University Finance Report: Time Value Concepts in Management Decisions

VerifiedAdded on 2021/06/18

|44

|10106

|153

Report

AI Summary

This comprehensive report delves into the core concepts of business finance, focusing on the time value of money and its implications in management decisions. It begins by explaining the fundamental principles of time value, including present and future value calculations, discounting, and compounding processes. The report then explores the application of these concepts in the valuation of financial instruments such as bonds, equity, and preference shares, highlighting their advantages and disadvantages. Furthermore, it examines the role of time value in capital budgeting, analyzing the impact of exchange rates and other economic factors. The report also addresses potential issues associated with time value of money calculations and concludes with a case study analyzing Studebaker's financial goals and investment strategies.

Running head: BUSINESS FINANCE

Business Finance

Student Name

University Name

Business Finance

Student Name

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

BUSINESS FINANCE

Table of Contents

Task 1 Time value concepts in management decisions...................................................................3

Task 2:-..........................................................................................................................................11

Question 1......................................................................................................................................11

Question 2......................................................................................................................................11

Question 3......................................................................................................................................12

Question 4......................................................................................................................................21

Question 5......................................................................................................................................32

Question 6a....................................................................................................................................34

Question 6b....................................................................................................................................35

Question 7......................................................................................................................................36

Question 8......................................................................................................................................38

Question 9a and 9b........................................................................................................................38

Question 10....................................................................................................................................42

Question 11...................................................................................................................................47

Question 12....................................................................................................................................47

Question 13....................................................................................................................................48

References and Bibliography.........................................................................................................49

BUSINESS FINANCE

Table of Contents

Task 1 Time value concepts in management decisions...................................................................3

Task 2:-..........................................................................................................................................11

Question 1......................................................................................................................................11

Question 2......................................................................................................................................11

Question 3......................................................................................................................................12

Question 4......................................................................................................................................21

Question 5......................................................................................................................................32

Question 6a....................................................................................................................................34

Question 6b....................................................................................................................................35

Question 7......................................................................................................................................36

Question 8......................................................................................................................................38

Question 9a and 9b........................................................................................................................38

Question 10....................................................................................................................................42

Question 11...................................................................................................................................47

Question 12....................................................................................................................................47

Question 13....................................................................................................................................48

References and Bibliography.........................................................................................................49

3

BUSINESS FINANCE

Task 1 Time value concepts in management decisions

Answer a: Fundamentals of time value concepts

The Concept of time value of money indicates that value of money depreciates year after year.

It further reflects that at the present value of money is more than the future value. As per Chan

and Rate (2018), time value of money refers to the concept that the value of money at present is

more than the value the amount of money would have in the future. This is due to the potential

earning capacity of money. A certain amount of money would earn more amount of interest if it

is deposited at an earlier phase provided the rate of interest remains the same (Burns and Walker

2015).

For example, if $1000 is deposited at 10 percent interest for 1 year on 01.01.2018, it would earn

an interest of $100 and the total amount combining the principal and interest would come to

$1100 on 01.01.2019. Again, if the same amount of $1000 is deposited for 6 months on

01.07.2018, at 10 percent it would only yield at interest of 50. This means that the total amount

would come to $ 1050 on 01.01.2019.

The above example shows that money used earlier would bear more utility than used in

the future. One can point out that for same amount of money, the value of disbursement remains

the same but the utility or benefit that can be availed or purchased with that money will be less in

future. This difference is known as opportunity cost which a person incurs because he used a

certain amount of money in the future. The value of time value of money is as follows:

FV=PV*[1+ (i/n)] ^ (n*t)

BUSINESS FINANCE

Task 1 Time value concepts in management decisions

Answer a: Fundamentals of time value concepts

The Concept of time value of money indicates that value of money depreciates year after year.

It further reflects that at the present value of money is more than the future value. As per Chan

and Rate (2018), time value of money refers to the concept that the value of money at present is

more than the value the amount of money would have in the future. This is due to the potential

earning capacity of money. A certain amount of money would earn more amount of interest if it

is deposited at an earlier phase provided the rate of interest remains the same (Burns and Walker

2015).

For example, if $1000 is deposited at 10 percent interest for 1 year on 01.01.2018, it would earn

an interest of $100 and the total amount combining the principal and interest would come to

$1100 on 01.01.2019. Again, if the same amount of $1000 is deposited for 6 months on

01.07.2018, at 10 percent it would only yield at interest of 50. This means that the total amount

would come to $ 1050 on 01.01.2019.

The above example shows that money used earlier would bear more utility than used in

the future. One can point out that for same amount of money, the value of disbursement remains

the same but the utility or benefit that can be availed or purchased with that money will be less in

future. This difference is known as opportunity cost which a person incurs because he used a

certain amount of money in the future. The value of time value of money is as follows:

FV=PV*[1+ (i/n)] ^ (n*t)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

BUSINESS FINANCE

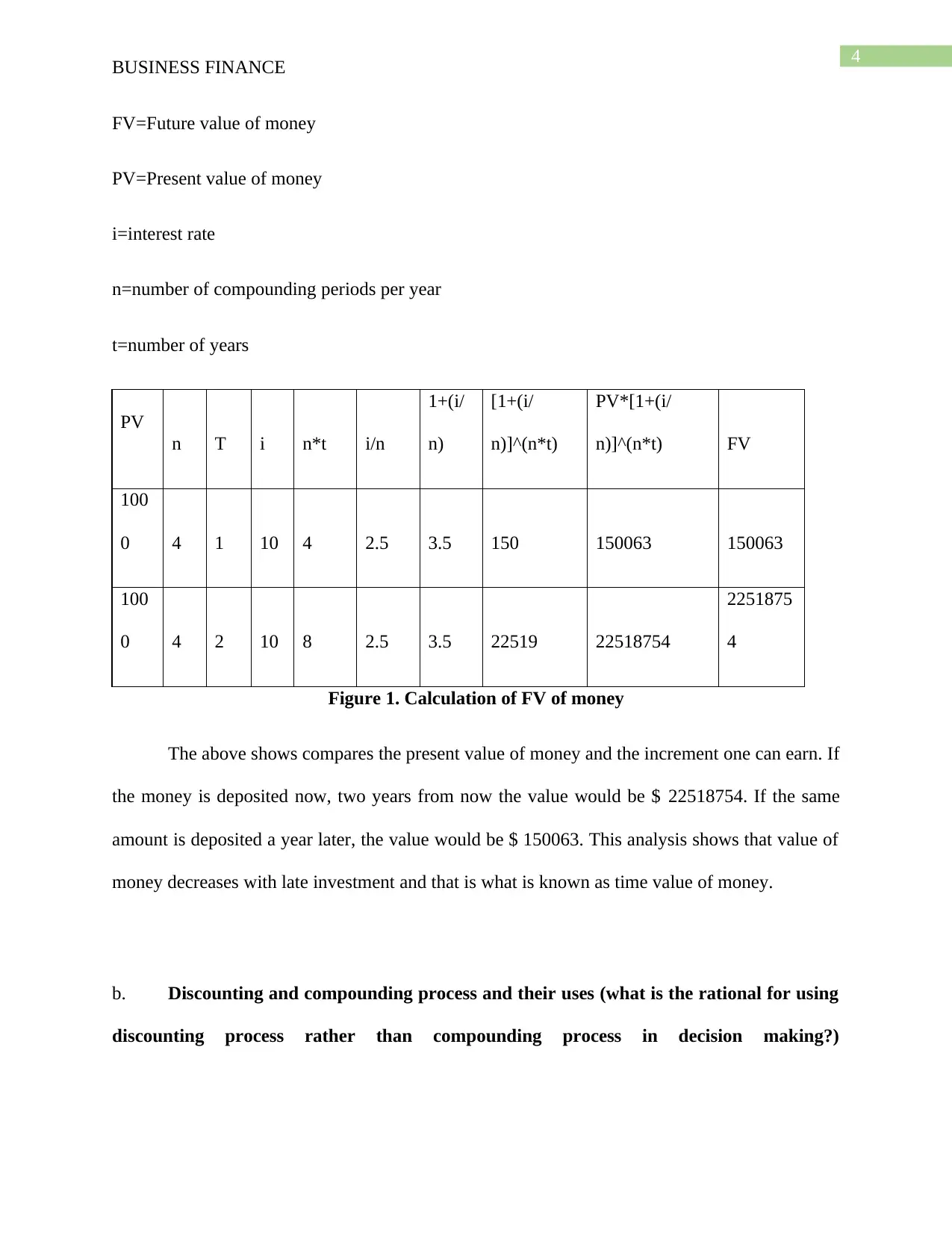

FV=Future value of money

PV=Present value of money

i=interest rate

n=number of compounding periods per year

t=number of years

PV

n T i n*t i/n

1+(i/

n)

[1+(i/

n)]^(n*t)

PV*[1+(i/

n)]^(n*t) FV

100

0 4 1 10 4 2.5 3.5 150 150063 150063

100

0 4 2 10 8 2.5 3.5 22519 22518754

2251875

4

Figure 1. Calculation of FV of money

The above shows compares the present value of money and the increment one can earn. If

the money is deposited now, two years from now the value would be $ 22518754. If the same

amount is deposited a year later, the value would be $ 150063. This analysis shows that value of

money decreases with late investment and that is what is known as time value of money.

b. Discounting and compounding process and their uses (what is the rational for using

discounting process rather than compounding process in decision making?)

BUSINESS FINANCE

FV=Future value of money

PV=Present value of money

i=interest rate

n=number of compounding periods per year

t=number of years

PV

n T i n*t i/n

1+(i/

n)

[1+(i/

n)]^(n*t)

PV*[1+(i/

n)]^(n*t) FV

100

0 4 1 10 4 2.5 3.5 150 150063 150063

100

0 4 2 10 8 2.5 3.5 22519 22518754

2251875

4

Figure 1. Calculation of FV of money

The above shows compares the present value of money and the increment one can earn. If

the money is deposited now, two years from now the value would be $ 22518754. If the same

amount is deposited a year later, the value would be $ 150063. This analysis shows that value of

money decreases with late investment and that is what is known as time value of money.

b. Discounting and compounding process and their uses (what is the rational for using

discounting process rather than compounding process in decision making?)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

BUSINESS FINANCE

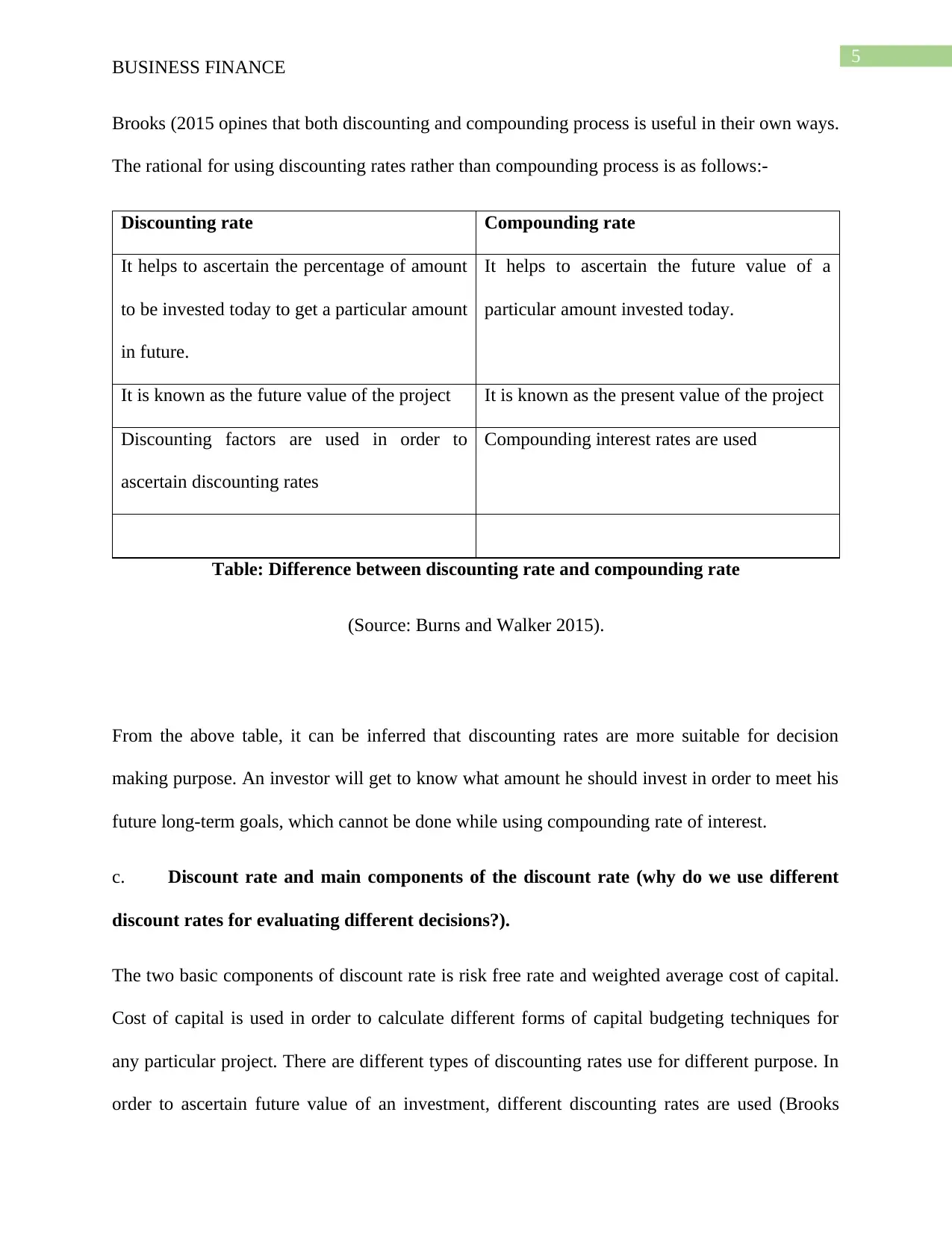

Brooks (2015 opines that both discounting and compounding process is useful in their own ways.

The rational for using discounting rates rather than compounding process is as follows:-

Discounting rate Compounding rate

It helps to ascertain the percentage of amount

to be invested today to get a particular amount

in future.

It helps to ascertain the future value of a

particular amount invested today.

It is known as the future value of the project It is known as the present value of the project

Discounting factors are used in order to

ascertain discounting rates

Compounding interest rates are used

Table: Difference between discounting rate and compounding rate

(Source: Burns and Walker 2015).

From the above table, it can be inferred that discounting rates are more suitable for decision

making purpose. An investor will get to know what amount he should invest in order to meet his

future long-term goals, which cannot be done while using compounding rate of interest.

c. Discount rate and main components of the discount rate (why do we use different

discount rates for evaluating different decisions?).

The two basic components of discount rate is risk free rate and weighted average cost of capital.

Cost of capital is used in order to calculate different forms of capital budgeting techniques for

any particular project. There are different types of discounting rates use for different purpose. In

order to ascertain future value of an investment, different discounting rates are used (Brooks

BUSINESS FINANCE

Brooks (2015 opines that both discounting and compounding process is useful in their own ways.

The rational for using discounting rates rather than compounding process is as follows:-

Discounting rate Compounding rate

It helps to ascertain the percentage of amount

to be invested today to get a particular amount

in future.

It helps to ascertain the future value of a

particular amount invested today.

It is known as the future value of the project It is known as the present value of the project

Discounting factors are used in order to

ascertain discounting rates

Compounding interest rates are used

Table: Difference between discounting rate and compounding rate

(Source: Burns and Walker 2015).

From the above table, it can be inferred that discounting rates are more suitable for decision

making purpose. An investor will get to know what amount he should invest in order to meet his

future long-term goals, which cannot be done while using compounding rate of interest.

c. Discount rate and main components of the discount rate (why do we use different

discount rates for evaluating different decisions?).

The two basic components of discount rate is risk free rate and weighted average cost of capital.

Cost of capital is used in order to calculate different forms of capital budgeting techniques for

any particular project. There are different types of discounting rates use for different purpose. In

order to ascertain future value of an investment, different discounting rates are used (Brooks

6

BUSINESS FINANCE

2015).On the other hand, single discounting values are used to ascertain value of future cash

flows. On the other various discounting techniques, which are as follows:-

Discounted cash flows

Net Present Value

Internal rate of return

All the above types are suitable for different purposes. Net present value is used to ascertain

the excess of future inflows versus outflows. On the other hand, internal rate of return is used

to ascertain the rate of return from a particular project. In addition to this, payback period is

used to determine the time frame to get back the initial investment amount.

d. Use of time value in valuation of financial instruments such as bonds, equity and

preference shares.

There are various forms of financial instruments of time valuation. These can be in the

form of bonds, equity and preference shares. Bonds is generally consider as safe and fixed

money market instrument. Equity is considered as a capital market instrument and yields a high

rate of interest. On the other hand, preference shares also entitles a shareholder to get a fixed

percentage of dividend over a period of time (Faccio, Marchica and Mura 2016). There are

several advantages and disadvantages of these financial instruments which can further evaluated

with the help of the following table:-

Instruments Advantages Disadvantages

Equity 1. High rate of return

2. Limited liability

1. High risk

2. Depends on market

BUSINESS FINANCE

2015).On the other hand, single discounting values are used to ascertain value of future cash

flows. On the other various discounting techniques, which are as follows:-

Discounted cash flows

Net Present Value

Internal rate of return

All the above types are suitable for different purposes. Net present value is used to ascertain

the excess of future inflows versus outflows. On the other hand, internal rate of return is used

to ascertain the rate of return from a particular project. In addition to this, payback period is

used to determine the time frame to get back the initial investment amount.

d. Use of time value in valuation of financial instruments such as bonds, equity and

preference shares.

There are various forms of financial instruments of time valuation. These can be in the

form of bonds, equity and preference shares. Bonds is generally consider as safe and fixed

money market instrument. Equity is considered as a capital market instrument and yields a high

rate of interest. On the other hand, preference shares also entitles a shareholder to get a fixed

percentage of dividend over a period of time (Faccio, Marchica and Mura 2016). There are

several advantages and disadvantages of these financial instruments which can further evaluated

with the help of the following table:-

Instruments Advantages Disadvantages

Equity 1. High rate of return

2. Limited liability

1. High risk

2. Depends on market

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

BUSINESS FINANCE

fluctuation

3. High volatility

Bonds 1. Low volatility

2. Liquidity is high

3. Less risky investment

1. Reinvestment risk is

there

2. Fixed rate of interest

which can be lower

than market prices

3. The investors will lose

their money if the

company is declared

bankrupt

4. Exchange rate risk is

also there

Preference shares 1. Fixed rate of dividend

2. Less risky

1. No voting rights

2. Low rate of return

Table: Advantages and disadvantages of financial instruments

(Source: Delaney, Rich and Rose 2016)

From the above table, it can be inferred that all the given financial instruments have several

advantages and disadvantages. It will solely depend upon the investor in which financial

BUSINESS FINANCE

fluctuation

3. High volatility

Bonds 1. Low volatility

2. Liquidity is high

3. Less risky investment

1. Reinvestment risk is

there

2. Fixed rate of interest

which can be lower

than market prices

3. The investors will lose

their money if the

company is declared

bankrupt

4. Exchange rate risk is

also there

Preference shares 1. Fixed rate of dividend

2. Less risky

1. No voting rights

2. Low rate of return

Table: Advantages and disadvantages of financial instruments

(Source: Delaney, Rich and Rose 2016)

From the above table, it can be inferred that all the given financial instruments have several

advantages and disadvantages. It will solely depend upon the investor in which financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

BUSINESS FINANCE

instrument he/she will invest. Apart from this, it is choice of the investor whether he will choose

risk prone investments and risk free requirements according to the respective aims and objectives

(Finnerty 2013).

e. Capital budgeting and time value.

Delaney, Rich and Rose (2016) defined capital budgeting as the process in which

business organizations, especially large business organizations determine the potential

expenditure and return on investments which they can face in the future.

Time value of money is important for capital budgeting. There are various factors which affect

capital budgeting like time value, discount rates and converting values. Future value and present

value is critical in case of capital budgeting.

Using time value of money, an investor can understand the decision of investment in a project in

a better manner.

BUSINESS FINANCE

instrument he/she will invest. Apart from this, it is choice of the investor whether he will choose

risk prone investments and risk free requirements according to the respective aims and objectives

(Finnerty 2013).

e. Capital budgeting and time value.

Delaney, Rich and Rose (2016) defined capital budgeting as the process in which

business organizations, especially large business organizations determine the potential

expenditure and return on investments which they can face in the future.

Time value of money is important for capital budgeting. There are various factors which affect

capital budgeting like time value, discount rates and converting values. Future value and present

value is critical in case of capital budgeting.

Using time value of money, an investor can understand the decision of investment in a project in

a better manner.

9

BUSINESS FINANCE

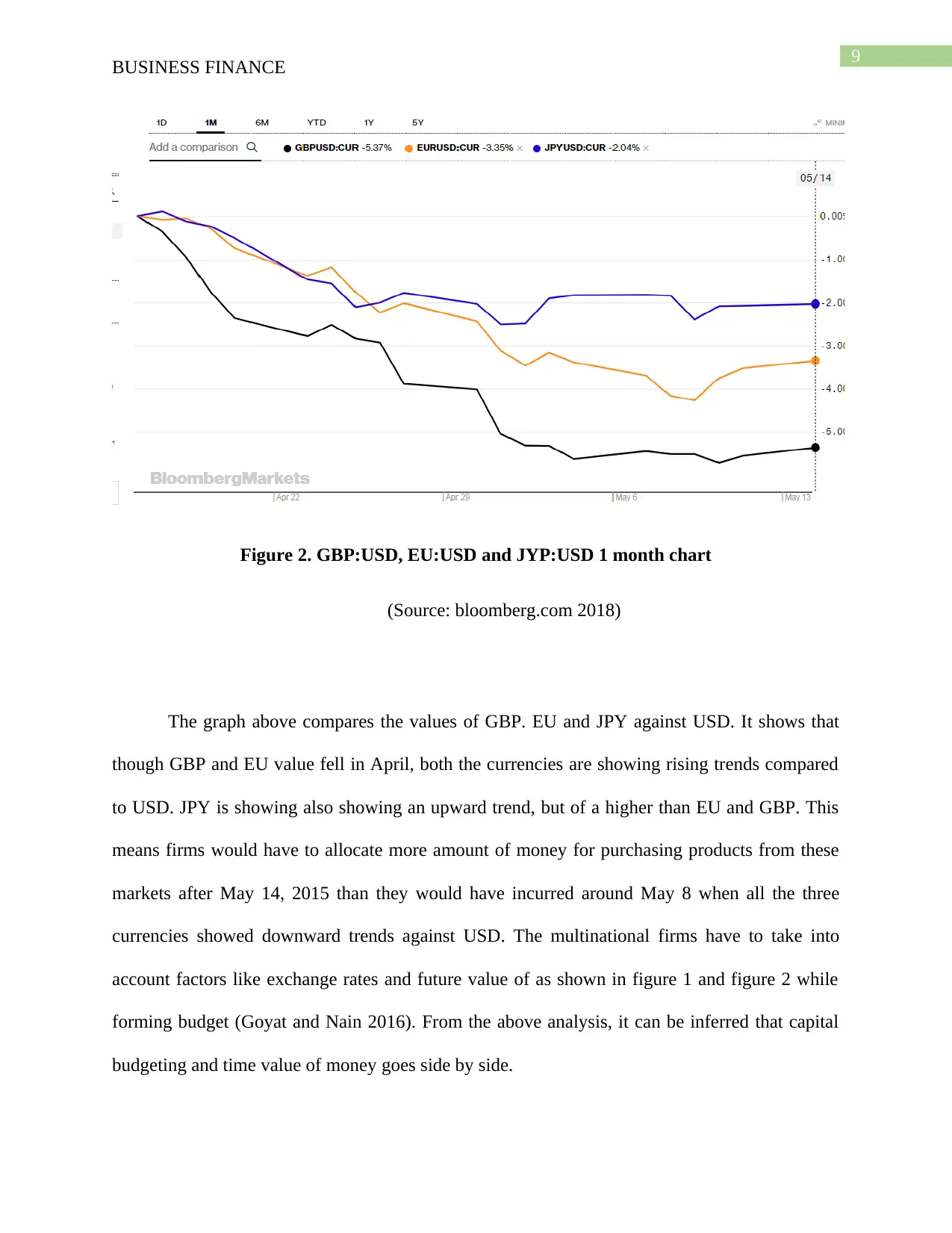

Figure 2. GBP:USD, EU:USD and JYP:USD 1 month chart

(Source: bloomberg.com 2018)

The graph above compares the values of GBP. EU and JPY against USD. It shows that

though GBP and EU value fell in April, both the currencies are showing rising trends compared

to USD. JPY is showing also showing an upward trend, but of a higher than EU and GBP. This

means firms would have to allocate more amount of money for purchasing products from these

markets after May 14, 2015 than they would have incurred around May 8 when all the three

currencies showed downward trends against USD. The multinational firms have to take into

account factors like exchange rates and future value of as shown in figure 1 and figure 2 while

forming budget (Goyat and Nain 2016). From the above analysis, it can be inferred that capital

budgeting and time value of money goes side by side.

BUSINESS FINANCE

Figure 2. GBP:USD, EU:USD and JYP:USD 1 month chart

(Source: bloomberg.com 2018)

The graph above compares the values of GBP. EU and JPY against USD. It shows that

though GBP and EU value fell in April, both the currencies are showing rising trends compared

to USD. JPY is showing also showing an upward trend, but of a higher than EU and GBP. This

means firms would have to allocate more amount of money for purchasing products from these

markets after May 14, 2015 than they would have incurred around May 8 when all the three

currencies showed downward trends against USD. The multinational firms have to take into

account factors like exchange rates and future value of as shown in figure 1 and figure 2 while

forming budget (Goyat and Nain 2016). From the above analysis, it can be inferred that capital

budgeting and time value of money goes side by side.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

BUSINESS FINANCE

f. The other issues

There are various issues or disadvantages associated with time value of money. These can be as

follows:-

Calculation of Net Present value is sensitive with discounting rates- Net present value

is based on summation of all the respective discounted cash flow of any particular given

project. Therefore, any considerable percentage of increase or decrease of discounted

cash flows can reflect a wrong value of Net present Value (Brooks 2015).

Cannot use different rates of discounted cash flows- It is true that market rates cannot

be same for entire time horizon. It may happen that the risk is more in first year in

comparison with the second year. However, capital budgeting techniques of NPV, IRR

keeps the discounting rate same for the entire time horizon. This can be considered as

another issue of these methods.

Real options are excluded- The calculations of NPV or any capital budgeting technique

do not include real options which are there in a respective project. This can be considered

as a disadvantage of capital budgeting methods.

These are the disadvantages which are associated with time value of money.

BUSINESS FINANCE

f. The other issues

There are various issues or disadvantages associated with time value of money. These can be as

follows:-

Calculation of Net Present value is sensitive with discounting rates- Net present value

is based on summation of all the respective discounted cash flow of any particular given

project. Therefore, any considerable percentage of increase or decrease of discounted

cash flows can reflect a wrong value of Net present Value (Brooks 2015).

Cannot use different rates of discounted cash flows- It is true that market rates cannot

be same for entire time horizon. It may happen that the risk is more in first year in

comparison with the second year. However, capital budgeting techniques of NPV, IRR

keeps the discounting rate same for the entire time horizon. This can be considered as

another issue of these methods.

Real options are excluded- The calculations of NPV or any capital budgeting technique

do not include real options which are there in a respective project. This can be considered

as a disadvantage of capital budgeting methods.

These are the disadvantages which are associated with time value of money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

BUSINESS FINANCE

Task 2:-

Question 1

Financial goals of Studebaker

There are several financial goals of Studebaker which are as follows:-

He wants to accumulate as much additional money as he could as he is planning an early

retirement in next 20 years or by 2038 at the age of 60.

He had a mortgage which he had to clear within next 20 years

He wanted to accumulate all the funds of the money market into one single life insurance

policy.

However, it is not a correct goal. There are few reasons behind it. These reasons are as follows:-

Opportunity costs are not taken into consideration

The annual costs will be 47,145.31 if the excess amount of money market is

introduced into one single life insurance policy.

Life insurance would give him only 6 percent interest, however, any long term

investment will give him around 7 percent rate of interest.

He should invest in safety funds and try to avoid market risks.

Therefore, the financial goals of Studebaker cannot be considered as effective.

Question 2

The given return has been calculated by assuming 6 percent return on the total amount invested

$550,000. This return is calculated on the basis of accumulation. With the help of this, total

accumulated value of the single insurance premium has been calculated.

BUSINESS FINANCE

Task 2:-

Question 1

Financial goals of Studebaker

There are several financial goals of Studebaker which are as follows:-

He wants to accumulate as much additional money as he could as he is planning an early

retirement in next 20 years or by 2038 at the age of 60.

He had a mortgage which he had to clear within next 20 years

He wanted to accumulate all the funds of the money market into one single life insurance

policy.

However, it is not a correct goal. There are few reasons behind it. These reasons are as follows:-

Opportunity costs are not taken into consideration

The annual costs will be 47,145.31 if the excess amount of money market is

introduced into one single life insurance policy.

Life insurance would give him only 6 percent interest, however, any long term

investment will give him around 7 percent rate of interest.

He should invest in safety funds and try to avoid market risks.

Therefore, the financial goals of Studebaker cannot be considered as effective.

Question 2

The given return has been calculated by assuming 6 percent return on the total amount invested

$550,000. This return is calculated on the basis of accumulation. With the help of this, total

accumulated value of the single insurance premium has been calculated.

12

BUSINESS FINANCE

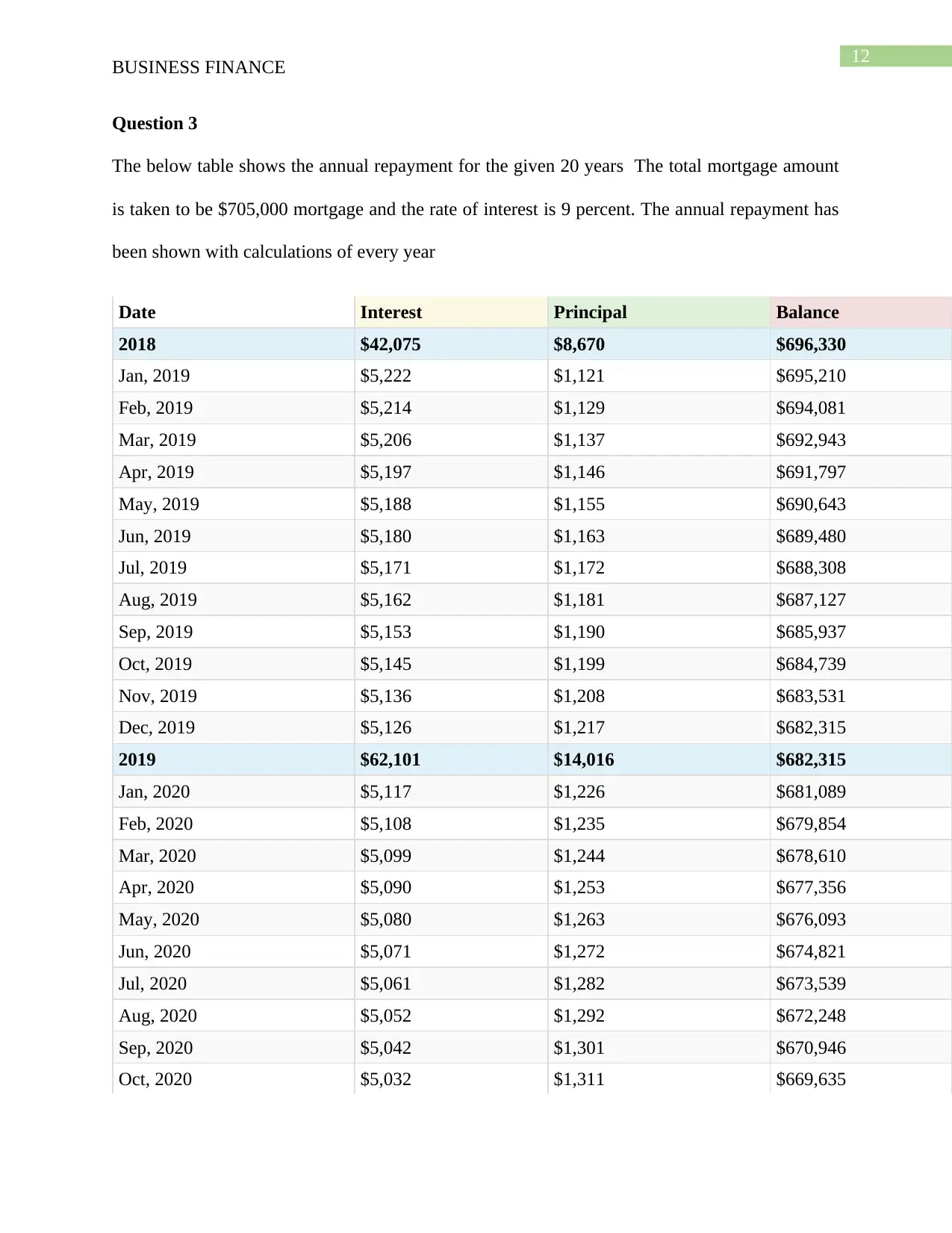

Question 3

The below table shows the annual repayment for the given 20 years The total mortgage amount

is taken to be $705,000 mortgage and the rate of interest is 9 percent. The annual repayment has

been shown with calculations of every year

Date Interest Principal Balance

2018 $42,075 $8,670 $696,330

Jan, 2019 $5,222 $1,121 $695,210

Feb, 2019 $5,214 $1,129 $694,081

Mar, 2019 $5,206 $1,137 $692,943

Apr, 2019 $5,197 $1,146 $691,797

May, 2019 $5,188 $1,155 $690,643

Jun, 2019 $5,180 $1,163 $689,480

Jul, 2019 $5,171 $1,172 $688,308

Aug, 2019 $5,162 $1,181 $687,127

Sep, 2019 $5,153 $1,190 $685,937

Oct, 2019 $5,145 $1,199 $684,739

Nov, 2019 $5,136 $1,208 $683,531

Dec, 2019 $5,126 $1,217 $682,315

2019 $62,101 $14,016 $682,315

Jan, 2020 $5,117 $1,226 $681,089

Feb, 2020 $5,108 $1,235 $679,854

Mar, 2020 $5,099 $1,244 $678,610

Apr, 2020 $5,090 $1,253 $677,356

May, 2020 $5,080 $1,263 $676,093

Jun, 2020 $5,071 $1,272 $674,821

Jul, 2020 $5,061 $1,282 $673,539

Aug, 2020 $5,052 $1,292 $672,248

Sep, 2020 $5,042 $1,301 $670,946

Oct, 2020 $5,032 $1,311 $669,635

BUSINESS FINANCE

Question 3

The below table shows the annual repayment for the given 20 years The total mortgage amount

is taken to be $705,000 mortgage and the rate of interest is 9 percent. The annual repayment has

been shown with calculations of every year

Date Interest Principal Balance

2018 $42,075 $8,670 $696,330

Jan, 2019 $5,222 $1,121 $695,210

Feb, 2019 $5,214 $1,129 $694,081

Mar, 2019 $5,206 $1,137 $692,943

Apr, 2019 $5,197 $1,146 $691,797

May, 2019 $5,188 $1,155 $690,643

Jun, 2019 $5,180 $1,163 $689,480

Jul, 2019 $5,171 $1,172 $688,308

Aug, 2019 $5,162 $1,181 $687,127

Sep, 2019 $5,153 $1,190 $685,937

Oct, 2019 $5,145 $1,199 $684,739

Nov, 2019 $5,136 $1,208 $683,531

Dec, 2019 $5,126 $1,217 $682,315

2019 $62,101 $14,016 $682,315

Jan, 2020 $5,117 $1,226 $681,089

Feb, 2020 $5,108 $1,235 $679,854

Mar, 2020 $5,099 $1,244 $678,610

Apr, 2020 $5,090 $1,253 $677,356

May, 2020 $5,080 $1,263 $676,093

Jun, 2020 $5,071 $1,272 $674,821

Jul, 2020 $5,061 $1,282 $673,539

Aug, 2020 $5,052 $1,292 $672,248

Sep, 2020 $5,042 $1,301 $670,946

Oct, 2020 $5,032 $1,311 $669,635

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.