Finance Assignment: Investment Analysis and Valuation

VerifiedAdded on 2022/09/07

|24

|2170

|31

Homework Assignment

AI Summary

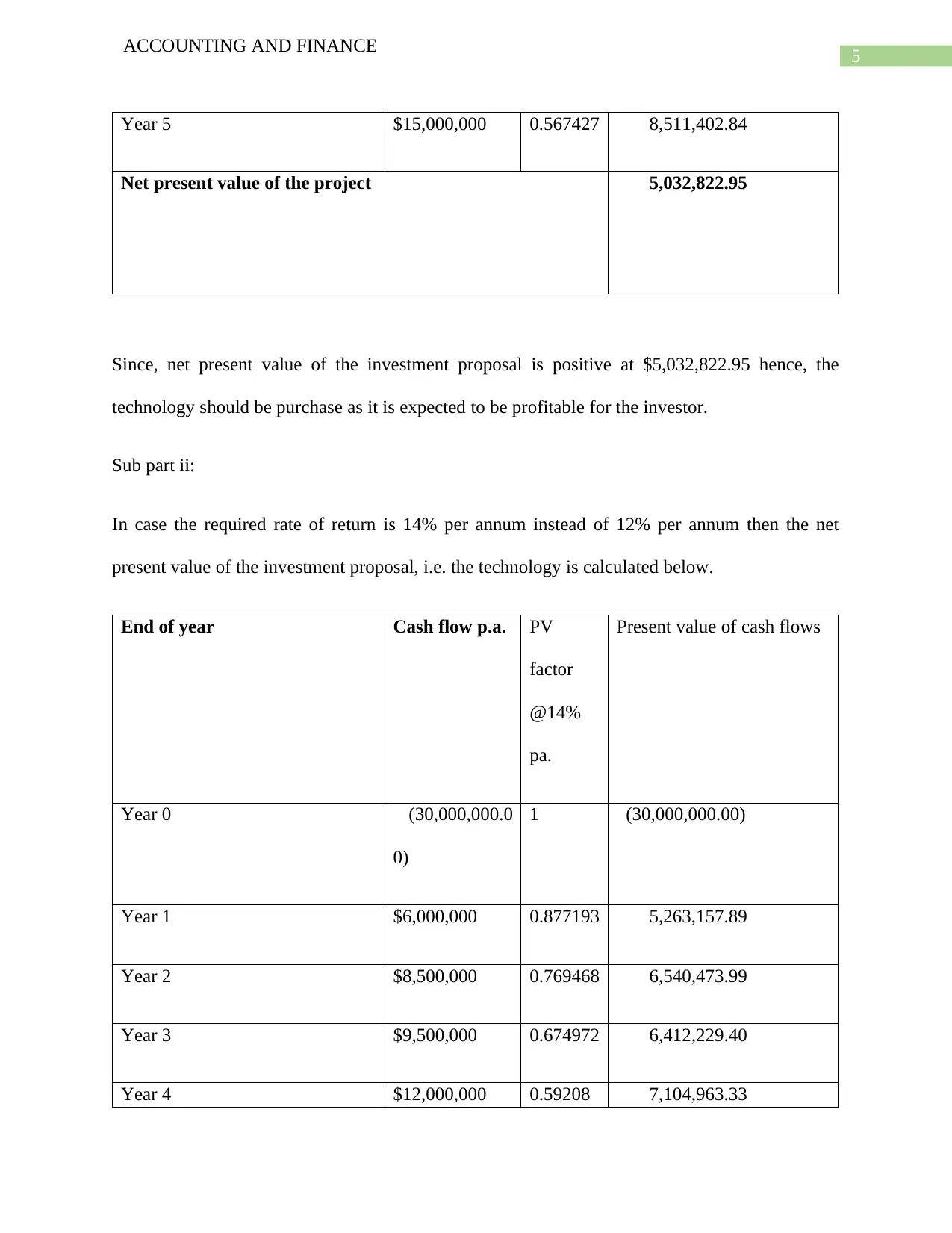

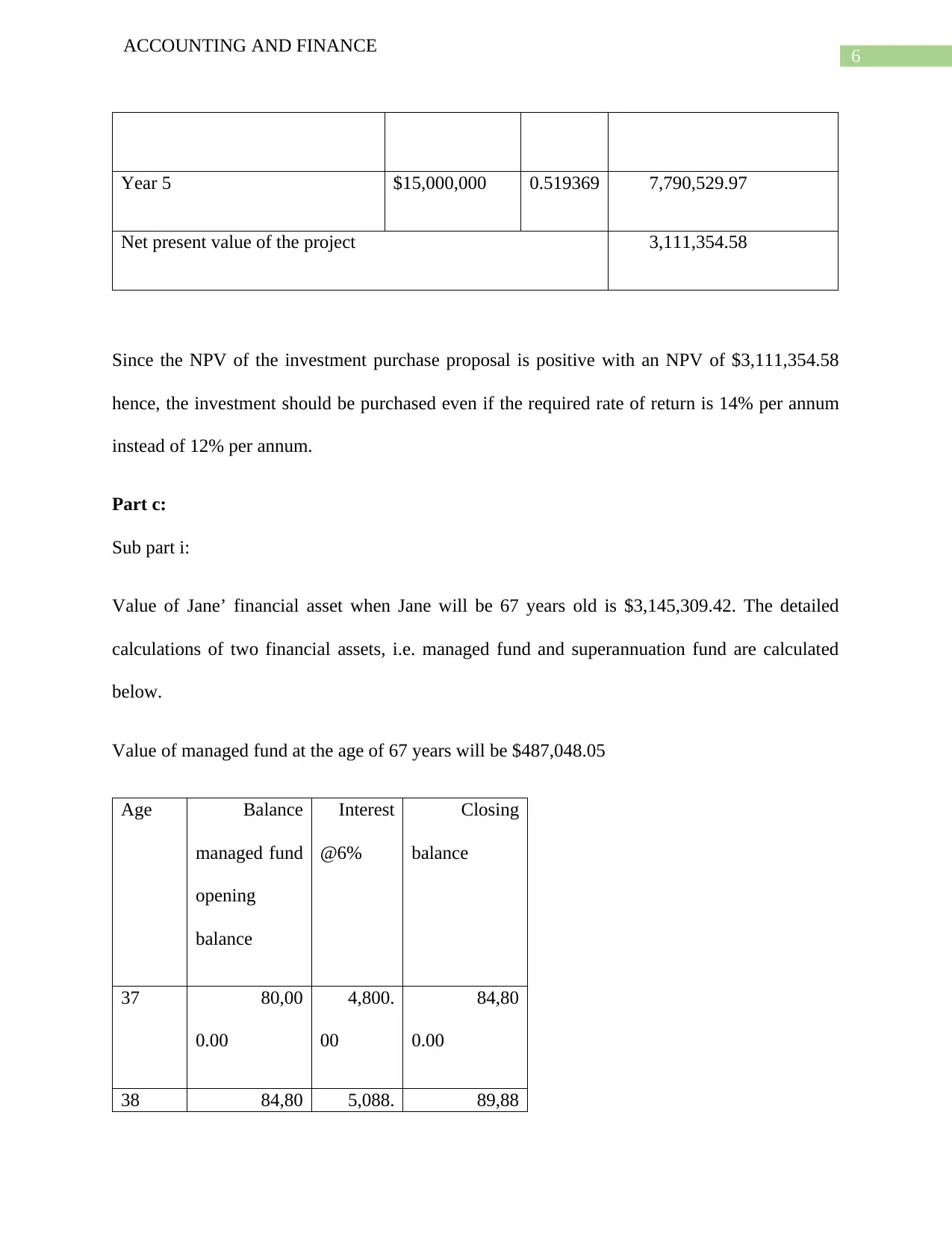

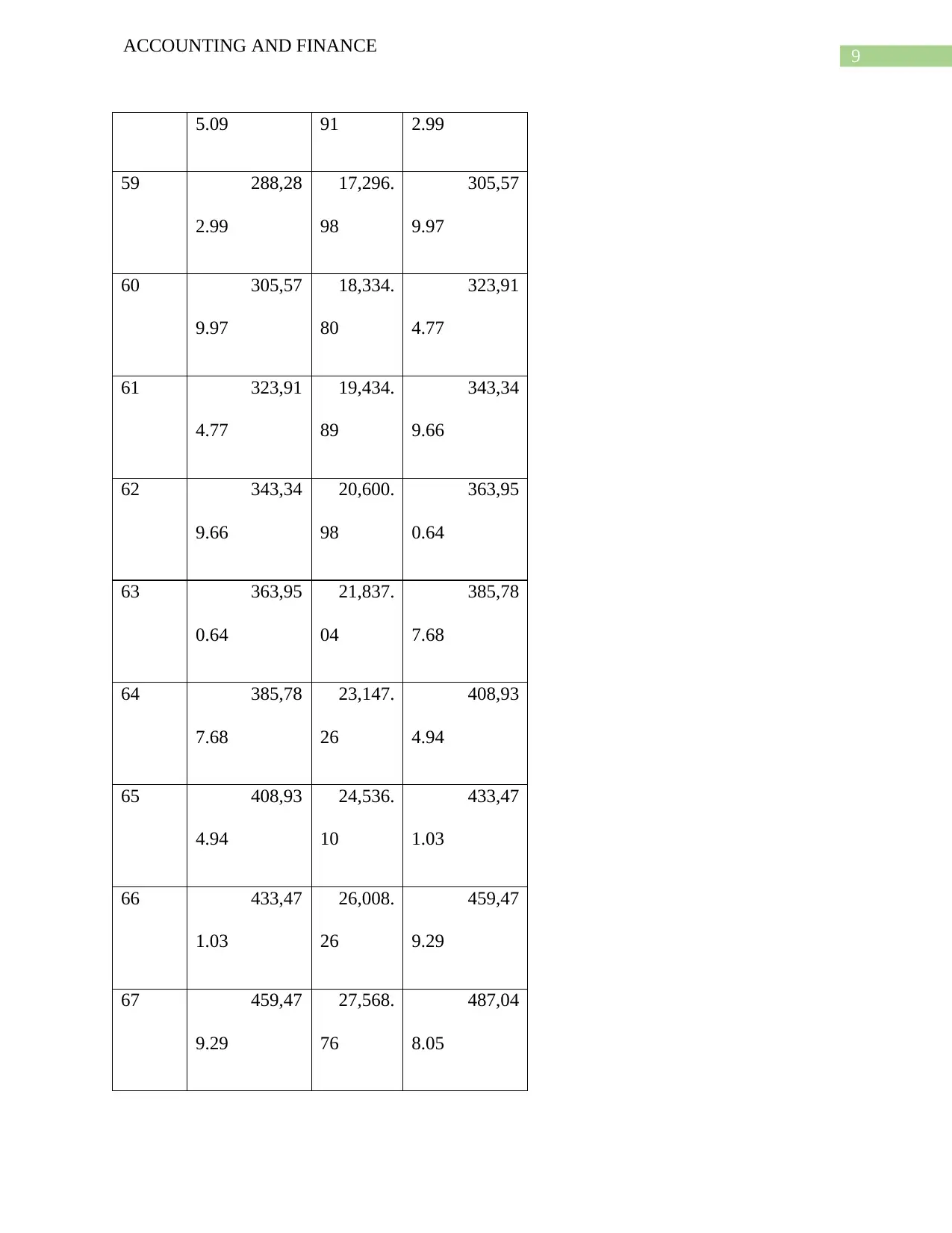

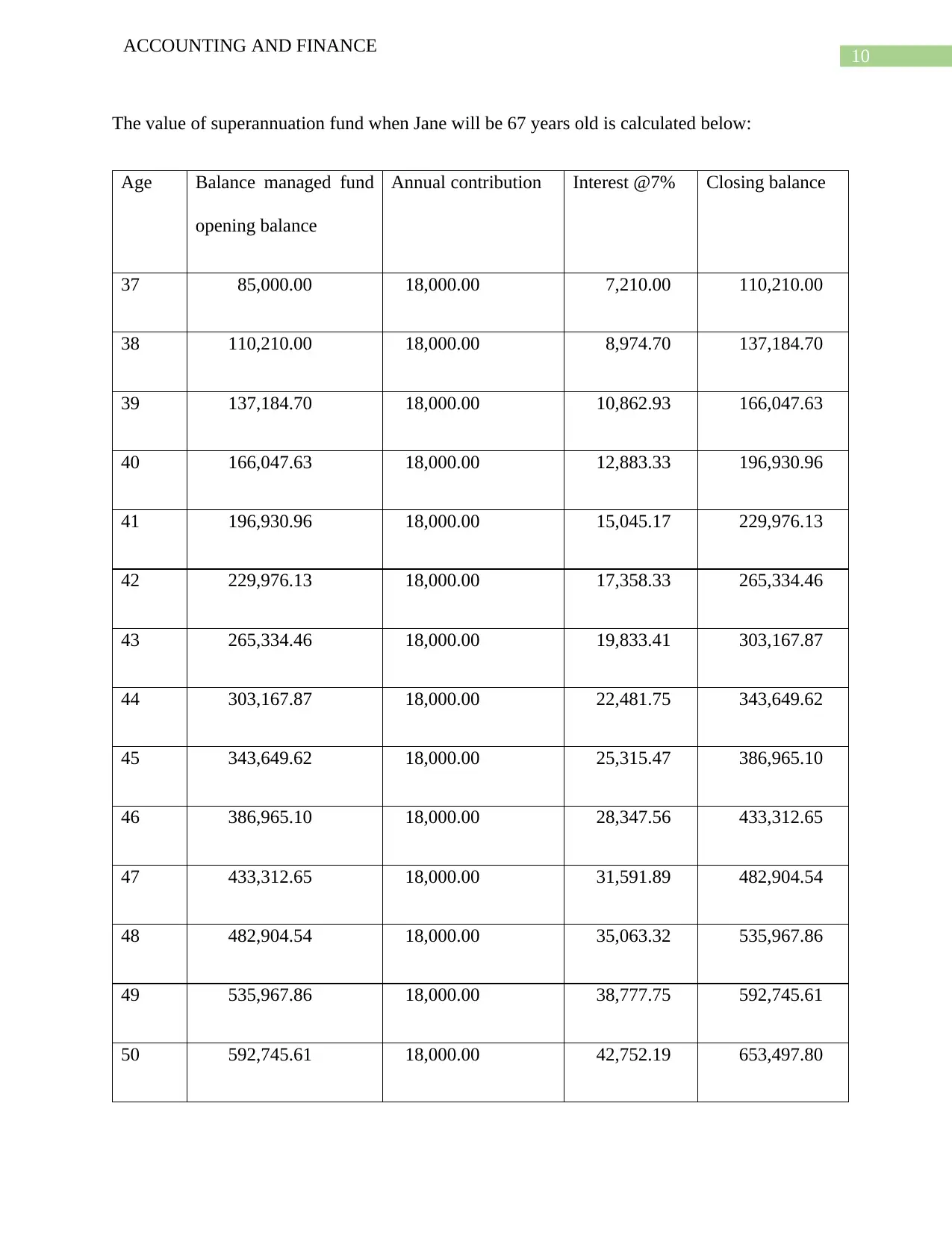

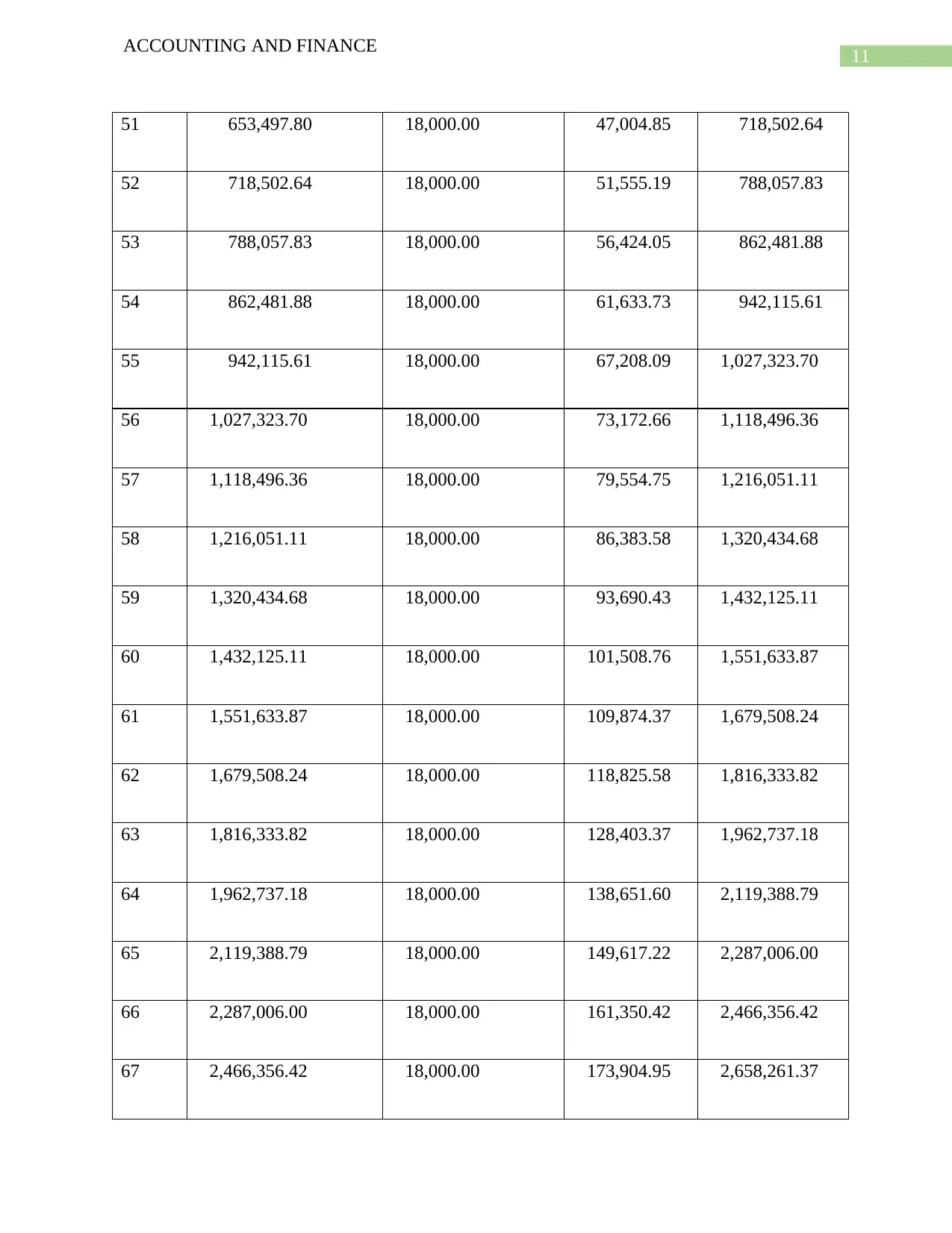

This finance assignment provides a comprehensive analysis of various financial concepts. It begins with calculating quarterly investments needed to reach a future savings goal, considering compound interest. The assignment then delves into investment appraisal, calculating the Net Present Value (NPV) of a recycling technology investment under different rates of return. Furthermore, the assignment explores personal financial planning, determining the future value of managed funds and superannuation. It includes calculations for portfolio beta and risk assessment, comparing the risk of a portfolio to the market. Finally, the assignment analyzes the performance of Qantas stock, calculating its expected rate of return and standard deviation, and comparing its risk profile to the overall market risk.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.