Finance for International Business: Investment Appraisal Report

VerifiedAdded on 2022/12/14

|9

|2698

|486

Report

AI Summary

This report provides an investment appraisal for the Bonita Foods SL investment project on behalf of Wholesome Organic Foods plc. The report evaluates the project using various financial techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), and Accounting Rate of Return (ARR), and payback period. It advises on whether the firm should undertake the project, identifies the maximum price Wholesome foods Plc should pay to acquire Bonita Foods SL, and assesses the potential impact of foreign exchange. The report also evaluates financing alternatives and considers non-financial factors such as market demand, consumer purchasing power, and the state of the economy. The analysis concludes with recommendations based on the financial metrics and provides insights into the project's viability and potential risks.

Title Investment

Appraisal Report

Appraisal Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Tasks................................................................................................................................................3

Evaluate the Bonita Foods SL investment project on behalf of Wholesome Organic Foods plc.

.....................................................................................................................................................3

Advise the firm on whether it should undertake the project........................................................4

Identify the maximum price Wholesome foods Plc should pay to acquire the Bonita Foods SL.

.....................................................................................................................................................5

Advise the firm on the potential impact of foreign exchange on the project..............................6

Evaluate the alternatives for financing the purchase...................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

Tasks................................................................................................................................................3

Evaluate the Bonita Foods SL investment project on behalf of Wholesome Organic Foods plc.

.....................................................................................................................................................3

Advise the firm on whether it should undertake the project........................................................4

Identify the maximum price Wholesome foods Plc should pay to acquire the Bonita Foods SL.

.....................................................................................................................................................5

Advise the firm on the potential impact of foreign exchange on the project..............................6

Evaluate the alternatives for financing the purchase...................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Investment evaluation is a process through which a company evaluates the feasibility of

potential acquisitions or programmes depending on the results of various budgetary control and

funding techniques (Massa, Tucci, and Afuah, 2017). This is a method of fundamental research

for shareholders and it can assist in identifying long-term patterns and a business's potential

profitability. Since investment valuation is a type of fundamental research, it may inform a

broker how well a stock or a firm has lengthy prospects depending on the feasibility of new

endeavors and efforts. When an organisation is engaged in a variety of huge investment

programmes, there seems to be a higher chance of sales, expense, and cashflow problems. It was

something which a trader should think about before investing in such a company's stock.

Tasks

Evaluate the Bonita Foods SL investment project on behalf of Wholesome Organic Foods plc.

The four investment valuation techniques can be divided into two groups. Non-discounting

approaches include the ARR as well as payback date, while price reduction methods include the

Net present Value. The accounting benefit rate is calculated using the ARR equation, which

divides average profits by average expenditure. The system is easy to use, although it has

significant drawbacks. It disregards the timeframe value of capital, which would be a significant

disadvantage mostly in form of heavy ventures. For reference, a benchmark level also is

expected. The payback cycle is the time that it takes for a project's original cost to be recovered

from its operational cash flows.

Projects with a negative net present value are favoured because they raise cash compared to its

original cost in a shorter time, which could be seen as a risk indicator. The payback period

system, on the other hand, avoids the time value of capital. This also discounts working capital

only after repayment date, which can lead to a project planning that contributes less benefit. The

NPV equation determines a project's net worth by disregarding cash flows at such a rate that

represents the uncertainties associated with such cash flows. The NPV approach has a significant

benefit over non-discounting approaches in terms of discounting potential cash flows. Since the

cash balances are compounded over a 10-year period, this really is critical for evaluating the 2

choices (Merton, 2016).

Investment evaluation is a process through which a company evaluates the feasibility of

potential acquisitions or programmes depending on the results of various budgetary control and

funding techniques (Massa, Tucci, and Afuah, 2017). This is a method of fundamental research

for shareholders and it can assist in identifying long-term patterns and a business's potential

profitability. Since investment valuation is a type of fundamental research, it may inform a

broker how well a stock or a firm has lengthy prospects depending on the feasibility of new

endeavors and efforts. When an organisation is engaged in a variety of huge investment

programmes, there seems to be a higher chance of sales, expense, and cashflow problems. It was

something which a trader should think about before investing in such a company's stock.

Tasks

Evaluate the Bonita Foods SL investment project on behalf of Wholesome Organic Foods plc.

The four investment valuation techniques can be divided into two groups. Non-discounting

approaches include the ARR as well as payback date, while price reduction methods include the

Net present Value. The accounting benefit rate is calculated using the ARR equation, which

divides average profits by average expenditure. The system is easy to use, although it has

significant drawbacks. It disregards the timeframe value of capital, which would be a significant

disadvantage mostly in form of heavy ventures. For reference, a benchmark level also is

expected. The payback cycle is the time that it takes for a project's original cost to be recovered

from its operational cash flows.

Projects with a negative net present value are favoured because they raise cash compared to its

original cost in a shorter time, which could be seen as a risk indicator. The payback period

system, on the other hand, avoids the time value of capital. This also discounts working capital

only after repayment date, which can lead to a project planning that contributes less benefit. The

NPV equation determines a project's net worth by disregarding cash flows at such a rate that

represents the uncertainties associated with such cash flows. The NPV approach has a significant

benefit over non-discounting approaches in terms of discounting potential cash flows. Since the

cash balances are compounded over a 10-year period, this really is critical for evaluating the 2

choices (Merton, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

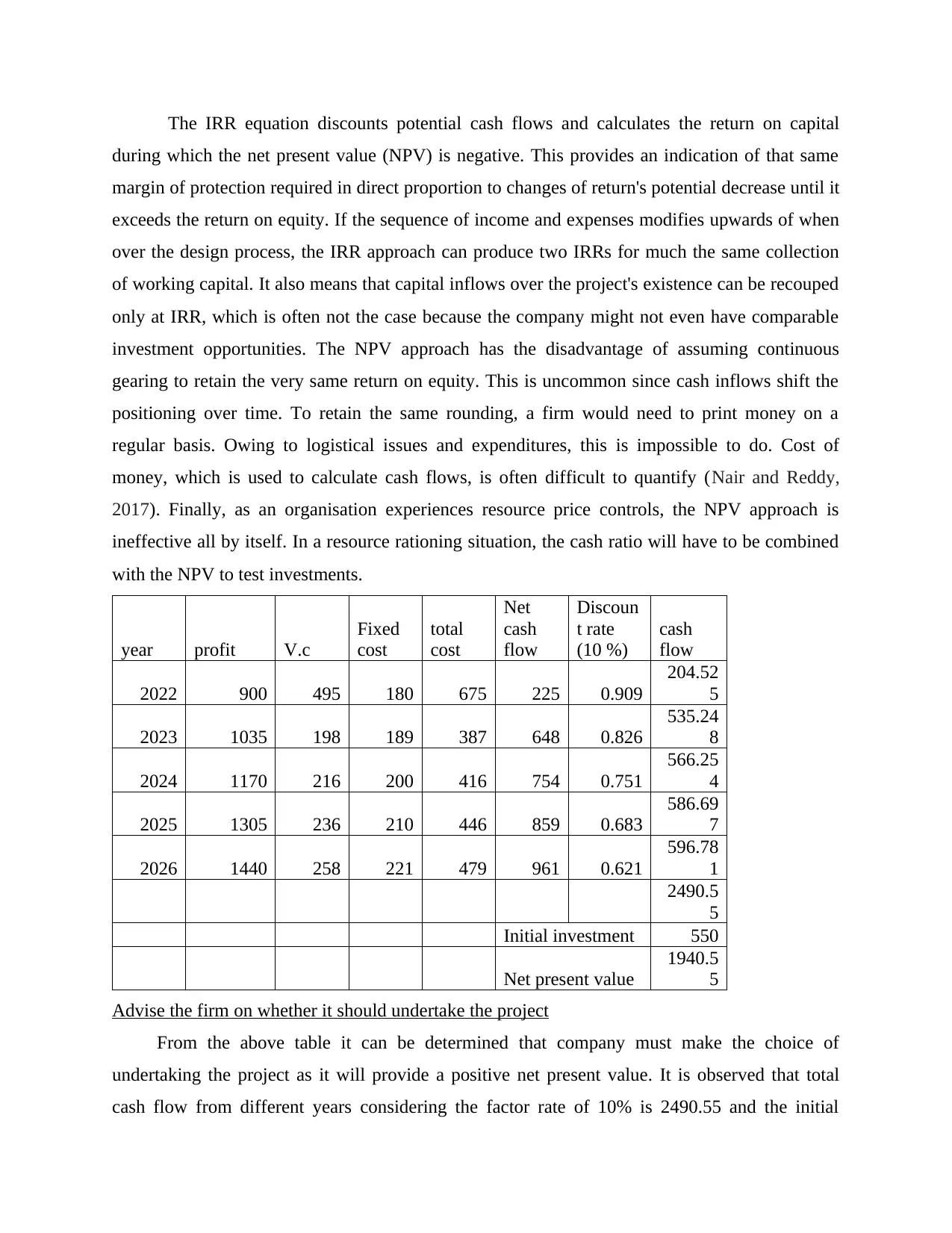

The IRR equation discounts potential cash flows and calculates the return on capital

during which the net present value (NPV) is negative. This provides an indication of that same

margin of protection required in direct proportion to changes of return's potential decrease until it

exceeds the return on equity. If the sequence of income and expenses modifies upwards of when

over the design process, the IRR approach can produce two IRRs for much the same collection

of working capital. It also means that capital inflows over the project's existence can be recouped

only at IRR, which is often not the case because the company might not even have comparable

investment opportunities. The NPV approach has the disadvantage of assuming continuous

gearing to retain the very same return on equity. This is uncommon since cash inflows shift the

positioning over time. To retain the same rounding, a firm would need to print money on a

regular basis. Owing to logistical issues and expenditures, this is impossible to do. Cost of

money, which is used to calculate cash flows, is often difficult to quantify (Nair and Reddy,

2017). Finally, as an organisation experiences resource price controls, the NPV approach is

ineffective all by itself. In a resource rationing situation, the cash ratio will have to be combined

with the NPV to test investments.

year profit V.c

Fixed

cost

total

cost

Net

cash

flow

Discoun

t rate

(10 %)

cash

flow

2022 900 495 180 675 225 0.909

204.52

5

2023 1035 198 189 387 648 0.826

535.24

8

2024 1170 216 200 416 754 0.751

566.25

4

2025 1305 236 210 446 859 0.683

586.69

7

2026 1440 258 221 479 961 0.621

596.78

1

2490.5

5

Initial investment 550

Net present value

1940.5

5

Advise the firm on whether it should undertake the project

From the above table it can be determined that company must make the choice of

undertaking the project as it will provide a positive net present value. It is observed that total

cash flow from different years considering the factor rate of 10% is 2490.55 and the initial

during which the net present value (NPV) is negative. This provides an indication of that same

margin of protection required in direct proportion to changes of return's potential decrease until it

exceeds the return on equity. If the sequence of income and expenses modifies upwards of when

over the design process, the IRR approach can produce two IRRs for much the same collection

of working capital. It also means that capital inflows over the project's existence can be recouped

only at IRR, which is often not the case because the company might not even have comparable

investment opportunities. The NPV approach has the disadvantage of assuming continuous

gearing to retain the very same return on equity. This is uncommon since cash inflows shift the

positioning over time. To retain the same rounding, a firm would need to print money on a

regular basis. Owing to logistical issues and expenditures, this is impossible to do. Cost of

money, which is used to calculate cash flows, is often difficult to quantify (Nair and Reddy,

2017). Finally, as an organisation experiences resource price controls, the NPV approach is

ineffective all by itself. In a resource rationing situation, the cash ratio will have to be combined

with the NPV to test investments.

year profit V.c

Fixed

cost

total

cost

Net

cash

flow

Discoun

t rate

(10 %)

cash

flow

2022 900 495 180 675 225 0.909

204.52

5

2023 1035 198 189 387 648 0.826

535.24

8

2024 1170 216 200 416 754 0.751

566.25

4

2025 1305 236 210 446 859 0.683

586.69

7

2026 1440 258 221 479 961 0.621

596.78

1

2490.5

5

Initial investment 550

Net present value

1940.5

5

Advise the firm on whether it should undertake the project

From the above table it can be determined that company must make the choice of

undertaking the project as it will provide a positive net present value. It is observed that total

cash flow from different years considering the factor rate of 10% is 2490.55 and the initial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investment will be 550 thus the value of NPV is 1940 which states that company will earn

positive cash flow from the project. The accounting rate of return (ARR) is indeed an investment

appraisal parameter that describes the estimated return on an expenditure in response to a

previous expense. ARR, unlike NPV, somehow doesn't take into investing a large amount of

capital, and even if the ARR becomes considerably greater than that of the payback period, the

venture is considered profitable.

ARR is reflected in the increasing yield, so a 20% ARR ensures that the company is

expected to return 20p for each and every 100p spent over all the course of a year. To find the

ARR, take the number return over a given time given time interval investment over the same

time period. The discrepancy between the real worth of initial investment as well as the

estimated price of income statement for a set period of time is called net present value (NPV).

NPV is really a capital market money management that estimates also for time level of resources

and can be used to measure a project's projected profitability (Naumovski, Taneski and

Dojcinovski, 2018). The financial leverage theorem states that assets are worth as much now as

this would be in the meantime and it has had sufficient time to collect appreciation. Revenues

and expenses are managed using the opportunity cost of capital principle, which takes into

account current interest rates.

Identify the maximum price Wholesome foods Plc should pay to acquire the Bonita Foods SL.

Option 1 has a 20.83 percent ARR. When there is no comparable benchmark, although it is

considerably greater than the price of capital around 12%, the ARR method supports investment

in Choice 1. 5.68 years seems to be the payback time. Despite the fact that the accounting rate of

return is considerably shorter than that of the program's 10-year lifespan, it falls short of the

financial producer's 5-year cut-off time. As a result, underneath the time value of money, the

contribution in scenario 1 is really not accepted. Option 1 has a really high and optimistic NPV

of £739,000. The purchasing of the property would raise the company's net worth by £739,000

over a ten-year term, so the transaction is accepted using the NPV process. Finally, profit IRR

around 19.43% is greater than the value of investment of 12%, indicating that the buying of the

company is justified.

Option 2 has an ARR cost 63.33 percent, and far more than the return on capital of 12

percent, so the ARR process accepts the expenditure. The payback term is 4.84 years, which is

below the financial director's 5-year cut-off duration. Option 2's contribution also is accepted

positive cash flow from the project. The accounting rate of return (ARR) is indeed an investment

appraisal parameter that describes the estimated return on an expenditure in response to a

previous expense. ARR, unlike NPV, somehow doesn't take into investing a large amount of

capital, and even if the ARR becomes considerably greater than that of the payback period, the

venture is considered profitable.

ARR is reflected in the increasing yield, so a 20% ARR ensures that the company is

expected to return 20p for each and every 100p spent over all the course of a year. To find the

ARR, take the number return over a given time given time interval investment over the same

time period. The discrepancy between the real worth of initial investment as well as the

estimated price of income statement for a set period of time is called net present value (NPV).

NPV is really a capital market money management that estimates also for time level of resources

and can be used to measure a project's projected profitability (Naumovski, Taneski and

Dojcinovski, 2018). The financial leverage theorem states that assets are worth as much now as

this would be in the meantime and it has had sufficient time to collect appreciation. Revenues

and expenses are managed using the opportunity cost of capital principle, which takes into

account current interest rates.

Identify the maximum price Wholesome foods Plc should pay to acquire the Bonita Foods SL.

Option 1 has a 20.83 percent ARR. When there is no comparable benchmark, although it is

considerably greater than the price of capital around 12%, the ARR method supports investment

in Choice 1. 5.68 years seems to be the payback time. Despite the fact that the accounting rate of

return is considerably shorter than that of the program's 10-year lifespan, it falls short of the

financial producer's 5-year cut-off time. As a result, underneath the time value of money, the

contribution in scenario 1 is really not accepted. Option 1 has a really high and optimistic NPV

of £739,000. The purchasing of the property would raise the company's net worth by £739,000

over a ten-year term, so the transaction is accepted using the NPV process. Finally, profit IRR

around 19.43% is greater than the value of investment of 12%, indicating that the buying of the

company is justified.

Option 2 has an ARR cost 63.33 percent, and far more than the return on capital of 12

percent, so the ARR process accepts the expenditure. The payback term is 4.84 years, which is

below the financial director's 5-year cut-off duration. Option 2's contribution also is accepted

using the payback period process. The disparities in outcomes between the different investment

valuation approaches are unsurprising. Future cash balances are not discounted using the ARR or

payback time models. This is a significant disadvantage in this situation since the cash balances

are distributed over a 10-year period. Furthermore, the return on capital remains high (12%), and

just not disregarding the working capital sometimes doesn't represent the investment manager

risk. The findings of the ARR and decision time approaches can be interpreted with scepticism in

light of the preceding claims.

Option 1 is preferred by the Payback period since the NPV levels £116,000 more than alternative

2. Option 1 has a higher upfront expenditure, which seems expressed through its low IRR

compared to option 2. Option 2 has a positive net present value of £623,000. Under that same

NPV method, Option 2 was therefore accepted. Eventually, the IRR around 27.48 percent is

cheaper than the increase of capital of 12 percent, indicating that the company should be

purchased. The ARR, usable life, and IRR approaches both favour option 2 above option 1. The

Npv approach, however, prefers following options over second option since the NPV of scenario

1 is greater than among option 2. Option 1 is the best option for such corporation because it

provides the most net value to the company. If funds are restricted, though, option 1 must be

chosen since this contributes more net worth per unit of money. Option 2 has a net worth per unit

expenditure of £2.08 to £0.49 for alternative 1 (Schade and et.al., 2016).

Advise the firm on the potential impact of foreign exchange on the project

In relation with the above examination, the investment plan must weigh a few additional,

but equally significant, factors. To begin, it was expected in the study of Option 1 that perhaps

the field would be purchased for £1,500,000 after ten years. O n the other hand, have risen in

recent years the sensitivity including its NPV on the basis of best and worst case scenario is to

increases the price as mentioned in the given information. Over a ten-year term, farmer wage

growth of 6% will significantly raise the NPV to £1,121,000. This is a substantial increase. The

NPV is still optimistic even though total agricultural rising prices is -2 percent. Forms in farm

prices, but at the other side, would have very little influence on NPV. Changes in plant values,

but from the other side, will have little influence on the NPV under option 2. The potential for a

direct gain from the purchasing of a farmland should be considered before making a decision.

Due to a massive variety of variables, predicting cash flows beyond a 10-year term is impossible.

Demand can fluctuate as a result of broader economic developments. Material as well as

valuation approaches are unsurprising. Future cash balances are not discounted using the ARR or

payback time models. This is a significant disadvantage in this situation since the cash balances

are distributed over a 10-year period. Furthermore, the return on capital remains high (12%), and

just not disregarding the working capital sometimes doesn't represent the investment manager

risk. The findings of the ARR and decision time approaches can be interpreted with scepticism in

light of the preceding claims.

Option 1 is preferred by the Payback period since the NPV levels £116,000 more than alternative

2. Option 1 has a higher upfront expenditure, which seems expressed through its low IRR

compared to option 2. Option 2 has a positive net present value of £623,000. Under that same

NPV method, Option 2 was therefore accepted. Eventually, the IRR around 27.48 percent is

cheaper than the increase of capital of 12 percent, indicating that the company should be

purchased. The ARR, usable life, and IRR approaches both favour option 2 above option 1. The

Npv approach, however, prefers following options over second option since the NPV of scenario

1 is greater than among option 2. Option 1 is the best option for such corporation because it

provides the most net value to the company. If funds are restricted, though, option 1 must be

chosen since this contributes more net worth per unit of money. Option 2 has a net worth per unit

expenditure of £2.08 to £0.49 for alternative 1 (Schade and et.al., 2016).

Advise the firm on the potential impact of foreign exchange on the project

In relation with the above examination, the investment plan must weigh a few additional,

but equally significant, factors. To begin, it was expected in the study of Option 1 that perhaps

the field would be purchased for £1,500,000 after ten years. O n the other hand, have risen in

recent years the sensitivity including its NPV on the basis of best and worst case scenario is to

increases the price as mentioned in the given information. Over a ten-year term, farmer wage

growth of 6% will significantly raise the NPV to £1,121,000. This is a substantial increase. The

NPV is still optimistic even though total agricultural rising prices is -2 percent. Forms in farm

prices, but at the other side, would have very little influence on NPV. Changes in plant values,

but from the other side, will have little influence on the NPV under option 2. The potential for a

direct gain from the purchasing of a farmland should be considered before making a decision.

Due to a massive variety of variables, predicting cash flows beyond a 10-year term is impossible.

Demand can fluctuate as a result of broader economic developments. Material as well as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production costs can increase more quickly than expected. In addition, bad weather will cause

problems on the development. As a result, doing a sensitivity analysis through cash flows is

useful. Variable costs are expected to fluctuate in directly proportional to fluctuations in sales

(Steinbart and et.al., 2018).

Evaluate the alternatives for financing the purchase.

Adjustments throughout the cost of capital will also affect the NPV. The vulnerability of two

alternatives' NPVs to increases mostly in cost of capital. Option 1 is much more affected by

increases in capital costs. Before implementing a definitive decision, the corporation should

consider the possible cost of capital rises for the next ten years. In response to the

aforementioned considerations, the corporation can look at a few important non-financial

initiatives to ensure that such investment pays off. In any scenario, it should assess if there was a

local market for organic foods. In comparison to synthetic foods, healthy products command a

higher price. Consumers have little purchasing power. Market purchasing power is influenced by

the state of the economy as a whole. The UK economy is going through a difficult period, with

investors worried about tax rises. This might make it possible for the business to export its goods

in the market. In comparison to current activities in the South, the organisation should also

identify the capital needed for successful monitoring of something like the plant inside the north.

Long-distance planning and evaluation are critical for an investment portfolio sustainability and

they can be hampered by distance (Wollschlaeger, Sauter and Jasperneite, 2017).

The financial director from Wholesome Organic Foods now has estimated the developments

inside the Spanish supermarket market and determined that the plan merits further examination.

The supervisors are worried about currency fluctuations because it's Wholesome Organic Foods'

first foray into international markets. The company is intrigued not only by the prospect of

expanding its product line, but also by the prospect of entering the supermarket market. Despite

the fact that several rivals, the directors believe that there really is a ready demand in Spain with

their well brand and product (Yeoh and Popovič, 2016).

CONCLUSION

The company's nominal shareholder equity is €550,000, as well as the representatives have

stated that a 100% valuation is required. There is no appropriate price/earnings calculation since

the company is currently home to people. The investigation into the purchase of Bonita Foods

problems on the development. As a result, doing a sensitivity analysis through cash flows is

useful. Variable costs are expected to fluctuate in directly proportional to fluctuations in sales

(Steinbart and et.al., 2018).

Evaluate the alternatives for financing the purchase.

Adjustments throughout the cost of capital will also affect the NPV. The vulnerability of two

alternatives' NPVs to increases mostly in cost of capital. Option 1 is much more affected by

increases in capital costs. Before implementing a definitive decision, the corporation should

consider the possible cost of capital rises for the next ten years. In response to the

aforementioned considerations, the corporation can look at a few important non-financial

initiatives to ensure that such investment pays off. In any scenario, it should assess if there was a

local market for organic foods. In comparison to synthetic foods, healthy products command a

higher price. Consumers have little purchasing power. Market purchasing power is influenced by

the state of the economy as a whole. The UK economy is going through a difficult period, with

investors worried about tax rises. This might make it possible for the business to export its goods

in the market. In comparison to current activities in the South, the organisation should also

identify the capital needed for successful monitoring of something like the plant inside the north.

Long-distance planning and evaluation are critical for an investment portfolio sustainability and

they can be hampered by distance (Wollschlaeger, Sauter and Jasperneite, 2017).

The financial director from Wholesome Organic Foods now has estimated the developments

inside the Spanish supermarket market and determined that the plan merits further examination.

The supervisors are worried about currency fluctuations because it's Wholesome Organic Foods'

first foray into international markets. The company is intrigued not only by the prospect of

expanding its product line, but also by the prospect of entering the supermarket market. Despite

the fact that several rivals, the directors believe that there really is a ready demand in Spain with

their well brand and product (Yeoh and Popovič, 2016).

CONCLUSION

The company's nominal shareholder equity is €550,000, as well as the representatives have

stated that a 100% valuation is required. There is no appropriate price/earnings calculation since

the company is currently home to people. The investigation into the purchase of Bonita Foods

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SL retail locations provides an extension of the business's exporting operations, as well as an

important aspect of diversity for the group.

important aspect of diversity for the group.

REFERENCES

Massa, L., Tucci, C. L. and Afuah, A., 2017. A critical assessment of business model research.

Academy of Management Annals. 11(1). pp.73-104.

Merton, R., 2016. Manifest and latent functions. Social theory re-wired: new connections to

classical and contemporary perspectives (2nd edition). New York: Routledge. pp.68-84.

Nair, J. and Reddy, D. B. S., 2017. Leveraging Enterprise Resource Planning Systems to Digitize

Business Functions. In Enterprise Information Systems and the Digitalization of

Business Functions (pp. 20-46). IGI Global.

Naumovski, T., Taneski, N. and Dojcinovski, M., 2018. Supporting Critical Business Functions

by using Public Key Infrastructure (PKI).

Schade, M. and et.al., 2016. The impact of attitude functions on luxury brand consumption: An

age-based group comparison. Journal of business research. 69(1). pp.314-322.

Steinbart, P. J. and et.al., 2018. The influence of a good relationship between the internal audit

and information security functions on information security outcomes. Accounting,

Organizations and Society. 71. pp.15-29.

Wollschlaeger, M., Sauter, T. and Jasperneite, J., 2017. The future of industrial communication:

Automation networks in the era of the internet of things and industry 4.0. IEEE

industrial electronics magazine. 11(1). pp.17-27.

Yeoh, W. and Popovič, A., 2016. Extending the understanding of critical success factors for

implementing business intelligence systems. Journal of the Association for Information

Science and Technology. 67(1). pp.134-147.

Massa, L., Tucci, C. L. and Afuah, A., 2017. A critical assessment of business model research.

Academy of Management Annals. 11(1). pp.73-104.

Merton, R., 2016. Manifest and latent functions. Social theory re-wired: new connections to

classical and contemporary perspectives (2nd edition). New York: Routledge. pp.68-84.

Nair, J. and Reddy, D. B. S., 2017. Leveraging Enterprise Resource Planning Systems to Digitize

Business Functions. In Enterprise Information Systems and the Digitalization of

Business Functions (pp. 20-46). IGI Global.

Naumovski, T., Taneski, N. and Dojcinovski, M., 2018. Supporting Critical Business Functions

by using Public Key Infrastructure (PKI).

Schade, M. and et.al., 2016. The impact of attitude functions on luxury brand consumption: An

age-based group comparison. Journal of business research. 69(1). pp.314-322.

Steinbart, P. J. and et.al., 2018. The influence of a good relationship between the internal audit

and information security functions on information security outcomes. Accounting,

Organizations and Society. 71. pp.15-29.

Wollschlaeger, M., Sauter, T. and Jasperneite, J., 2017. The future of industrial communication:

Automation networks in the era of the internet of things and industry 4.0. IEEE

industrial electronics magazine. 11(1). pp.17-27.

Yeoh, W. and Popovič, A., 2016. Extending the understanding of critical success factors for

implementing business intelligence systems. Journal of the Association for Information

Science and Technology. 67(1). pp.134-147.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.