Finance Homework: Money Multiplier, Interest Rates, and Bonds

VerifiedAdded on 2019/09/20

|5

|1772

|186

Homework Assignment

AI Summary

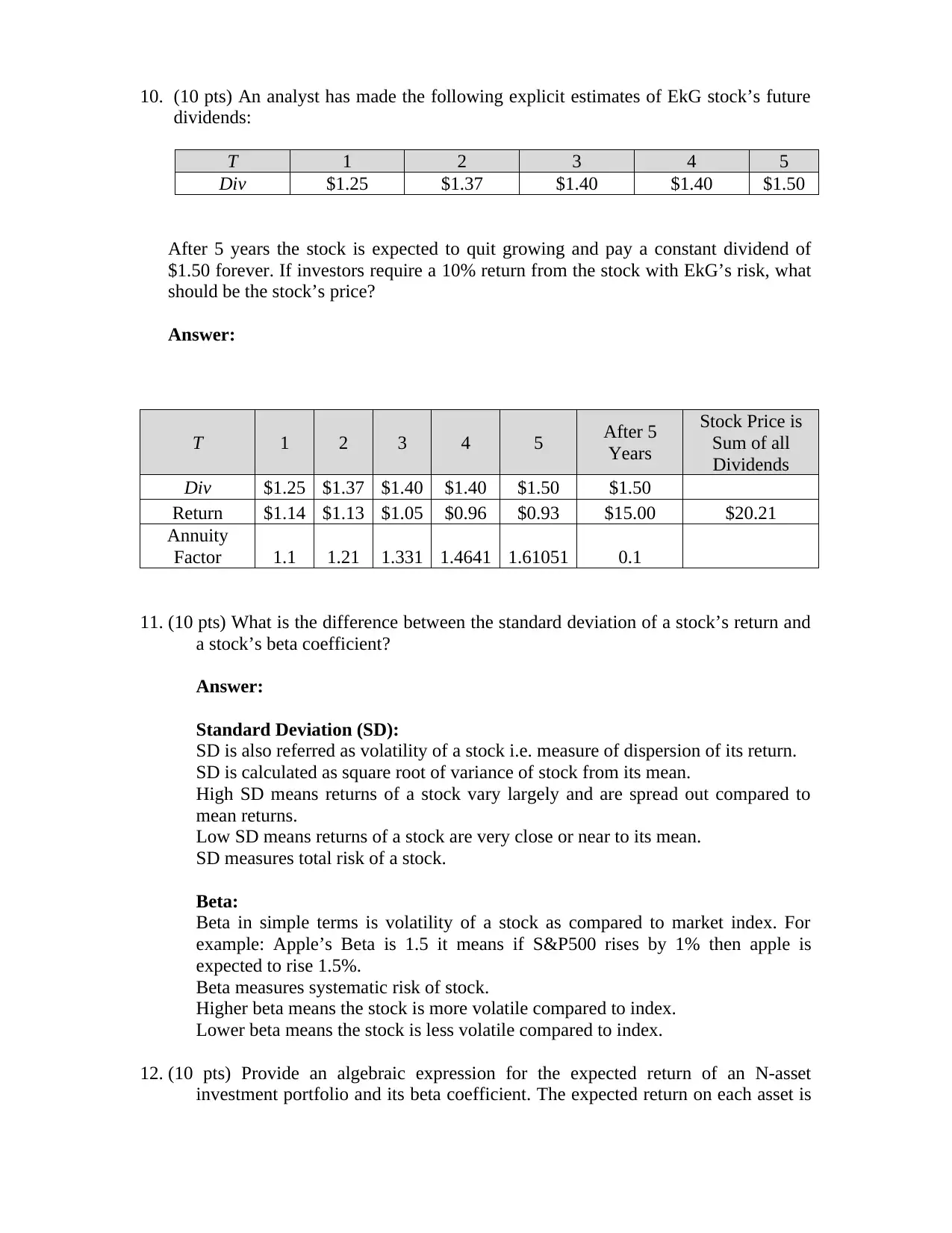

This finance homework assignment presents a series of problems covering key concepts in financial economics and investment analysis. The assignment begins with questions on the money multiplier and the impact of government securities purchases on the money supply. It then delves into macroeconomic topics, including the effects of tax cuts, interest rate parity, and the impact of inflation expectations on real and nominal interest rates. The assignment further explores investment strategies, including bond valuation, yield to maturity calculations, and the analysis of commercial paper and stock valuation using dividend discount models. Finally, it covers portfolio management, including the differences between standard deviation and beta coefficients and the calculation of expected portfolio returns and beta coefficients.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.