Finance Assignment 1: Budgeting, Break-Even, Investment Decisions

VerifiedAdded on 2023/05/28

|7

|729

|489

Homework Assignment

AI Summary

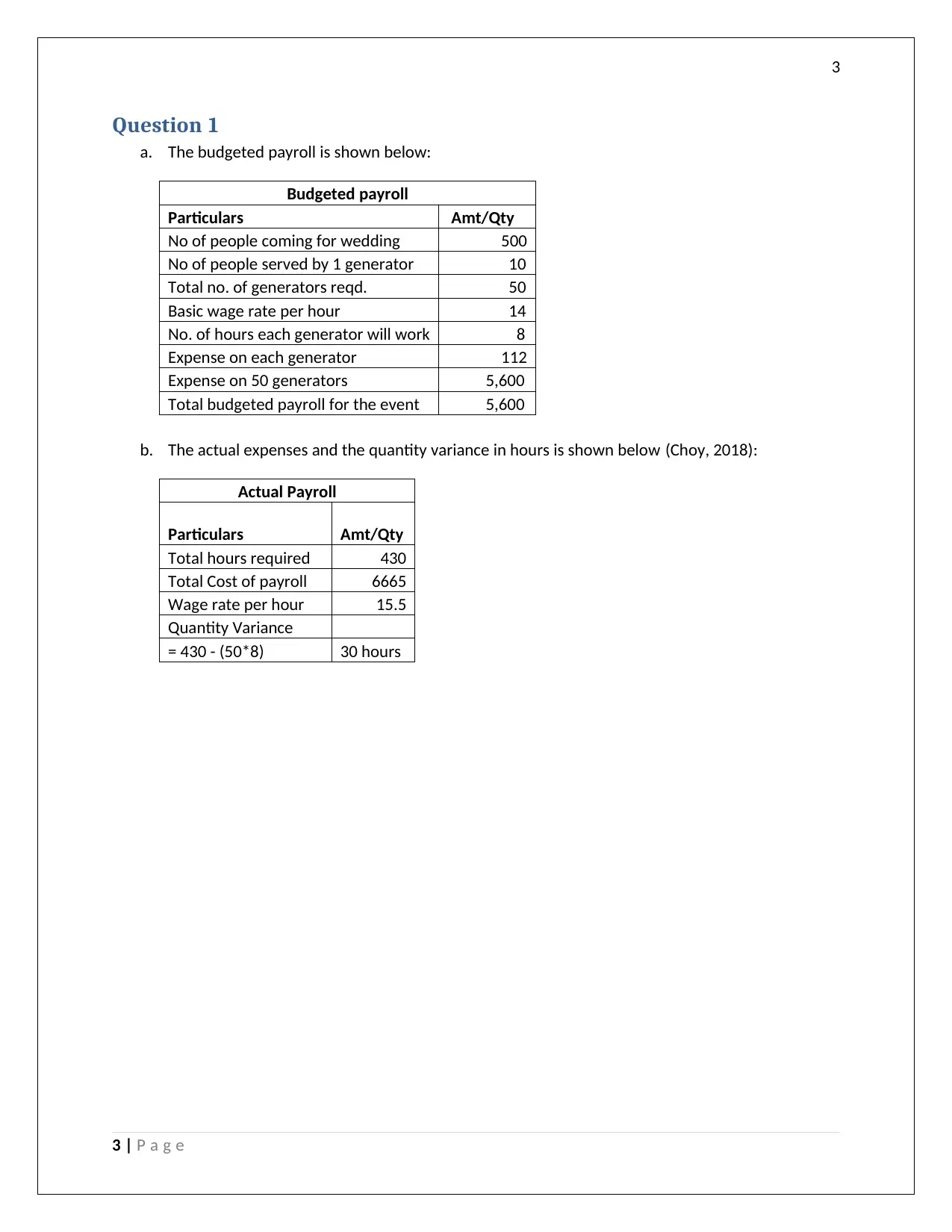

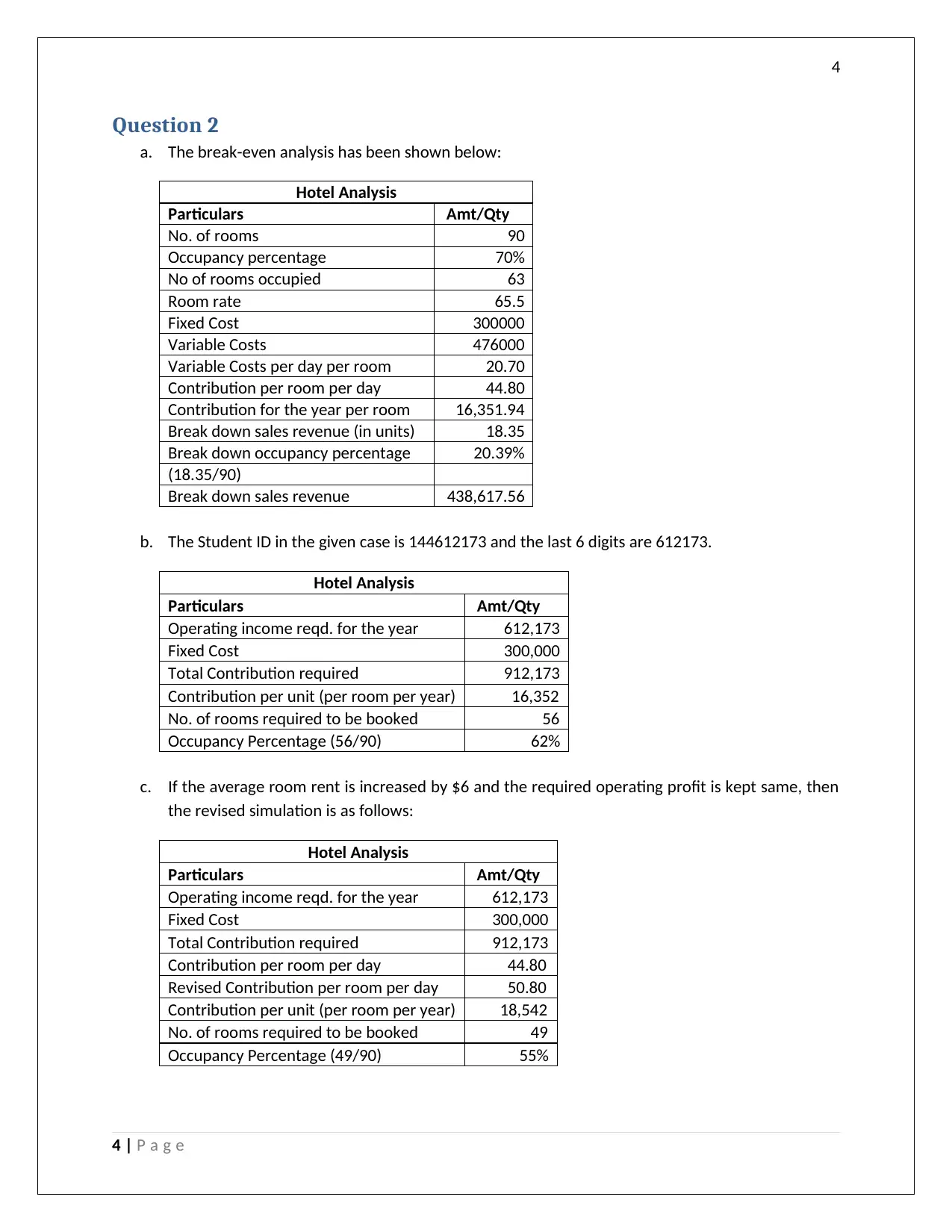

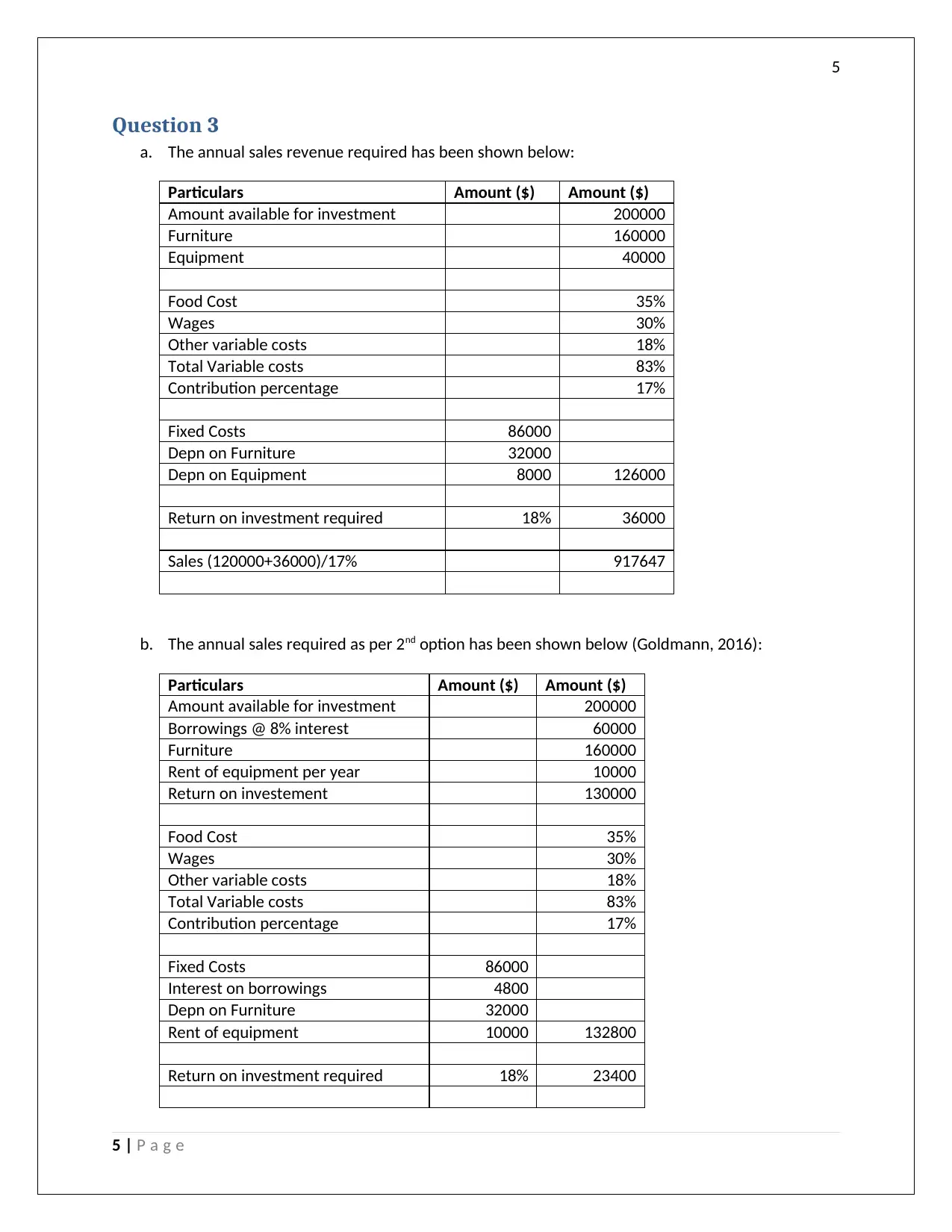

This document presents a solved Finance Assignment 1, addressing key concepts such as budgeting, variance analysis, break-even analysis, and investment decisions. The assignment begins with a budgeted payroll calculation, followed by an analysis of actual expenses and quantity variances. It then delves into break-even analysis for a hotel, considering factors like occupancy rates, room rates, and fixed/variable costs, further exploring scenarios with varying operating income requirements and room rent adjustments. Finally, the assignment evaluates two investment options, comparing annual sales revenue, return on investment, and the impact of borrowing, ultimately recommending the more financially advantageous option. Desklib offers a range of solved assignments and study tools to support students in their academic endeavors.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.