MBL502 Finance Report: Financial Management and Investment Analysis

VerifiedAdded on 2023/01/06

|14

|3672

|70

Report

AI Summary

This report provides a comprehensive financial analysis of ABC Pty Ltd, covering key aspects of financial management. It begins with the construction of essential financial statements, including the balance sheet, profit and loss statement, and cash flow statement. The report then delves into the identification and evaluation of various sources of finance, suitable for both start-up and growing businesses, considering factors such as debt, equity, and bank loans. Furthermore, it examines depreciation methods and their impact on financial performance, calculating the firm's additional EBIT and after-tax incremental earnings over a five-year period. The analysis extends to project evaluation, including the calculation of additional free cash flows, net present value (NPV), and project evaluation measures to assess the viability of potential investments. The report aims to provide a detailed understanding of financial management principles and their application in real-world business scenarios.

MBL502, Academic Analysis

FINANCE FOR MANAGERS

1

FINANCE FOR MANAGERS

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Part - 1..............................................................................................................................................3

1.1 Constructing balance for the ABC Pty Ltd for the year ended 30 June 20220.....................3

1.2 Constructing Profit of Loss Statement for the ABC Pty Ltd for the year ended 30 June

20220...........................................................................................................................................4

1.3 Constructing Cash Flow statement for the ABC Pty Ltd for the year ended 30 June 20220 5

Part – 2.............................................................................................................................................6

2.1 Alternative sources of finance and five characteristics or features that are considered by

individual.....................................................................................................................................6

2.2 Three sources of finance that are suitable for start-up business............................................7

2.3 Three sources of finance suitable for growing- expansion firm............................................8

Part – 3.............................................................................................................................................9

3.1 Rate of diminishing value depreciation.................................................................................9

3.2 Firm’s additional EBIT in years 1 to 5 and the after tax incremental earnings.....................9

3.3 Calculating additional free cash flows in year 0 to 6.............................................................9

3.4 NPV of cash flows generated by project.............................................................................10

3.5 Project evaluation measures:...............................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION...........................................................................................................................3

Part - 1..............................................................................................................................................3

1.1 Constructing balance for the ABC Pty Ltd for the year ended 30 June 20220.....................3

1.2 Constructing Profit of Loss Statement for the ABC Pty Ltd for the year ended 30 June

20220...........................................................................................................................................4

1.3 Constructing Cash Flow statement for the ABC Pty Ltd for the year ended 30 June 20220 5

Part – 2.............................................................................................................................................6

2.1 Alternative sources of finance and five characteristics or features that are considered by

individual.....................................................................................................................................6

2.2 Three sources of finance that are suitable for start-up business............................................7

2.3 Three sources of finance suitable for growing- expansion firm............................................8

Part – 3.............................................................................................................................................9

3.1 Rate of diminishing value depreciation.................................................................................9

3.2 Firm’s additional EBIT in years 1 to 5 and the after tax incremental earnings.....................9

3.3 Calculating additional free cash flows in year 0 to 6.............................................................9

3.4 NPV of cash flows generated by project.............................................................................10

3.5 Project evaluation measures:...............................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

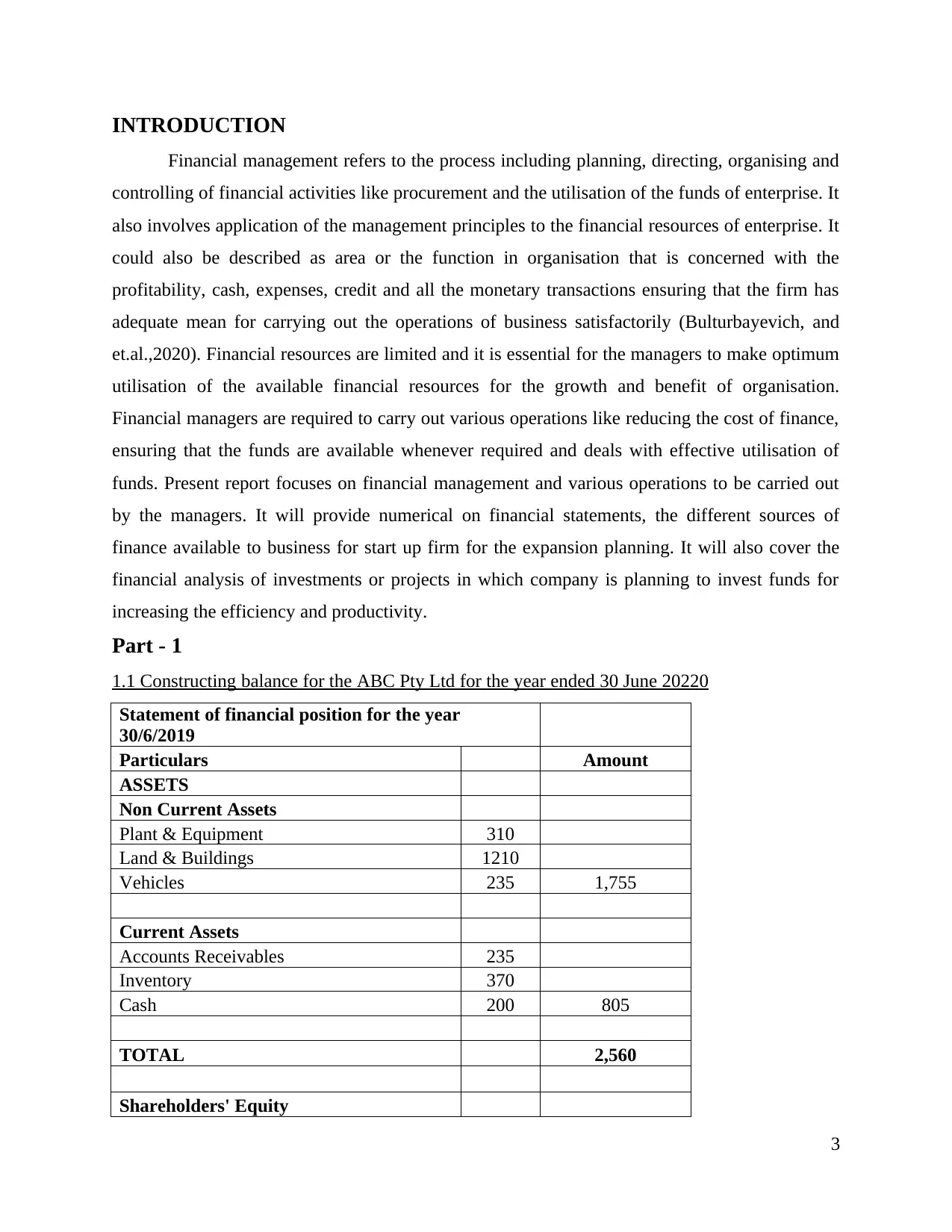

INTRODUCTION

Financial management refers to the process including planning, directing, organising and

controlling of financial activities like procurement and the utilisation of the funds of enterprise. It

also involves application of the management principles to the financial resources of enterprise. It

could also be described as area or the function in organisation that is concerned with the

profitability, cash, expenses, credit and all the monetary transactions ensuring that the firm has

adequate mean for carrying out the operations of business satisfactorily (Bulturbayevich, and

et.al.,2020). Financial resources are limited and it is essential for the managers to make optimum

utilisation of the available financial resources for the growth and benefit of organisation.

Financial managers are required to carry out various operations like reducing the cost of finance,

ensuring that the funds are available whenever required and deals with effective utilisation of

funds. Present report focuses on financial management and various operations to be carried out

by the managers. It will provide numerical on financial statements, the different sources of

finance available to business for start up firm for the expansion planning. It will also cover the

financial analysis of investments or projects in which company is planning to invest funds for

increasing the efficiency and productivity.

Part - 1

1.1 Constructing balance for the ABC Pty Ltd for the year ended 30 June 20220

Statement of financial position for the year

30/6/2019

Particulars Amount

ASSETS

Non Current Assets

Plant & Equipment 310

Land & Buildings 1210

Vehicles 235 1,755

Current Assets

Accounts Receivables 235

Inventory 370

Cash 200 805

TOTAL 2,560

Shareholders' Equity

3

Financial management refers to the process including planning, directing, organising and

controlling of financial activities like procurement and the utilisation of the funds of enterprise. It

also involves application of the management principles to the financial resources of enterprise. It

could also be described as area or the function in organisation that is concerned with the

profitability, cash, expenses, credit and all the monetary transactions ensuring that the firm has

adequate mean for carrying out the operations of business satisfactorily (Bulturbayevich, and

et.al.,2020). Financial resources are limited and it is essential for the managers to make optimum

utilisation of the available financial resources for the growth and benefit of organisation.

Financial managers are required to carry out various operations like reducing the cost of finance,

ensuring that the funds are available whenever required and deals with effective utilisation of

funds. Present report focuses on financial management and various operations to be carried out

by the managers. It will provide numerical on financial statements, the different sources of

finance available to business for start up firm for the expansion planning. It will also cover the

financial analysis of investments or projects in which company is planning to invest funds for

increasing the efficiency and productivity.

Part - 1

1.1 Constructing balance for the ABC Pty Ltd for the year ended 30 June 20220

Statement of financial position for the year

30/6/2019

Particulars Amount

ASSETS

Non Current Assets

Plant & Equipment 310

Land & Buildings 1210

Vehicles 235 1,755

Current Assets

Accounts Receivables 235

Inventory 370

Cash 200 805

TOTAL 2,560

Shareholders' Equity

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

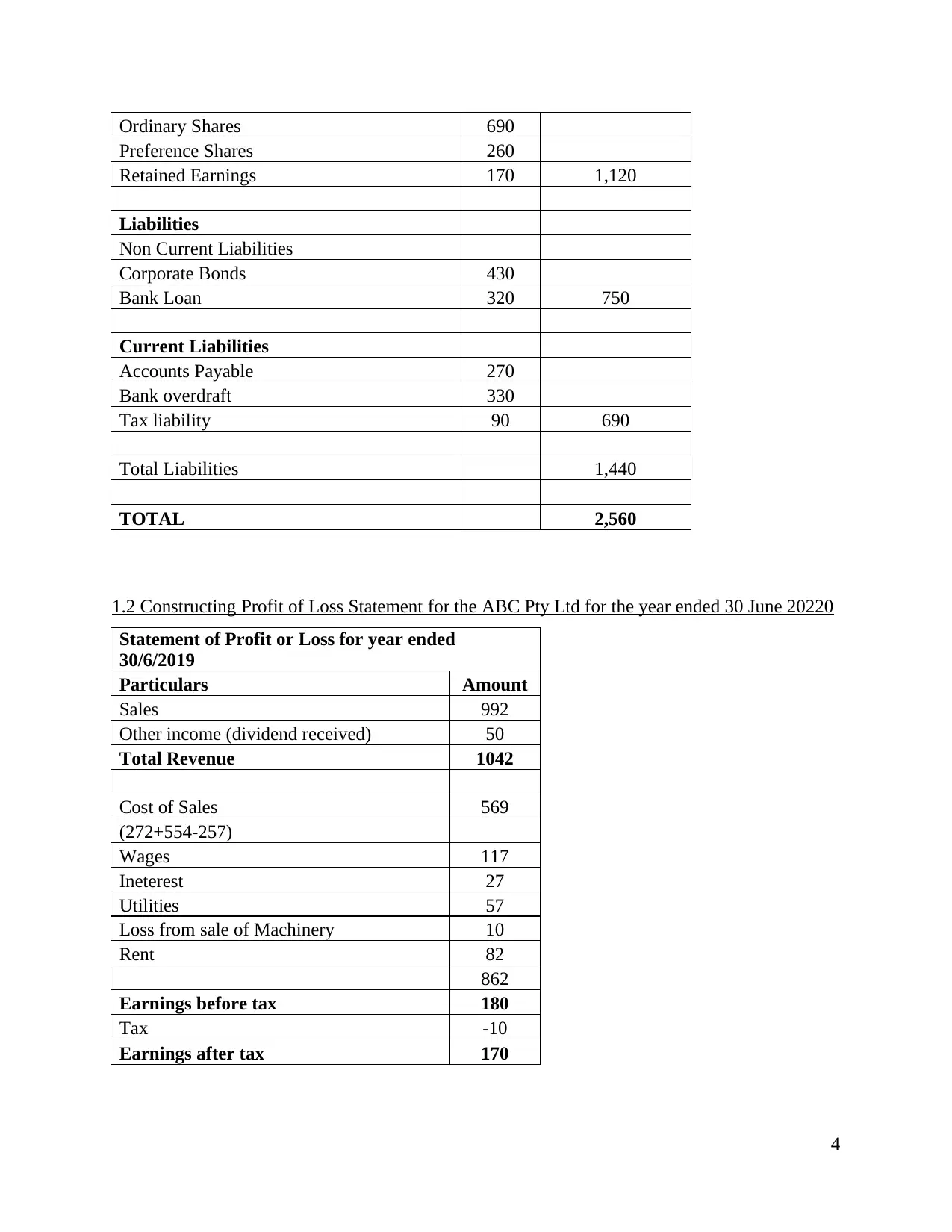

Ordinary Shares 690

Preference Shares 260

Retained Earnings 170 1,120

Liabilities

Non Current Liabilities

Corporate Bonds 430

Bank Loan 320 750

Current Liabilities

Accounts Payable 270

Bank overdraft 330

Tax liability 90 690

Total Liabilities 1,440

TOTAL 2,560

1.2 Constructing Profit of Loss Statement for the ABC Pty Ltd for the year ended 30 June 20220

Statement of Profit or Loss for year ended

30/6/2019

Particulars Amount

Sales 992

Other income (dividend received) 50

Total Revenue 1042

Cost of Sales 569

(272+554-257)

Wages 117

Ineterest 27

Utilities 57

Loss from sale of Machinery 10

Rent 82

862

Earnings before tax 180

Tax -10

Earnings after tax 170

4

Preference Shares 260

Retained Earnings 170 1,120

Liabilities

Non Current Liabilities

Corporate Bonds 430

Bank Loan 320 750

Current Liabilities

Accounts Payable 270

Bank overdraft 330

Tax liability 90 690

Total Liabilities 1,440

TOTAL 2,560

1.2 Constructing Profit of Loss Statement for the ABC Pty Ltd for the year ended 30 June 20220

Statement of Profit or Loss for year ended

30/6/2019

Particulars Amount

Sales 992

Other income (dividend received) 50

Total Revenue 1042

Cost of Sales 569

(272+554-257)

Wages 117

Ineterest 27

Utilities 57

Loss from sale of Machinery 10

Rent 82

862

Earnings before tax 180

Tax -10

Earnings after tax 170

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

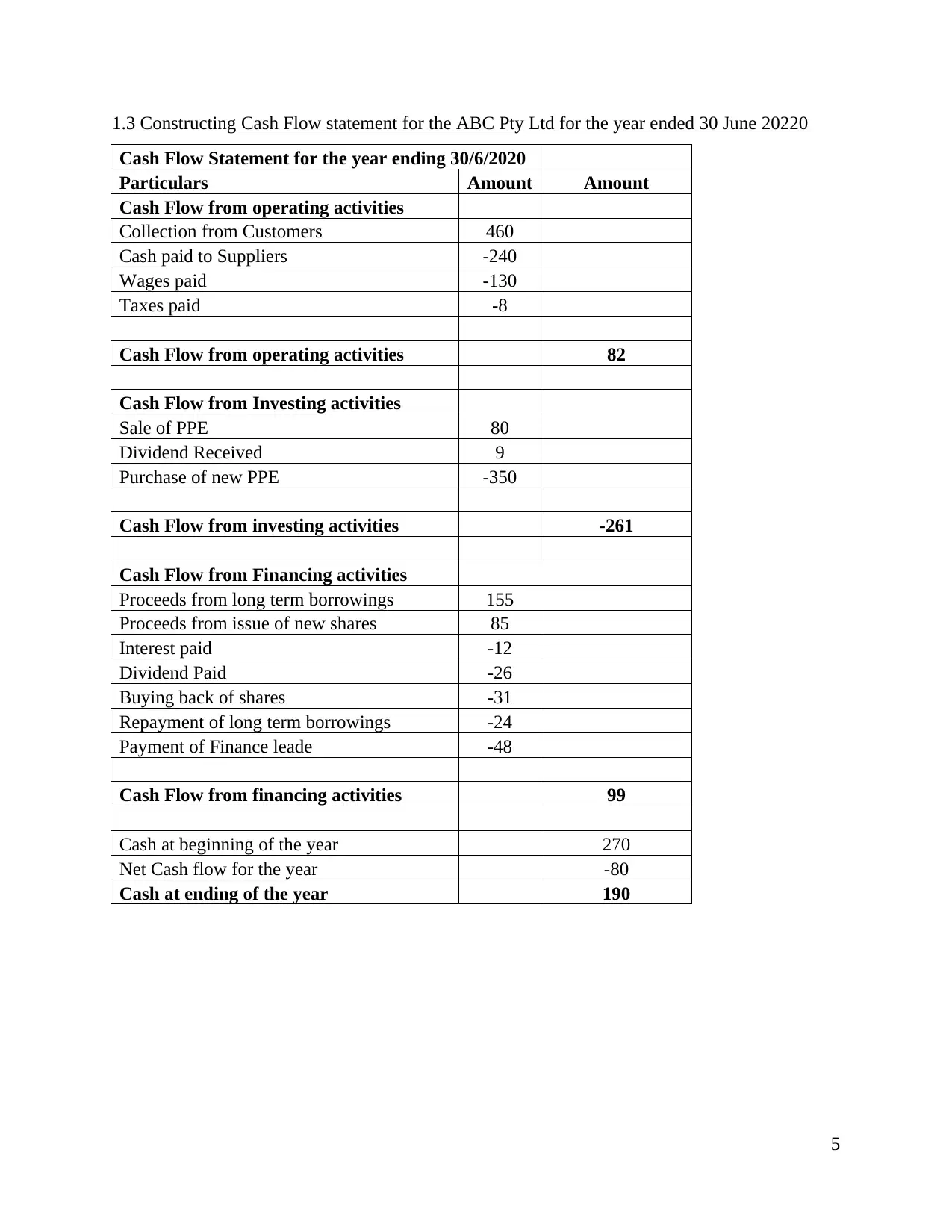

1.3 Constructing Cash Flow statement for the ABC Pty Ltd for the year ended 30 June 20220

Cash Flow Statement for the year ending 30/6/2020

Particulars Amount Amount

Cash Flow from operating activities

Collection from Customers 460

Cash paid to Suppliers -240

Wages paid -130

Taxes paid -8

Cash Flow from operating activities 82

Cash Flow from Investing activities

Sale of PPE 80

Dividend Received 9

Purchase of new PPE -350

Cash Flow from investing activities -261

Cash Flow from Financing activities

Proceeds from long term borrowings 155

Proceeds from issue of new shares 85

Interest paid -12

Dividend Paid -26

Buying back of shares -31

Repayment of long term borrowings -24

Payment of Finance leade -48

Cash Flow from financing activities 99

Cash at beginning of the year 270

Net Cash flow for the year -80

Cash at ending of the year 190

5

Cash Flow Statement for the year ending 30/6/2020

Particulars Amount Amount

Cash Flow from operating activities

Collection from Customers 460

Cash paid to Suppliers -240

Wages paid -130

Taxes paid -8

Cash Flow from operating activities 82

Cash Flow from Investing activities

Sale of PPE 80

Dividend Received 9

Purchase of new PPE -350

Cash Flow from investing activities -261

Cash Flow from Financing activities

Proceeds from long term borrowings 155

Proceeds from issue of new shares 85

Interest paid -12

Dividend Paid -26

Buying back of shares -31

Repayment of long term borrowings -24

Payment of Finance leade -48

Cash Flow from financing activities 99

Cash at beginning of the year 270

Net Cash flow for the year -80

Cash at ending of the year 190

5

Part – 2

2.1 Alternative sources of finance and five characteristics or features that are considered by

individual

Company requires finance or capital in order to establish and expand business operation

so that it can enjoy huge amount of profit margin and market share. Manager is responsible for

identifying, evaluating and analysing various alternative sources from which finance can be

raised so that company can meet its requirements. There are number of sources of finance for

business such as debt, equity, debentures, retained earnings, loan from banks and venture

funding (Kumar, 2016). All these sources of fund can be further classified on several basis

control, ownership and time period for which they are needed in firm. Some of the sources of

finance available for business are discussed below:

Debt: In this sources of finance, owner of business have to repay the amount of capital borrowed

along with specific interest. There are some benefits of raising finance through debt source such

as ownership does not dilute and it also deducts company tax return.

Equity: It is another source of finance in which owner have to give control of business to

shareholders in order to get sum of money for establishment and growth of enterprise. Thus, it

often needs to consult investors before deciding to make investment so that they can get

maximum return.

Loan from banks: There are number of financial institution that offers loans to business so that

they can run their operation effectively thus in return charge specific amount of interest. The

biggest limitation with this type of sources is that various formalities, rules and regulation need

to be abide in order to get loan (Nso, 2020). Thus, in short it can be termed as money that is not

paid to shareholders instead re-invested in business for its expansion.

Five features/ characteristics need to be considered while selecting of sources of finance

There are different features or characteristics that are considered by individual or

manager of firm while choosing specific sources of fund for business. Such as:

Scale of business operation: Amount of finance required depends upon scale of operation, its

existing capabilities and objectives. Such as if company have large scale operation that it have to

6

2.1 Alternative sources of finance and five characteristics or features that are considered by

individual

Company requires finance or capital in order to establish and expand business operation

so that it can enjoy huge amount of profit margin and market share. Manager is responsible for

identifying, evaluating and analysing various alternative sources from which finance can be

raised so that company can meet its requirements. There are number of sources of finance for

business such as debt, equity, debentures, retained earnings, loan from banks and venture

funding (Kumar, 2016). All these sources of fund can be further classified on several basis

control, ownership and time period for which they are needed in firm. Some of the sources of

finance available for business are discussed below:

Debt: In this sources of finance, owner of business have to repay the amount of capital borrowed

along with specific interest. There are some benefits of raising finance through debt source such

as ownership does not dilute and it also deducts company tax return.

Equity: It is another source of finance in which owner have to give control of business to

shareholders in order to get sum of money for establishment and growth of enterprise. Thus, it

often needs to consult investors before deciding to make investment so that they can get

maximum return.

Loan from banks: There are number of financial institution that offers loans to business so that

they can run their operation effectively thus in return charge specific amount of interest. The

biggest limitation with this type of sources is that various formalities, rules and regulation need

to be abide in order to get loan (Nso, 2020). Thus, in short it can be termed as money that is not

paid to shareholders instead re-invested in business for its expansion.

Five features/ characteristics need to be considered while selecting of sources of finance

There are different features or characteristics that are considered by individual or

manager of firm while choosing specific sources of fund for business. Such as:

Scale of business operation: Amount of finance required depends upon scale of operation, its

existing capabilities and objectives. Such as if company have large scale operation that it have to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

select debt and equity whereas in case of small, personal saving and borrowing form friend is

suitable.

Type of expenditure and amount required: Amount of capital required mainly depends upon

type of expenditure business wants to do such as long (building or purchase of machinery)and

short term (rent). Thus, it helps manager in selecting best sources of fund that can be used for

particular expenditure (Lé and Vinas, 2019).

Repayment terms: One of the key features that is considered by manager while selecting

particular sources of fund is repayment terms. Thereby, it means how often payment need to be

paid and in which quantity or amount at specific period. This feature is important as it help

manager in understanding at which time, amount company have to return borrowed capital.

Requirements: There are several requirements that need to be fulfilled by company while

borrowing fund from different sources such as credit score requirements and financial ratio test.

Therefore, manager is able to understand and evaluates best alternative sources of finances that it

can use for operation of business.

Interest and fee structure: Decision of selecting of particular financial sources also depends

upon interest rates and fee structure related to sources of funds. Thus, it is able to know actual

cost company have to incur in order to use particular finances for fulfilment of company

objectives (Factor need to consider when choosing a source of finance, 2019).

2.2 Three sources of finance that are suitable for start-up business

Start-up enterprises are firms that have initially started their operation with limited

products and services in order to earn sustain and earn profit. Three best suitable sources of

finances for start-up business can be stated as follows:

Personal saving: Every individual have his or her saving so it is used by owner to start and

establish business operation so that objectives can be achieved. It is one of the best and common

sources for start-up business as it does not involves high risk and requirements to get finance for

business (Top 10 sources of funding for start-up, 2019).

Bank finance: It is another best source of finance that is mostly selected by start-up business as

there are large number of financial institute that offers different financial options and interest

7

suitable.

Type of expenditure and amount required: Amount of capital required mainly depends upon

type of expenditure business wants to do such as long (building or purchase of machinery)and

short term (rent). Thus, it helps manager in selecting best sources of fund that can be used for

particular expenditure (Lé and Vinas, 2019).

Repayment terms: One of the key features that is considered by manager while selecting

particular sources of fund is repayment terms. Thereby, it means how often payment need to be

paid and in which quantity or amount at specific period. This feature is important as it help

manager in understanding at which time, amount company have to return borrowed capital.

Requirements: There are several requirements that need to be fulfilled by company while

borrowing fund from different sources such as credit score requirements and financial ratio test.

Therefore, manager is able to understand and evaluates best alternative sources of finances that it

can use for operation of business.

Interest and fee structure: Decision of selecting of particular financial sources also depends

upon interest rates and fee structure related to sources of funds. Thus, it is able to know actual

cost company have to incur in order to use particular finances for fulfilment of company

objectives (Factor need to consider when choosing a source of finance, 2019).

2.2 Three sources of finance that are suitable for start-up business

Start-up enterprises are firms that have initially started their operation with limited

products and services in order to earn sustain and earn profit. Three best suitable sources of

finances for start-up business can be stated as follows:

Personal saving: Every individual have his or her saving so it is used by owner to start and

establish business operation so that objectives can be achieved. It is one of the best and common

sources for start-up business as it does not involves high risk and requirements to get finance for

business (Top 10 sources of funding for start-up, 2019).

Bank finance: It is another best source of finance that is mostly selected by start-up business as

there are large number of financial institute that offers different financial options and interest

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rates. So, owner can select best alternative options at specific rates in order to meet its

requirements.

Cloud funding: There are numbers of innovation in external environment or more and more

people are making use of digital media to share information. In cloud funding group of people or

investors are invited to contribute their funds in business through internet. Thus, start-up

business is able to get sufficient fund within minimum cost and time.

2.3 Three sources of finance suitable for growing- expansion firm

Growing firm are enterprise that continuously innovates its products and services to cater

needs of existing as well as new customers so that company can enjoy more profit margin and

market share in industry. Therefore, best suitable sources of fund for growing/ expansion firm

can be illustrated below:

Retained earnings: Net income of business that is left after paying dividends to all stakeholders

is termed as retained earnings. Thus, company can make use of retained earnings as sources of

fund for meeting various expenses that are related to expansion of business.

Angel investors: It includes investors that are likely to spend their capital in business that have

objectives to grow and expand their business operation. These investors like to spread risk by

investing it different areas so that they can enjoy high return (Le and Vinas, 2019). It is suitable

option for growing firm as angel investors have more experienced and knowledge related to

particular industry that helps in providing guidance to business about the way it can expand.

Venture Capital: When company is planning for expansion in the new areas or regions where

the market is not much familiar companies adopt for venture capital. It is the source of funds

using which the organisations receives funds from the ventures who may be wealthy individuals

or firms that invest in companies with high growth prospects. In this source company gets

experienced knowledge and expertise of the investors that could help the organisation in

reaching their target aims and objectives. They also exercise control on the operations of

business through investment of funds in business.

Crow funding: It is another best option of raising fund for growing enterprise as it allows

business idea to spread among thousands of potential investors by several mediums or platform.

8

requirements.

Cloud funding: There are numbers of innovation in external environment or more and more

people are making use of digital media to share information. In cloud funding group of people or

investors are invited to contribute their funds in business through internet. Thus, start-up

business is able to get sufficient fund within minimum cost and time.

2.3 Three sources of finance suitable for growing- expansion firm

Growing firm are enterprise that continuously innovates its products and services to cater

needs of existing as well as new customers so that company can enjoy more profit margin and

market share in industry. Therefore, best suitable sources of fund for growing/ expansion firm

can be illustrated below:

Retained earnings: Net income of business that is left after paying dividends to all stakeholders

is termed as retained earnings. Thus, company can make use of retained earnings as sources of

fund for meeting various expenses that are related to expansion of business.

Angel investors: It includes investors that are likely to spend their capital in business that have

objectives to grow and expand their business operation. These investors like to spread risk by

investing it different areas so that they can enjoy high return (Le and Vinas, 2019). It is suitable

option for growing firm as angel investors have more experienced and knowledge related to

particular industry that helps in providing guidance to business about the way it can expand.

Venture Capital: When company is planning for expansion in the new areas or regions where

the market is not much familiar companies adopt for venture capital. It is the source of funds

using which the organisations receives funds from the ventures who may be wealthy individuals

or firms that invest in companies with high growth prospects. In this source company gets

experienced knowledge and expertise of the investors that could help the organisation in

reaching their target aims and objectives. They also exercise control on the operations of

business through investment of funds in business.

Crow funding: It is another best option of raising fund for growing enterprise as it allows

business idea to spread among thousands of potential investors by several mediums or platform.

8

Such as debt, equity that can be used by firms in order to get large amount of capital for meeting

all requirements of expansion of business.

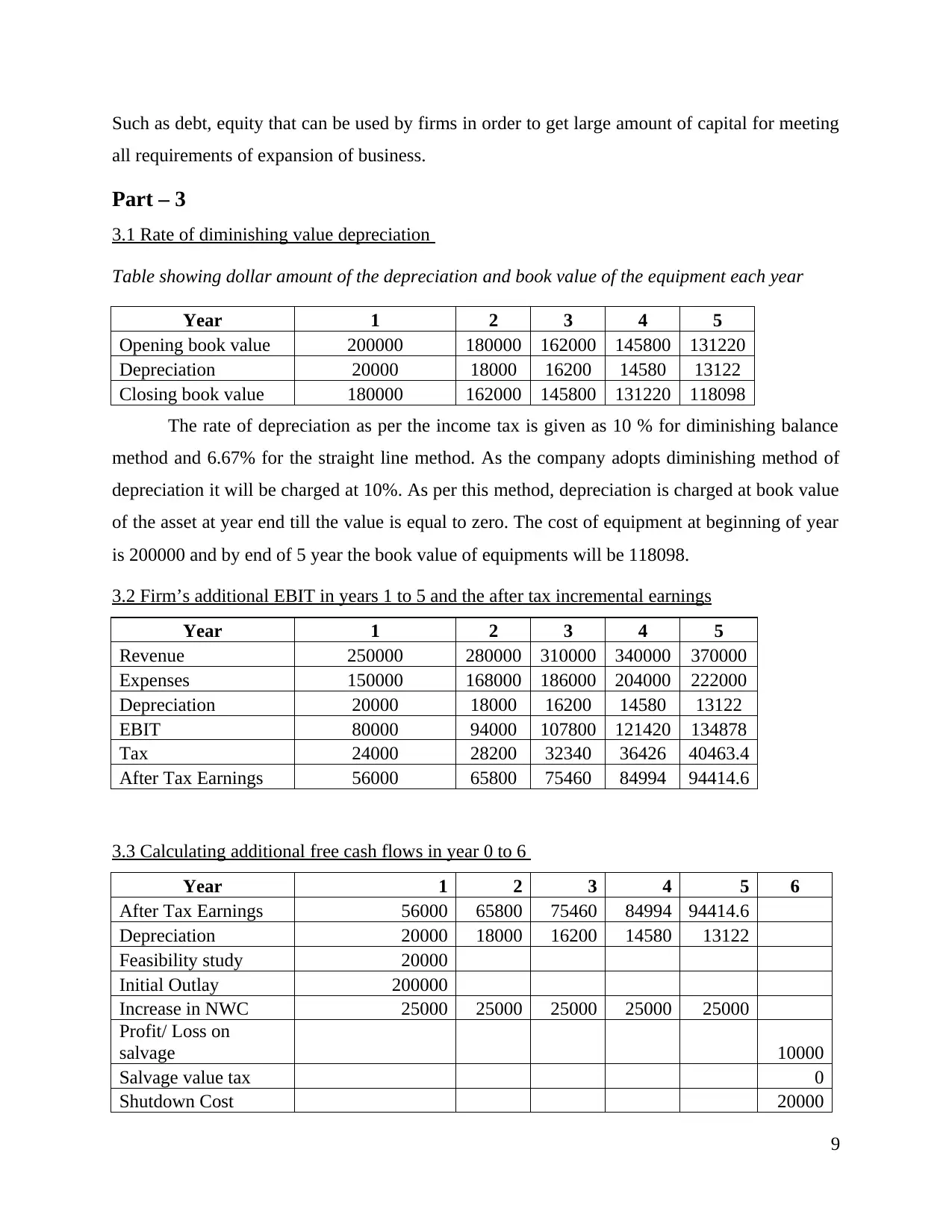

Part – 3

3.1 Rate of diminishing value depreciation

Table showing dollar amount of the depreciation and book value of the equipment each year

Year 1 2 3 4 5

Opening book value 200000 180000 162000 145800 131220

Depreciation 20000 18000 16200 14580 13122

Closing book value 180000 162000 145800 131220 118098

The rate of depreciation as per the income tax is given as 10 % for diminishing balance

method and 6.67% for the straight line method. As the company adopts diminishing method of

depreciation it will be charged at 10%. As per this method, depreciation is charged at book value

of the asset at year end till the value is equal to zero. The cost of equipment at beginning of year

is 200000 and by end of 5 year the book value of equipments will be 118098.

3.2 Firm’s additional EBIT in years 1 to 5 and the after tax incremental earnings

Year 1 2 3 4 5

Revenue 250000 280000 310000 340000 370000

Expenses 150000 168000 186000 204000 222000

Depreciation 20000 18000 16200 14580 13122

EBIT 80000 94000 107800 121420 134878

Tax 24000 28200 32340 36426 40463.4

After Tax Earnings 56000 65800 75460 84994 94414.6

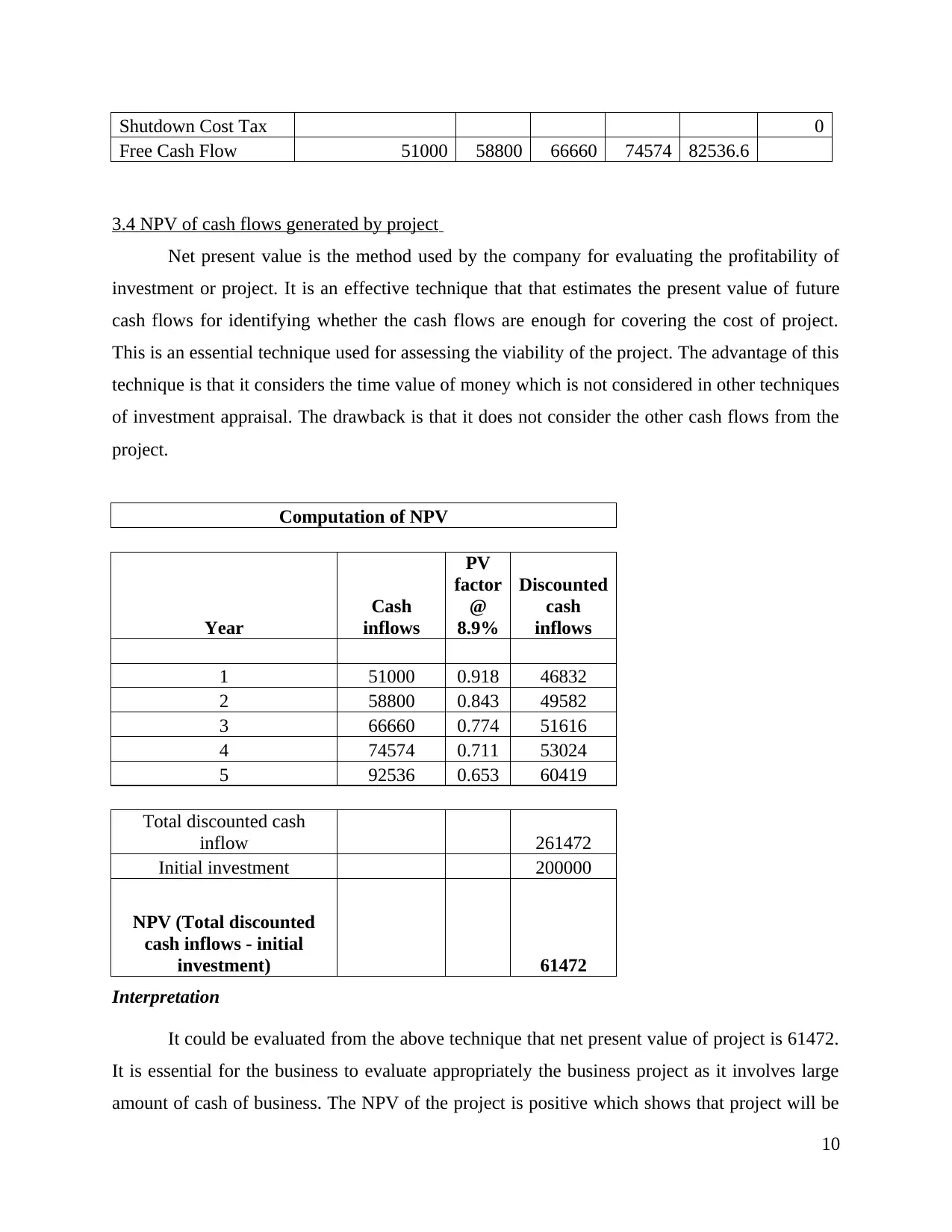

3.3 Calculating additional free cash flows in year 0 to 6

Year 1 2 3 4 5 6

After Tax Earnings 56000 65800 75460 84994 94414.6

Depreciation 20000 18000 16200 14580 13122

Feasibility study 20000

Initial Outlay 200000

Increase in NWC 25000 25000 25000 25000 25000

Profit/ Loss on

salvage 10000

Salvage value tax 0

Shutdown Cost 20000

9

all requirements of expansion of business.

Part – 3

3.1 Rate of diminishing value depreciation

Table showing dollar amount of the depreciation and book value of the equipment each year

Year 1 2 3 4 5

Opening book value 200000 180000 162000 145800 131220

Depreciation 20000 18000 16200 14580 13122

Closing book value 180000 162000 145800 131220 118098

The rate of depreciation as per the income tax is given as 10 % for diminishing balance

method and 6.67% for the straight line method. As the company adopts diminishing method of

depreciation it will be charged at 10%. As per this method, depreciation is charged at book value

of the asset at year end till the value is equal to zero. The cost of equipment at beginning of year

is 200000 and by end of 5 year the book value of equipments will be 118098.

3.2 Firm’s additional EBIT in years 1 to 5 and the after tax incremental earnings

Year 1 2 3 4 5

Revenue 250000 280000 310000 340000 370000

Expenses 150000 168000 186000 204000 222000

Depreciation 20000 18000 16200 14580 13122

EBIT 80000 94000 107800 121420 134878

Tax 24000 28200 32340 36426 40463.4

After Tax Earnings 56000 65800 75460 84994 94414.6

3.3 Calculating additional free cash flows in year 0 to 6

Year 1 2 3 4 5 6

After Tax Earnings 56000 65800 75460 84994 94414.6

Depreciation 20000 18000 16200 14580 13122

Feasibility study 20000

Initial Outlay 200000

Increase in NWC 25000 25000 25000 25000 25000

Profit/ Loss on

salvage 10000

Salvage value tax 0

Shutdown Cost 20000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shutdown Cost Tax 0

Free Cash Flow 51000 58800 66660 74574 82536.6

3.4 NPV of cash flows generated by project

Net present value is the method used by the company for evaluating the profitability of

investment or project. It is an effective technique that that estimates the present value of future

cash flows for identifying whether the cash flows are enough for covering the cost of project.

This is an essential technique used for assessing the viability of the project. The advantage of this

technique is that it considers the time value of money which is not considered in other techniques

of investment appraisal. The drawback is that it does not consider the other cash flows from the

project.

Computation of NPV

Year

Cash

inflows

PV

factor

@

8.9%

Discounted

cash

inflows

1 51000 0.918 46832

2 58800 0.843 49582

3 66660 0.774 51616

4 74574 0.711 53024

5 92536 0.653 60419

Total discounted cash

inflow 261472

Initial investment 200000

NPV (Total discounted

cash inflows - initial

investment) 61472

Interpretation

It could be evaluated from the above technique that net present value of project is 61472.

It is essential for the business to evaluate appropriately the business project as it involves large

amount of cash of business. The NPV of the project is positive which shows that project will be

10

Free Cash Flow 51000 58800 66660 74574 82536.6

3.4 NPV of cash flows generated by project

Net present value is the method used by the company for evaluating the profitability of

investment or project. It is an effective technique that that estimates the present value of future

cash flows for identifying whether the cash flows are enough for covering the cost of project.

This is an essential technique used for assessing the viability of the project. The advantage of this

technique is that it considers the time value of money which is not considered in other techniques

of investment appraisal. The drawback is that it does not consider the other cash flows from the

project.

Computation of NPV

Year

Cash

inflows

PV

factor

@

8.9%

Discounted

cash

inflows

1 51000 0.918 46832

2 58800 0.843 49582

3 66660 0.774 51616

4 74574 0.711 53024

5 92536 0.653 60419

Total discounted cash

inflow 261472

Initial investment 200000

NPV (Total discounted

cash inflows - initial

investment) 61472

Interpretation

It could be evaluated from the above technique that net present value of project is 61472.

It is essential for the business to evaluate appropriately the business project as it involves large

amount of cash of business. The NPV of the project is positive which shows that project will be

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitable for the business and will draw adequate returns. As per NPV technique project should

be adopted when the present value is positive and higher (Siminica, Motoi and Dumitru, 2017).

Lower NPV is also not suggested for the project as the lower amount of profit is not beneficial

for the organisation. The cash flows from the business are discounted at the cost of capital which

is 8.9% and the rate of depreciation is 10% as per ATO. According to this technique it could be

assessed that project is profitable and should be implemented by the company. It will derive

adequate return for the business and also enable it to cover the cost of project considering the

scrap value. There are also other measures that could be used for measuring the viability of the

project.

3.5 Project evaluation measures:

Quality: The quality of project is highly important to analyse evaluation fundamentals

and keep track of success which is determined by how new original timeline planned is

able to be obtained. The pros of this evaluation measure is that t is easy to monitor and

analyse on larger growth scenarios but cons on other hands are that quality parameters

cannot check the amount of revenue obtained as profits in return. The quality metric will

be also highly focused on keeping progress in check within functional attributes and for

generating new functional avenues, and costs measures are also difficult to calculate.

This project evaluation measure is also widely important for gaining functional scope of

how varied new scope shall be taking place, and also to potentially develop focus on new

working measures of varied changes which needs to be taken place. Quality shall be

checked mainly to keep monitoring actively done on all phases of working within project

for longer time efficacy. (Elghaish, 2020).

Cost returns: The cost returns from customers and target group among projects is also

highly important for gaining record of project evaluation measure and analysis of how

much returns are able to get from the inputs developed in. The cost returns are an

important domain where focus shall be developed on how varied competitive profits can

be reached on within future domains and also to strategically build new strategies. Cons

of cost returns are that financial reports should be managed properly by project

managers, leaders for gaining focus on cost returns and how are profits coming in within

working scenarios. It could be also understood that along with quality growth wider

11

be adopted when the present value is positive and higher (Siminica, Motoi and Dumitru, 2017).

Lower NPV is also not suggested for the project as the lower amount of profit is not beneficial

for the organisation. The cash flows from the business are discounted at the cost of capital which

is 8.9% and the rate of depreciation is 10% as per ATO. According to this technique it could be

assessed that project is profitable and should be implemented by the company. It will derive

adequate return for the business and also enable it to cover the cost of project considering the

scrap value. There are also other measures that could be used for measuring the viability of the

project.

3.5 Project evaluation measures:

Quality: The quality of project is highly important to analyse evaluation fundamentals

and keep track of success which is determined by how new original timeline planned is

able to be obtained. The pros of this evaluation measure is that t is easy to monitor and

analyse on larger growth scenarios but cons on other hands are that quality parameters

cannot check the amount of revenue obtained as profits in return. The quality metric will

be also highly focused on keeping progress in check within functional attributes and for

generating new functional avenues, and costs measures are also difficult to calculate.

This project evaluation measure is also widely important for gaining functional scope of

how varied new scope shall be taking place, and also to potentially develop focus on new

working measures of varied changes which needs to be taken place. Quality shall be

checked mainly to keep monitoring actively done on all phases of working within project

for longer time efficacy. (Elghaish, 2020).

Cost returns: The cost returns from customers and target group among projects is also

highly important for gaining record of project evaluation measure and analysis of how

much returns are able to get from the inputs developed in. The cost returns are an

important domain where focus shall be developed on how varied competitive profits can

be reached on within future domains and also to strategically build new strategies. Cons

of cost returns are that financial reports should be managed properly by project

managers, leaders for gaining focus on cost returns and how are profits coming in within

working scenarios. It could be also understood that along with quality growth wider

11

positive shift in profits and revenue scope measures are also an important aspect, where

new focus and active exploration shall be there (Atmadja and Saputra, 2018). It could be

also analysed that fruitful growth in cost returns are highly important for targeting

growth avenues in business for larger performance enhancement. Cons are that cost

results may deviate and also change, which may impact on monitoring.

Stakeholder’s satisfaction: The stakeholders satisfaction is also widely important for

gaining new functional working synergy of how various step and research actions taken

place among project management have been positively or negatively impacting

stakeholders. Gaining stakeholder’s confidence is highly important as feedbacks from

them will enable to generate effective monitor and also to pertain focus on wider

domains expertise, which will generate new profits and sustainable profits in future.

Pros of stakeholder’s satisfaction are that it enable company to be active for generating

new functional growth among major domains, also to yearn capacities which can be

actively explored. Cons on other hand are that taking feedbacks and satisfaction from

stakeholders will be long time taking procedures; also there may be divergence of

thoughts and actions which may impact onto wider domains. Project manager has to

positively build new functional working opportunities for gaining stakeholder

satisfaction and also actively communicate vision with regular meetings and

brainstorming session, where interactions with stakeholders will enable to monitor work

growth more actively. (Rahmat and Simanjuntak, 2020).

CONCLUSION

From the above report it could be summarised that the financial management plays a

critical role in the success of organisation. It requires the business to ensure that all the functions

are carried out efficiently by the company. The main focus of the managers is over procuring the

funds from best sources where cost to company is company. They are also concerned with the

effective utilisation of the funds raised and the existing resources of company. The growth and

expansion of business is possible if the existing financial resources are used for generating

further returns. They control the costs and expenditures of the business by preparing the budgets.

12

new focus and active exploration shall be there (Atmadja and Saputra, 2018). It could be

also analysed that fruitful growth in cost returns are highly important for targeting

growth avenues in business for larger performance enhancement. Cons are that cost

results may deviate and also change, which may impact on monitoring.

Stakeholder’s satisfaction: The stakeholders satisfaction is also widely important for

gaining new functional working synergy of how various step and research actions taken

place among project management have been positively or negatively impacting

stakeholders. Gaining stakeholder’s confidence is highly important as feedbacks from

them will enable to generate effective monitor and also to pertain focus on wider

domains expertise, which will generate new profits and sustainable profits in future.

Pros of stakeholder’s satisfaction are that it enable company to be active for generating

new functional growth among major domains, also to yearn capacities which can be

actively explored. Cons on other hand are that taking feedbacks and satisfaction from

stakeholders will be long time taking procedures; also there may be divergence of

thoughts and actions which may impact onto wider domains. Project manager has to

positively build new functional working opportunities for gaining stakeholder

satisfaction and also actively communicate vision with regular meetings and

brainstorming session, where interactions with stakeholders will enable to monitor work

growth more actively. (Rahmat and Simanjuntak, 2020).

CONCLUSION

From the above report it could be summarised that the financial management plays a

critical role in the success of organisation. It requires the business to ensure that all the functions

are carried out efficiently by the company. The main focus of the managers is over procuring the

funds from best sources where cost to company is company. They are also concerned with the

effective utilisation of the funds raised and the existing resources of company. The growth and

expansion of business is possible if the existing financial resources are used for generating

further returns. They control the costs and expenditures of the business by preparing the budgets.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.