M.M., Ullah, Z., Rasheed, H. and Basit, A., 2018. An Analytical Review

of Dividend Policy Theories. Journal of Advanced Research in Business and Management

Studies, 11(1), pp.62-76.

11QUESTION AND ANSWERS

Thalassinos, E.I., Stamatopoulos, T. and Thalassinos, P.E., 2016. The European sovereign

debt crisis and the role of credit swaps. In THE WORLD SCIENTIFIC HANDBOOK OF

FUTURES MARKETS (pp. 605-639).

Han, R., 2018. The Impact of Exchange Rate Volatility on Portfolio Investment.

Nirmali, H. and Rajapakse, R.P.C.R., 2016. The Uncovered Interest rate Parity-A Literature

Review.

Har, W.M., Tan, A.L., Lim, C.H. and Tan, C.T., 2017. Does Interest Rate Still Matter in

Determining Exchange Rate?. Capital Markets Review, 25(1), pp.19-25.

Thalassinos, E.I., Stamatopoulos, T. and Thalassinos, P.E., 2016. The European sovereign

debt crisis and the role of credit swaps. In THE WORLD SCIENTIFIC HANDBOOK OF

FUTURES MARKETS (pp. 605-639).

Han, R., 2018. The Impact of Exchange Rate Volatility on Portfolio Investment.

Nirmali, H. and Rajapakse, R.P.C.R., 2016. The Uncovered Interest rate Parity-A Literature

Review.

Har, W.M., Tan, A.L., Lim, C.H. and Tan, C.T., 2017. Does Interest Rate Still Matter in

Determining Exchange Rate?. Capital Markets Review, 25(1), pp.19-25.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.