University Finance Report: Management Accounting Techniques and Tools

VerifiedAdded on 2023/01/13

|20

|4629

|57

Report

AI Summary

This report on management accounting delves into various techniques, focusing on cost analysis and budgeting. It begins with an introduction to management accounting and its significance, followed by an in-depth exploration of cost calculation methods, including marginal and absorption costing. The report provides detailed income statements for both costing methods, comparing their impact on profit and loss. It also covers the application of different management accounting techniques such as financial planning, financial statement analysis, cost accounting, fund flow analysis, cash flow analysis, standard costing, decision-making accounting, management information systems, statistical techniques, management reporting, and ratio analysis. Furthermore, the report explains the use of planning tools, particularly budgets, for planning and control, outlining the advantages and disadvantages of different budgetary control types. Finally, it examines how organizations can use management accounting to respond to financial problems, analyzing adaptations in management accounting systems to achieve sustainable success.

B07929

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 2...........................................................................................................................3

Introduction........................................................................................................................3

L.O.2: Apply a range of management accounting techniques..........................................3

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs................................................................3

M2. Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents........................................................................8

L.O.3: Explain the use of planning tools used in management accounting Using budgets

for planning and control:..................................................................................................11

P4. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control........................................................................................................11

M3. Use of different planning tools and their application for preparing and forecasting

budgets:...........................................................................................................................13

L. O. 4: Compare ways in which organizations could use management accounting to

respond to financial problems..........................................................................................14

P5. Compare how organizations are adapting management accounting systems to

respond to financial problems..........................................................................................14

M4. Analyze how, in responding to financial problems, management accounting can

lead organizations to sustainable success......................................................................17

Conclusion.......................................................................................................................19

REFERENCES________________________________________............................20

TASK 2...........................................................................................................................3

Introduction........................................................................................................................3

L.O.2: Apply a range of management accounting techniques..........................................3

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs................................................................3

M2. Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents........................................................................8

L.O.3: Explain the use of planning tools used in management accounting Using budgets

for planning and control:..................................................................................................11

P4. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control........................................................................................................11

M3. Use of different planning tools and their application for preparing and forecasting

budgets:...........................................................................................................................13

L. O. 4: Compare ways in which organizations could use management accounting to

respond to financial problems..........................................................................................14

P5. Compare how organizations are adapting management accounting systems to

respond to financial problems..........................................................................................14

M4. Analyze how, in responding to financial problems, management accounting can

lead organizations to sustainable success......................................................................17

Conclusion.......................................................................................................................19

REFERENCES________________________________________............................20

TASK 2

Introduction

Management accounting evolved before the Industrial Revolution. It is important for

the organisational people; it introduces specific information even for non-accountants

anytime, and observes present firm’s finances and helps creating actual professional

way out. In my words, Management accounting is accounting for managers to set up

reports using financial information to achieve business objectives, planning, control and

decision making. It mixes accounting, finance and management with the business skills

and techniques (What Is a Management Accounting System?, 2020). The scope of it is:

Cost Accounting, Tools and technique of management control, Tax accounting and

Statistical and quantitative techniques.

Managerial accounting is carrying out by identifying, measuring, analyzing,

interpreting, and communicating financial information to line managers for chase of an

organizational goal (What Is a Management Accounting System?, 2020).

L.O.2: Apply a range of management accounting techniques.

P3. Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption

costs

Costs: Costs are the expenses of business which is to be reduced from sales

revenue to get net profit earn by company during year.

Different costs and cost analysis:

There are mainly two types of costs; fixed and variable. Fixed costs are constant

over year and contains fixed amount paid by business for entire year; while on the

Introduction

Management accounting evolved before the Industrial Revolution. It is important for

the organisational people; it introduces specific information even for non-accountants

anytime, and observes present firm’s finances and helps creating actual professional

way out. In my words, Management accounting is accounting for managers to set up

reports using financial information to achieve business objectives, planning, control and

decision making. It mixes accounting, finance and management with the business skills

and techniques (What Is a Management Accounting System?, 2020). The scope of it is:

Cost Accounting, Tools and technique of management control, Tax accounting and

Statistical and quantitative techniques.

Managerial accounting is carrying out by identifying, measuring, analyzing,

interpreting, and communicating financial information to line managers for chase of an

organizational goal (What Is a Management Accounting System?, 2020).

L.O.2: Apply a range of management accounting techniques.

P3. Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption

costs

Costs: Costs are the expenses of business which is to be reduced from sales

revenue to get net profit earn by company during year.

Different costs and cost analysis:

There are mainly two types of costs; fixed and variable. Fixed costs are constant

over year and contains fixed amount paid by business for entire year; while on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

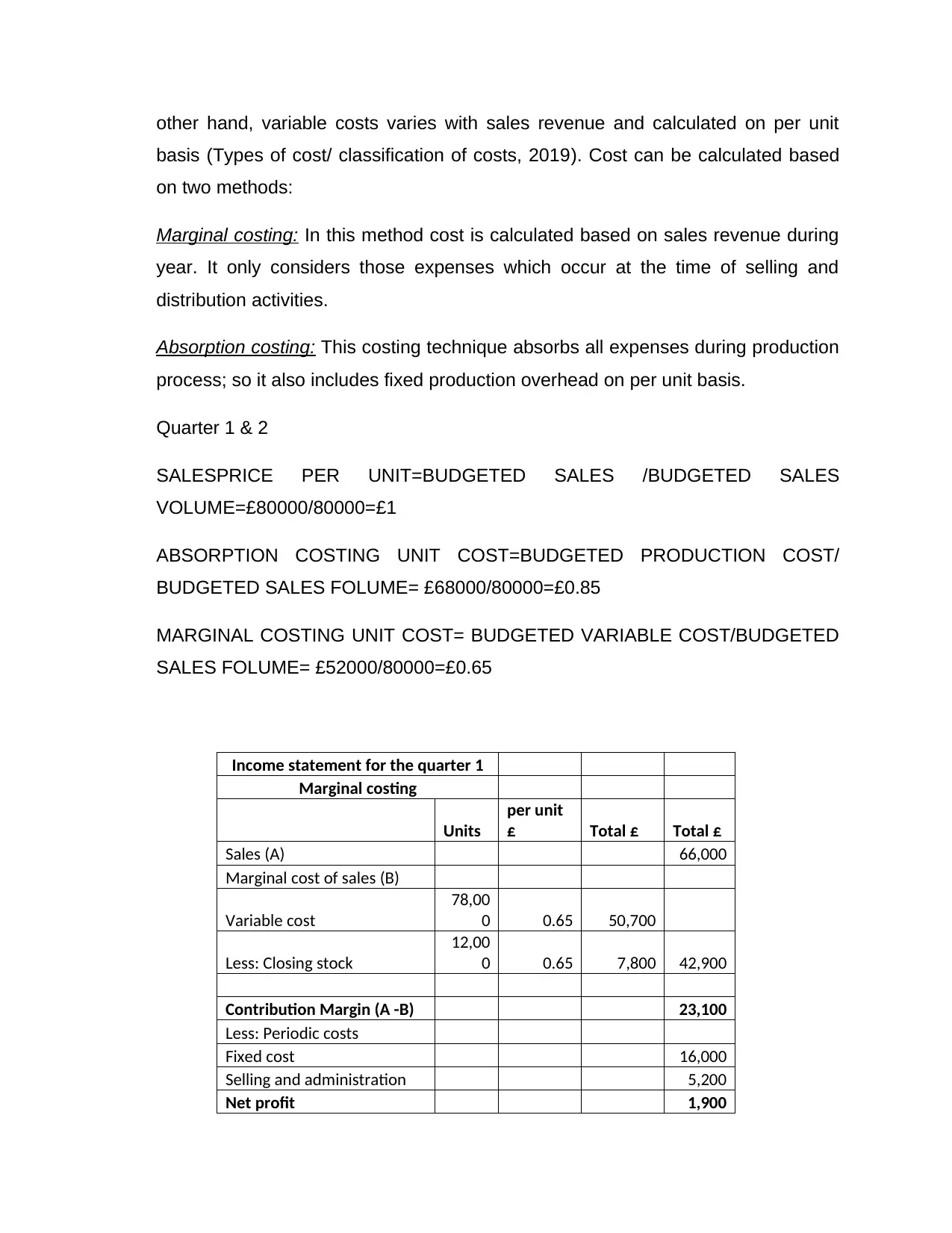

other hand, variable costs varies with sales revenue and calculated on per unit

basis (Types of cost/ classification of costs, 2019). Cost can be calculated based

on two methods:

Marginal costing: In this method cost is calculated based on sales revenue during

year. It only considers those expenses which occur at the time of selling and

distribution activities.

Absorption costing: This costing technique absorbs all expenses during production

process; so it also includes fixed production overhead on per unit basis.

Quarter 1 & 2

SALESPRICE PER UNIT=BUDGETED SALES /BUDGETED SALES

VOLUME=£80000/80000=£1

ABSORPTION COSTING UNIT COST=BUDGETED PRODUCTION COST/

BUDGETED SALES FOLUME= £68000/80000=£0.85

MARGINAL COSTING UNIT COST= BUDGETED VARIABLE COST/BUDGETED

SALES FOLUME= £52000/80000=£0.65

Income statement for the quarter 1

Marginal costing

Units

per unit

£ Total £ Total £

Sales (A) 66,000

Marginal cost of sales (B)

Variable cost

78,00

0 0.65 50,700

Less: Closing stock

12,00

0 0.65 7,800 42,900

Contribution Margin (A -B) 23,100

Less: Periodic costs

Fixed cost 16,000

Selling and administration 5,200

Net profit 1,900

basis (Types of cost/ classification of costs, 2019). Cost can be calculated based

on two methods:

Marginal costing: In this method cost is calculated based on sales revenue during

year. It only considers those expenses which occur at the time of selling and

distribution activities.

Absorption costing: This costing technique absorbs all expenses during production

process; so it also includes fixed production overhead on per unit basis.

Quarter 1 & 2

SALESPRICE PER UNIT=BUDGETED SALES /BUDGETED SALES

VOLUME=£80000/80000=£1

ABSORPTION COSTING UNIT COST=BUDGETED PRODUCTION COST/

BUDGETED SALES FOLUME= £68000/80000=£0.85

MARGINAL COSTING UNIT COST= BUDGETED VARIABLE COST/BUDGETED

SALES FOLUME= £52000/80000=£0.65

Income statement for the quarter 1

Marginal costing

Units

per unit

£ Total £ Total £

Sales (A) 66,000

Marginal cost of sales (B)

Variable cost

78,00

0 0.65 50,700

Less: Closing stock

12,00

0 0.65 7,800 42,900

Contribution Margin (A -B) 23,100

Less: Periodic costs

Fixed cost 16,000

Selling and administration 5,200

Net profit 1,900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

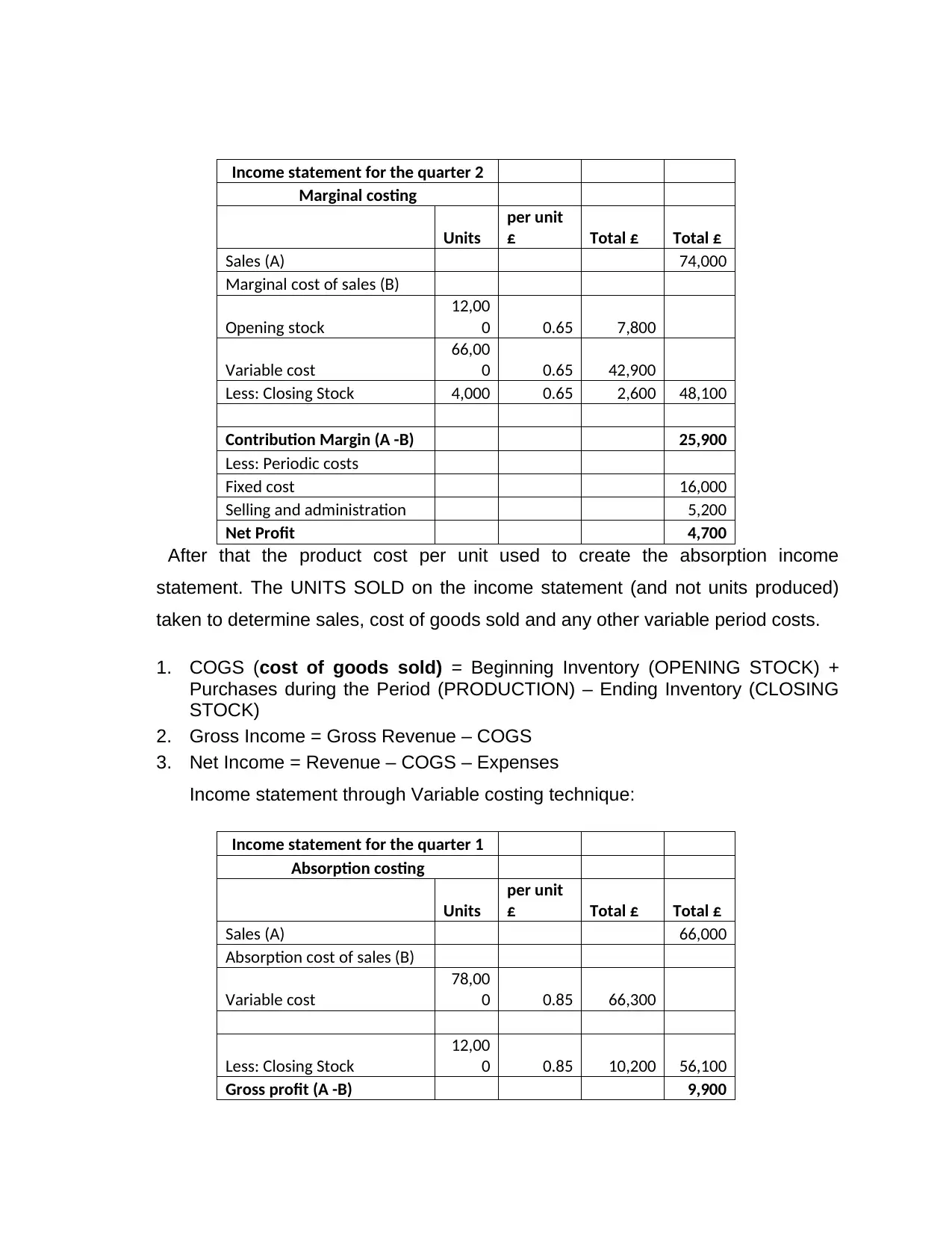

Income statement for the quarter 2

Marginal costing

Units

per unit

£ Total £ Total £

Sales (A) 74,000

Marginal cost of sales (B)

Opening stock

12,00

0 0.65 7,800

Variable cost

66,00

0 0.65 42,900

Less: Closing Stock 4,000 0.65 2,600 48,100

Contribution Margin (A -B) 25,900

Less: Periodic costs

Fixed cost 16,000

Selling and administration 5,200

Net Profit 4,700

After that the product cost per unit used to create the absorption income

statement. The UNITS SOLD on the income statement (and not units produced)

taken to determine sales, cost of goods sold and any other variable period costs.

1. COGS (cost of goods sold) = Beginning Inventory (OPENING STOCK) +

Purchases during the Period (PRODUCTION) – Ending Inventory (CLOSING

STOCK)

2. Gross Income = Gross Revenue – COGS

3. Net Income = Revenue – COGS – Expenses

Income statement through Variable costing technique:

Income statement for the quarter 1

Absorption costing

Units

per unit

£ Total £ Total £

Sales (A) 66,000

Absorption cost of sales (B)

Variable cost

78,00

0 0.85 66,300

Less: Closing Stock

12,00

0 0.85 10,200 56,100

Gross profit (A -B) 9,900

Marginal costing

Units

per unit

£ Total £ Total £

Sales (A) 74,000

Marginal cost of sales (B)

Opening stock

12,00

0 0.65 7,800

Variable cost

66,00

0 0.65 42,900

Less: Closing Stock 4,000 0.65 2,600 48,100

Contribution Margin (A -B) 25,900

Less: Periodic costs

Fixed cost 16,000

Selling and administration 5,200

Net Profit 4,700

After that the product cost per unit used to create the absorption income

statement. The UNITS SOLD on the income statement (and not units produced)

taken to determine sales, cost of goods sold and any other variable period costs.

1. COGS (cost of goods sold) = Beginning Inventory (OPENING STOCK) +

Purchases during the Period (PRODUCTION) – Ending Inventory (CLOSING

STOCK)

2. Gross Income = Gross Revenue – COGS

3. Net Income = Revenue – COGS – Expenses

Income statement through Variable costing technique:

Income statement for the quarter 1

Absorption costing

Units

per unit

£ Total £ Total £

Sales (A) 66,000

Absorption cost of sales (B)

Variable cost

78,00

0 0.85 66,300

Less: Closing Stock

12,00

0 0.85 10,200 56,100

Gross profit (A -B) 9,900

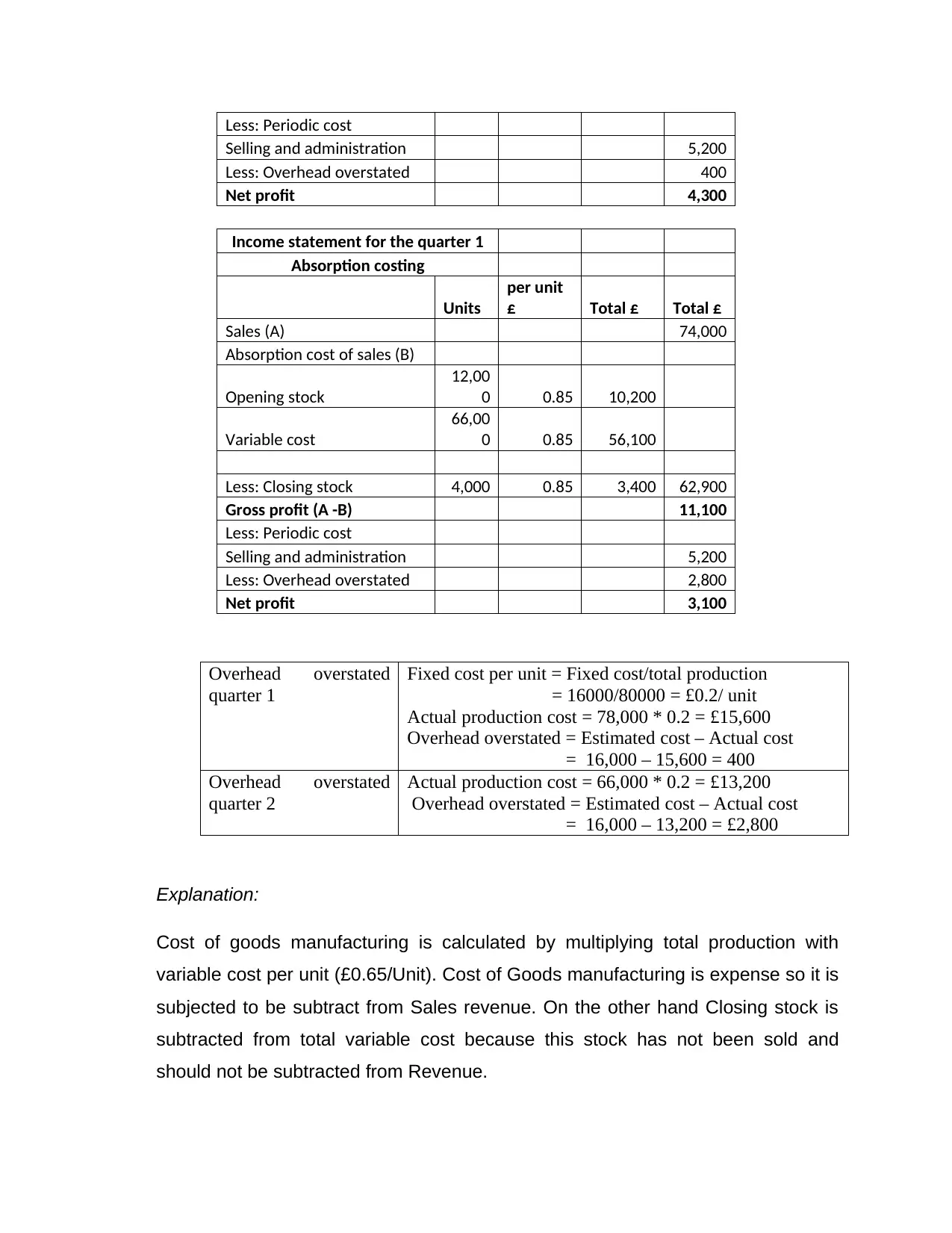

Less: Periodic cost

Selling and administration 5,200

Less: Overhead overstated 400

Net profit 4,300

Income statement for the quarter 1

Absorption costing

Units

per unit

£ Total £ Total £

Sales (A) 74,000

Absorption cost of sales (B)

Opening stock

12,00

0 0.85 10,200

Variable cost

66,00

0 0.85 56,100

Less: Closing stock 4,000 0.85 3,400 62,900

Gross profit (A -B) 11,100

Less: Periodic cost

Selling and administration 5,200

Less: Overhead overstated 2,800

Net profit 3,100

Overhead overstated

quarter 1

Fixed cost per unit = Fixed cost/total production

= 16000/80000 = £0.2/ unit

Actual production cost = 78,000 * 0.2 = £15,600

Overhead overstated = Estimated cost – Actual cost

= 16,000 – 15,600 = 400

Overhead overstated

quarter 2

Actual production cost = 66,000 * 0.2 = £13,200

Overhead overstated = Estimated cost – Actual cost

= 16,000 – 13,200 = £2,800

Explanation:

Cost of goods manufacturing is calculated by multiplying total production with

variable cost per unit (£0.65/Unit). Cost of Goods manufacturing is expense so it is

subjected to be subtract from Sales revenue. On the other hand Closing stock is

subtracted from total variable cost because this stock has not been sold and

should not be subtracted from Revenue.

Selling and administration 5,200

Less: Overhead overstated 400

Net profit 4,300

Income statement for the quarter 1

Absorption costing

Units

per unit

£ Total £ Total £

Sales (A) 74,000

Absorption cost of sales (B)

Opening stock

12,00

0 0.85 10,200

Variable cost

66,00

0 0.85 56,100

Less: Closing stock 4,000 0.85 3,400 62,900

Gross profit (A -B) 11,100

Less: Periodic cost

Selling and administration 5,200

Less: Overhead overstated 2,800

Net profit 3,100

Overhead overstated

quarter 1

Fixed cost per unit = Fixed cost/total production

= 16000/80000 = £0.2/ unit

Actual production cost = 78,000 * 0.2 = £15,600

Overhead overstated = Estimated cost – Actual cost

= 16,000 – 15,600 = 400

Overhead overstated

quarter 2

Actual production cost = 66,000 * 0.2 = £13,200

Overhead overstated = Estimated cost – Actual cost

= 16,000 – 13,200 = £2,800

Explanation:

Cost of goods manufacturing is calculated by multiplying total production with

variable cost per unit (£0.65/Unit). Cost of Goods manufacturing is expense so it is

subjected to be subtract from Sales revenue. On the other hand Closing stock is

subtracted from total variable cost because this stock has not been sold and

should not be subtracted from Revenue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reason for difference in Profit & Loss or Income statement calculating by Absorption

and Variable techniques:

The difference in Net profit of income statement through absorption and variable

costing is due to different gross profit.

Gross profit difference occurs due to different units while calculating variable cost

through variable and absorption costing method.

Absorption costing absorbs all cost of production, without considering how much

sales have done; while on the other hand; variable cost method only considers

cost which occurs at the time of selling product.

M2. Accurately apply a range of management accounting techniques

and produce appropriate financial reporting documents

There are various techniques of management accounting useful for organizations, but

all tools cannot help organization to achieve its targets. These techniques are discussed

below:

1. Financial Planning: The main aim of any organization is maximization of profits

by minimizing expenses. This aim can only be achieved through proper financial

planning. It is the best techniques for achieving business targets. There are 5

golden rules for better financial planning through Prime furniture can build sound

plan:

and Variable techniques:

The difference in Net profit of income statement through absorption and variable

costing is due to different gross profit.

Gross profit difference occurs due to different units while calculating variable cost

through variable and absorption costing method.

Absorption costing absorbs all cost of production, without considering how much

sales have done; while on the other hand; variable cost method only considers

cost which occurs at the time of selling product.

M2. Accurately apply a range of management accounting techniques

and produce appropriate financial reporting documents

There are various techniques of management accounting useful for organizations, but

all tools cannot help organization to achieve its targets. These techniques are discussed

below:

1. Financial Planning: The main aim of any organization is maximization of profits

by minimizing expenses. This aim can only be achieved through proper financial

planning. It is the best techniques for achieving business targets. There are 5

golden rules for better financial planning through Prime furniture can build sound

plan:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prime furniture can build unbreakable financial plan through identifying the

answers of above 5 strategic questions. The goal of Prime furniture is to deliver

genuine product to its consumers, it requires proper plan to cut its

manufacturing cost to bring feasible price in front of its customers. Company

was established in 2000, it’s not new comer it has enormous experience and

goodwill, hence company need not to take any risk which can harm its image.

But if talking about entering into new product Line Company should take

initiative to take risk invest in product modification and adding new product line

to grab new market.

2. Financial Statement Analysis: This statement consist Profit & loss a/c and

Balance Sheet. Financial statement analysis is done through comparative

financial statements, common size statements and ratio analysis of previous

years.

answers of above 5 strategic questions. The goal of Prime furniture is to deliver

genuine product to its consumers, it requires proper plan to cut its

manufacturing cost to bring feasible price in front of its customers. Company

was established in 2000, it’s not new comer it has enormous experience and

goodwill, hence company need not to take any risk which can harm its image.

But if talking about entering into new product Line Company should take

initiative to take risk invest in product modification and adding new product line

to grab new market.

2. Financial Statement Analysis: This statement consist Profit & loss a/c and

Balance Sheet. Financial statement analysis is done through comparative

financial statements, common size statements and ratio analysis of previous

years.

In case of Prime furniture, after doing analysis of its previous income statement

and Balance sheet with current year’s statement it was found that company’s

sales revenue has increased by 20% but its expenses also increased by 50%,

the reason behind this is company has invested handsome amount on

advertisement and brand promotion. So this increase in expenses is not an

issue as it will generate good revenue in near future. While on the other hand

Prime furniture’s ratio analysis report shows that company’s debt-equity ratio is

raised from 2/3 to 1/4 which means company debt is increased from previous

year. This can be an issue if company is not generating regular income to pay

its interests.

3. Cost Accounting: It shows cost information in product wise, department wise,

process wise and branch wise. These costs are compared with previous years

overall costs. These difference in costs of two or financial years’ helps

management in identifying the reason behind this increment.

As discussed above, Prime furniture’s cost is increased this financial year

due to more expenditure on promotions and advertisement of its products. So

it’s clear that this cost is incurring from sales and advertisement department.

This cost should not be considering as pure expenditure by company as it’s an

investment for future growth of the business.

4. Fund flow analysis: This analysis shows the report on the movement of fund

from one period to another. These analysis useful to get information whether the

fund is properly utilized or not. Fund flow consists of two side’s application of

funds (expenses) and sources of funds (loan and equity). It’s a mixture of both

balance sheet and income statement.

Prime furniture fund flow analysis reveal that company’s working capital has

increased in comparison with previous year due to hiring of more sales persons

but this recruitment is for business expansion and will be source of income for

Prime furniture.

5. Cash flow analysis: Through cash flow statement company knows about

movement of cash from one period to another. Besides these changes in cash

and Balance sheet with current year’s statement it was found that company’s

sales revenue has increased by 20% but its expenses also increased by 50%,

the reason behind this is company has invested handsome amount on

advertisement and brand promotion. So this increase in expenses is not an

issue as it will generate good revenue in near future. While on the other hand

Prime furniture’s ratio analysis report shows that company’s debt-equity ratio is

raised from 2/3 to 1/4 which means company debt is increased from previous

year. This can be an issue if company is not generating regular income to pay

its interests.

3. Cost Accounting: It shows cost information in product wise, department wise,

process wise and branch wise. These costs are compared with previous years

overall costs. These difference in costs of two or financial years’ helps

management in identifying the reason behind this increment.

As discussed above, Prime furniture’s cost is increased this financial year

due to more expenditure on promotions and advertisement of its products. So

it’s clear that this cost is incurring from sales and advertisement department.

This cost should not be considering as pure expenditure by company as it’s an

investment for future growth of the business.

4. Fund flow analysis: This analysis shows the report on the movement of fund

from one period to another. These analysis useful to get information whether the

fund is properly utilized or not. Fund flow consists of two side’s application of

funds (expenses) and sources of funds (loan and equity). It’s a mixture of both

balance sheet and income statement.

Prime furniture fund flow analysis reveal that company’s working capital has

increased in comparison with previous year due to hiring of more sales persons

but this recruitment is for business expansion and will be source of income for

Prime furniture.

5. Cash flow analysis: Through cash flow statement company knows about

movement of cash from one period to another. Besides these changes in cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

balance for two periods also reveals by this analysis. Cash flow statement is

different from Fund flow statement as in cash flow statement it calculates cash

in and out from 3 different activities like operating, investing and financial

activities.

Prime furniture’s cash flow analysis shows that company’s cash from

operations is negative that means cash out from operational activities due to

changes in working capital. Company has not invested in any business so there

is no change in investment activities, while financial activities shows increase in

equity shares as company has issued some shares to increase its funds.

6. Standard Costing: It is predetermined cost, it is useful in measuring actual

performance of the company.

7. Decision-making Accounting: This technique is useful in solving business

problem by choosing best alternatives. To find such alternatives relevant costs

are compared,

Prime furniture can solve the business problem arising due to increasing in

complexity of nature of business processes.

8. Management Information System: This technique is useful in integrating

different line departments and stores into one system. Prime Furniture use this

tool to get exact number on how much stock is left, how much money is blocked

into market and how much time it will take to deliver product to the customer.

Other then this company will also get to know what current status of unused

inventory.

9. Statistical Techniques: There are various statistical techniques used for

removing management problems like least square, regression and quality

control tool. Prime furniture has raised the quality of its product through quality

control tool and estimates its future sales through regression method.

10. Management Reporting: This report consists of information’s of financial

statement of previous years. Prime furniture use this report to find its business

growth, wealth and its financial health.

different from Fund flow statement as in cash flow statement it calculates cash

in and out from 3 different activities like operating, investing and financial

activities.

Prime furniture’s cash flow analysis shows that company’s cash from

operations is negative that means cash out from operational activities due to

changes in working capital. Company has not invested in any business so there

is no change in investment activities, while financial activities shows increase in

equity shares as company has issued some shares to increase its funds.

6. Standard Costing: It is predetermined cost, it is useful in measuring actual

performance of the company.

7. Decision-making Accounting: This technique is useful in solving business

problem by choosing best alternatives. To find such alternatives relevant costs

are compared,

Prime furniture can solve the business problem arising due to increasing in

complexity of nature of business processes.

8. Management Information System: This technique is useful in integrating

different line departments and stores into one system. Prime Furniture use this

tool to get exact number on how much stock is left, how much money is blocked

into market and how much time it will take to deliver product to the customer.

Other then this company will also get to know what current status of unused

inventory.

9. Statistical Techniques: There are various statistical techniques used for

removing management problems like least square, regression and quality

control tool. Prime furniture has raised the quality of its product through quality

control tool and estimates its future sales through regression method.

10. Management Reporting: This report consists of information’s of financial

statement of previous years. Prime furniture use this report to find its business

growth, wealth and its financial health.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio Analysis: This is the more powerful technique to get estimate performance

of the company. But this analysis has a drawback that it only expresses data in

proportional and percentage basis.

L.O.3: Explain the use of planning tools used in management

accounting Using budgets for planning and control:

P4. Explain the advantages and disadvantages of different types of

planning tools used for budgetary control.

Budget: The budget is a quantitative as well as fiscal articulation of approach for a

characterized future period (Budgeting and Forecasting Software, 2020).

Importance of Budget:

Budgets facilitate effective control.

Budgets facilitate coordination and communication.

Budgets facilitate record keeping.

Budgets are a natural complement to planning (Budgeting software, 2020).

Types of Budgets:

1. Cash flow budget: It is forecasting of future cash inflow and outflow into the

business. It is prepared for specific time period which is one year. The elements

taken by cash flow budget are accounts payables and receivables.

2. Operating budget: This budget forecasts future operational activities of the

business like selling and distribution, paying salaries, advertisement and

marketing expenses. This budget support in knowing estimated net earnings gain

by business in next year.

3. Financial budget: This budget covers the strategies and estimation made by

managerial accountant for managing assets, income statement and other

of the company. But this analysis has a drawback that it only expresses data in

proportional and percentage basis.

L.O.3: Explain the use of planning tools used in management

accounting Using budgets for planning and control:

P4. Explain the advantages and disadvantages of different types of

planning tools used for budgetary control.

Budget: The budget is a quantitative as well as fiscal articulation of approach for a

characterized future period (Budgeting and Forecasting Software, 2020).

Importance of Budget:

Budgets facilitate effective control.

Budgets facilitate coordination and communication.

Budgets facilitate record keeping.

Budgets are a natural complement to planning (Budgeting software, 2020).

Types of Budgets:

1. Cash flow budget: It is forecasting of future cash inflow and outflow into the

business. It is prepared for specific time period which is one year. The elements

taken by cash flow budget are accounts payables and receivables.

2. Operating budget: This budget forecasts future operational activities of the

business like selling and distribution, paying salaries, advertisement and

marketing expenses. This budget support in knowing estimated net earnings gain

by business in next year.

3. Financial budget: This budget covers the strategies and estimation made by

managerial accountant for managing assets, income statement and other

financial related documentations. It is prepared to identify the elements which

can affect wealth of company.

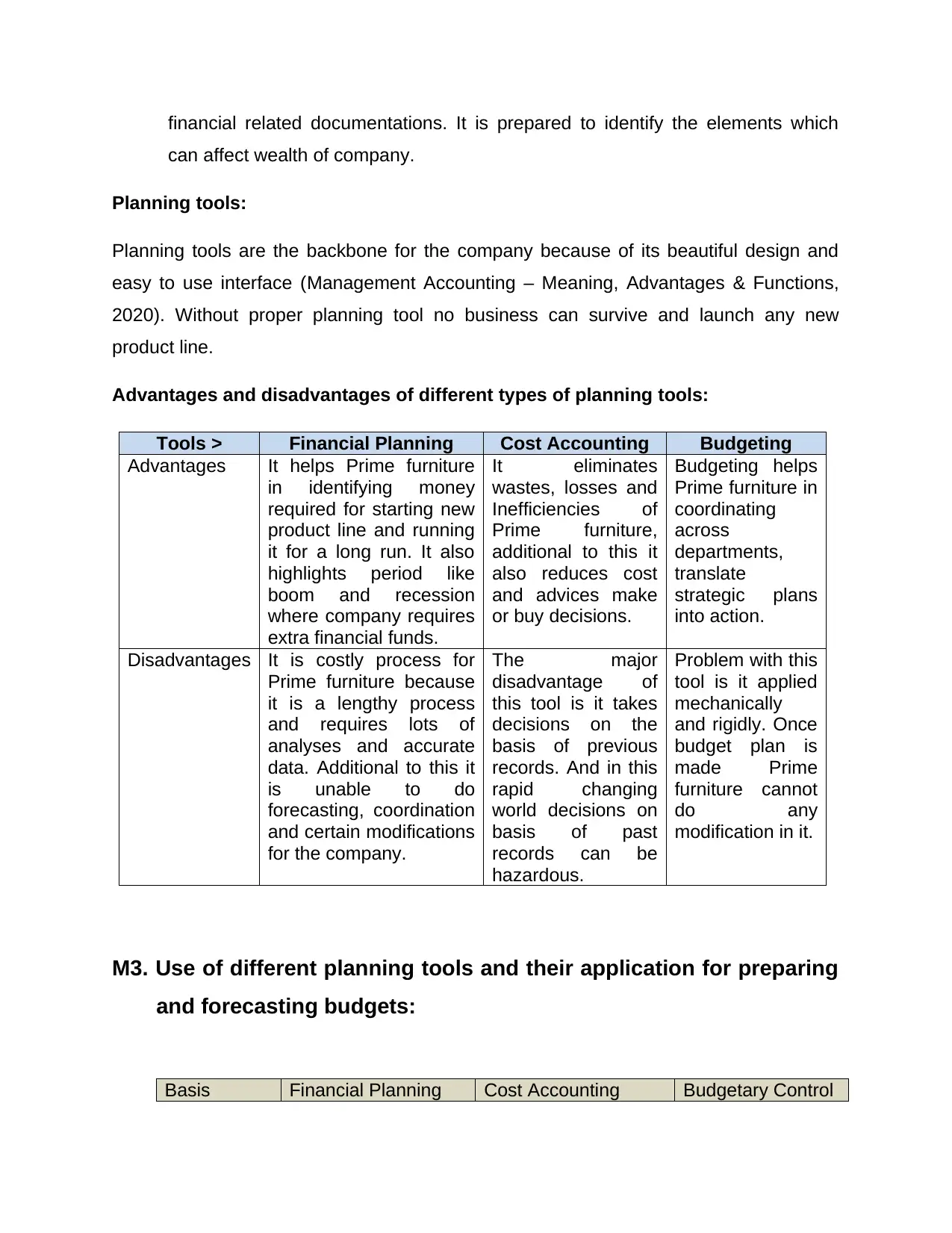

Planning tools:

Planning tools are the backbone for the company because of its beautiful design and

easy to use interface (Management Accounting – Meaning, Advantages & Functions,

2020). Without proper planning tool no business can survive and launch any new

product line.

Advantages and disadvantages of different types of planning tools:

Tools ˃ Financial Planning Cost Accounting Budgeting

Advantages It helps Prime furniture

in identifying money

required for starting new

product line and running

it for a long run. It also

highlights period like

boom and recession

where company requires

extra financial funds.

It eliminates

wastes, losses and

Inefficiencies of

Prime furniture,

additional to this it

also reduces cost

and advices make

or buy decisions.

Budgeting helps

Prime furniture in

coordinating

across

departments,

translate

strategic plans

into action.

Disadvantages It is costly process for

Prime furniture because

it is a lengthy process

and requires lots of

analyses and accurate

data. Additional to this it

is unable to do

forecasting, coordination

and certain modifications

for the company.

The major

disadvantage of

this tool is it takes

decisions on the

basis of previous

records. And in this

rapid changing

world decisions on

basis of past

records can be

hazardous.

Problem with this

tool is it applied

mechanically

and rigidly. Once

budget plan is

made Prime

furniture cannot

do any

modification in it.

M3. Use of different planning tools and their application for preparing

and forecasting budgets:

Basis Financial Planning Cost Accounting Budgetary Control

can affect wealth of company.

Planning tools:

Planning tools are the backbone for the company because of its beautiful design and

easy to use interface (Management Accounting – Meaning, Advantages & Functions,

2020). Without proper planning tool no business can survive and launch any new

product line.

Advantages and disadvantages of different types of planning tools:

Tools ˃ Financial Planning Cost Accounting Budgeting

Advantages It helps Prime furniture

in identifying money

required for starting new

product line and running

it for a long run. It also

highlights period like

boom and recession

where company requires

extra financial funds.

It eliminates

wastes, losses and

Inefficiencies of

Prime furniture,

additional to this it

also reduces cost

and advices make

or buy decisions.

Budgeting helps

Prime furniture in

coordinating

across

departments,

translate

strategic plans

into action.

Disadvantages It is costly process for

Prime furniture because

it is a lengthy process

and requires lots of

analyses and accurate

data. Additional to this it

is unable to do

forecasting, coordination

and certain modifications

for the company.

The major

disadvantage of

this tool is it takes

decisions on the

basis of previous

records. And in this

rapid changing

world decisions on

basis of past

records can be

hazardous.

Problem with this

tool is it applied

mechanically

and rigidly. Once

budget plan is

made Prime

furniture cannot

do any

modification in it.

M3. Use of different planning tools and their application for preparing

and forecasting budgets:

Basis Financial Planning Cost Accounting Budgetary Control

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.