Financial Management Assignment: Risk, Return, and Investment Analysis

VerifiedAdded on 2022/09/24

|7

|907

|20

Homework Assignment

AI Summary

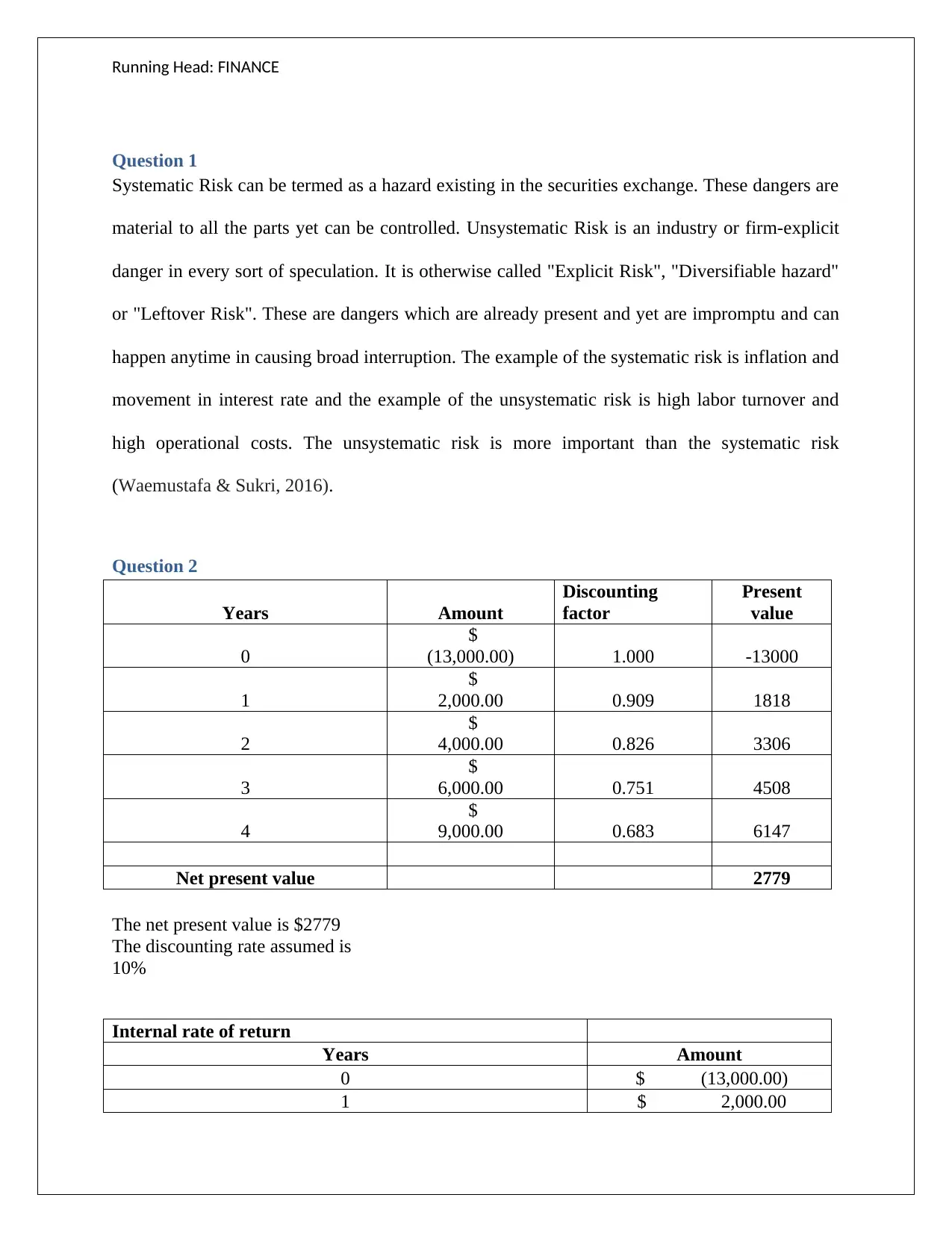

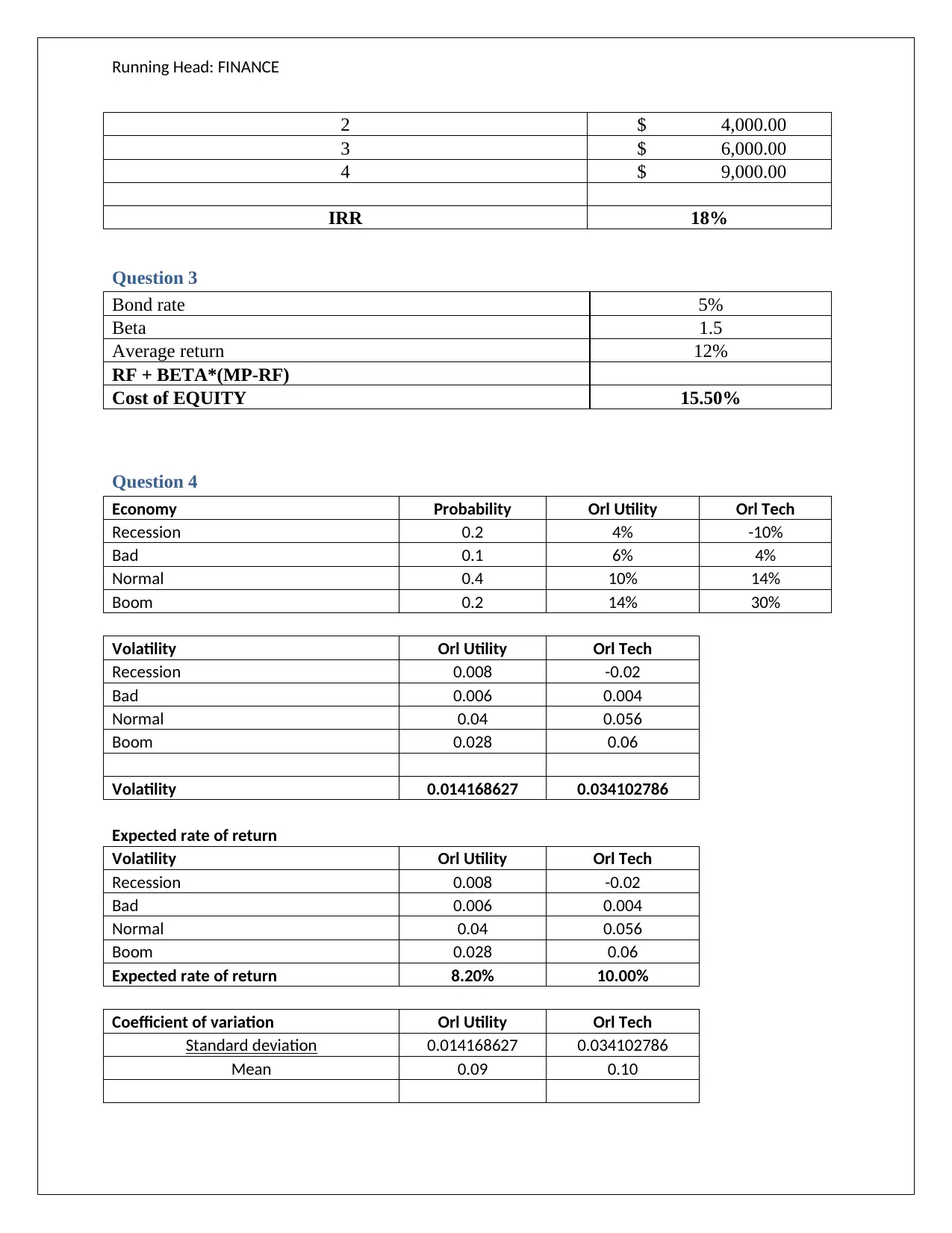

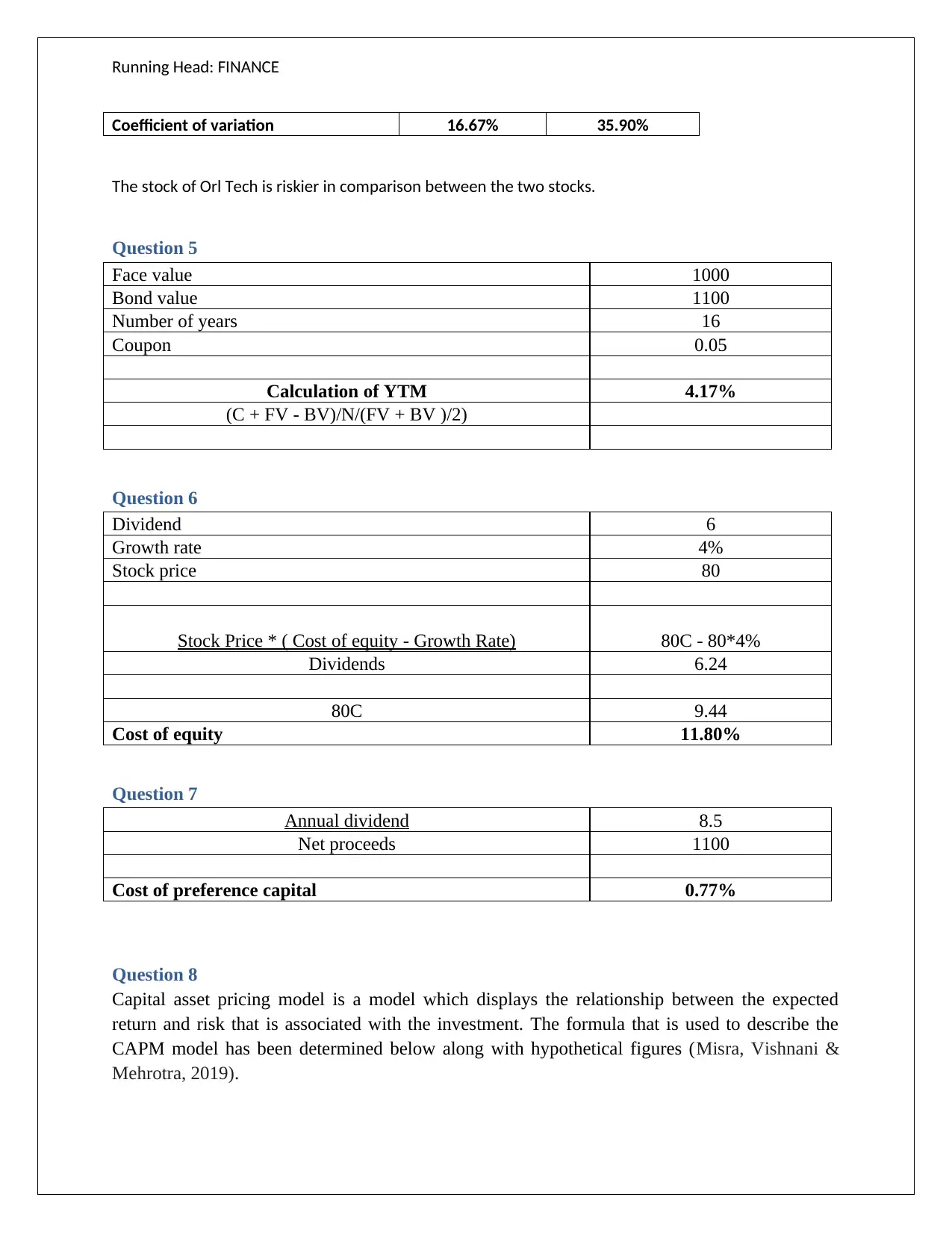

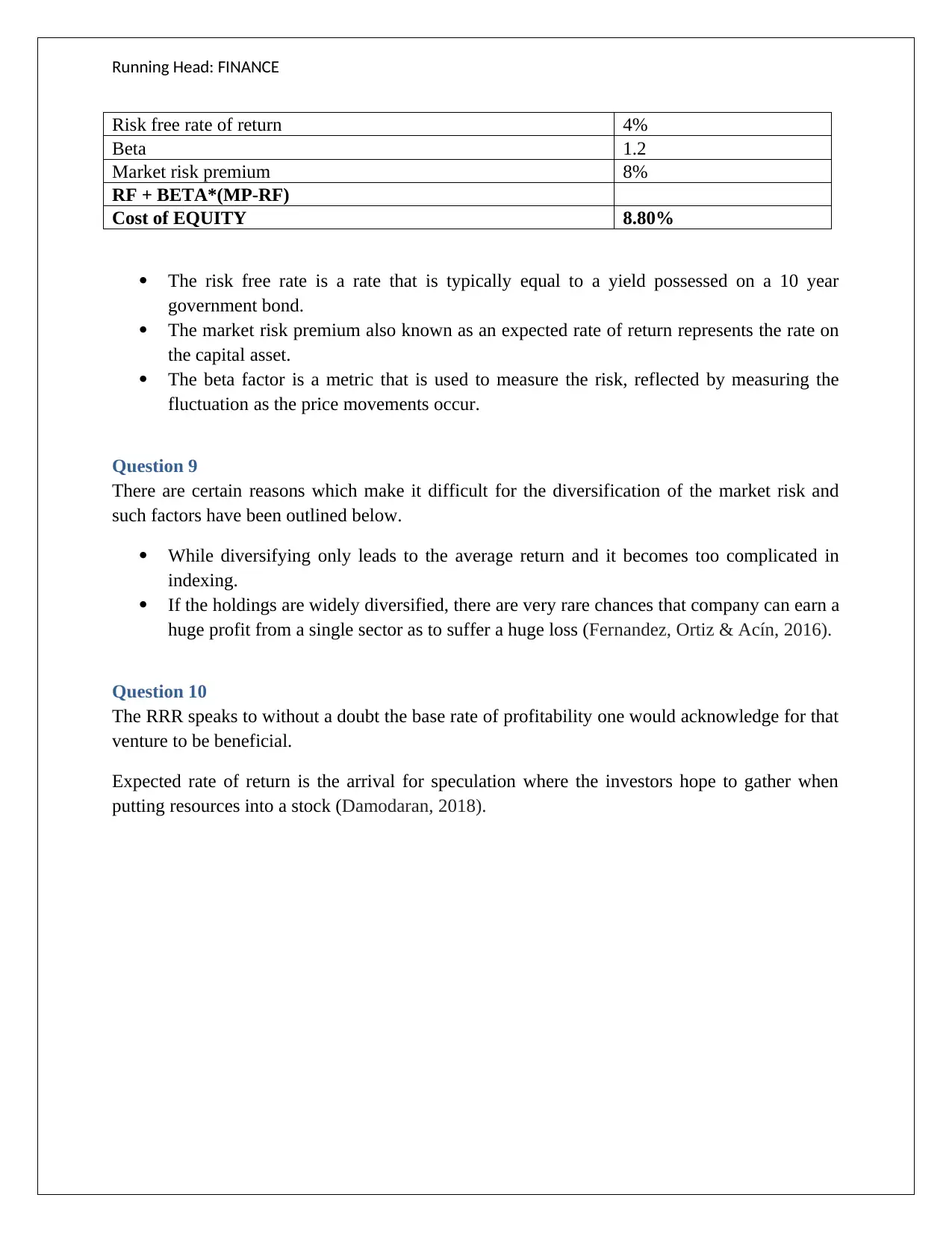

This finance assignment solution addresses key concepts in financial management. It begins by defining and differentiating between systematic and unsystematic risks, providing examples for each. The solution then calculates the Net Present Value (NPV) and Internal Rate of Return (IRR) of a project, advising on project acceptance. The Capital Asset Pricing Model (CAPM) is applied to determine the required rate of return for a stock. The assignment further analyzes the volatility, expected return, and coefficient of variation for two stocks, comparing their risk profiles. Bond and stock valuation are also calculated, including the calculation of Yield to Maturity (YTM) and the cost of equity using the dividend growth model and preference capital. The assignment concludes by discussing diversification and the expected rate of return, providing a comprehensive overview of financial analysis and investment decision-making.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.