Finance Assignment: Investment Analysis, Portfolio and Tax Policy

VerifiedAdded on 2023/06/13

|11

|2123

|499

Homework Assignment

AI Summary

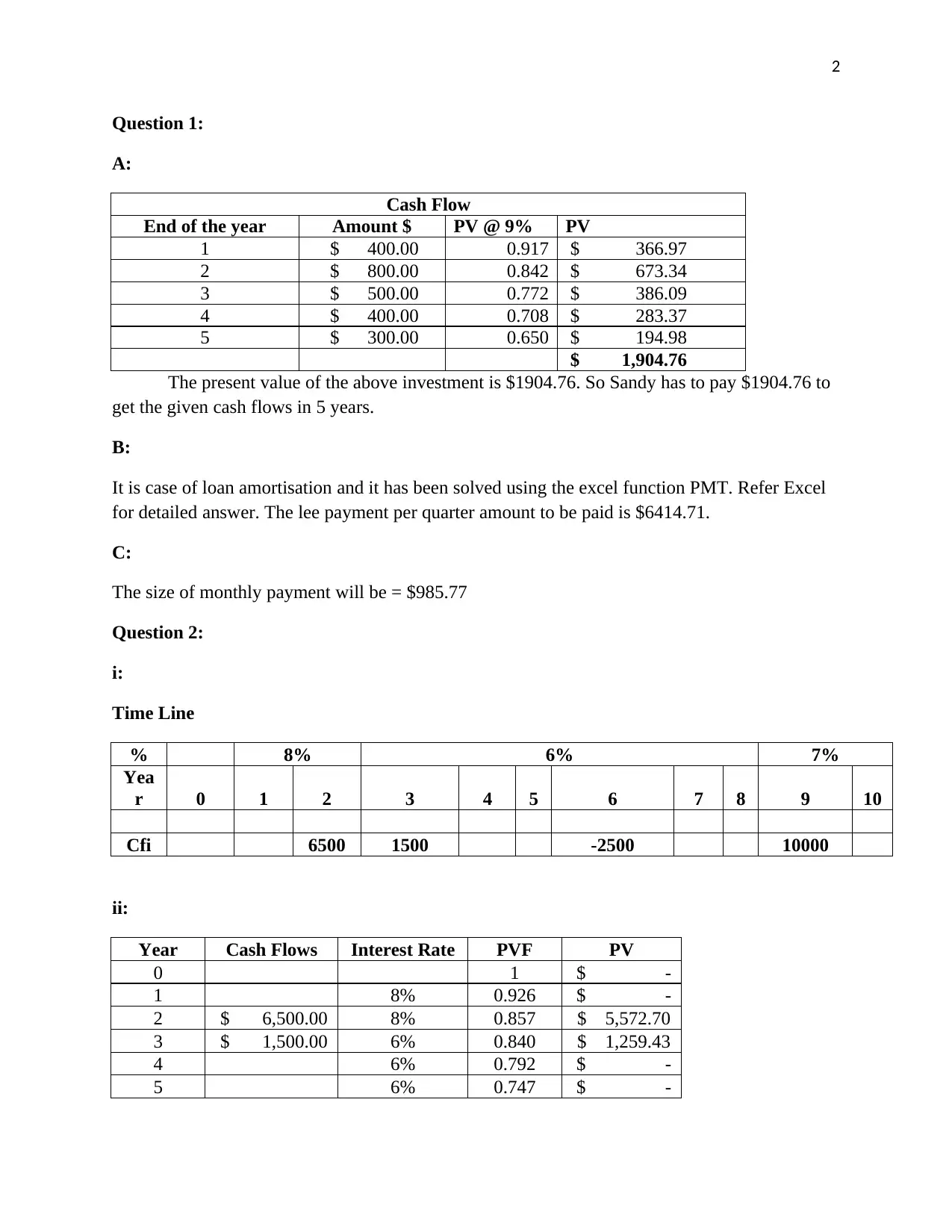

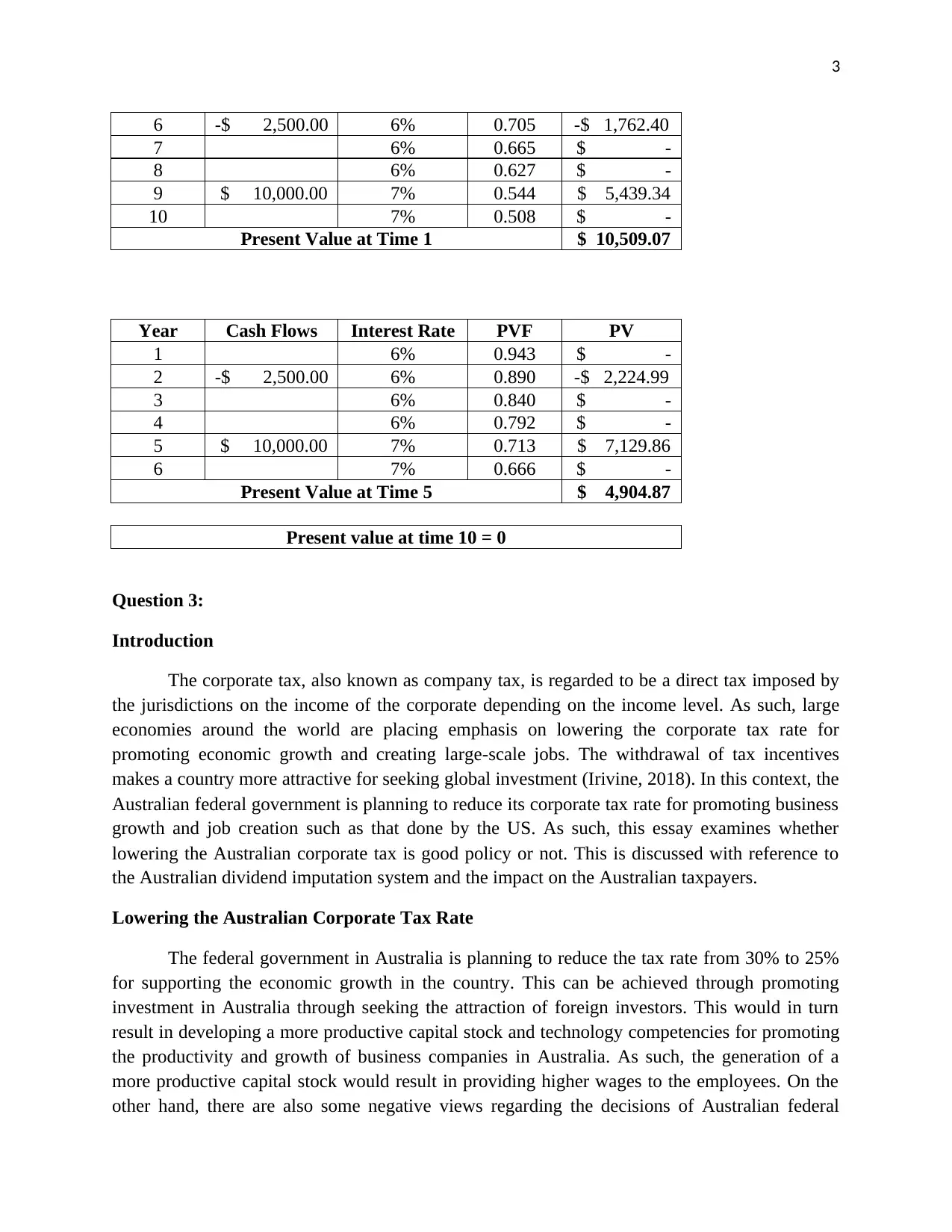

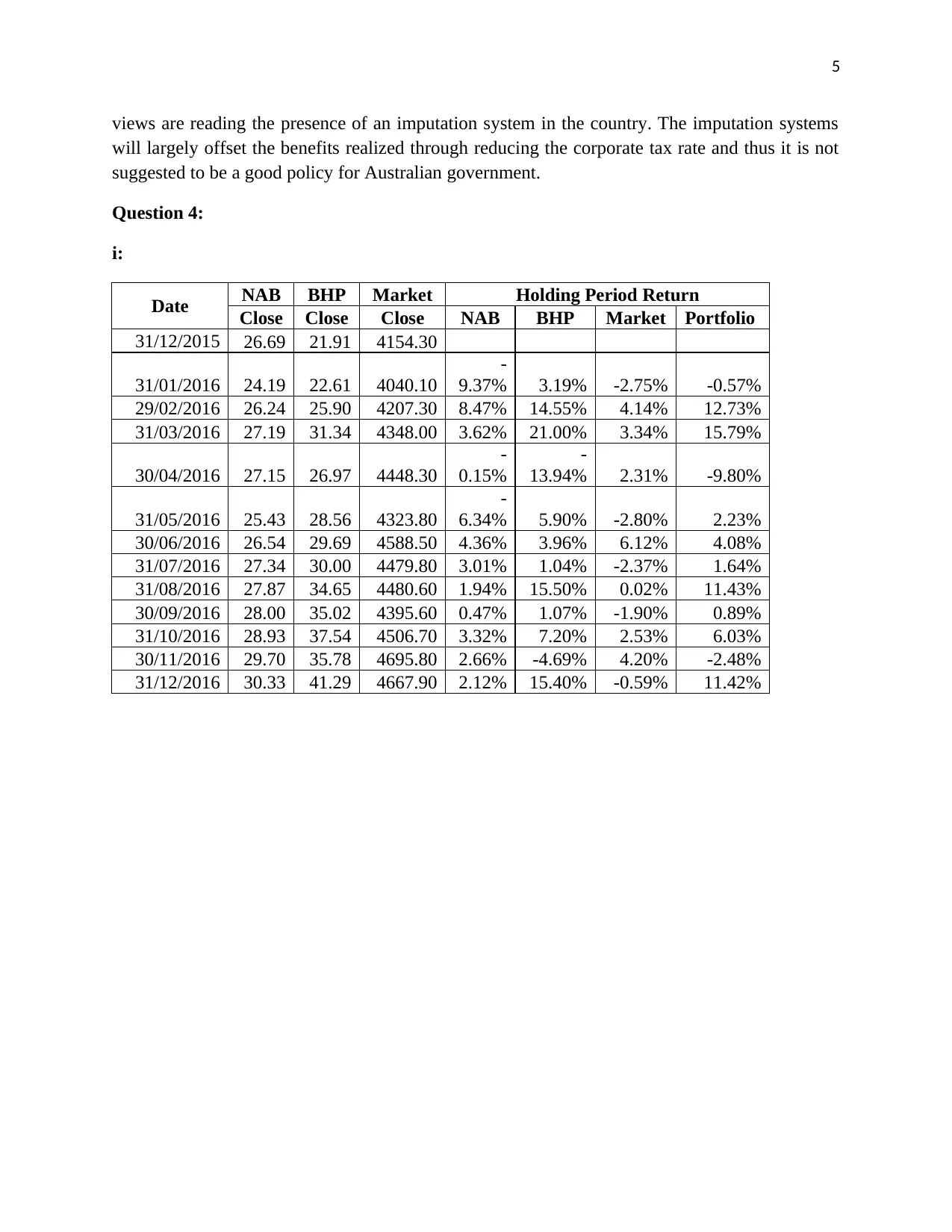

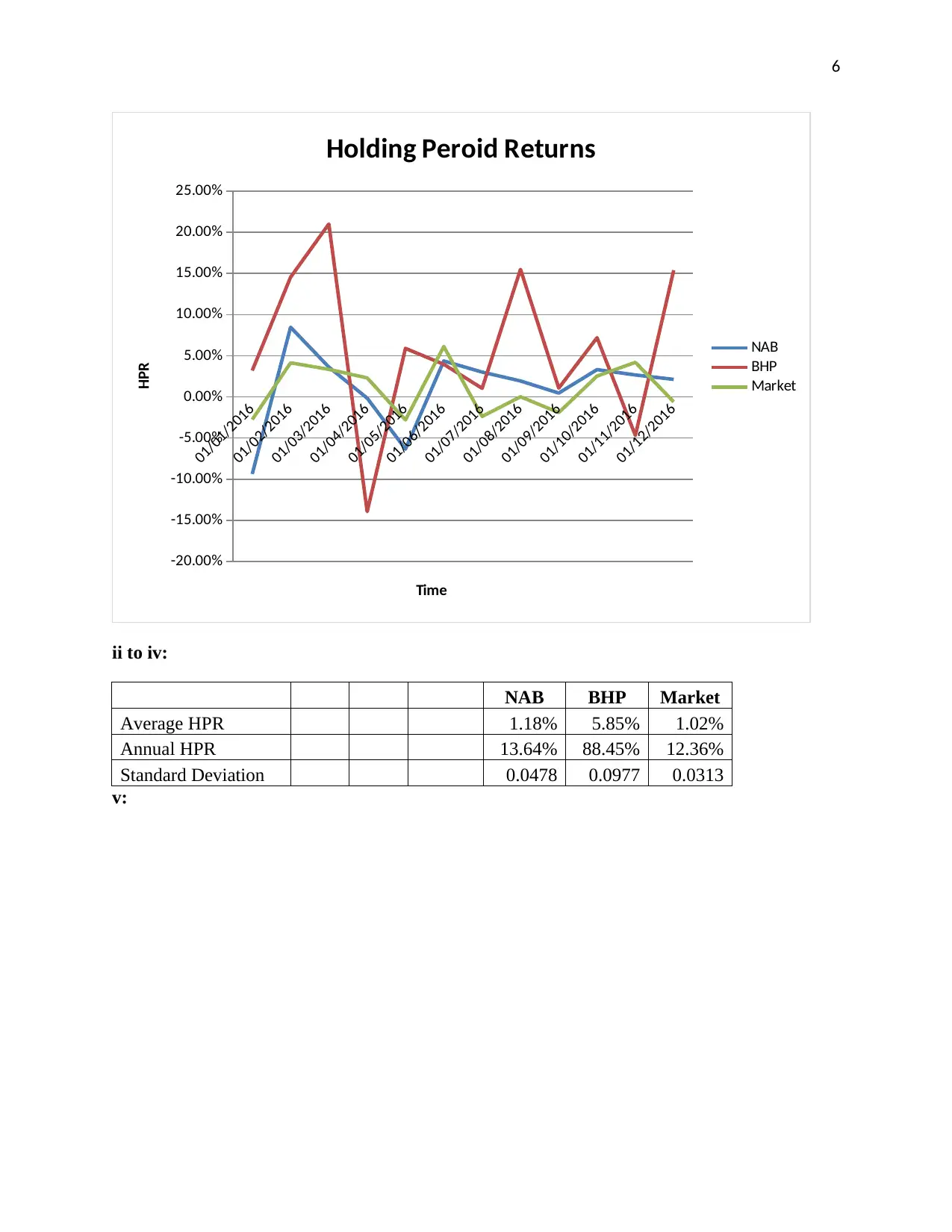

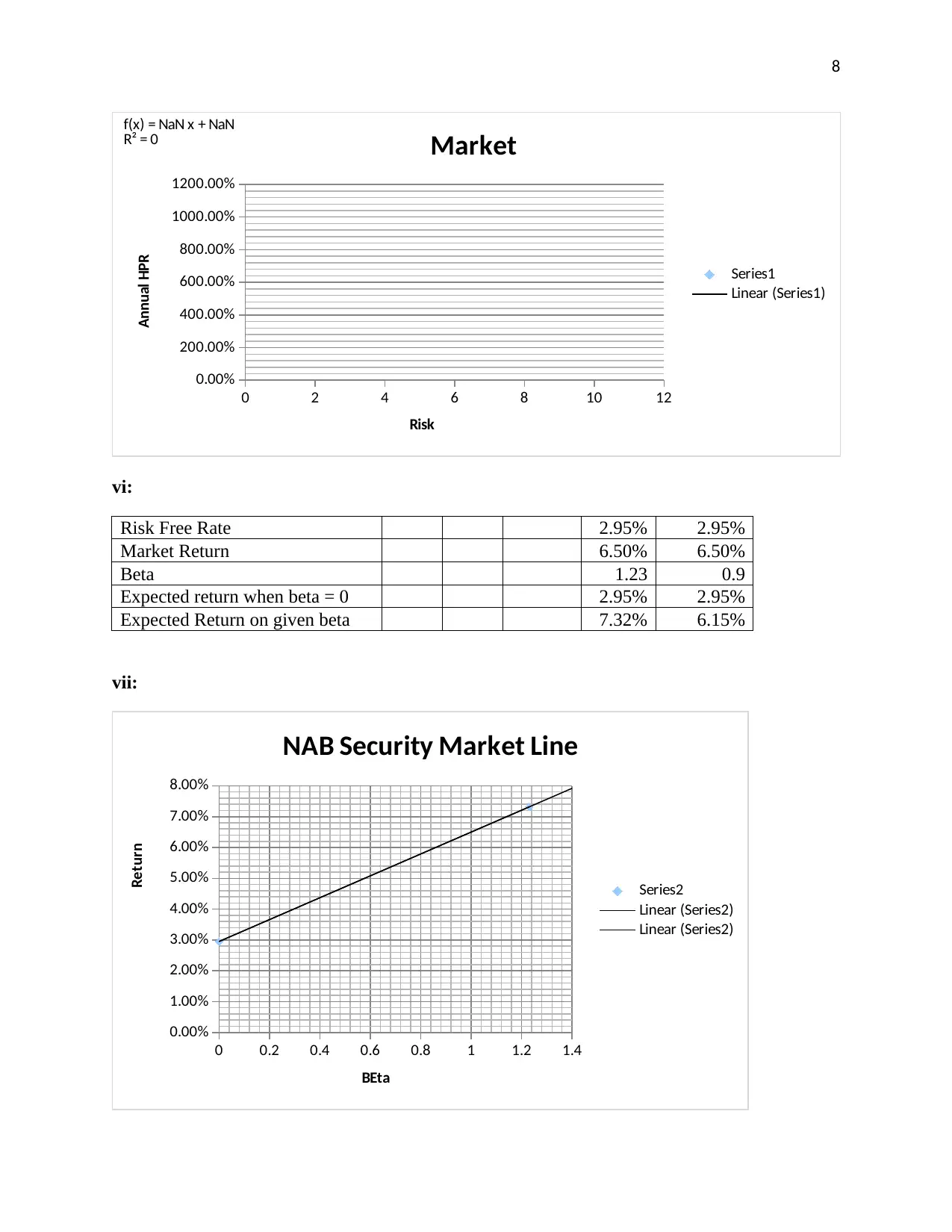

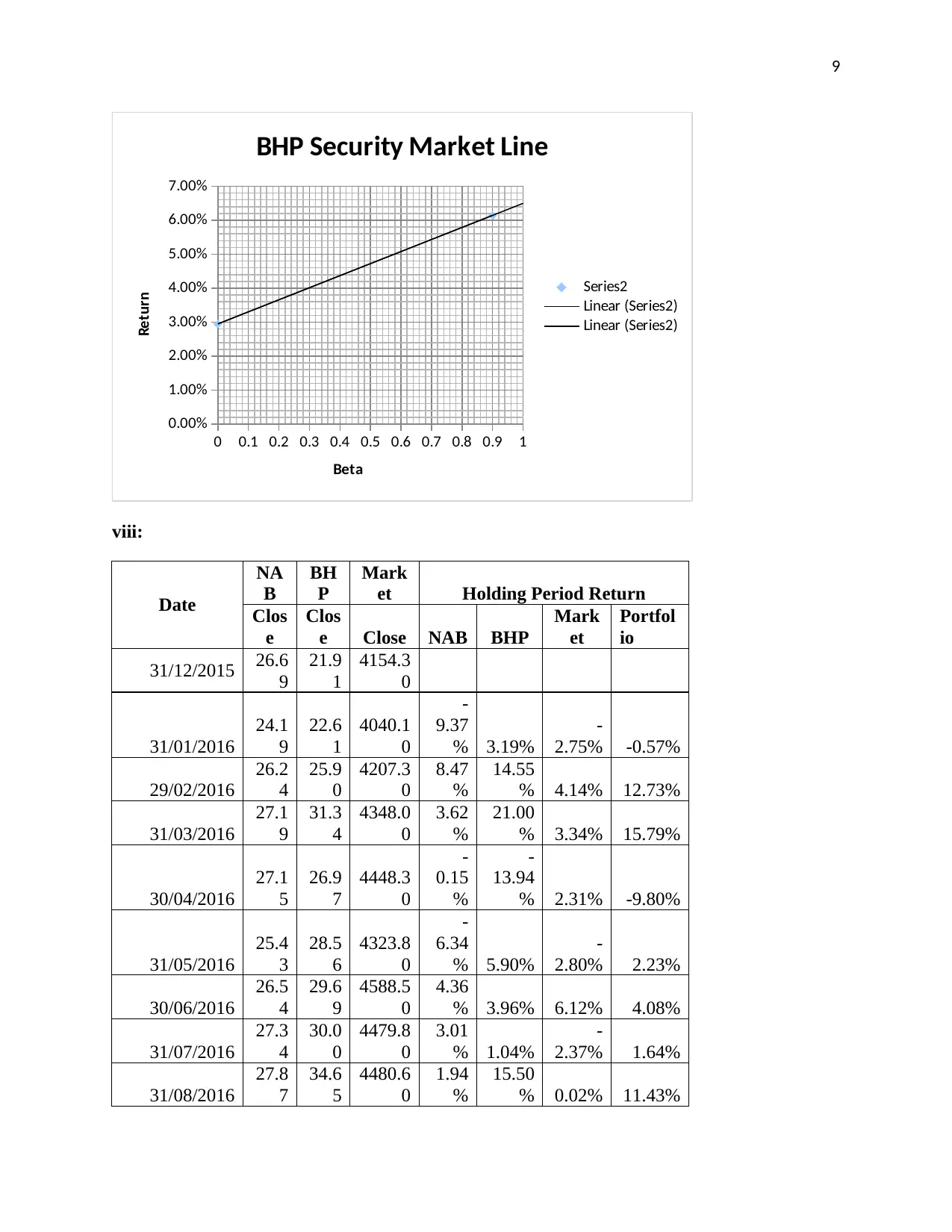

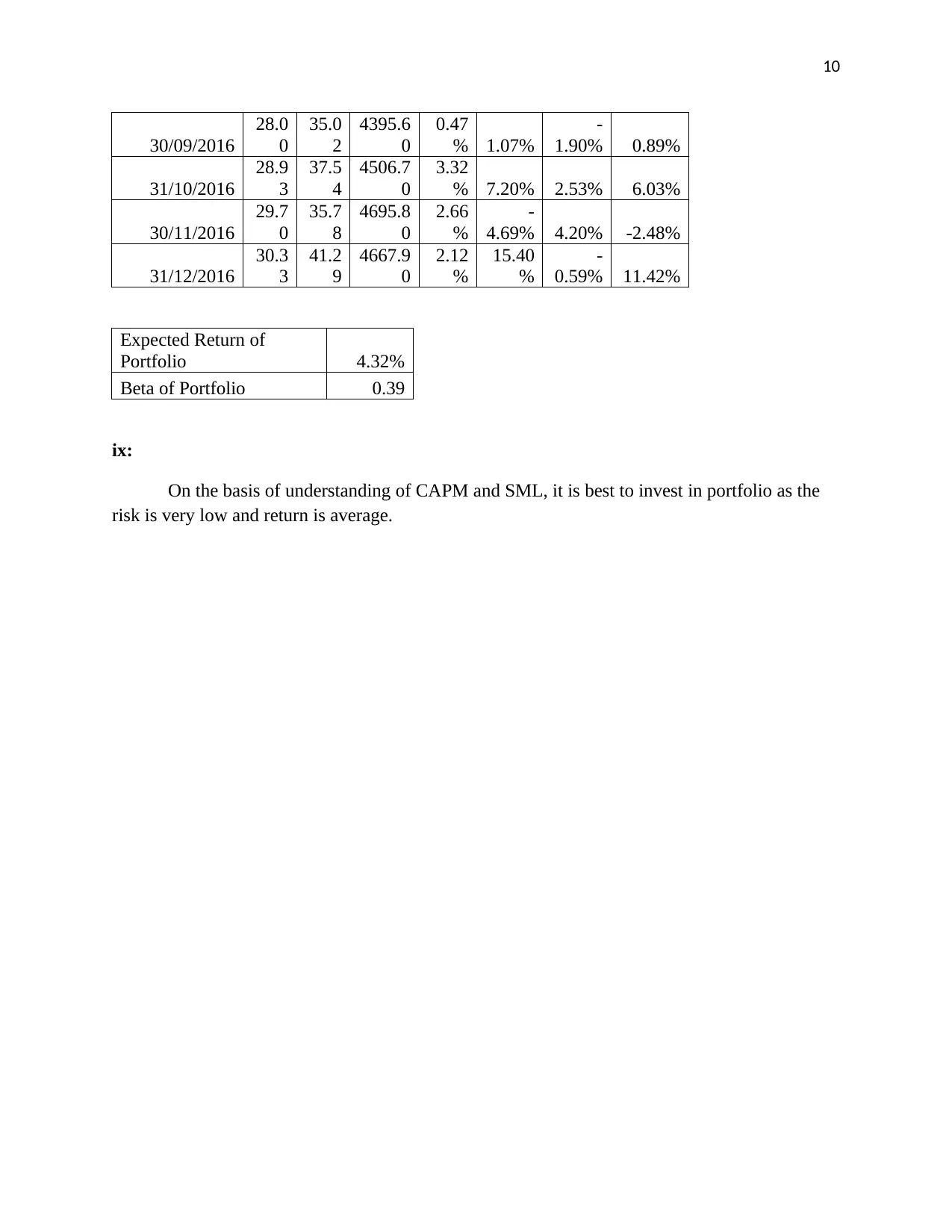

This finance assignment provides solutions to questions covering various topics, starting with calculating the present value of an investment's cash flows and determining the payment amount for loan amortization. It further analyzes the impact of reducing the Australian corporate tax rate, considering the dividend imputation system and its effects on Australian taxpayers and foreign investors. Additionally, the assignment includes a portfolio analysis, calculating holding period returns for NAB, BHP, and the market portfolio, and applying the Capital Asset Pricing Model (CAPM) and Security Market Line (SML) to assess investment risk and expected returns. The analysis helps determine the best investment strategy based on risk and return, concluding that investing in a portfolio is preferable due to its low risk and average return. Desklib offers a platform for students to access this and other solved assignments for academic assistance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.