Finance Assignment 1: Depreciation, Cash Flow, and Investment Analysis

VerifiedAdded on 2023/01/06

|5

|892

|24

Homework Assignment

AI Summary

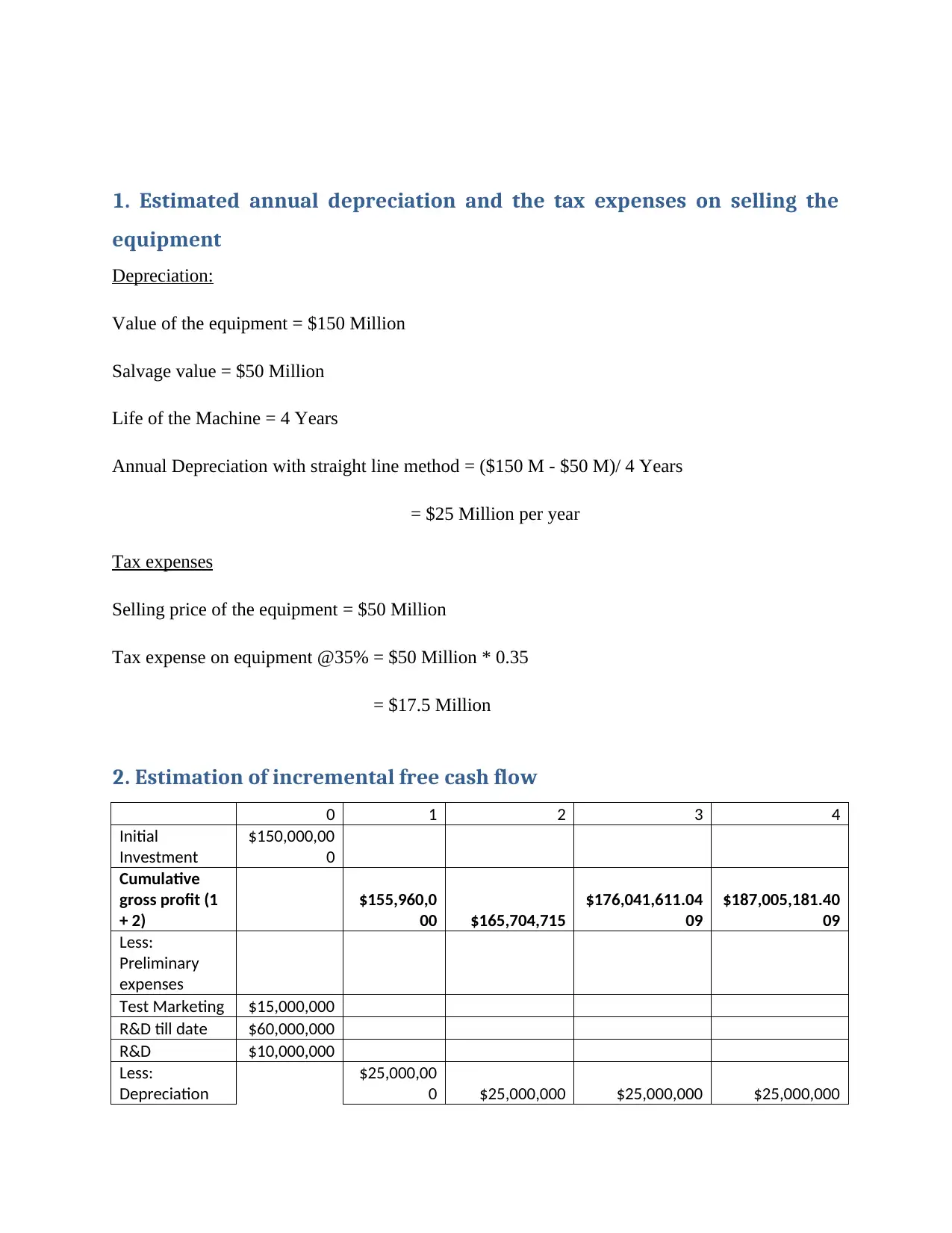

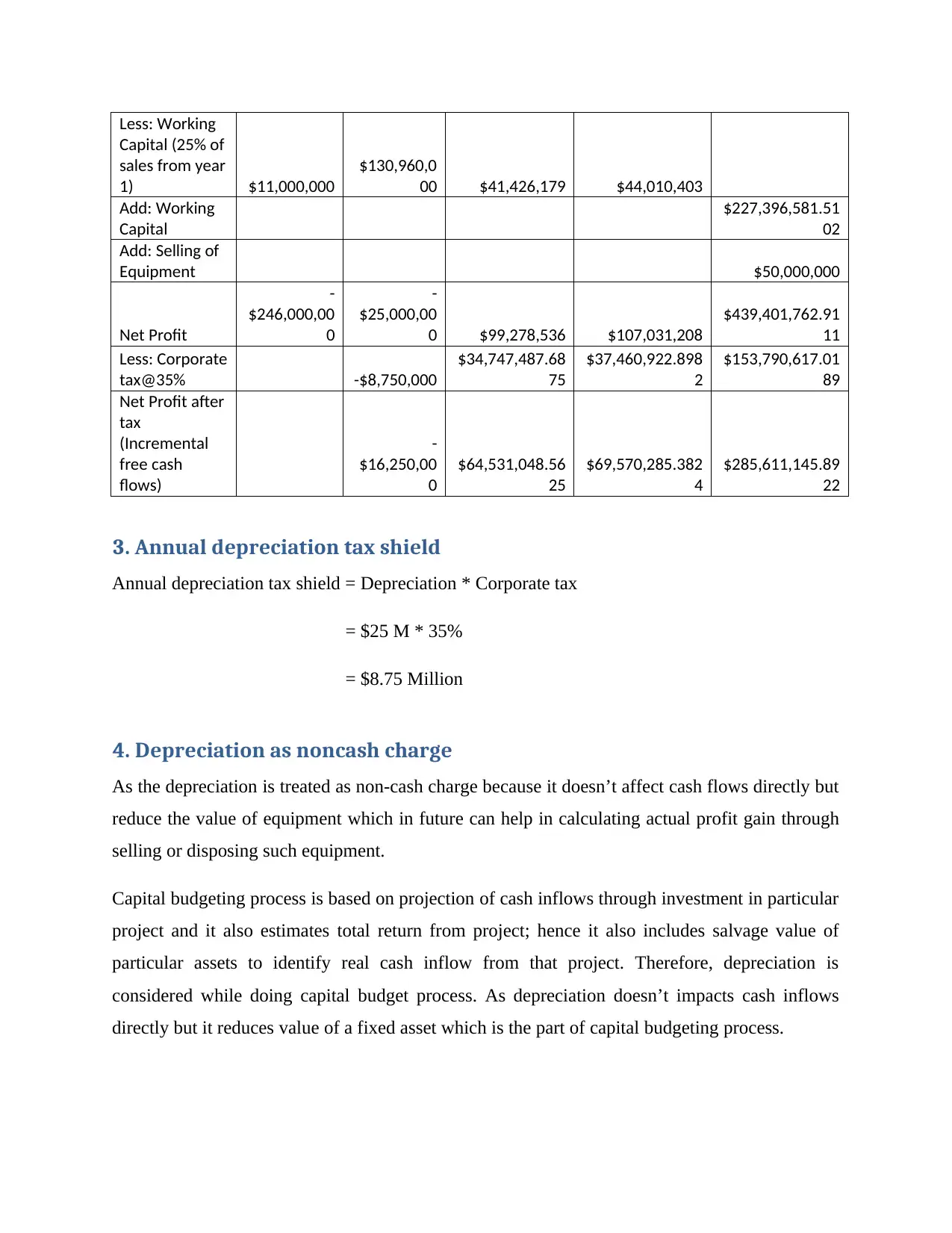

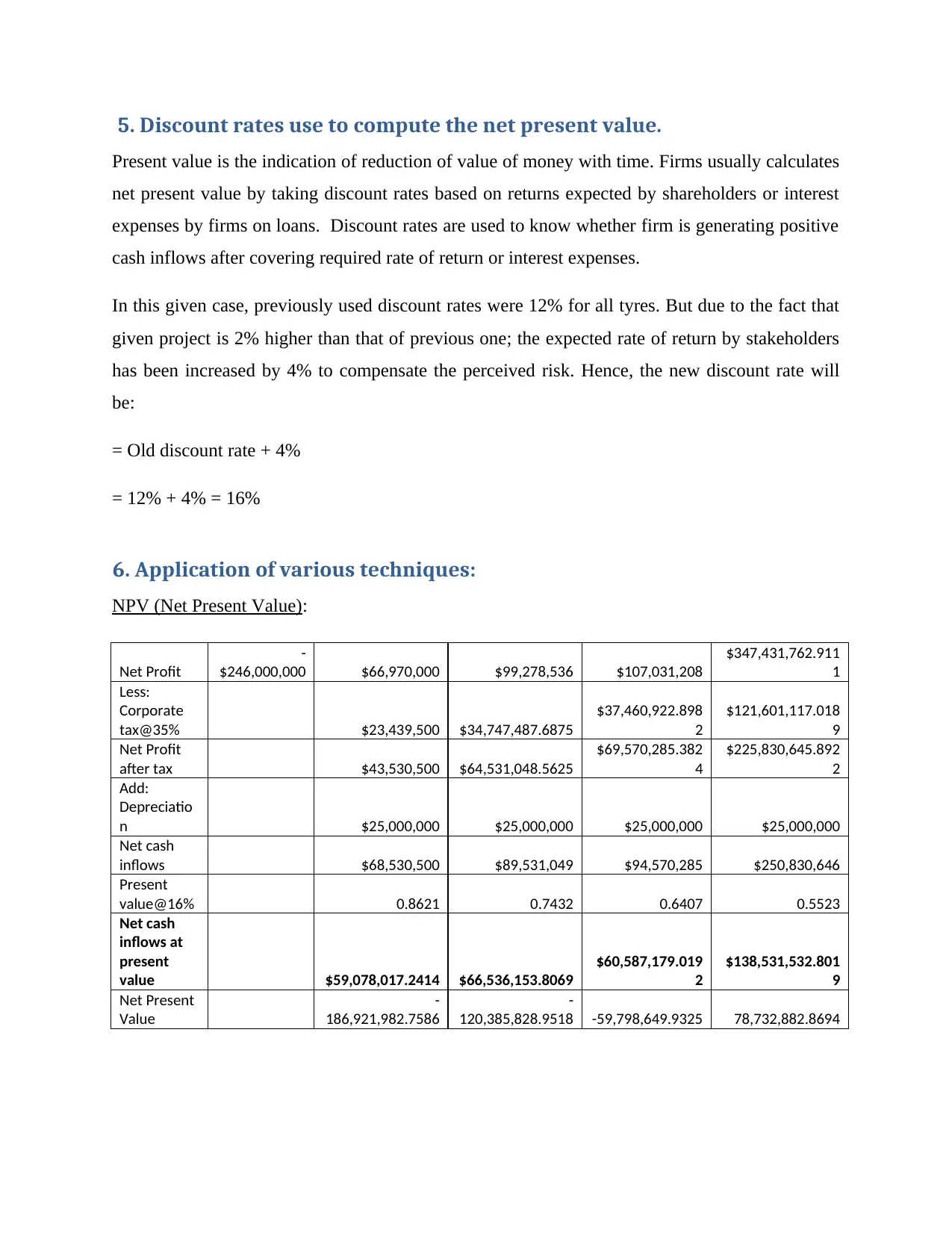

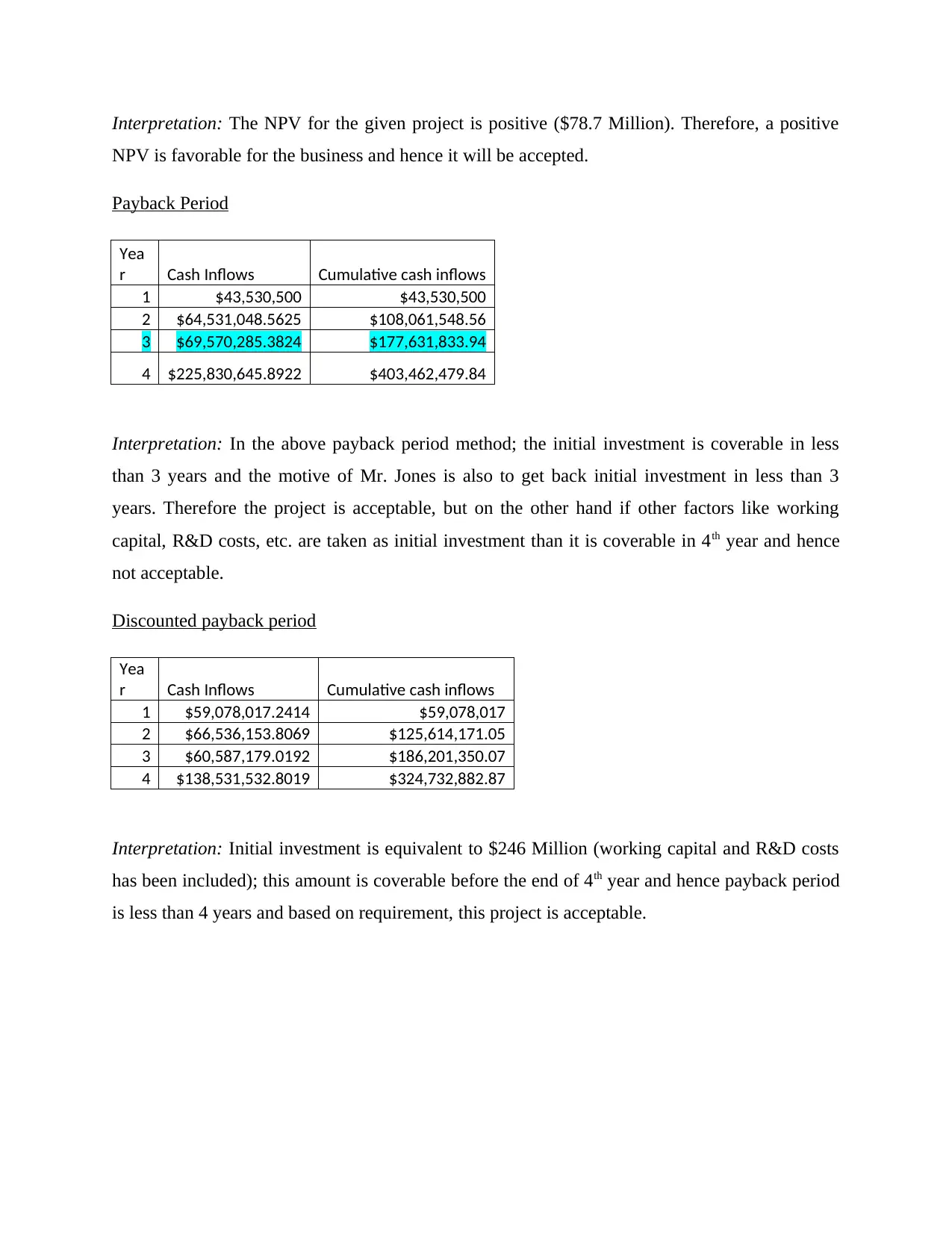

This finance assignment provides a comprehensive analysis of an investment project. It begins by calculating annual depreciation using the straight-line method and determining the tax expenses associated with selling the equipment. The assignment then estimates incremental free cash flows over a four-year period, considering initial investments, gross profits, preliminary expenses, depreciation, and working capital. The annual depreciation tax shield is calculated, and the concept of depreciation as a non-cash charge is explained within the context of capital budgeting. Furthermore, the assignment addresses the use of discount rates, explaining the rationale behind adjusting the rate to reflect project-specific risks. Finally, the assignment applies various capital budgeting techniques, including Net Present Value (NPV), Payback Period, and Discounted Payback Period, providing interpretations and conclusions regarding the project's financial viability. The NPV is calculated to be positive, supporting the project's acceptance, while the payback periods are evaluated against the investor's criteria.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.