Tesco and Sainsbury: Finance Report on Ratio Analysis and Investment

VerifiedAdded on 2022/12/30

|19

|3991

|77

Report

AI Summary

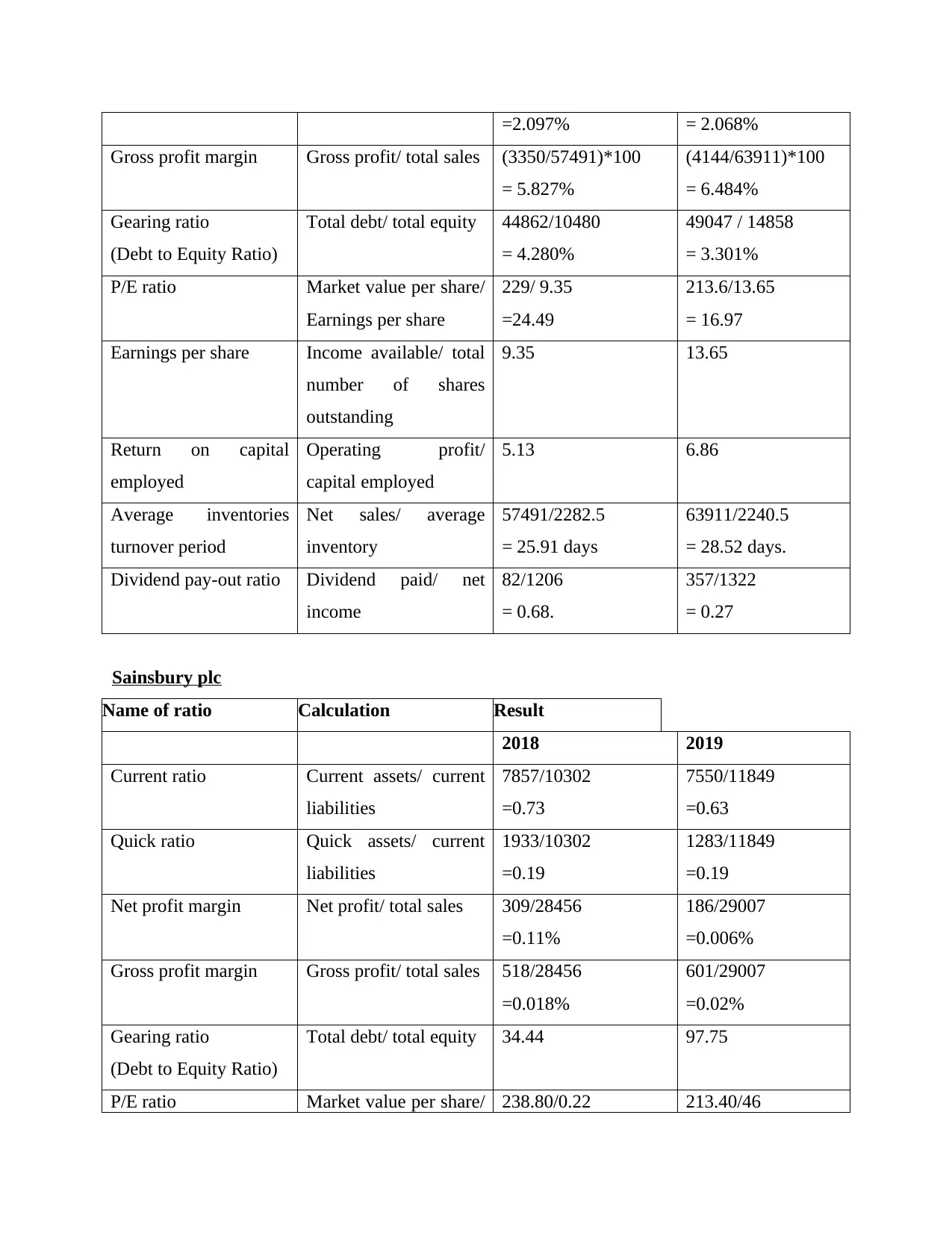

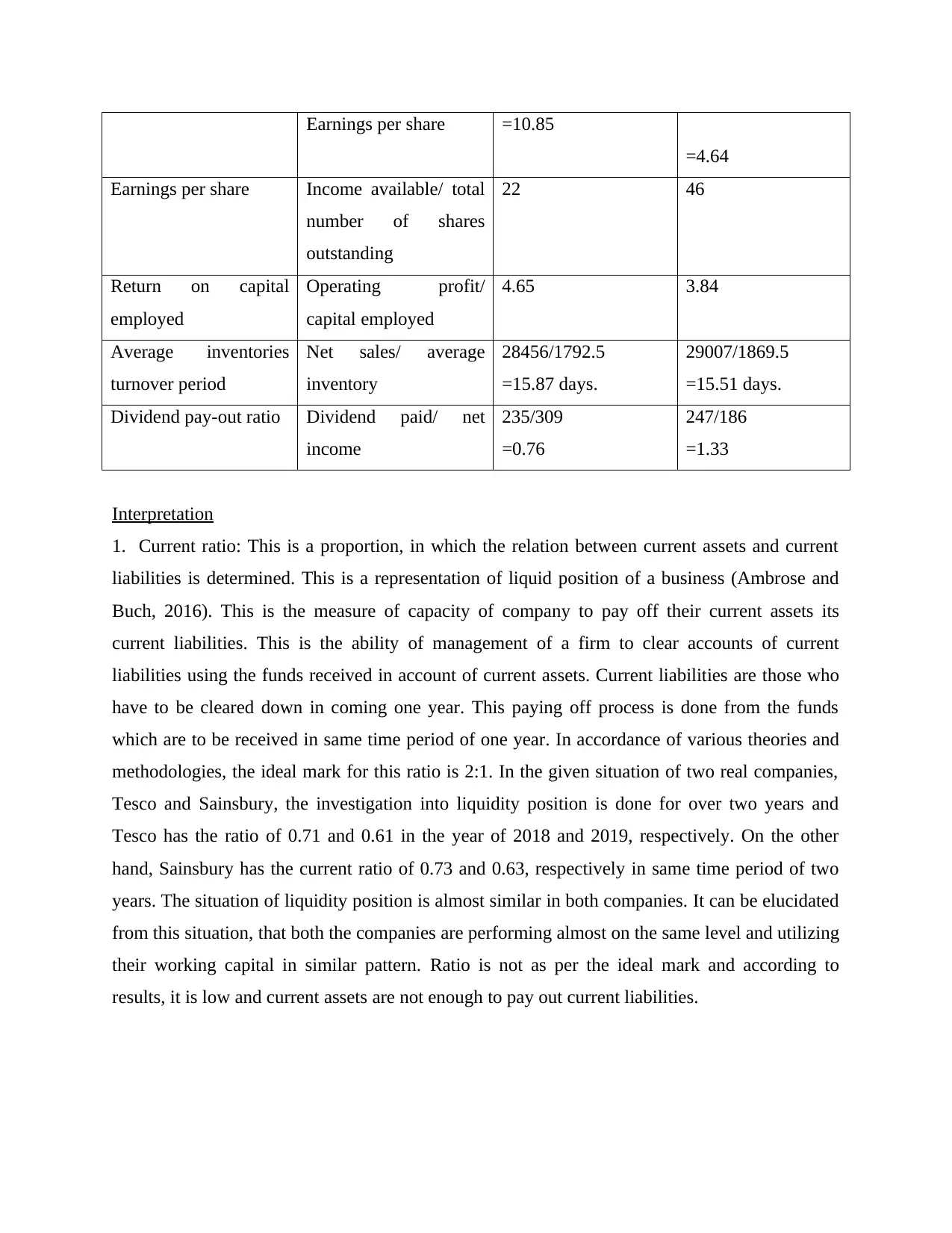

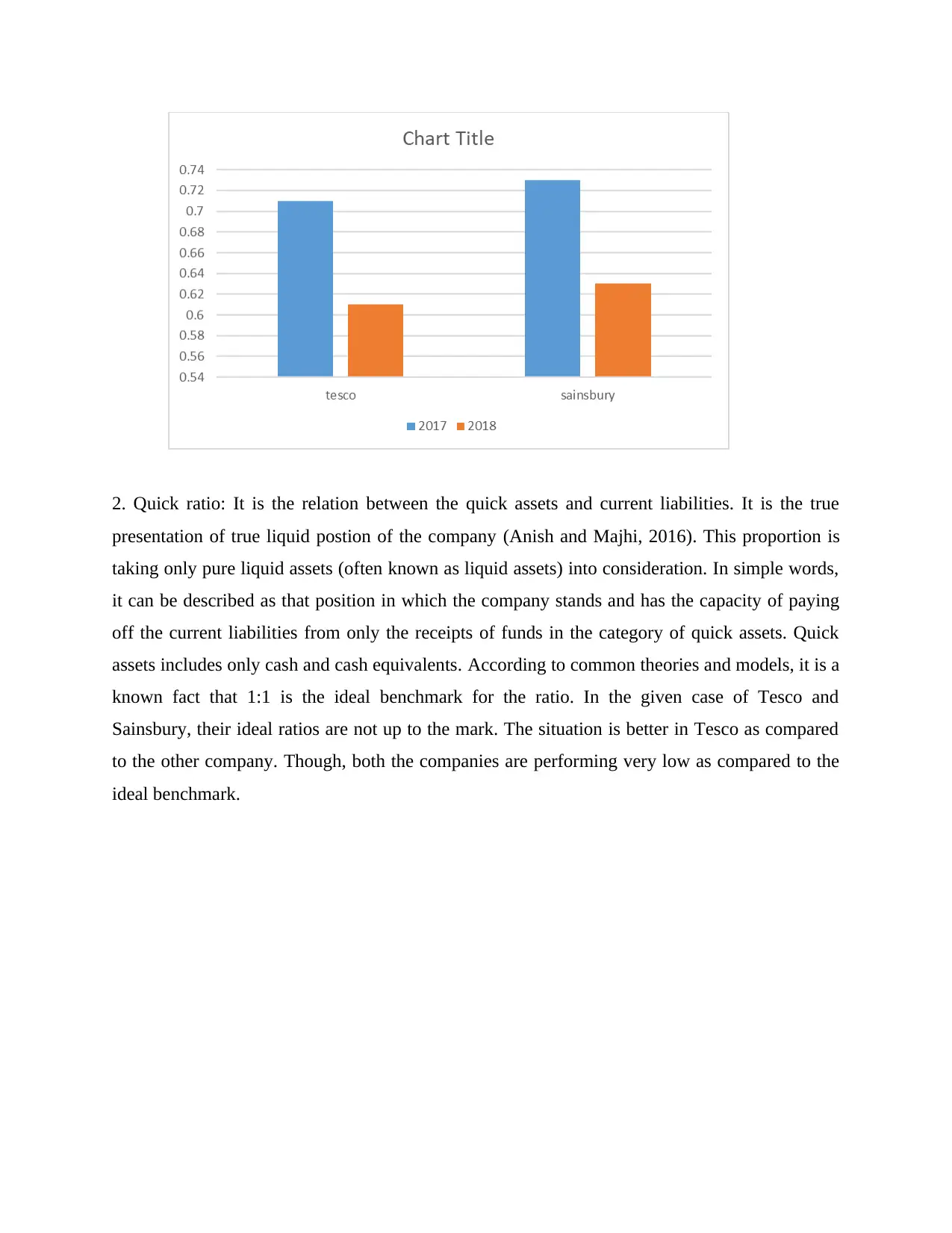

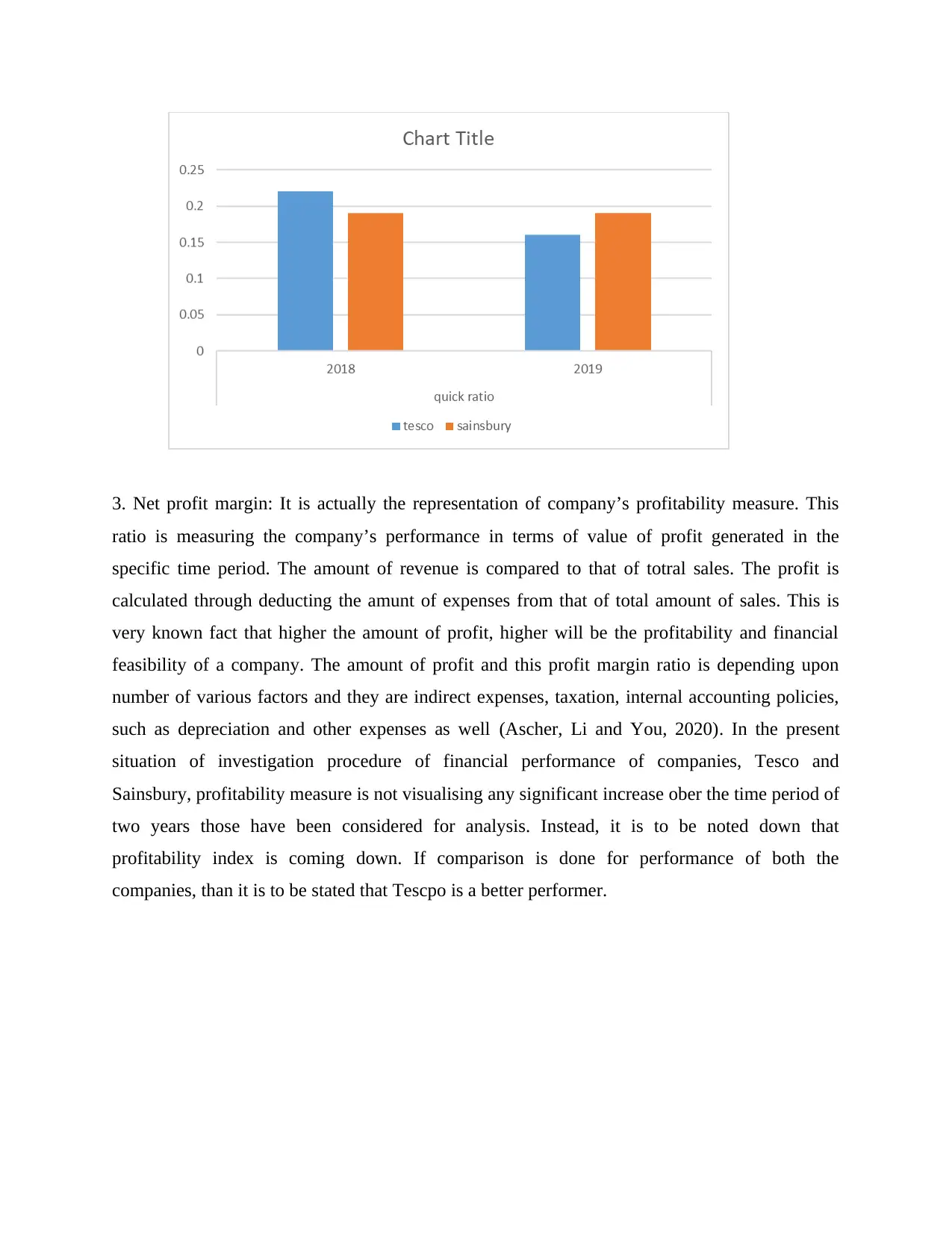

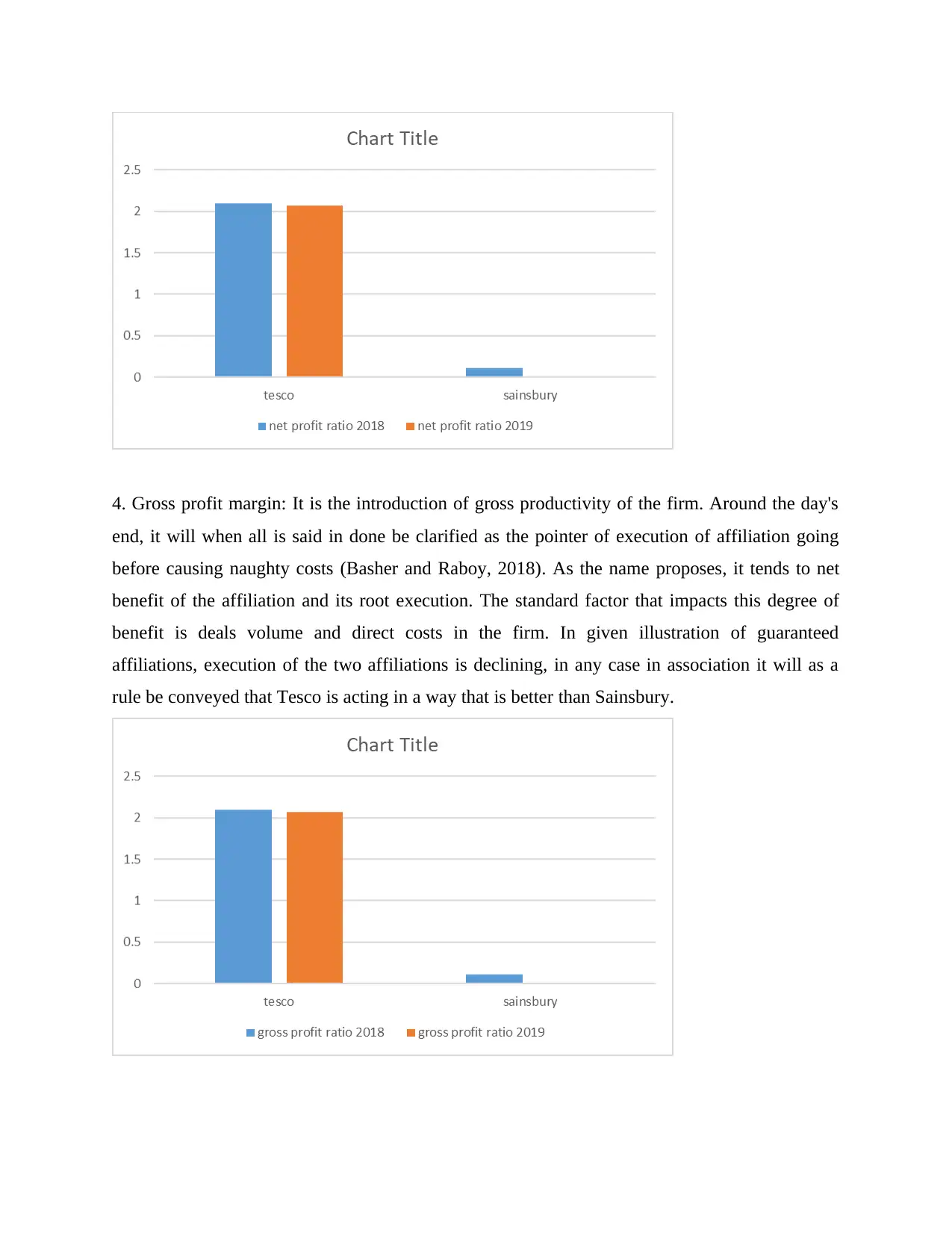

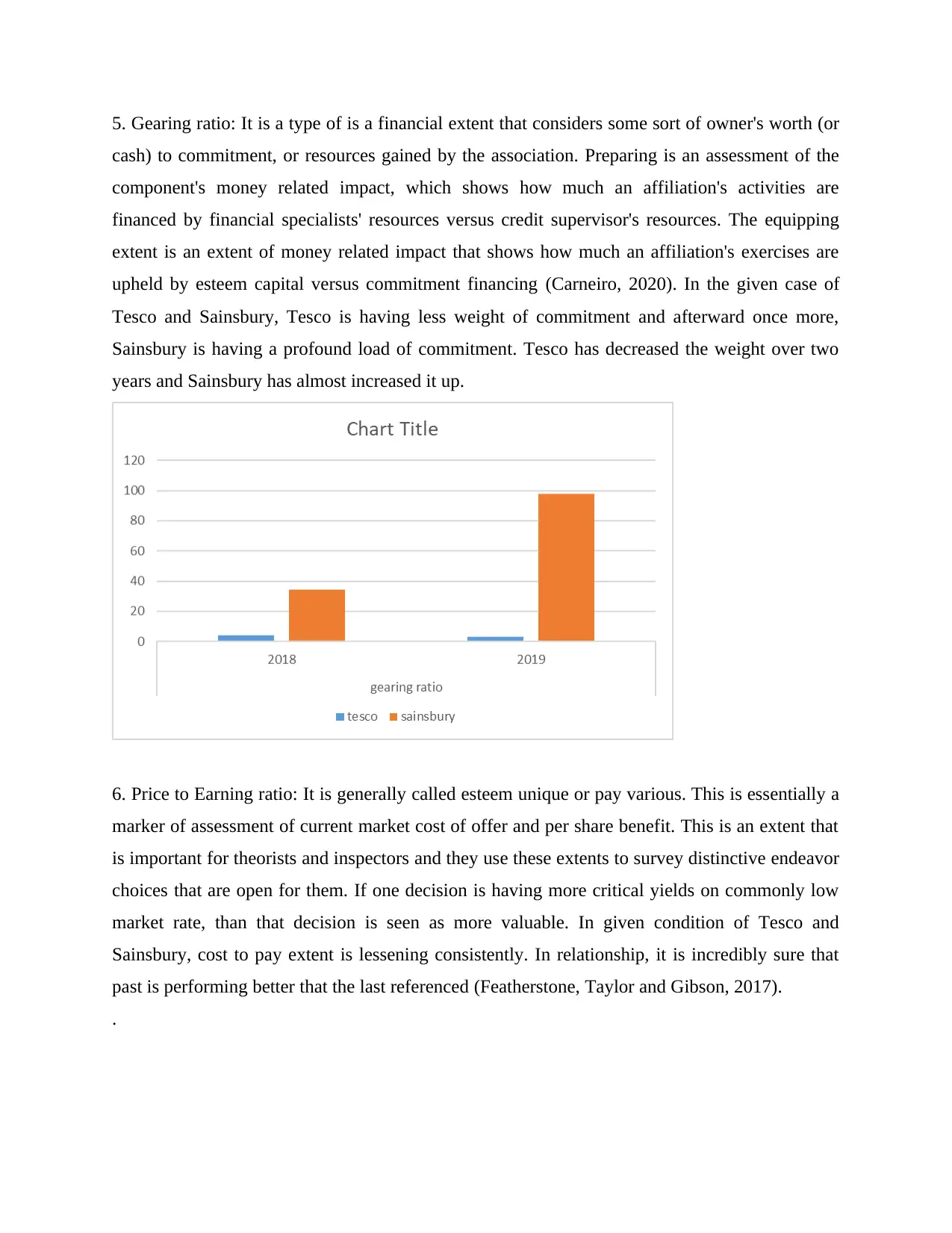

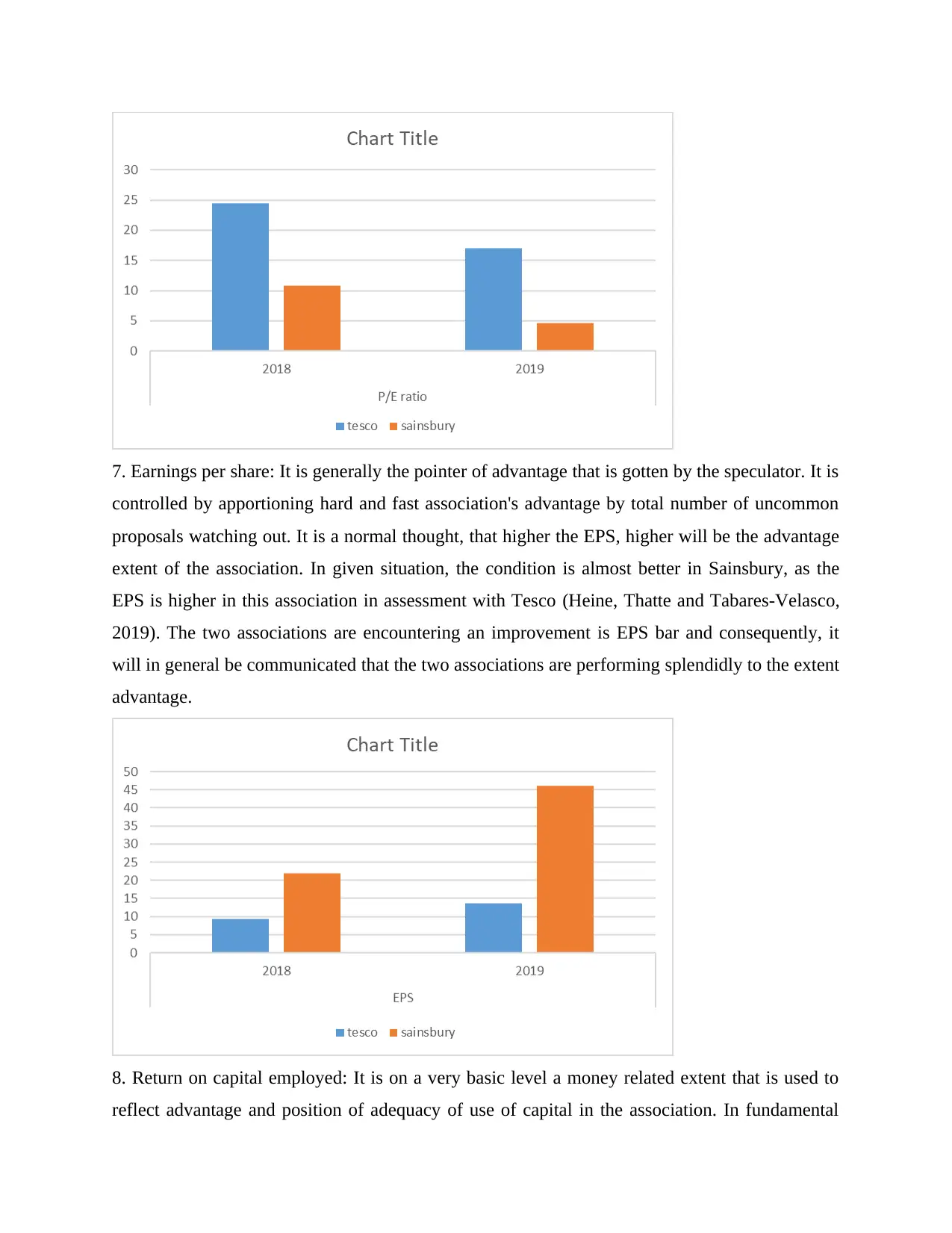

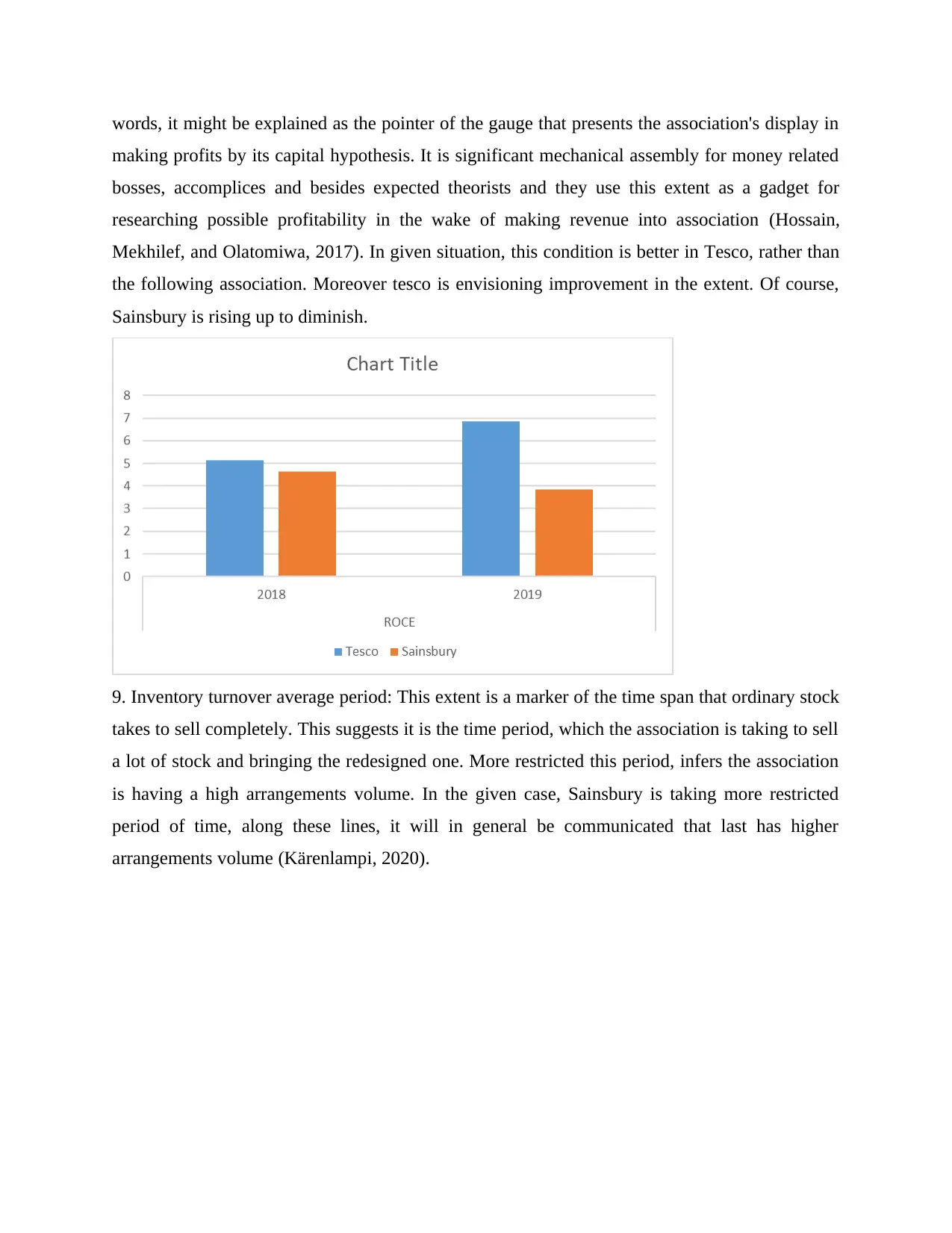

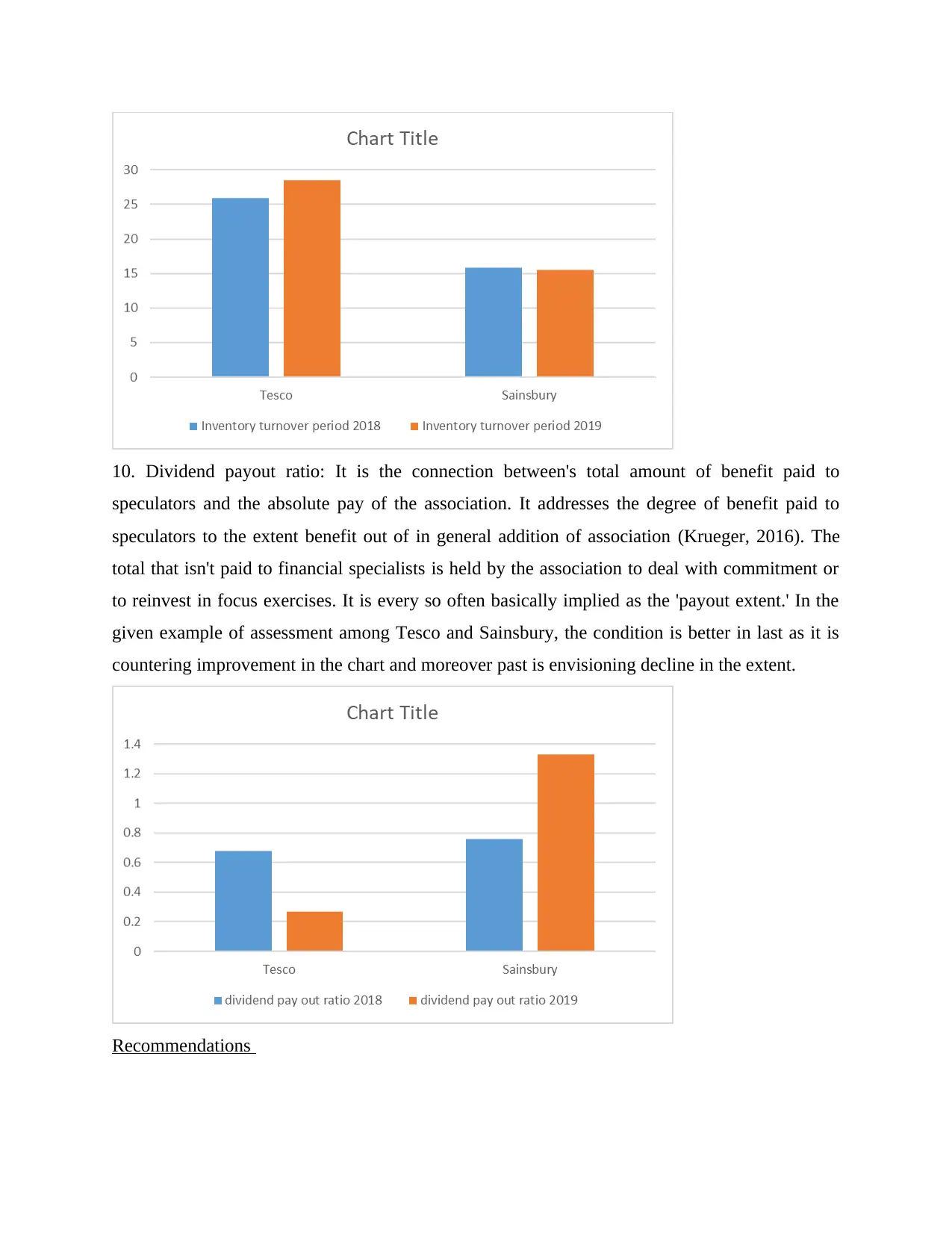

This report provides a comprehensive analysis of the financial performance of Tesco plc and Sainsbury's plc, focusing on ratio analysis and investment appraisal techniques. Portfolio 1 delves into the financial situations of both companies using ratio analysis, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, P/E ratio, earnings per share, return on capital employed, inventory turnover period, and dividend payout ratio. The analysis compares the performance of Tesco and Sainsbury's across these metrics, offering interpretations and recommendations for improvement. Portfolio 2 examines the significance of investment appraisal techniques in making informed financial decisions. The report highlights the limitations of relying solely on investment appraisal techniques for long-term decision-making. The report concludes with recommendations for improving financial performance and liquidity, emphasizing the importance of monitoring stock levels, reducing working expenses, and assessing market demand.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.