Personal Finance Report: Investment, Tax and Financial Planning 2018

VerifiedAdded on 2023/03/29

|11

|1751

|352

Report

AI Summary

This personal finance report provides a detailed analysis of an individual's financial situation, covering aspects such as income computation, tax liability, and investment strategies. It includes an income statement, balance sheet, and a projected budget for the upcoming year. The report assesses the adequacy of current health insurance coverage and provides recommendations for investment portfolio diversification, considering risk preferences and return expectations. The document also touches upon the significance of superannuation and other investment options. Desklib offers a range of study tools and solved assignments to aid students in understanding personal finance concepts and applications.

Running head: PERSONAL FINANCE

Personal Finance

Name of the Student:

Name of the University:

Author’s Note:

Personal Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PERSONAL FINANCE

Table of Contents

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................3

Answer to question 3:......................................................................................................................5

Answer to question 4:......................................................................................................................7

Answer to question 5:......................................................................................................................7

References and bibliography:..........................................................................................................9

Table of Contents

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................3

Answer to question 3:......................................................................................................................5

Answer to question 4:......................................................................................................................7

Answer to question 5:......................................................................................................................7

References and bibliography:..........................................................................................................9

2PERSONAL FINANCE

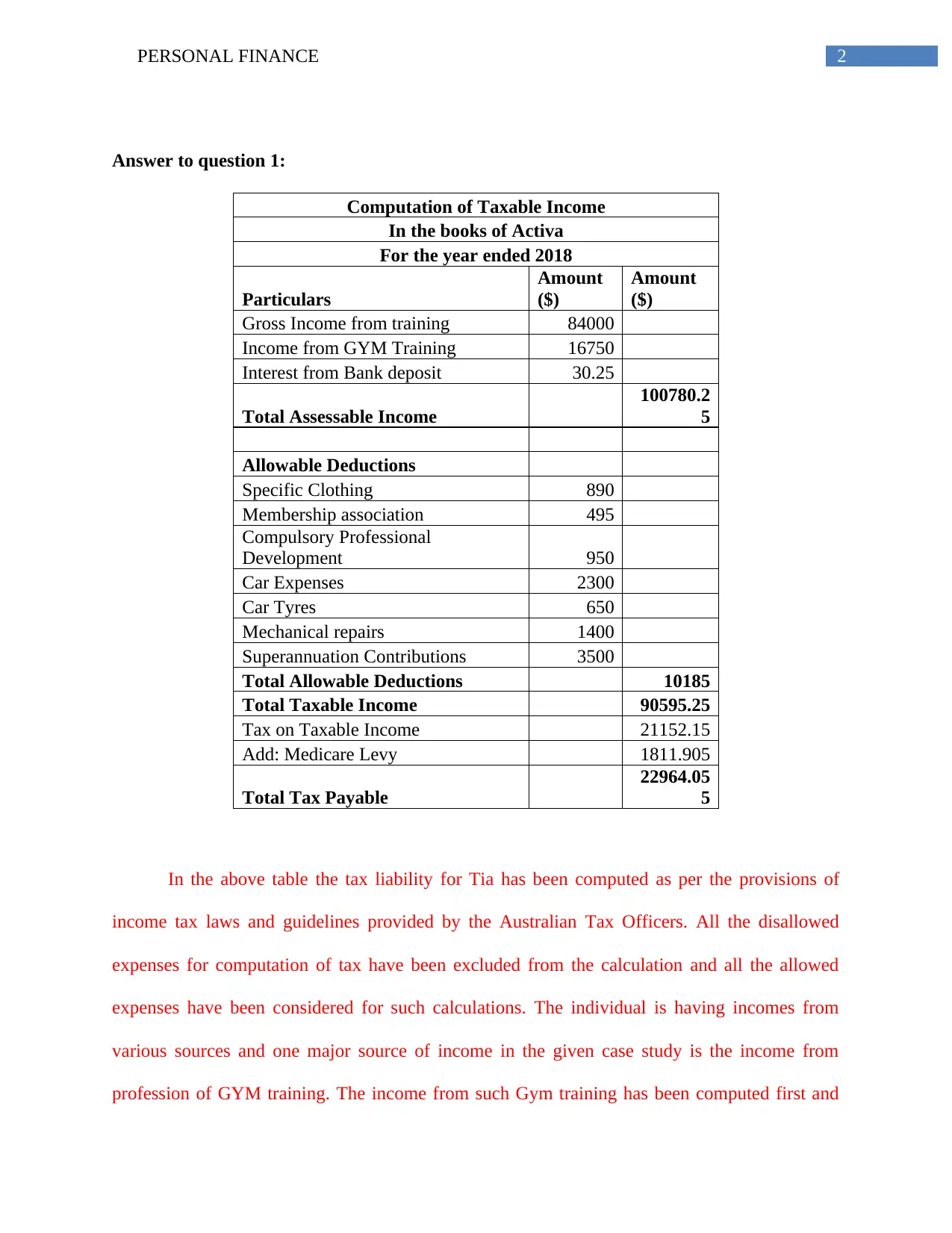

Answer to question 1:

Computation of Taxable Income

In the books of Activa

For the year ended 2018

Particulars

Amount

($)

Amount

($)

Gross Income from training 84000

Income from GYM Training 16750

Interest from Bank deposit 30.25

Total Assessable Income

100780.2

5

Allowable Deductions

Specific Clothing 890

Membership association 495

Compulsory Professional

Development 950

Car Expenses 2300

Car Tyres 650

Mechanical repairs 1400

Superannuation Contributions 3500

Total Allowable Deductions 10185

Total Taxable Income 90595.25

Tax on Taxable Income 21152.15

Add: Medicare Levy 1811.905

Total Tax Payable

22964.05

5

In the above table the tax liability for Tia has been computed as per the provisions of

income tax laws and guidelines provided by the Australian Tax Officers. All the disallowed

expenses for computation of tax have been excluded from the calculation and all the allowed

expenses have been considered for such calculations. The individual is having incomes from

various sources and one major source of income in the given case study is the income from

profession of GYM training. The income from such Gym training has been computed first and

Answer to question 1:

Computation of Taxable Income

In the books of Activa

For the year ended 2018

Particulars

Amount

($)

Amount

($)

Gross Income from training 84000

Income from GYM Training 16750

Interest from Bank deposit 30.25

Total Assessable Income

100780.2

5

Allowable Deductions

Specific Clothing 890

Membership association 495

Compulsory Professional

Development 950

Car Expenses 2300

Car Tyres 650

Mechanical repairs 1400

Superannuation Contributions 3500

Total Allowable Deductions 10185

Total Taxable Income 90595.25

Tax on Taxable Income 21152.15

Add: Medicare Levy 1811.905

Total Tax Payable

22964.05

5

In the above table the tax liability for Tia has been computed as per the provisions of

income tax laws and guidelines provided by the Australian Tax Officers. All the disallowed

expenses for computation of tax have been excluded from the calculation and all the allowed

expenses have been considered for such calculations. The individual is having incomes from

various sources and one major source of income in the given case study is the income from

profession of GYM training. The income from such Gym training has been computed first and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PERSONAL FINANCE

applying the applicable tax rate and Medicare levy rate the income tax liability and Medicare

levy have been computed and the total these two has been shown as the total tax liability.

Answer to question 2:

Income Statement of Tia

For the Year 2018

Incomes:

Gross Earnings from Gym Training 84,000

Less: Expenses related to Gym:

Payment to Gym Chain (335*50) 16,750

Sports Wear 890

Membership to personal trainers

association 495

Professional Insurance Coverage 950

Car Expenses 4,350

Total Expenses related to Gym training 23,435

Income from the Gym training 60,565

Other Expenses:

Electricity Expenses 2,600

Strata Fees 1,600

Council Rates 1,100

Water 850

Groceries and household products 16,900

Clothing 1,910

Insurance 3,380

Medical and other health related costs 975

Mobile phone and internet 1,680

Entertainment Expenses 4,800

Total other expenses 35,795

Net Income of Tia Bore Tax 24,770

Less: Tax Expenses 22,964

Net Surplus of Tia 1,806

To find out the net surplus or deficit generated by Tia’s income and spending, the above

income statement of Tia have been prepared. In this statement all the incomes or revenues are

applying the applicable tax rate and Medicare levy rate the income tax liability and Medicare

levy have been computed and the total these two has been shown as the total tax liability.

Answer to question 2:

Income Statement of Tia

For the Year 2018

Incomes:

Gross Earnings from Gym Training 84,000

Less: Expenses related to Gym:

Payment to Gym Chain (335*50) 16,750

Sports Wear 890

Membership to personal trainers

association 495

Professional Insurance Coverage 950

Car Expenses 4,350

Total Expenses related to Gym training 23,435

Income from the Gym training 60,565

Other Expenses:

Electricity Expenses 2,600

Strata Fees 1,600

Council Rates 1,100

Water 850

Groceries and household products 16,900

Clothing 1,910

Insurance 3,380

Medical and other health related costs 975

Mobile phone and internet 1,680

Entertainment Expenses 4,800

Total other expenses 35,795

Net Income of Tia Bore Tax 24,770

Less: Tax Expenses 22,964

Net Surplus of Tia 1,806

To find out the net surplus or deficit generated by Tia’s income and spending, the above

income statement of Tia have been prepared. In this statement all the incomes or revenues are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PERSONAL FINANCE

listed first and all the expenses are also shown separately. In the first part the income from Gym

training has been computed taking all the receipts from such profession and all the expenses

made towards that profession. It can be found that Tia has earned $60,565 of net income from

the profession. In the second part of the statement all the personal spending has been listed and it

can be observed that there is total $35,795 of expenses. After adjusting the incomes and expenses

the profit or earnings before tax con be found out, and after paying the income tax liability as

have been computed in the first table, the net surplus generated in a year can be ascertained.

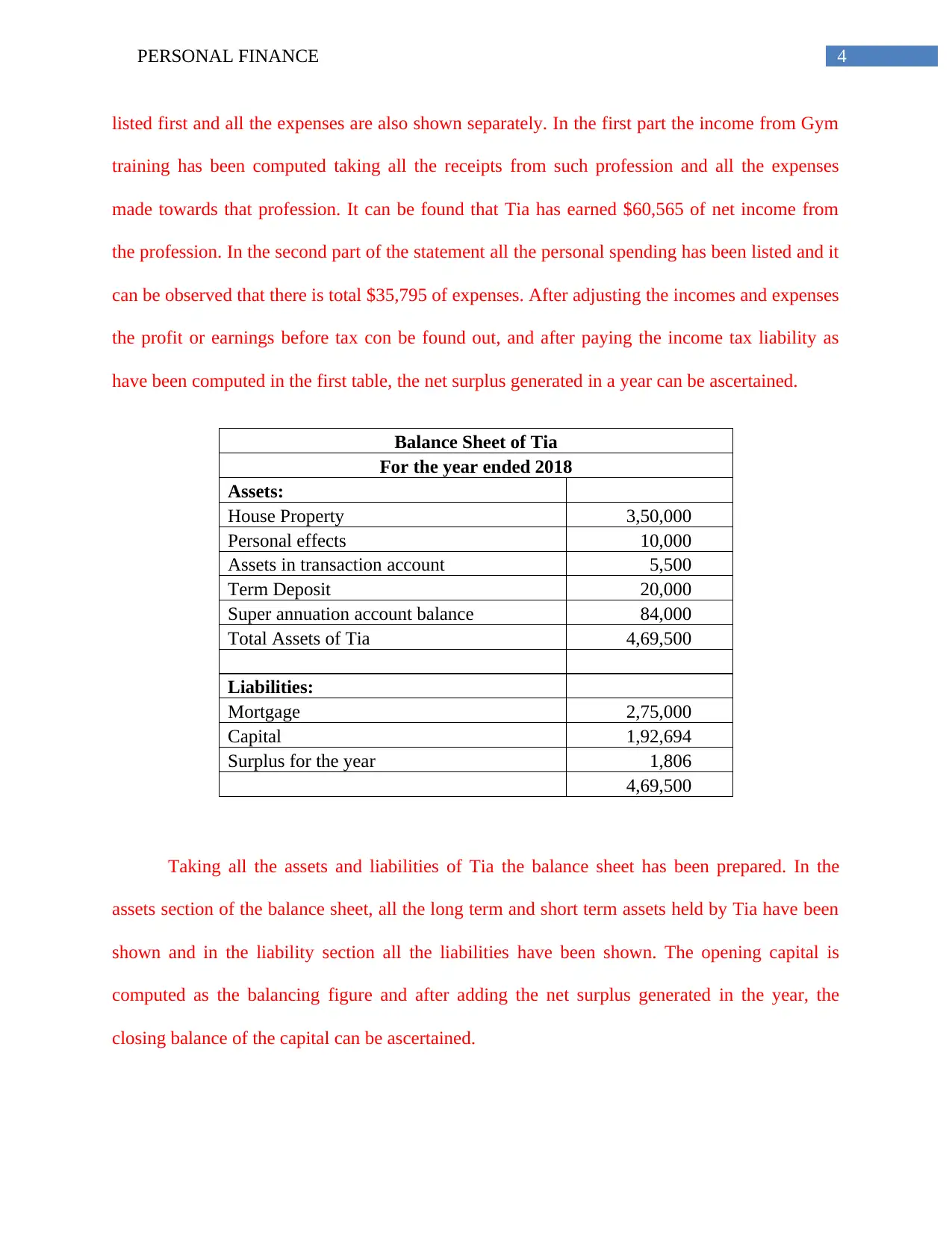

Balance Sheet of Tia

For the year ended 2018

Assets:

House Property 3,50,000

Personal effects 10,000

Assets in transaction account 5,500

Term Deposit 20,000

Super annuation account balance 84,000

Total Assets of Tia 4,69,500

Liabilities:

Mortgage 2,75,000

Capital 1,92,694

Surplus for the year 1,806

4,69,500

Taking all the assets and liabilities of Tia the balance sheet has been prepared. In the

assets section of the balance sheet, all the long term and short term assets held by Tia have been

shown and in the liability section all the liabilities have been shown. The opening capital is

computed as the balancing figure and after adding the net surplus generated in the year, the

closing balance of the capital can be ascertained.

listed first and all the expenses are also shown separately. In the first part the income from Gym

training has been computed taking all the receipts from such profession and all the expenses

made towards that profession. It can be found that Tia has earned $60,565 of net income from

the profession. In the second part of the statement all the personal spending has been listed and it

can be observed that there is total $35,795 of expenses. After adjusting the incomes and expenses

the profit or earnings before tax con be found out, and after paying the income tax liability as

have been computed in the first table, the net surplus generated in a year can be ascertained.

Balance Sheet of Tia

For the year ended 2018

Assets:

House Property 3,50,000

Personal effects 10,000

Assets in transaction account 5,500

Term Deposit 20,000

Super annuation account balance 84,000

Total Assets of Tia 4,69,500

Liabilities:

Mortgage 2,75,000

Capital 1,92,694

Surplus for the year 1,806

4,69,500

Taking all the assets and liabilities of Tia the balance sheet has been prepared. In the

assets section of the balance sheet, all the long term and short term assets held by Tia have been

shown and in the liability section all the liabilities have been shown. The opening capital is

computed as the balancing figure and after adding the net surplus generated in the year, the

closing balance of the capital can be ascertained.

5PERSONAL FINANCE

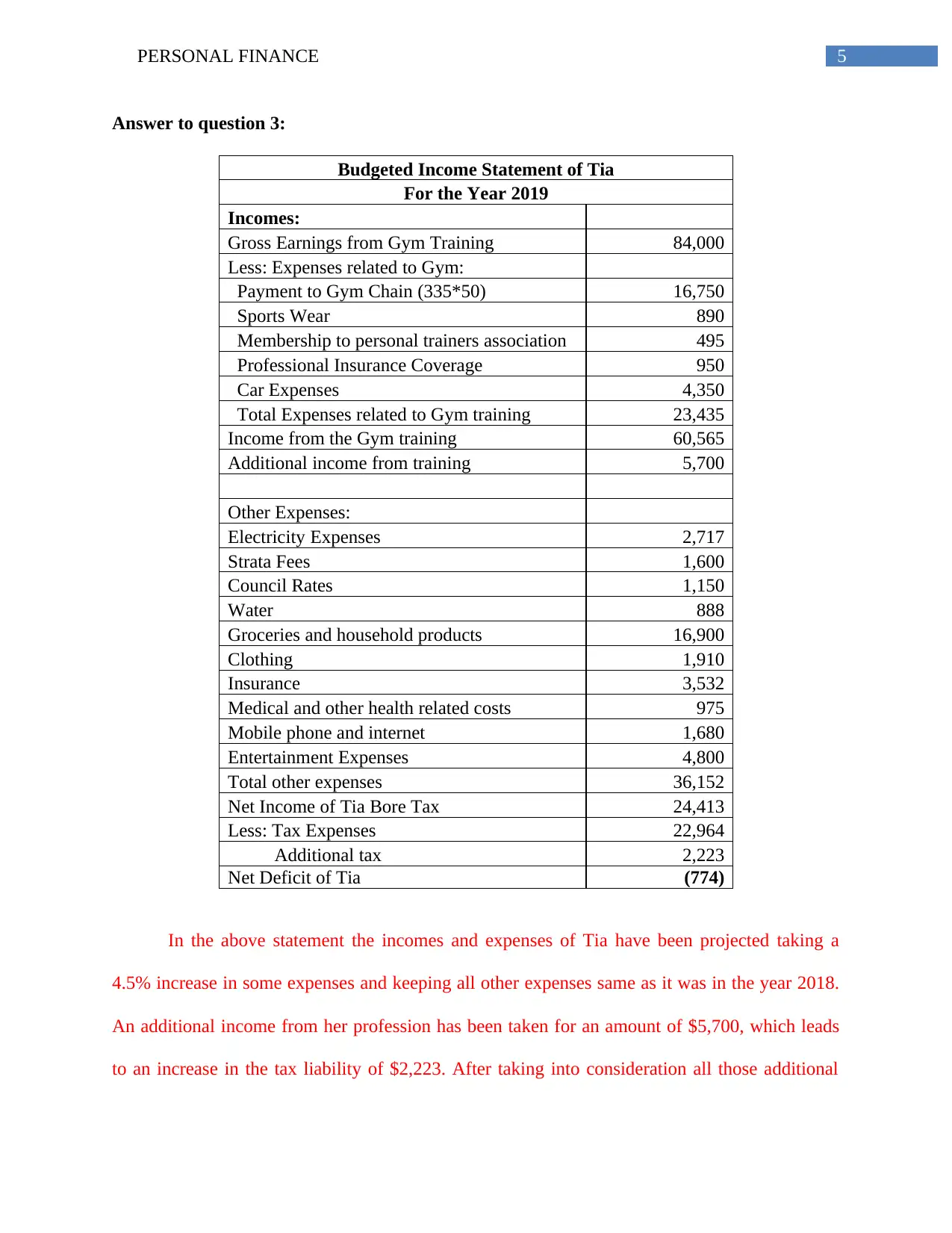

Answer to question 3:

Budgeted Income Statement of Tia

For the Year 2019

Incomes:

Gross Earnings from Gym Training 84,000

Less: Expenses related to Gym:

Payment to Gym Chain (335*50) 16,750

Sports Wear 890

Membership to personal trainers association 495

Professional Insurance Coverage 950

Car Expenses 4,350

Total Expenses related to Gym training 23,435

Income from the Gym training 60,565

Additional income from training 5,700

Other Expenses:

Electricity Expenses 2,717

Strata Fees 1,600

Council Rates 1,150

Water 888

Groceries and household products 16,900

Clothing 1,910

Insurance 3,532

Medical and other health related costs 975

Mobile phone and internet 1,680

Entertainment Expenses 4,800

Total other expenses 36,152

Net Income of Tia Bore Tax 24,413

Less: Tax Expenses 22,964

Additional tax 2,223

Net Deficit of Tia (774)

In the above statement the incomes and expenses of Tia have been projected taking a

4.5% increase in some expenses and keeping all other expenses same as it was in the year 2018.

An additional income from her profession has been taken for an amount of $5,700, which leads

to an increase in the tax liability of $2,223. After taking into consideration all those additional

Answer to question 3:

Budgeted Income Statement of Tia

For the Year 2019

Incomes:

Gross Earnings from Gym Training 84,000

Less: Expenses related to Gym:

Payment to Gym Chain (335*50) 16,750

Sports Wear 890

Membership to personal trainers association 495

Professional Insurance Coverage 950

Car Expenses 4,350

Total Expenses related to Gym training 23,435

Income from the Gym training 60,565

Additional income from training 5,700

Other Expenses:

Electricity Expenses 2,717

Strata Fees 1,600

Council Rates 1,150

Water 888

Groceries and household products 16,900

Clothing 1,910

Insurance 3,532

Medical and other health related costs 975

Mobile phone and internet 1,680

Entertainment Expenses 4,800

Total other expenses 36,152

Net Income of Tia Bore Tax 24,413

Less: Tax Expenses 22,964

Additional tax 2,223

Net Deficit of Tia (774)

In the above statement the incomes and expenses of Tia have been projected taking a

4.5% increase in some expenses and keeping all other expenses same as it was in the year 2018.

An additional income from her profession has been taken for an amount of $5,700, which leads

to an increase in the tax liability of $2,223. After taking into consideration all those additional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PERSONAL FINANCE

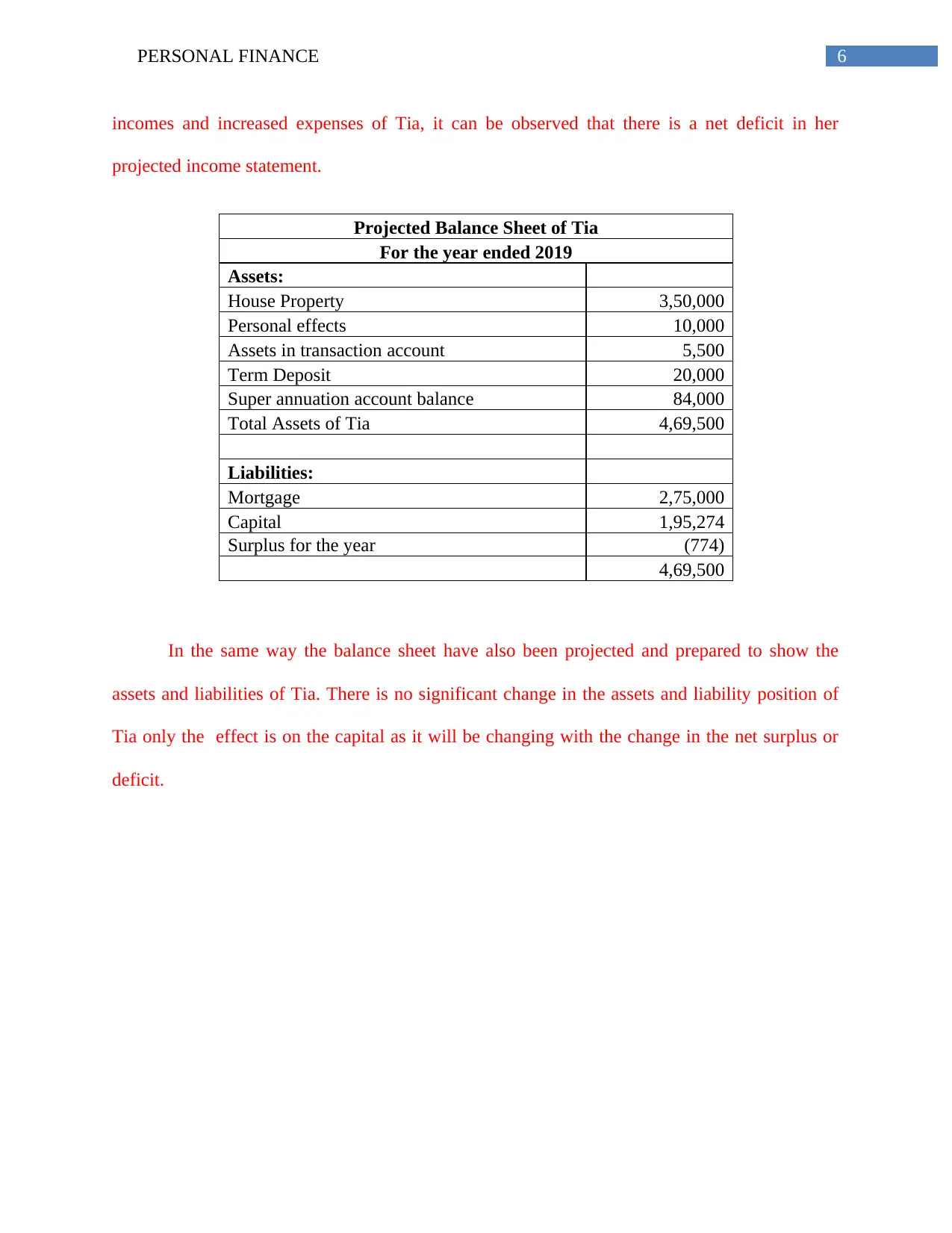

incomes and increased expenses of Tia, it can be observed that there is a net deficit in her

projected income statement.

Projected Balance Sheet of Tia

For the year ended 2019

Assets:

House Property 3,50,000

Personal effects 10,000

Assets in transaction account 5,500

Term Deposit 20,000

Super annuation account balance 84,000

Total Assets of Tia 4,69,500

Liabilities:

Mortgage 2,75,000

Capital 1,95,274

Surplus for the year (774)

4,69,500

In the same way the balance sheet have also been projected and prepared to show the

assets and liabilities of Tia. There is no significant change in the assets and liability position of

Tia only the effect is on the capital as it will be changing with the change in the net surplus or

deficit.

incomes and increased expenses of Tia, it can be observed that there is a net deficit in her

projected income statement.

Projected Balance Sheet of Tia

For the year ended 2019

Assets:

House Property 3,50,000

Personal effects 10,000

Assets in transaction account 5,500

Term Deposit 20,000

Super annuation account balance 84,000

Total Assets of Tia 4,69,500

Liabilities:

Mortgage 2,75,000

Capital 1,95,274

Surplus for the year (774)

4,69,500

In the same way the balance sheet have also been projected and prepared to show the

assets and liabilities of Tia. There is no significant change in the assets and liability position of

Tia only the effect is on the capital as it will be changing with the change in the net surplus or

deficit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PERSONAL FINANCE

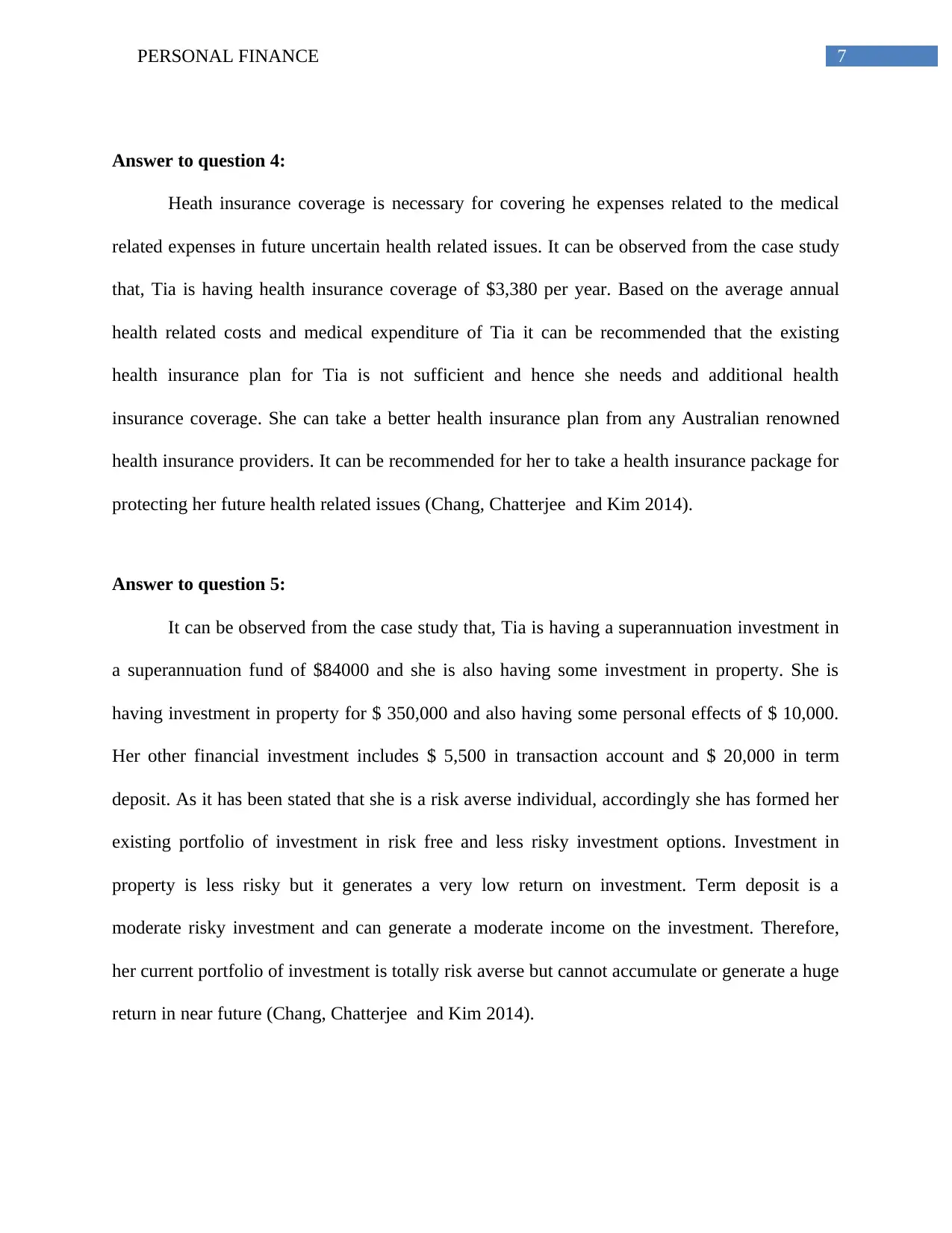

Answer to question 4:

Heath insurance coverage is necessary for covering he expenses related to the medical

related expenses in future uncertain health related issues. It can be observed from the case study

that, Tia is having health insurance coverage of $3,380 per year. Based on the average annual

health related costs and medical expenditure of Tia it can be recommended that the existing

health insurance plan for Tia is not sufficient and hence she needs and additional health

insurance coverage. She can take a better health insurance plan from any Australian renowned

health insurance providers. It can be recommended for her to take a health insurance package for

protecting her future health related issues (Chang, Chatterjee and Kim 2014).

Answer to question 5:

It can be observed from the case study that, Tia is having a superannuation investment in

a superannuation fund of $84000 and she is also having some investment in property. She is

having investment in property for $ 350,000 and also having some personal effects of $ 10,000.

Her other financial investment includes $ 5,500 in transaction account and $ 20,000 in term

deposit. As it has been stated that she is a risk averse individual, accordingly she has formed her

existing portfolio of investment in risk free and less risky investment options. Investment in

property is less risky but it generates a very low return on investment. Term deposit is a

moderate risky investment and can generate a moderate income on the investment. Therefore,

her current portfolio of investment is totally risk averse but cannot accumulate or generate a huge

return in near future (Chang, Chatterjee and Kim 2014).

Answer to question 4:

Heath insurance coverage is necessary for covering he expenses related to the medical

related expenses in future uncertain health related issues. It can be observed from the case study

that, Tia is having health insurance coverage of $3,380 per year. Based on the average annual

health related costs and medical expenditure of Tia it can be recommended that the existing

health insurance plan for Tia is not sufficient and hence she needs and additional health

insurance coverage. She can take a better health insurance plan from any Australian renowned

health insurance providers. It can be recommended for her to take a health insurance package for

protecting her future health related issues (Chang, Chatterjee and Kim 2014).

Answer to question 5:

It can be observed from the case study that, Tia is having a superannuation investment in

a superannuation fund of $84000 and she is also having some investment in property. She is

having investment in property for $ 350,000 and also having some personal effects of $ 10,000.

Her other financial investment includes $ 5,500 in transaction account and $ 20,000 in term

deposit. As it has been stated that she is a risk averse individual, accordingly she has formed her

existing portfolio of investment in risk free and less risky investment options. Investment in

property is less risky but it generates a very low return on investment. Term deposit is a

moderate risky investment and can generate a moderate income on the investment. Therefore,

her current portfolio of investment is totally risk averse but cannot accumulate or generate a huge

return in near future (Chang, Chatterjee and Kim 2014).

8PERSONAL FINANCE

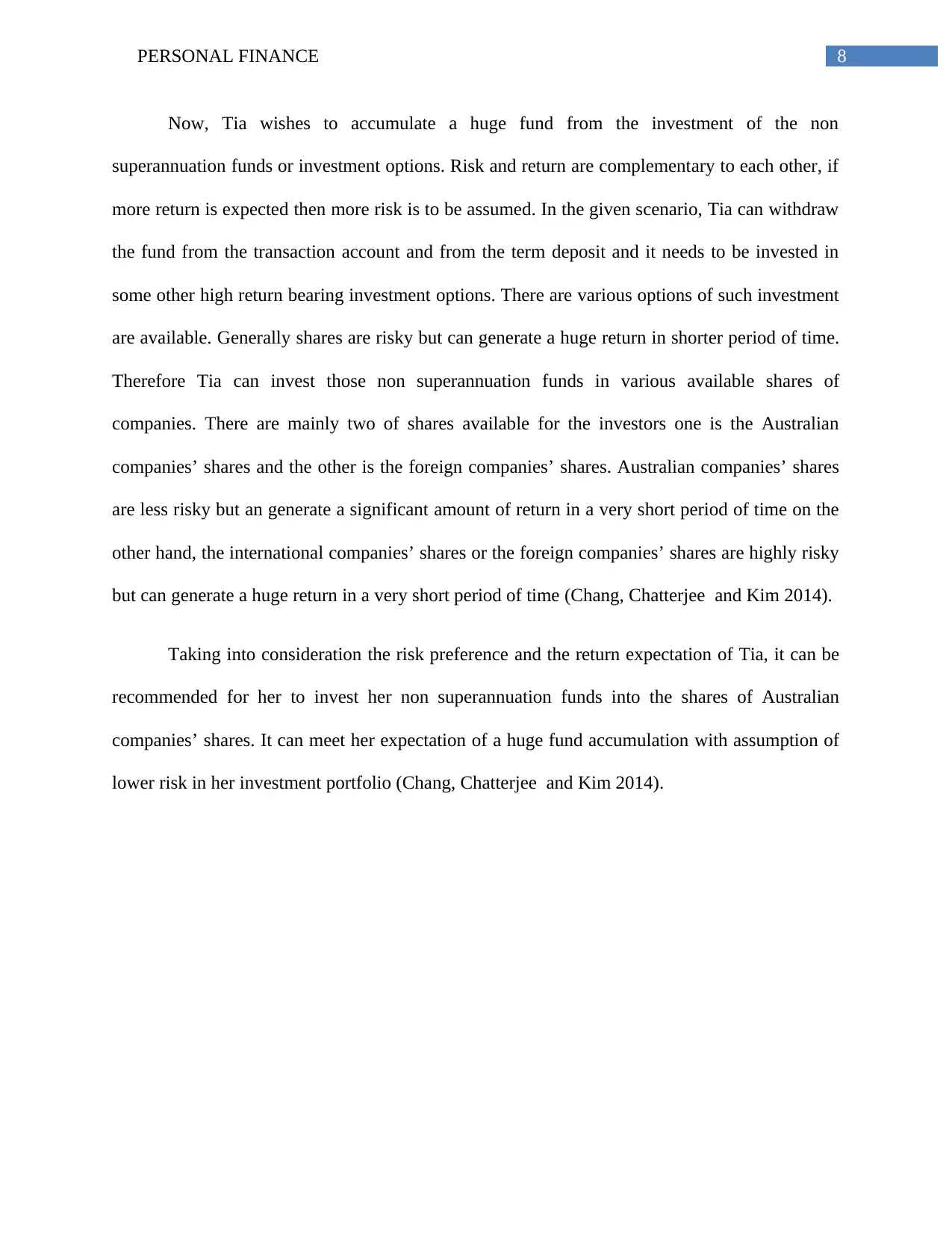

Now, Tia wishes to accumulate a huge fund from the investment of the non

superannuation funds or investment options. Risk and return are complementary to each other, if

more return is expected then more risk is to be assumed. In the given scenario, Tia can withdraw

the fund from the transaction account and from the term deposit and it needs to be invested in

some other high return bearing investment options. There are various options of such investment

are available. Generally shares are risky but can generate a huge return in shorter period of time.

Therefore Tia can invest those non superannuation funds in various available shares of

companies. There are mainly two of shares available for the investors one is the Australian

companies’ shares and the other is the foreign companies’ shares. Australian companies’ shares

are less risky but an generate a significant amount of return in a very short period of time on the

other hand, the international companies’ shares or the foreign companies’ shares are highly risky

but can generate a huge return in a very short period of time (Chang, Chatterjee and Kim 2014).

Taking into consideration the risk preference and the return expectation of Tia, it can be

recommended for her to invest her non superannuation funds into the shares of Australian

companies’ shares. It can meet her expectation of a huge fund accumulation with assumption of

lower risk in her investment portfolio (Chang, Chatterjee and Kim 2014).

Now, Tia wishes to accumulate a huge fund from the investment of the non

superannuation funds or investment options. Risk and return are complementary to each other, if

more return is expected then more risk is to be assumed. In the given scenario, Tia can withdraw

the fund from the transaction account and from the term deposit and it needs to be invested in

some other high return bearing investment options. There are various options of such investment

are available. Generally shares are risky but can generate a huge return in shorter period of time.

Therefore Tia can invest those non superannuation funds in various available shares of

companies. There are mainly two of shares available for the investors one is the Australian

companies’ shares and the other is the foreign companies’ shares. Australian companies’ shares

are less risky but an generate a significant amount of return in a very short period of time on the

other hand, the international companies’ shares or the foreign companies’ shares are highly risky

but can generate a huge return in a very short period of time (Chang, Chatterjee and Kim 2014).

Taking into consideration the risk preference and the return expectation of Tia, it can be

recommended for her to invest her non superannuation funds into the shares of Australian

companies’ shares. It can meet her expectation of a huge fund accumulation with assumption of

lower risk in her investment portfolio (Chang, Chatterjee and Kim 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PERSONAL FINANCE

References and bibliography:

Chang, Y., Chatterjee, S. and Kim, J., 2014. Household finance and food insecurity. Journal of

Family and Economic Issues, 35(4), pp.499-515.

Cole, S., Paulson, A. and Shastry, G.K., 2016. High school curriculum and financial outcomes:

The impact of mandated personal finance and mathematics courses. Journal of Human

Resources, 51(3), pp.656-698.

Cutler, N.E., 2015. Millennials and Finance: The" Amazon Generation". Journal of Financial

Service Professionals, 69(6).

Farrell, L., Fry, T.R. and Risse, L., 2016. The significance of financial self-efficacy in explaining

women’s personal finance behaviour. Journal of Economic Psychology, 54, pp.85-99.

Inderst, G. and Della Croce, R., 2014. Pension fund investment in infrastructure: A comparison

between Australia and Canada. OECD.

Jensen, N.R. and Steffensen, M., 2015. Personal finance and life insurance under separation of

risk aversion and elasticity of substitution. Insurance: mathematics and economics, 62, pp.28-41.

Kausel, E.E., Hansen, E. and Tapia, P., 2016. Responsible Personal Finance: The Role of

Conscientiousness in Bank and Pension Savings in C hile. International Review of Finance,

16(1), pp.161-167.

Moessinger, M.D., 2014. Do the personal characteristics of finance ministers affect changes in

public debt?. Public choice, 161(1-2), pp.183-207.

References and bibliography:

Chang, Y., Chatterjee, S. and Kim, J., 2014. Household finance and food insecurity. Journal of

Family and Economic Issues, 35(4), pp.499-515.

Cole, S., Paulson, A. and Shastry, G.K., 2016. High school curriculum and financial outcomes:

The impact of mandated personal finance and mathematics courses. Journal of Human

Resources, 51(3), pp.656-698.

Cutler, N.E., 2015. Millennials and Finance: The" Amazon Generation". Journal of Financial

Service Professionals, 69(6).

Farrell, L., Fry, T.R. and Risse, L., 2016. The significance of financial self-efficacy in explaining

women’s personal finance behaviour. Journal of Economic Psychology, 54, pp.85-99.

Inderst, G. and Della Croce, R., 2014. Pension fund investment in infrastructure: A comparison

between Australia and Canada. OECD.

Jensen, N.R. and Steffensen, M., 2015. Personal finance and life insurance under separation of

risk aversion and elasticity of substitution. Insurance: mathematics and economics, 62, pp.28-41.

Kausel, E.E., Hansen, E. and Tapia, P., 2016. Responsible Personal Finance: The Role of

Conscientiousness in Bank and Pension Savings in C hile. International Review of Finance,

16(1), pp.161-167.

Moessinger, M.D., 2014. Do the personal characteristics of finance ministers affect changes in

public debt?. Public choice, 161(1-2), pp.183-207.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PERSONAL FINANCE

Ramiah, V., Zhao, Y. and Moosa, I., 2014. Working capital management during the global

financial crisis: the Australian experience. Qualitative Research in Financial Markets, 6(3),

pp.332-351.

Tyson, E., 2018. Personal finance for dummies. For Dummies.

Young, M., Young, R. and Romero Zapata, J., 2014. Project, programme and portfolio maturity:

a case study of Australian Federal Government. International Journal of Managing Projects in

Business, 7(2), pp.215-230.

Ramiah, V., Zhao, Y. and Moosa, I., 2014. Working capital management during the global

financial crisis: the Australian experience. Qualitative Research in Financial Markets, 6(3),

pp.332-351.

Tyson, E., 2018. Personal finance for dummies. For Dummies.

Young, M., Young, R. and Romero Zapata, J., 2014. Project, programme and portfolio maturity:

a case study of Australian Federal Government. International Journal of Managing Projects in

Business, 7(2), pp.215-230.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.