Comprehensive Finance Assignment Solution: Analysis and Calculations

VerifiedAdded on 2020/03/16

|11

|1640

|128

Homework Assignment

AI Summary

This finance assignment solution provides detailed calculations and analysis for various financial concepts. It includes the calculation of Weighted Average Cost of Capital (WACC) for different divisions, forecasting of Free Cash Flow (FCF) without expansion, and present value calculations. The solution also covers the impact of expansion on Net Present Value (NPV), value of abandonment, and economic depreciation. Furthermore, it addresses shareholders' concerns regarding Earnings per Share (EPS) and dividend per share, discusses the impact of long-term incentives and provides recommendations on dividend policies. The assignment analyzes financial statements, investment strategies, and provides insights into capital budgeting decisions.

Running Head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Answer 1:.........................................................................................................................................2

Answer 2:.........................................................................................................................................2

Answer 3:.........................................................................................................................................2

Answer 4:.........................................................................................................................................2

Answer 5:.........................................................................................................................................3

Answer 6:.........................................................................................................................................5

Answer 7:.........................................................................................................................................5

Answer 8:.........................................................................................................................................6

Answer 9:.........................................................................................................................................6

Answer 10:.......................................................................................................................................6

Answer 11:.......................................................................................................................................7

Answer 12:.......................................................................................................................................7

Answer 13:.......................................................................................................................................7

Answer 14:.......................................................................................................................................7

Answer 15:.......................................................................................................................................8

Answer 16:.......................................................................................................................................8

Answer 17:.......................................................................................................................................8

References:......................................................................................................................................9

Table of Contents

Answer 1:.........................................................................................................................................2

Answer 2:.........................................................................................................................................2

Answer 3:.........................................................................................................................................2

Answer 4:.........................................................................................................................................2

Answer 5:.........................................................................................................................................3

Answer 6:.........................................................................................................................................5

Answer 7:.........................................................................................................................................5

Answer 8:.........................................................................................................................................6

Answer 9:.........................................................................................................................................6

Answer 10:.......................................................................................................................................6

Answer 11:.......................................................................................................................................7

Answer 12:.......................................................................................................................................7

Answer 13:.......................................................................................................................................7

Answer 14:.......................................................................................................................................7

Answer 15:.......................................................................................................................................8

Answer 16:.......................................................................................................................................8

Answer 17:.......................................................................................................................................8

References:......................................................................................................................................9

2FINANCE

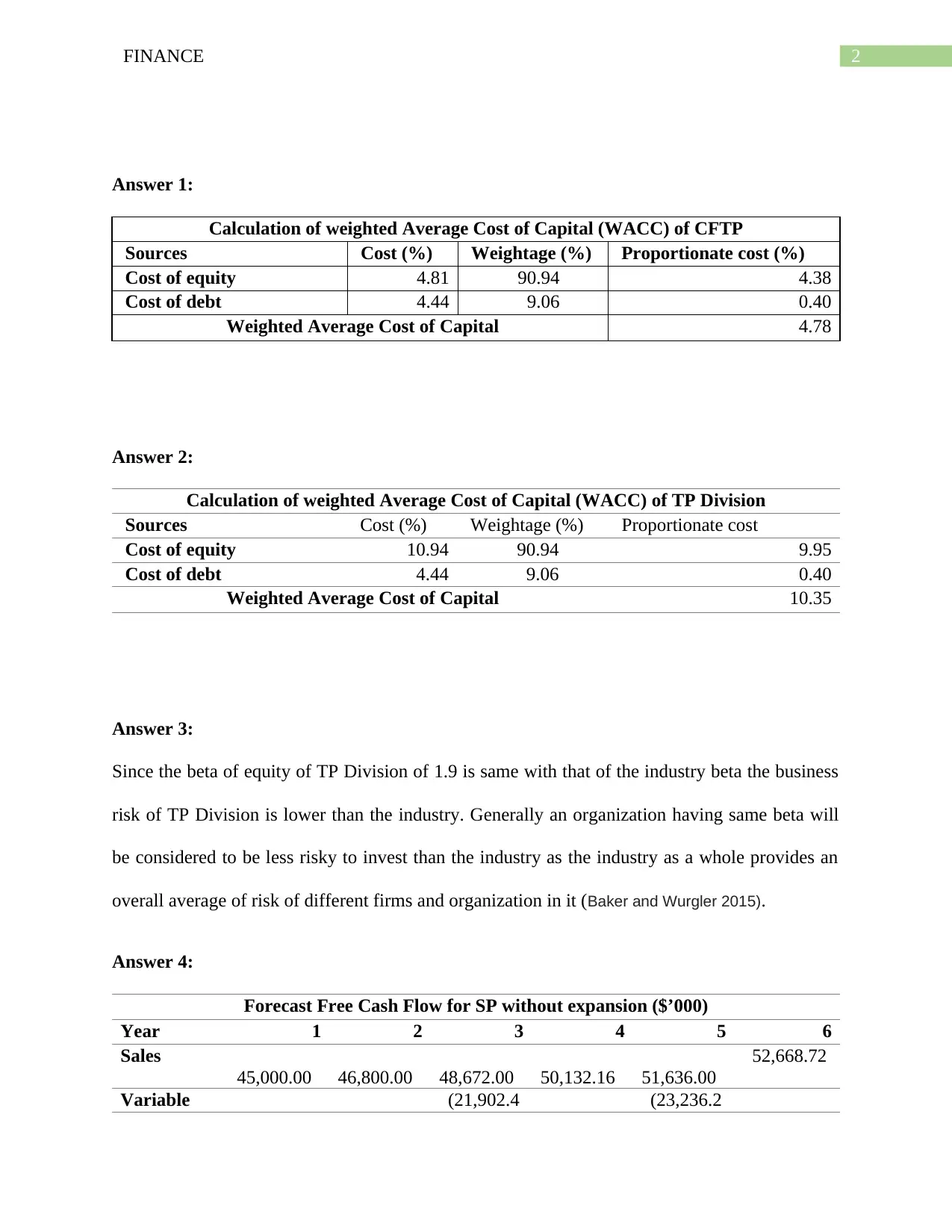

Answer 1:

Calculation of weighted Average Cost of Capital (WACC) of CFTP

Sources Cost (%) Weightage (%) Proportionate cost (%)

Cost of equity 4.81 90.94 4.38

Cost of debt 4.44 9.06 0.40

Weighted Average Cost of Capital 4.78

Answer 2:

Calculation of weighted Average Cost of Capital (WACC) of TP Division

Sources Cost (%) Weightage (%) Proportionate cost

Cost of equity 10.94 90.94 9.95

Cost of debt 4.44 9.06 0.40

Weighted Average Cost of Capital 10.35

Answer 3:

Since the beta of equity of TP Division of 1.9 is same with that of the industry beta the business

risk of TP Division is lower than the industry. Generally an organization having same beta will

be considered to be less risky to invest than the industry as the industry as a whole provides an

overall average of risk of different firms and organization in it (Baker and Wurgler 2015).

Answer 4:

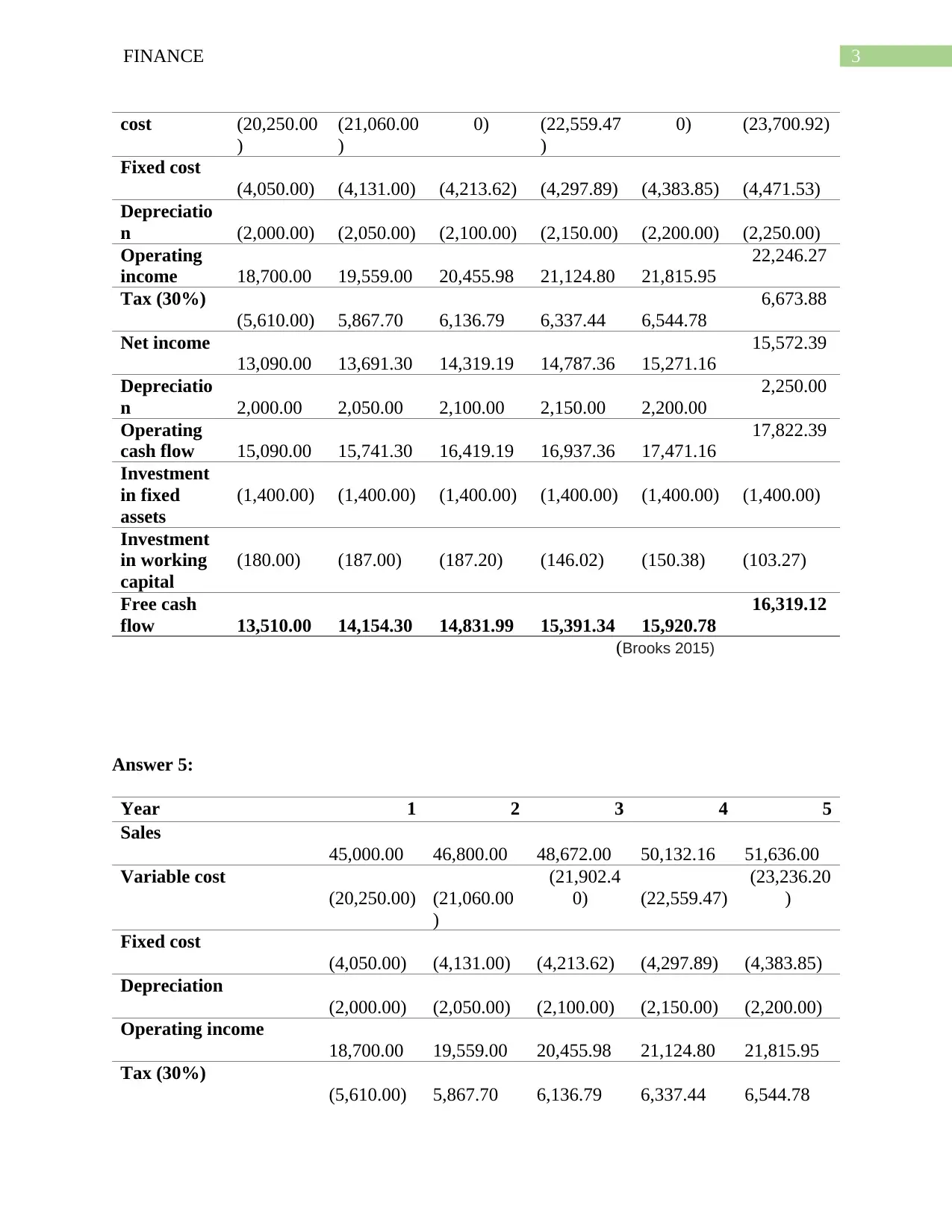

Forecast Free Cash Flow for SP without expansion ($’000)

Year 1 2 3 4 5 6

Sales

45,000.00 46,800.00 48,672.00 50,132.16 51,636.00

52,668.72

Variable (21,902.4 (23,236.2

Answer 1:

Calculation of weighted Average Cost of Capital (WACC) of CFTP

Sources Cost (%) Weightage (%) Proportionate cost (%)

Cost of equity 4.81 90.94 4.38

Cost of debt 4.44 9.06 0.40

Weighted Average Cost of Capital 4.78

Answer 2:

Calculation of weighted Average Cost of Capital (WACC) of TP Division

Sources Cost (%) Weightage (%) Proportionate cost

Cost of equity 10.94 90.94 9.95

Cost of debt 4.44 9.06 0.40

Weighted Average Cost of Capital 10.35

Answer 3:

Since the beta of equity of TP Division of 1.9 is same with that of the industry beta the business

risk of TP Division is lower than the industry. Generally an organization having same beta will

be considered to be less risky to invest than the industry as the industry as a whole provides an

overall average of risk of different firms and organization in it (Baker and Wurgler 2015).

Answer 4:

Forecast Free Cash Flow for SP without expansion ($’000)

Year 1 2 3 4 5 6

Sales

45,000.00 46,800.00 48,672.00 50,132.16 51,636.00

52,668.72

Variable (21,902.4 (23,236.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

cost (20,250.00

)

(21,060.00

)

0) (22,559.47

)

0) (23,700.92)

Fixed cost

(4,050.00) (4,131.00) (4,213.62) (4,297.89) (4,383.85) (4,471.53)

Depreciatio

n (2,000.00) (2,050.00) (2,100.00) (2,150.00) (2,200.00) (2,250.00)

Operating

income 18,700.00 19,559.00 20,455.98 21,124.80 21,815.95

22,246.27

Tax (30%)

(5,610.00) 5,867.70 6,136.79 6,337.44 6,544.78

6,673.88

Net income

13,090.00 13,691.30 14,319.19 14,787.36 15,271.16

15,572.39

Depreciatio

n 2,000.00 2,050.00 2,100.00 2,150.00 2,200.00

2,250.00

Operating

cash flow 15,090.00 15,741.30 16,419.19 16,937.36 17,471.16

17,822.39

Investment

in fixed

assets

(1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00)

Investment

in working

capital

(180.00) (187.00) (187.20) (146.02) (150.38) (103.27)

Free cash

flow 13,510.00 14,154.30 14,831.99 15,391.34 15,920.78

16,319.12

(Brooks 2015)

Answer 5:

Year 1 2 3 4 5

Sales

45,000.00 46,800.00 48,672.00 50,132.16 51,636.00

Variable cost

(20,250.00) (21,060.00

)

(21,902.4

0) (22,559.47)

(23,236.20

)

Fixed cost

(4,050.00) (4,131.00) (4,213.62) (4,297.89) (4,383.85)

Depreciation

(2,000.00) (2,050.00) (2,100.00) (2,150.00) (2,200.00)

Operating income

18,700.00 19,559.00 20,455.98 21,124.80 21,815.95

Tax (30%)

(5,610.00) 5,867.70 6,136.79 6,337.44 6,544.78

cost (20,250.00

)

(21,060.00

)

0) (22,559.47

)

0) (23,700.92)

Fixed cost

(4,050.00) (4,131.00) (4,213.62) (4,297.89) (4,383.85) (4,471.53)

Depreciatio

n (2,000.00) (2,050.00) (2,100.00) (2,150.00) (2,200.00) (2,250.00)

Operating

income 18,700.00 19,559.00 20,455.98 21,124.80 21,815.95

22,246.27

Tax (30%)

(5,610.00) 5,867.70 6,136.79 6,337.44 6,544.78

6,673.88

Net income

13,090.00 13,691.30 14,319.19 14,787.36 15,271.16

15,572.39

Depreciatio

n 2,000.00 2,050.00 2,100.00 2,150.00 2,200.00

2,250.00

Operating

cash flow 15,090.00 15,741.30 16,419.19 16,937.36 17,471.16

17,822.39

Investment

in fixed

assets

(1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00)

Investment

in working

capital

(180.00) (187.00) (187.20) (146.02) (150.38) (103.27)

Free cash

flow 13,510.00 14,154.30 14,831.99 15,391.34 15,920.78

16,319.12

(Brooks 2015)

Answer 5:

Year 1 2 3 4 5

Sales

45,000.00 46,800.00 48,672.00 50,132.16 51,636.00

Variable cost

(20,250.00) (21,060.00

)

(21,902.4

0) (22,559.47)

(23,236.20

)

Fixed cost

(4,050.00) (4,131.00) (4,213.62) (4,297.89) (4,383.85)

Depreciation

(2,000.00) (2,050.00) (2,100.00) (2,150.00) (2,200.00)

Operating income

18,700.00 19,559.00 20,455.98 21,124.80 21,815.95

Tax (30%)

(5,610.00) 5,867.70 6,136.79 6,337.44 6,544.78

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

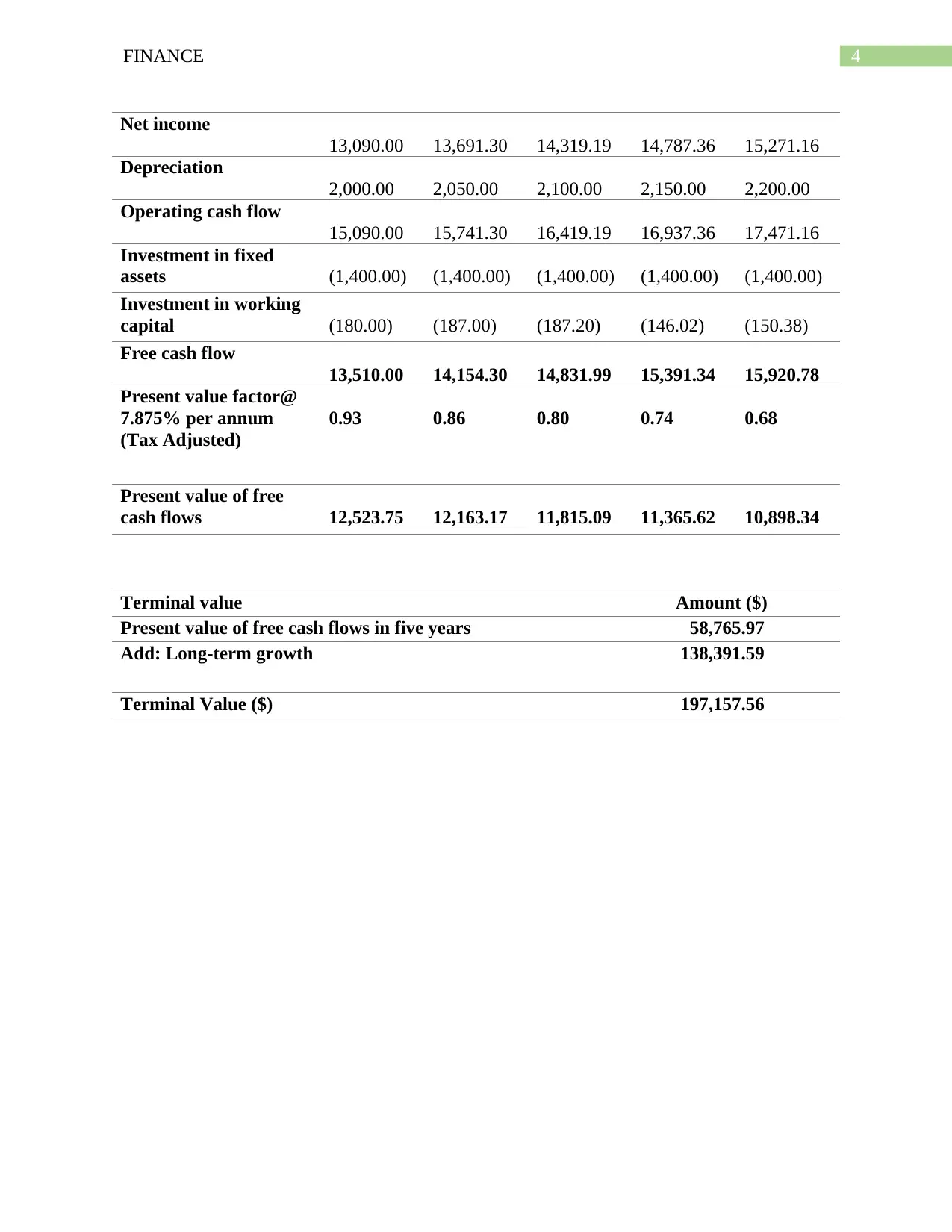

Net income

13,090.00 13,691.30 14,319.19 14,787.36 15,271.16

Depreciation

2,000.00 2,050.00 2,100.00 2,150.00 2,200.00

Operating cash flow

15,090.00 15,741.30 16,419.19 16,937.36 17,471.16

Investment in fixed

assets (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00)

Investment in working

capital (180.00) (187.00) (187.20) (146.02) (150.38)

Free cash flow

13,510.00 14,154.30 14,831.99 15,391.34 15,920.78

Present value factor@

7.875% per annum

(Tax Adjusted)

0.93 0.86 0.80 0.74 0.68

Present value of free

cash flows 12,523.75 12,163.17 11,815.09 11,365.62 10,898.34

Terminal value Amount ($)

Present value of free cash flows in five years 58,765.97

Add: Long-term growth 138,391.59

Terminal Value ($) 197,157.56

Net income

13,090.00 13,691.30 14,319.19 14,787.36 15,271.16

Depreciation

2,000.00 2,050.00 2,100.00 2,150.00 2,200.00

Operating cash flow

15,090.00 15,741.30 16,419.19 16,937.36 17,471.16

Investment in fixed

assets (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00)

Investment in working

capital (180.00) (187.00) (187.20) (146.02) (150.38)

Free cash flow

13,510.00 14,154.30 14,831.99 15,391.34 15,920.78

Present value factor@

7.875% per annum

(Tax Adjusted)

0.93 0.86 0.80 0.74 0.68

Present value of free

cash flows 12,523.75 12,163.17 11,815.09 11,365.62 10,898.34

Terminal value Amount ($)

Present value of free cash flows in five years 58,765.97

Add: Long-term growth 138,391.59

Terminal Value ($) 197,157.56

5FINANCE

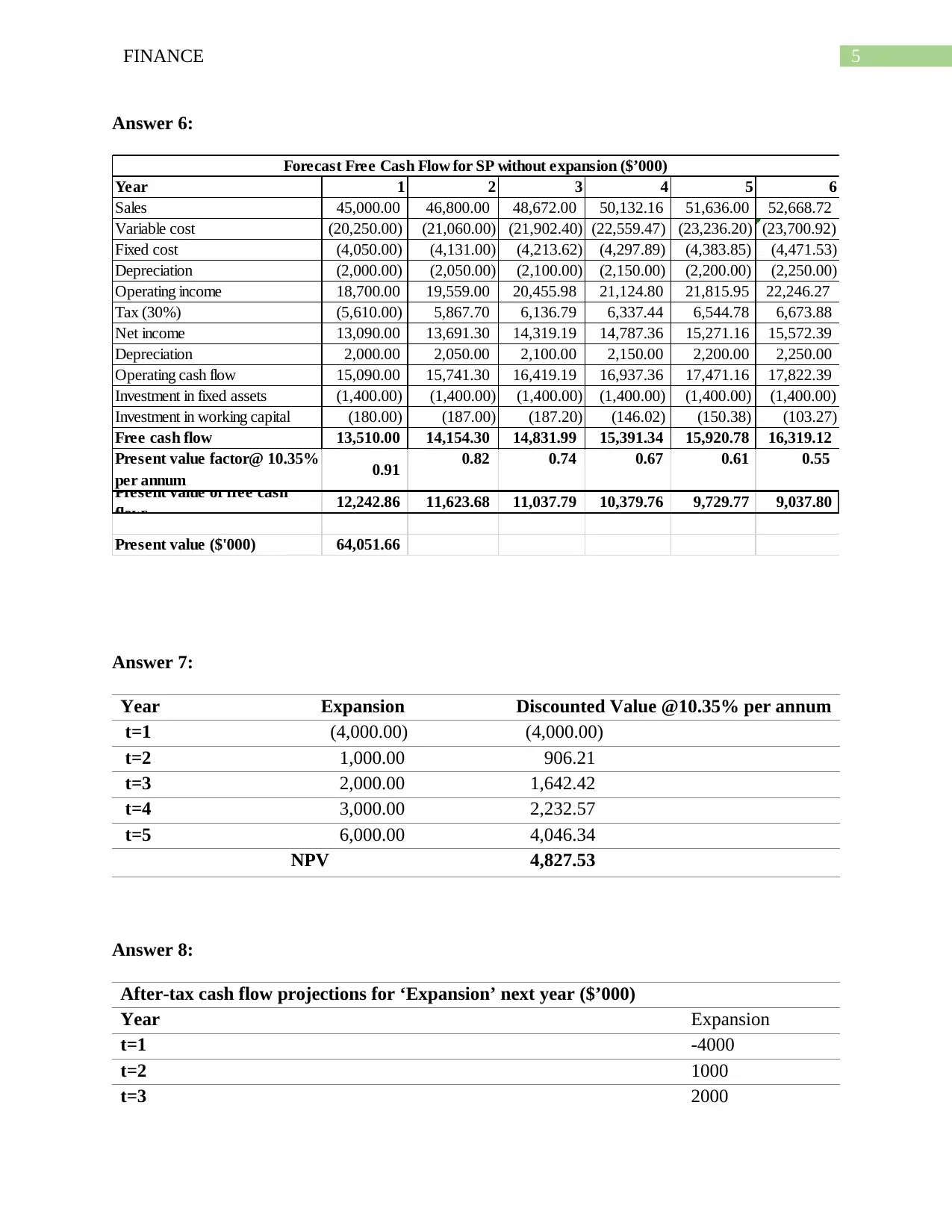

Answer 6:

Year 1 2 3 4 5 6

Sales 45,000.00 46,800.00 48,672.00 50,132.16 51,636.00 52,668.72

Variable cost (20,250.00) (21,060.00) (21,902.40) (22,559.47) (23,236.20) (23,700.92)

Fixed cost (4,050.00) (4,131.00) (4,213.62) (4,297.89) (4,383.85) (4,471.53)

Depreciation (2,000.00) (2,050.00) (2,100.00) (2,150.00) (2,200.00) (2,250.00)

Operating income 18,700.00 19,559.00 20,455.98 21,124.80 21,815.95 22,246.27

Tax (30%) (5,610.00) 5,867.70 6,136.79 6,337.44 6,544.78 6,673.88

Net income 13,090.00 13,691.30 14,319.19 14,787.36 15,271.16 15,572.39

Depreciation 2,000.00 2,050.00 2,100.00 2,150.00 2,200.00 2,250.00

Operating cash flow 15,090.00 15,741.30 16,419.19 16,937.36 17,471.16 17,822.39

Investment in fixed assets (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00)

Investment in working capital (180.00) (187.00) (187.20) (146.02) (150.38) (103.27)

Free cash flow 13,510.00 14,154.30 14,831.99 15,391.34 15,920.78 16,319.12

Present value factor@ 10.35%

per annum 0.91 0.82 0.74 0.67 0.61 0.55

Present value of free cash

flows 12,242.86 11,623.68 11,037.79 10,379.76 9,729.77 9,037.80

Present value ($'000) 64,051.66

Forecast Free Cash Flow for SP without expansion ($’000)

Answer 7:

Year Expansion Discounted Value @10.35% per annum

t=1 (4,000.00) (4,000.00)

t=2 1,000.00 906.21

t=3 2,000.00 1,642.42

t=4 3,000.00 2,232.57

t=5 6,000.00 4,046.34

NPV 4,827.53

Answer 8:

After-tax cash flow projections for ‘Expansion’ next year ($’000)

Year Expansion

t=1 -4000

t=2 1000

t=3 2000

Answer 6:

Year 1 2 3 4 5 6

Sales 45,000.00 46,800.00 48,672.00 50,132.16 51,636.00 52,668.72

Variable cost (20,250.00) (21,060.00) (21,902.40) (22,559.47) (23,236.20) (23,700.92)

Fixed cost (4,050.00) (4,131.00) (4,213.62) (4,297.89) (4,383.85) (4,471.53)

Depreciation (2,000.00) (2,050.00) (2,100.00) (2,150.00) (2,200.00) (2,250.00)

Operating income 18,700.00 19,559.00 20,455.98 21,124.80 21,815.95 22,246.27

Tax (30%) (5,610.00) 5,867.70 6,136.79 6,337.44 6,544.78 6,673.88

Net income 13,090.00 13,691.30 14,319.19 14,787.36 15,271.16 15,572.39

Depreciation 2,000.00 2,050.00 2,100.00 2,150.00 2,200.00 2,250.00

Operating cash flow 15,090.00 15,741.30 16,419.19 16,937.36 17,471.16 17,822.39

Investment in fixed assets (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00) (1,400.00)

Investment in working capital (180.00) (187.00) (187.20) (146.02) (150.38) (103.27)

Free cash flow 13,510.00 14,154.30 14,831.99 15,391.34 15,920.78 16,319.12

Present value factor@ 10.35%

per annum 0.91 0.82 0.74 0.67 0.61 0.55

Present value of free cash

flows 12,242.86 11,623.68 11,037.79 10,379.76 9,729.77 9,037.80

Present value ($'000) 64,051.66

Forecast Free Cash Flow for SP without expansion ($’000)

Answer 7:

Year Expansion Discounted Value @10.35% per annum

t=1 (4,000.00) (4,000.00)

t=2 1,000.00 906.21

t=3 2,000.00 1,642.42

t=4 3,000.00 2,232.57

t=5 6,000.00 4,046.34

NPV 4,827.53

Answer 8:

After-tax cash flow projections for ‘Expansion’ next year ($’000)

Year Expansion

t=1 -4000

t=2 1000

t=3 2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

t=4 3000

t=5 6000

Value of the option at year 0 8000

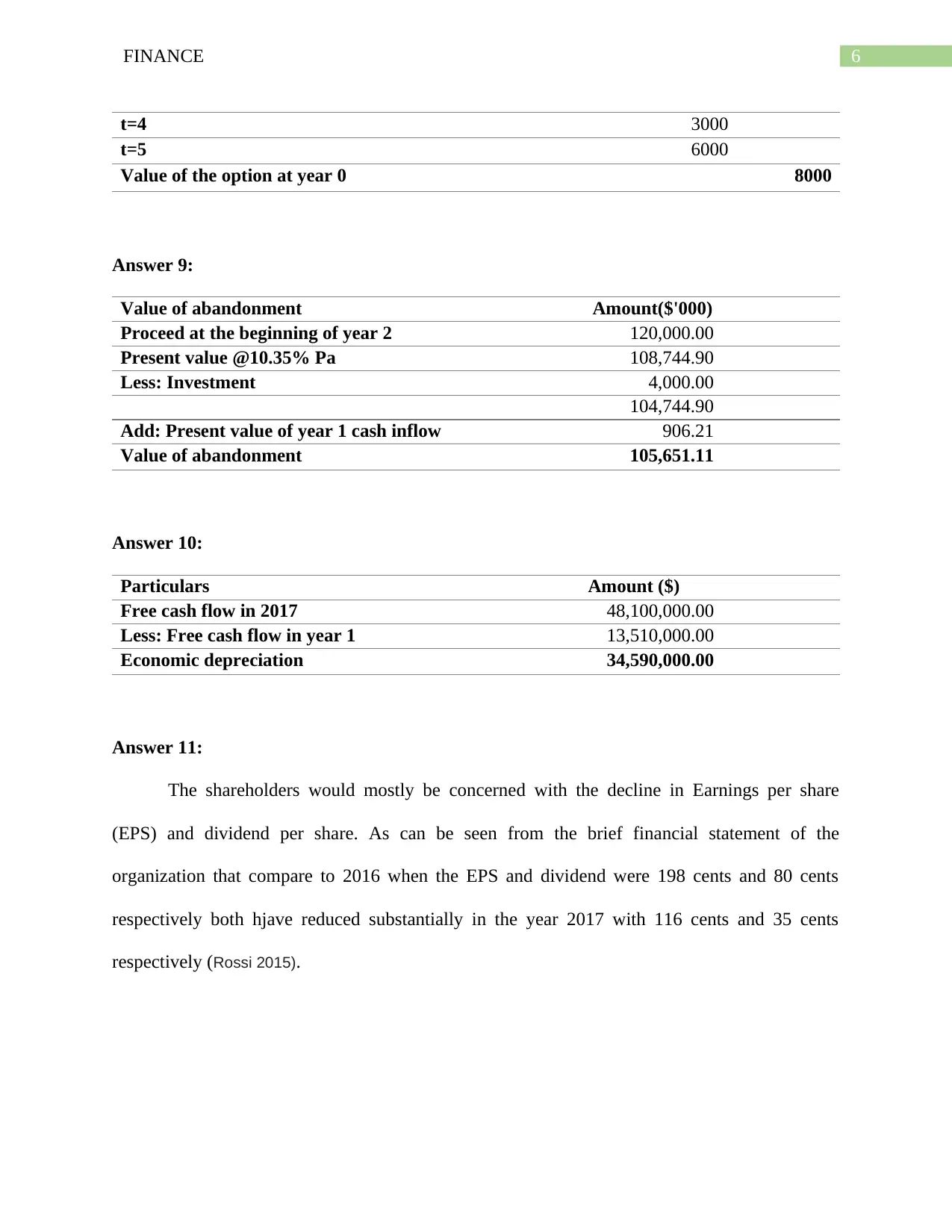

Answer 9:

Value of abandonment Amount($'000)

Proceed at the beginning of year 2 120,000.00

Present value @10.35% Pa 108,744.90

Less: Investment 4,000.00

104,744.90

Add: Present value of year 1 cash inflow 906.21

Value of abandonment 105,651.11

Answer 10:

Particulars Amount ($)

Free cash flow in 2017 48,100,000.00

Less: Free cash flow in year 1 13,510,000.00

Economic depreciation 34,590,000.00

Answer 11:

The shareholders would mostly be concerned with the decline in Earnings per share

(EPS) and dividend per share. As can be seen from the brief financial statement of the

organization that compare to 2016 when the EPS and dividend were 198 cents and 80 cents

respectively both hjave reduced substantially in the year 2017 with 116 cents and 35 cents

respectively (Rossi 2015).

t=4 3000

t=5 6000

Value of the option at year 0 8000

Answer 9:

Value of abandonment Amount($'000)

Proceed at the beginning of year 2 120,000.00

Present value @10.35% Pa 108,744.90

Less: Investment 4,000.00

104,744.90

Add: Present value of year 1 cash inflow 906.21

Value of abandonment 105,651.11

Answer 10:

Particulars Amount ($)

Free cash flow in 2017 48,100,000.00

Less: Free cash flow in year 1 13,510,000.00

Economic depreciation 34,590,000.00

Answer 11:

The shareholders would mostly be concerned with the decline in Earnings per share

(EPS) and dividend per share. As can be seen from the brief financial statement of the

organization that compare to 2016 when the EPS and dividend were 198 cents and 80 cents

respectively both hjave reduced substantially in the year 2017 with 116 cents and 35 cents

respectively (Rossi 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

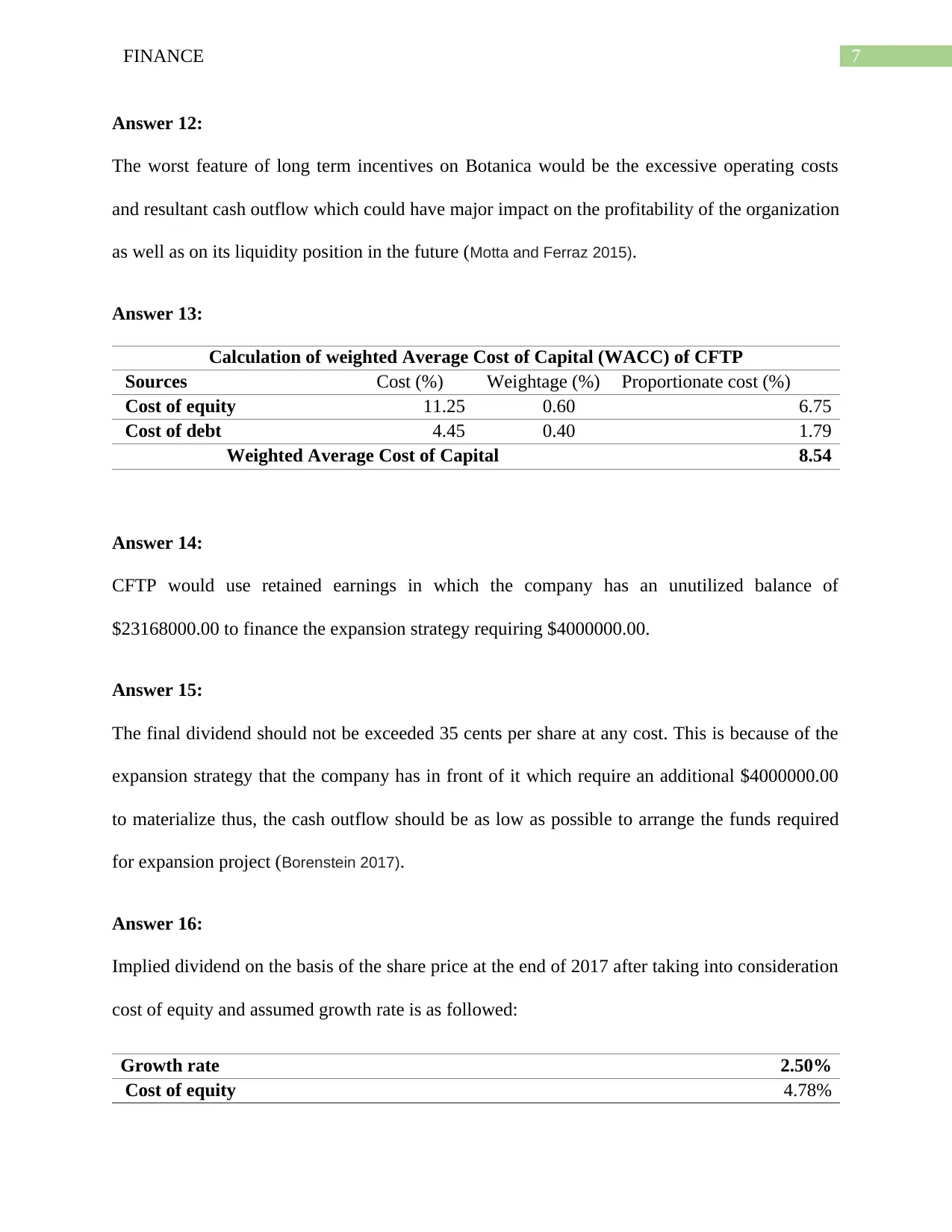

Answer 12:

The worst feature of long term incentives on Botanica would be the excessive operating costs

and resultant cash outflow which could have major impact on the profitability of the organization

as well as on its liquidity position in the future (Motta and Ferraz 2015).

Answer 13:

Calculation of weighted Average Cost of Capital (WACC) of CFTP

Sources Cost (%) Weightage (%) Proportionate cost (%)

Cost of equity 11.25 0.60 6.75

Cost of debt 4.45 0.40 1.79

Weighted Average Cost of Capital 8.54

Answer 14:

CFTP would use retained earnings in which the company has an unutilized balance of

$23168000.00 to finance the expansion strategy requiring $4000000.00.

Answer 15:

The final dividend should not be exceeded 35 cents per share at any cost. This is because of the

expansion strategy that the company has in front of it which require an additional $4000000.00

to materialize thus, the cash outflow should be as low as possible to arrange the funds required

for expansion project (Borenstein 2017).

Answer 16:

Implied dividend on the basis of the share price at the end of 2017 after taking into consideration

cost of equity and assumed growth rate is as followed:

Growth rate 2.50%

Cost of equity 4.78%

Answer 12:

The worst feature of long term incentives on Botanica would be the excessive operating costs

and resultant cash outflow which could have major impact on the profitability of the organization

as well as on its liquidity position in the future (Motta and Ferraz 2015).

Answer 13:

Calculation of weighted Average Cost of Capital (WACC) of CFTP

Sources Cost (%) Weightage (%) Proportionate cost (%)

Cost of equity 11.25 0.60 6.75

Cost of debt 4.45 0.40 1.79

Weighted Average Cost of Capital 8.54

Answer 14:

CFTP would use retained earnings in which the company has an unutilized balance of

$23168000.00 to finance the expansion strategy requiring $4000000.00.

Answer 15:

The final dividend should not be exceeded 35 cents per share at any cost. This is because of the

expansion strategy that the company has in front of it which require an additional $4000000.00

to materialize thus, the cash outflow should be as low as possible to arrange the funds required

for expansion project (Borenstein 2017).

Answer 16:

Implied dividend on the basis of the share price at the end of 2017 after taking into consideration

cost of equity and assumed growth rate is as followed:

Growth rate 2.50%

Cost of equity 4.78%

8FINANCE

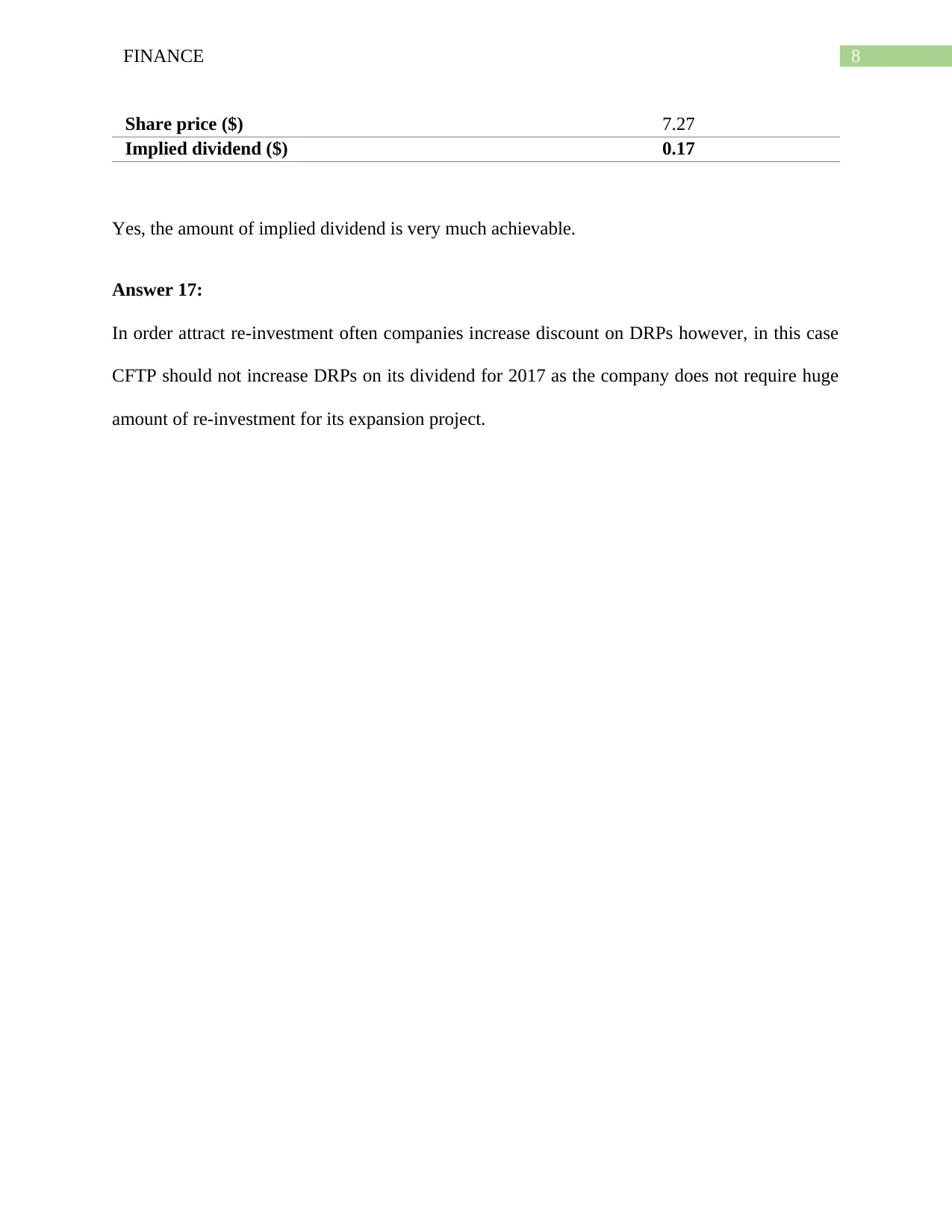

Share price ($) 7.27

Implied dividend ($) 0.17

Yes, the amount of implied dividend is very much achievable.

Answer 17:

In order attract re-investment often companies increase discount on DRPs however, in this case

CFTP should not increase DRPs on its dividend for 2017 as the company does not require huge

amount of re-investment for its expansion project.

Share price ($) 7.27

Implied dividend ($) 0.17

Yes, the amount of implied dividend is very much achievable.

Answer 17:

In order attract re-investment often companies increase discount on DRPs however, in this case

CFTP should not increase DRPs on its dividend for 2017 as the company does not require huge

amount of re-investment for its expansion project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

References:

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), pp.300-315.

Bodie, Z., 2013. Investments. McGraw-Hill.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. The American Economic Review, 105(5),

pp.315-320.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Brotherson, W.T., Eades, K.M., Harris, R.S. and Higgins, R.C., 2015. 'Best Practices' in

Estimating the Cost of Capital: An Update.

Franks, D.M., Davis, R., Bebbington, A.J., Ali, S.H., Kemp, D. and Scurrah, M., 2014. Conflict

translates environmental and social risk into business costs. Proceedings of the National

Academy of Sciences, 111(21), pp.7576-7581.

Hull, J.C., 2014. The evaluation of risk in business investment. Elsevier.

Huikku, J., Mouritsen, J. and Silvola, H., 2017. Relative reliability and the recognisable firm:

Calculating goodwill impairment value. Accounting, Organizations and Society, 56, pp.68-83.

vom Brocke, J. and Sonnenberg, C., 2015. Value-orientation in business process management.

In Handbook on Business Process Management 2 (pp. 101-132). Springer Berlin Heidelberg.

Larson, E.W. and Gray, C., 2013. Project Management: The Managerial Process with MS

Project. McGraw-Hill.

References:

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), pp.300-315.

Bodie, Z., 2013. Investments. McGraw-Hill.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. The American Economic Review, 105(5),

pp.315-320.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Brotherson, W.T., Eades, K.M., Harris, R.S. and Higgins, R.C., 2015. 'Best Practices' in

Estimating the Cost of Capital: An Update.

Franks, D.M., Davis, R., Bebbington, A.J., Ali, S.H., Kemp, D. and Scurrah, M., 2014. Conflict

translates environmental and social risk into business costs. Proceedings of the National

Academy of Sciences, 111(21), pp.7576-7581.

Hull, J.C., 2014. The evaluation of risk in business investment. Elsevier.

Huikku, J., Mouritsen, J. and Silvola, H., 2017. Relative reliability and the recognisable firm:

Calculating goodwill impairment value. Accounting, Organizations and Society, 56, pp.68-83.

vom Brocke, J. and Sonnenberg, C., 2015. Value-orientation in business process management.

In Handbook on Business Process Management 2 (pp. 101-132). Springer Berlin Heidelberg.

Larson, E.W. and Gray, C., 2013. Project Management: The Managerial Process with MS

Project. McGraw-Hill.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

Crill, R., Hanchar, J., Gooch, C. and Richard, S., 2014. Net Present Value Economic Analysis

Model for Adoption of Photoperiod Manipulation in Lactating Cow Barns.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

Stiglitz, J.E. and Rosengard, J.K., 2015. Economics of the Public Sector: Fourth International

Student Edition. WW Norton & Company.

Borenstein, S., 2017. Private Net Benefits of Residential Solar PV: The Role of Electricity

Tariffs, Tax Incentives, and Rebates. Journal of the Association of Environmental and Resource

Economists, 4(S1), pp.S85-S122.

Anderson, V., 2014. Alternative Economic Indicators (Routledge Revivals). Routledge.

Motta, R.S.D. and Ferraz, C., 2015. Estimating timber depreciation in the Brazilian Amazon.

Crill, R., Hanchar, J., Gooch, C. and Richard, S., 2014. Net Present Value Economic Analysis

Model for Adoption of Photoperiod Manipulation in Lactating Cow Barns.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

Stiglitz, J.E. and Rosengard, J.K., 2015. Economics of the Public Sector: Fourth International

Student Edition. WW Norton & Company.

Borenstein, S., 2017. Private Net Benefits of Residential Solar PV: The Role of Electricity

Tariffs, Tax Incentives, and Rebates. Journal of the Association of Environmental and Resource

Economists, 4(S1), pp.S85-S122.

Anderson, V., 2014. Alternative Economic Indicators (Routledge Revivals). Routledge.

Motta, R.S.D. and Ferraz, C., 2015. Estimating timber depreciation in the Brazilian Amazon.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.