Business Finance: Working Capital, Sources & Investment Appraisal

VerifiedAdded on 2024/05/30

|13

|2842

|173

Report

AI Summary

This report provides a comprehensive analysis of key business finance concepts. It begins by examining the constituent parts of working capital—accounts receivable, accounts payable, and inventories—and justifies its importance for the long-term survival of a company. The report then assesses the suitability of various internal sources of finance, such as retained profits, sale of fixed assets, and sale of stock, for particular business needs. It also judges the appropriateness of external sources of finance, including the issue of shares, bank loans, and factoring. Furthermore, the report applies techniques of capital investment appraisal, including Net Present Value (NPV), Internal Rate of Return (IRR), and payback period, to a specific investment decision, using the example of XYZ Ltd. Finally, it demonstrates how to apply cost-benefit analysis to investment decisions, emphasizing the importance of evaluating costs and benefits to determine investment viability, with Desklib offering additional resources for students.

Business Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1 - Understand working capital...............................................................................................3

1.1 Analyze the constituent parts of working capital......................................................................3

1.2 Justify its importance for the long-term survival of a company................................................3

Task 2 - Understand the internal sources of finance available to a business...................................5

2.1 Assess the suitability of three different internal sources of finance for particular business

needs................................................................................................................................................5

Task 3 - Understand the external sources of finance available to a business..................................6

3.1 Judge the appropriateness of three different external sources of finance for particular business

needs................................................................................................................................................6

Task 4 - Understand financial capital investment appraisal............................................................7

4.1 Apply the techniques of capital investment appraisal to making a particular investment

decision............................................................................................................................................7

Task 5 - Know how to apply cost-benefit analysis to investment decisions.................................10

5.1 Apply the techniques of cost benefit analysis to making a particular investment decision.....10

Reference list.................................................................................................................................12

2

Task 1 - Understand working capital...............................................................................................3

1.1 Analyze the constituent parts of working capital......................................................................3

1.2 Justify its importance for the long-term survival of a company................................................3

Task 2 - Understand the internal sources of finance available to a business...................................5

2.1 Assess the suitability of three different internal sources of finance for particular business

needs................................................................................................................................................5

Task 3 - Understand the external sources of finance available to a business..................................6

3.1 Judge the appropriateness of three different external sources of finance for particular business

needs................................................................................................................................................6

Task 4 - Understand financial capital investment appraisal............................................................7

4.1 Apply the techniques of capital investment appraisal to making a particular investment

decision............................................................................................................................................7

Task 5 - Know how to apply cost-benefit analysis to investment decisions.................................10

5.1 Apply the techniques of cost benefit analysis to making a particular investment decision.....10

Reference list.................................................................................................................................12

2

Task 1 - Understand working capital

1.1 Analyze the constituent parts of working capital

The working capital refers to the financial metric, which is used for representing the operating

liquidity available to an organization (Banos-Caballero et al., 2014). The working capital of an

organization is derived from the difference between the current assets and current liabilities of an

organization. The current assets and current liabilities are the two major components of working

capital. According to Bhattacharya (2014), the further breaking down of the two components

indicate that working capital comprises of three main constituents, which are as follows -

Accounts receivable - The revenues of a company, which are due from its customers, are

known as accounts receivables or sundry debtors. The accounts receivable in a business is

a major part of the current assets of the business.

Accounts payable - Accounts payables (also known as sundry creditors) refer to the

money that a business is obligated to be paying out over a short period. This is a key

constituent of working capital, as these are the major current financial obligations of a

business.

Inventories - Inventories are the primary assets of a company, which a company converts

it into sales revenue. High inventories are good for working capital management.

However, extremely high inventory levels indicate inefficient and wasteful utilization of

working capital.

1.2 Justify its importance for the long-term survival of a company

Working capital management is an important part of every company. It helps a company in

different ways along with ensuring its long-term survival (Corelli, 2016). According to Sagner

(2014), the following points show the importance and the ways in which working capital and its

management helps a company in ensuring long-term survival -

Working capital helps in generating higher returns on capital

It helps in improving the credit profile as well as the solvency of an organization

3

1.1 Analyze the constituent parts of working capital

The working capital refers to the financial metric, which is used for representing the operating

liquidity available to an organization (Banos-Caballero et al., 2014). The working capital of an

organization is derived from the difference between the current assets and current liabilities of an

organization. The current assets and current liabilities are the two major components of working

capital. According to Bhattacharya (2014), the further breaking down of the two components

indicate that working capital comprises of three main constituents, which are as follows -

Accounts receivable - The revenues of a company, which are due from its customers, are

known as accounts receivables or sundry debtors. The accounts receivable in a business is

a major part of the current assets of the business.

Accounts payable - Accounts payables (also known as sundry creditors) refer to the

money that a business is obligated to be paying out over a short period. This is a key

constituent of working capital, as these are the major current financial obligations of a

business.

Inventories - Inventories are the primary assets of a company, which a company converts

it into sales revenue. High inventories are good for working capital management.

However, extremely high inventory levels indicate inefficient and wasteful utilization of

working capital.

1.2 Justify its importance for the long-term survival of a company

Working capital management is an important part of every company. It helps a company in

different ways along with ensuring its long-term survival (Corelli, 2016). According to Sagner

(2014), the following points show the importance and the ways in which working capital and its

management helps a company in ensuring long-term survival -

Working capital helps in generating higher returns on capital

It helps in improving the credit profile as well as the solvency of an organization

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps in leading to higher profitability of a business through effective management of

accounts receivables and payables

Working capital also helps in increasing the business value of a business through

generation of more free cash flows

It helps in creation of competitive advantage of a business

It ensures that a company has the ability of facing shocks and survive under peak

demands

Helps in continuing the production process uninterruptedly

Thus, in the above ways, working capital and effective working capital management helps a

business in surviving in the long run.

4

accounts receivables and payables

Working capital also helps in increasing the business value of a business through

generation of more free cash flows

It helps in creation of competitive advantage of a business

It ensures that a company has the ability of facing shocks and survive under peak

demands

Helps in continuing the production process uninterruptedly

Thus, in the above ways, working capital and effective working capital management helps a

business in surviving in the long run.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2 - Understand the internal sources of finance available to a business

2.1 Assess the suitability of three different internal sources of finance for particular

business needs

Sources of finance refer to the sources from which funds or money is derived for financing the

operations or the potential investments of an organization, which facilitates the organization to

meet its operational requirements such as purchase of material, payment of wages, etc. along

with facilitating it to undertake the projects or investment it desired to (Peirson et al., 2014).

According to Aliona (2017), financing also helps an organization in long-term expansion of

projects, such as investment on acquisition or merger. Sources of finance can be both internal

and external in nature. The three major internal sources of finance are as follows -

Retained profits - Retained profits refer to the amount of profit kept in an organization

after paying dividends to all the stockholders of the organization (Storey et al., 2016).

Retained profit acts as a major source of finance for every established and profitable

business. This internal source of finance can be used for funding additional growth of a

business related to areas such as capital expenditures, research and development

activities, working capital, acquisitions, marketing, etc. Sale of fixed or old assets - The sale of assets held in a business, which are no longer

required in the business in order to free up cash is also a good internal source for

generating finance (Fields, 2016). This source of finance helps in generating quick money

in a business, which can be used for satisfying different business needs such as purchase

of new assets, investment into new projects, etc. Sale of stock - The sale of old stock held in a business also helps in generating funds. The

stocks of a business are usually sold off at lower prices in order to generate funds through

sale (Fields, 2016). This method is also useful for generation of quick money, which can

be used for satisfying business needs such as purchase of new stock, production of new

goods and services, capital investment, etc.

5

2.1 Assess the suitability of three different internal sources of finance for particular

business needs

Sources of finance refer to the sources from which funds or money is derived for financing the

operations or the potential investments of an organization, which facilitates the organization to

meet its operational requirements such as purchase of material, payment of wages, etc. along

with facilitating it to undertake the projects or investment it desired to (Peirson et al., 2014).

According to Aliona (2017), financing also helps an organization in long-term expansion of

projects, such as investment on acquisition or merger. Sources of finance can be both internal

and external in nature. The three major internal sources of finance are as follows -

Retained profits - Retained profits refer to the amount of profit kept in an organization

after paying dividends to all the stockholders of the organization (Storey et al., 2016).

Retained profit acts as a major source of finance for every established and profitable

business. This internal source of finance can be used for funding additional growth of a

business related to areas such as capital expenditures, research and development

activities, working capital, acquisitions, marketing, etc. Sale of fixed or old assets - The sale of assets held in a business, which are no longer

required in the business in order to free up cash is also a good internal source for

generating finance (Fields, 2016). This source of finance helps in generating quick money

in a business, which can be used for satisfying different business needs such as purchase

of new assets, investment into new projects, etc. Sale of stock - The sale of old stock held in a business also helps in generating funds. The

stocks of a business are usually sold off at lower prices in order to generate funds through

sale (Fields, 2016). This method is also useful for generation of quick money, which can

be used for satisfying business needs such as purchase of new stock, production of new

goods and services, capital investment, etc.

5

Task 3 - Understand the external sources of finance available to a business

3.1 Judge the appropriateness of three different external sources of finance for particular

business needs.

Internal sources of finance are a good source for generating funds in an organization. However, it

is usually difficult to generate huge amount of funds from internal sources. In such a case, an

organization has to depend on external sources of finance. The external sources of finance refer

to the sources available in the external environment of an organization, which can be used for

generating funds (Storey et al., 2016). The following are the three different and most effective

external sources of finance for fulfilling the needs of a business -

Issue of shares - The issue of new equity shares of a company acts as a source of finance

for the company (Abor, 2017). The sale of equity shares of a business generates funds

from application, allotment and call of shares to shareholders. The benefit of issue of

shares is that there is no obligatory requirement of paying interests to shareholders.

However, the ownership of the company is transferred to the shareholders, which is the

major disadvantage of this source of finance. Bank loans - The loans taken from banks for a fixed term in exchange of fixed interest

payments also helps in generating funds. Bank loans are both cost effective and flexible

in nature (Qian and Yeung, 2015). However, in case if bank loans are used for generating

finance, the burden of interest payment remains in a company. Factoring - Factoring refers to a kind of debtor finance or financial transaction in which

companies sell off its accounts receivables (the invoices) to third parties (known as

factors) at a discounted rate (Michalski, 2014). The immediate and current needs of cash

in a company can be met with this source of finance.

6

3.1 Judge the appropriateness of three different external sources of finance for particular

business needs.

Internal sources of finance are a good source for generating funds in an organization. However, it

is usually difficult to generate huge amount of funds from internal sources. In such a case, an

organization has to depend on external sources of finance. The external sources of finance refer

to the sources available in the external environment of an organization, which can be used for

generating funds (Storey et al., 2016). The following are the three different and most effective

external sources of finance for fulfilling the needs of a business -

Issue of shares - The issue of new equity shares of a company acts as a source of finance

for the company (Abor, 2017). The sale of equity shares of a business generates funds

from application, allotment and call of shares to shareholders. The benefit of issue of

shares is that there is no obligatory requirement of paying interests to shareholders.

However, the ownership of the company is transferred to the shareholders, which is the

major disadvantage of this source of finance. Bank loans - The loans taken from banks for a fixed term in exchange of fixed interest

payments also helps in generating funds. Bank loans are both cost effective and flexible

in nature (Qian and Yeung, 2015). However, in case if bank loans are used for generating

finance, the burden of interest payment remains in a company. Factoring - Factoring refers to a kind of debtor finance or financial transaction in which

companies sell off its accounts receivables (the invoices) to third parties (known as

factors) at a discounted rate (Michalski, 2014). The immediate and current needs of cash

in a company can be met with this source of finance.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 4 - Understand financial capital investment appraisal

4.1 Apply the techniques of capital investment appraisal to making a particular investment

decision.

Capital investment appraisal is one of the most important aspects of making decisions on

investment (Gotze et al., 2015). This is because capital investment appraisal ensures that the

organization or business that is making the capital investment is benefitted from the investment.

According to Gotze et al. (2016), the techniques of capital investment appraisal helps a company

in making investment decisions through revealing the general feasibility of an investment and

evaluating the possible and beneficial alternatives.

Different capital investment techniques help in measuring feasibility of an investment in

different ways and from different aspects. For example, the NPV (Net Present Value) is one of

the most effectual techniques in capital investment appraisal, which determine the difference in

the present value of cash outflow and present value of cash inflow (Ben-Horin and Kroll, 2017).

The IRR (Internal Rate of Return) is another technique used in capital investment appraisal that

estimates the profitability of the potential investments of an organization with deriving a

discounting rate, which makes the NPV of cash flows zero (Brigham and Houston, 2015).

According to Lane and Rosewall (2015), the payback period is also an important investment

appraisal technique, which derives the time needed for any investment to recover the initial

outlays made by it in terms of savings and profits. These techniques of capital investment

appraisal can be applied for making a particular investment decision in the following manner -

XYZ Ltd. is a manufacturing company, which plans to invest into development of a new product.

The initial investment needed to develop the new product is £20 million, with a cost of capital of

12%. The cash inflows from the investment are £4 million, £6 million, £11 million, £17 million

and £22 million each year.

According to the above information, the following are the calculations of the feasibility of the

investment of the investment of XYZ Ltd -

NPV

7

4.1 Apply the techniques of capital investment appraisal to making a particular investment

decision.

Capital investment appraisal is one of the most important aspects of making decisions on

investment (Gotze et al., 2015). This is because capital investment appraisal ensures that the

organization or business that is making the capital investment is benefitted from the investment.

According to Gotze et al. (2016), the techniques of capital investment appraisal helps a company

in making investment decisions through revealing the general feasibility of an investment and

evaluating the possible and beneficial alternatives.

Different capital investment techniques help in measuring feasibility of an investment in

different ways and from different aspects. For example, the NPV (Net Present Value) is one of

the most effectual techniques in capital investment appraisal, which determine the difference in

the present value of cash outflow and present value of cash inflow (Ben-Horin and Kroll, 2017).

The IRR (Internal Rate of Return) is another technique used in capital investment appraisal that

estimates the profitability of the potential investments of an organization with deriving a

discounting rate, which makes the NPV of cash flows zero (Brigham and Houston, 2015).

According to Lane and Rosewall (2015), the payback period is also an important investment

appraisal technique, which derives the time needed for any investment to recover the initial

outlays made by it in terms of savings and profits. These techniques of capital investment

appraisal can be applied for making a particular investment decision in the following manner -

XYZ Ltd. is a manufacturing company, which plans to invest into development of a new product.

The initial investment needed to develop the new product is £20 million, with a cost of capital of

12%. The cash inflows from the investment are £4 million, £6 million, £11 million, £17 million

and £22 million each year.

According to the above information, the following are the calculations of the feasibility of the

investment of the investment of XYZ Ltd -

NPV

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount

Initial investment - £20 million

Year 1 £4 million

Year 2 £6 million

Year 3 £11 million

Year 4 £17 million

Year 5 £22 million

Cost of capital 12%

NPV £17.39 million

IRR

Particulars Amount

Initial investment - £20 million

Year 1 £4 million

Year 2 £6 million

Year 3 £11 million

Year 4 £17 million

Year 5 £22 million

Cost of capital 12%

IRR 37%

Payback Period

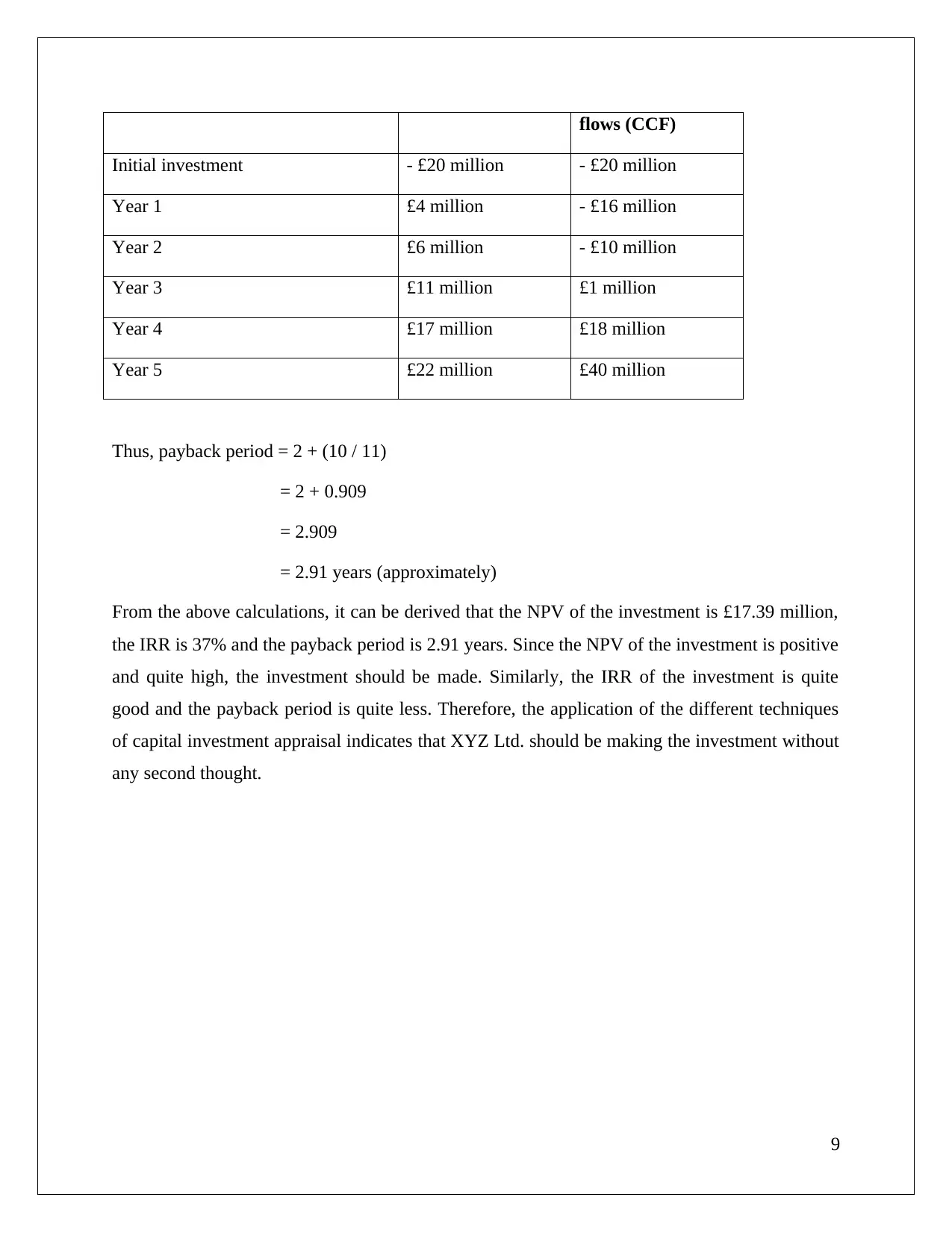

Particulars Cash flows (CF) Cumulative cash

8

Initial investment - £20 million

Year 1 £4 million

Year 2 £6 million

Year 3 £11 million

Year 4 £17 million

Year 5 £22 million

Cost of capital 12%

NPV £17.39 million

IRR

Particulars Amount

Initial investment - £20 million

Year 1 £4 million

Year 2 £6 million

Year 3 £11 million

Year 4 £17 million

Year 5 £22 million

Cost of capital 12%

IRR 37%

Payback Period

Particulars Cash flows (CF) Cumulative cash

8

flows (CCF)

Initial investment - £20 million - £20 million

Year 1 £4 million - £16 million

Year 2 £6 million - £10 million

Year 3 £11 million £1 million

Year 4 £17 million £18 million

Year 5 £22 million £40 million

Thus, payback period = 2 + (10 / 11)

= 2 + 0.909

= 2.909

= 2.91 years (approximately)

From the above calculations, it can be derived that the NPV of the investment is £17.39 million,

the IRR is 37% and the payback period is 2.91 years. Since the NPV of the investment is positive

and quite high, the investment should be made. Similarly, the IRR of the investment is quite

good and the payback period is quite less. Therefore, the application of the different techniques

of capital investment appraisal indicates that XYZ Ltd. should be making the investment without

any second thought.

9

Initial investment - £20 million - £20 million

Year 1 £4 million - £16 million

Year 2 £6 million - £10 million

Year 3 £11 million £1 million

Year 4 £17 million £18 million

Year 5 £22 million £40 million

Thus, payback period = 2 + (10 / 11)

= 2 + 0.909

= 2.909

= 2.91 years (approximately)

From the above calculations, it can be derived that the NPV of the investment is £17.39 million,

the IRR is 37% and the payback period is 2.91 years. Since the NPV of the investment is positive

and quite high, the investment should be made. Similarly, the IRR of the investment is quite

good and the payback period is quite less. Therefore, the application of the different techniques

of capital investment appraisal indicates that XYZ Ltd. should be making the investment without

any second thought.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 5 - Know how to apply cost-benefit analysis to investment decisions

5.1 Apply the techniques of cost benefit analysis to making a particular investment

decision.

The cost benefit analysis is another effective technique that helps in making investment

decisions. The cost benefit analysis, also known as the CBAM, refers to an analytical framework

that helps in the assessment of the costs as well as the benefits of different policy proposals and

investments (Boardman et al., 2017). The method focuses on economic efficiency through the

computation of the net benefits derived from each investment. According to Reniers and Van Erp

(2016), the evaluation of the benefits from a potential investment and comparison of the benefits

with the costs spent on it helps in making decisions on investment.

The cost benefit analysis of a particular investment can be conducted with the help of the

computation of the cost to benefit ratio of the investment (Josselin and Le Maux, 2017). This

technique of cost benefit analysis evaluates both the costs required to be spent for an investment

and the benefits that can be derived from the investment, followed by a comparison of the two.

In case if this ratio is greater than one, it is an indication that the investment is viable in nature.

The application of the technique of cost benefit analysis for making a particular investment can

be derived from the example of the potential investment of the XYZ Ltd. The cost benefit

analysis of the investment of XYZ Ltd. is as follows -

Cost = £ 20 million

Benefits = £4 million + £6 million + £11 million + £17 million + £22 million

= £60 million

Hence, cost to benefit ratio = Total benefits / Total costs

= £60 million / £20 million

= 3

10

5.1 Apply the techniques of cost benefit analysis to making a particular investment

decision.

The cost benefit analysis is another effective technique that helps in making investment

decisions. The cost benefit analysis, also known as the CBAM, refers to an analytical framework

that helps in the assessment of the costs as well as the benefits of different policy proposals and

investments (Boardman et al., 2017). The method focuses on economic efficiency through the

computation of the net benefits derived from each investment. According to Reniers and Van Erp

(2016), the evaluation of the benefits from a potential investment and comparison of the benefits

with the costs spent on it helps in making decisions on investment.

The cost benefit analysis of a particular investment can be conducted with the help of the

computation of the cost to benefit ratio of the investment (Josselin and Le Maux, 2017). This

technique of cost benefit analysis evaluates both the costs required to be spent for an investment

and the benefits that can be derived from the investment, followed by a comparison of the two.

In case if this ratio is greater than one, it is an indication that the investment is viable in nature.

The application of the technique of cost benefit analysis for making a particular investment can

be derived from the example of the potential investment of the XYZ Ltd. The cost benefit

analysis of the investment of XYZ Ltd. is as follows -

Cost = £ 20 million

Benefits = £4 million + £6 million + £11 million + £17 million + £22 million

= £60 million

Hence, cost to benefit ratio = Total benefits / Total costs

= £60 million / £20 million

= 3

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above calculation of the cost to benefit ratio of XYZ Ltd. is 3.0, which is greater than 1.0.

Therefore, since the cost to benefit ratio of the investment of XYZ Ltd. is more than 1.0, the

decision can be made by the company to make the investment. In this manner, the techniques of

cost benefit analysis can be used in order to make decisions on a particular investment.

11

Therefore, since the cost to benefit ratio of the investment of XYZ Ltd. is more than 1.0, the

decision can be made by the company to make the investment. In this manner, the techniques of

cost benefit analysis can be used in order to make decisions on a particular investment.

11

Reference list

Abor, J.Y., 2017. Venture Capital Finance. In Entrepreneurial Finance for MSMEs (pp. 87-105).

Palgrave Macmillan, Cham.

Aliona, L., 2017. Improvement of financing sources’ management for dwelling. Development.

Banos-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Ben-Horin, M. and Kroll, Y., 2017. A simple intuitive NPV-IRR consistent ranking. The

Quarterly Review of Economics and Finance, 66, pp.108-114.

Bhattacharya, H., 2014. Working capital management: Strategies and techniques. PHI Learning

Pvt. Ltd..

Boardman, A.E., Greenberg, D.H., Vining, A.R. and Weimer, D.L., 2017. Cost-benefit analysis:

concepts and practice. Cambridge University Press.

Brigham, E.F. and Houston, J.F., 2015. Fundamentals of Financial Management Concise 8E.

Corelli, A., 2016. Working Capital Management. In Analytical Corporate Finance (pp. 351-

378). Springer, Cham.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers.

AMACOM Div American Mgmt Assn.

Gotze, U., Northcott, D. and Schuster, P., 2015. Selected Further Applications of Investment

Appraisal Methods. In Investment Appraisal (pp. 105-159). Springer, Berlin, Heidelberg.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

Josselin, J.M. and Le Maux, B., 2017. Cost Benefit Analysis. In Statistical Tools for Program

Evaluation (pp. 291-324). Springer, Cham.

12

Abor, J.Y., 2017. Venture Capital Finance. In Entrepreneurial Finance for MSMEs (pp. 87-105).

Palgrave Macmillan, Cham.

Aliona, L., 2017. Improvement of financing sources’ management for dwelling. Development.

Banos-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Ben-Horin, M. and Kroll, Y., 2017. A simple intuitive NPV-IRR consistent ranking. The

Quarterly Review of Economics and Finance, 66, pp.108-114.

Bhattacharya, H., 2014. Working capital management: Strategies and techniques. PHI Learning

Pvt. Ltd..

Boardman, A.E., Greenberg, D.H., Vining, A.R. and Weimer, D.L., 2017. Cost-benefit analysis:

concepts and practice. Cambridge University Press.

Brigham, E.F. and Houston, J.F., 2015. Fundamentals of Financial Management Concise 8E.

Corelli, A., 2016. Working Capital Management. In Analytical Corporate Finance (pp. 351-

378). Springer, Cham.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers.

AMACOM Div American Mgmt Assn.

Gotze, U., Northcott, D. and Schuster, P., 2015. Selected Further Applications of Investment

Appraisal Methods. In Investment Appraisal (pp. 105-159). Springer, Berlin, Heidelberg.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

Josselin, J.M. and Le Maux, B., 2017. Cost Benefit Analysis. In Statistical Tools for Program

Evaluation (pp. 291-324). Springer, Cham.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.