Finance for Managers: Financial Analysis and Investment Appraisal

VerifiedAdded on 2023/01/06

|15

|3869

|39

Report

AI Summary

This report, titled "Finance for Managers," delves into crucial aspects of financial management. It begins with an introduction to financial analysis, emphasizing the significance of data sources both internal and external to an organization. The report then performs a detailed ratio analysis of Unilever plc, assessing its profitability, efficiency, liquidity, and gearing ratios. Following this, it explores various budgeting approaches, including input/output, activity-based, and incremental budgeting, considering financial constraints, organizational targets, accounting conventions, and legal requirements. Furthermore, the report discusses cash flow issues and legal requirements related to budgeting, providing insights into effective resource allocation. Finally, it examines investment appraisal techniques, offering a comprehensive overview of financial management principles and their practical application. The report uses financial statements, ratio analysis, and budgeting techniques to assess organizational performance and guide financial decision-making.

FINANCE FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................2

Ratio analysis of Unilever plc......................................................................................................2

TASK 3............................................................................................................................................5

Approaches to production of budget with reference to financial constraints, achievement of the

organisational targets, accounting conventions and the legal requirements................................5

TASK 4 ...........................................................................................................................................6

TASK 5 600.....................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................2

Ratio analysis of Unilever plc......................................................................................................2

TASK 3............................................................................................................................................5

Approaches to production of budget with reference to financial constraints, achievement of the

organisational targets, accounting conventions and the legal requirements................................5

TASK 4 ...........................................................................................................................................6

TASK 5 600.....................................................................................................................................8

REFERENCES..............................................................................................................................10

EXECUTIVE SUMMARY

Financial management could be described as function or area in organisation that is

concerned with the profits, expenses and funds so that organisation have required resources for

meeting the goals and objectives. The report reveals about the different financial information that

is available for users to analyse the performance and position of organisation. The financial

information has to be analysed from different sources before establishing trading relationship or

making investments. Ratio analysis is an effective tool which is used by the investors and

management for assessing profitability, efficiency and liquidity of company. Ratio analysis of

Unilever plc has been done for identifying strengths and weaknesses of the organisational

processes. Budget which is an important planning tool plays an important role in company. The

different approaches enable the company to assess the issues and make allocation of resources

accordingly. Report has analysed the budget and provided alternate actions that could be taken

by organisation. At the last investment appraisal techniques have been used for analysing the

viability of investments before making capital expenditures.

TASK 1

Main sources of data available inside and outside of organisation and use of information for

reviewing the financial performance.

Financial analysis could be defined as the process used for measuring results of the

policies and operations of the management. Internal as well as external users could analyse the

financial health of the organisation over a period of time.

Main sources of data of the organisation

There are different sources of data that are used for reviewing financial performance are:

Income Statement

It is the main source of financial information providing summarised information about

the company incomes and expenditures. Users could identify the returns and different costs of

the organisation to know the areas from company is earning and also making the spendings. It

could be evaluated whether the policies and strategies of the management are working

effectively for earning profits. It is essential as the if company is not earning adequate profits it

represents in inefficient and it will not be able to provide adequate returns.

Balance Sheet

1

Financial management could be described as function or area in organisation that is

concerned with the profits, expenses and funds so that organisation have required resources for

meeting the goals and objectives. The report reveals about the different financial information that

is available for users to analyse the performance and position of organisation. The financial

information has to be analysed from different sources before establishing trading relationship or

making investments. Ratio analysis is an effective tool which is used by the investors and

management for assessing profitability, efficiency and liquidity of company. Ratio analysis of

Unilever plc has been done for identifying strengths and weaknesses of the organisational

processes. Budget which is an important planning tool plays an important role in company. The

different approaches enable the company to assess the issues and make allocation of resources

accordingly. Report has analysed the budget and provided alternate actions that could be taken

by organisation. At the last investment appraisal techniques have been used for analysing the

viability of investments before making capital expenditures.

TASK 1

Main sources of data available inside and outside of organisation and use of information for

reviewing the financial performance.

Financial analysis could be defined as the process used for measuring results of the

policies and operations of the management. Internal as well as external users could analyse the

financial health of the organisation over a period of time.

Main sources of data of the organisation

There are different sources of data that are used for reviewing financial performance are:

Income Statement

It is the main source of financial information providing summarised information about

the company incomes and expenditures. Users could identify the returns and different costs of

the organisation to know the areas from company is earning and also making the spendings. It

could be evaluated whether the policies and strategies of the management are working

effectively for earning profits. It is essential as the if company is not earning adequate profits it

represents in inefficient and it will not be able to provide adequate returns.

Balance Sheet

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It provides information about the financial status and wealth of the enterprise. Areas such

as capital structure, liquidity and efficiency of the management could be identified using the

statement. The in depth analysis of the balance sheet is performed to identify the investments,

equity and the obligations of the enterprise (Lin, Hsiao and Yeh, 2017). It is also used for

assessing the financial risks associated with the company.

Different situations in which financial information is used.

Entering into trading relationship

Before entering into trading relationship, firms have to analyse the cash flow statement

and balance sheet to identify the liquidity position and to know the financial obligations.

Management has to identify whether the other party will be able to make payments timely for the

supplies. If it is having inadequate cash flows or high financial obligation trding with such party

could be riskier. However the actual performance and the reasons for the outstanding obligations

could not be identified from these statements clearly.

Investment decisions

For making investments in any enterprise it is essential for the investors to assess the

performance and position of the enterprise. From the income statement and balance investors

assess the returns over equity, capital employed, net profits and return over capital employed for

evaluating the performance and management efficiency. It provides whether adequate returns

will be earned by making the investments or not.

Acquisitions or mergers

In the current scenarios mergers and acquisitions are on the top trends through which

companies are expanding or growing. It involves considerable amount of investment of the

company therefore management has to analyse the target company performance and position

using the financial statements of past years. They analyse the profitability of the firms using

income statement, liquidity and stakeholders of the firm from balance sheet (Lee and Tweedie,

2020). Also the information about the share prices could be analysed from securities exchange.

However the information about internal management efficiency and internal controls could not

be identified.

TASK 2

Ratio analysis of Unilever plc

UNILEVER PLC

2

as capital structure, liquidity and efficiency of the management could be identified using the

statement. The in depth analysis of the balance sheet is performed to identify the investments,

equity and the obligations of the enterprise (Lin, Hsiao and Yeh, 2017). It is also used for

assessing the financial risks associated with the company.

Different situations in which financial information is used.

Entering into trading relationship

Before entering into trading relationship, firms have to analyse the cash flow statement

and balance sheet to identify the liquidity position and to know the financial obligations.

Management has to identify whether the other party will be able to make payments timely for the

supplies. If it is having inadequate cash flows or high financial obligation trding with such party

could be riskier. However the actual performance and the reasons for the outstanding obligations

could not be identified from these statements clearly.

Investment decisions

For making investments in any enterprise it is essential for the investors to assess the

performance and position of the enterprise. From the income statement and balance investors

assess the returns over equity, capital employed, net profits and return over capital employed for

evaluating the performance and management efficiency. It provides whether adequate returns

will be earned by making the investments or not.

Acquisitions or mergers

In the current scenarios mergers and acquisitions are on the top trends through which

companies are expanding or growing. It involves considerable amount of investment of the

company therefore management has to analyse the target company performance and position

using the financial statements of past years. They analyse the profitability of the firms using

income statement, liquidity and stakeholders of the firm from balance sheet (Lee and Tweedie,

2020). Also the information about the share prices could be analysed from securities exchange.

However the information about internal management efficiency and internal controls could not

be identified.

TASK 2

Ratio analysis of Unilever plc

UNILEVER PLC

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

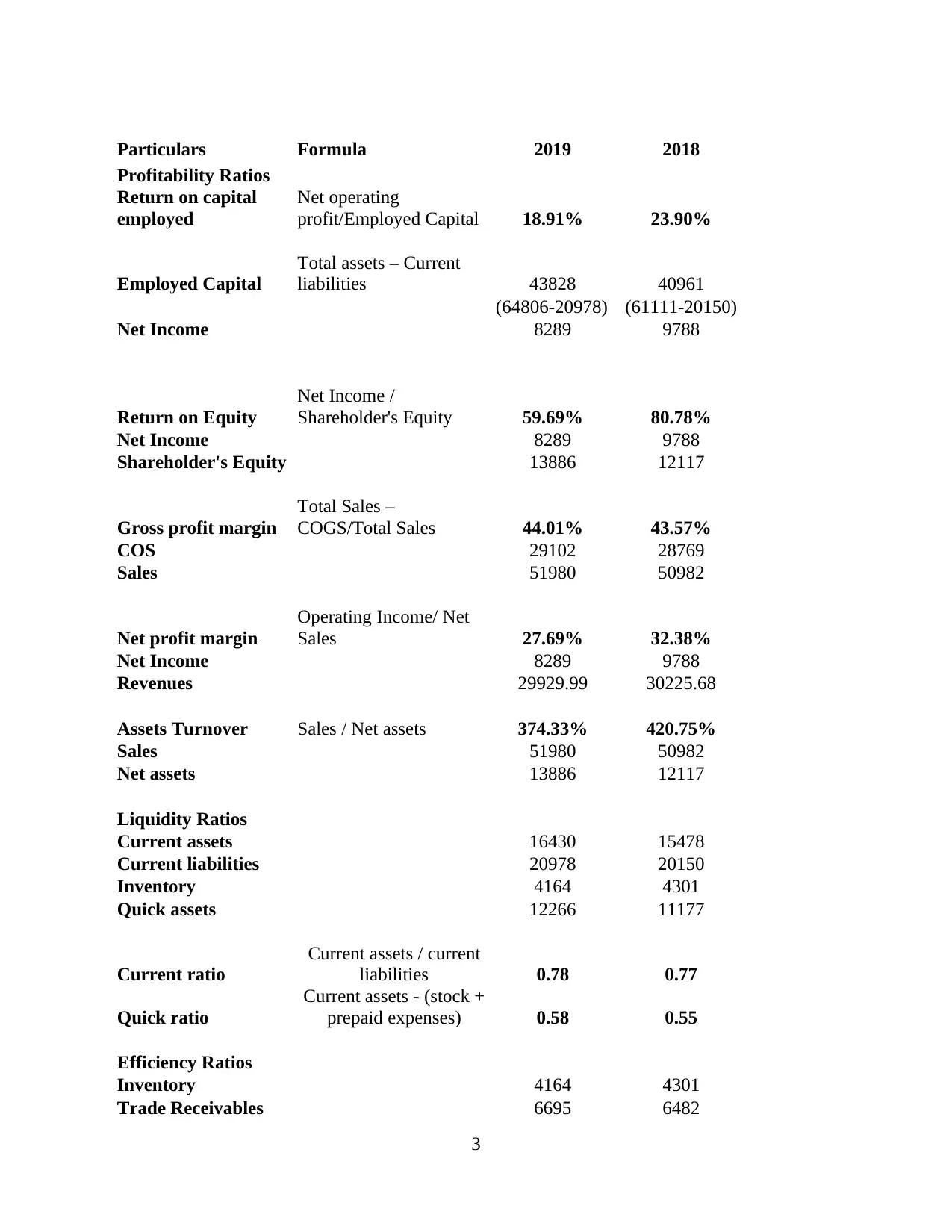

Particulars Formula 2019 2018

Profitability Ratios

Return on capital

employed

Net operating

profit/Employed Capital 18.91% 23.90%

Employed Capital

Total assets – Current

liabilities 43828 40961

(64806-20978) (61111-20150)

Net Income 8289 9788

Return on Equity

Net Income /

Shareholder's Equity 59.69% 80.78%

Net Income 8289 9788

Shareholder's Equity 13886 12117

Gross profit margin

Total Sales –

COGS/Total Sales 44.01% 43.57%

COS 29102 28769

Sales 51980 50982

Net profit margin

Operating Income/ Net

Sales 27.69% 32.38%

Net Income 8289 9788

Revenues 29929.99 30225.68

Assets Turnover Sales / Net assets 374.33% 420.75%

Sales 51980 50982

Net assets 13886 12117

Liquidity Ratios

Current assets 16430 15478

Current liabilities 20978 20150

Inventory 4164 4301

Quick assets 12266 11177

Current ratio

Current assets / current

liabilities 0.78 0.77

Quick ratio

Current assets - (stock +

prepaid expenses) 0.58 0.55

Efficiency Ratios

Inventory 4164 4301

Trade Receivables 6695 6482

3

Profitability Ratios

Return on capital

employed

Net operating

profit/Employed Capital 18.91% 23.90%

Employed Capital

Total assets – Current

liabilities 43828 40961

(64806-20978) (61111-20150)

Net Income 8289 9788

Return on Equity

Net Income /

Shareholder's Equity 59.69% 80.78%

Net Income 8289 9788

Shareholder's Equity 13886 12117

Gross profit margin

Total Sales –

COGS/Total Sales 44.01% 43.57%

COS 29102 28769

Sales 51980 50982

Net profit margin

Operating Income/ Net

Sales 27.69% 32.38%

Net Income 8289 9788

Revenues 29929.99 30225.68

Assets Turnover Sales / Net assets 374.33% 420.75%

Sales 51980 50982

Net assets 13886 12117

Liquidity Ratios

Current assets 16430 15478

Current liabilities 20978 20150

Inventory 4164 4301

Quick assets 12266 11177

Current ratio

Current assets / current

liabilities 0.78 0.77

Quick ratio

Current assets - (stock +

prepaid expenses) 0.58 0.55

Efficiency Ratios

Inventory 4164 4301

Trade Receivables 6695 6482

3

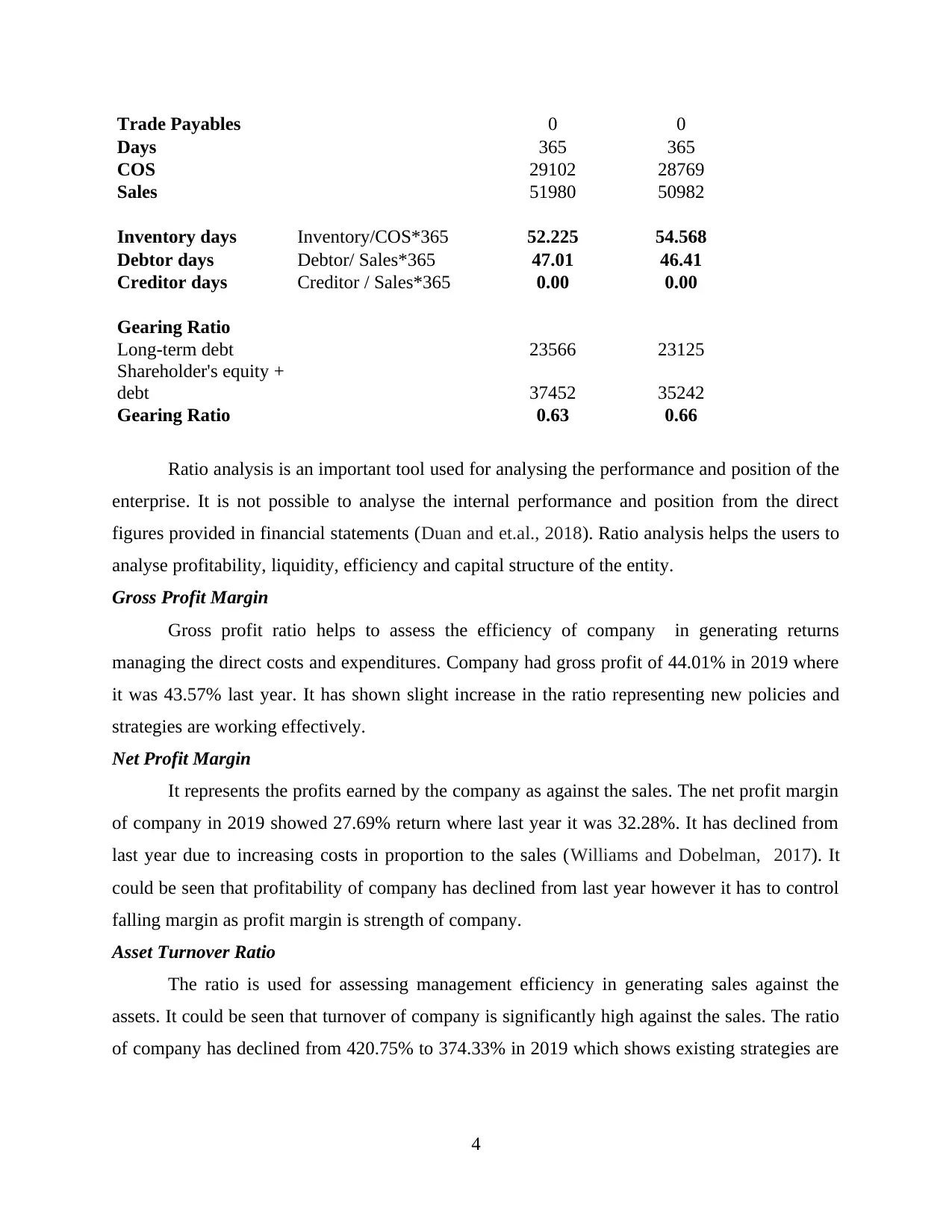

Trade Payables 0 0

Days 365 365

COS 29102 28769

Sales 51980 50982

Inventory days Inventory/COS*365 52.225 54.568

Debtor days Debtor/ Sales*365 47.01 46.41

Creditor days Creditor / Sales*365 0.00 0.00

Gearing Ratio

Long-term debt 23566 23125

Shareholder's equity +

debt 37452 35242

Gearing Ratio 0.63 0.66

Ratio analysis is an important tool used for analysing the performance and position of the

enterprise. It is not possible to analyse the internal performance and position from the direct

figures provided in financial statements (Duan and et.al., 2018). Ratio analysis helps the users to

analyse profitability, liquidity, efficiency and capital structure of the entity.

Gross Profit Margin

Gross profit ratio helps to assess the efficiency of company in generating returns

managing the direct costs and expenditures. Company had gross profit of 44.01% in 2019 where

it was 43.57% last year. It has shown slight increase in the ratio representing new policies and

strategies are working effectively.

Net Profit Margin

It represents the profits earned by the company as against the sales. The net profit margin

of company in 2019 showed 27.69% return where last year it was 32.28%. It has declined from

last year due to increasing costs in proportion to the sales (Williams and Dobelman, 2017). It

could be seen that profitability of company has declined from last year however it has to control

falling margin as profit margin is strength of company.

Asset Turnover Ratio

The ratio is used for assessing management efficiency in generating sales against the

assets. It could be seen that turnover of company is significantly high against the sales. The ratio

of company has declined from 420.75% to 374.33% in 2019 which shows existing strategies are

4

Days 365 365

COS 29102 28769

Sales 51980 50982

Inventory days Inventory/COS*365 52.225 54.568

Debtor days Debtor/ Sales*365 47.01 46.41

Creditor days Creditor / Sales*365 0.00 0.00

Gearing Ratio

Long-term debt 23566 23125

Shareholder's equity +

debt 37452 35242

Gearing Ratio 0.63 0.66

Ratio analysis is an important tool used for analysing the performance and position of the

enterprise. It is not possible to analyse the internal performance and position from the direct

figures provided in financial statements (Duan and et.al., 2018). Ratio analysis helps the users to

analyse profitability, liquidity, efficiency and capital structure of the entity.

Gross Profit Margin

Gross profit ratio helps to assess the efficiency of company in generating returns

managing the direct costs and expenditures. Company had gross profit of 44.01% in 2019 where

it was 43.57% last year. It has shown slight increase in the ratio representing new policies and

strategies are working effectively.

Net Profit Margin

It represents the profits earned by the company as against the sales. The net profit margin

of company in 2019 showed 27.69% return where last year it was 32.28%. It has declined from

last year due to increasing costs in proportion to the sales (Williams and Dobelman, 2017). It

could be seen that profitability of company has declined from last year however it has to control

falling margin as profit margin is strength of company.

Asset Turnover Ratio

The ratio is used for assessing management efficiency in generating sales against the

assets. It could be seen that turnover of company is significantly high against the sales. The ratio

of company has declined from 420.75% to 374.33% in 2019 which shows existing strategies are

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not effective and management is required to take actions for increasing turnover. However as per

the industry trends asset turnover is high which is strength of management.

Current Ratio

The ability of company in meeting the short term obligations is assessed using current

ratio. Current ratio is 0.78 in 2019 where it was 0.77 in 2018. It could be analysed that current

ratio is below 1 which means it will not be meet the short term liabilities from the current assets.

The liquidity position is significantly lower that could lead the company to borrow high loans to

meet working capital requirements.

Gearing Ratio

Company is having gearing ratio of 0.63 in 2019 which represents company is having

63% of debt in total capital structure which is higher. Company needs to control the increasing

debt by taking corrective measures to reduce the financial risks.

Debtor Days

Debtor days of company are adequate at 47 days which shows that collection from the

debtors is made quickly for managing the cash cycle (Monahan, 2018). The management is

efficient in managing the operating cycle for meeting the working capital requirements.

It could be analysed that company has highly adequate profitability, efficiency ratios are

also adequate however the liquidity position is very weak that could impact the long term growth

of business if not fixed on immediate basis.

Limitations of ratio analysis are that it only uses quantitative data and does not consider

qualitative aspects that are influencing the organisation.

TASK 3

Approaches to production of budget with reference to financial constraints, achievement of the

organisational targets, accounting conventions and the legal requirements.

Financial plan of the company is known as the budget. It is an effective tool used by the

organisations for planning and controlling. Budget is prepared in the planning stage by

management for properly allocating the resources after analysing the previous budgets and trends

that will best meet the goals and objectives. Management have different approaches to budget

considering different factors. Unilever uses the below stated production approaches for preparing

budgets to effectively all the requirements of the budgets including meeting organisational

targets, meeting the legal requirements and accounting conventions.

5

the industry trends asset turnover is high which is strength of management.

Current Ratio

The ability of company in meeting the short term obligations is assessed using current

ratio. Current ratio is 0.78 in 2019 where it was 0.77 in 2018. It could be analysed that current

ratio is below 1 which means it will not be meet the short term liabilities from the current assets.

The liquidity position is significantly lower that could lead the company to borrow high loans to

meet working capital requirements.

Gearing Ratio

Company is having gearing ratio of 0.63 in 2019 which represents company is having

63% of debt in total capital structure which is higher. Company needs to control the increasing

debt by taking corrective measures to reduce the financial risks.

Debtor Days

Debtor days of company are adequate at 47 days which shows that collection from the

debtors is made quickly for managing the cash cycle (Monahan, 2018). The management is

efficient in managing the operating cycle for meeting the working capital requirements.

It could be analysed that company has highly adequate profitability, efficiency ratios are

also adequate however the liquidity position is very weak that could impact the long term growth

of business if not fixed on immediate basis.

Limitations of ratio analysis are that it only uses quantitative data and does not consider

qualitative aspects that are influencing the organisation.

TASK 3

Approaches to production of budget with reference to financial constraints, achievement of the

organisational targets, accounting conventions and the legal requirements.

Financial plan of the company is known as the budget. It is an effective tool used by the

organisations for planning and controlling. Budget is prepared in the planning stage by

management for properly allocating the resources after analysing the previous budgets and trends

that will best meet the goals and objectives. Management have different approaches to budget

considering different factors. Unilever uses the below stated production approaches for preparing

budgets to effectively all the requirements of the budgets including meeting organisational

targets, meeting the legal requirements and accounting conventions.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Input/Output Approach

The approach is used for budgeting physical costs and inputs as function of the planned

activities at unit level. The approach is also used for merchandising, service, distribution and

manufacturing activities which are having defined relationship between efforts and

accomplishment. Budget inputs are function of planned output (Das and Pandit, 2020). The

approach starts with planned output and work backward to budget inputs. Drawback of approach

is that there is difficulty in using approach for the costs not responding to the changes in the unit

level drivers of cost. The method is used by Unilever in distribution activities by analysing the

supplies and demand of the previous years and of different regions.

Activity Based Approach

It is similar to input/output method but reduces distortion in transformation by emphasis

on expected costs planned activities that are consumed for the processes, products, services or

budget objective. Amount of every activity cost driver which is used by budget objective is

multiplied and determined by cost per unit of activity cost drivers like assembly line set-ups or

inspections. The approach is used by Unilever for estimating cost of products and services based

over cost drivers. It also sometimes uses traditional volume based drivers like like labour hours

or direct material consumption (Karaömer and Özbirecikli, 2019). Company is performing

number of activities and operations and activity based budgeting plays critical role in allocating

the resources of organisation.

Incremental Budget

It costs for coming period as pound change or percentage change from amount budgeted

for the previous period. The approach is used often when relationship between the outputs and

inputs are non-existent or weak. For instance, when it is difficult for Unilever to setup clear

relation between the sales and advertising expenses. Consequently budget amount for

advertisement in future period is based over actual or budgeted expenses in previous period.

Suppose expenditure for last year were 20000 the budgeted expense for next year will be with

some increment percentage. Management will take 20000 as base and pay attention over

justifying the increment. The approach is used where there is no or very slight fluctuations in the

items from previous year (Talmon and Faliszewski, 2019). However the approach considers all

the expenditures and items such as taxes or other expenditures and also helps company in

tracking the variances between budgeted and actuals outcomes.

6

The approach is used for budgeting physical costs and inputs as function of the planned

activities at unit level. The approach is also used for merchandising, service, distribution and

manufacturing activities which are having defined relationship between efforts and

accomplishment. Budget inputs are function of planned output (Das and Pandit, 2020). The

approach starts with planned output and work backward to budget inputs. Drawback of approach

is that there is difficulty in using approach for the costs not responding to the changes in the unit

level drivers of cost. The method is used by Unilever in distribution activities by analysing the

supplies and demand of the previous years and of different regions.

Activity Based Approach

It is similar to input/output method but reduces distortion in transformation by emphasis

on expected costs planned activities that are consumed for the processes, products, services or

budget objective. Amount of every activity cost driver which is used by budget objective is

multiplied and determined by cost per unit of activity cost drivers like assembly line set-ups or

inspections. The approach is used by Unilever for estimating cost of products and services based

over cost drivers. It also sometimes uses traditional volume based drivers like like labour hours

or direct material consumption (Karaömer and Özbirecikli, 2019). Company is performing

number of activities and operations and activity based budgeting plays critical role in allocating

the resources of organisation.

Incremental Budget

It costs for coming period as pound change or percentage change from amount budgeted

for the previous period. The approach is used often when relationship between the outputs and

inputs are non-existent or weak. For instance, when it is difficult for Unilever to setup clear

relation between the sales and advertising expenses. Consequently budget amount for

advertisement in future period is based over actual or budgeted expenses in previous period.

Suppose expenditure for last year were 20000 the budgeted expense for next year will be with

some increment percentage. Management will take 20000 as base and pay attention over

justifying the increment. The approach is used where there is no or very slight fluctuations in the

items from previous year (Talmon and Faliszewski, 2019). However the approach considers all

the expenditures and items such as taxes or other expenditures and also helps company in

tracking the variances between budgeted and actuals outcomes.

6

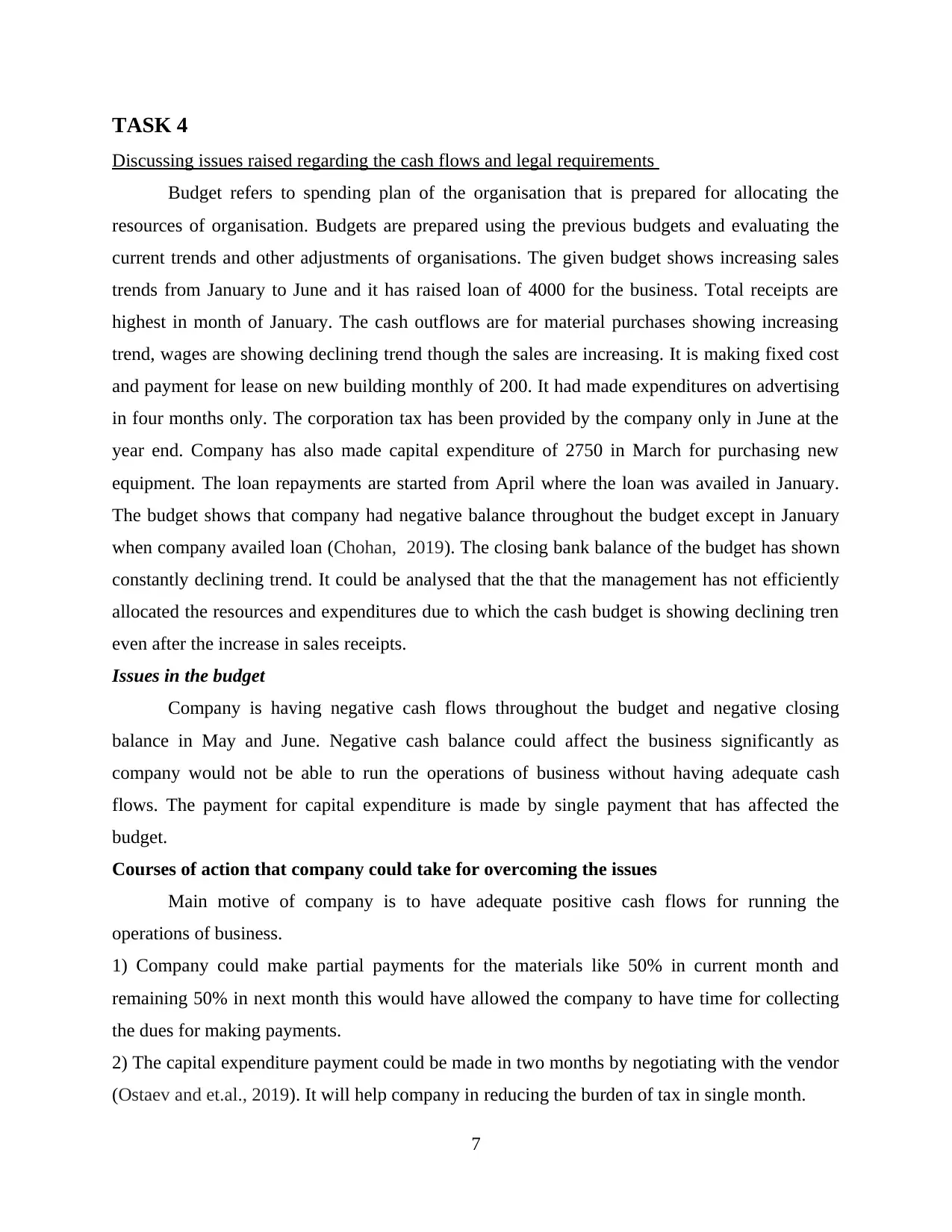

TASK 4

Discussing issues raised regarding the cash flows and legal requirements

Budget refers to spending plan of the organisation that is prepared for allocating the

resources of organisation. Budgets are prepared using the previous budgets and evaluating the

current trends and other adjustments of organisations. The given budget shows increasing sales

trends from January to June and it has raised loan of 4000 for the business. Total receipts are

highest in month of January. The cash outflows are for material purchases showing increasing

trend, wages are showing declining trend though the sales are increasing. It is making fixed cost

and payment for lease on new building monthly of 200. It had made expenditures on advertising

in four months only. The corporation tax has been provided by the company only in June at the

year end. Company has also made capital expenditure of 2750 in March for purchasing new

equipment. The loan repayments are started from April where the loan was availed in January.

The budget shows that company had negative balance throughout the budget except in January

when company availed loan (Chohan, 2019). The closing bank balance of the budget has shown

constantly declining trend. It could be analysed that the that the management has not efficiently

allocated the resources and expenditures due to which the cash budget is showing declining tren

even after the increase in sales receipts.

Issues in the budget

Company is having negative cash flows throughout the budget and negative closing

balance in May and June. Negative cash balance could affect the business significantly as

company would not be able to run the operations of business without having adequate cash

flows. The payment for capital expenditure is made by single payment that has affected the

budget.

Courses of action that company could take for overcoming the issues

Main motive of company is to have adequate positive cash flows for running the

operations of business.

1) Company could make partial payments for the materials like 50% in current month and

remaining 50% in next month this would have allowed the company to have time for collecting

the dues for making payments.

2) The capital expenditure payment could be made in two months by negotiating with the vendor

(Ostaev and et.al., 2019). It will help company in reducing the burden of tax in single month.

7

Discussing issues raised regarding the cash flows and legal requirements

Budget refers to spending plan of the organisation that is prepared for allocating the

resources of organisation. Budgets are prepared using the previous budgets and evaluating the

current trends and other adjustments of organisations. The given budget shows increasing sales

trends from January to June and it has raised loan of 4000 for the business. Total receipts are

highest in month of January. The cash outflows are for material purchases showing increasing

trend, wages are showing declining trend though the sales are increasing. It is making fixed cost

and payment for lease on new building monthly of 200. It had made expenditures on advertising

in four months only. The corporation tax has been provided by the company only in June at the

year end. Company has also made capital expenditure of 2750 in March for purchasing new

equipment. The loan repayments are started from April where the loan was availed in January.

The budget shows that company had negative balance throughout the budget except in January

when company availed loan (Chohan, 2019). The closing bank balance of the budget has shown

constantly declining trend. It could be analysed that the that the management has not efficiently

allocated the resources and expenditures due to which the cash budget is showing declining tren

even after the increase in sales receipts.

Issues in the budget

Company is having negative cash flows throughout the budget and negative closing

balance in May and June. Negative cash balance could affect the business significantly as

company would not be able to run the operations of business without having adequate cash

flows. The payment for capital expenditure is made by single payment that has affected the

budget.

Courses of action that company could take for overcoming the issues

Main motive of company is to have adequate positive cash flows for running the

operations of business.

1) Company could make partial payments for the materials like 50% in current month and

remaining 50% in next month this would have allowed the company to have time for collecting

the dues for making payments.

2) The capital expenditure payment could be made in two months by negotiating with the vendor

(Ostaev and et.al., 2019). It will help company in reducing the burden of tax in single month.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3) It could reduce the advertisement expenditure for continuous month and can make expenses in

alternate months in February and April for reducing the negative cash balance.

The below budget shows the manner in which company could adjust the budgets for

reducing the negative balance.

Task 4

exercise: Jan Feb March April May June

Receipts: £0.00 £0.00 £0.00 £0.00 £0.00 £0.00

Sales

Receipts 2110 2156 2164 2219 2284 2444

Proceeds

from Loan 4000

Total

Receipts 6110 2156 2164 2219 2284 2444

Payments: £0.00 £0.00 £0.00 £0.00 £0.00 £0.00

Material

Purchases 359 366.5 378.5 388.5 411 440

50% in next

month 359 366.5 378.5 388.5 411

Wages 600 600 550 550 550 450

Fixed Costs 700 700 710 710 715 715

Lease of

New

Building 200 200 200 200 200

Advertising

Fees 120 120

Corporation

Tax 650

Capital

Expenditure 1375 1375

Loan

Repayment 450 450 450

Total

Payments 1659 2345.5 3580 2797 4089.5 3316

Net Cash

Flow 4451 -189.5 -1416 -578 -1805.5 -872

8

alternate months in February and April for reducing the negative cash balance.

The below budget shows the manner in which company could adjust the budgets for

reducing the negative balance.

Task 4

exercise: Jan Feb March April May June

Receipts: £0.00 £0.00 £0.00 £0.00 £0.00 £0.00

Sales

Receipts 2110 2156 2164 2219 2284 2444

Proceeds

from Loan 4000

Total

Receipts 6110 2156 2164 2219 2284 2444

Payments: £0.00 £0.00 £0.00 £0.00 £0.00 £0.00

Material

Purchases 359 366.5 378.5 388.5 411 440

50% in next

month 359 366.5 378.5 388.5 411

Wages 600 600 550 550 550 450

Fixed Costs 700 700 710 710 715 715

Lease of

New

Building 200 200 200 200 200

Advertising

Fees 120 120

Corporation

Tax 650

Capital

Expenditure 1375 1375

Loan

Repayment 450 450 450

Total

Payments 1659 2345.5 3580 2797 4089.5 3316

Net Cash

Flow 4451 -189.5 -1416 -578 -1805.5 -872

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Opening

Bank

Balance 185 4636 4446.5 3030.5 2452.5 647

Closing

Bank

Balance 4636 4446.5 3030.5 2452.5 647 -225

TASK 5

Methods of capital investments and reasons why it is essential for organisation to develop capital

expenditure policies.

There are different techniques that are used in the capital budgeting.

Net Present Value

This is a metric used in capital budgeting for evaluating the profitability of proposed

capital expenditures. It assess whether the estimated future cash flows would be enough for

meeting the cost of project or not.

Payback Period

It is the metric used for evaluating the time period within which the costs will be

recovered of the project. It is also used for evaluating the break even point of the project after

which it will be able to earn profits.

Importance of capital expenditure policies

The policies regarding capital expenditures is essential as companies are required to

maintain the existing equipments and property while investing in the new technology and assets

for growth. Policies provide frameworks about the procedure to be followed for making capital

expenditures (Kengatharan and Clamenthu, 2017). As it involves considerable investments

companies make investments after properly analysing the viability of expenditure.

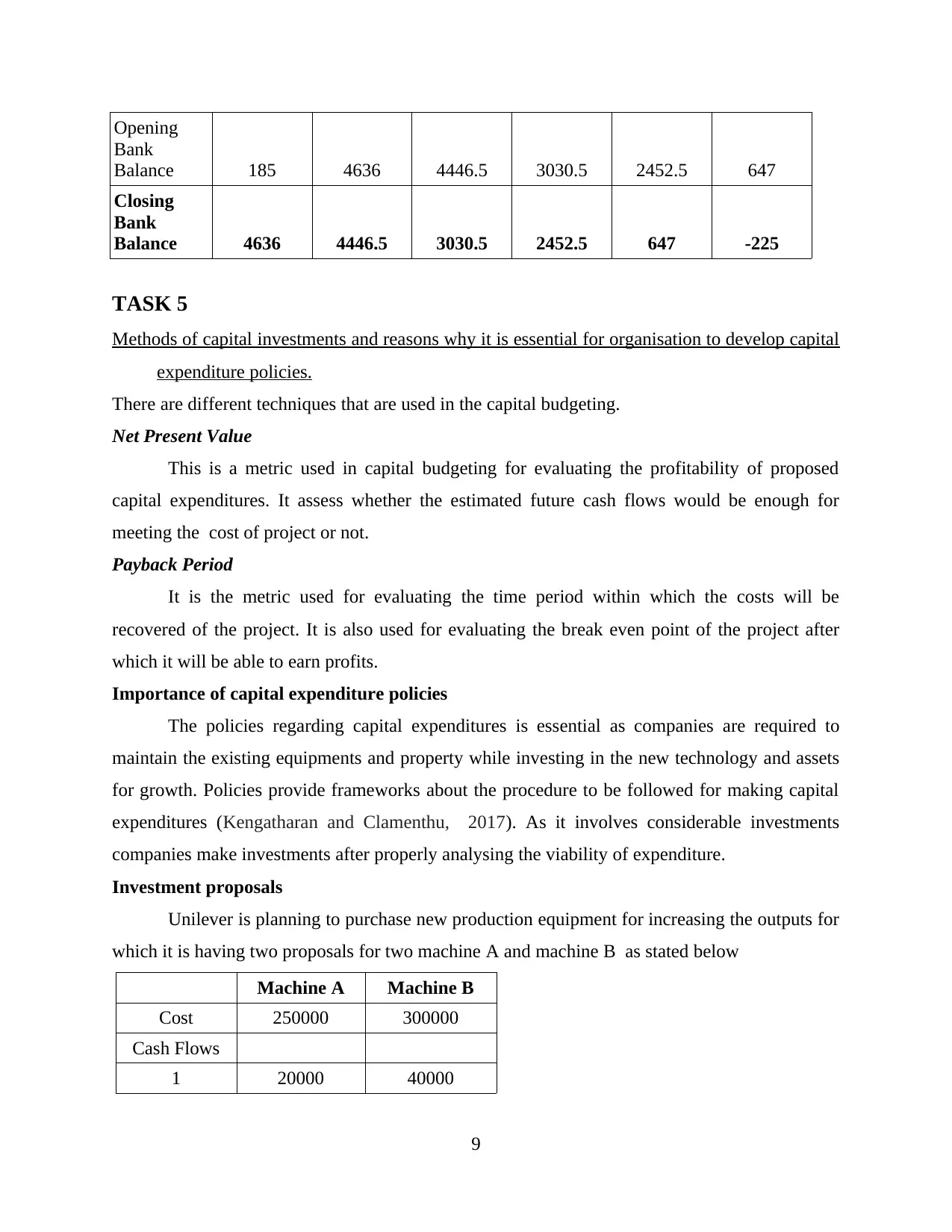

Investment proposals

Unilever is planning to purchase new production equipment for increasing the outputs for

which it is having two proposals for two machine A and machine B as stated below

Machine A Machine B

Cost 250000 300000

Cash Flows

1 20000 40000

9

Bank

Balance 185 4636 4446.5 3030.5 2452.5 647

Closing

Bank

Balance 4636 4446.5 3030.5 2452.5 647 -225

TASK 5

Methods of capital investments and reasons why it is essential for organisation to develop capital

expenditure policies.

There are different techniques that are used in the capital budgeting.

Net Present Value

This is a metric used in capital budgeting for evaluating the profitability of proposed

capital expenditures. It assess whether the estimated future cash flows would be enough for

meeting the cost of project or not.

Payback Period

It is the metric used for evaluating the time period within which the costs will be

recovered of the project. It is also used for evaluating the break even point of the project after

which it will be able to earn profits.

Importance of capital expenditure policies

The policies regarding capital expenditures is essential as companies are required to

maintain the existing equipments and property while investing in the new technology and assets

for growth. Policies provide frameworks about the procedure to be followed for making capital

expenditures (Kengatharan and Clamenthu, 2017). As it involves considerable investments

companies make investments after properly analysing the viability of expenditure.

Investment proposals

Unilever is planning to purchase new production equipment for increasing the outputs for

which it is having two proposals for two machine A and machine B as stated below

Machine A Machine B

Cost 250000 300000

Cash Flows

1 20000 40000

9

2 45000 65000

3 60000 90000

4 85000 125000

5 95000 160000

WACC :10%

Analysis

Analysing the viability of investments using investment appraisal techniques of the two

machines.

Net Present Value

Computation of NPV Computation of NPV

MACHINE A MACHINE B

Year

Cash

inflows

PV factor

@ 10%

Discounte

d cash

inflows Year

Cash

inflows

PV factor

@ 10%

Discounte

d cash

inflows

1 20000 0.909 18181.82 1 40000 0.909 36363.64

2 45000 0.826 37190 2 65000 0.826 53719

3 60000 0.751 45079 3 90000 0.751 67618

4 85000 0.683 58056 4 125000 0.683 85377

5 95000 0.621 58988 5 160000 0.621 99347

Total

discounted

cash

inflow 217494

Total

discounted

cash inflow 342425

Initial

investment 250000

Initial

investment 300000

NPV

(Total

discounted

cash

inflows -

initial

investmen

t) -32506

NPV (Total

discounted

cash inflows

- initial

investment) 42425

10

3 60000 90000

4 85000 125000

5 95000 160000

WACC :10%

Analysis

Analysing the viability of investments using investment appraisal techniques of the two

machines.

Net Present Value

Computation of NPV Computation of NPV

MACHINE A MACHINE B

Year

Cash

inflows

PV factor

@ 10%

Discounte

d cash

inflows Year

Cash

inflows

PV factor

@ 10%

Discounte

d cash

inflows

1 20000 0.909 18181.82 1 40000 0.909 36363.64

2 45000 0.826 37190 2 65000 0.826 53719

3 60000 0.751 45079 3 90000 0.751 67618

4 85000 0.683 58056 4 125000 0.683 85377

5 95000 0.621 58988 5 160000 0.621 99347

Total

discounted

cash

inflow 217494

Total

discounted

cash inflow 342425

Initial

investment 250000

Initial

investment 300000

NPV

(Total

discounted

cash

inflows -

initial

investmen

t) -32506

NPV (Total

discounted

cash inflows

- initial

investment) 42425

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.