Project Report: Business Finance - Office Building Loan Analysis

VerifiedAdded on 2020/05/16

|27

|6318

|64

Project

AI Summary

This project report delves into the financial analysis of an office building loan, providing a detailed breakdown of loan calculations. It starts with the determination of the monthly EMI, calculated to be $2,42,655. The report proceeds to calculate the monthly interest payment, which is $1,33,333 for the first month, and the monthly principle payment, which is $1,09,322. The report also includes a loan schedule showing the loan amount after 3 years, which is $1,55,68,577.62. Furthermore, the report compares the total EMI and interest amounts for an 8% interest rate versus a 7% interest rate, along with the costs associated with refinancing. Finally, the report presents a loan schedule for the remaining loan amount after refinancing, with a new EMI of $2,34,972 and a detailed breakdown of interest and closing balance over 84 months. The analysis is based on the data and financial models related to loan amortization and repayment schedules.

Running Head: Business Finance

1

Project report: Business Finance

1

Project report: Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

2

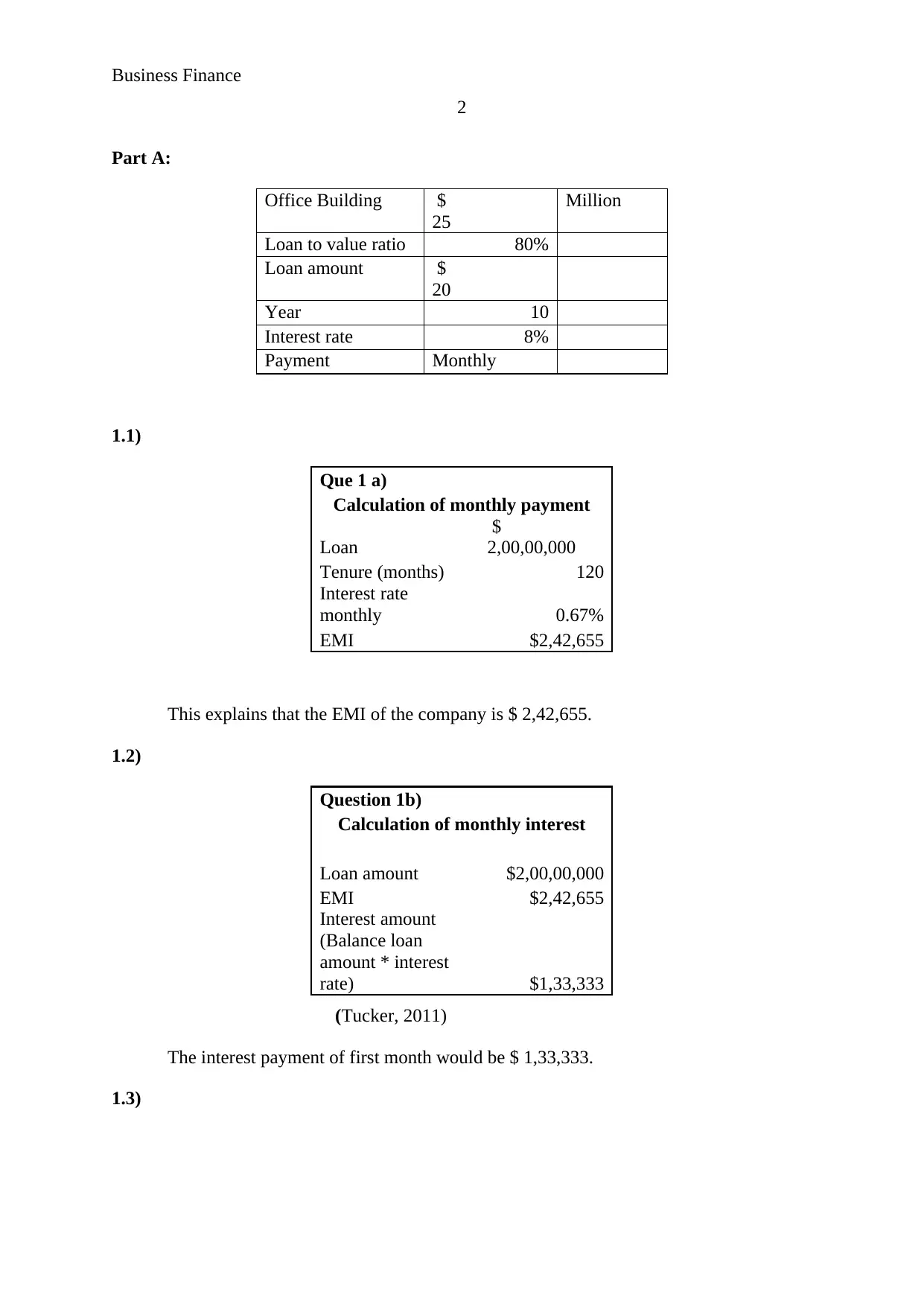

Part A:

Office Building $

25

Million

Loan to value ratio 80%

Loan amount $

20

Year 10

Interest rate 8%

Payment Monthly

1.1)

Que 1 a)

Calculation of monthly payment

Loan

$

2,00,00,000

Tenure (months) 120

Interest rate

monthly 0.67%

EMI $2,42,655

This explains that the EMI of the company is $ 2,42,655.

1.2)

Question 1b)

Calculation of monthly interest

Loan amount $2,00,00,000

EMI $2,42,655

Interest amount

(Balance loan

amount * interest

rate) $1,33,333

(Tucker, 2011)

The interest payment of first month would be $ 1,33,333.

1.3)

2

Part A:

Office Building $

25

Million

Loan to value ratio 80%

Loan amount $

20

Year 10

Interest rate 8%

Payment Monthly

1.1)

Que 1 a)

Calculation of monthly payment

Loan

$

2,00,00,000

Tenure (months) 120

Interest rate

monthly 0.67%

EMI $2,42,655

This explains that the EMI of the company is $ 2,42,655.

1.2)

Question 1b)

Calculation of monthly interest

Loan amount $2,00,00,000

EMI $2,42,655

Interest amount

(Balance loan

amount * interest

rate) $1,33,333

(Tucker, 2011)

The interest payment of first month would be $ 1,33,333.

1.3)

Business Finance

3

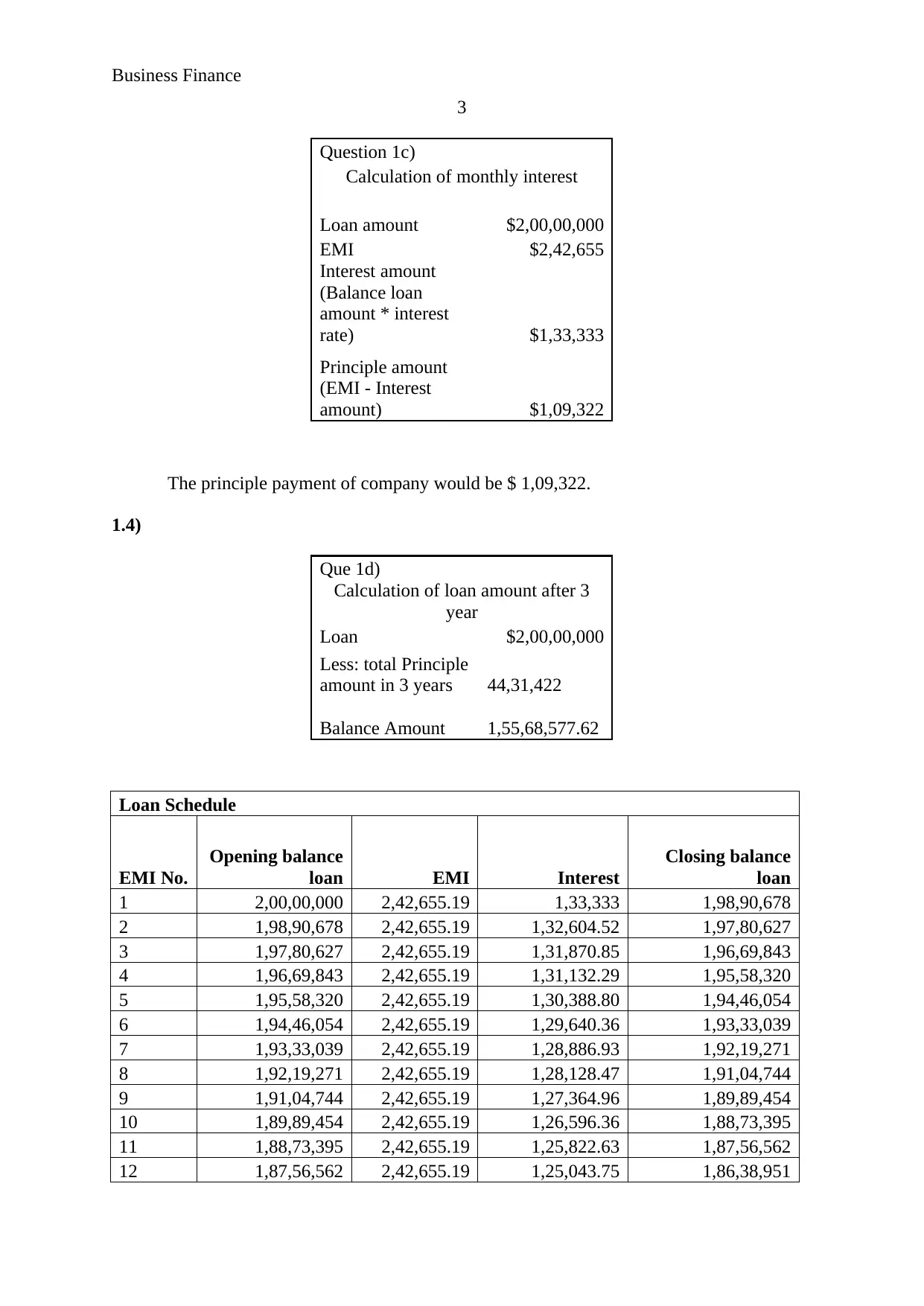

Question 1c)

Calculation of monthly interest

Loan amount $2,00,00,000

EMI $2,42,655

Interest amount

(Balance loan

amount * interest

rate) $1,33,333

Principle amount

(EMI - Interest

amount) $1,09,322

The principle payment of company would be $ 1,09,322.

1.4)

Que 1d)

Calculation of loan amount after 3

year

Loan $2,00,00,000

Less: total Principle

amount in 3 years 44,31,422

Balance Amount 1,55,68,577.62

Loan Schedule

EMI No.

Opening balance

loan EMI Interest

Closing balance

loan

1 2,00,00,000 2,42,655.19 1,33,333 1,98,90,678

2 1,98,90,678 2,42,655.19 1,32,604.52 1,97,80,627

3 1,97,80,627 2,42,655.19 1,31,870.85 1,96,69,843

4 1,96,69,843 2,42,655.19 1,31,132.29 1,95,58,320

5 1,95,58,320 2,42,655.19 1,30,388.80 1,94,46,054

6 1,94,46,054 2,42,655.19 1,29,640.36 1,93,33,039

7 1,93,33,039 2,42,655.19 1,28,886.93 1,92,19,271

8 1,92,19,271 2,42,655.19 1,28,128.47 1,91,04,744

9 1,91,04,744 2,42,655.19 1,27,364.96 1,89,89,454

10 1,89,89,454 2,42,655.19 1,26,596.36 1,88,73,395

11 1,88,73,395 2,42,655.19 1,25,822.63 1,87,56,562

12 1,87,56,562 2,42,655.19 1,25,043.75 1,86,38,951

3

Question 1c)

Calculation of monthly interest

Loan amount $2,00,00,000

EMI $2,42,655

Interest amount

(Balance loan

amount * interest

rate) $1,33,333

Principle amount

(EMI - Interest

amount) $1,09,322

The principle payment of company would be $ 1,09,322.

1.4)

Que 1d)

Calculation of loan amount after 3

year

Loan $2,00,00,000

Less: total Principle

amount in 3 years 44,31,422

Balance Amount 1,55,68,577.62

Loan Schedule

EMI No.

Opening balance

loan EMI Interest

Closing balance

loan

1 2,00,00,000 2,42,655.19 1,33,333 1,98,90,678

2 1,98,90,678 2,42,655.19 1,32,604.52 1,97,80,627

3 1,97,80,627 2,42,655.19 1,31,870.85 1,96,69,843

4 1,96,69,843 2,42,655.19 1,31,132.29 1,95,58,320

5 1,95,58,320 2,42,655.19 1,30,388.80 1,94,46,054

6 1,94,46,054 2,42,655.19 1,29,640.36 1,93,33,039

7 1,93,33,039 2,42,655.19 1,28,886.93 1,92,19,271

8 1,92,19,271 2,42,655.19 1,28,128.47 1,91,04,744

9 1,91,04,744 2,42,655.19 1,27,364.96 1,89,89,454

10 1,89,89,454 2,42,655.19 1,26,596.36 1,88,73,395

11 1,88,73,395 2,42,655.19 1,25,822.63 1,87,56,562

12 1,87,56,562 2,42,655.19 1,25,043.75 1,86,38,951

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance

4

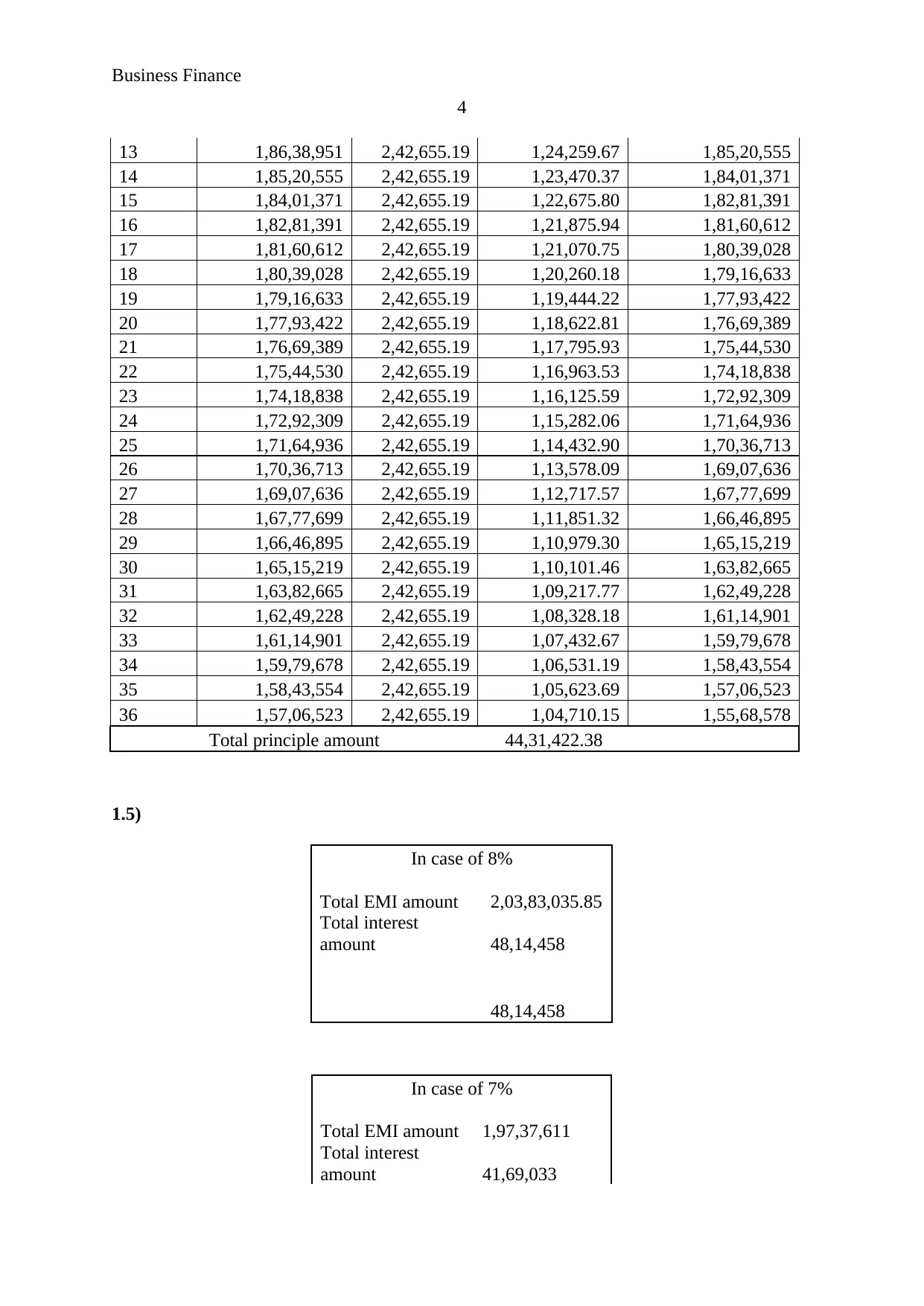

13 1,86,38,951 2,42,655.19 1,24,259.67 1,85,20,555

14 1,85,20,555 2,42,655.19 1,23,470.37 1,84,01,371

15 1,84,01,371 2,42,655.19 1,22,675.80 1,82,81,391

16 1,82,81,391 2,42,655.19 1,21,875.94 1,81,60,612

17 1,81,60,612 2,42,655.19 1,21,070.75 1,80,39,028

18 1,80,39,028 2,42,655.19 1,20,260.18 1,79,16,633

19 1,79,16,633 2,42,655.19 1,19,444.22 1,77,93,422

20 1,77,93,422 2,42,655.19 1,18,622.81 1,76,69,389

21 1,76,69,389 2,42,655.19 1,17,795.93 1,75,44,530

22 1,75,44,530 2,42,655.19 1,16,963.53 1,74,18,838

23 1,74,18,838 2,42,655.19 1,16,125.59 1,72,92,309

24 1,72,92,309 2,42,655.19 1,15,282.06 1,71,64,936

25 1,71,64,936 2,42,655.19 1,14,432.90 1,70,36,713

26 1,70,36,713 2,42,655.19 1,13,578.09 1,69,07,636

27 1,69,07,636 2,42,655.19 1,12,717.57 1,67,77,699

28 1,67,77,699 2,42,655.19 1,11,851.32 1,66,46,895

29 1,66,46,895 2,42,655.19 1,10,979.30 1,65,15,219

30 1,65,15,219 2,42,655.19 1,10,101.46 1,63,82,665

31 1,63,82,665 2,42,655.19 1,09,217.77 1,62,49,228

32 1,62,49,228 2,42,655.19 1,08,328.18 1,61,14,901

33 1,61,14,901 2,42,655.19 1,07,432.67 1,59,79,678

34 1,59,79,678 2,42,655.19 1,06,531.19 1,58,43,554

35 1,58,43,554 2,42,655.19 1,05,623.69 1,57,06,523

36 1,57,06,523 2,42,655.19 1,04,710.15 1,55,68,578

Total principle amount 44,31,422.38

1.5)

In case of 8%

Total EMI amount 2,03,83,035.85

Total interest

amount 48,14,458

48,14,458

In case of 7%

Total EMI amount 1,97,37,611

Total interest

amount 41,69,033

4

13 1,86,38,951 2,42,655.19 1,24,259.67 1,85,20,555

14 1,85,20,555 2,42,655.19 1,23,470.37 1,84,01,371

15 1,84,01,371 2,42,655.19 1,22,675.80 1,82,81,391

16 1,82,81,391 2,42,655.19 1,21,875.94 1,81,60,612

17 1,81,60,612 2,42,655.19 1,21,070.75 1,80,39,028

18 1,80,39,028 2,42,655.19 1,20,260.18 1,79,16,633

19 1,79,16,633 2,42,655.19 1,19,444.22 1,77,93,422

20 1,77,93,422 2,42,655.19 1,18,622.81 1,76,69,389

21 1,76,69,389 2,42,655.19 1,17,795.93 1,75,44,530

22 1,75,44,530 2,42,655.19 1,16,963.53 1,74,18,838

23 1,74,18,838 2,42,655.19 1,16,125.59 1,72,92,309

24 1,72,92,309 2,42,655.19 1,15,282.06 1,71,64,936

25 1,71,64,936 2,42,655.19 1,14,432.90 1,70,36,713

26 1,70,36,713 2,42,655.19 1,13,578.09 1,69,07,636

27 1,69,07,636 2,42,655.19 1,12,717.57 1,67,77,699

28 1,67,77,699 2,42,655.19 1,11,851.32 1,66,46,895

29 1,66,46,895 2,42,655.19 1,10,979.30 1,65,15,219

30 1,65,15,219 2,42,655.19 1,10,101.46 1,63,82,665

31 1,63,82,665 2,42,655.19 1,09,217.77 1,62,49,228

32 1,62,49,228 2,42,655.19 1,08,328.18 1,61,14,901

33 1,61,14,901 2,42,655.19 1,07,432.67 1,59,79,678

34 1,59,79,678 2,42,655.19 1,06,531.19 1,58,43,554

35 1,58,43,554 2,42,655.19 1,05,623.69 1,57,06,523

36 1,57,06,523 2,42,655.19 1,04,710.15 1,55,68,578

Total principle amount 44,31,422.38

1.5)

In case of 8%

Total EMI amount 2,03,83,035.85

Total interest

amount 48,14,458

48,14,458

In case of 7%

Total EMI amount 1,97,37,611

Total interest

amount 41,69,033

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

5

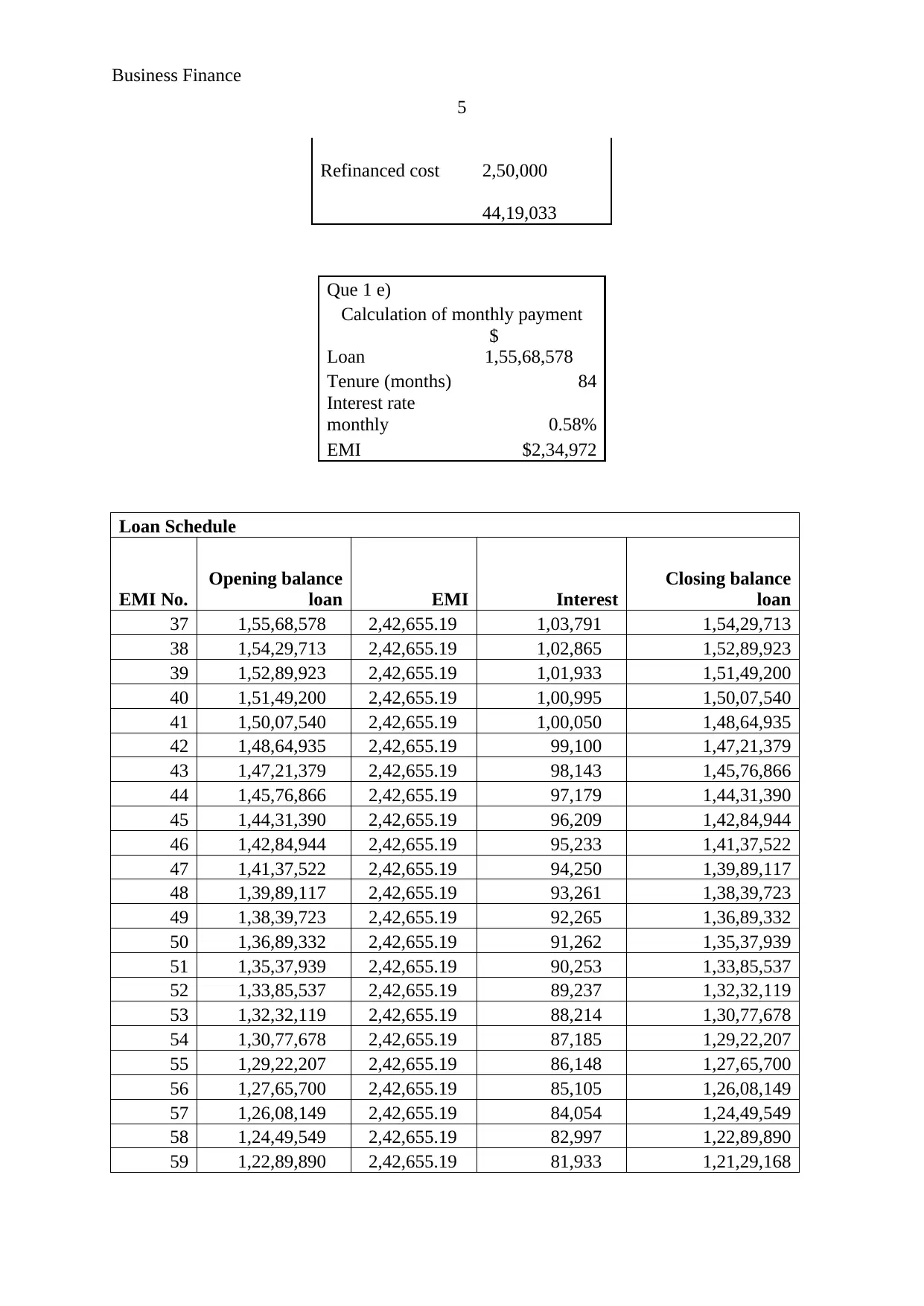

Refinanced cost 2,50,000

44,19,033

Que 1 e)

Calculation of monthly payment

Loan

$

1,55,68,578

Tenure (months) 84

Interest rate

monthly 0.58%

EMI $2,34,972

Loan Schedule

EMI No.

Opening balance

loan EMI Interest

Closing balance

loan

37 1,55,68,578 2,42,655.19 1,03,791 1,54,29,713

38 1,54,29,713 2,42,655.19 1,02,865 1,52,89,923

39 1,52,89,923 2,42,655.19 1,01,933 1,51,49,200

40 1,51,49,200 2,42,655.19 1,00,995 1,50,07,540

41 1,50,07,540 2,42,655.19 1,00,050 1,48,64,935

42 1,48,64,935 2,42,655.19 99,100 1,47,21,379

43 1,47,21,379 2,42,655.19 98,143 1,45,76,866

44 1,45,76,866 2,42,655.19 97,179 1,44,31,390

45 1,44,31,390 2,42,655.19 96,209 1,42,84,944

46 1,42,84,944 2,42,655.19 95,233 1,41,37,522

47 1,41,37,522 2,42,655.19 94,250 1,39,89,117

48 1,39,89,117 2,42,655.19 93,261 1,38,39,723

49 1,38,39,723 2,42,655.19 92,265 1,36,89,332

50 1,36,89,332 2,42,655.19 91,262 1,35,37,939

51 1,35,37,939 2,42,655.19 90,253 1,33,85,537

52 1,33,85,537 2,42,655.19 89,237 1,32,32,119

53 1,32,32,119 2,42,655.19 88,214 1,30,77,678

54 1,30,77,678 2,42,655.19 87,185 1,29,22,207

55 1,29,22,207 2,42,655.19 86,148 1,27,65,700

56 1,27,65,700 2,42,655.19 85,105 1,26,08,149

57 1,26,08,149 2,42,655.19 84,054 1,24,49,549

58 1,24,49,549 2,42,655.19 82,997 1,22,89,890

59 1,22,89,890 2,42,655.19 81,933 1,21,29,168

5

Refinanced cost 2,50,000

44,19,033

Que 1 e)

Calculation of monthly payment

Loan

$

1,55,68,578

Tenure (months) 84

Interest rate

monthly 0.58%

EMI $2,34,972

Loan Schedule

EMI No.

Opening balance

loan EMI Interest

Closing balance

loan

37 1,55,68,578 2,42,655.19 1,03,791 1,54,29,713

38 1,54,29,713 2,42,655.19 1,02,865 1,52,89,923

39 1,52,89,923 2,42,655.19 1,01,933 1,51,49,200

40 1,51,49,200 2,42,655.19 1,00,995 1,50,07,540

41 1,50,07,540 2,42,655.19 1,00,050 1,48,64,935

42 1,48,64,935 2,42,655.19 99,100 1,47,21,379

43 1,47,21,379 2,42,655.19 98,143 1,45,76,866

44 1,45,76,866 2,42,655.19 97,179 1,44,31,390

45 1,44,31,390 2,42,655.19 96,209 1,42,84,944

46 1,42,84,944 2,42,655.19 95,233 1,41,37,522

47 1,41,37,522 2,42,655.19 94,250 1,39,89,117

48 1,39,89,117 2,42,655.19 93,261 1,38,39,723

49 1,38,39,723 2,42,655.19 92,265 1,36,89,332

50 1,36,89,332 2,42,655.19 91,262 1,35,37,939

51 1,35,37,939 2,42,655.19 90,253 1,33,85,537

52 1,33,85,537 2,42,655.19 89,237 1,32,32,119

53 1,32,32,119 2,42,655.19 88,214 1,30,77,678

54 1,30,77,678 2,42,655.19 87,185 1,29,22,207

55 1,29,22,207 2,42,655.19 86,148 1,27,65,700

56 1,27,65,700 2,42,655.19 85,105 1,26,08,149

57 1,26,08,149 2,42,655.19 84,054 1,24,49,549

58 1,24,49,549 2,42,655.19 82,997 1,22,89,890

59 1,22,89,890 2,42,655.19 81,933 1,21,29,168

Business Finance

6

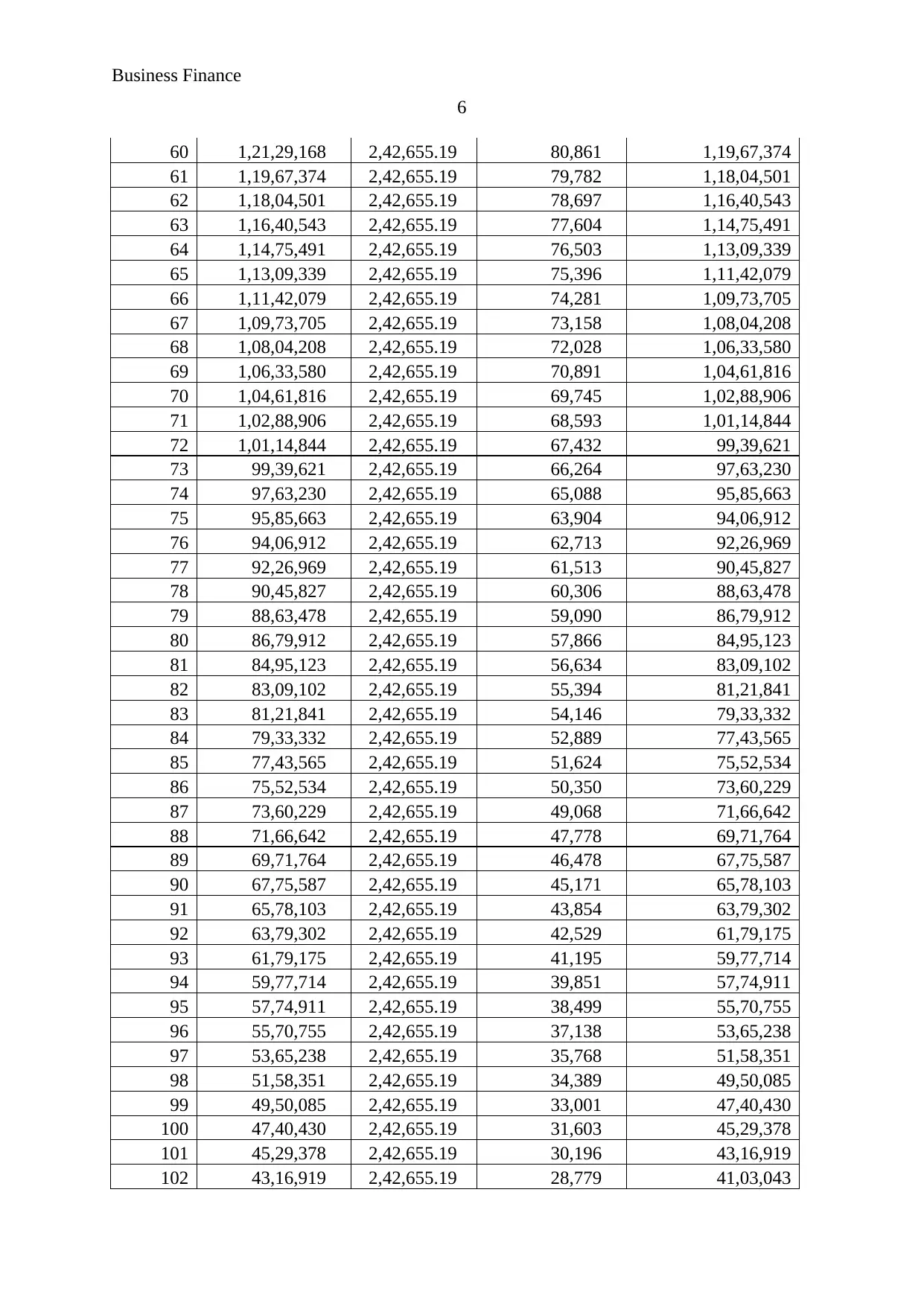

60 1,21,29,168 2,42,655.19 80,861 1,19,67,374

61 1,19,67,374 2,42,655.19 79,782 1,18,04,501

62 1,18,04,501 2,42,655.19 78,697 1,16,40,543

63 1,16,40,543 2,42,655.19 77,604 1,14,75,491

64 1,14,75,491 2,42,655.19 76,503 1,13,09,339

65 1,13,09,339 2,42,655.19 75,396 1,11,42,079

66 1,11,42,079 2,42,655.19 74,281 1,09,73,705

67 1,09,73,705 2,42,655.19 73,158 1,08,04,208

68 1,08,04,208 2,42,655.19 72,028 1,06,33,580

69 1,06,33,580 2,42,655.19 70,891 1,04,61,816

70 1,04,61,816 2,42,655.19 69,745 1,02,88,906

71 1,02,88,906 2,42,655.19 68,593 1,01,14,844

72 1,01,14,844 2,42,655.19 67,432 99,39,621

73 99,39,621 2,42,655.19 66,264 97,63,230

74 97,63,230 2,42,655.19 65,088 95,85,663

75 95,85,663 2,42,655.19 63,904 94,06,912

76 94,06,912 2,42,655.19 62,713 92,26,969

77 92,26,969 2,42,655.19 61,513 90,45,827

78 90,45,827 2,42,655.19 60,306 88,63,478

79 88,63,478 2,42,655.19 59,090 86,79,912

80 86,79,912 2,42,655.19 57,866 84,95,123

81 84,95,123 2,42,655.19 56,634 83,09,102

82 83,09,102 2,42,655.19 55,394 81,21,841

83 81,21,841 2,42,655.19 54,146 79,33,332

84 79,33,332 2,42,655.19 52,889 77,43,565

85 77,43,565 2,42,655.19 51,624 75,52,534

86 75,52,534 2,42,655.19 50,350 73,60,229

87 73,60,229 2,42,655.19 49,068 71,66,642

88 71,66,642 2,42,655.19 47,778 69,71,764

89 69,71,764 2,42,655.19 46,478 67,75,587

90 67,75,587 2,42,655.19 45,171 65,78,103

91 65,78,103 2,42,655.19 43,854 63,79,302

92 63,79,302 2,42,655.19 42,529 61,79,175

93 61,79,175 2,42,655.19 41,195 59,77,714

94 59,77,714 2,42,655.19 39,851 57,74,911

95 57,74,911 2,42,655.19 38,499 55,70,755

96 55,70,755 2,42,655.19 37,138 53,65,238

97 53,65,238 2,42,655.19 35,768 51,58,351

98 51,58,351 2,42,655.19 34,389 49,50,085

99 49,50,085 2,42,655.19 33,001 47,40,430

100 47,40,430 2,42,655.19 31,603 45,29,378

101 45,29,378 2,42,655.19 30,196 43,16,919

102 43,16,919 2,42,655.19 28,779 41,03,043

6

60 1,21,29,168 2,42,655.19 80,861 1,19,67,374

61 1,19,67,374 2,42,655.19 79,782 1,18,04,501

62 1,18,04,501 2,42,655.19 78,697 1,16,40,543

63 1,16,40,543 2,42,655.19 77,604 1,14,75,491

64 1,14,75,491 2,42,655.19 76,503 1,13,09,339

65 1,13,09,339 2,42,655.19 75,396 1,11,42,079

66 1,11,42,079 2,42,655.19 74,281 1,09,73,705

67 1,09,73,705 2,42,655.19 73,158 1,08,04,208

68 1,08,04,208 2,42,655.19 72,028 1,06,33,580

69 1,06,33,580 2,42,655.19 70,891 1,04,61,816

70 1,04,61,816 2,42,655.19 69,745 1,02,88,906

71 1,02,88,906 2,42,655.19 68,593 1,01,14,844

72 1,01,14,844 2,42,655.19 67,432 99,39,621

73 99,39,621 2,42,655.19 66,264 97,63,230

74 97,63,230 2,42,655.19 65,088 95,85,663

75 95,85,663 2,42,655.19 63,904 94,06,912

76 94,06,912 2,42,655.19 62,713 92,26,969

77 92,26,969 2,42,655.19 61,513 90,45,827

78 90,45,827 2,42,655.19 60,306 88,63,478

79 88,63,478 2,42,655.19 59,090 86,79,912

80 86,79,912 2,42,655.19 57,866 84,95,123

81 84,95,123 2,42,655.19 56,634 83,09,102

82 83,09,102 2,42,655.19 55,394 81,21,841

83 81,21,841 2,42,655.19 54,146 79,33,332

84 79,33,332 2,42,655.19 52,889 77,43,565

85 77,43,565 2,42,655.19 51,624 75,52,534

86 75,52,534 2,42,655.19 50,350 73,60,229

87 73,60,229 2,42,655.19 49,068 71,66,642

88 71,66,642 2,42,655.19 47,778 69,71,764

89 69,71,764 2,42,655.19 46,478 67,75,587

90 67,75,587 2,42,655.19 45,171 65,78,103

91 65,78,103 2,42,655.19 43,854 63,79,302

92 63,79,302 2,42,655.19 42,529 61,79,175

93 61,79,175 2,42,655.19 41,195 59,77,714

94 59,77,714 2,42,655.19 39,851 57,74,911

95 57,74,911 2,42,655.19 38,499 55,70,755

96 55,70,755 2,42,655.19 37,138 53,65,238

97 53,65,238 2,42,655.19 35,768 51,58,351

98 51,58,351 2,42,655.19 34,389 49,50,085

99 49,50,085 2,42,655.19 33,001 47,40,430

100 47,40,430 2,42,655.19 31,603 45,29,378

101 45,29,378 2,42,655.19 30,196 43,16,919

102 43,16,919 2,42,655.19 28,779 41,03,043

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance

7

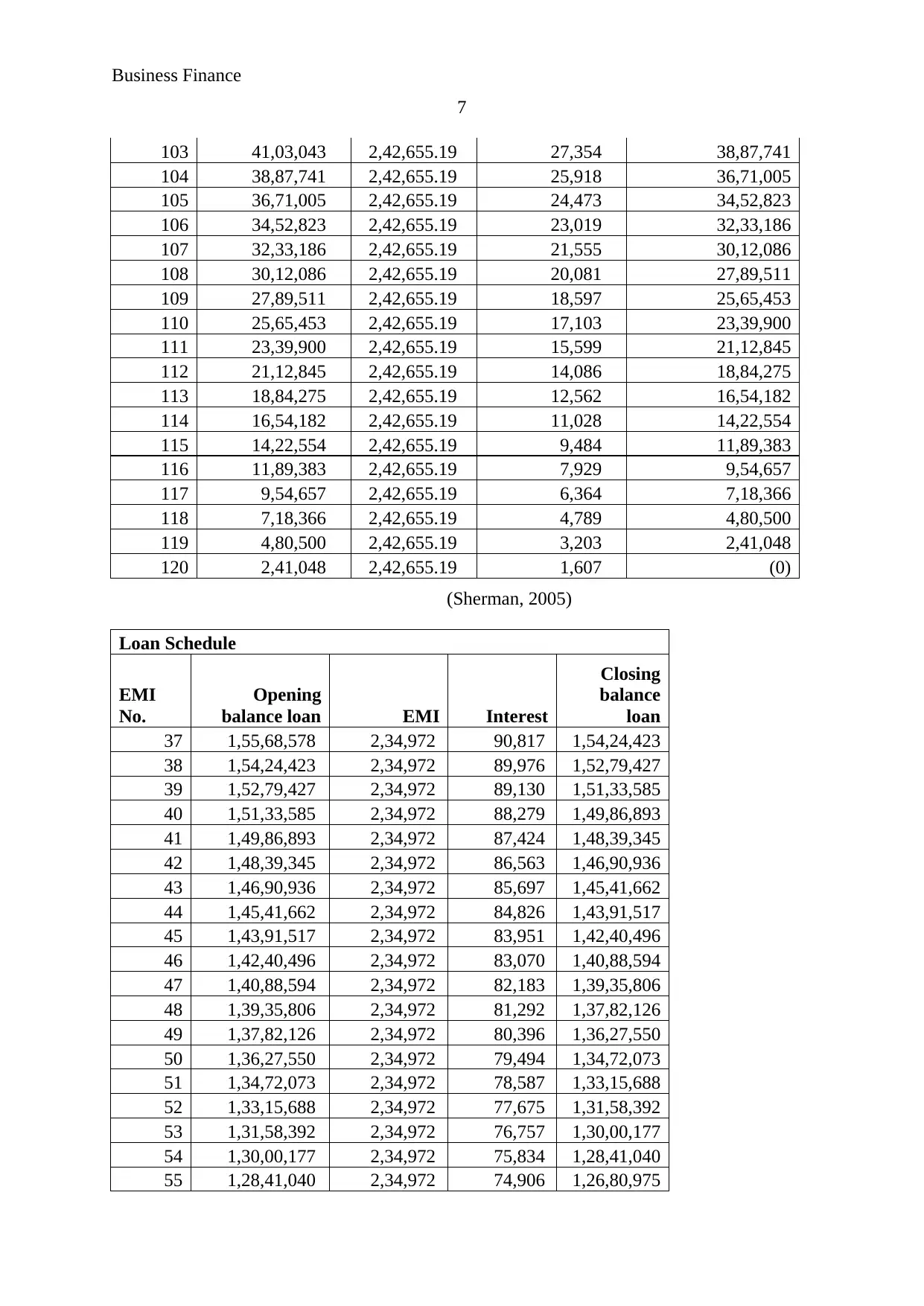

103 41,03,043 2,42,655.19 27,354 38,87,741

104 38,87,741 2,42,655.19 25,918 36,71,005

105 36,71,005 2,42,655.19 24,473 34,52,823

106 34,52,823 2,42,655.19 23,019 32,33,186

107 32,33,186 2,42,655.19 21,555 30,12,086

108 30,12,086 2,42,655.19 20,081 27,89,511

109 27,89,511 2,42,655.19 18,597 25,65,453

110 25,65,453 2,42,655.19 17,103 23,39,900

111 23,39,900 2,42,655.19 15,599 21,12,845

112 21,12,845 2,42,655.19 14,086 18,84,275

113 18,84,275 2,42,655.19 12,562 16,54,182

114 16,54,182 2,42,655.19 11,028 14,22,554

115 14,22,554 2,42,655.19 9,484 11,89,383

116 11,89,383 2,42,655.19 7,929 9,54,657

117 9,54,657 2,42,655.19 6,364 7,18,366

118 7,18,366 2,42,655.19 4,789 4,80,500

119 4,80,500 2,42,655.19 3,203 2,41,048

120 2,41,048 2,42,655.19 1,607 (0)

(Sherman, 2005)

Loan Schedule

EMI

No.

Opening

balance loan EMI Interest

Closing

balance

loan

37 1,55,68,578 2,34,972 90,817 1,54,24,423

38 1,54,24,423 2,34,972 89,976 1,52,79,427

39 1,52,79,427 2,34,972 89,130 1,51,33,585

40 1,51,33,585 2,34,972 88,279 1,49,86,893

41 1,49,86,893 2,34,972 87,424 1,48,39,345

42 1,48,39,345 2,34,972 86,563 1,46,90,936

43 1,46,90,936 2,34,972 85,697 1,45,41,662

44 1,45,41,662 2,34,972 84,826 1,43,91,517

45 1,43,91,517 2,34,972 83,951 1,42,40,496

46 1,42,40,496 2,34,972 83,070 1,40,88,594

47 1,40,88,594 2,34,972 82,183 1,39,35,806

48 1,39,35,806 2,34,972 81,292 1,37,82,126

49 1,37,82,126 2,34,972 80,396 1,36,27,550

50 1,36,27,550 2,34,972 79,494 1,34,72,073

51 1,34,72,073 2,34,972 78,587 1,33,15,688

52 1,33,15,688 2,34,972 77,675 1,31,58,392

53 1,31,58,392 2,34,972 76,757 1,30,00,177

54 1,30,00,177 2,34,972 75,834 1,28,41,040

55 1,28,41,040 2,34,972 74,906 1,26,80,975

7

103 41,03,043 2,42,655.19 27,354 38,87,741

104 38,87,741 2,42,655.19 25,918 36,71,005

105 36,71,005 2,42,655.19 24,473 34,52,823

106 34,52,823 2,42,655.19 23,019 32,33,186

107 32,33,186 2,42,655.19 21,555 30,12,086

108 30,12,086 2,42,655.19 20,081 27,89,511

109 27,89,511 2,42,655.19 18,597 25,65,453

110 25,65,453 2,42,655.19 17,103 23,39,900

111 23,39,900 2,42,655.19 15,599 21,12,845

112 21,12,845 2,42,655.19 14,086 18,84,275

113 18,84,275 2,42,655.19 12,562 16,54,182

114 16,54,182 2,42,655.19 11,028 14,22,554

115 14,22,554 2,42,655.19 9,484 11,89,383

116 11,89,383 2,42,655.19 7,929 9,54,657

117 9,54,657 2,42,655.19 6,364 7,18,366

118 7,18,366 2,42,655.19 4,789 4,80,500

119 4,80,500 2,42,655.19 3,203 2,41,048

120 2,41,048 2,42,655.19 1,607 (0)

(Sherman, 2005)

Loan Schedule

EMI

No.

Opening

balance loan EMI Interest

Closing

balance

loan

37 1,55,68,578 2,34,972 90,817 1,54,24,423

38 1,54,24,423 2,34,972 89,976 1,52,79,427

39 1,52,79,427 2,34,972 89,130 1,51,33,585

40 1,51,33,585 2,34,972 88,279 1,49,86,893

41 1,49,86,893 2,34,972 87,424 1,48,39,345

42 1,48,39,345 2,34,972 86,563 1,46,90,936

43 1,46,90,936 2,34,972 85,697 1,45,41,662

44 1,45,41,662 2,34,972 84,826 1,43,91,517

45 1,43,91,517 2,34,972 83,951 1,42,40,496

46 1,42,40,496 2,34,972 83,070 1,40,88,594

47 1,40,88,594 2,34,972 82,183 1,39,35,806

48 1,39,35,806 2,34,972 81,292 1,37,82,126

49 1,37,82,126 2,34,972 80,396 1,36,27,550

50 1,36,27,550 2,34,972 79,494 1,34,72,073

51 1,34,72,073 2,34,972 78,587 1,33,15,688

52 1,33,15,688 2,34,972 77,675 1,31,58,392

53 1,31,58,392 2,34,972 76,757 1,30,00,177

54 1,30,00,177 2,34,972 75,834 1,28,41,040

55 1,28,41,040 2,34,972 74,906 1,26,80,975

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

8

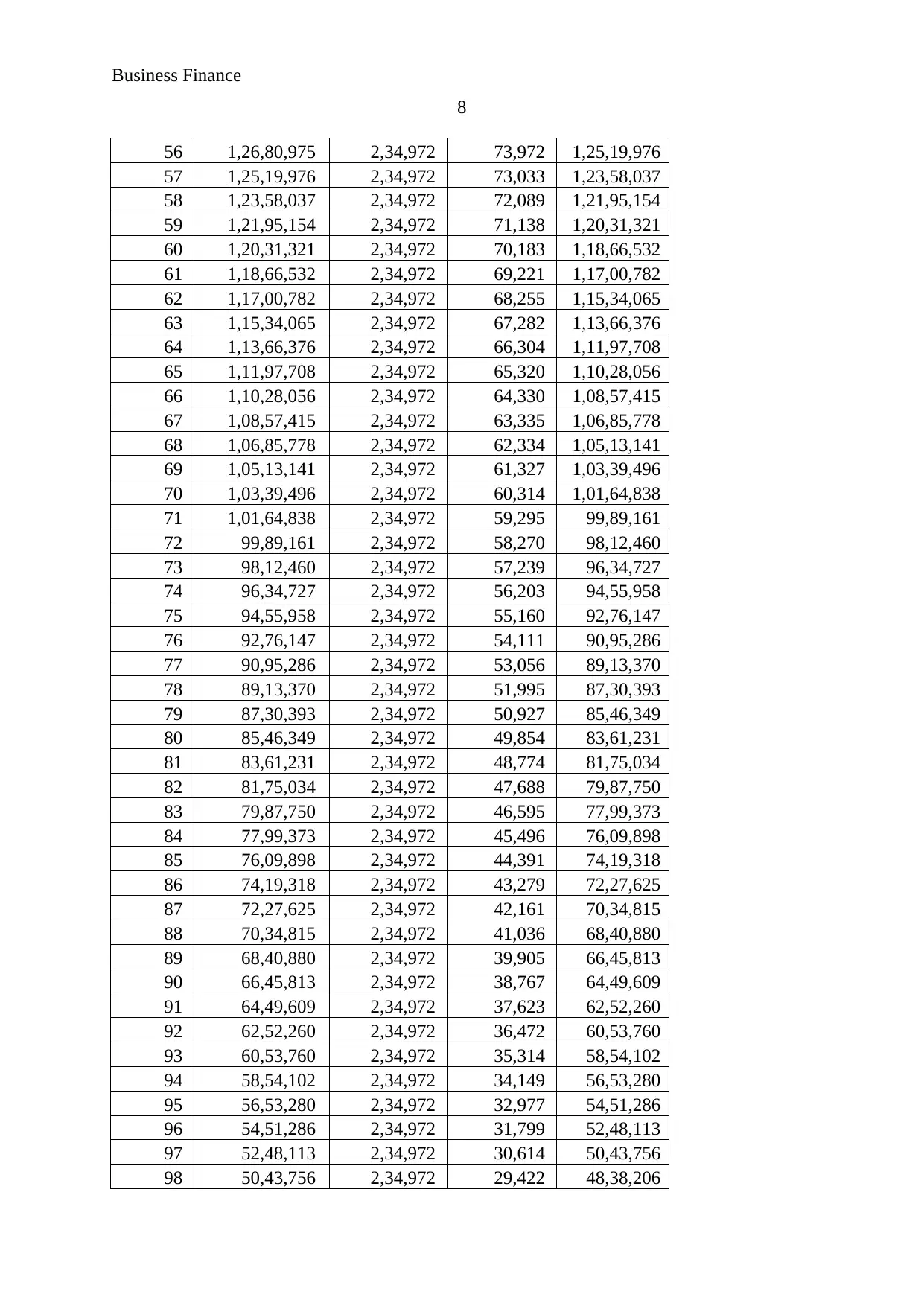

56 1,26,80,975 2,34,972 73,972 1,25,19,976

57 1,25,19,976 2,34,972 73,033 1,23,58,037

58 1,23,58,037 2,34,972 72,089 1,21,95,154

59 1,21,95,154 2,34,972 71,138 1,20,31,321

60 1,20,31,321 2,34,972 70,183 1,18,66,532

61 1,18,66,532 2,34,972 69,221 1,17,00,782

62 1,17,00,782 2,34,972 68,255 1,15,34,065

63 1,15,34,065 2,34,972 67,282 1,13,66,376

64 1,13,66,376 2,34,972 66,304 1,11,97,708

65 1,11,97,708 2,34,972 65,320 1,10,28,056

66 1,10,28,056 2,34,972 64,330 1,08,57,415

67 1,08,57,415 2,34,972 63,335 1,06,85,778

68 1,06,85,778 2,34,972 62,334 1,05,13,141

69 1,05,13,141 2,34,972 61,327 1,03,39,496

70 1,03,39,496 2,34,972 60,314 1,01,64,838

71 1,01,64,838 2,34,972 59,295 99,89,161

72 99,89,161 2,34,972 58,270 98,12,460

73 98,12,460 2,34,972 57,239 96,34,727

74 96,34,727 2,34,972 56,203 94,55,958

75 94,55,958 2,34,972 55,160 92,76,147

76 92,76,147 2,34,972 54,111 90,95,286

77 90,95,286 2,34,972 53,056 89,13,370

78 89,13,370 2,34,972 51,995 87,30,393

79 87,30,393 2,34,972 50,927 85,46,349

80 85,46,349 2,34,972 49,854 83,61,231

81 83,61,231 2,34,972 48,774 81,75,034

82 81,75,034 2,34,972 47,688 79,87,750

83 79,87,750 2,34,972 46,595 77,99,373

84 77,99,373 2,34,972 45,496 76,09,898

85 76,09,898 2,34,972 44,391 74,19,318

86 74,19,318 2,34,972 43,279 72,27,625

87 72,27,625 2,34,972 42,161 70,34,815

88 70,34,815 2,34,972 41,036 68,40,880

89 68,40,880 2,34,972 39,905 66,45,813

90 66,45,813 2,34,972 38,767 64,49,609

91 64,49,609 2,34,972 37,623 62,52,260

92 62,52,260 2,34,972 36,472 60,53,760

93 60,53,760 2,34,972 35,314 58,54,102

94 58,54,102 2,34,972 34,149 56,53,280

95 56,53,280 2,34,972 32,977 54,51,286

96 54,51,286 2,34,972 31,799 52,48,113

97 52,48,113 2,34,972 30,614 50,43,756

98 50,43,756 2,34,972 29,422 48,38,206

8

56 1,26,80,975 2,34,972 73,972 1,25,19,976

57 1,25,19,976 2,34,972 73,033 1,23,58,037

58 1,23,58,037 2,34,972 72,089 1,21,95,154

59 1,21,95,154 2,34,972 71,138 1,20,31,321

60 1,20,31,321 2,34,972 70,183 1,18,66,532

61 1,18,66,532 2,34,972 69,221 1,17,00,782

62 1,17,00,782 2,34,972 68,255 1,15,34,065

63 1,15,34,065 2,34,972 67,282 1,13,66,376

64 1,13,66,376 2,34,972 66,304 1,11,97,708

65 1,11,97,708 2,34,972 65,320 1,10,28,056

66 1,10,28,056 2,34,972 64,330 1,08,57,415

67 1,08,57,415 2,34,972 63,335 1,06,85,778

68 1,06,85,778 2,34,972 62,334 1,05,13,141

69 1,05,13,141 2,34,972 61,327 1,03,39,496

70 1,03,39,496 2,34,972 60,314 1,01,64,838

71 1,01,64,838 2,34,972 59,295 99,89,161

72 99,89,161 2,34,972 58,270 98,12,460

73 98,12,460 2,34,972 57,239 96,34,727

74 96,34,727 2,34,972 56,203 94,55,958

75 94,55,958 2,34,972 55,160 92,76,147

76 92,76,147 2,34,972 54,111 90,95,286

77 90,95,286 2,34,972 53,056 89,13,370

78 89,13,370 2,34,972 51,995 87,30,393

79 87,30,393 2,34,972 50,927 85,46,349

80 85,46,349 2,34,972 49,854 83,61,231

81 83,61,231 2,34,972 48,774 81,75,034

82 81,75,034 2,34,972 47,688 79,87,750

83 79,87,750 2,34,972 46,595 77,99,373

84 77,99,373 2,34,972 45,496 76,09,898

85 76,09,898 2,34,972 44,391 74,19,318

86 74,19,318 2,34,972 43,279 72,27,625

87 72,27,625 2,34,972 42,161 70,34,815

88 70,34,815 2,34,972 41,036 68,40,880

89 68,40,880 2,34,972 39,905 66,45,813

90 66,45,813 2,34,972 38,767 64,49,609

91 64,49,609 2,34,972 37,623 62,52,260

92 62,52,260 2,34,972 36,472 60,53,760

93 60,53,760 2,34,972 35,314 58,54,102

94 58,54,102 2,34,972 34,149 56,53,280

95 56,53,280 2,34,972 32,977 54,51,286

96 54,51,286 2,34,972 31,799 52,48,113

97 52,48,113 2,34,972 30,614 50,43,756

98 50,43,756 2,34,972 29,422 48,38,206

Business Finance

9

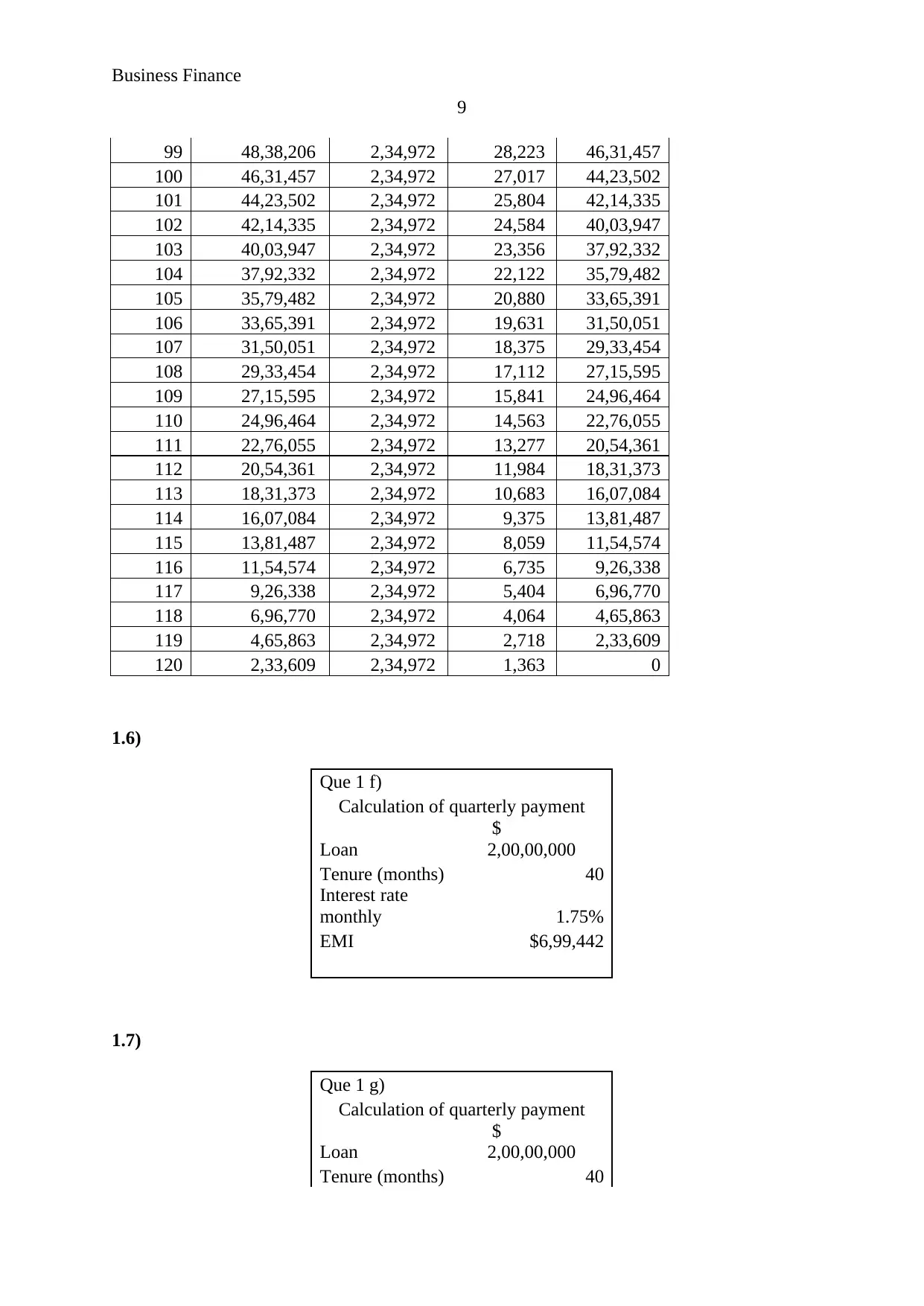

99 48,38,206 2,34,972 28,223 46,31,457

100 46,31,457 2,34,972 27,017 44,23,502

101 44,23,502 2,34,972 25,804 42,14,335

102 42,14,335 2,34,972 24,584 40,03,947

103 40,03,947 2,34,972 23,356 37,92,332

104 37,92,332 2,34,972 22,122 35,79,482

105 35,79,482 2,34,972 20,880 33,65,391

106 33,65,391 2,34,972 19,631 31,50,051

107 31,50,051 2,34,972 18,375 29,33,454

108 29,33,454 2,34,972 17,112 27,15,595

109 27,15,595 2,34,972 15,841 24,96,464

110 24,96,464 2,34,972 14,563 22,76,055

111 22,76,055 2,34,972 13,277 20,54,361

112 20,54,361 2,34,972 11,984 18,31,373

113 18,31,373 2,34,972 10,683 16,07,084

114 16,07,084 2,34,972 9,375 13,81,487

115 13,81,487 2,34,972 8,059 11,54,574

116 11,54,574 2,34,972 6,735 9,26,338

117 9,26,338 2,34,972 5,404 6,96,770

118 6,96,770 2,34,972 4,064 4,65,863

119 4,65,863 2,34,972 2,718 2,33,609

120 2,33,609 2,34,972 1,363 0

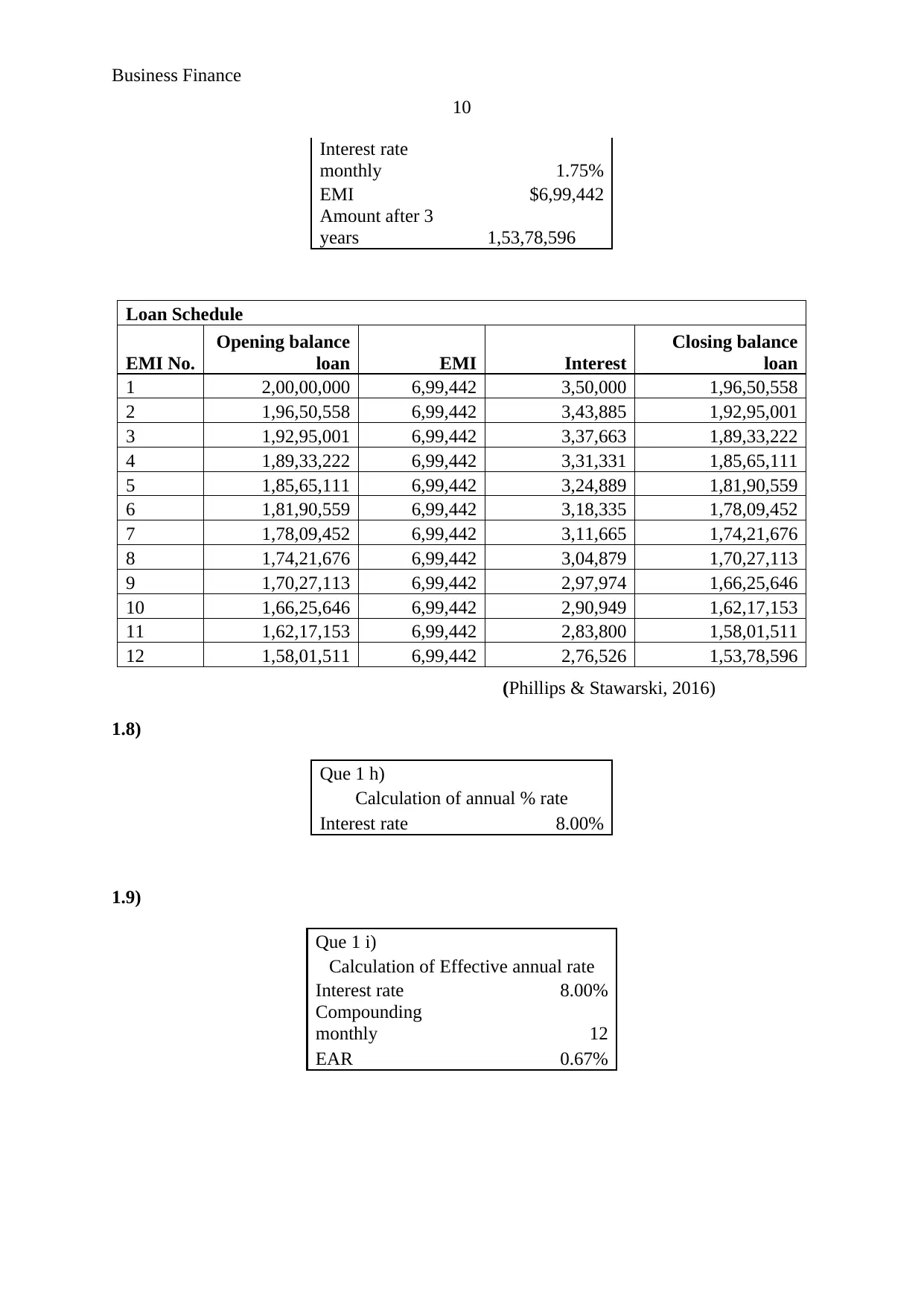

1.6)

Que 1 f)

Calculation of quarterly payment

Loan

$

2,00,00,000

Tenure (months) 40

Interest rate

monthly 1.75%

EMI $6,99,442

1.7)

Que 1 g)

Calculation of quarterly payment

Loan

$

2,00,00,000

Tenure (months) 40

9

99 48,38,206 2,34,972 28,223 46,31,457

100 46,31,457 2,34,972 27,017 44,23,502

101 44,23,502 2,34,972 25,804 42,14,335

102 42,14,335 2,34,972 24,584 40,03,947

103 40,03,947 2,34,972 23,356 37,92,332

104 37,92,332 2,34,972 22,122 35,79,482

105 35,79,482 2,34,972 20,880 33,65,391

106 33,65,391 2,34,972 19,631 31,50,051

107 31,50,051 2,34,972 18,375 29,33,454

108 29,33,454 2,34,972 17,112 27,15,595

109 27,15,595 2,34,972 15,841 24,96,464

110 24,96,464 2,34,972 14,563 22,76,055

111 22,76,055 2,34,972 13,277 20,54,361

112 20,54,361 2,34,972 11,984 18,31,373

113 18,31,373 2,34,972 10,683 16,07,084

114 16,07,084 2,34,972 9,375 13,81,487

115 13,81,487 2,34,972 8,059 11,54,574

116 11,54,574 2,34,972 6,735 9,26,338

117 9,26,338 2,34,972 5,404 6,96,770

118 6,96,770 2,34,972 4,064 4,65,863

119 4,65,863 2,34,972 2,718 2,33,609

120 2,33,609 2,34,972 1,363 0

1.6)

Que 1 f)

Calculation of quarterly payment

Loan

$

2,00,00,000

Tenure (months) 40

Interest rate

monthly 1.75%

EMI $6,99,442

1.7)

Que 1 g)

Calculation of quarterly payment

Loan

$

2,00,00,000

Tenure (months) 40

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance

10

Interest rate

monthly 1.75%

EMI $6,99,442

Amount after 3

years 1,53,78,596

Loan Schedule

EMI No.

Opening balance

loan EMI Interest

Closing balance

loan

1 2,00,00,000 6,99,442 3,50,000 1,96,50,558

2 1,96,50,558 6,99,442 3,43,885 1,92,95,001

3 1,92,95,001 6,99,442 3,37,663 1,89,33,222

4 1,89,33,222 6,99,442 3,31,331 1,85,65,111

5 1,85,65,111 6,99,442 3,24,889 1,81,90,559

6 1,81,90,559 6,99,442 3,18,335 1,78,09,452

7 1,78,09,452 6,99,442 3,11,665 1,74,21,676

8 1,74,21,676 6,99,442 3,04,879 1,70,27,113

9 1,70,27,113 6,99,442 2,97,974 1,66,25,646

10 1,66,25,646 6,99,442 2,90,949 1,62,17,153

11 1,62,17,153 6,99,442 2,83,800 1,58,01,511

12 1,58,01,511 6,99,442 2,76,526 1,53,78,596

(Phillips & Stawarski, 2016)

1.8)

Que 1 h)

Calculation of annual % rate

Interest rate 8.00%

1.9)

Que 1 i)

Calculation of Effective annual rate

Interest rate 8.00%

Compounding

monthly 12

EAR 0.67%

10

Interest rate

monthly 1.75%

EMI $6,99,442

Amount after 3

years 1,53,78,596

Loan Schedule

EMI No.

Opening balance

loan EMI Interest

Closing balance

loan

1 2,00,00,000 6,99,442 3,50,000 1,96,50,558

2 1,96,50,558 6,99,442 3,43,885 1,92,95,001

3 1,92,95,001 6,99,442 3,37,663 1,89,33,222

4 1,89,33,222 6,99,442 3,31,331 1,85,65,111

5 1,85,65,111 6,99,442 3,24,889 1,81,90,559

6 1,81,90,559 6,99,442 3,18,335 1,78,09,452

7 1,78,09,452 6,99,442 3,11,665 1,74,21,676

8 1,74,21,676 6,99,442 3,04,879 1,70,27,113

9 1,70,27,113 6,99,442 2,97,974 1,66,25,646

10 1,66,25,646 6,99,442 2,90,949 1,62,17,153

11 1,62,17,153 6,99,442 2,83,800 1,58,01,511

12 1,58,01,511 6,99,442 2,76,526 1,53,78,596

(Phillips & Stawarski, 2016)

1.8)

Que 1 h)

Calculation of annual % rate

Interest rate 8.00%

1.9)

Que 1 i)

Calculation of Effective annual rate

Interest rate 8.00%

Compounding

monthly 12

EAR 0.67%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance

11

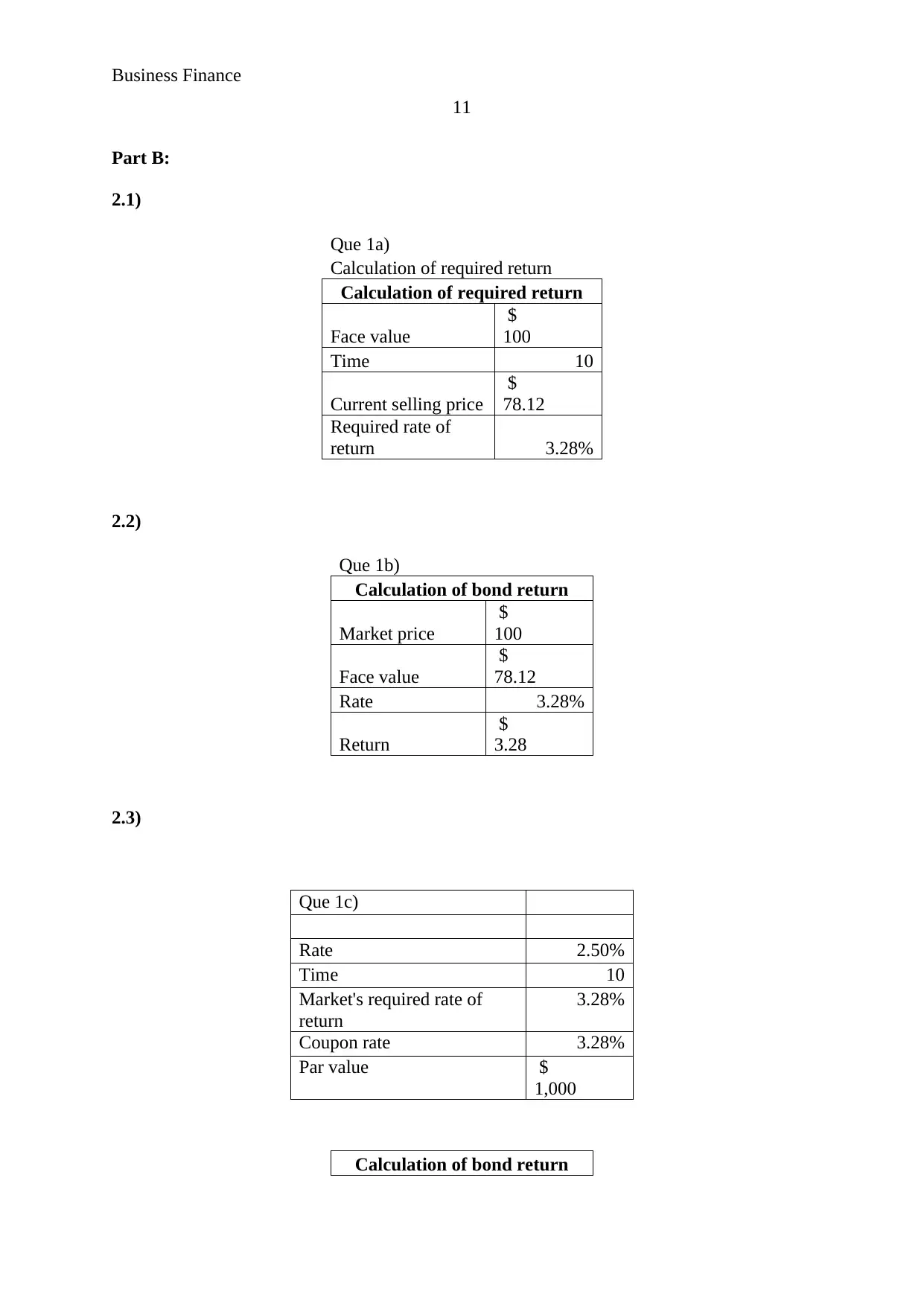

Part B:

2.1)

Que 1a)

Calculation of required return

Calculation of required return

Face value

$

100

Time 10

Current selling price

$

78.12

Required rate of

return 3.28%

2.2)

Que 1b)

Calculation of bond return

Market price

$

100

Face value

$

78.12

Rate 3.28%

Return

$

3.28

2.3)

Que 1c)

Rate 2.50%

Time 10

Market's required rate of

return

3.28%

Coupon rate 3.28%

Par value $

1,000

Calculation of bond return

11

Part B:

2.1)

Que 1a)

Calculation of required return

Calculation of required return

Face value

$

100

Time 10

Current selling price

$

78.12

Required rate of

return 3.28%

2.2)

Que 1b)

Calculation of bond return

Market price

$

100

Face value

$

78.12

Rate 3.28%

Return

$

3.28

2.3)

Que 1c)

Rate 2.50%

Time 10

Market's required rate of

return

3.28%

Coupon rate 3.28%

Par value $

1,000

Calculation of bond return

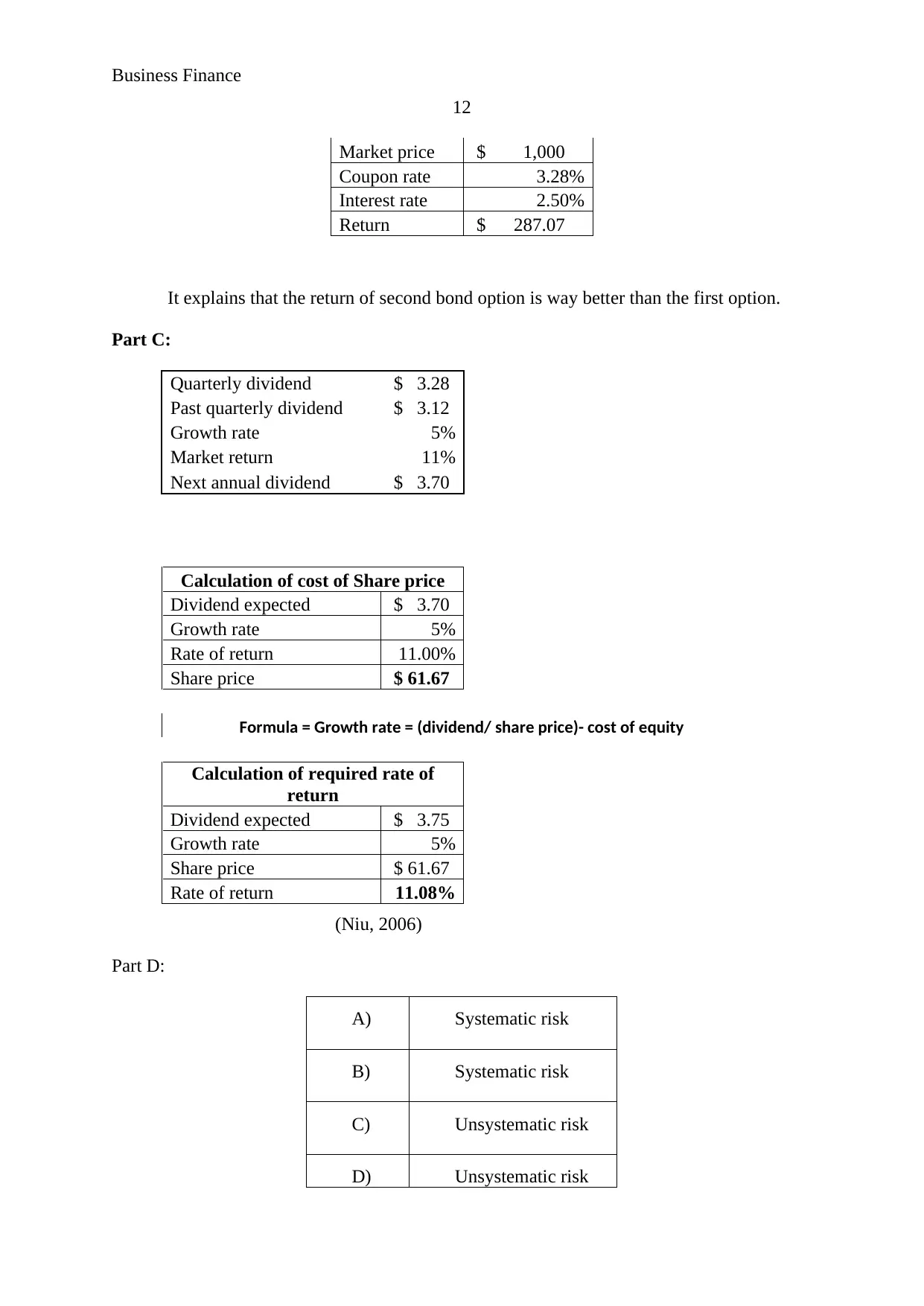

Business Finance

12

Market price $ 1,000

Coupon rate 3.28%

Interest rate 2.50%

Return $ 287.07

It explains that the return of second bond option is way better than the first option.

Part C:

Quarterly dividend $ 3.28

Past quarterly dividend $ 3.12

Growth rate 5%

Market return 11%

Next annual dividend $ 3.70

Calculation of cost of Share price

Dividend expected $ 3.70

Growth rate 5%

Rate of return 11.00%

Share price $ 61.67

Formula = Growth rate = (dividend/ share price)- cost of equity

Calculation of required rate of

return

Dividend expected $ 3.75

Growth rate 5%

Share price $ 61.67

Rate of return 11.08%

(Niu, 2006)

Part D:

A) Systematic risk

B) Systematic risk

C) Unsystematic risk

D) Unsystematic risk

12

Market price $ 1,000

Coupon rate 3.28%

Interest rate 2.50%

Return $ 287.07

It explains that the return of second bond option is way better than the first option.

Part C:

Quarterly dividend $ 3.28

Past quarterly dividend $ 3.12

Growth rate 5%

Market return 11%

Next annual dividend $ 3.70

Calculation of cost of Share price

Dividend expected $ 3.70

Growth rate 5%

Rate of return 11.00%

Share price $ 61.67

Formula = Growth rate = (dividend/ share price)- cost of equity

Calculation of required rate of

return

Dividend expected $ 3.75

Growth rate 5%

Share price $ 61.67

Rate of return 11.08%

(Niu, 2006)

Part D:

A) Systematic risk

B) Systematic risk

C) Unsystematic risk

D) Unsystematic risk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.