Finance for Managers: Recording, Budgeting, and Appraisal

VerifiedAdded on 2020/01/21

|19

|5560

|89

Report

AI Summary

This report, created for a Finance for Managers course, delves into key aspects of financial management within a business context. It begins by exploring the importance of financial records, different methods for recording financial data (including income statements, balance sheets, and cash flow statements), and the legal and organizational needs for financial recording. The report then analyzes the use of financial statements by stakeholders and differentiates between financial and management accounting. A significant portion is dedicated to budgetary control, outlining the process and its various steps, including revenue and cost projections, profit margin analysis, board approval, and budget review. The report further examines variance calculation and interpretation, various project appraisal techniques, and methods for securing funds for business projects. It concludes by discussing the elements of working capital and effective management strategies. The report provides a comprehensive overview of financial principles and practices relevant to managerial decision-making.

FINANCE FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance for managers

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose and need of financial records..............................................................................1

1.2 Methods to record financial data and information...........................................................1

1.3 Analysing need of financial recording in terms of legal and organisation.......................2

1.4 Use of financial statements for stakeholders....................................................................3

1.5 Difference among financial and management accounting...............................................3

1.6 Explanation of process of budgetary control....................................................................4

1.7 Evaluating several kinds of costing techniques................................................................6

TASK 2............................................................................................................................................7

2.1 Calculation as well as interpretation of variances............................................................7

TASK 3............................................................................................................................................8

3.1 Key techniques of project appraisal.................................................................................8

3.2 Evaluation of project appraisal methods........................................................................11

3.3 Ways to obtain fund for business project.......................................................................12

3.4 Elements of working capital (WC).................................................................................13

3.5 Ways to manage working capital effectively.................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose and need of financial records..............................................................................1

1.2 Methods to record financial data and information...........................................................1

1.3 Analysing need of financial recording in terms of legal and organisation.......................2

1.4 Use of financial statements for stakeholders....................................................................3

1.5 Difference among financial and management accounting...............................................3

1.6 Explanation of process of budgetary control....................................................................4

1.7 Evaluating several kinds of costing techniques................................................................6

TASK 2............................................................................................................................................7

2.1 Calculation as well as interpretation of variances............................................................7

TASK 3............................................................................................................................................8

3.1 Key techniques of project appraisal.................................................................................8

3.2 Evaluation of project appraisal methods........................................................................11

3.3 Ways to obtain fund for business project.......................................................................12

3.4 Elements of working capital (WC).................................................................................13

3.5 Ways to manage working capital effectively.................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

Finance for managers

INTRODUCTION

Finance is very important concept of each and every business organisation in order to

exist, run and produce goods within market. Due to this, it is highly necessary for the managers

to have knowledge about basic financial aspect by which they able to manage financial resources

effectively. The present project divides into four parts where first part focuses on methods as

well as requirements in order to keep records of various financial transactions and reporting

them. In the second part, key elements of the working capital along with methods for managing

them effectually are explained. Third part of the report shows about different kinds of

management accounting tools and techniques along with making difference with the financial

accounting. At the end of project, explanation regarding to the appraisal methods and financing

sources is provided.

TASK 1

1.1 Purpose and need of financial records

Very basic need to record all the financial transactions is to determine about financial

health of the company and assess that whether it is profitable or not. The firm records the

financial data in order to know that total cost of production within small business of Malta is

whether enhancing or reducing and on the basis of that further decisions can be made properly.

Value of net profit is also derived through recording financial data which supports the small

business to take generally two financing decisions like dividend and investment. In case, firm

generates more profit, then it will take decision to invest money in several avenues and purchase

business equipments (Cotter, Tarca and Wee, 2012). Along with this, higher net profit leads to

provide more amount of dividend to existing and potential both shareholders. Another

requirement to make record of financial transactions is to compare financial performance of the

small business with previous years and rivals.

1.2 Methods to record financial data and information

When the management is going to record various financial data then different methods

are used which are such as follows: Income statement- In this method mainly three types of financial information are

recorded which are like revenue or net sales, incomes and expenses. It supports to the

Page 1

INTRODUCTION

Finance is very important concept of each and every business organisation in order to

exist, run and produce goods within market. Due to this, it is highly necessary for the managers

to have knowledge about basic financial aspect by which they able to manage financial resources

effectively. The present project divides into four parts where first part focuses on methods as

well as requirements in order to keep records of various financial transactions and reporting

them. In the second part, key elements of the working capital along with methods for managing

them effectually are explained. Third part of the report shows about different kinds of

management accounting tools and techniques along with making difference with the financial

accounting. At the end of project, explanation regarding to the appraisal methods and financing

sources is provided.

TASK 1

1.1 Purpose and need of financial records

Very basic need to record all the financial transactions is to determine about financial

health of the company and assess that whether it is profitable or not. The firm records the

financial data in order to know that total cost of production within small business of Malta is

whether enhancing or reducing and on the basis of that further decisions can be made properly.

Value of net profit is also derived through recording financial data which supports the small

business to take generally two financing decisions like dividend and investment. In case, firm

generates more profit, then it will take decision to invest money in several avenues and purchase

business equipments (Cotter, Tarca and Wee, 2012). Along with this, higher net profit leads to

provide more amount of dividend to existing and potential both shareholders. Another

requirement to make record of financial transactions is to compare financial performance of the

small business with previous years and rivals.

1.2 Methods to record financial data and information

When the management is going to record various financial data then different methods

are used which are such as follows: Income statement- In this method mainly three types of financial information are

recorded which are like revenue or net sales, incomes and expenses. It supports to the

Page 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance for managers

small business in order to assess three kinds of profit at the fiscal year ending which are

such as gross, operating and net income. Balance sheet- Another technique to record financial information is balance sheet under

which majorly two kinds of data involved which are like assets and liabilities. Under both

the sections current and non-current assets and liabilities included which provide liquidity

position to the small business at the end of year (Otley and Emmanuel, 2013).

Cash flow- The method under which cash receipts as well as outflows both are recorded

which depict framework of net cash position to the management. For assessing cash

balance of every month end such method is one of the best to recording financial data.

In order to record such all the financial transactions in above stated statements there are

some small reports are prepared. After completing the reporting system of accounting final

accounts of the firm are to be prepared. Moreover, the different reports include inventory,

payroll, receivables ageing, cost sheet, sales, production, expenses etc. In addition to this, for

making such all the treatments in books of account accounting standards, theories, principles etc.

used which come under IAS and IFRS.

1.3 Analysing need of financial recording in terms of legal and organisation

The small business organisation requires financial recording system to assess business

performance and take several financing decisions within workplace. At the time of framing profit

and loss account, it is mandatory to follow the tax rate which is charged by the government of

Malta. If taxation rules along with applicable rate are not used in the small business while

preparing income statement then not considered in the legal manner. Further, accounting

principles like prudence, consistency etc. and standards framed by International Financial

Reporting Standards (IFRS) are needs to use by small business. Apart from this, those principles,

accounting theories and standards considered while preparing financial accounts are mandatory

to show at the end of all the statements by following legal rules. When looking at the reporting

aspect then small business record all the financial transactions with the help of international

standards and theories. The reason for using international methods is that, across the world any

person or firm can analyse overall financials of the small entity. Use of IAS which known for

international accounting standards at the time of making accounting treatments is highly

Page 2

small business in order to assess three kinds of profit at the fiscal year ending which are

such as gross, operating and net income. Balance sheet- Another technique to record financial information is balance sheet under

which majorly two kinds of data involved which are like assets and liabilities. Under both

the sections current and non-current assets and liabilities included which provide liquidity

position to the small business at the end of year (Otley and Emmanuel, 2013).

Cash flow- The method under which cash receipts as well as outflows both are recorded

which depict framework of net cash position to the management. For assessing cash

balance of every month end such method is one of the best to recording financial data.

In order to record such all the financial transactions in above stated statements there are

some small reports are prepared. After completing the reporting system of accounting final

accounts of the firm are to be prepared. Moreover, the different reports include inventory,

payroll, receivables ageing, cost sheet, sales, production, expenses etc. In addition to this, for

making such all the treatments in books of account accounting standards, theories, principles etc.

used which come under IAS and IFRS.

1.3 Analysing need of financial recording in terms of legal and organisation

The small business organisation requires financial recording system to assess business

performance and take several financing decisions within workplace. At the time of framing profit

and loss account, it is mandatory to follow the tax rate which is charged by the government of

Malta. If taxation rules along with applicable rate are not used in the small business while

preparing income statement then not considered in the legal manner. Further, accounting

principles like prudence, consistency etc. and standards framed by International Financial

Reporting Standards (IFRS) are needs to use by small business. Apart from this, those principles,

accounting theories and standards considered while preparing financial accounts are mandatory

to show at the end of all the statements by following legal rules. When looking at the reporting

aspect then small business record all the financial transactions with the help of international

standards and theories. The reason for using international methods is that, across the world any

person or firm can analyse overall financials of the small entity. Use of IAS which known for

international accounting standards at the time of making accounting treatments is highly

Page 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance for managers

necessary in legal manner. The reason is that every company can assess business valuation and

financial performance at the end of an accounting period.

1.4 Use of financial statements for stakeholders

Stakeholders like employees, customers, suppliers, investors, government etc. use

financial statements of the firm while making decisions relating to it. Very basic requirement of

the financial accounts is to assess the profitable and liquid position of the company which

currently operates in Malta and on the basis of that different decisions are taken. When enterprise

generates more profit in the books of account then investors will put money into it and purchase

more shares (The purpose of financial statements, 2012). When talking about the suppliers then

they take decision to provide raw materials consistently by considering such position of it.

Moreover, as profitability and liquidity of the small business is higher, then employees will

attract towards it because it leads to provide more salary and other monetary benefits.

The banks also require statements related to financials of the company which are useful at

the time of providing loan or capital. When the small business goes to raise capital through

particular financing source i.e. bank loan then bank firstly determine business valuation. Along

with this, liquidity position, profitability etc. of the firm is mandatory consider while providing

the loan. Hence, it can be said that bank needs financial statements of the firm for various

purposes.

When talking about the public companies then they usually go for merger and acquisition

of those small firms which are generating higher revenue or profit. Such kinds of businesses

when going to acquire small firm then analyse profitability of past years along with the

appropriate value of overall business. In order to determine these all the values and terms of

financial they needed statements which are relied under the financials.

1.5 Difference among financial and management accounting

Financial Accounting Management Accounting

Financial accounting basically focuses on

financial statements that are allocated to

stakeholders, borrowers, financial analysts and

Management accounting basically focuses on

within the company operations, like providing

information and instructing internal stakeholders

Page 3

necessary in legal manner. The reason is that every company can assess business valuation and

financial performance at the end of an accounting period.

1.4 Use of financial statements for stakeholders

Stakeholders like employees, customers, suppliers, investors, government etc. use

financial statements of the firm while making decisions relating to it. Very basic requirement of

the financial accounts is to assess the profitable and liquid position of the company which

currently operates in Malta and on the basis of that different decisions are taken. When enterprise

generates more profit in the books of account then investors will put money into it and purchase

more shares (The purpose of financial statements, 2012). When talking about the suppliers then

they take decision to provide raw materials consistently by considering such position of it.

Moreover, as profitability and liquidity of the small business is higher, then employees will

attract towards it because it leads to provide more salary and other monetary benefits.

The banks also require statements related to financials of the company which are useful at

the time of providing loan or capital. When the small business goes to raise capital through

particular financing source i.e. bank loan then bank firstly determine business valuation. Along

with this, liquidity position, profitability etc. of the firm is mandatory consider while providing

the loan. Hence, it can be said that bank needs financial statements of the firm for various

purposes.

When talking about the public companies then they usually go for merger and acquisition

of those small firms which are generating higher revenue or profit. Such kinds of businesses

when going to acquire small firm then analyse profitability of past years along with the

appropriate value of overall business. In order to determine these all the values and terms of

financial they needed statements which are relied under the financials.

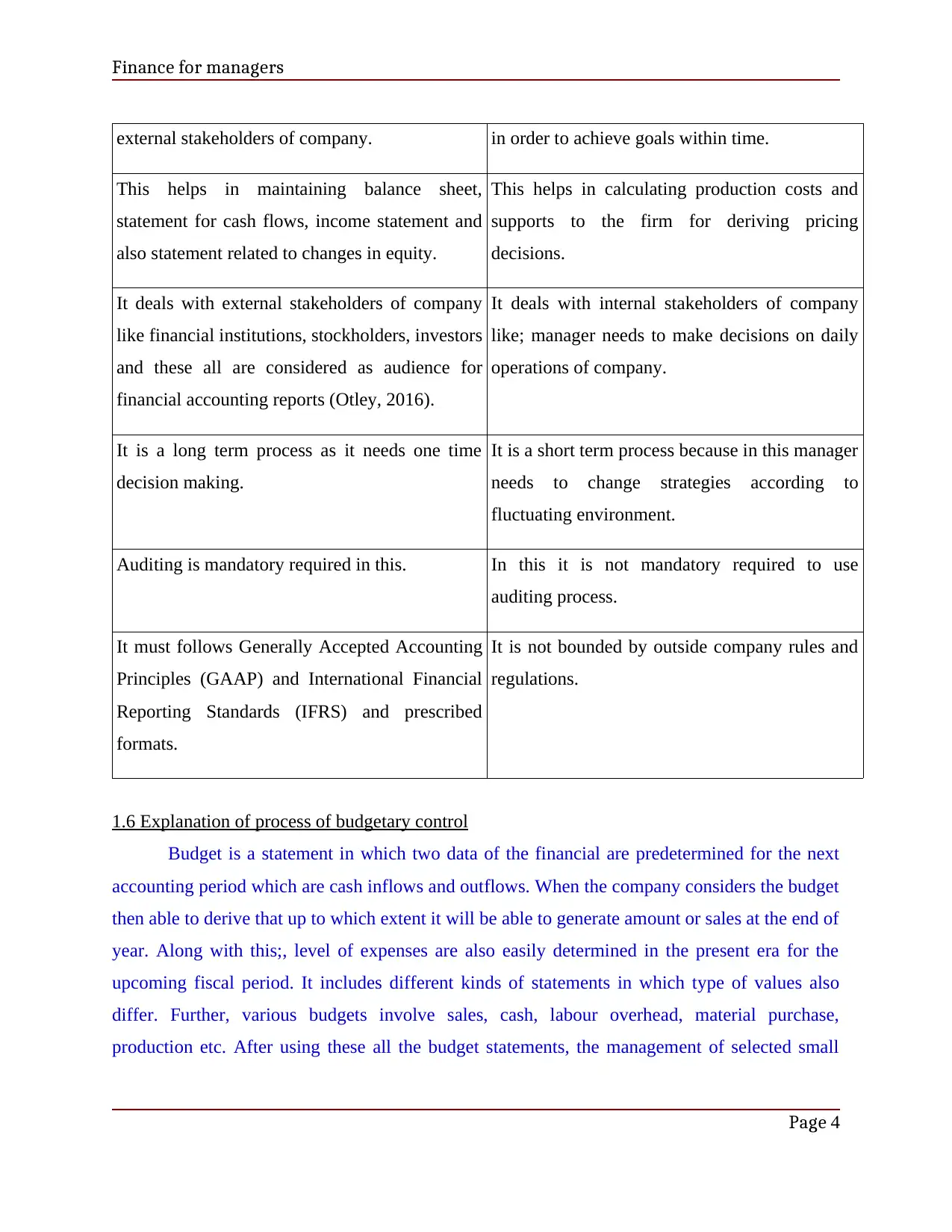

1.5 Difference among financial and management accounting

Financial Accounting Management Accounting

Financial accounting basically focuses on

financial statements that are allocated to

stakeholders, borrowers, financial analysts and

Management accounting basically focuses on

within the company operations, like providing

information and instructing internal stakeholders

Page 3

Finance for managers

external stakeholders of company. in order to achieve goals within time.

This helps in maintaining balance sheet,

statement for cash flows, income statement and

also statement related to changes in equity.

This helps in calculating production costs and

supports to the firm for deriving pricing

decisions.

It deals with external stakeholders of company

like financial institutions, stockholders, investors

and these all are considered as audience for

financial accounting reports (Otley, 2016).

It deals with internal stakeholders of company

like; manager needs to make decisions on daily

operations of company.

It is a long term process as it needs one time

decision making.

It is a short term process because in this manager

needs to change strategies according to

fluctuating environment.

Auditing is mandatory required in this. In this it is not mandatory required to use

auditing process.

It must follows Generally Accepted Accounting

Principles (GAAP) and International Financial

Reporting Standards (IFRS) and prescribed

formats.

It is not bounded by outside company rules and

regulations.

1.6 Explanation of process of budgetary control

Budget is a statement in which two data of the financial are predetermined for the next

accounting period which are cash inflows and outflows. When the company considers the budget

then able to derive that up to which extent it will be able to generate amount or sales at the end of

year. Along with this;, level of expenses are also easily determined in the present era for the

upcoming fiscal period. It includes different kinds of statements in which type of values also

differ. Further, various budgets involve sales, cash, labour overhead, material purchase,

production etc. After using these all the budget statements, the management of selected small

Page 4

external stakeholders of company. in order to achieve goals within time.

This helps in maintaining balance sheet,

statement for cash flows, income statement and

also statement related to changes in equity.

This helps in calculating production costs and

supports to the firm for deriving pricing

decisions.

It deals with external stakeholders of company

like financial institutions, stockholders, investors

and these all are considered as audience for

financial accounting reports (Otley, 2016).

It deals with internal stakeholders of company

like; manager needs to make decisions on daily

operations of company.

It is a long term process as it needs one time

decision making.

It is a short term process because in this manager

needs to change strategies according to

fluctuating environment.

Auditing is mandatory required in this. In this it is not mandatory required to use

auditing process.

It must follows Generally Accepted Accounting

Principles (GAAP) and International Financial

Reporting Standards (IFRS) and prescribed

formats.

It is not bounded by outside company rules and

regulations.

1.6 Explanation of process of budgetary control

Budget is a statement in which two data of the financial are predetermined for the next

accounting period which are cash inflows and outflows. When the company considers the budget

then able to derive that up to which extent it will be able to generate amount or sales at the end of

year. Along with this;, level of expenses are also easily determined in the present era for the

upcoming fiscal period. It includes different kinds of statements in which type of values also

differ. Further, various budgets involve sales, cash, labour overhead, material purchase,

production etc. After using these all the budget statements, the management of selected small

Page 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance for managers

business capable to boost up business performance in the future accounting periods. Process of

Budgetary Control Involves various steps which are described as below:

Revenue Projections: This is based on past projected growth income and financial

performance of the small business which operates in Malta. The projected growth is

connected with planned initiatives which will help business in growing. Further, at the

time of preparing budget of small business, it is identified initially that, revenue will be

up to which level generated. With the help of projecting or predetermining sales for the

next year, management go for further stages.

Cost Projections: This involves both the cost that is fixed and variable cost. Fixed cost

doest not change and should be involved in budget like utility costs, facility expenses,

mortgage or rent payments, insurance etc. While variable cost keeps on fluctuating and

should be controlled in budget like supply costs, overtime cost etc. Moreover, in the

second step, such both kinds of the expenses estimated for the small business for

upcoming year. After projections of the sales and revenue, cost as well as total expenses

which will be incurred are estimated by the managers of small business.

Profit Margin: Every company should have profit margins because it will help

management in making further investments, improving facilities and also it shows

strength of organisation (Elhamma and Taouab, 2015). In the cited small business firm, if

margin of the income generated is in the positive or favourable condition then helps to

control on the budgets. Due to this, the small entity will able to meet with the budgeted

values. By considering above projections of both the values like cost and revenue, level

of profit is to be predetermined at this current stage.

Board Approval: The president or head of the organisation provides approval of budget

who will also keep report of budget performance, will be familiar with expenses. Once

above stated all the steps completed in the small business then presented to the authorised

managers. The reason for present in front of them is to take approval for further process.

The estimated values and profit is known as raw budget which is presented in front of

authorised manager for taking approval.

Budget Review: Committee sets for keeping a check over budget, review budget

performance against goals & will also make changes if needed in any case of

Page 5

business capable to boost up business performance in the future accounting periods. Process of

Budgetary Control Involves various steps which are described as below:

Revenue Projections: This is based on past projected growth income and financial

performance of the small business which operates in Malta. The projected growth is

connected with planned initiatives which will help business in growing. Further, at the

time of preparing budget of small business, it is identified initially that, revenue will be

up to which level generated. With the help of projecting or predetermining sales for the

next year, management go for further stages.

Cost Projections: This involves both the cost that is fixed and variable cost. Fixed cost

doest not change and should be involved in budget like utility costs, facility expenses,

mortgage or rent payments, insurance etc. While variable cost keeps on fluctuating and

should be controlled in budget like supply costs, overtime cost etc. Moreover, in the

second step, such both kinds of the expenses estimated for the small business for

upcoming year. After projections of the sales and revenue, cost as well as total expenses

which will be incurred are estimated by the managers of small business.

Profit Margin: Every company should have profit margins because it will help

management in making further investments, improving facilities and also it shows

strength of organisation (Elhamma and Taouab, 2015). In the cited small business firm, if

margin of the income generated is in the positive or favourable condition then helps to

control on the budgets. Due to this, the small entity will able to meet with the budgeted

values. By considering above projections of both the values like cost and revenue, level

of profit is to be predetermined at this current stage.

Board Approval: The president or head of the organisation provides approval of budget

who will also keep report of budget performance, will be familiar with expenses. Once

above stated all the steps completed in the small business then presented to the authorised

managers. The reason for present in front of them is to take approval for further process.

The estimated values and profit is known as raw budget which is presented in front of

authorised manager for taking approval.

Budget Review: Committee sets for keeping a check over budget, review budget

performance against goals & will also make changes if needed in any case of

Page 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance for managers

overspending or wastage. In this last stage of budgetary control, reviews are taken that

whether it is going on track and as per the estimated. It is the position, where small

business able to make changes in budget after considering the evaluation. At this specific

step, budget is evaluated that whether any problem or issue is remained or not. After

completion of reviewing procedure it is implemented within workplace of small business.

Dealing with Budget Variances: In case of variance in actual budget and planned

budget, responsible department manager is answerable for changes. At the end, both

actual data generated and estimated data of the budget are compared. Further, outcome of

both the values is considered as the budget variance. At the last and after completion of

next year, estimated data are compared with the actual generated facts and figures.

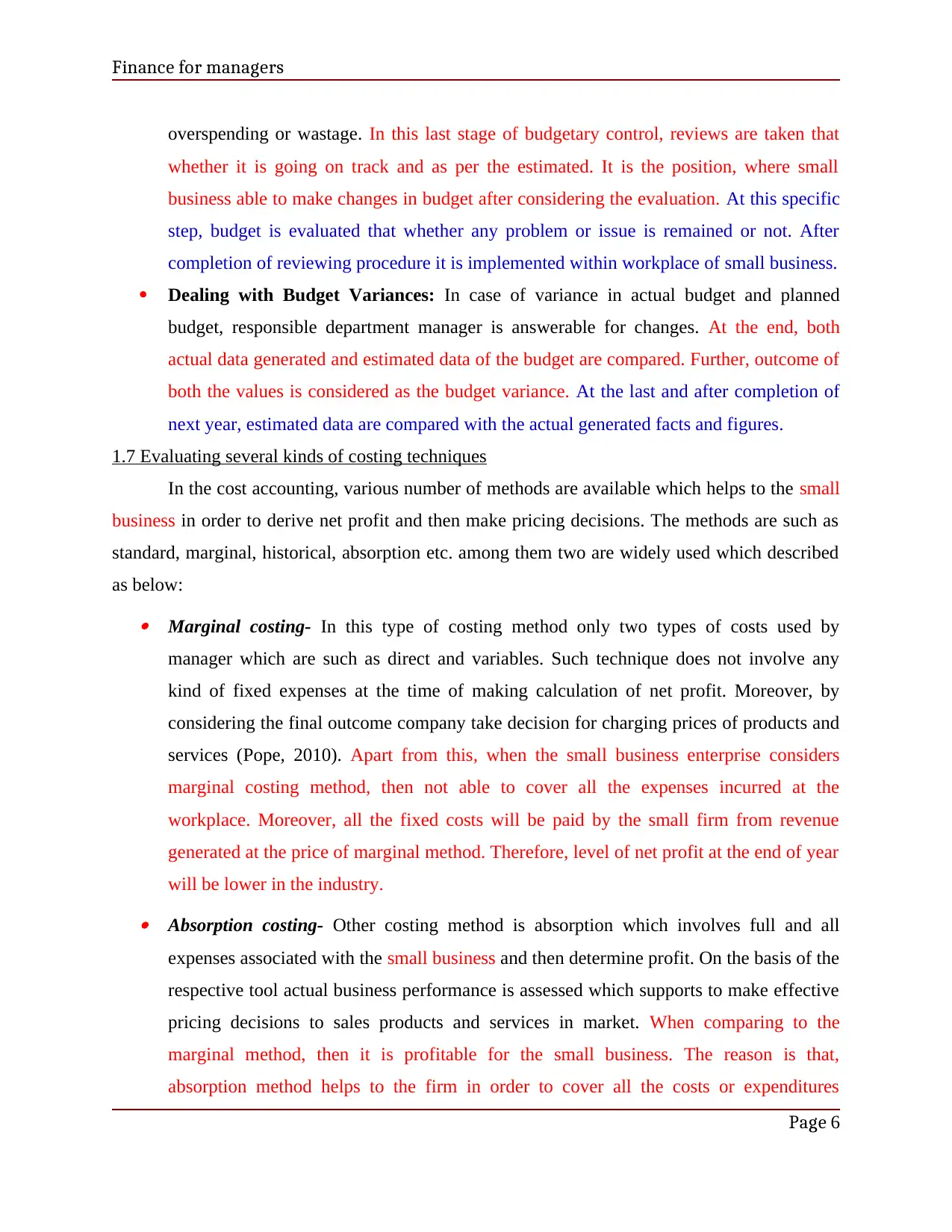

1.7 Evaluating several kinds of costing techniques

In the cost accounting, various number of methods are available which helps to the small

business in order to derive net profit and then make pricing decisions. The methods are such as

standard, marginal, historical, absorption etc. among them two are widely used which described

as below: Marginal costing- In this type of costing method only two types of costs used by

manager which are such as direct and variables. Such technique does not involve any

kind of fixed expenses at the time of making calculation of net profit. Moreover, by

considering the final outcome company take decision for charging prices of products and

services (Pope, 2010). Apart from this, when the small business enterprise considers

marginal costing method, then not able to cover all the expenses incurred at the

workplace. Moreover, all the fixed costs will be paid by the small firm from revenue

generated at the price of marginal method. Therefore, level of net profit at the end of year

will be lower in the industry. Absorption costing- Other costing method is absorption which involves full and all

expenses associated with the small business and then determine profit. On the basis of the

respective tool actual business performance is assessed which supports to make effective

pricing decisions to sales products and services in market. When comparing to the

marginal method, then it is profitable for the small business. The reason is that,

absorption method helps to the firm in order to cover all the costs or expenditures

Page 6

overspending or wastage. In this last stage of budgetary control, reviews are taken that

whether it is going on track and as per the estimated. It is the position, where small

business able to make changes in budget after considering the evaluation. At this specific

step, budget is evaluated that whether any problem or issue is remained or not. After

completion of reviewing procedure it is implemented within workplace of small business.

Dealing with Budget Variances: In case of variance in actual budget and planned

budget, responsible department manager is answerable for changes. At the end, both

actual data generated and estimated data of the budget are compared. Further, outcome of

both the values is considered as the budget variance. At the last and after completion of

next year, estimated data are compared with the actual generated facts and figures.

1.7 Evaluating several kinds of costing techniques

In the cost accounting, various number of methods are available which helps to the small

business in order to derive net profit and then make pricing decisions. The methods are such as

standard, marginal, historical, absorption etc. among them two are widely used which described

as below: Marginal costing- In this type of costing method only two types of costs used by

manager which are such as direct and variables. Such technique does not involve any

kind of fixed expenses at the time of making calculation of net profit. Moreover, by

considering the final outcome company take decision for charging prices of products and

services (Pope, 2010). Apart from this, when the small business enterprise considers

marginal costing method, then not able to cover all the expenses incurred at the

workplace. Moreover, all the fixed costs will be paid by the small firm from revenue

generated at the price of marginal method. Therefore, level of net profit at the end of year

will be lower in the industry. Absorption costing- Other costing method is absorption which involves full and all

expenses associated with the small business and then determine profit. On the basis of the

respective tool actual business performance is assessed which supports to make effective

pricing decisions to sales products and services in market. When comparing to the

marginal method, then it is profitable for the small business. The reason is that,

absorption method helps to the firm in order to cover all the costs or expenditures

Page 6

Finance for managers

incurred at the workplace. Henceforth, net profit and business performance will be higher

in this situation as compare to marginal costing. Standard costing: Method of costing in which expense level is estimated before

completion of the production process is known as standard costing. Base of

predetermining expenditures is standards which are mentioned in the situations of

operation department. In this costing is considered as outdated in which chances of

incurring losses are there. Further, in order to avoid the loss standard expenses are to be

compared with the actual data within specific period.

Historical costing: This technique of costing is totally opposite from the above explained

standard costing, under this, once total expenses incurred within workplace then used for

determining pricing level. Moreover, chances of incurring profit are high in the historical

method of costing.

TASK 2

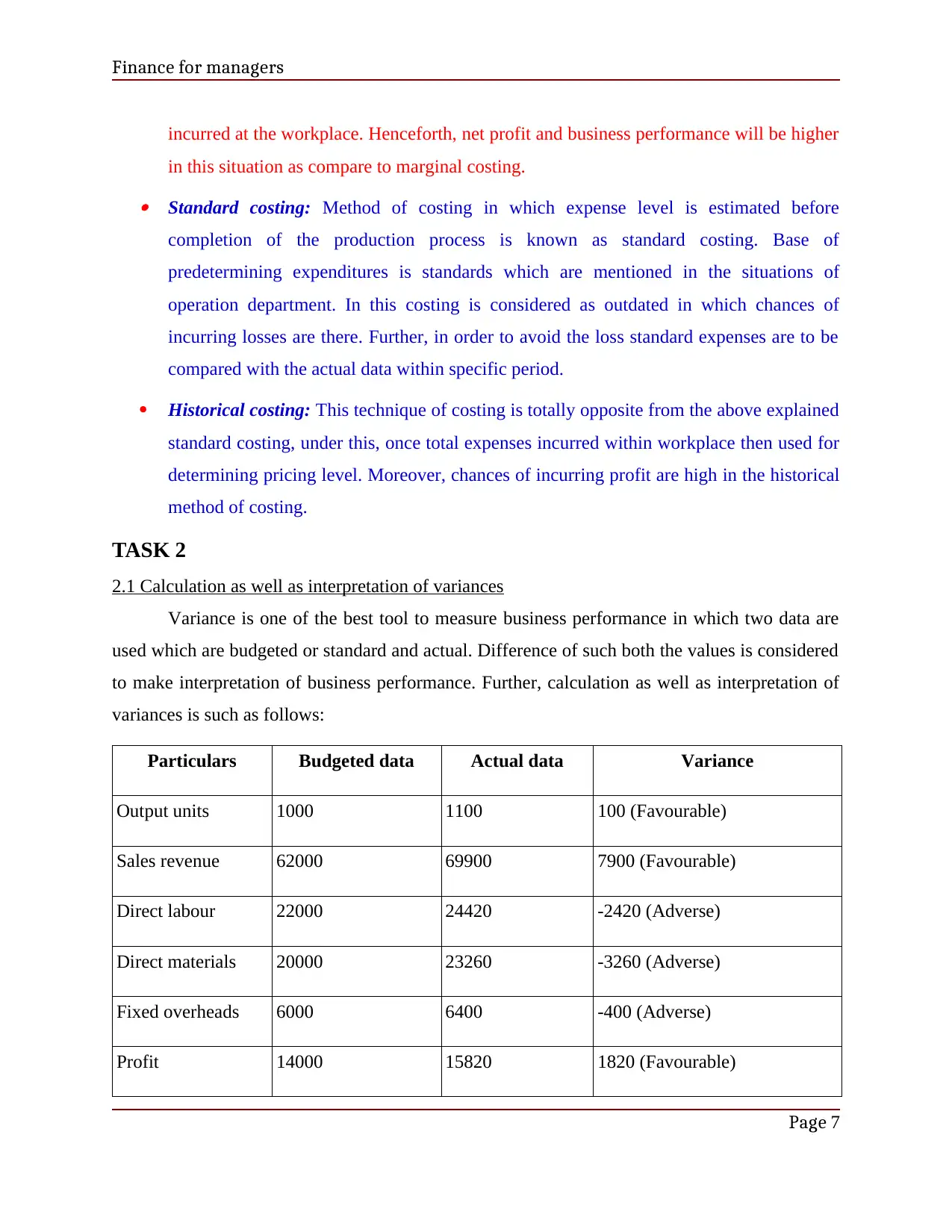

2.1 Calculation as well as interpretation of variances

Variance is one of the best tool to measure business performance in which two data are

used which are budgeted or standard and actual. Difference of such both the values is considered

to make interpretation of business performance. Further, calculation as well as interpretation of

variances is such as follows:

Particulars Budgeted data Actual data Variance

Output units 1000 1100 100 (Favourable)

Sales revenue 62000 69900 7900 (Favourable)

Direct labour 22000 24420 -2420 (Adverse)

Direct materials 20000 23260 -3260 (Adverse)

Fixed overheads 6000 6400 -400 (Adverse)

Profit 14000 15820 1820 (Favourable)

Page 7

incurred at the workplace. Henceforth, net profit and business performance will be higher

in this situation as compare to marginal costing. Standard costing: Method of costing in which expense level is estimated before

completion of the production process is known as standard costing. Base of

predetermining expenditures is standards which are mentioned in the situations of

operation department. In this costing is considered as outdated in which chances of

incurring losses are there. Further, in order to avoid the loss standard expenses are to be

compared with the actual data within specific period.

Historical costing: This technique of costing is totally opposite from the above explained

standard costing, under this, once total expenses incurred within workplace then used for

determining pricing level. Moreover, chances of incurring profit are high in the historical

method of costing.

TASK 2

2.1 Calculation as well as interpretation of variances

Variance is one of the best tool to measure business performance in which two data are

used which are budgeted or standard and actual. Difference of such both the values is considered

to make interpretation of business performance. Further, calculation as well as interpretation of

variances is such as follows:

Particulars Budgeted data Actual data Variance

Output units 1000 1100 100 (Favourable)

Sales revenue 62000 69900 7900 (Favourable)

Direct labour 22000 24420 -2420 (Adverse)

Direct materials 20000 23260 -3260 (Adverse)

Fixed overheads 6000 6400 -400 (Adverse)

Profit 14000 15820 1820 (Favourable)

Page 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance for managers

Interpretation

It can be interpreted from above mentioned variance analysis is that; output units are in

the favourable condition with the 100 units. The firm predetermined that at the end of year 1000

units must be produce but instead of that it manufactures 1100 units with same raw materials

which are profitable for it. When looking at the sales and revenue digits then it can be found that

it generates 7900 GBP more amounts compare to budget. Because of this it can be said that

management utilise resources in optimum ways and reduce total costs (Elhamma, 2015). Along

with this, profit variance is also favourable for the entity in which it generates 1820 GBP more.

In the budget it determined that 14000 GBP profit required to generate where actual value comes

at 15820 GBP which is highly beneficial for it.

Apart from this, all the expense variances are in the adverse situation which shows that

management not able to control on costing aspect. Direct labour and materials variance in the

current case are -2420 GBP and -3260 GBP respectively which both are at the adverse condition.

When talking about the fixed overhead expenses variance then also it is in unfavourable situation

where value of variance is worth of -400 GBP.

TASK 3

3.1 Key techniques of project appraisal

Accounting rate of return (ARR)-

Formula of ARR = Total profit / Average investment * 100

Years Profit of project 1 (in €) Profit of project 2 (in €)

Cost or initial investment -200000 -120000

Year 1 58000 36000

Year 2 2000 4000

Year 3 4000 8000

Page 8

Interpretation

It can be interpreted from above mentioned variance analysis is that; output units are in

the favourable condition with the 100 units. The firm predetermined that at the end of year 1000

units must be produce but instead of that it manufactures 1100 units with same raw materials

which are profitable for it. When looking at the sales and revenue digits then it can be found that

it generates 7900 GBP more amounts compare to budget. Because of this it can be said that

management utilise resources in optimum ways and reduce total costs (Elhamma, 2015). Along

with this, profit variance is also favourable for the entity in which it generates 1820 GBP more.

In the budget it determined that 14000 GBP profit required to generate where actual value comes

at 15820 GBP which is highly beneficial for it.

Apart from this, all the expense variances are in the adverse situation which shows that

management not able to control on costing aspect. Direct labour and materials variance in the

current case are -2420 GBP and -3260 GBP respectively which both are at the adverse condition.

When talking about the fixed overhead expenses variance then also it is in unfavourable situation

where value of variance is worth of -400 GBP.

TASK 3

3.1 Key techniques of project appraisal

Accounting rate of return (ARR)-

Formula of ARR = Total profit / Average investment * 100

Years Profit of project 1 (in €) Profit of project 2 (in €)

Cost or initial investment -200000 -120000

Year 1 58000 36000

Year 2 2000 4000

Year 3 4000 8000

Page 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance for managers

Scrape value 14000 12000

Total profit 64000 48000

Average investment 107000 66000

ARR

= 64000 / 107000 * 100

59.81%

= 48000 / 66000 * 100

72.73%

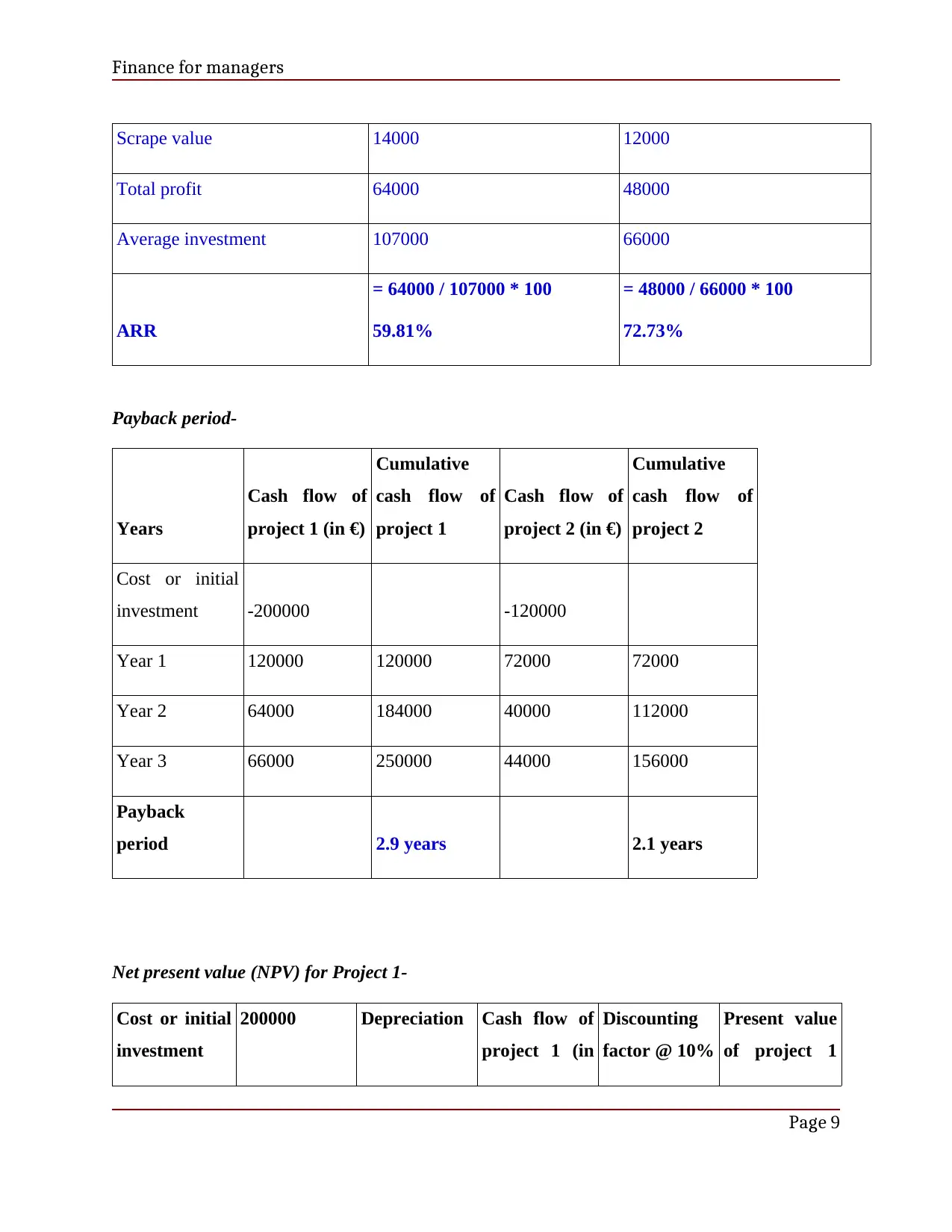

Payback period-

Years

Cash flow of

project 1 (in €)

Cumulative

cash flow of

project 1

Cash flow of

project 2 (in €)

Cumulative

cash flow of

project 2

Cost or initial

investment -200000 -120000

Year 1 120000 120000 72000 72000

Year 2 64000 184000 40000 112000

Year 3 66000 250000 44000 156000

Payback

period 2.9 years 2.1 years

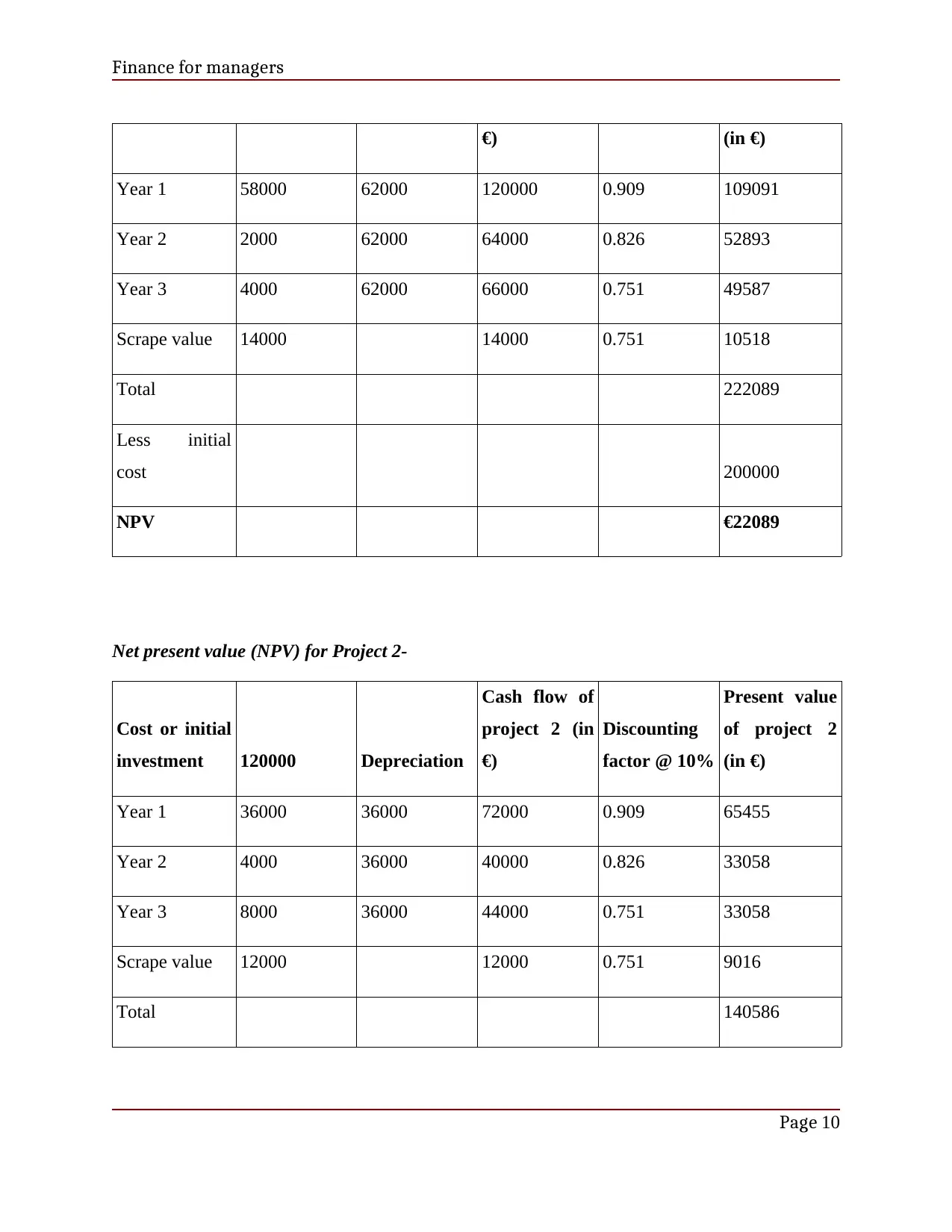

Net present value (NPV) for Project 1-

Cost or initial

investment

200000 Depreciation Cash flow of

project 1 (in

Discounting

factor @ 10%

Present value

of project 1

Page 9

Scrape value 14000 12000

Total profit 64000 48000

Average investment 107000 66000

ARR

= 64000 / 107000 * 100

59.81%

= 48000 / 66000 * 100

72.73%

Payback period-

Years

Cash flow of

project 1 (in €)

Cumulative

cash flow of

project 1

Cash flow of

project 2 (in €)

Cumulative

cash flow of

project 2

Cost or initial

investment -200000 -120000

Year 1 120000 120000 72000 72000

Year 2 64000 184000 40000 112000

Year 3 66000 250000 44000 156000

Payback

period 2.9 years 2.1 years

Net present value (NPV) for Project 1-

Cost or initial

investment

200000 Depreciation Cash flow of

project 1 (in

Discounting

factor @ 10%

Present value

of project 1

Page 9

Finance for managers

€) (in €)

Year 1 58000 62000 120000 0.909 109091

Year 2 2000 62000 64000 0.826 52893

Year 3 4000 62000 66000 0.751 49587

Scrape value 14000 14000 0.751 10518

Total 222089

Less initial

cost 200000

NPV €22089

Net present value (NPV) for Project 2-

Cost or initial

investment 120000 Depreciation

Cash flow of

project 2 (in

€)

Discounting

factor @ 10%

Present value

of project 2

(in €)

Year 1 36000 36000 72000 0.909 65455

Year 2 4000 36000 40000 0.826 33058

Year 3 8000 36000 44000 0.751 33058

Scrape value 12000 12000 0.751 9016

Total 140586

Page 10

€) (in €)

Year 1 58000 62000 120000 0.909 109091

Year 2 2000 62000 64000 0.826 52893

Year 3 4000 62000 66000 0.751 49587

Scrape value 14000 14000 0.751 10518

Total 222089

Less initial

cost 200000

NPV €22089

Net present value (NPV) for Project 2-

Cost or initial

investment 120000 Depreciation

Cash flow of

project 2 (in

€)

Discounting

factor @ 10%

Present value

of project 2

(in €)

Year 1 36000 36000 72000 0.909 65455

Year 2 4000 36000 40000 0.826 33058

Year 3 8000 36000 44000 0.751 33058

Scrape value 12000 12000 0.751 9016

Total 140586

Page 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.